Australian Income Tax Project: Assessing Income and Deductions

VerifiedAdded on 2020/12/29

|7

|1736

|410

Project

AI Summary

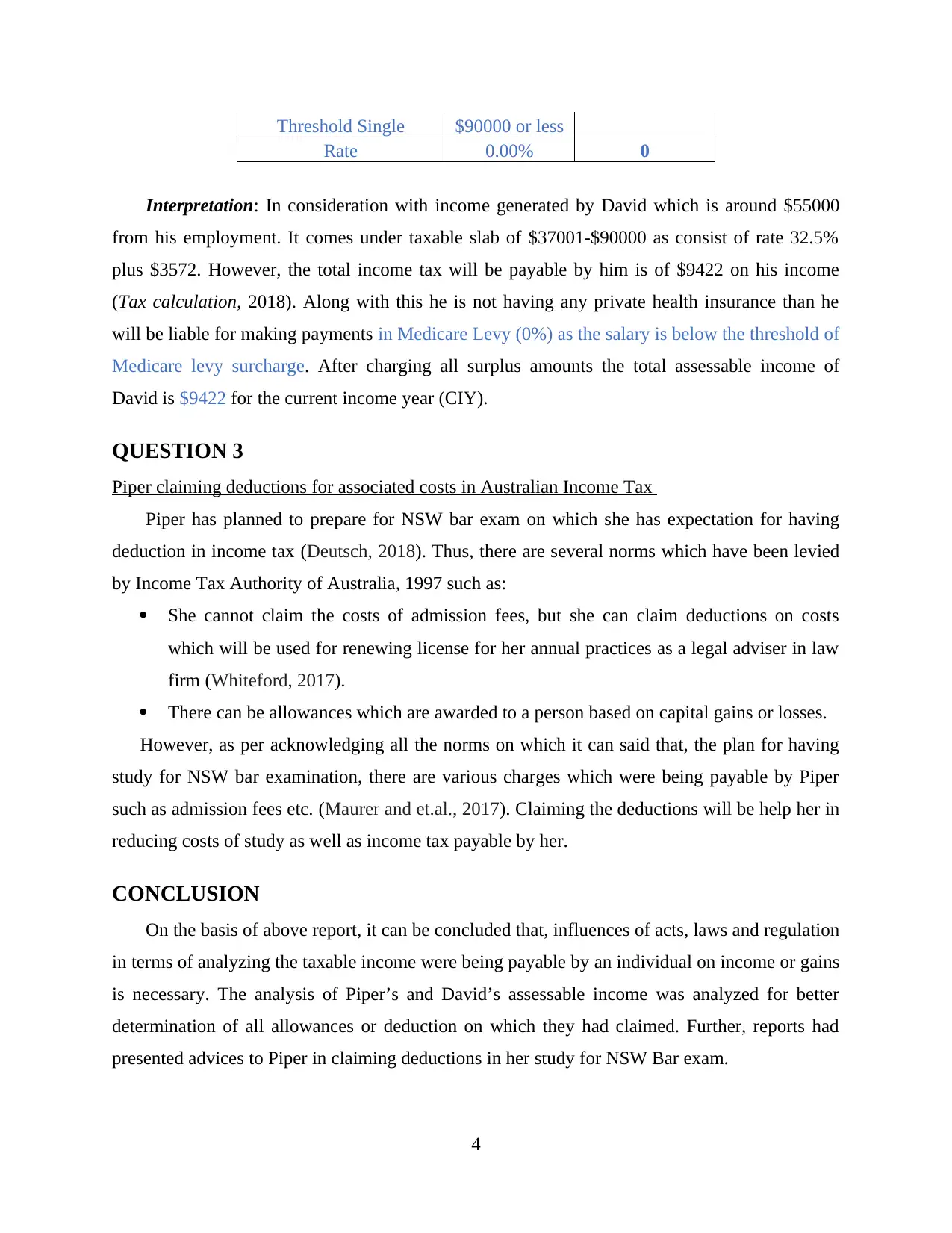

This project analyzes the income tax liabilities of two individuals, Piper and David, in the context of Australian taxation laws. The project begins with an introduction to income tax and its implications, followed by a detailed assessment of Piper's assessable income, considering income from multiple sources (guest lecturer and volunteer work) and allowable deductions, including depreciation on a printer and tickets. The analysis calculates her total income tax payable, including Medicare levy surcharge. The project then assesses David's income tax liability, based on his salary as a full-time lecturer. The project also addresses Piper's plan to prepare for the NSW bar exam and the potential for claiming deductions related to associated costs. The project concludes with a summary of the findings and relevant references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.