Comprehensive Analysis of Australian Macroeconomic Performance Report

VerifiedAdded on 2023/01/03

|25

|5048

|20

Report

AI Summary

This report provides a comprehensive analysis of the Australian macroeconomic performance from 1995 to 2015. It examines various key macroeconomic indicators, including real gross domestic product (GDP) growth rates, inflation rates, unemployment rates, exchange rates, net exports, and cash rates. The report presents data from the International Monetary Fund and the World Bank, offering a detailed overview of economic trends. It explores the relationships between real GDP growth and inflation, real GDP growth and unemployment, and net exports and exchange rates. Additionally, it investigates the correlation between Australian cash rates and the Federal Reserve Fund’s rates. The report concludes with an Australian macroeconomic outlook prediction, providing valuable insights into the country's economic landscape and assisting businesses, governments, and investors in making informed decisions. The analysis highlights the factors contributing to Australia's strong economic performance and its position in the Asia-Pacific region.

AUSTRALIAN MACROECONOMIC PERFORMANCE i

AN ANALYSIS OF THE AUSTRALIAN MACROECONOMIC PERFORMANCE

Student Name

Institution Affiliation

Facilitator

Course

Date

AN ANALYSIS OF THE AUSTRALIAN MACROECONOMIC PERFORMANCE

Student Name

Institution Affiliation

Facilitator

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUSTRALIAN MACROECONOMIC PERFORMANCE ii

Executive Summary

The Australian economy is among the largest and richest economies in the world. Australian is

situated in the Asia-Pacific which has 43 nations. Australia highly embraces business, trade,

monetary, labor, investment and financial freedom which reflect the level of trade freedom in the

nation (Uy, Yi and Zhang 2013, p.667). Australia occupies position 5 according to the 2019

Index in terms of economic freedom having a score of 80.9. Trade and labor freedom, as well as

government integrity and fiscal health, have highly improved hence maintaining the nation’s

score of economic freedom while its efficiency of the judiciary slightly deteriorated. Australia

has been experiencing economic growth almost for the last decade and also the nation was lucky

enough to record a positive economic growth though at a reduced rate during the 2008 to 2009

global financial crisis (Kenc and Dibooglu 2010, p.3). The nation has a current economic growth

of 2.3 percent which is relatively a good economic growth as compared to many nations. In

terms of economic performance, Australia occupies position 4 out of the 43 nations in the region

of Asia-Pacific. Australian sound macroeconomic goals and policies, as well as highly skilled

labor force, have highly contributed towards the nation’s better economic performance and hence

the nation remains a center of attraction for many investors both domestically and internationally

(McDonald and Morling 2011, p.1). The Australian economic performance is well above that

anticipated both at the regional and world levels. In this report, an analysis of the Australian

macroeconomic performance has been done based on various macroeconomic indicators which

include unemployment, inflation and exchange rates as well as the real gross domestic product

growth rate has been done. The overall macroeconomic performance assists existing businesses,

the government and also the prospective investors to make their goals with great certainty.

Executive Summary

The Australian economy is among the largest and richest economies in the world. Australian is

situated in the Asia-Pacific which has 43 nations. Australia highly embraces business, trade,

monetary, labor, investment and financial freedom which reflect the level of trade freedom in the

nation (Uy, Yi and Zhang 2013, p.667). Australia occupies position 5 according to the 2019

Index in terms of economic freedom having a score of 80.9. Trade and labor freedom, as well as

government integrity and fiscal health, have highly improved hence maintaining the nation’s

score of economic freedom while its efficiency of the judiciary slightly deteriorated. Australia

has been experiencing economic growth almost for the last decade and also the nation was lucky

enough to record a positive economic growth though at a reduced rate during the 2008 to 2009

global financial crisis (Kenc and Dibooglu 2010, p.3). The nation has a current economic growth

of 2.3 percent which is relatively a good economic growth as compared to many nations. In

terms of economic performance, Australia occupies position 4 out of the 43 nations in the region

of Asia-Pacific. Australian sound macroeconomic goals and policies, as well as highly skilled

labor force, have highly contributed towards the nation’s better economic performance and hence

the nation remains a center of attraction for many investors both domestically and internationally

(McDonald and Morling 2011, p.1). The Australian economic performance is well above that

anticipated both at the regional and world levels. In this report, an analysis of the Australian

macroeconomic performance has been done based on various macroeconomic indicators which

include unemployment, inflation and exchange rates as well as the real gross domestic product

growth rate has been done. The overall macroeconomic performance assists existing businesses,

the government and also the prospective investors to make their goals with great certainty.

AUSTRALIAN MACROECONOMIC PERFORMANCE iii

Table of Contents

Executive Summary....................................................................................................................................ii

Australian macroeconomic data from the year 1995 to 2015.......................................................................1

Australian Real Gross Domestic Product Growth Rates from 1995 to 2015............................................1

Australian Inflation Rates for the period 1995 to 2015............................................................................1

Australian Unemployment Rates for the period 1995 to 2015.................................................................2

Australian Exchange Rates for the period 1995 to 2015..........................................................................3

Australian Net Exports for the period 1995 to 2015................................................................................3

Australian Cash Rates and the Federal Reserve Fund’s Rates for the period 1995 to 2015 monthly data

(%)...........................................................................................................................................................4

Relationship between the Australian Real GDP growth rates and inflation rates.........................................9

Relationship between the Australian Real GDP growth rates and unemployment rates............................12

Relationship between the Australian net exports and the exchange rates..................................................13

The Australian cash rates relationship with the Federal Reserve Fund’s rates...........................................16

Australian Macroeconomic Outlook Prediction.........................................................................................18

Conclusion.................................................................................................................................................19

References.................................................................................................................................................20

Table of Contents

Executive Summary....................................................................................................................................ii

Australian macroeconomic data from the year 1995 to 2015.......................................................................1

Australian Real Gross Domestic Product Growth Rates from 1995 to 2015............................................1

Australian Inflation Rates for the period 1995 to 2015............................................................................1

Australian Unemployment Rates for the period 1995 to 2015.................................................................2

Australian Exchange Rates for the period 1995 to 2015..........................................................................3

Australian Net Exports for the period 1995 to 2015................................................................................3

Australian Cash Rates and the Federal Reserve Fund’s Rates for the period 1995 to 2015 monthly data

(%)...........................................................................................................................................................4

Relationship between the Australian Real GDP growth rates and inflation rates.........................................9

Relationship between the Australian Real GDP growth rates and unemployment rates............................12

Relationship between the Australian net exports and the exchange rates..................................................13

The Australian cash rates relationship with the Federal Reserve Fund’s rates...........................................16

Australian Macroeconomic Outlook Prediction.........................................................................................18

Conclusion.................................................................................................................................................19

References.................................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

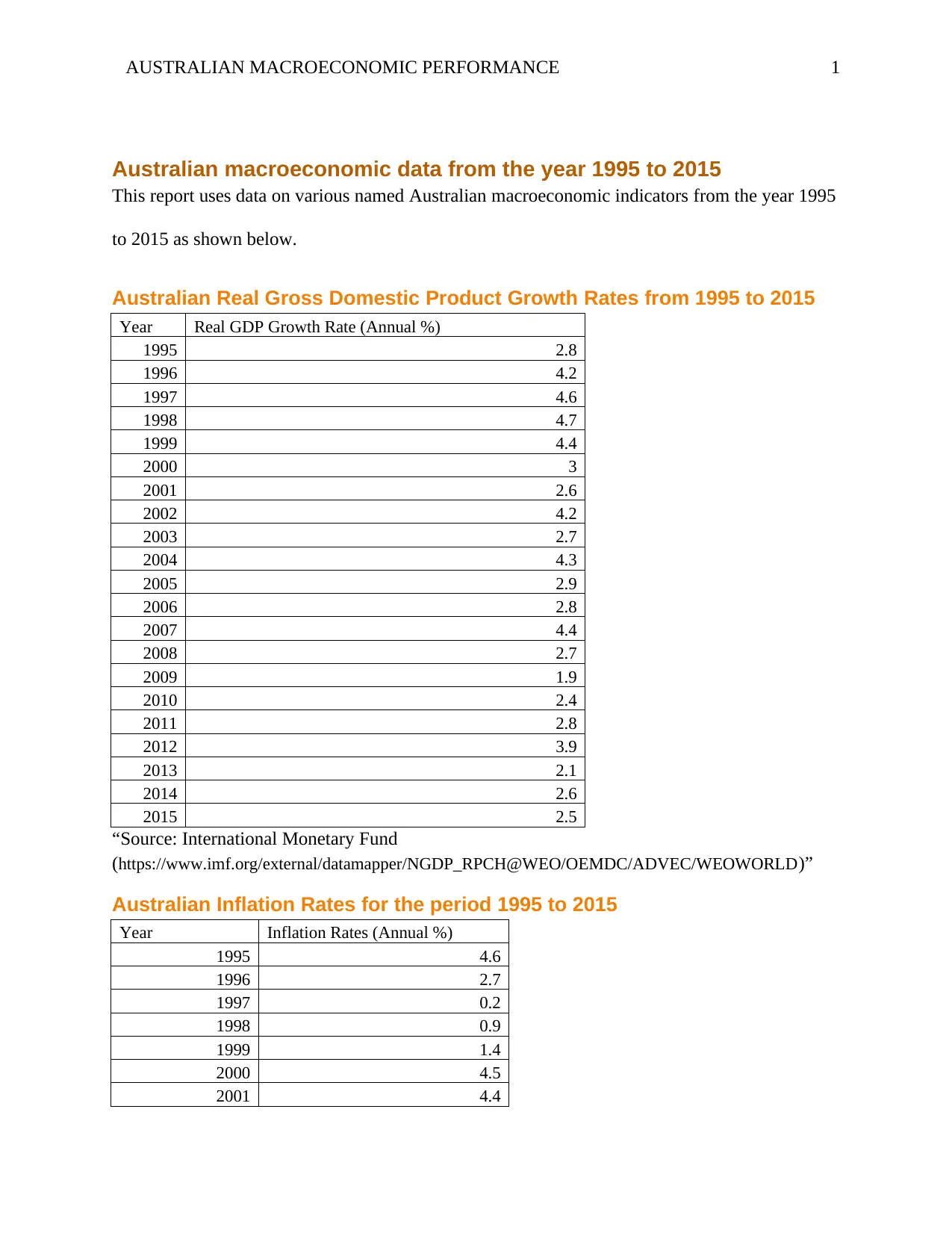

AUSTRALIAN MACROECONOMIC PERFORMANCE 1

Australian macroeconomic data from the year 1995 to 2015

This report uses data on various named Australian macroeconomic indicators from the year 1995

to 2015 as shown below.

Australian Real Gross Domestic Product Growth Rates from 1995 to 2015

Year Real GDP Growth Rate (Annual %)

1995 2.8

1996 4.2

1997 4.6

1998 4.7

1999 4.4

2000 3

2001 2.6

2002 4.2

2003 2.7

2004 4.3

2005 2.9

2006 2.8

2007 4.4

2008 2.7

2009 1.9

2010 2.4

2011 2.8

2012 3.9

2013 2.1

2014 2.6

2015 2.5

“Source: International Monetary Fund

(https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/OEMDC/ADVEC/WEOWORLD)”

Australian Inflation Rates for the period 1995 to 2015

Year Inflation Rates (Annual %)

1995 4.6

1996 2.7

1997 0.2

1998 0.9

1999 1.4

2000 4.5

2001 4.4

Australian macroeconomic data from the year 1995 to 2015

This report uses data on various named Australian macroeconomic indicators from the year 1995

to 2015 as shown below.

Australian Real Gross Domestic Product Growth Rates from 1995 to 2015

Year Real GDP Growth Rate (Annual %)

1995 2.8

1996 4.2

1997 4.6

1998 4.7

1999 4.4

2000 3

2001 2.6

2002 4.2

2003 2.7

2004 4.3

2005 2.9

2006 2.8

2007 4.4

2008 2.7

2009 1.9

2010 2.4

2011 2.8

2012 3.9

2013 2.1

2014 2.6

2015 2.5

“Source: International Monetary Fund

(https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/OEMDC/ADVEC/WEOWORLD)”

Australian Inflation Rates for the period 1995 to 2015

Year Inflation Rates (Annual %)

1995 4.6

1996 2.7

1997 0.2

1998 0.9

1999 1.4

2000 4.5

2001 4.4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

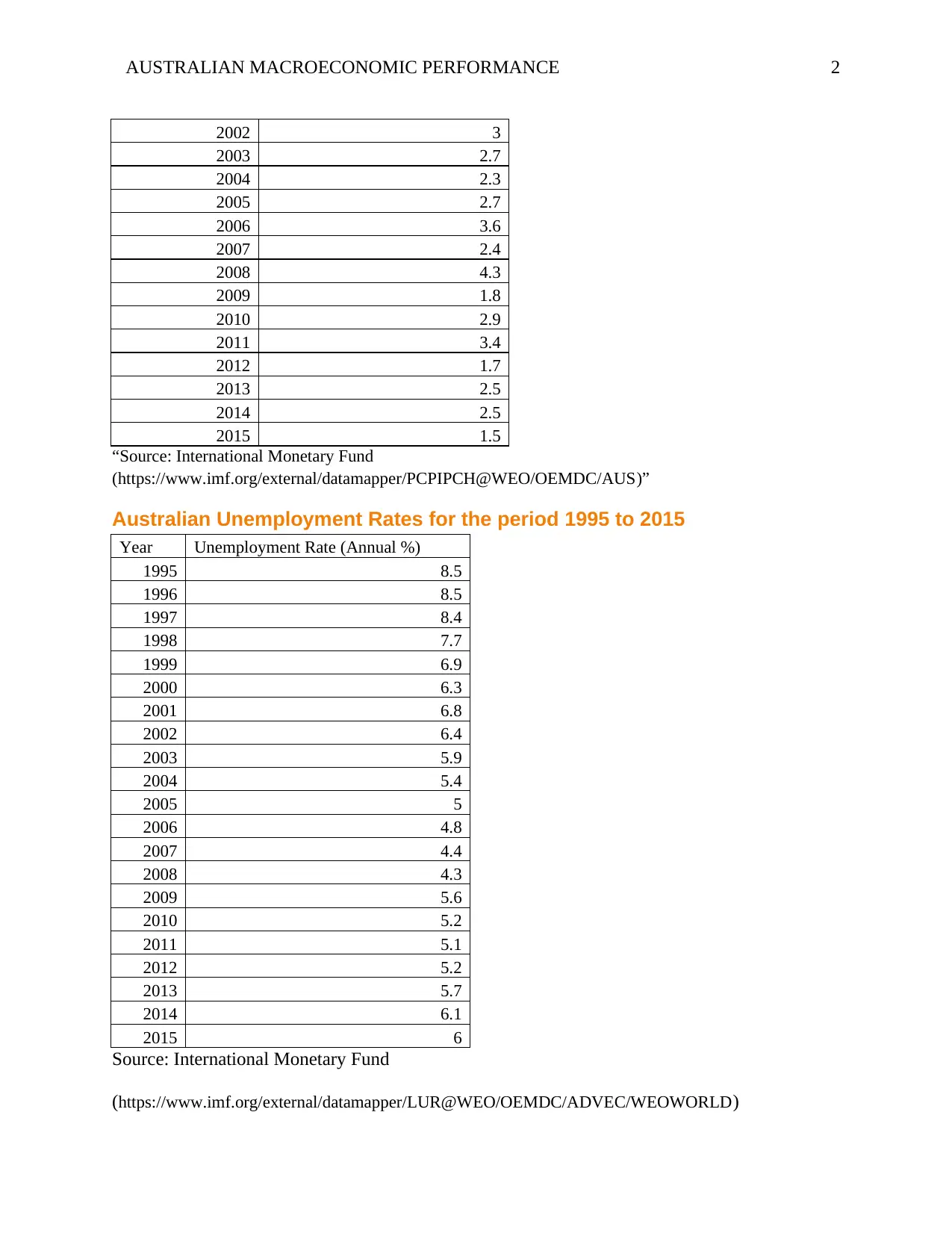

AUSTRALIAN MACROECONOMIC PERFORMANCE 2

2002 3

2003 2.7

2004 2.3

2005 2.7

2006 3.6

2007 2.4

2008 4.3

2009 1.8

2010 2.9

2011 3.4

2012 1.7

2013 2.5

2014 2.5

2015 1.5

“Source: International Monetary Fund

(https://www.imf.org/external/datamapper/PCPIPCH@WEO/OEMDC/AUS)”

Australian Unemployment Rates for the period 1995 to 2015

Year Unemployment Rate (Annual %)

1995 8.5

1996 8.5

1997 8.4

1998 7.7

1999 6.9

2000 6.3

2001 6.8

2002 6.4

2003 5.9

2004 5.4

2005 5

2006 4.8

2007 4.4

2008 4.3

2009 5.6

2010 5.2

2011 5.1

2012 5.2

2013 5.7

2014 6.1

2015 6

Source: International Monetary Fund

(https://www.imf.org/external/datamapper/LUR@WEO/OEMDC/ADVEC/WEOWORLD)

2002 3

2003 2.7

2004 2.3

2005 2.7

2006 3.6

2007 2.4

2008 4.3

2009 1.8

2010 2.9

2011 3.4

2012 1.7

2013 2.5

2014 2.5

2015 1.5

“Source: International Monetary Fund

(https://www.imf.org/external/datamapper/PCPIPCH@WEO/OEMDC/AUS)”

Australian Unemployment Rates for the period 1995 to 2015

Year Unemployment Rate (Annual %)

1995 8.5

1996 8.5

1997 8.4

1998 7.7

1999 6.9

2000 6.3

2001 6.8

2002 6.4

2003 5.9

2004 5.4

2005 5

2006 4.8

2007 4.4

2008 4.3

2009 5.6

2010 5.2

2011 5.1

2012 5.2

2013 5.7

2014 6.1

2015 6

Source: International Monetary Fund

(https://www.imf.org/external/datamapper/LUR@WEO/OEMDC/ADVEC/WEOWORLD)

AUSTRALIAN MACROECONOMIC PERFORMANCE 3

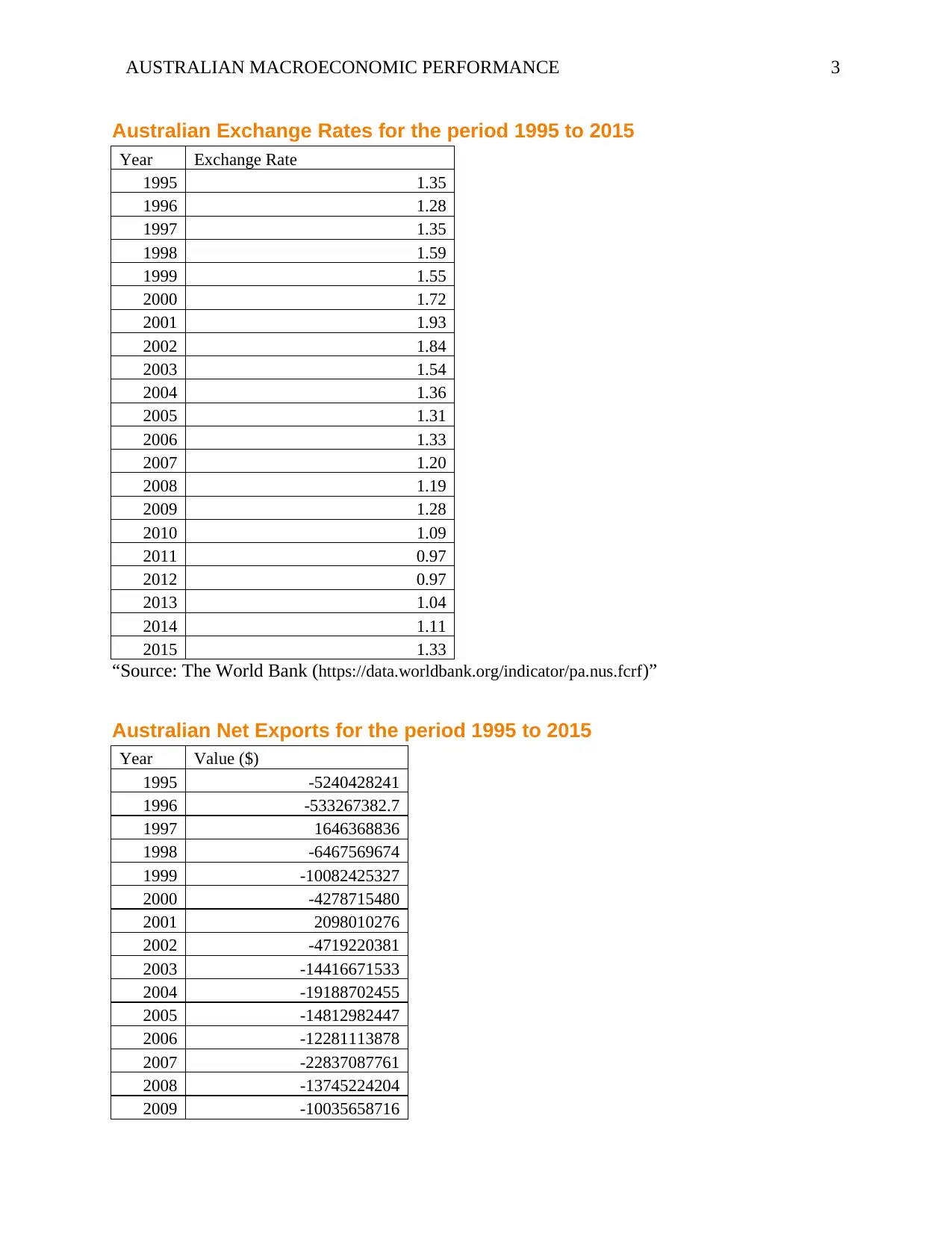

Australian Exchange Rates for the period 1995 to 2015

Year Exchange Rate

1995 1.35

1996 1.28

1997 1.35

1998 1.59

1999 1.55

2000 1.72

2001 1.93

2002 1.84

2003 1.54

2004 1.36

2005 1.31

2006 1.33

2007 1.20

2008 1.19

2009 1.28

2010 1.09

2011 0.97

2012 0.97

2013 1.04

2014 1.11

2015 1.33

“Source: The World Bank (https://data.worldbank.org/indicator/pa.nus.fcrf)”

Australian Net Exports for the period 1995 to 2015

Year Value ($)

1995 -5240428241

1996 -533267382.7

1997 1646368836

1998 -6467569674

1999 -10082425327

2000 -4278715480

2001 2098010276

2002 -4719220381

2003 -14416671533

2004 -19188702455

2005 -14812982447

2006 -12281113878

2007 -22837087761

2008 -13745224204

2009 -10035658716

Australian Exchange Rates for the period 1995 to 2015

Year Exchange Rate

1995 1.35

1996 1.28

1997 1.35

1998 1.59

1999 1.55

2000 1.72

2001 1.93

2002 1.84

2003 1.54

2004 1.36

2005 1.31

2006 1.33

2007 1.20

2008 1.19

2009 1.28

2010 1.09

2011 0.97

2012 0.97

2013 1.04

2014 1.11

2015 1.33

“Source: The World Bank (https://data.worldbank.org/indicator/pa.nus.fcrf)”

Australian Net Exports for the period 1995 to 2015

Year Value ($)

1995 -5240428241

1996 -533267382.7

1997 1646368836

1998 -6467569674

1999 -10082425327

2000 -4278715480

2001 2098010276

2002 -4719220381

2003 -14416671533

2004 -19188702455

2005 -14812982447

2006 -12281113878

2007 -22837087761

2008 -13745224204

2009 -10035658716

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUSTRALIAN MACROECONOMIC PERFORMANCE 4

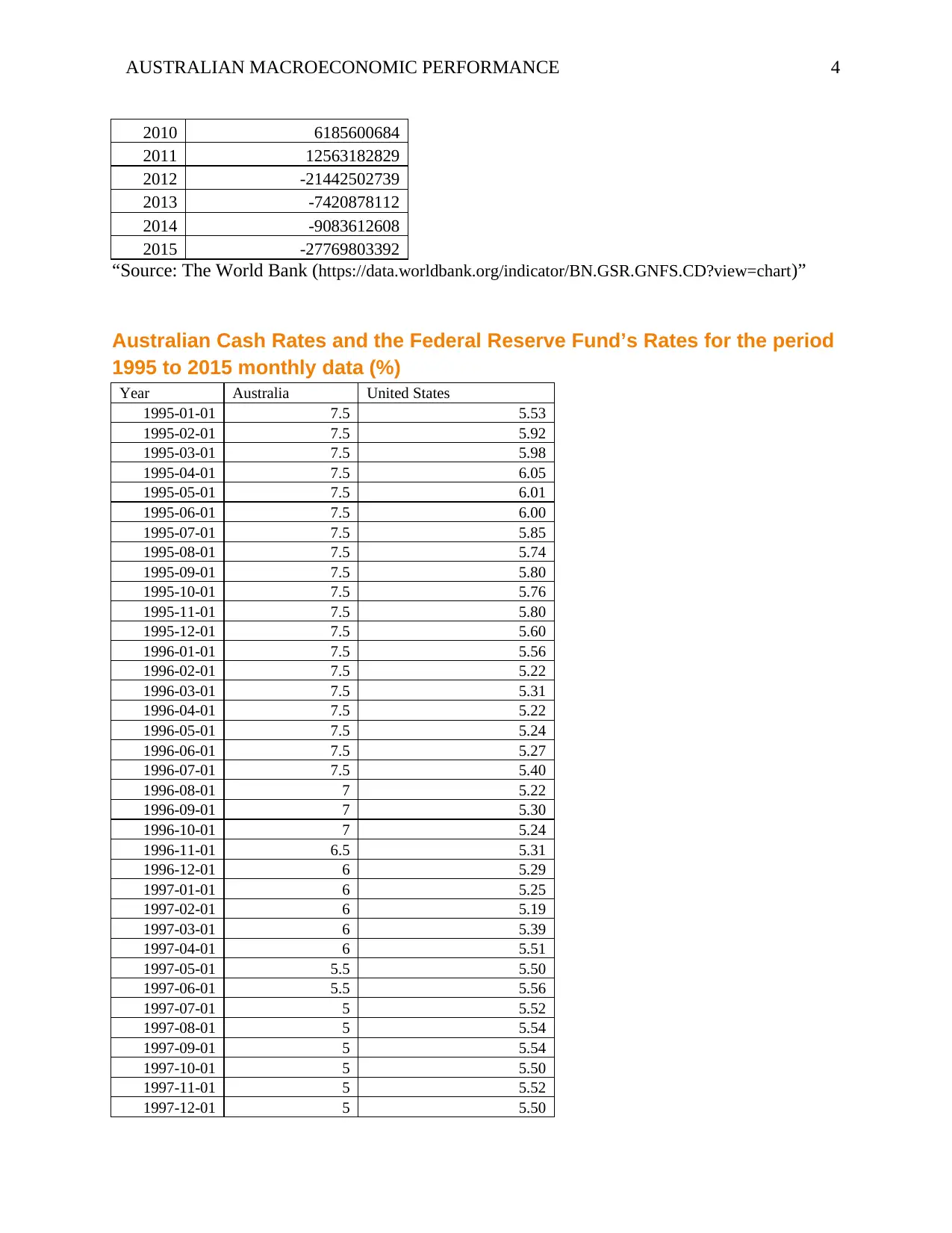

2010 6185600684

2011 12563182829

2012 -21442502739

2013 -7420878112

2014 -9083612608

2015 -27769803392

“Source: The World Bank (https://data.worldbank.org/indicator/BN.GSR.GNFS.CD?view=chart)”

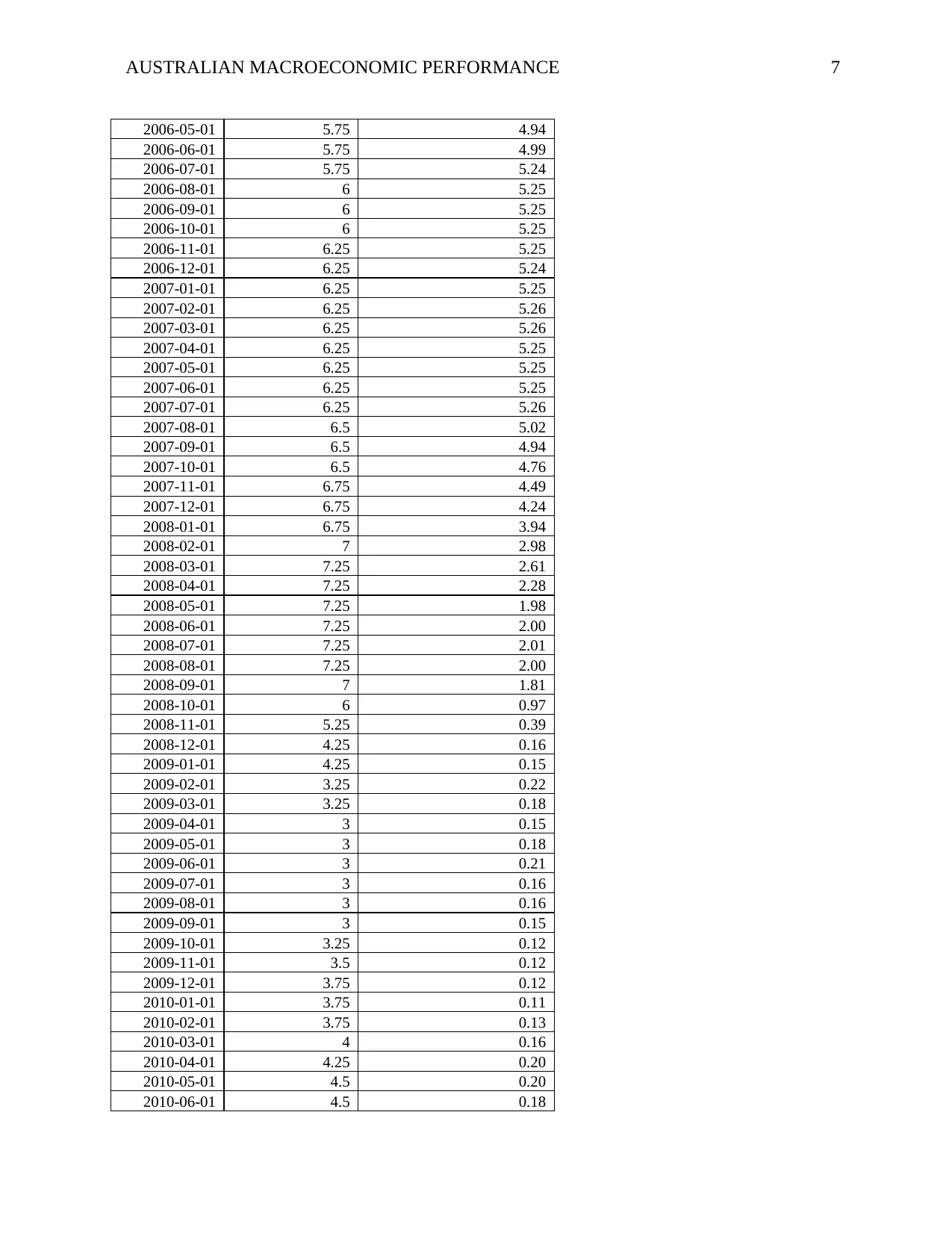

Australian Cash Rates and the Federal Reserve Fund’s Rates for the period

1995 to 2015 monthly data (%)

Year Australia United States

1995-01-01 7.5 5.53

1995-02-01 7.5 5.92

1995-03-01 7.5 5.98

1995-04-01 7.5 6.05

1995-05-01 7.5 6.01

1995-06-01 7.5 6.00

1995-07-01 7.5 5.85

1995-08-01 7.5 5.74

1995-09-01 7.5 5.80

1995-10-01 7.5 5.76

1995-11-01 7.5 5.80

1995-12-01 7.5 5.60

1996-01-01 7.5 5.56

1996-02-01 7.5 5.22

1996-03-01 7.5 5.31

1996-04-01 7.5 5.22

1996-05-01 7.5 5.24

1996-06-01 7.5 5.27

1996-07-01 7.5 5.40

1996-08-01 7 5.22

1996-09-01 7 5.30

1996-10-01 7 5.24

1996-11-01 6.5 5.31

1996-12-01 6 5.29

1997-01-01 6 5.25

1997-02-01 6 5.19

1997-03-01 6 5.39

1997-04-01 6 5.51

1997-05-01 5.5 5.50

1997-06-01 5.5 5.56

1997-07-01 5 5.52

1997-08-01 5 5.54

1997-09-01 5 5.54

1997-10-01 5 5.50

1997-11-01 5 5.52

1997-12-01 5 5.50

2010 6185600684

2011 12563182829

2012 -21442502739

2013 -7420878112

2014 -9083612608

2015 -27769803392

“Source: The World Bank (https://data.worldbank.org/indicator/BN.GSR.GNFS.CD?view=chart)”

Australian Cash Rates and the Federal Reserve Fund’s Rates for the period

1995 to 2015 monthly data (%)

Year Australia United States

1995-01-01 7.5 5.53

1995-02-01 7.5 5.92

1995-03-01 7.5 5.98

1995-04-01 7.5 6.05

1995-05-01 7.5 6.01

1995-06-01 7.5 6.00

1995-07-01 7.5 5.85

1995-08-01 7.5 5.74

1995-09-01 7.5 5.80

1995-10-01 7.5 5.76

1995-11-01 7.5 5.80

1995-12-01 7.5 5.60

1996-01-01 7.5 5.56

1996-02-01 7.5 5.22

1996-03-01 7.5 5.31

1996-04-01 7.5 5.22

1996-05-01 7.5 5.24

1996-06-01 7.5 5.27

1996-07-01 7.5 5.40

1996-08-01 7 5.22

1996-09-01 7 5.30

1996-10-01 7 5.24

1996-11-01 6.5 5.31

1996-12-01 6 5.29

1997-01-01 6 5.25

1997-02-01 6 5.19

1997-03-01 6 5.39

1997-04-01 6 5.51

1997-05-01 5.5 5.50

1997-06-01 5.5 5.56

1997-07-01 5 5.52

1997-08-01 5 5.54

1997-09-01 5 5.54

1997-10-01 5 5.50

1997-11-01 5 5.52

1997-12-01 5 5.50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUSTRALIAN MACROECONOMIC PERFORMANCE 5

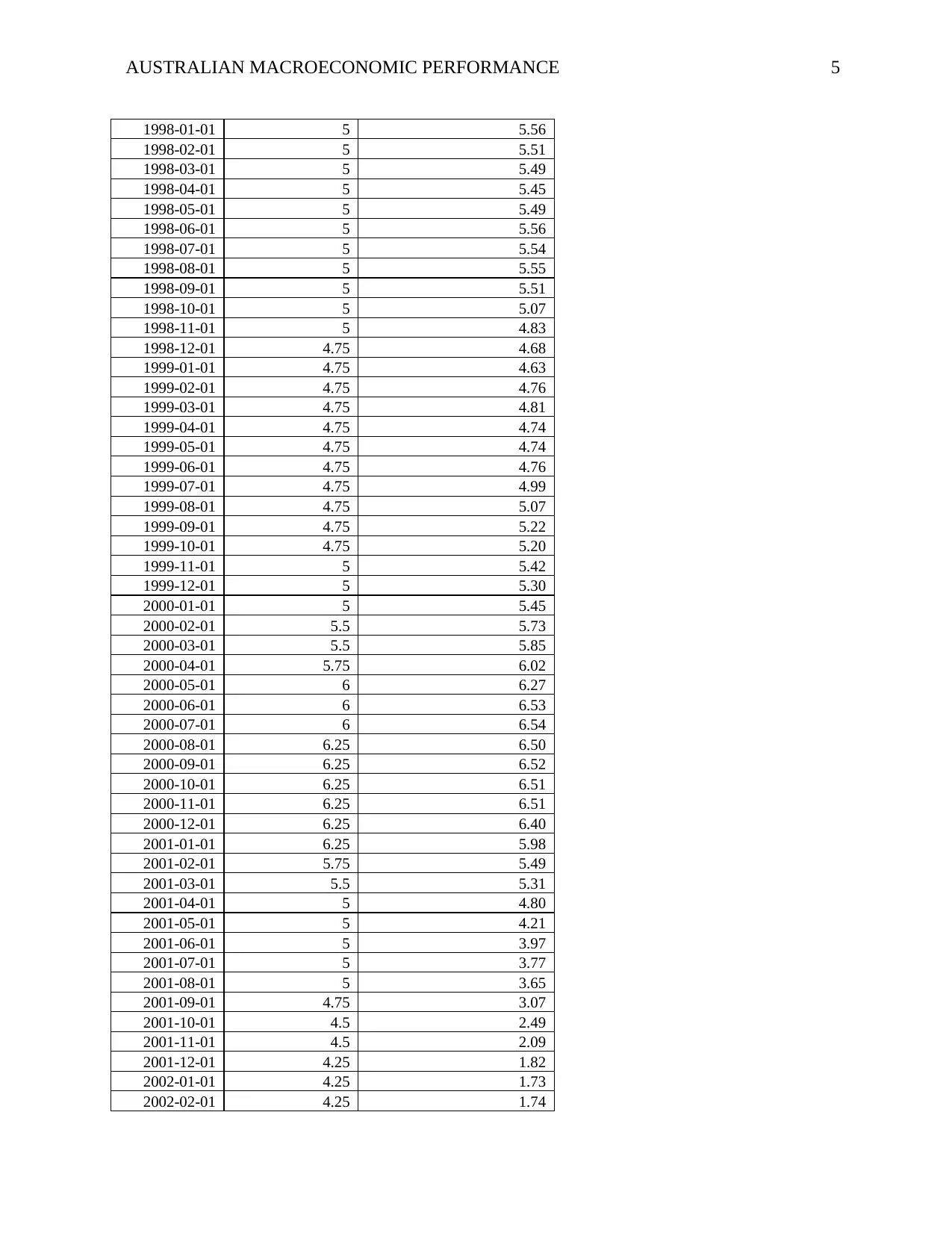

1998-01-01 5 5.56

1998-02-01 5 5.51

1998-03-01 5 5.49

1998-04-01 5 5.45

1998-05-01 5 5.49

1998-06-01 5 5.56

1998-07-01 5 5.54

1998-08-01 5 5.55

1998-09-01 5 5.51

1998-10-01 5 5.07

1998-11-01 5 4.83

1998-12-01 4.75 4.68

1999-01-01 4.75 4.63

1999-02-01 4.75 4.76

1999-03-01 4.75 4.81

1999-04-01 4.75 4.74

1999-05-01 4.75 4.74

1999-06-01 4.75 4.76

1999-07-01 4.75 4.99

1999-08-01 4.75 5.07

1999-09-01 4.75 5.22

1999-10-01 4.75 5.20

1999-11-01 5 5.42

1999-12-01 5 5.30

2000-01-01 5 5.45

2000-02-01 5.5 5.73

2000-03-01 5.5 5.85

2000-04-01 5.75 6.02

2000-05-01 6 6.27

2000-06-01 6 6.53

2000-07-01 6 6.54

2000-08-01 6.25 6.50

2000-09-01 6.25 6.52

2000-10-01 6.25 6.51

2000-11-01 6.25 6.51

2000-12-01 6.25 6.40

2001-01-01 6.25 5.98

2001-02-01 5.75 5.49

2001-03-01 5.5 5.31

2001-04-01 5 4.80

2001-05-01 5 4.21

2001-06-01 5 3.97

2001-07-01 5 3.77

2001-08-01 5 3.65

2001-09-01 4.75 3.07

2001-10-01 4.5 2.49

2001-11-01 4.5 2.09

2001-12-01 4.25 1.82

2002-01-01 4.25 1.73

2002-02-01 4.25 1.74

1998-01-01 5 5.56

1998-02-01 5 5.51

1998-03-01 5 5.49

1998-04-01 5 5.45

1998-05-01 5 5.49

1998-06-01 5 5.56

1998-07-01 5 5.54

1998-08-01 5 5.55

1998-09-01 5 5.51

1998-10-01 5 5.07

1998-11-01 5 4.83

1998-12-01 4.75 4.68

1999-01-01 4.75 4.63

1999-02-01 4.75 4.76

1999-03-01 4.75 4.81

1999-04-01 4.75 4.74

1999-05-01 4.75 4.74

1999-06-01 4.75 4.76

1999-07-01 4.75 4.99

1999-08-01 4.75 5.07

1999-09-01 4.75 5.22

1999-10-01 4.75 5.20

1999-11-01 5 5.42

1999-12-01 5 5.30

2000-01-01 5 5.45

2000-02-01 5.5 5.73

2000-03-01 5.5 5.85

2000-04-01 5.75 6.02

2000-05-01 6 6.27

2000-06-01 6 6.53

2000-07-01 6 6.54

2000-08-01 6.25 6.50

2000-09-01 6.25 6.52

2000-10-01 6.25 6.51

2000-11-01 6.25 6.51

2000-12-01 6.25 6.40

2001-01-01 6.25 5.98

2001-02-01 5.75 5.49

2001-03-01 5.5 5.31

2001-04-01 5 4.80

2001-05-01 5 4.21

2001-06-01 5 3.97

2001-07-01 5 3.77

2001-08-01 5 3.65

2001-09-01 4.75 3.07

2001-10-01 4.5 2.49

2001-11-01 4.5 2.09

2001-12-01 4.25 1.82

2002-01-01 4.25 1.73

2002-02-01 4.25 1.74

AUSTRALIAN MACROECONOMIC PERFORMANCE 6

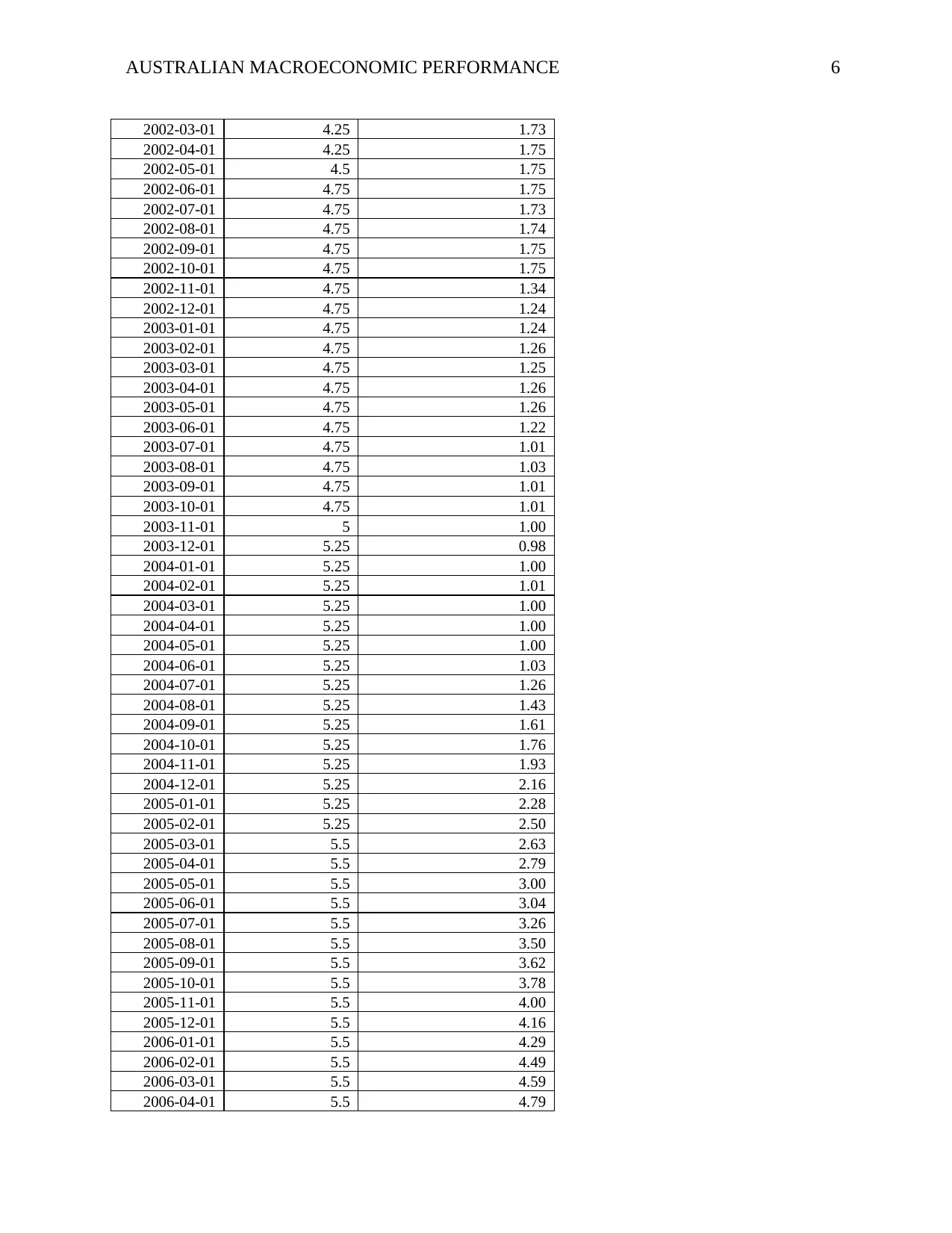

2002-03-01 4.25 1.73

2002-04-01 4.25 1.75

2002-05-01 4.5 1.75

2002-06-01 4.75 1.75

2002-07-01 4.75 1.73

2002-08-01 4.75 1.74

2002-09-01 4.75 1.75

2002-10-01 4.75 1.75

2002-11-01 4.75 1.34

2002-12-01 4.75 1.24

2003-01-01 4.75 1.24

2003-02-01 4.75 1.26

2003-03-01 4.75 1.25

2003-04-01 4.75 1.26

2003-05-01 4.75 1.26

2003-06-01 4.75 1.22

2003-07-01 4.75 1.01

2003-08-01 4.75 1.03

2003-09-01 4.75 1.01

2003-10-01 4.75 1.01

2003-11-01 5 1.00

2003-12-01 5.25 0.98

2004-01-01 5.25 1.00

2004-02-01 5.25 1.01

2004-03-01 5.25 1.00

2004-04-01 5.25 1.00

2004-05-01 5.25 1.00

2004-06-01 5.25 1.03

2004-07-01 5.25 1.26

2004-08-01 5.25 1.43

2004-09-01 5.25 1.61

2004-10-01 5.25 1.76

2004-11-01 5.25 1.93

2004-12-01 5.25 2.16

2005-01-01 5.25 2.28

2005-02-01 5.25 2.50

2005-03-01 5.5 2.63

2005-04-01 5.5 2.79

2005-05-01 5.5 3.00

2005-06-01 5.5 3.04

2005-07-01 5.5 3.26

2005-08-01 5.5 3.50

2005-09-01 5.5 3.62

2005-10-01 5.5 3.78

2005-11-01 5.5 4.00

2005-12-01 5.5 4.16

2006-01-01 5.5 4.29

2006-02-01 5.5 4.49

2006-03-01 5.5 4.59

2006-04-01 5.5 4.79

2002-03-01 4.25 1.73

2002-04-01 4.25 1.75

2002-05-01 4.5 1.75

2002-06-01 4.75 1.75

2002-07-01 4.75 1.73

2002-08-01 4.75 1.74

2002-09-01 4.75 1.75

2002-10-01 4.75 1.75

2002-11-01 4.75 1.34

2002-12-01 4.75 1.24

2003-01-01 4.75 1.24

2003-02-01 4.75 1.26

2003-03-01 4.75 1.25

2003-04-01 4.75 1.26

2003-05-01 4.75 1.26

2003-06-01 4.75 1.22

2003-07-01 4.75 1.01

2003-08-01 4.75 1.03

2003-09-01 4.75 1.01

2003-10-01 4.75 1.01

2003-11-01 5 1.00

2003-12-01 5.25 0.98

2004-01-01 5.25 1.00

2004-02-01 5.25 1.01

2004-03-01 5.25 1.00

2004-04-01 5.25 1.00

2004-05-01 5.25 1.00

2004-06-01 5.25 1.03

2004-07-01 5.25 1.26

2004-08-01 5.25 1.43

2004-09-01 5.25 1.61

2004-10-01 5.25 1.76

2004-11-01 5.25 1.93

2004-12-01 5.25 2.16

2005-01-01 5.25 2.28

2005-02-01 5.25 2.50

2005-03-01 5.5 2.63

2005-04-01 5.5 2.79

2005-05-01 5.5 3.00

2005-06-01 5.5 3.04

2005-07-01 5.5 3.26

2005-08-01 5.5 3.50

2005-09-01 5.5 3.62

2005-10-01 5.5 3.78

2005-11-01 5.5 4.00

2005-12-01 5.5 4.16

2006-01-01 5.5 4.29

2006-02-01 5.5 4.49

2006-03-01 5.5 4.59

2006-04-01 5.5 4.79

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUSTRALIAN MACROECONOMIC PERFORMANCE 7

2006-05-01 5.75 4.94

2006-06-01 5.75 4.99

2006-07-01 5.75 5.24

2006-08-01 6 5.25

2006-09-01 6 5.25

2006-10-01 6 5.25

2006-11-01 6.25 5.25

2006-12-01 6.25 5.24

2007-01-01 6.25 5.25

2007-02-01 6.25 5.26

2007-03-01 6.25 5.26

2007-04-01 6.25 5.25

2007-05-01 6.25 5.25

2007-06-01 6.25 5.25

2007-07-01 6.25 5.26

2007-08-01 6.5 5.02

2007-09-01 6.5 4.94

2007-10-01 6.5 4.76

2007-11-01 6.75 4.49

2007-12-01 6.75 4.24

2008-01-01 6.75 3.94

2008-02-01 7 2.98

2008-03-01 7.25 2.61

2008-04-01 7.25 2.28

2008-05-01 7.25 1.98

2008-06-01 7.25 2.00

2008-07-01 7.25 2.01

2008-08-01 7.25 2.00

2008-09-01 7 1.81

2008-10-01 6 0.97

2008-11-01 5.25 0.39

2008-12-01 4.25 0.16

2009-01-01 4.25 0.15

2009-02-01 3.25 0.22

2009-03-01 3.25 0.18

2009-04-01 3 0.15

2009-05-01 3 0.18

2009-06-01 3 0.21

2009-07-01 3 0.16

2009-08-01 3 0.16

2009-09-01 3 0.15

2009-10-01 3.25 0.12

2009-11-01 3.5 0.12

2009-12-01 3.75 0.12

2010-01-01 3.75 0.11

2010-02-01 3.75 0.13

2010-03-01 4 0.16

2010-04-01 4.25 0.20

2010-05-01 4.5 0.20

2010-06-01 4.5 0.18

2006-05-01 5.75 4.94

2006-06-01 5.75 4.99

2006-07-01 5.75 5.24

2006-08-01 6 5.25

2006-09-01 6 5.25

2006-10-01 6 5.25

2006-11-01 6.25 5.25

2006-12-01 6.25 5.24

2007-01-01 6.25 5.25

2007-02-01 6.25 5.26

2007-03-01 6.25 5.26

2007-04-01 6.25 5.25

2007-05-01 6.25 5.25

2007-06-01 6.25 5.25

2007-07-01 6.25 5.26

2007-08-01 6.5 5.02

2007-09-01 6.5 4.94

2007-10-01 6.5 4.76

2007-11-01 6.75 4.49

2007-12-01 6.75 4.24

2008-01-01 6.75 3.94

2008-02-01 7 2.98

2008-03-01 7.25 2.61

2008-04-01 7.25 2.28

2008-05-01 7.25 1.98

2008-06-01 7.25 2.00

2008-07-01 7.25 2.01

2008-08-01 7.25 2.00

2008-09-01 7 1.81

2008-10-01 6 0.97

2008-11-01 5.25 0.39

2008-12-01 4.25 0.16

2009-01-01 4.25 0.15

2009-02-01 3.25 0.22

2009-03-01 3.25 0.18

2009-04-01 3 0.15

2009-05-01 3 0.18

2009-06-01 3 0.21

2009-07-01 3 0.16

2009-08-01 3 0.16

2009-09-01 3 0.15

2009-10-01 3.25 0.12

2009-11-01 3.5 0.12

2009-12-01 3.75 0.12

2010-01-01 3.75 0.11

2010-02-01 3.75 0.13

2010-03-01 4 0.16

2010-04-01 4.25 0.20

2010-05-01 4.5 0.20

2010-06-01 4.5 0.18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUSTRALIAN MACROECONOMIC PERFORMANCE 8

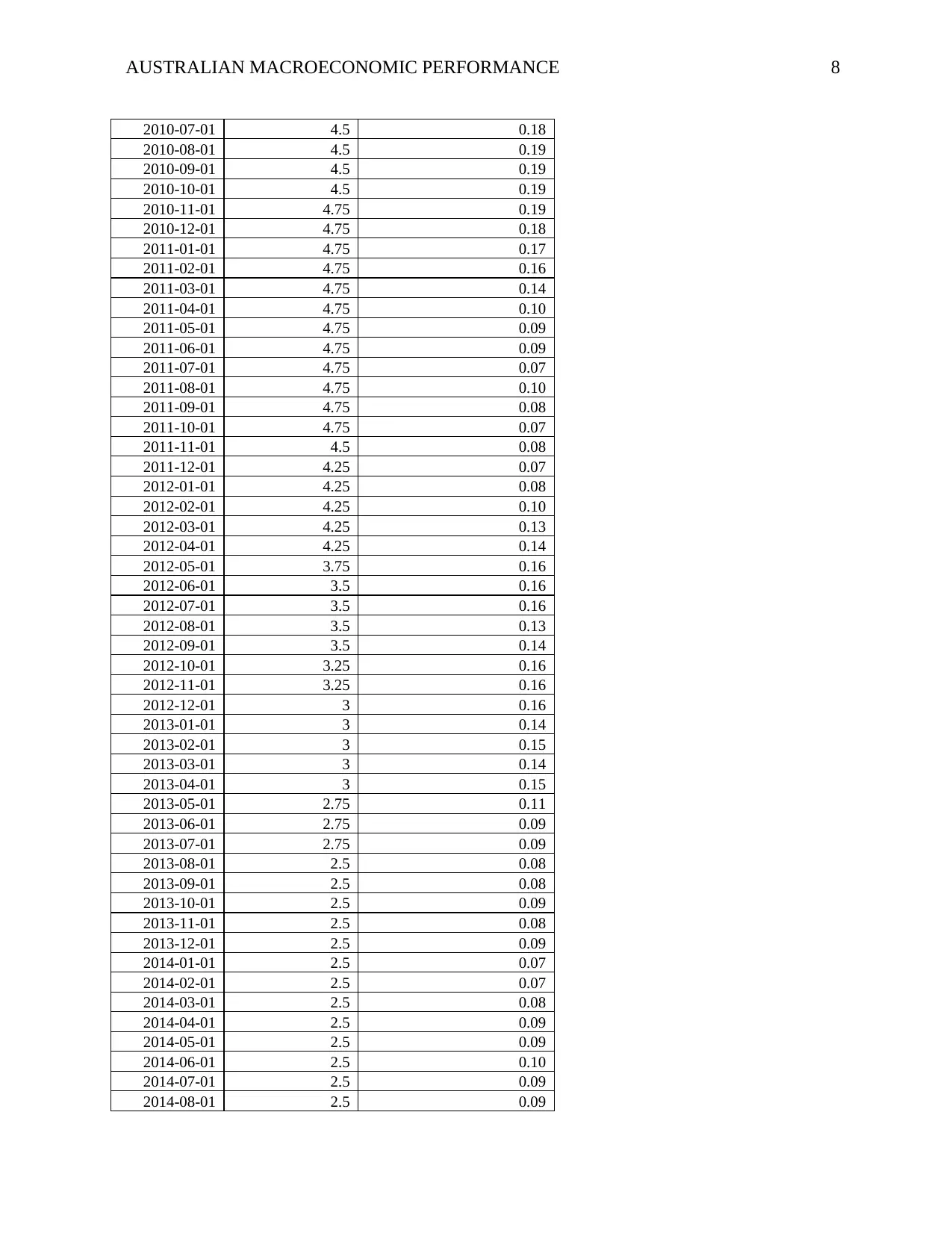

2010-07-01 4.5 0.18

2010-08-01 4.5 0.19

2010-09-01 4.5 0.19

2010-10-01 4.5 0.19

2010-11-01 4.75 0.19

2010-12-01 4.75 0.18

2011-01-01 4.75 0.17

2011-02-01 4.75 0.16

2011-03-01 4.75 0.14

2011-04-01 4.75 0.10

2011-05-01 4.75 0.09

2011-06-01 4.75 0.09

2011-07-01 4.75 0.07

2011-08-01 4.75 0.10

2011-09-01 4.75 0.08

2011-10-01 4.75 0.07

2011-11-01 4.5 0.08

2011-12-01 4.25 0.07

2012-01-01 4.25 0.08

2012-02-01 4.25 0.10

2012-03-01 4.25 0.13

2012-04-01 4.25 0.14

2012-05-01 3.75 0.16

2012-06-01 3.5 0.16

2012-07-01 3.5 0.16

2012-08-01 3.5 0.13

2012-09-01 3.5 0.14

2012-10-01 3.25 0.16

2012-11-01 3.25 0.16

2012-12-01 3 0.16

2013-01-01 3 0.14

2013-02-01 3 0.15

2013-03-01 3 0.14

2013-04-01 3 0.15

2013-05-01 2.75 0.11

2013-06-01 2.75 0.09

2013-07-01 2.75 0.09

2013-08-01 2.5 0.08

2013-09-01 2.5 0.08

2013-10-01 2.5 0.09

2013-11-01 2.5 0.08

2013-12-01 2.5 0.09

2014-01-01 2.5 0.07

2014-02-01 2.5 0.07

2014-03-01 2.5 0.08

2014-04-01 2.5 0.09

2014-05-01 2.5 0.09

2014-06-01 2.5 0.10

2014-07-01 2.5 0.09

2014-08-01 2.5 0.09

2010-07-01 4.5 0.18

2010-08-01 4.5 0.19

2010-09-01 4.5 0.19

2010-10-01 4.5 0.19

2010-11-01 4.75 0.19

2010-12-01 4.75 0.18

2011-01-01 4.75 0.17

2011-02-01 4.75 0.16

2011-03-01 4.75 0.14

2011-04-01 4.75 0.10

2011-05-01 4.75 0.09

2011-06-01 4.75 0.09

2011-07-01 4.75 0.07

2011-08-01 4.75 0.10

2011-09-01 4.75 0.08

2011-10-01 4.75 0.07

2011-11-01 4.5 0.08

2011-12-01 4.25 0.07

2012-01-01 4.25 0.08

2012-02-01 4.25 0.10

2012-03-01 4.25 0.13

2012-04-01 4.25 0.14

2012-05-01 3.75 0.16

2012-06-01 3.5 0.16

2012-07-01 3.5 0.16

2012-08-01 3.5 0.13

2012-09-01 3.5 0.14

2012-10-01 3.25 0.16

2012-11-01 3.25 0.16

2012-12-01 3 0.16

2013-01-01 3 0.14

2013-02-01 3 0.15

2013-03-01 3 0.14

2013-04-01 3 0.15

2013-05-01 2.75 0.11

2013-06-01 2.75 0.09

2013-07-01 2.75 0.09

2013-08-01 2.5 0.08

2013-09-01 2.5 0.08

2013-10-01 2.5 0.09

2013-11-01 2.5 0.08

2013-12-01 2.5 0.09

2014-01-01 2.5 0.07

2014-02-01 2.5 0.07

2014-03-01 2.5 0.08

2014-04-01 2.5 0.09

2014-05-01 2.5 0.09

2014-06-01 2.5 0.10

2014-07-01 2.5 0.09

2014-08-01 2.5 0.09

AUSTRALIAN MACROECONOMIC PERFORMANCE 9

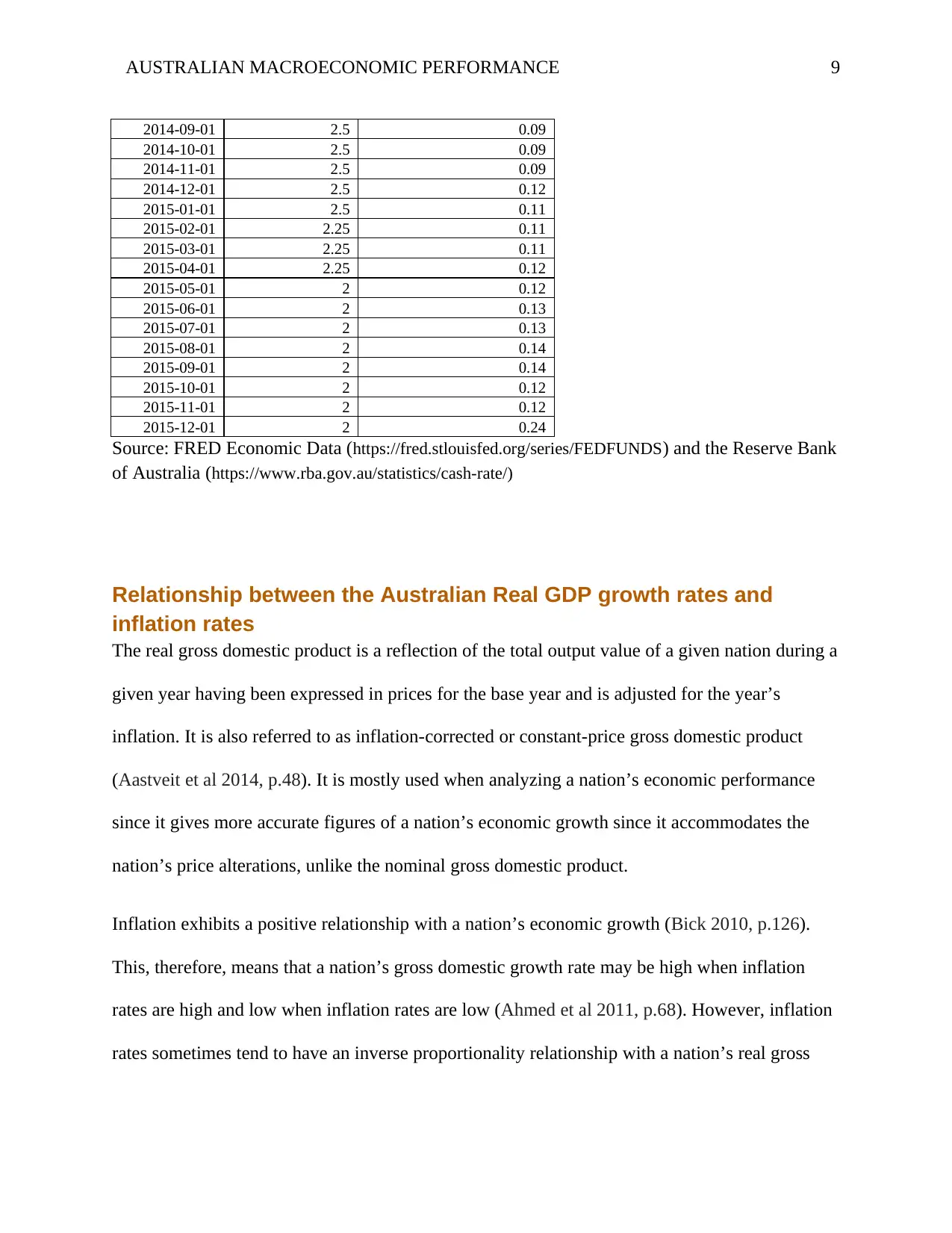

2014-09-01 2.5 0.09

2014-10-01 2.5 0.09

2014-11-01 2.5 0.09

2014-12-01 2.5 0.12

2015-01-01 2.5 0.11

2015-02-01 2.25 0.11

2015-03-01 2.25 0.11

2015-04-01 2.25 0.12

2015-05-01 2 0.12

2015-06-01 2 0.13

2015-07-01 2 0.13

2015-08-01 2 0.14

2015-09-01 2 0.14

2015-10-01 2 0.12

2015-11-01 2 0.12

2015-12-01 2 0.24

Source: FRED Economic Data (https://fred.stlouisfed.org/series/FEDFUNDS) and the Reserve Bank

of Australia (https://www.rba.gov.au/statistics/cash-rate/)

Relationship between the Australian Real GDP growth rates and

inflation rates

The real gross domestic product is a reflection of the total output value of a given nation during a

given year having been expressed in prices for the base year and is adjusted for the year’s

inflation. It is also referred to as inflation-corrected or constant-price gross domestic product

(Aastveit et al 2014, p.48). It is mostly used when analyzing a nation’s economic performance

since it gives more accurate figures of a nation’s economic growth since it accommodates the

nation’s price alterations, unlike the nominal gross domestic product.

Inflation exhibits a positive relationship with a nation’s economic growth (Bick 2010, p.126).

This, therefore, means that a nation’s gross domestic growth rate may be high when inflation

rates are high and low when inflation rates are low (Ahmed et al 2011, p.68). However, inflation

rates sometimes tend to have an inverse proportionality relationship with a nation’s real gross

2014-09-01 2.5 0.09

2014-10-01 2.5 0.09

2014-11-01 2.5 0.09

2014-12-01 2.5 0.12

2015-01-01 2.5 0.11

2015-02-01 2.25 0.11

2015-03-01 2.25 0.11

2015-04-01 2.25 0.12

2015-05-01 2 0.12

2015-06-01 2 0.13

2015-07-01 2 0.13

2015-08-01 2 0.14

2015-09-01 2 0.14

2015-10-01 2 0.12

2015-11-01 2 0.12

2015-12-01 2 0.24

Source: FRED Economic Data (https://fred.stlouisfed.org/series/FEDFUNDS) and the Reserve Bank

of Australia (https://www.rba.gov.au/statistics/cash-rate/)

Relationship between the Australian Real GDP growth rates and

inflation rates

The real gross domestic product is a reflection of the total output value of a given nation during a

given year having been expressed in prices for the base year and is adjusted for the year’s

inflation. It is also referred to as inflation-corrected or constant-price gross domestic product

(Aastveit et al 2014, p.48). It is mostly used when analyzing a nation’s economic performance

since it gives more accurate figures of a nation’s economic growth since it accommodates the

nation’s price alterations, unlike the nominal gross domestic product.

Inflation exhibits a positive relationship with a nation’s economic growth (Bick 2010, p.126).

This, therefore, means that a nation’s gross domestic growth rate may be high when inflation

rates are high and low when inflation rates are low (Ahmed et al 2011, p.68). However, inflation

rates sometimes tend to have an inverse proportionality relationship with a nation’s real gross

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.