TAX305 Taxation Law: Assignment

Added on 2020-05-01

9 Pages1560 Words70 Views

AUSTRALIAN PARTNERSHIP TAXATION APPROACHThe Two B’s Partners Income Statement & Mary’s Tax Payable BreakdownStudents' NameCourse Title Instructor’s NameInstitutional AffiliationCity and State Date of Submission

AUSTRALIAN PARTNERSHIP TAXATION APPROACHAASB 101(2009) guides us on how to prepare and present partnership income statements and requires us to similarly approach partnership preparation of statements just alike to what constitutes other statements whereby the vertical format of presentation is deemed applicable whereas rules guiding when and how revenue ought to be earned and reported prevails as well when expense relating to the revenue should be accounted for and reported referenced in Gran(2008.Pg 7).The Australian partnership tax return instruction 2013 further emphasize on what entails partnership profit income or loss and how it is calculated and reported it further outlines on how the profit income or loss should be distributed. Partners get into business upon agreeing in a partnership agreement on how operations and management of the business should be conducted. They further agree on how profit and losses as well as liabilities and assets ought to be shared in case of dissolution or cessation if any Hodge (2005.Pg 13).I further wish to state that although a partnership business is deemed independent most decision and actions lies with the partners in any case there is no single regulation that requires a partnership business to pay income tax instead the burden is shifted to individual partners themselves who after accounting for revenue and expenses thus expected to share theloss or profit as per agreed sharing ratios and later on report the profit or loss in their individual income statement for tax purpose Udovitch (2011.Pg 25)(. It can therefore be stated that partnership income profit or loss stands as individual income statement item during reporting Saez (2012.Pg 35). ‘The Two B’s’Net Partnership Profit or Loss Income StatementFor The Year Ended 30th June 2017Revenue;$

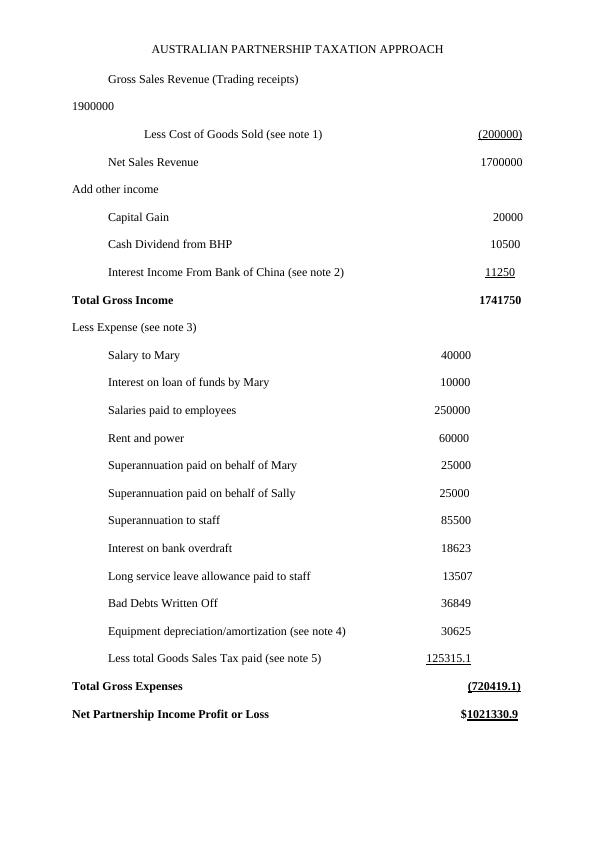

AUSTRALIAN PARTNERSHIP TAXATION APPROACHGross Sales Revenue (Trading receipts) 1900000Less Cost of Goods Sold (see note 1) (200000) Net Sales Revenue 1700000Add other incomeCapital Gain 20000Cash Dividend from BHP 10500Interest Income From Bank of China (see note 2) 11250Total Gross Income 1741750Less Expense (see note 3) Salary to Mary 40000Interest on loan of funds by Mary 10000Salaries paid to employees 250000Rent and power 60000Superannuation paid on behalf of Mary 25000Superannuation paid on behalf of Sally 25000Superannuation to staff 85500Interest on bank overdraft 18623Long service leave allowance paid to staff 13507Bad Debts Written Off 36849Equipment depreciation/amortization (see note 4) 30625Less total Goods Sales Tax paid (see note 5) 125315.1Total Gross Expenses (720419.1)Net Partnership Income Profit or Loss $1021330.9

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

TAX305 Taxation Assignmentlg...

|9

|1590

|73

Taxation Assignment Reportlg...

|8

|2017

|42

ACC3TAX Taxation Group Assignmentlg...

|9

|1991

|44

Janet Brown Taxable Income and Adviselg...

|5

|608

|79

TAXATION LAW. TAXATION LAW. TAXATION LAW. 4. 4. Taxatiolg...

|6

|489

|47

Taxation Of Partnership Business: Assignmentlg...

|10

|1883

|39