Australian Tax | Taxation Law | Assignment

VerifiedAdded on 2022/08/26

|7

|1292

|15

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................3

References:.................................................................................................................................5

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................3

References:.................................................................................................................................5

2TAXATION LAW

Answer to Part 1:

As per the definition under “sec 108-5” Capital Gain Tax (CGT) asset refers a terms

of property and lawful or equivalent rights which would not be treated as property (Deutsch

2018). Talking about the examples of CGT asset is the building, shares, debts and the land.

These assets is owned by an individual taxpayer, which has a right to enter an agreement and

foreign currency. It is very important to calculate the capital gains tax on the specific CGT

assets after identifying the CGT event. As eminent, “CGT event A1” takes into consideration

under “sec 104-10 (1)” when a CGT asset is sold CGT.

The court of law in “FCT v Sara Lee Household (2002)” suggest that CGT event is

very essential. While the taxpayer’s individual forms a contract or no contract given, then it is

crucial to determine the change of ownership (Grange, Jover-Ledesma and Maydew 2014).

One the other perspective “McDonald v FCT (1998)” a verbal arrangement refers to the

acquisition including, whether the contract is applicable or not. It has to be measured based

on purchase date. On finding the contract preliminary and not actual arrangement for

purchase, the final date of agreement is identified.

Taxpayers usually enters into the agreement for selling the assets when the CGT

assets needs to be sold. Assets might be involved in the real estates. However, CGT events

happens when the taxpayers enter into an agreement but does not involves the time of

settlement happens. CGT events normally conducted for investors, when capital gains are

raised from disposal of shares (Kenny, Blissenden and Villios 2018). It is very essential to

calculate the time for CGT events. Meanwhile the responsibilities fall on taxpayer to include

the capital gains or loss in assessable earnings that might influence the tax position at the time

of calculating tax obligation.

Answer to Part 1:

As per the definition under “sec 108-5” Capital Gain Tax (CGT) asset refers a terms

of property and lawful or equivalent rights which would not be treated as property (Deutsch

2018). Talking about the examples of CGT asset is the building, shares, debts and the land.

These assets is owned by an individual taxpayer, which has a right to enter an agreement and

foreign currency. It is very important to calculate the capital gains tax on the specific CGT

assets after identifying the CGT event. As eminent, “CGT event A1” takes into consideration

under “sec 104-10 (1)” when a CGT asset is sold CGT.

The court of law in “FCT v Sara Lee Household (2002)” suggest that CGT event is

very essential. While the taxpayer’s individual forms a contract or no contract given, then it is

crucial to determine the change of ownership (Grange, Jover-Ledesma and Maydew 2014).

One the other perspective “McDonald v FCT (1998)” a verbal arrangement refers to the

acquisition including, whether the contract is applicable or not. It has to be measured based

on purchase date. On finding the contract preliminary and not actual arrangement for

purchase, the final date of agreement is identified.

Taxpayers usually enters into the agreement for selling the assets when the CGT

assets needs to be sold. Assets might be involved in the real estates. However, CGT events

happens when the taxpayers enter into an agreement but does not involves the time of

settlement happens. CGT events normally conducted for investors, when capital gains are

raised from disposal of shares (Kenny, Blissenden and Villios 2018). It is very essential to

calculate the time for CGT events. Meanwhile the responsibilities fall on taxpayer to include

the capital gains or loss in assessable earnings that might influence the tax position at the time

of calculating tax obligation.

3TAXATION LAW

Answer to Part 2:

The situation that has arose by the event of Harrison, depicts that he invested in

property in 2001 at a cost of acquisition of $800,000. As per the “sec 108-5 ITAA 1997” the

property will be considered as CGT assets. Throughout the year 2018, He sold the property

investment for $1.3 million. The sale of investment property rise to “CGT event A1” under

“sec 104-10 (1)”. Giving the instance of the verdict made in “FCT v Sara Lee Household

(2002)” a “CGT event A1” occurred at the time of Harrison schedule a covenant of disposing

the investment property (McCouat 2018). As far as the concern of the ownership, it gets

change when he sale off the investment property. Conferring to the “sec 116-20” the amount

of $1.3 million was accumulated by Harrison at the time he sold the property. The receiving

amount represents the capital proceedings depending on the market value for the CGT (Sadiq

et al. 2018). The net asset value of capital gains which Harrison earned by the selling of the

property that will be considered as taxable earnings, refer to “sec 102-5 ITAA 1997”.

Harrison also refers the purchase of shares in October 1985 by giving $4 each share.

He finally dispose of the shares at $12 per share on 20th June 2018. Rendering to “sec 108-5”

shares must be categorized as CGT asset. The shares is ought to be viewed as post CGT asset

and consequently the capital gains tax must be applied, as he accumulated the shares in

October 1985. (Sadiq 2014). Harrison entered into the covenant of sale on 20th June 2018.

The sale of shares has followed by “CGT event A1” within “sect 104-10 (1)”. Citing the

justification on “FCT v Sara Lee Household (2002)” Harrison arrived into the contract of

disposing the shares on 20th June, therefore the capital gains is derived during the year of

2017-2018. The time of CGT event is when Harrison signed the contract rather not at that

time when settlement happened.

Answer to Part 2:

The situation that has arose by the event of Harrison, depicts that he invested in

property in 2001 at a cost of acquisition of $800,000. As per the “sec 108-5 ITAA 1997” the

property will be considered as CGT assets. Throughout the year 2018, He sold the property

investment for $1.3 million. The sale of investment property rise to “CGT event A1” under

“sec 104-10 (1)”. Giving the instance of the verdict made in “FCT v Sara Lee Household

(2002)” a “CGT event A1” occurred at the time of Harrison schedule a covenant of disposing

the investment property (McCouat 2018). As far as the concern of the ownership, it gets

change when he sale off the investment property. Conferring to the “sec 116-20” the amount

of $1.3 million was accumulated by Harrison at the time he sold the property. The receiving

amount represents the capital proceedings depending on the market value for the CGT (Sadiq

et al. 2018). The net asset value of capital gains which Harrison earned by the selling of the

property that will be considered as taxable earnings, refer to “sec 102-5 ITAA 1997”.

Harrison also refers the purchase of shares in October 1985 by giving $4 each share.

He finally dispose of the shares at $12 per share on 20th June 2018. Rendering to “sec 108-5”

shares must be categorized as CGT asset. The shares is ought to be viewed as post CGT asset

and consequently the capital gains tax must be applied, as he accumulated the shares in

October 1985. (Sadiq 2014). Harrison entered into the covenant of sale on 20th June 2018.

The sale of shares has followed by “CGT event A1” within “sect 104-10 (1)”. Citing the

justification on “FCT v Sara Lee Household (2002)” Harrison arrived into the contract of

disposing the shares on 20th June, therefore the capital gains is derived during the year of

2017-2018. The time of CGT event is when Harrison signed the contract rather not at that

time when settlement happened.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

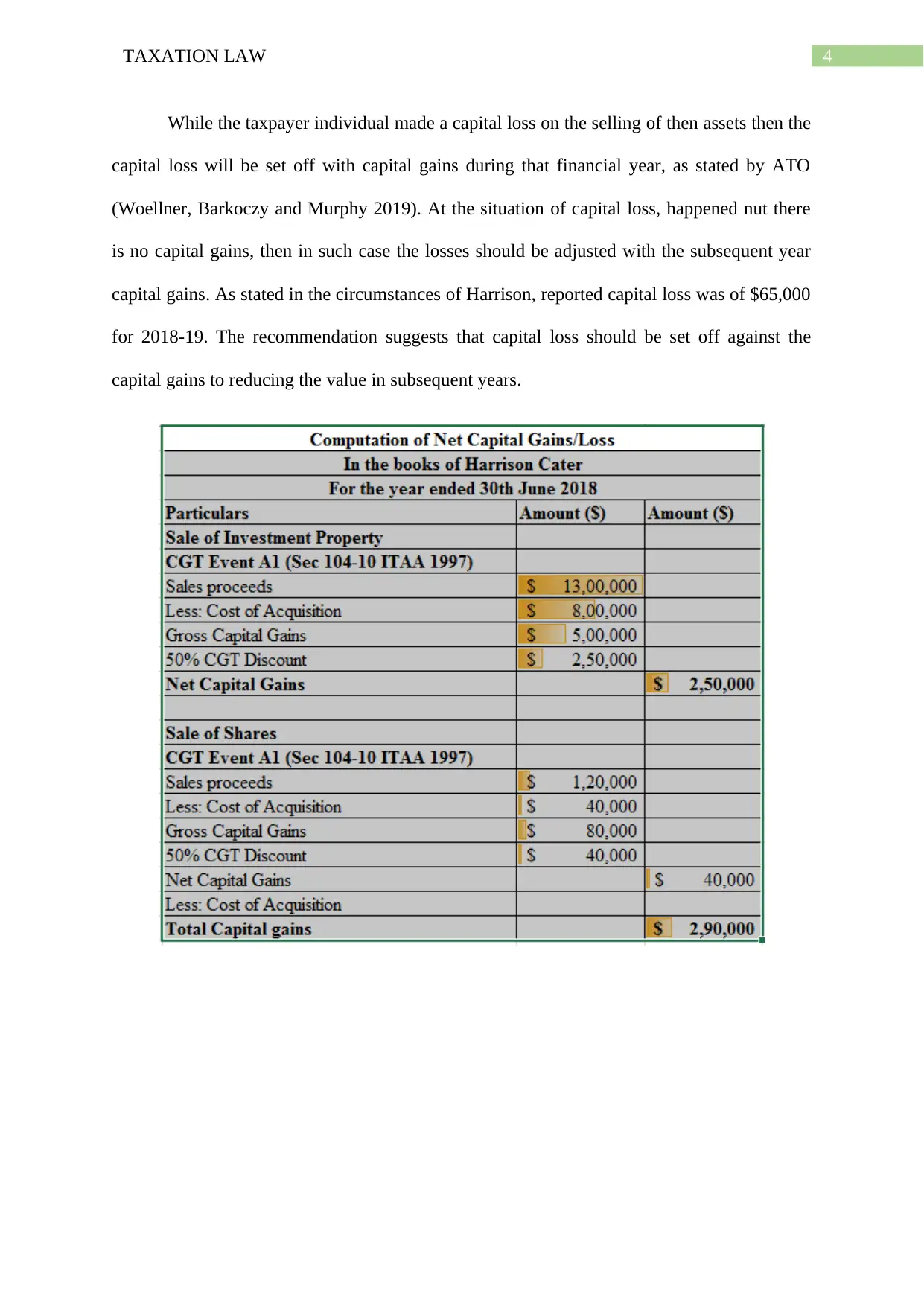

While the taxpayer individual made a capital loss on the selling of then assets then the

capital loss will be set off with capital gains during that financial year, as stated by ATO

(Woellner, Barkoczy and Murphy 2019). At the situation of capital loss, happened nut there

is no capital gains, then in such case the losses should be adjusted with the subsequent year

capital gains. As stated in the circumstances of Harrison, reported capital loss was of $65,000

for 2018-19. The recommendation suggests that capital loss should be set off against the

capital gains to reducing the value in subsequent years.

While the taxpayer individual made a capital loss on the selling of then assets then the

capital loss will be set off with capital gains during that financial year, as stated by ATO

(Woellner, Barkoczy and Murphy 2019). At the situation of capital loss, happened nut there

is no capital gains, then in such case the losses should be adjusted with the subsequent year

capital gains. As stated in the circumstances of Harrison, reported capital loss was of $65,000

for 2018-19. The recommendation suggests that capital loss should be set off against the

capital gains to reducing the value in subsequent years.

5TAXATION LAW

Part C: Video Transcript:

I am about to begin presentation on Capital Gains Tax. At first I would like to say that

the CGT asset normally involves the property and lawful or equivalent rights which would

not be treated as property.

I would further like to say that it is necessary to calculate the capital gains tax on the

specific CGT assets after identifying the CGT event. I have understood that, “CGT event A1”

takes into consideration under “sec 104-10 (1)” when a CGT asset is sold CGT. To determine

the CGT event

I have referred to decision given in “FCT v Sara Lee Household (2002)”. I have

understood from this case that it is important to determine on which the change of ownership

happened.

I understood that taxpayers typically enters into the agreement for selling the assets

when the CGT assets needs to be sold. Hence the taxpayer should calculate the time for CGT

events.

I applied the decision given in “FCT v Sara Lee Household (2002)” to know the

timing of the CGT event in the case of Harrison.

I found that the contract of selling the shares was entered into by Harrison in June

2018 and hence it will be taxable within the same year when the contract was entered into.

Part C: Video Transcript:

I am about to begin presentation on Capital Gains Tax. At first I would like to say that

the CGT asset normally involves the property and lawful or equivalent rights which would

not be treated as property.

I would further like to say that it is necessary to calculate the capital gains tax on the

specific CGT assets after identifying the CGT event. I have understood that, “CGT event A1”

takes into consideration under “sec 104-10 (1)” when a CGT asset is sold CGT. To determine

the CGT event

I have referred to decision given in “FCT v Sara Lee Household (2002)”. I have

understood from this case that it is important to determine on which the change of ownership

happened.

I understood that taxpayers typically enters into the agreement for selling the assets

when the CGT assets needs to be sold. Hence the taxpayer should calculate the time for CGT

events.

I applied the decision given in “FCT v Sara Lee Household (2002)” to know the

timing of the CGT event in the case of Harrison.

I found that the contract of selling the shares was entered into by Harrison in June

2018 and hence it will be taxable within the same year when the contract was entered into.

6TAXATION LAW

References:

Deutsch, R. (2018). Australian Tax Handbook 2018: Thomson Reuters Australia.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. principles of business taxation.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

McCouat, P. 2018. Australian master GST guide.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Sadiq, K. 2014. Principles of taxation law.

Woellner, R., Barkoczy, S. and Murphy, S. 2019. Australian taxation law.

References:

Deutsch, R. (2018). Australian Tax Handbook 2018: Thomson Reuters Australia.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. principles of business taxation.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

McCouat, P. 2018. Australian master GST guide.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Sadiq, K. 2014. Principles of taxation law.

Woellner, R., Barkoczy, S. and Murphy, S. 2019. Australian taxation law.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.