Australian Taxation Law Assignment: Analysis of Tax Scenarios and Laws

VerifiedAdded on 2020/04/07

|14

|2743

|35

Homework Assignment

AI Summary

This assignment provides a detailed analysis of various aspects of Australian Taxation Law. It addresses key issues such as calculating net capital gains or losses from asset sales, exploring the implications of the Fringe Benefit Tax (FBT) and its application based on the Taxation Ruling TR 93/6, and evaluating the taxable positions of co-owners of rental properties. The assignment also examines tax avoidance strategies and the rights of individuals to plan their tax affairs, referencing the IRC v Duke Westminster case. Furthermore, it investigates the taxable income of a primary producer, Bill, considering forestry operations and relevant tax rulings, including TR 95/6 and the Income Tax Assessment Act 1936. The document uses relevant case laws and sections of the ITAA 1997 to support the analysis and provides practical applications of the tax laws in the context of the given scenarios.

Running head: AUSTRALIAN TAXATION LAW

Australian Taxation Law

Name of the Student:

Name of the University:

Author Note:

Australian Taxation Law

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUSTRALIAN TAXATION LAW

Answer to Question 1

Issue

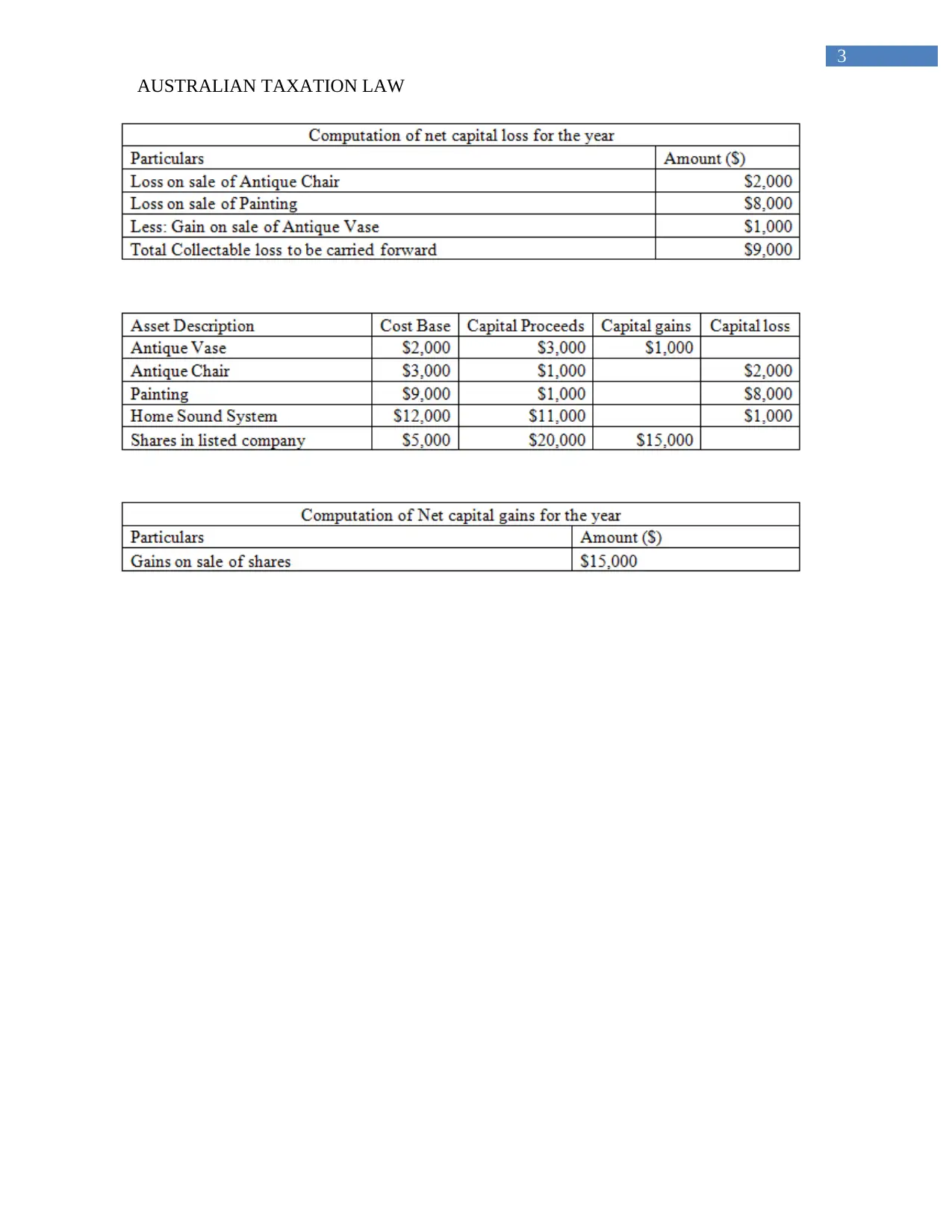

The provided case requires calculation of net capital gain or net capital loss for the year

(Coleman and Sadiq 2013). Hence, it is important to resolve the situation that arises from net

capital gains or losses as derived from asset sale for a given period of time frame. In this

particular question, Eric bought different assets over past 12 months and decided to sell it. The

assets bought by Eric are antique vase, painting, home sound system as well as antique chair and

shares that are listed business. After selling the assets, it is necessary to calculate capital gains or

loss by keeping in mind whether Eric had net capital gain or loss from sale of these assets

(Grange, Jover-Ledesma and Maydew 2014).

Laws

“Section 108 (20) of the ITAA 1997”

“Section 108 (10) of ITAA 1997”

AUSTRALIAN TAXATION LAW

Answer to Question 1

Issue

The provided case requires calculation of net capital gain or net capital loss for the year

(Coleman and Sadiq 2013). Hence, it is important to resolve the situation that arises from net

capital gains or losses as derived from asset sale for a given period of time frame. In this

particular question, Eric bought different assets over past 12 months and decided to sell it. The

assets bought by Eric are antique vase, painting, home sound system as well as antique chair and

shares that are listed business. After selling the assets, it is necessary to calculate capital gains or

loss by keeping in mind whether Eric had net capital gain or loss from sale of these assets

(Grange, Jover-Ledesma and Maydew 2014).

Laws

“Section 108 (20) of the ITAA 1997”

“Section 108 (10) of ITAA 1997”

3

AUSTRALIAN TAXATION LAW

AUSTRALIAN TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUSTRALIAN TAXATION LAW

Applications

No loss can be measured based on the removal of personal use of assets. In addition, it is

found that counterbalance need to be taken into explanation based on the Section 108-10 of

ITAA 1997 (Grange, Jover-Ledesma and Maydew 2014). It is important to understand the fact

on how Eric dealt with capital loss or gain after disposal of assets. From the section, it is implicit

that CST assets are treated cost base that is not prejudiced to decrease as it involves those where

capital gain or capital loss will not be made (Coleman and Sadiq 2013). In addition, CST assets

that are acquired before 20th of September 1985 should be dealt under the section 108-20 of the

ITAA 1997 as it needs to track stock or any of the personal assets. Consequently, the capital gain

for Eric has current stand of $15000 (Sadiq et al. 2014).

Question 2

To that, it was clearly understood that ATO has formerly issued by the Section Taxation

Ruling TR 93/6 from the perspective of loan account in case of arranging for offset of account

(Kenny 2013). The provided case deals with the issue of Fringe Benefit Tax that is properly

explained under Fringe Benefit Act 1999. The issue that is recognized in the given situation is

related with ascertainment of FBT and in agreement with the “Taxation Ruling of TR 93/6”

(Coleman and Sadiq 2013)

AUSTRALIAN TAXATION LAW

Applications

No loss can be measured based on the removal of personal use of assets. In addition, it is

found that counterbalance need to be taken into explanation based on the Section 108-10 of

ITAA 1997 (Grange, Jover-Ledesma and Maydew 2014). It is important to understand the fact

on how Eric dealt with capital loss or gain after disposal of assets. From the section, it is implicit

that CST assets are treated cost base that is not prejudiced to decrease as it involves those where

capital gain or capital loss will not be made (Coleman and Sadiq 2013). In addition, CST assets

that are acquired before 20th of September 1985 should be dealt under the section 108-20 of the

ITAA 1997 as it needs to track stock or any of the personal assets. Consequently, the capital gain

for Eric has current stand of $15000 (Sadiq et al. 2014).

Question 2

To that, it was clearly understood that ATO has formerly issued by the Section Taxation

Ruling TR 93/6 from the perspective of loan account in case of arranging for offset of account

(Kenny 2013). The provided case deals with the issue of Fringe Benefit Tax that is properly

explained under Fringe Benefit Act 1999. The issue that is recognized in the given situation is

related with ascertainment of FBT and in agreement with the “Taxation Ruling of TR 93/6”

(Coleman and Sadiq 2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUSTRALIAN TAXATION LAW

Applications

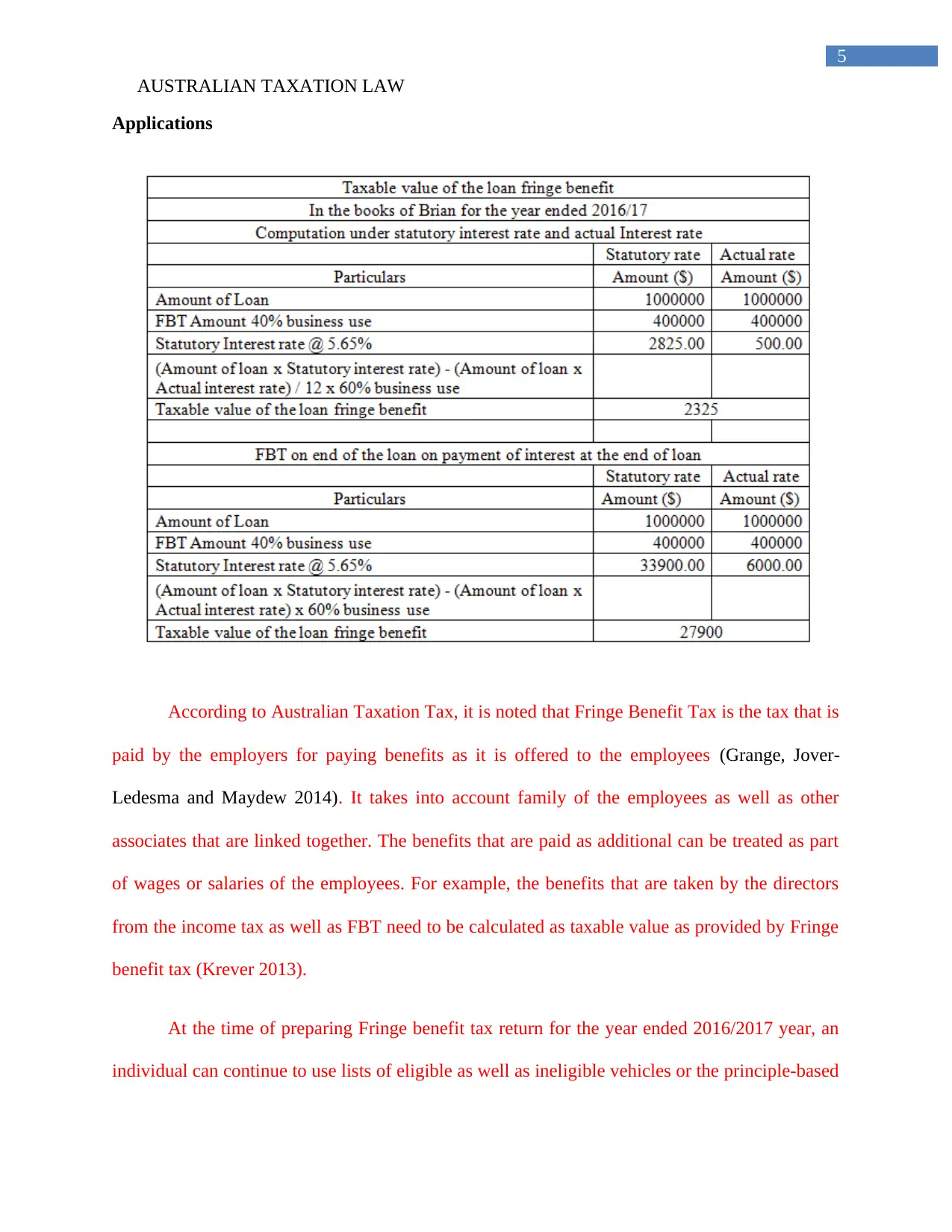

According to Australian Taxation Tax, it is noted that Fringe Benefit Tax is the tax that is

paid by the employers for paying benefits as it is offered to the employees (Grange, Jover-

Ledesma and Maydew 2014). It takes into account family of the employees as well as other

associates that are linked together. The benefits that are paid as additional can be treated as part

of wages or salaries of the employees. For example, the benefits that are taken by the directors

from the income tax as well as FBT need to be calculated as taxable value as provided by Fringe

benefit tax (Krever 2013).

At the time of preparing Fringe benefit tax return for the year ended 2016/2017 year, an

individual can continue to use lists of eligible as well as ineligible vehicles or the principle-based

AUSTRALIAN TAXATION LAW

Applications

According to Australian Taxation Tax, it is noted that Fringe Benefit Tax is the tax that is

paid by the employers for paying benefits as it is offered to the employees (Grange, Jover-

Ledesma and Maydew 2014). It takes into account family of the employees as well as other

associates that are linked together. The benefits that are paid as additional can be treated as part

of wages or salaries of the employees. For example, the benefits that are taken by the directors

from the income tax as well as FBT need to be calculated as taxable value as provided by Fringe

benefit tax (Krever 2013).

At the time of preparing Fringe benefit tax return for the year ended 2016/2017 year, an

individual can continue to use lists of eligible as well as ineligible vehicles or the principle-based

6

AUSTRALIAN TAXATION LAW

approach or methods. In addition, the eligible as well as ineligible vehicle lists can be removed

after 2017 (Grange, Jover-Ledesma and Maydew 2014). To that, the product mentioned are

structured for offsetting the rate of interest that is maintained by the clients. The above table

explains the calculation of loan fringe benefits under the section Taxation Rulings TR 93/6. In

this section, it explains how business plans for their loan offset that in actual is known as interest

offset accord. It is further concluded by saying that paying any sum of income legal

responsibility is taken into considered when Brian is unrestricted from paying interest by the

bank (Krever 2015).

It is important to understand person who are liable to pay for fringe benefit tax (Grange,

Jover-Ledesma and Maydew 2014). This is where any person or employer offers any of the

fringe benefits to his employee or the associate of the employee that aligns with status of

employment as paid for fringe benefit tax. Furthermore, the employee for which the employer is

needed to pay fringe benefit tax can be done for past, present or for future employee. The

imposition of fringe benefit tax is mainly proposed to tax companies on situation provided to

their employees as mentioned in the budget among the corporate and tax circles (Morgan,

Mortimer and Pinto 2013). The fringe benefit provided by an employer to his employees in

addition to cash salary or wages payments considered as fringe benefit tax (Coleman and Sadiq

2013).

Question 3

Laws

Section 51 of the ITAA 1997

Taxation rulings of TR 93/32

AUSTRALIAN TAXATION LAW

approach or methods. In addition, the eligible as well as ineligible vehicle lists can be removed

after 2017 (Grange, Jover-Ledesma and Maydew 2014). To that, the product mentioned are

structured for offsetting the rate of interest that is maintained by the clients. The above table

explains the calculation of loan fringe benefits under the section Taxation Rulings TR 93/6. In

this section, it explains how business plans for their loan offset that in actual is known as interest

offset accord. It is further concluded by saying that paying any sum of income legal

responsibility is taken into considered when Brian is unrestricted from paying interest by the

bank (Krever 2015).

It is important to understand person who are liable to pay for fringe benefit tax (Grange,

Jover-Ledesma and Maydew 2014). This is where any person or employer offers any of the

fringe benefits to his employee or the associate of the employee that aligns with status of

employment as paid for fringe benefit tax. Furthermore, the employee for which the employer is

needed to pay fringe benefit tax can be done for past, present or for future employee. The

imposition of fringe benefit tax is mainly proposed to tax companies on situation provided to

their employees as mentioned in the budget among the corporate and tax circles (Morgan,

Mortimer and Pinto 2013). The fringe benefit provided by an employer to his employees in

addition to cash salary or wages payments considered as fringe benefit tax (Coleman and Sadiq

2013).

Question 3

Laws

Section 51 of the ITAA 1997

Taxation rulings of TR 93/32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUSTRALIAN TAXATION LAW

FC of T v McDonald (1987)

Applications

In addition, the rulings highlight evaluating regarding the taxable position of co-owners

of those who are not responsible to carry out their values within actions. From the given

situation, it is noted that Jack and Jill need to evaluate their taxable position of the rental

property. In addition, the loss of profits gained from the leasing possessions in actual need to be

managed through co-ownership of rental property and deal out business proceeds and losses.

Thus, the co-owners of the leasing possessions named as Jack and Jill will be investment the

property as joint ventures and this act as an ordinary issue in the given case state of affairs (Sadiq

et al. 2014). As far as Taxation ruling of TR 93/32 is concerned, it highlights the fact when

acceptability for the purpose of income tax can be treated as net income profit or loss. Here, Jack

gets a share of 10% and Jill will get 90% of the total profit gained (Grange, Jover-Ledesma and

Maydew 2014). In that case, if Jack and Jill both sell property when the cost base as well as

reduced cost needs to be taken into addressed with gains or losses in alignment of interest

ownership for specific property

Question 4

The provided case is in accordance with the law named as IRC v Duke Westminster

(1936) that is shown in specific event for the purpose of avoiding tax. In this case, one gardener

was employed by the dyke who actually paid from the post-tax income of Duke (Morgan,

Mortimer and Pinto 2013). Furthermore, it is noted that the tax purpose is chargeable when he

stopped paying the gardener irrespective of paying for the same amount of money. The present

case deals with taxation ruling that enables Duke for claiming deduction from his taxable income

AUSTRALIAN TAXATION LAW

FC of T v McDonald (1987)

Applications

In addition, the rulings highlight evaluating regarding the taxable position of co-owners

of those who are not responsible to carry out their values within actions. From the given

situation, it is noted that Jack and Jill need to evaluate their taxable position of the rental

property. In addition, the loss of profits gained from the leasing possessions in actual need to be

managed through co-ownership of rental property and deal out business proceeds and losses.

Thus, the co-owners of the leasing possessions named as Jack and Jill will be investment the

property as joint ventures and this act as an ordinary issue in the given case state of affairs (Sadiq

et al. 2014). As far as Taxation ruling of TR 93/32 is concerned, it highlights the fact when

acceptability for the purpose of income tax can be treated as net income profit or loss. Here, Jack

gets a share of 10% and Jill will get 90% of the total profit gained (Grange, Jover-Ledesma and

Maydew 2014). In that case, if Jack and Jill both sell property when the cost base as well as

reduced cost needs to be taken into addressed with gains or losses in alignment of interest

ownership for specific property

Question 4

The provided case is in accordance with the law named as IRC v Duke Westminster

(1936) that is shown in specific event for the purpose of avoiding tax. In this case, one gardener

was employed by the dyke who actually paid from the post-tax income of Duke (Morgan,

Mortimer and Pinto 2013). Furthermore, it is noted that the tax purpose is chargeable when he

stopped paying the gardener irrespective of paying for the same amount of money. The present

case deals with taxation ruling that enables Duke for claiming deduction from his taxable income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUSTRALIAN TAXATION LAW

as it get reduced with the income tax liability. As far as present case is concerned, each person is

entitled for planning the tax avoidance based on the current requirement or preference where no

person can be forced to pay higher amount of tax. This present case study has proper relevance

from Australia where it is clearly mentioned that each of the individual has the right to select

their own transaction where taxpayer achieves the advantage of given asset as a matter of fact

(Novikov, Ling and Kordzakhia 2014). The person will be able to select or choose the option of

the transaction as it will subject to tax or subject that is deducted tax as compared to others. The

case law states the fact about principles where every person or individual should be permitted to

understand the tax affairs and laws properly to avoid further confusion. The cases explained

reveals the fact that courts have looked over the overall impact and made the decisions

accordingly (Schreiber 2013). As far as present case is concerned, the transaction has to be pre-

arranged artificially as well as not served properly for commercial activities. The cases explained

reveals the fact that courts have looked over the overall impact and made the decisions

accordingly. As far as present case is concerned, the transaction has to be pre-arranged

artificially as well as not served properly for commercial activities (Davis et al. 2015).

In the current complex state of affairs, it is noted that the standard within Australia

depicts the fact that if an individual start achieving success for making the results secured, then

the Inland Revenue might be current as a proposal as they cannot force anyone for paying any

increased amount of tax (Woellner 2013).

AUSTRALIAN TAXATION LAW

as it get reduced with the income tax liability. As far as present case is concerned, each person is

entitled for planning the tax avoidance based on the current requirement or preference where no

person can be forced to pay higher amount of tax. This present case study has proper relevance

from Australia where it is clearly mentioned that each of the individual has the right to select

their own transaction where taxpayer achieves the advantage of given asset as a matter of fact

(Novikov, Ling and Kordzakhia 2014). The person will be able to select or choose the option of

the transaction as it will subject to tax or subject that is deducted tax as compared to others. The

case law states the fact about principles where every person or individual should be permitted to

understand the tax affairs and laws properly to avoid further confusion. The cases explained

reveals the fact that courts have looked over the overall impact and made the decisions

accordingly (Schreiber 2013). As far as present case is concerned, the transaction has to be pre-

arranged artificially as well as not served properly for commercial activities. The cases explained

reveals the fact that courts have looked over the overall impact and made the decisions

accordingly. As far as present case is concerned, the transaction has to be pre-arranged

artificially as well as not served properly for commercial activities (Davis et al. 2015).

In the current complex state of affairs, it is noted that the standard within Australia

depicts the fact that if an individual start achieving success for making the results secured, then

the Inland Revenue might be current as a proposal as they cannot force anyone for paying any

increased amount of tax (Woellner 2013).

9

AUSTRALIAN TAXATION LAW

Question 5

Issue

The provided case on Bill relates to taxable income as it is explained by the taxpayer as

Bill is the Primary Producer as under Section 6 (1) of the ITAA 1997.

Laws

Subsection 6 (1) of the Income Tax Assessment Act 1936

McCauley v. The Federal Commissioner of Taxation (1944)

Section 26 (f)

Taxation Rulings 95/6

Applications

As far as current situation is concerned, it is noted that Bill owns a large piece of land

where there are several pine trees (Woellner 2013). In addition, Bill principally aims at using the

land for grazing sheep as well as wanted to have it cleared. To that, it is noted that the logging

company had grabbed from his piece of land. These aspects mainly explain assessable income

whether the taxpayers gets indulged with the activities of forestry industry. To that, the forest

operations take into account felling of trees in a forest or plantation where the taxpayers show no

interest about the planted trees (Douglas et al. 2014).

Under Taxation Ruling TR 95/6 that explain about Income tax dealing with primary

production as well as forestry that highlights different deductions that are made available to the

primary producers that is engaged at the time of conducting forest operations or activities

(Coleman and Sadiq 2013). In addition, the deductibility of these expenses cannot be altered by

simple fact that an individual derive income from carbon sequestration activities as it is carried

AUSTRALIAN TAXATION LAW

Question 5

Issue

The provided case on Bill relates to taxable income as it is explained by the taxpayer as

Bill is the Primary Producer as under Section 6 (1) of the ITAA 1997.

Laws

Subsection 6 (1) of the Income Tax Assessment Act 1936

McCauley v. The Federal Commissioner of Taxation (1944)

Section 26 (f)

Taxation Rulings 95/6

Applications

As far as current situation is concerned, it is noted that Bill owns a large piece of land

where there are several pine trees (Woellner 2013). In addition, Bill principally aims at using the

land for grazing sheep as well as wanted to have it cleared. To that, it is noted that the logging

company had grabbed from his piece of land. These aspects mainly explain assessable income

whether the taxpayers gets indulged with the activities of forestry industry. To that, the forest

operations take into account felling of trees in a forest or plantation where the taxpayers show no

interest about the planted trees (Douglas et al. 2014).

Under Taxation Ruling TR 95/6 that explain about Income tax dealing with primary

production as well as forestry that highlights different deductions that are made available to the

primary producers that is engaged at the time of conducting forest operations or activities

(Coleman and Sadiq 2013). In addition, the deductibility of these expenses cannot be altered by

simple fact that an individual derive income from carbon sequestration activities as it is carried

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUSTRALIAN TAXATION LAW

on in conjunction and aligns according to forestry activities or operations (Petty et al. 2015).

Here, it is important to consider the fact that general deduction is not allowed for cost of planting

trees when the individual purpose is participating in carbon sequestration activities as well as

those trees as it is not intended to be felled in a business of forestry. In addition, it is because of

the cost for planting in these conditions and is known as capital expenditure. Capital expenditure

for planting trees can be perceived as other income tax treatment that majorly depends upon the

context in which expenditure is incurred when the trees are treated as horticultural plants

(Coleman and Sadiq 2013). The trees that are used for sale of products or parts and the cost for

establishment are mainly written off after referring to the effective life of the plant. Hence, trees

that are used solely for carbon credit arrangements are mainly not cultivated for any of the

products or parts as it does not constitute horticultural pants for the purpose of applying the

horticultural plant deduction as shown in the section (Taylor and Richardson 2013).

As per the case, the concerned sale combines either completely or partial assets of the

business (Ross, Walker and Walker 2017). In that case, McCauley v The Federal Commissioner

of Taxation payments mainly obtains from the grantor under the right of performing the

operations in correct way. From the given case study, it is noted that Bill is treated as a basic

producer because he gets engaged into the process of primary production in accordance to

subsection 6 (1) of the Income Tax Assessment Act 1936 (Coleman and Sadiq 2013). To that, the

forest operations take into account felling of trees in a forest or plantation where the taxpayers

show no interest about the planted trees. In that case, McCauley v The Federal Commissioner of

Taxation payments mainly obtains from the grantor under the right of performing the operations

in correct way (Woellner et al. 2014).

AUSTRALIAN TAXATION LAW

on in conjunction and aligns according to forestry activities or operations (Petty et al. 2015).

Here, it is important to consider the fact that general deduction is not allowed for cost of planting

trees when the individual purpose is participating in carbon sequestration activities as well as

those trees as it is not intended to be felled in a business of forestry. In addition, it is because of

the cost for planting in these conditions and is known as capital expenditure. Capital expenditure

for planting trees can be perceived as other income tax treatment that majorly depends upon the

context in which expenditure is incurred when the trees are treated as horticultural plants

(Coleman and Sadiq 2013). The trees that are used for sale of products or parts and the cost for

establishment are mainly written off after referring to the effective life of the plant. Hence, trees

that are used solely for carbon credit arrangements are mainly not cultivated for any of the

products or parts as it does not constitute horticultural pants for the purpose of applying the

horticultural plant deduction as shown in the section (Taylor and Richardson 2013).

As per the case, the concerned sale combines either completely or partial assets of the

business (Ross, Walker and Walker 2017). In that case, McCauley v The Federal Commissioner

of Taxation payments mainly obtains from the grantor under the right of performing the

operations in correct way. From the given case study, it is noted that Bill is treated as a basic

producer because he gets engaged into the process of primary production in accordance to

subsection 6 (1) of the Income Tax Assessment Act 1936 (Coleman and Sadiq 2013). To that, the

forest operations take into account felling of trees in a forest or plantation where the taxpayers

show no interest about the planted trees. In that case, McCauley v The Federal Commissioner of

Taxation payments mainly obtains from the grantor under the right of performing the operations

in correct way (Woellner et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

AUSTRALIAN TAXATION LAW

It is concluded that the outcomes from the cases shows that first case is received from the

amount of Bill that will be taxable under income tax. As far as second case is concerned, the

amount of Bill received by him will be treated as royalty.

AUSTRALIAN TAXATION LAW

It is concluded that the outcomes from the cases shows that first case is received from the

amount of Bill that will be taxable under income tax. As far as second case is concerned, the

amount of Bill received by him will be treated as royalty.

12

AUSTRALIAN TAXATION LAW

References and Bibliography

Australian Taxation Law Cases 2014. 2014. Pyrmont, NSW: Thomson Reuters.

Coleman, C. and Sadiq, K. 2013. Principles of taxation law 2013.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Douglas, H., Bartlett, F., Luker, T. and Hunter, R. eds., 2014. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. 2014 principles of business taxation.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Krever, R. 2015. Australian taxation law cases 2015.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Novikov, A.A., Ling, T.G. and Kordzakhia, N., 2014. Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp. 461-474).

Springer International Publishing.

AUSTRALIAN TAXATION LAW

References and Bibliography

Australian Taxation Law Cases 2014. 2014. Pyrmont, NSW: Thomson Reuters.

Coleman, C. and Sadiq, K. 2013. Principles of taxation law 2013.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), pp.47-68.

Douglas, H., Bartlett, F., Luker, T. and Hunter, R. eds., 2014. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. 2014 principles of business taxation.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Krever, R. 2015. Australian taxation law cases 2015.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Novikov, A.A., Ling, T.G. and Kordzakhia, N., 2014. Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp. 461-474).

Springer International Publishing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.