Australian Taxation Law

Added on 2022-11-25

30 Pages5219 Words396 Views

Australian Taxation Law

TABLE OF CONTENTS

QUESTION ONE.......................................................................................................................4

QUESTION TWO......................................................................................................................4

QUESTION THREE..................................................................................................................5

QUESTION ONE.......................................................................................................................6

QUESTION TWO......................................................................................................................7

QUESTION THREE..................................................................................................................8

SECTION A.............................................................................................................................10

QUESTION 1...........................................................................................................................10

QUIESTION 2.........................................................................................................................10

Part A..................................................................................................................................10

Part B...................................................................................................................................12

QUESTION 3...........................................................................................................................13

a)..........................................................................................................................................13

b)..........................................................................................................................................14

QUESTION 4...........................................................................................................................15

Part A..................................................................................................................................15

Part B...................................................................................................................................16

QUESTION ONE.....................................................................................................................18

QUESTION TWO....................................................................................................................19

QUESTION THREE................................................................................................................20

QUESTION ONE.....................................................................................................................21

QUESTION TWO....................................................................................................................22

QUESTION THREE................................................................................................................24

QUESTION ONE.....................................................................................................................25

QUESTION TWO....................................................................................................................26

QUESTION THREE................................................................................................................27

QUESTION ONE.......................................................................................................................4

QUESTION TWO......................................................................................................................4

QUESTION THREE..................................................................................................................5

QUESTION ONE.......................................................................................................................6

QUESTION TWO......................................................................................................................7

QUESTION THREE..................................................................................................................8

SECTION A.............................................................................................................................10

QUESTION 1...........................................................................................................................10

QUIESTION 2.........................................................................................................................10

Part A..................................................................................................................................10

Part B...................................................................................................................................12

QUESTION 3...........................................................................................................................13

a)..........................................................................................................................................13

b)..........................................................................................................................................14

QUESTION 4...........................................................................................................................15

Part A..................................................................................................................................15

Part B...................................................................................................................................16

QUESTION ONE.....................................................................................................................18

QUESTION TWO....................................................................................................................19

QUESTION THREE................................................................................................................20

QUESTION ONE.....................................................................................................................21

QUESTION TWO....................................................................................................................22

QUESTION THREE................................................................................................................24

QUESTION ONE.....................................................................................................................25

QUESTION TWO....................................................................................................................26

QUESTION THREE................................................................................................................27

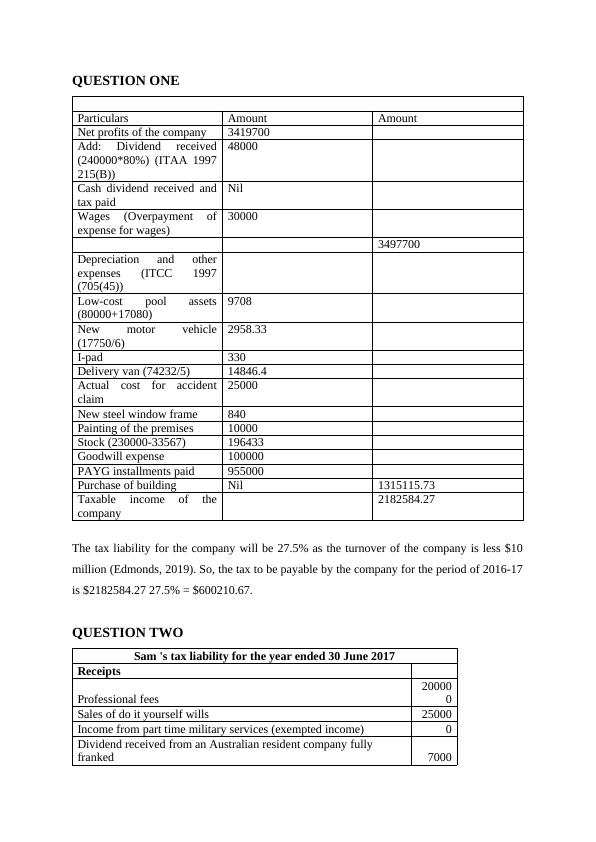

QUESTION ONE

Particulars Amount Amount

Net profits of the company 3419700

Add: Dividend received

(240000*80%) (ITAA 1997

215(B))

48000

Cash dividend received and

tax paid

Nil

Wages (Overpayment of

expense for wages)

30000

3497700

Depreciation and other

expenses (ITCC 1997

(705(45))

Low-cost pool assets

(80000+17080)

9708

New motor vehicle

(17750/6)

2958.33

I-pad 330

Delivery van (74232/5) 14846.4

Actual cost for accident

claim

25000

New steel window frame 840

Painting of the premises 10000

Stock (230000-33567) 196433

Goodwill expense 100000

PAYG installments paid 955000

Purchase of building Nil 1315115.73

Taxable income of the

company

2182584.27

The tax liability for the company will be 27.5% as the turnover of the company is less $10

million (Edmonds, 2019). So, the tax to be payable by the company for the period of 2016-17

is $2182584.27 27.5% = $600210.67.

QUESTION TWO

Sam 's tax liability for the year ended 30 June 2017

Receipts

Professional fees

20000

0

Sales of do it yourself wills 25000

Income from part time military services (exempted income) 0

Dividend received from an Australian resident company fully

franked 7000

Particulars Amount Amount

Net profits of the company 3419700

Add: Dividend received

(240000*80%) (ITAA 1997

215(B))

48000

Cash dividend received and

tax paid

Nil

Wages (Overpayment of

expense for wages)

30000

3497700

Depreciation and other

expenses (ITCC 1997

(705(45))

Low-cost pool assets

(80000+17080)

9708

New motor vehicle

(17750/6)

2958.33

I-pad 330

Delivery van (74232/5) 14846.4

Actual cost for accident

claim

25000

New steel window frame 840

Painting of the premises 10000

Stock (230000-33567) 196433

Goodwill expense 100000

PAYG installments paid 955000

Purchase of building Nil 1315115.73

Taxable income of the

company

2182584.27

The tax liability for the company will be 27.5% as the turnover of the company is less $10

million (Edmonds, 2019). So, the tax to be payable by the company for the period of 2016-17

is $2182584.27 27.5% = $600210.67.

QUESTION TWO

Sam 's tax liability for the year ended 30 June 2017

Receipts

Professional fees

20000

0

Sales of do it yourself wills 25000

Income from part time military services (exempted income) 0

Dividend received from an Australian resident company fully

franked 7000

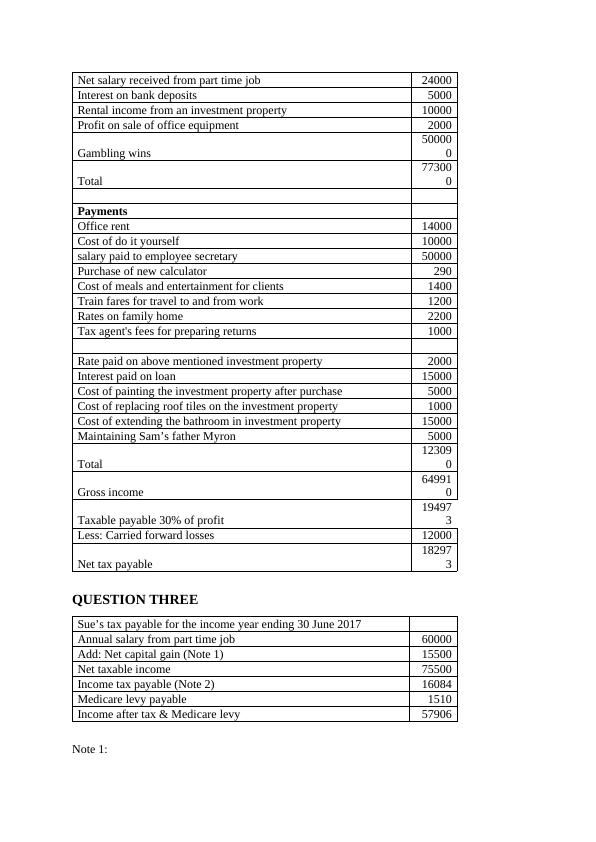

Net salary received from part time job 24000

Interest on bank deposits 5000

Rental income from an investment property 10000

Profit on sale of office equipment 2000

Gambling wins

50000

0

Total

77300

0

Payments

Office rent 14000

Cost of do it yourself 10000

salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 1400

Train fares for travel to and from work 1200

Rates on family home 2200

Tax agent's fees for preparing returns 1000

Rate paid on above mentioned investment property 2000

Interest paid on loan 15000

Cost of painting the investment property after purchase 5000

Cost of replacing roof tiles on the investment property 1000

Cost of extending the bathroom in investment property 15000

Maintaining Sam’s father Myron 5000

Total

12309

0

Gross income

64991

0

Taxable payable 30% of profit

19497

3

Less: Carried forward losses 12000

Net tax payable

18297

3

QUESTION THREE

Sue’s tax payable for the income year ending 30 June 2017

Annual salary from part time job 60000

Add: Net capital gain (Note 1) 15500

Net taxable income 75500

Income tax payable (Note 2) 16084

Medicare levy payable 1510

Income after tax & Medicare levy 57906

Note 1:

Interest on bank deposits 5000

Rental income from an investment property 10000

Profit on sale of office equipment 2000

Gambling wins

50000

0

Total

77300

0

Payments

Office rent 14000

Cost of do it yourself 10000

salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 1400

Train fares for travel to and from work 1200

Rates on family home 2200

Tax agent's fees for preparing returns 1000

Rate paid on above mentioned investment property 2000

Interest paid on loan 15000

Cost of painting the investment property after purchase 5000

Cost of replacing roof tiles on the investment property 1000

Cost of extending the bathroom in investment property 15000

Maintaining Sam’s father Myron 5000

Total

12309

0

Gross income

64991

0

Taxable payable 30% of profit

19497

3

Less: Carried forward losses 12000

Net tax payable

18297

3

QUESTION THREE

Sue’s tax payable for the income year ending 30 June 2017

Annual salary from part time job 60000

Add: Net capital gain (Note 1) 15500

Net taxable income 75500

Income tax payable (Note 2) 16084

Medicare levy payable 1510

Income after tax & Medicare levy 57906

Note 1:

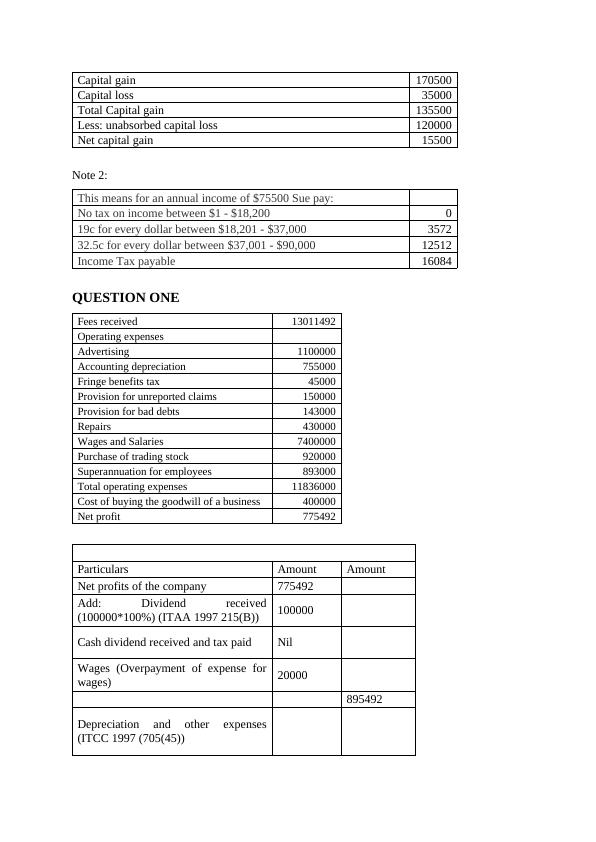

Capital gain 170500

Capital loss 35000

Total Capital gain 135500

Less: unabsorbed capital loss 120000

Net capital gain 15500

Note 2:

This means for an annual income of $75500 Sue pay:

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 - $90,000 12512

Income Tax payable 16084

QUESTION ONE

Fees received 13011492

Operating expenses

Advertising 1100000

Accounting depreciation 755000

Fringe benefits tax 45000

Provision for unreported claims 150000

Provision for bad debts 143000

Repairs 430000

Wages and Salaries 7400000

Purchase of trading stock 920000

Superannuation for employees 893000

Total operating expenses 11836000

Cost of buying the goodwill of a business 400000

Net profit 775492

Particulars Amount Amount

Net profits of the company 775492

Add: Dividend received

(100000*100%) (ITAA 1997 215(B)) 100000

Cash dividend received and tax paid Nil

Wages (Overpayment of expense for

wages) 20000

895492

Depreciation and other expenses

(ITCC 1997 (705(45))

Capital loss 35000

Total Capital gain 135500

Less: unabsorbed capital loss 120000

Net capital gain 15500

Note 2:

This means for an annual income of $75500 Sue pay:

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 - $90,000 12512

Income Tax payable 16084

QUESTION ONE

Fees received 13011492

Operating expenses

Advertising 1100000

Accounting depreciation 755000

Fringe benefits tax 45000

Provision for unreported claims 150000

Provision for bad debts 143000

Repairs 430000

Wages and Salaries 7400000

Purchase of trading stock 920000

Superannuation for employees 893000

Total operating expenses 11836000

Cost of buying the goodwill of a business 400000

Net profit 775492

Particulars Amount Amount

Net profits of the company 775492

Add: Dividend received

(100000*100%) (ITAA 1997 215(B)) 100000

Cash dividend received and tax paid Nil

Wages (Overpayment of expense for

wages) 20000

895492

Depreciation and other expenses

(ITCC 1997 (705(45))

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation Law Exam: Practice Questions and Solutionslg...

|8

|1128

|394

Taxation Law - Assignment PDFlg...

|10

|1477

|25

TAX305 Taxation Assignmentlg...

|9

|1590

|73

projected profit and loss, projected balance sheet, projected cash flowlg...

|6

|384

|1

TAXATION LAW. TAXATION LAW. TAXATION LAW. 4. 4. Taxatiolg...

|6

|489

|47

ACC3TAX Taxation Group Assignmentlg...

|9

|1991

|44