B124 EMA: Preparing Financial Statements for Ayla King - December 2020

VerifiedAdded on 2023/05/03

|10

|2634

|364

Homework Assignment

AI Summary

This assignment solution includes the preparation of an income statement and balance sheet for Ayla King as of December 31, 2020, along with detailed workings for calculations like depreciation, receivables allowance, and various expenses. It also covers key accounting concepts such as comparability, understandability, adaptability, and time management in accounting, illustrating their importance with practical examples. Further, the assignment delves into cash budgeting, semi-variable costs, the controllability principle in responsibility accounting, and limitations of budgeting. Finally, it addresses cost accounting calculations, opportunity cost analysis, and factory production cost considerations, providing a comprehensive overview of essential accounting principles and practices. Desklib provides similar solved assignments and resources for students.

Module: B124 EMA

Tutor:

Name:

PI:

Due Date:

Tutor:

Name:

PI:

Due Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

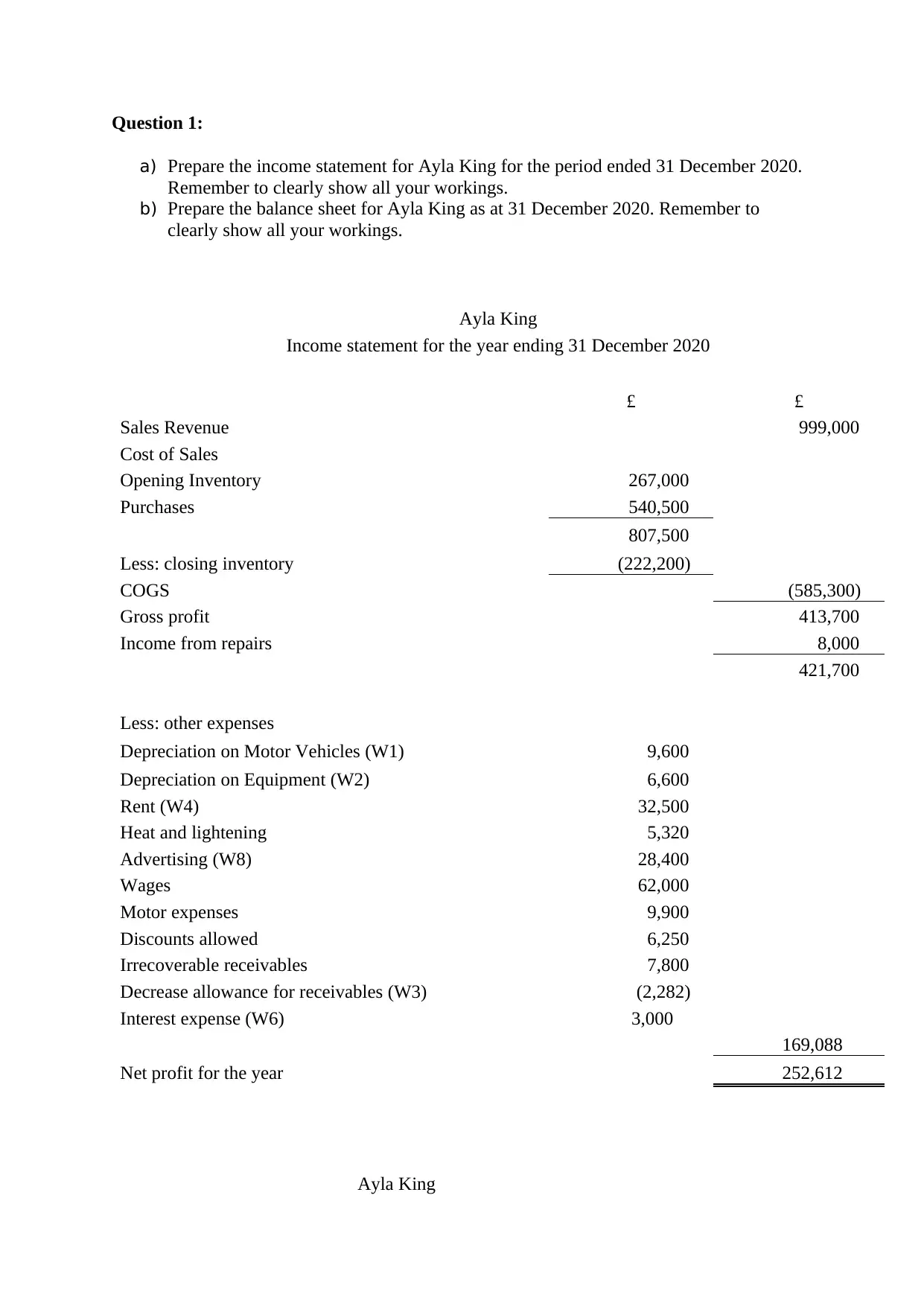

Question 1:

a) Prepare the income statement for Ayla King for the period ended 31 December 2020.

Remember to clearly show all your workings.

b) Prepare the balance sheet for Ayla King as at 31 December 2020. Remember to

clearly show all your workings.

Ayla King

Income statement for the year ending 31 December 2020

£ £

Sales Revenue 999,000

Cost of Sales

Opening Inventory 267,000

Purchases 540,500

807,500

Less: closing inventory (222,200)

COGS (585,300)

Gross profit 413,700

Income from repairs 8,000

421,700

Less: other expenses

Depreciation on Motor Vehicles (W1) 9,600

Depreciation on Equipment (W2) 6,600

Rent (W4) 32,500

Heat and lightening 5,320

Advertising (W8) 28,400

Wages 62,000

Motor expenses 9,900

Discounts allowed 6,250

Irrecoverable receivables 7,800

Decrease allowance for receivables (W3) (2,282)

Interest expense (W6) 3,000

169,088

Net profit for the year 252,612

Ayla King

a) Prepare the income statement for Ayla King for the period ended 31 December 2020.

Remember to clearly show all your workings.

b) Prepare the balance sheet for Ayla King as at 31 December 2020. Remember to

clearly show all your workings.

Ayla King

Income statement for the year ending 31 December 2020

£ £

Sales Revenue 999,000

Cost of Sales

Opening Inventory 267,000

Purchases 540,500

807,500

Less: closing inventory (222,200)

COGS (585,300)

Gross profit 413,700

Income from repairs 8,000

421,700

Less: other expenses

Depreciation on Motor Vehicles (W1) 9,600

Depreciation on Equipment (W2) 6,600

Rent (W4) 32,500

Heat and lightening 5,320

Advertising (W8) 28,400

Wages 62,000

Motor expenses 9,900

Discounts allowed 6,250

Irrecoverable receivables 7,800

Decrease allowance for receivables (W3) (2,282)

Interest expense (W6) 3,000

169,088

Net profit for the year 252,612

Ayla King

Balance sheet as 31 December 2020

Assets £ £ £

Non-current Cost Acc depn NBV

Motor Vehicle 60,000 21,600 38,400

Equipment 66,000 19,800 46,200

126,000 41,400 84,600

Current Assets:

Inventory 222,200

Prepayments 7,000

Receivables 89,232

Bank 44,000

Total current assets 362,432

Total assets 447,032

Capital and Liabilities

Capital

Opening Capital 80,000

Profit for year 252,612

332,612

Less: Drawings 50,000

Total capital 282,612

Liabilities:

Non-current:

Bank Loan 50,000

Current Liabilities:

VAT liability 23,000

Payables 87,500

Accruals 3,920

114,420

Total liabilities 164,420

Closing capital and liabilities 447,032

Workings:

W1) (60,000 – 12,000) x 20% = £ 9,600

W2) (66000 x 10%) = £ 6,600

W3) Receivables as per TB 100,750

Less: Irrecoverable receivables (7,800)

Net receivables 92,950

Less: allowance for receivables to be (4%) 89,232

Assets £ £ £

Non-current Cost Acc depn NBV

Motor Vehicle 60,000 21,600 38,400

Equipment 66,000 19,800 46,200

126,000 41,400 84,600

Current Assets:

Inventory 222,200

Prepayments 7,000

Receivables 89,232

Bank 44,000

Total current assets 362,432

Total assets 447,032

Capital and Liabilities

Capital

Opening Capital 80,000

Profit for year 252,612

332,612

Less: Drawings 50,000

Total capital 282,612

Liabilities:

Non-current:

Bank Loan 50,000

Current Liabilities:

VAT liability 23,000

Payables 87,500

Accruals 3,920

114,420

Total liabilities 164,420

Closing capital and liabilities 447,032

Workings:

W1) (60,000 – 12,000) x 20% = £ 9,600

W2) (66000 x 10%) = £ 6,600

W3) Receivables as per TB 100,750

Less: Irrecoverable receivables (7,800)

Net receivables 92,950

Less: allowance for receivables to be (4%) 89,232

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Allowance for receivables to be 3,718

Less: allowance for receivables as per TB (6,000)

Decrease in allowance 2,282

W4) Rent 35,500 – 3,000 = 32,500

W5) Heat and lighting 4,400 + 920 = 5,320

W6) 6% x 50,000= 3,000

W7) Prepayments: Rent 3000 + 4000 advertising

W8) Advertising expenses 8,000 TB - 4,000 prepayment

32,400 – 4,000 = 28,400

Question 2

a) Explain, by means of appropriate examples, the following two characteristics of good

quality accounting information:

(i) Comparability

Information within financial statements should be appropriate for comparison

between different accounting periods and be able to analyse financial

performance and entity’s position over time by the use of similar accounting

practices / policies. For example, if a company selling fans uses the LIFO*

method a switch to FIFO* would result in a change of inventory valuation,

hence the importance of consistency.

*Last in first out (LIFO) and First in First Out (FIFO) relates to inventory

valuation methods.

(ii) Understandability

Information displayed should be clearly presented and understandable

otherwise, if information is complex displayed for users, it would undermine

the reliability of its statements. For example, ENRON Corporation ended

dissolved after one of the biggest scandals, contained complex financial

statements that were not understandable and clear, which lead to the

overvaluation by markets and finally its collapse.

b)

(i) Explain any two of the seven general skills and abilities of effective

accountants that are covered in Unit 1.

Adaptability is an essential skill for accounting. Other than proving the

resourcefulness of an individual or company, it is important to comply and

adapt to constant changes set by markets and legislators. Meanwhile, time

management, the ability to multitask while effectively plan ahead to meet

deadlines individual and collectively while delivering high standards, is

essential since many projects can be happening at the same time.

Less: allowance for receivables as per TB (6,000)

Decrease in allowance 2,282

W4) Rent 35,500 – 3,000 = 32,500

W5) Heat and lighting 4,400 + 920 = 5,320

W6) 6% x 50,000= 3,000

W7) Prepayments: Rent 3000 + 4000 advertising

W8) Advertising expenses 8,000 TB - 4,000 prepayment

32,400 – 4,000 = 28,400

Question 2

a) Explain, by means of appropriate examples, the following two characteristics of good

quality accounting information:

(i) Comparability

Information within financial statements should be appropriate for comparison

between different accounting periods and be able to analyse financial

performance and entity’s position over time by the use of similar accounting

practices / policies. For example, if a company selling fans uses the LIFO*

method a switch to FIFO* would result in a change of inventory valuation,

hence the importance of consistency.

*Last in first out (LIFO) and First in First Out (FIFO) relates to inventory

valuation methods.

(ii) Understandability

Information displayed should be clearly presented and understandable

otherwise, if information is complex displayed for users, it would undermine

the reliability of its statements. For example, ENRON Corporation ended

dissolved after one of the biggest scandals, contained complex financial

statements that were not understandable and clear, which lead to the

overvaluation by markets and finally its collapse.

b)

(i) Explain any two of the seven general skills and abilities of effective

accountants that are covered in Unit 1.

Adaptability is an essential skill for accounting. Other than proving the

resourcefulness of an individual or company, it is important to comply and

adapt to constant changes set by markets and legislators. Meanwhile, time

management, the ability to multitask while effectively plan ahead to meet

deadlines individual and collectively while delivering high standards, is

essential since many projects can be happening at the same time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

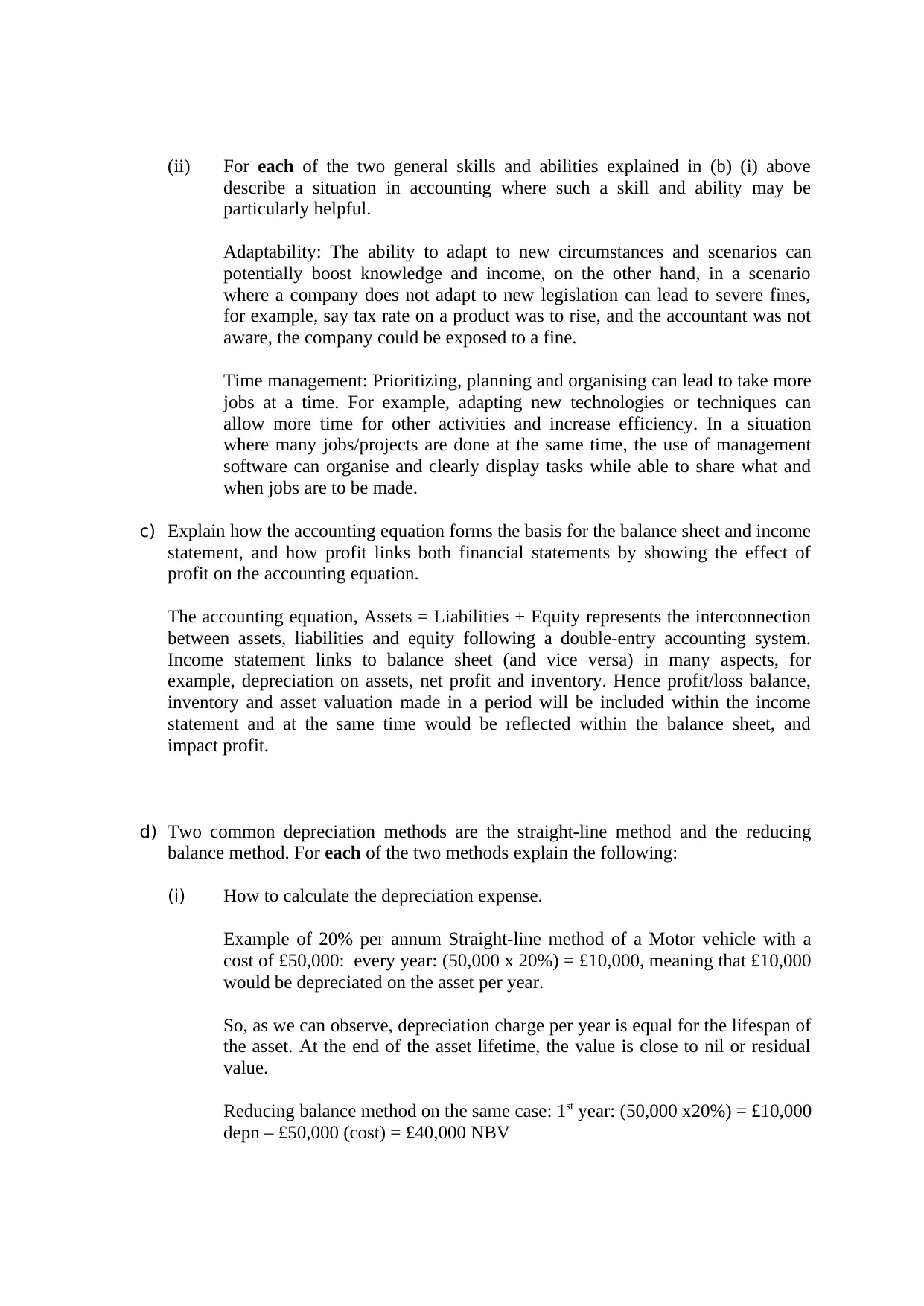

(ii) For each of the two general skills and abilities explained in (b) (i) above

describe a situation in accounting where such a skill and ability may be

particularly helpful.

Adaptability: The ability to adapt to new circumstances and scenarios can

potentially boost knowledge and income, on the other hand, in a scenario

where a company does not adapt to new legislation can lead to severe fines,

for example, say tax rate on a product was to rise, and the accountant was not

aware, the company could be exposed to a fine.

Time management: Prioritizing, planning and organising can lead to take more

jobs at a time. For example, adapting new technologies or techniques can

allow more time for other activities and increase efficiency. In a situation

where many jobs/projects are done at the same time, the use of management

software can organise and clearly display tasks while able to share what and

when jobs are to be made.

c) Explain how the accounting equation forms the basis for the balance sheet and income

statement, and how profit links both financial statements by showing the effect of

profit on the accounting equation.

The accounting equation, Assets = Liabilities + Equity represents the interconnection

between assets, liabilities and equity following a double-entry accounting system.

Income statement links to balance sheet (and vice versa) in many aspects, for

example, depreciation on assets, net profit and inventory. Hence profit/loss balance,

inventory and asset valuation made in a period will be included within the income

statement and at the same time would be reflected within the balance sheet, and

impact profit.

d) Two common depreciation methods are the straight-line method and the reducing

balance method. For each of the two methods explain the following:

(i) How to calculate the depreciation expense.

Example of 20% per annum Straight-line method of a Motor vehicle with a

cost of £50,000: every year: (50,000 x 20%) = £10,000, meaning that £10,000

would be depreciated on the asset per year.

So, as we can observe, depreciation charge per year is equal for the lifespan of

the asset. At the end of the asset lifetime, the value is close to nil or residual

value.

Reducing balance method on the same case: 1st year: (50,000 x20%) = £10,000

depn – £50,000 (cost) = £40,000 NBV

describe a situation in accounting where such a skill and ability may be

particularly helpful.

Adaptability: The ability to adapt to new circumstances and scenarios can

potentially boost knowledge and income, on the other hand, in a scenario

where a company does not adapt to new legislation can lead to severe fines,

for example, say tax rate on a product was to rise, and the accountant was not

aware, the company could be exposed to a fine.

Time management: Prioritizing, planning and organising can lead to take more

jobs at a time. For example, adapting new technologies or techniques can

allow more time for other activities and increase efficiency. In a situation

where many jobs/projects are done at the same time, the use of management

software can organise and clearly display tasks while able to share what and

when jobs are to be made.

c) Explain how the accounting equation forms the basis for the balance sheet and income

statement, and how profit links both financial statements by showing the effect of

profit on the accounting equation.

The accounting equation, Assets = Liabilities + Equity represents the interconnection

between assets, liabilities and equity following a double-entry accounting system.

Income statement links to balance sheet (and vice versa) in many aspects, for

example, depreciation on assets, net profit and inventory. Hence profit/loss balance,

inventory and asset valuation made in a period will be included within the income

statement and at the same time would be reflected within the balance sheet, and

impact profit.

d) Two common depreciation methods are the straight-line method and the reducing

balance method. For each of the two methods explain the following:

(i) How to calculate the depreciation expense.

Example of 20% per annum Straight-line method of a Motor vehicle with a

cost of £50,000: every year: (50,000 x 20%) = £10,000, meaning that £10,000

would be depreciated on the asset per year.

So, as we can observe, depreciation charge per year is equal for the lifespan of

the asset. At the end of the asset lifetime, the value is close to nil or residual

value.

Reducing balance method on the same case: 1st year: (50,000 x20%) = £10,000

depn – £50,000 (cost) = £40,000 NBV

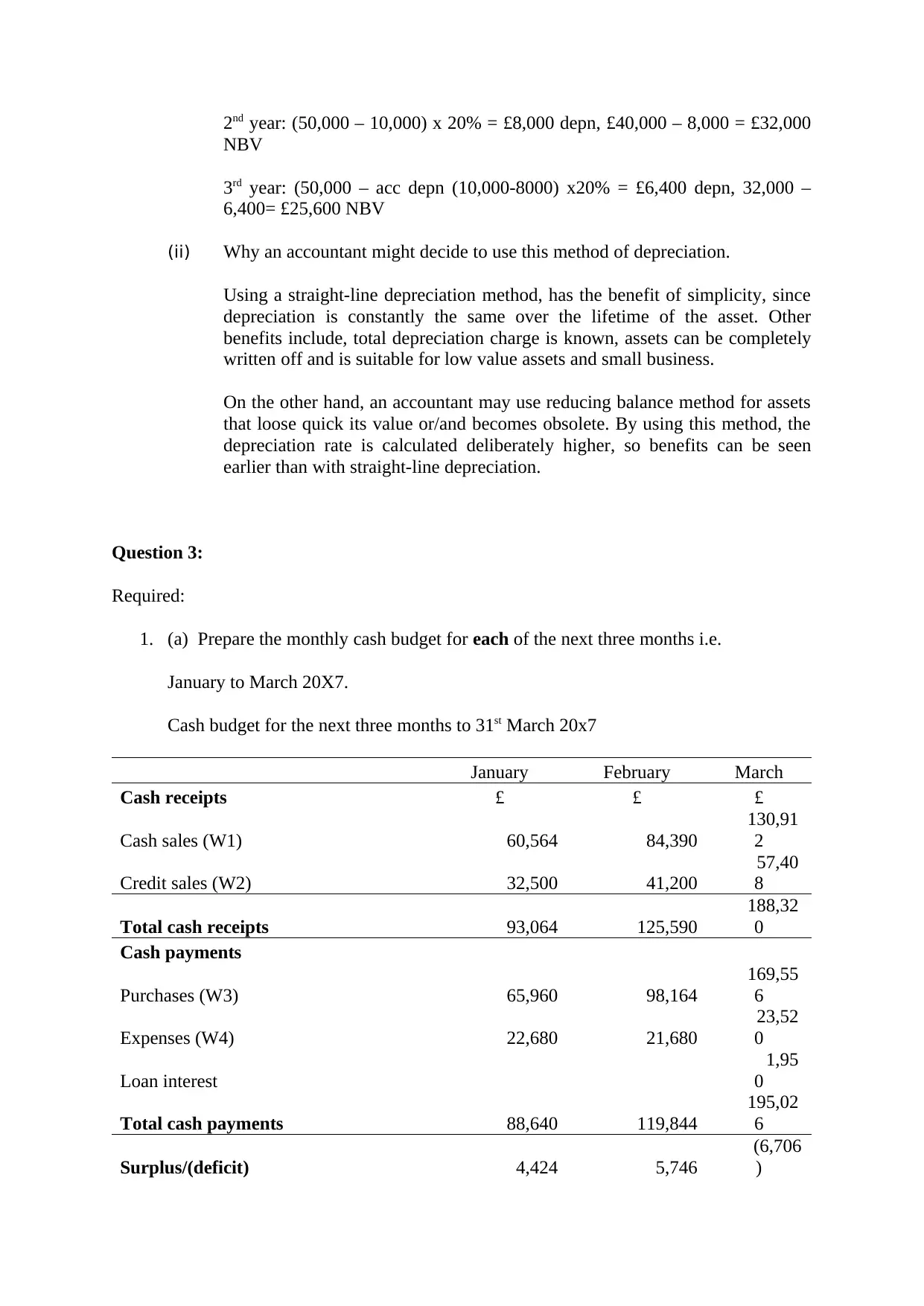

2nd year: (50,000 – 10,000) x 20% = £8,000 depn, £40,000 – 8,000 = £32,000

NBV

3rd year: (50,000 – acc depn (10,000-8000) x20% = £6,400 depn, 32,000 –

6,400= £25,600 NBV

(ii) Why an accountant might decide to use this method of depreciation.

Using a straight-line depreciation method, has the benefit of simplicity, since

depreciation is constantly the same over the lifetime of the asset. Other

benefits include, total depreciation charge is known, assets can be completely

written off and is suitable for low value assets and small business.

On the other hand, an accountant may use reducing balance method for assets

that loose quick its value or/and becomes obsolete. By using this method, the

depreciation rate is calculated deliberately higher, so benefits can be seen

earlier than with straight-line depreciation.

Question 3:

Required:

1. (a) Prepare the monthly cash budget for each of the next three months i.e.

January to March 20X7.

Cash budget for the next three months to 31st March 20x7

January February March

Cash receipts £ £ £

Cash sales (W1) 60,564 84,390

130,91

2

Credit sales (W2) 32,500 41,200

57,40

8

Total cash receipts 93,064 125,590

188,32

0

Cash payments

Purchases (W3) 65,960 98,164

169,55

6

Expenses (W4) 22,680 21,680

23,52

0

Loan interest

1,95

0

Total cash payments 88,640 119,844

195,02

6

Surplus/(deficit) 4,424 5,746

(6,706

)

NBV

3rd year: (50,000 – acc depn (10,000-8000) x20% = £6,400 depn, 32,000 –

6,400= £25,600 NBV

(ii) Why an accountant might decide to use this method of depreciation.

Using a straight-line depreciation method, has the benefit of simplicity, since

depreciation is constantly the same over the lifetime of the asset. Other

benefits include, total depreciation charge is known, assets can be completely

written off and is suitable for low value assets and small business.

On the other hand, an accountant may use reducing balance method for assets

that loose quick its value or/and becomes obsolete. By using this method, the

depreciation rate is calculated deliberately higher, so benefits can be seen

earlier than with straight-line depreciation.

Question 3:

Required:

1. (a) Prepare the monthly cash budget for each of the next three months i.e.

January to March 20X7.

Cash budget for the next three months to 31st March 20x7

January February March

Cash receipts £ £ £

Cash sales (W1) 60,564 84,390

130,91

2

Credit sales (W2) 32,500 41,200

57,40

8

Total cash receipts 93,064 125,590

188,32

0

Cash payments

Purchases (W3) 65,960 98,164

169,55

6

Expenses (W4) 22,680 21,680

23,52

0

Loan interest

1,95

0

Total cash payments 88,640 119,844

195,02

6

Surplus/(deficit) 4,424 5,746

(6,706

)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balance b/f 16,800 21,224

26,97

0

Balance c/f 21,224 26,970

20,26

4

Working 1: January cash sales (103,000 x 60%) = 61,800 - 2%= £60,564. Cash sales

for all other months are calculated the same way.

Working 2: January credit sales shown are receivables from balance sheet, 32,500

(December sales). January credit sales, which will be received on February is

calculated as: (103,000 x 40%) = 41,200. The credit sales for all other months are

calculated the same way.

Working 3: Purchases for January are 68,000 x 4% = 65,960. Cash purchases for all

other months are calculated the same way.

Working 4: Expenses for January are 24,000 – 1,320 = 22,680. Expenses for all other

months are calculated the same way.

(b) By means of an appropriate example, explain what is meant by a semi-

variable cost.

Semi-variable costs are expenses that have a mix of fixed and variable costs. For

example, electricity usage is a fixed cost, however, the cost is variable (in most cases)

since the usage of electricity will vary day-to-day, week-to-week, month to month…

2. (c) (i) Explain what is meant by the controllability principle in the context of

responsibility accounting.

Controllability principle relates to the responsibility implied by the accountant, where

it should be responsible only for items that (he/she) can control. For example, an

accountant may be responsible for the financial statement reports, on the other hand,

if the company does not make profit as expected due to unforeseen circumstances i.e.,

competitors having a competitive price or better product, it should not be the

accountant’s responsibility.

(iii) Why is the controllability principle difficult to apply in practice?

However, defining boundaries to held responsible is hard in most cases. Many

cases, results depend on multiple internal and external uncontrollable factors,

individuals and other business interacting as well as unexpected events is a

challenge that can delay tasks and so delivery dates. For example, if a motor

vehicle needs to be sold after 3 years, and that particular model of vehicle has

devaluated at a faster pace than expected, may be because of recalls or just

because a change of taste in the market or new technologies, it is not the

accountant responsibility and it should not be accountable for it.

26,97

0

Balance c/f 21,224 26,970

20,26

4

Working 1: January cash sales (103,000 x 60%) = 61,800 - 2%= £60,564. Cash sales

for all other months are calculated the same way.

Working 2: January credit sales shown are receivables from balance sheet, 32,500

(December sales). January credit sales, which will be received on February is

calculated as: (103,000 x 40%) = 41,200. The credit sales for all other months are

calculated the same way.

Working 3: Purchases for January are 68,000 x 4% = 65,960. Cash purchases for all

other months are calculated the same way.

Working 4: Expenses for January are 24,000 – 1,320 = 22,680. Expenses for all other

months are calculated the same way.

(b) By means of an appropriate example, explain what is meant by a semi-

variable cost.

Semi-variable costs are expenses that have a mix of fixed and variable costs. For

example, electricity usage is a fixed cost, however, the cost is variable (in most cases)

since the usage of electricity will vary day-to-day, week-to-week, month to month…

2. (c) (i) Explain what is meant by the controllability principle in the context of

responsibility accounting.

Controllability principle relates to the responsibility implied by the accountant, where

it should be responsible only for items that (he/she) can control. For example, an

accountant may be responsible for the financial statement reports, on the other hand,

if the company does not make profit as expected due to unforeseen circumstances i.e.,

competitors having a competitive price or better product, it should not be the

accountant’s responsibility.

(iii) Why is the controllability principle difficult to apply in practice?

However, defining boundaries to held responsible is hard in most cases. Many

cases, results depend on multiple internal and external uncontrollable factors,

individuals and other business interacting as well as unexpected events is a

challenge that can delay tasks and so delivery dates. For example, if a motor

vehicle needs to be sold after 3 years, and that particular model of vehicle has

devaluated at a faster pace than expected, may be because of recalls or just

because a change of taste in the market or new technologies, it is not the

accountant responsibility and it should not be accountable for it.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

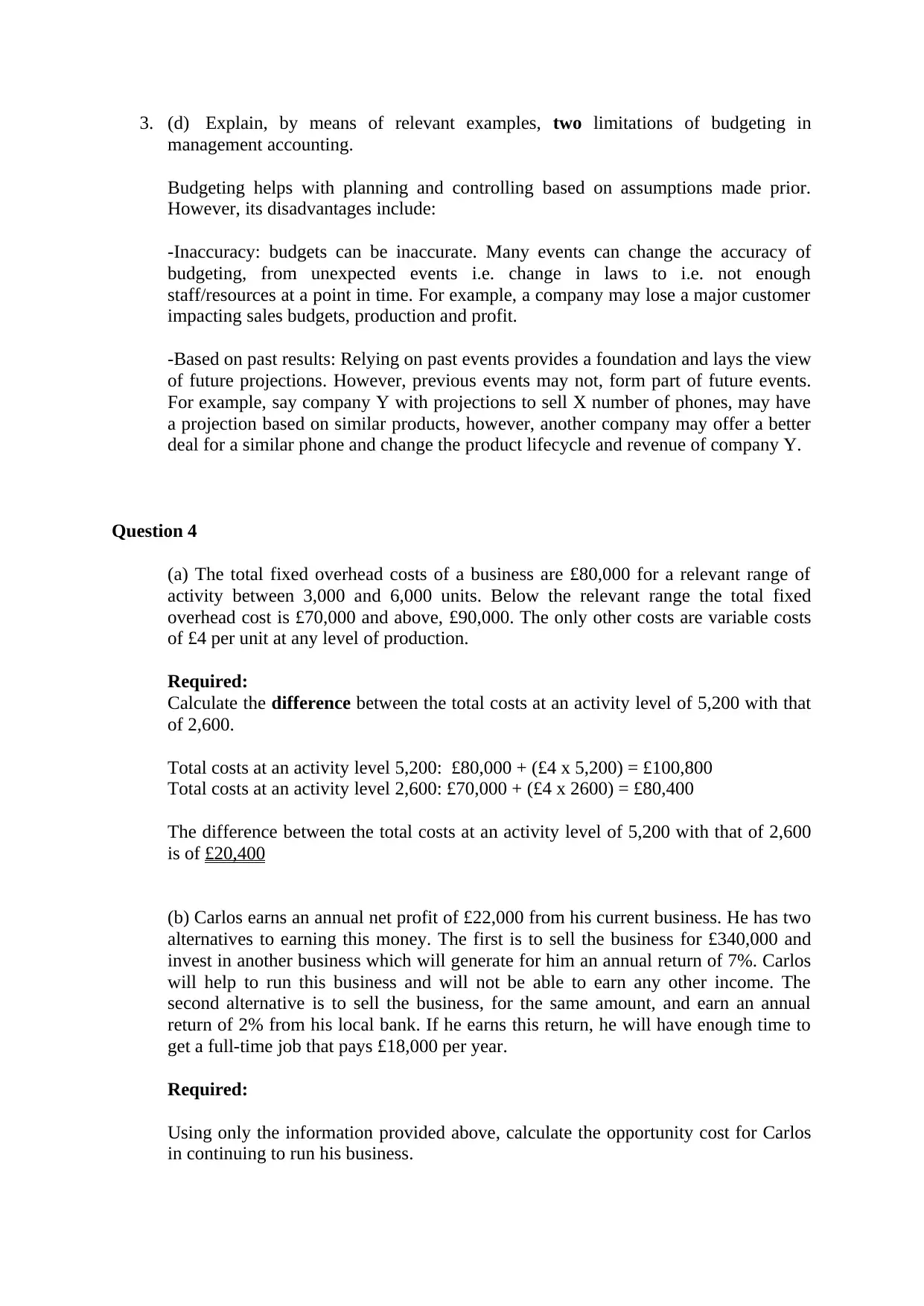

3. (d) Explain, by means of relevant examples, two limitations of budgeting in

management accounting.

Budgeting helps with planning and controlling based on assumptions made prior.

However, its disadvantages include:

-Inaccuracy: budgets can be inaccurate. Many events can change the accuracy of

budgeting, from unexpected events i.e. change in laws to i.e. not enough

staff/resources at a point in time. For example, a company may lose a major customer

impacting sales budgets, production and profit.

-Based on past results: Relying on past events provides a foundation and lays the view

of future projections. However, previous events may not, form part of future events.

For example, say company Y with projections to sell X number of phones, may have

a projection based on similar products, however, another company may offer a better

deal for a similar phone and change the product lifecycle and revenue of company Y.

Question 4

(a) The total fixed overhead costs of a business are £80,000 for a relevant range of

activity between 3,000 and 6,000 units. Below the relevant range the total fixed

overhead cost is £70,000 and above, £90,000. The only other costs are variable costs

of £4 per unit at any level of production.

Required:

Calculate the difference between the total costs at an activity level of 5,200 with that

of 2,600.

Total costs at an activity level 5,200: £80,000 + (£4 x 5,200) = £100,800

Total costs at an activity level 2,600: £70,000 + (£4 x 2600) = £80,400

The difference between the total costs at an activity level of 5,200 with that of 2,600

is of £20,400

(b) Carlos earns an annual net profit of £22,000 from his current business. He has two

alternatives to earning this money. The first is to sell the business for £340,000 and

invest in another business which will generate for him an annual return of 7%. Carlos

will help to run this business and will not be able to earn any other income. The

second alternative is to sell the business, for the same amount, and earn an annual

return of 2% from his local bank. If he earns this return, he will have enough time to

get a full-time job that pays £18,000 per year.

Required:

Using only the information provided above, calculate the opportunity cost for Carlos

in continuing to run his business.

management accounting.

Budgeting helps with planning and controlling based on assumptions made prior.

However, its disadvantages include:

-Inaccuracy: budgets can be inaccurate. Many events can change the accuracy of

budgeting, from unexpected events i.e. change in laws to i.e. not enough

staff/resources at a point in time. For example, a company may lose a major customer

impacting sales budgets, production and profit.

-Based on past results: Relying on past events provides a foundation and lays the view

of future projections. However, previous events may not, form part of future events.

For example, say company Y with projections to sell X number of phones, may have

a projection based on similar products, however, another company may offer a better

deal for a similar phone and change the product lifecycle and revenue of company Y.

Question 4

(a) The total fixed overhead costs of a business are £80,000 for a relevant range of

activity between 3,000 and 6,000 units. Below the relevant range the total fixed

overhead cost is £70,000 and above, £90,000. The only other costs are variable costs

of £4 per unit at any level of production.

Required:

Calculate the difference between the total costs at an activity level of 5,200 with that

of 2,600.

Total costs at an activity level 5,200: £80,000 + (£4 x 5,200) = £100,800

Total costs at an activity level 2,600: £70,000 + (£4 x 2600) = £80,400

The difference between the total costs at an activity level of 5,200 with that of 2,600

is of £20,400

(b) Carlos earns an annual net profit of £22,000 from his current business. He has two

alternatives to earning this money. The first is to sell the business for £340,000 and

invest in another business which will generate for him an annual return of 7%. Carlos

will help to run this business and will not be able to earn any other income. The

second alternative is to sell the business, for the same amount, and earn an annual

return of 2% from his local bank. If he earns this return, he will have enough time to

get a full-time job that pays £18,000 per year.

Required:

Using only the information provided above, calculate the opportunity cost for Carlos

in continuing to run his business.

Current income= £22,000

Sell and invest into another business: £340,000 x 7% = £23,800

Selling, bank deposit and full-time job: £340,000 x 2%= £ 6,800+ £18,000 = £24,800

Respective selling and investing into another business Carlos has a chance of making

an extra £1,800 that what he is earning now. However, by investing into a local bank

at 2% and working full time, he will make £2,800 more than he is currently.

(c)Martha wants to work out the factory production cost of a manufacturing job,

called AC45. The job consumed £2,600 of materials, incurred 28 hours of direct

labour and used 42 machine hours in May 20X1.

The relevant total production data for the factory during May 20X1 were as follows.

Production department

Direct wages (£) 64,000

Budgeted overheads chargeable (£) 44,800

Direct labour hours worked 12,800

Machine hours operated 6,000

Required:

Calculate to the nearest £ the total production cost of job AC45 if overheads are

absorbed on the basis of labour hours.

Total production Cost = Direct Materials + Direct Labour + Applied Overhead

Total production Cost = £2,600 + 44,800

Total production Cost = £47,400

(d)Le Clerc is a business that manufactures exclusive scarves. The budgeted selling

price is £12 and the budgeted variable cost is £6. The budgeted fixed cost for the

relevant accounting period is £13,000.

Sell and invest into another business: £340,000 x 7% = £23,800

Selling, bank deposit and full-time job: £340,000 x 2%= £ 6,800+ £18,000 = £24,800

Respective selling and investing into another business Carlos has a chance of making

an extra £1,800 that what he is earning now. However, by investing into a local bank

at 2% and working full time, he will make £2,800 more than he is currently.

(c)Martha wants to work out the factory production cost of a manufacturing job,

called AC45. The job consumed £2,600 of materials, incurred 28 hours of direct

labour and used 42 machine hours in May 20X1.

The relevant total production data for the factory during May 20X1 were as follows.

Production department

Direct wages (£) 64,000

Budgeted overheads chargeable (£) 44,800

Direct labour hours worked 12,800

Machine hours operated 6,000

Required:

Calculate to the nearest £ the total production cost of job AC45 if overheads are

absorbed on the basis of labour hours.

Total production Cost = Direct Materials + Direct Labour + Applied Overhead

Total production Cost = £2,600 + 44,800

Total production Cost = £47,400

(d)Le Clerc is a business that manufactures exclusive scarves. The budgeted selling

price is £12 and the budgeted variable cost is £6. The budgeted fixed cost for the

relevant accounting period is £13,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The actual sales were 15% more than the budgeted amount of 8,400. The only other

relevant difference between the budget and the actual accounting figures was that the

actual selling price fell by 25% from the budgeted price.

Required:

Calculate the actual profit made in the relevant accounting period.

Actual selling price: 12 x 25% = £9

Actual sales: 15% x 8,400 = £9,660

Budgeted variable cost £6

Budgeted fixed cost £13,000

8400 / 12 = 700 units to be sold (budgeted)

For 15% more, (15% 700) = extra 105 units required. Total units 700 + 105= 805

units

805 units sold at £9 = £7245 revenue

805 units at cost (£6 variable) = £4830 + £10,000 fix costs = £14,830

Business will have a loss of £7,585

relevant difference between the budget and the actual accounting figures was that the

actual selling price fell by 25% from the budgeted price.

Required:

Calculate the actual profit made in the relevant accounting period.

Actual selling price: 12 x 25% = £9

Actual sales: 15% x 8,400 = £9,660

Budgeted variable cost £6

Budgeted fixed cost £13,000

8400 / 12 = 700 units to be sold (budgeted)

For 15% more, (15% 700) = extra 105 units required. Total units 700 + 105= 805

units

805 units sold at £9 = £7245 revenue

805 units at cost (£6 variable) = £4830 + £10,000 fix costs = £14,830

Business will have a loss of £7,585

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.