Audit Risk Analysis: TWC Case Study

VerifiedAdded on 2019/09/23

|8

|2616

|147

Report

AI Summary

The assignment content requires students to analyze business risks that TWC faces, identify internal controls in their system that are potentially effective, and test these controls. Additionally, students need to list and justify weaknesses in internal control for purchases and accounts payable. The assessment also evaluates the students' ability to demonstrate risk management methodologies and the role of internal controls in an audit context, as well as their design of an audit plan and selection of appropriate audit procedures.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Background

You are a manager in the audit division at Miller Yates Howarth (MYH), an accounting firm with offices throughout the major regional centres

of NSW and Queensland. Although a medium sized firm by national standards, MYH is the second largest regional accounting firm in Australia.

Most of MYH’s audit clients are in the agriculture, mining, manufacturing and property industries. All those industries are currently under

pressure, either from a downturn in commodity prices or fierce competition from overseas competitors. Ratios extracted from an unaudited set of

financial reports at 30 June 2018 together with audited comparatives for the year ended 30 June 2017 and 2016 are set out below for your

review.

You are gathering information to prepare the audit plan of Trunkey Creek Wines Limited for the year ended 30 June 2018. Trunkey Creek Wines

(TCW) is one of MYH’s most significant and longstanding clients. The following information has been gathered to date.

Principal activities of TCW

• growing grapes for wine production;

• production and distribution of red, white and sparkling wines;

• beef cattle production on land surplus to grape production; and

• investment of surplus funds.

TCW was originally a family company incorporated in 1968 and has operated successfully and profitably since that date. In the 1990’s shares

were sold to a small number of investors to increase funds for the development and upgrading of the winery and the purchase of additional land

for the vineyards. Insufficient rainfall had meant that some land was no longer suitable for wine grape production, as a result, TWC moved into

Wagyu beef cattle production on this surplus land. The Wagyu operation is now starting to return a profit.

TWC now find that the 2 degrees increase in temperature at some vineyards is affecting the production of sparkling wine and are now looking at

purchasing land in cooler climates. TWC has built up a strong following for their sparkling wine which earns significant profits in both domestic

and overseas markets. TWC are currently negotiating the land purchase and part funding in part from medium term bank loans. The remaining

purchase price will be sourced from surplus funds.

The Wagyu beef is sold through the Wagyu Selling Group (WSG) in which TWC has shares. These shares form a material part of TWC’s

investment portfolio. WSG buys, butchers and sells the Wagyu beef to high end domestic restaurants and regularly sends frozen shipments to

Japan and China. TWC are heavily marketing their pinot, both domestically and overseas, as a perfect accompaniment to the Wagyu beef.

The directors of TCW are:

You are a manager in the audit division at Miller Yates Howarth (MYH), an accounting firm with offices throughout the major regional centres

of NSW and Queensland. Although a medium sized firm by national standards, MYH is the second largest regional accounting firm in Australia.

Most of MYH’s audit clients are in the agriculture, mining, manufacturing and property industries. All those industries are currently under

pressure, either from a downturn in commodity prices or fierce competition from overseas competitors. Ratios extracted from an unaudited set of

financial reports at 30 June 2018 together with audited comparatives for the year ended 30 June 2017 and 2016 are set out below for your

review.

You are gathering information to prepare the audit plan of Trunkey Creek Wines Limited for the year ended 30 June 2018. Trunkey Creek Wines

(TCW) is one of MYH’s most significant and longstanding clients. The following information has been gathered to date.

Principal activities of TCW

• growing grapes for wine production;

• production and distribution of red, white and sparkling wines;

• beef cattle production on land surplus to grape production; and

• investment of surplus funds.

TCW was originally a family company incorporated in 1968 and has operated successfully and profitably since that date. In the 1990’s shares

were sold to a small number of investors to increase funds for the development and upgrading of the winery and the purchase of additional land

for the vineyards. Insufficient rainfall had meant that some land was no longer suitable for wine grape production, as a result, TWC moved into

Wagyu beef cattle production on this surplus land. The Wagyu operation is now starting to return a profit.

TWC now find that the 2 degrees increase in temperature at some vineyards is affecting the production of sparkling wine and are now looking at

purchasing land in cooler climates. TWC has built up a strong following for their sparkling wine which earns significant profits in both domestic

and overseas markets. TWC are currently negotiating the land purchase and part funding in part from medium term bank loans. The remaining

purchase price will be sourced from surplus funds.

The Wagyu beef is sold through the Wagyu Selling Group (WSG) in which TWC has shares. These shares form a material part of TWC’s

investment portfolio. WSG buys, butchers and sells the Wagyu beef to high end domestic restaurants and regularly sends frozen shipments to

Japan and China. TWC are heavily marketing their pinot, both domestically and overseas, as a perfect accompaniment to the Wagyu beef.

The directors of TCW are:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

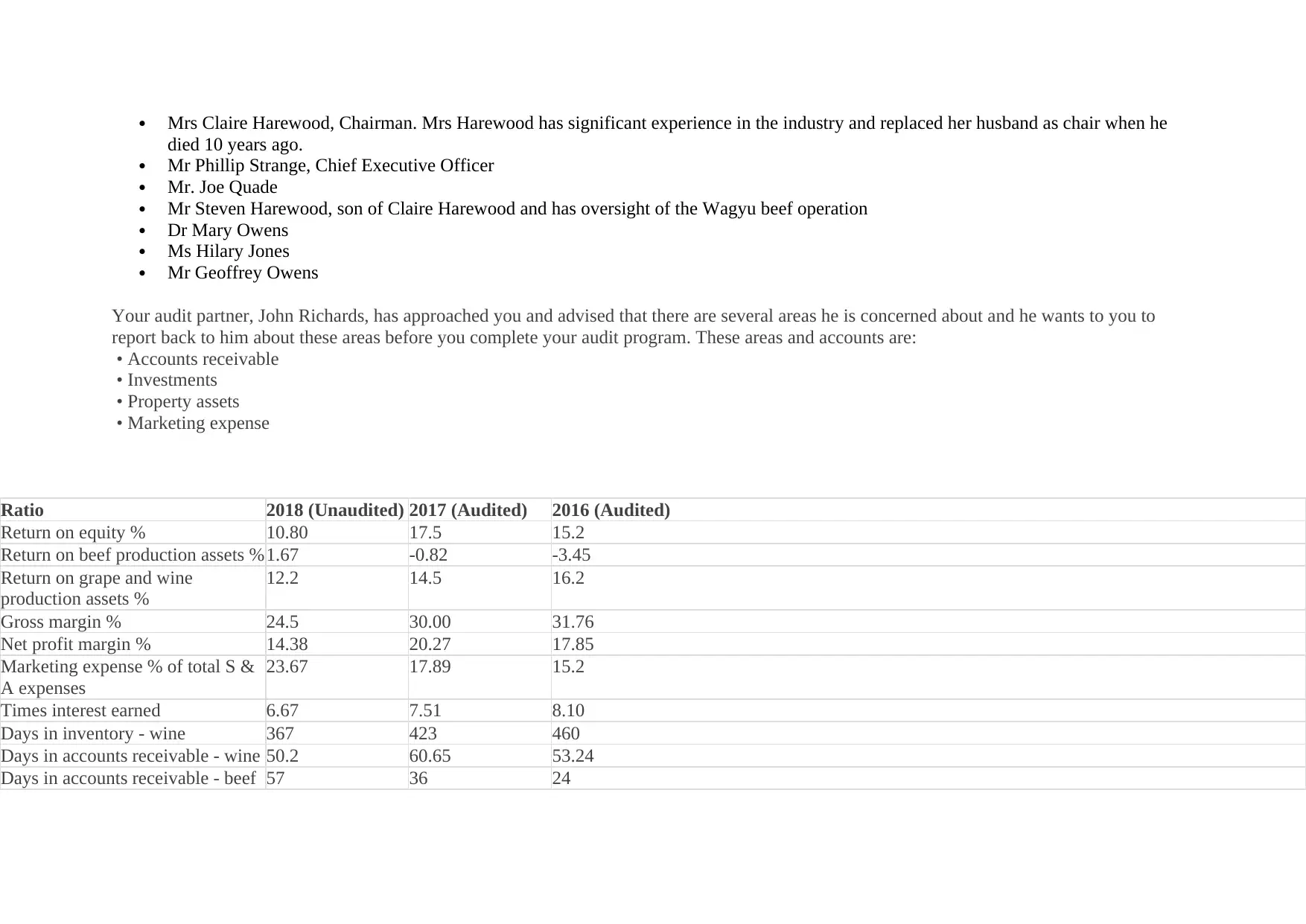

Mrs Claire Harewood, Chairman. Mrs Harewood has significant experience in the industry and replaced her husband as chair when he

died 10 years ago.

Mr Phillip Strange, Chief Executive Officer

Mr. Joe Quade

Mr Steven Harewood, son of Claire Harewood and has oversight of the Wagyu beef operation

Dr Mary Owens

Ms Hilary Jones

Mr Geoffrey Owens

Your audit partner, John Richards, has approached you and advised that there are several areas he is concerned about and he wants to you to

report back to him about these areas before you complete your audit program. These areas and accounts are:

• Accounts receivable

• Investments

• Property assets

• Marketing expense

Ratio 2018 (Unaudited) 2017 (Audited) 2016 (Audited)

Return on equity % 10.80 17.5 15.2

Return on beef production assets %1.67 -0.82 -3.45

Return on grape and wine

production assets %

12.2 14.5 16.2

Gross margin % 24.5 30.00 31.76

Net profit margin % 14.38 20.27 17.85

Marketing expense % of total S &

A expenses

23.67 17.89 15.2

Times interest earned 6.67 7.51 8.10

Days in inventory - wine 367 423 460

Days in accounts receivable - wine 50.2 60.65 53.24

Days in accounts receivable - beef 57 36 24

died 10 years ago.

Mr Phillip Strange, Chief Executive Officer

Mr. Joe Quade

Mr Steven Harewood, son of Claire Harewood and has oversight of the Wagyu beef operation

Dr Mary Owens

Ms Hilary Jones

Mr Geoffrey Owens

Your audit partner, John Richards, has approached you and advised that there are several areas he is concerned about and he wants to you to

report back to him about these areas before you complete your audit program. These areas and accounts are:

• Accounts receivable

• Investments

• Property assets

• Marketing expense

Ratio 2018 (Unaudited) 2017 (Audited) 2016 (Audited)

Return on equity % 10.80 17.5 15.2

Return on beef production assets %1.67 -0.82 -3.45

Return on grape and wine

production assets %

12.2 14.5 16.2

Gross margin % 24.5 30.00 31.76

Net profit margin % 14.38 20.27 17.85

Marketing expense % of total S &

A expenses

23.67 17.89 15.2

Times interest earned 6.67 7.51 8.10

Days in inventory - wine 367 423 460

Days in accounts receivable - wine 50.2 60.65 53.24

Days in accounts receivable - beef 57 36 24

Current ratio:1 2.80 2.54 2.66

Quick asset ratio:1 1.18 1.15 1.20

Debt to equity ratio:1 0.54 0.63 0.67

Internal control

The financial controller at TCW has been refining the system of internal controls and informs you, at the planning stage of the current year's

audit, that he has put together an internal control manual for the company. He has stated that this manual will create greater awareness of

controls in the company, particularly with management which, in the past, has not been overly conscious of the need to implement and enforce

effective internal controls.

Management staff receive bonuses based on certain agreed-upon target ratios which include measures such as targeted monthly sales volumes,

variance of actual to budget departmental overheads and profit before interest and tax. The Board takes an active interest in the performance of

the company and is quick to request explanations on variances from the agreed-upon monthly budgets.

Two years ago, the company devoted significant time and resources to the development and implementation of a new IT system. All teething

problems associated with the implementation phase have now been resolved, and the financial controller is satisfied that the automated controls

in place are assisting in producing accurate and complete accounting records. The management accountant also looks after the IT function as the

position is not regarded by management as being a full-time job. Once application programs have been tested, strict password control exists over

access to the programs. Passwords are not required for access to databases.

To assist in the planning for the current year's audit engagement, you extracted the following information from a review of the systems notes in

the permanent file and a perusal of the new internal control manual:

There are three section managers, one each for grape production, wine production and beef production. Each can order supplies for their

respective operations up to a limit of $10,000 for each order. Orders between $10,000 and $30,000 must be approved by the management

accountant. Orders over $30,000 must be approved by the CEO. Orders over $50,000 must be approved by the Board.

Orders must be made through the computer ordering system which has direct links to the approved suppliers.

Supplier information is contained in a supplier master file. Each supplier has a unique supplier code. If a section manager orders from an

unapproved supplier, the order is rejected and sent to the management accountant for approval.

The supplier information file is maintained by the accounts clerk. Changes to the file are approved manually by the management

accountant.

Quick asset ratio:1 1.18 1.15 1.20

Debt to equity ratio:1 0.54 0.63 0.67

Internal control

The financial controller at TCW has been refining the system of internal controls and informs you, at the planning stage of the current year's

audit, that he has put together an internal control manual for the company. He has stated that this manual will create greater awareness of

controls in the company, particularly with management which, in the past, has not been overly conscious of the need to implement and enforce

effective internal controls.

Management staff receive bonuses based on certain agreed-upon target ratios which include measures such as targeted monthly sales volumes,

variance of actual to budget departmental overheads and profit before interest and tax. The Board takes an active interest in the performance of

the company and is quick to request explanations on variances from the agreed-upon monthly budgets.

Two years ago, the company devoted significant time and resources to the development and implementation of a new IT system. All teething

problems associated with the implementation phase have now been resolved, and the financial controller is satisfied that the automated controls

in place are assisting in producing accurate and complete accounting records. The management accountant also looks after the IT function as the

position is not regarded by management as being a full-time job. Once application programs have been tested, strict password control exists over

access to the programs. Passwords are not required for access to databases.

To assist in the planning for the current year's audit engagement, you extracted the following information from a review of the systems notes in

the permanent file and a perusal of the new internal control manual:

There are three section managers, one each for grape production, wine production and beef production. Each can order supplies for their

respective operations up to a limit of $10,000 for each order. Orders between $10,000 and $30,000 must be approved by the management

accountant. Orders over $30,000 must be approved by the CEO. Orders over $50,000 must be approved by the Board.

Orders must be made through the computer ordering system which has direct links to the approved suppliers.

Supplier information is contained in a supplier master file. Each supplier has a unique supplier code. If a section manager orders from an

unapproved supplier, the order is rejected and sent to the management accountant for approval.

The supplier information file is maintained by the accounts clerk. Changes to the file are approved manually by the management

accountant.

When supplies are received at the winery, the storeman checks the supplies received to the online copy of the order and the delivery

docket provided by the supplier. Any discrepancies are noted on the online copy of the order.

The delivery docket is filed by the storeman in a folder that is kept at the winery.

The invoice is received electronically from the supplier and matched to the order by the accounts clerk. If the order and the invoice match

the invoice is included in a payments file.

The payments file is approved online by the management accountant once a week and used to generate an ABA file which is then

uploaded to the bank by the management accountant.

When the payments file is approved by the management accountant, the invoice is automatically recorded as being paid in the accounting

system.

When services such as repairs are ordered for the winery by the wine production manager, a service order is generated within the

computer system and automatically sent to the service provider.

When the service has been delivered, the wine production manager or the storeman signs the service delivery docket on the service man’s

tablet.

The invoice from the service company, with a copy of the signed service delivery docket, is received online by the accounts clerk.

The accounts clerk checks the signed service delivery docket to the invoice and the order and adds the invoice to the payments file for

final approval by the management accountant.

In the case of discrepancies, the accounts clerk contacts the supplier and the wine production manager to resolve the issue. Payments are

not made until the issue has been resolved.

Required

Write a report, including a brief executive summary, to your managing partner that addresses the questions below. Where indicated, use the

required format to answer that question.

Question 1A 8%

Analyse the ratios and additional information associated with the four accounts listed by your audit partner, John Richards. Identify the potential

audit risks and any audit steps that need to be undertaken to reduce audit risk.

Answer this question using the following table:

Account Analysis Audit Risk Audit Steps to reduce risk

docket provided by the supplier. Any discrepancies are noted on the online copy of the order.

The delivery docket is filed by the storeman in a folder that is kept at the winery.

The invoice is received electronically from the supplier and matched to the order by the accounts clerk. If the order and the invoice match

the invoice is included in a payments file.

The payments file is approved online by the management accountant once a week and used to generate an ABA file which is then

uploaded to the bank by the management accountant.

When the payments file is approved by the management accountant, the invoice is automatically recorded as being paid in the accounting

system.

When services such as repairs are ordered for the winery by the wine production manager, a service order is generated within the

computer system and automatically sent to the service provider.

When the service has been delivered, the wine production manager or the storeman signs the service delivery docket on the service man’s

tablet.

The invoice from the service company, with a copy of the signed service delivery docket, is received online by the accounts clerk.

The accounts clerk checks the signed service delivery docket to the invoice and the order and adds the invoice to the payments file for

final approval by the management accountant.

In the case of discrepancies, the accounts clerk contacts the supplier and the wine production manager to resolve the issue. Payments are

not made until the issue has been resolved.

Required

Write a report, including a brief executive summary, to your managing partner that addresses the questions below. Where indicated, use the

required format to answer that question.

Question 1A 8%

Analyse the ratios and additional information associated with the four accounts listed by your audit partner, John Richards. Identify the potential

audit risks and any audit steps that need to be undertaken to reduce audit risk.

Answer this question using the following table:

Account Analysis Audit Risk Audit Steps to reduce risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1B 2%

Analyse the ratios and additional information to outline business risks that TWC faces.

Question 2A 7%

Identify the internal controls in the system that are potentially effective, the risk that the control could alleviate and one test of control for each of

the identified potentially effective controls.

Answer this question using the following headings:

Effective control Risk alleviated Test of control

Question 2B 2%

List and justify the weaknesses in internal control for purchases and accounts payable.

Weakness Justification

Rationale

back to top

This assessment task will assess the following learning outcome/s:

Analyse the ratios and additional information to outline business risks that TWC faces.

Question 2A 7%

Identify the internal controls in the system that are potentially effective, the risk that the control could alleviate and one test of control for each of

the identified potentially effective controls.

Answer this question using the following headings:

Effective control Risk alleviated Test of control

Question 2B 2%

List and justify the weaknesses in internal control for purchases and accounts payable.

Weakness Justification

Rationale

back to top

This assessment task will assess the following learning outcome/s:

be able to demonstrate risk management methodologies and the role of internal controls in an audit context.

be able to design an audit plan and select and apply appropriate audit procedures for a financial statement audit.

be able to exercise critical and reflective judgement and appreciate the value of ethical practice.

Marking criteria and standards

back to top

Criteria High Distinction Distinction Credit Pass

Question 1

Analysis of ratios and other

information

demonstrating auditrisk

assessment skills and critical

and reflective judgement (4

marks).

Correct interpretation of

ratios and other

information provided,

demonstrating a

sophisticated

understanding of how

the ratios can be used to

analyse the audit risks.

Correct interpretation

of ratios and other

information provided,

demonstrating a clear

understanding of how

the ratios can be used

to analyse the audit

risks.

Most interpretations of ratios

and other

information provided correct,

demonstrating an

understanding of how the

ratios can be used to analyse

the audit risks.

Most interpretations of ratios and

other

information provided correct but

a limited understanding of their

usefulness in identifying the audit

risks.

Identification of audit steps

that minimise audit risk

identified through the

analysis of the ratios and the

additional information (4

marks).

All appropriate audit

steps identified with a

clear statement as to

how these will minimise

audit risk, demonstrating

a sophisticated level of

audit planning.

Most appropriate audit

steps identified. A

clear understanding of

how audit tests

minimise audit risk.

Many appropriate audit steps

identified. Some

understanding of how audit

tests minimise audit risk.

Some appropriate audit steps

identified.

Basic understanding of how audit

tests minimise audit risk.

Analysis of ratios and other

information

demonstrating business risk

Strong application of

analytical procedures

and other provided

Sound application of

analytical procedures

and other provided

Some application of analytical

procedures and other provided

information to assessment of

Use of some provided information

in listing at least three items of

business risk. Basic application of

be able to design an audit plan and select and apply appropriate audit procedures for a financial statement audit.

be able to exercise critical and reflective judgement and appreciate the value of ethical practice.

Marking criteria and standards

back to top

Criteria High Distinction Distinction Credit Pass

Question 1

Analysis of ratios and other

information

demonstrating auditrisk

assessment skills and critical

and reflective judgement (4

marks).

Correct interpretation of

ratios and other

information provided,

demonstrating a

sophisticated

understanding of how

the ratios can be used to

analyse the audit risks.

Correct interpretation

of ratios and other

information provided,

demonstrating a clear

understanding of how

the ratios can be used

to analyse the audit

risks.

Most interpretations of ratios

and other

information provided correct,

demonstrating an

understanding of how the

ratios can be used to analyse

the audit risks.

Most interpretations of ratios and

other

information provided correct but

a limited understanding of their

usefulness in identifying the audit

risks.

Identification of audit steps

that minimise audit risk

identified through the

analysis of the ratios and the

additional information (4

marks).

All appropriate audit

steps identified with a

clear statement as to

how these will minimise

audit risk, demonstrating

a sophisticated level of

audit planning.

Most appropriate audit

steps identified. A

clear understanding of

how audit tests

minimise audit risk.

Many appropriate audit steps

identified. Some

understanding of how audit

tests minimise audit risk.

Some appropriate audit steps

identified.

Basic understanding of how audit

tests minimise audit risk.

Analysis of ratios and other

information

demonstrating business risk

Strong application of

analytical procedures

and other provided

Sound application of

analytical procedures

and other provided

Some application of analytical

procedures and other provided

information to assessment of

Use of some provided information

in listing at least three items of

business risk. Basic application of

Criteria High Distinction Distinction Credit Pass

identification skills (2

marks).

information to provide

comprehensive

assessment of at least

four items of business

risk.

information to provide

assessment of at least

four items of business

risk.

at least three items of business

risk.

analytical procedures.

Question 2

Appraisal of the client's

internal control environment

and application to the audit

risk model (5 marks)

Identification of at least

four internal controls

that are potentially

effective, with

a comprehensive

explanation of the risk

each one could mitigate.

Tests of control

Identification of at

least four internal

controls that are

potentially effective,

with an explanation of

the risk each one could

mitigate.

Identification of at least three

internal controls that are

potentially effective, with an

explanation of the risk each

one could mitigate.

Identification of three internal

controls that are potentially

effective with basic explanation of

the risk each one could mitigate.

Development of a series of

audit steps that assess the

effectiveness of

internal controls (2 marks).

Development of a

comprehensive series of

audit steps designed

to assess the

effectiveness of internal

controls. This

demonstrates a deep

understanding of the

audit process.

Development of a

series of high quality

audit steps designed to

assess the effectiveness

of internal controls.

This demonstrates

a clear understanding

of the audit process.

Development of audit steps

designed to assess the

effectiveness of internal

controls. This demonstrates a

moderate understanding of the

audit process.

Development of basic audit steps

designed to assess the

effectiveness of internal controls.

This demonstrates a basic

understanding of the audit

process.

Identified internal control

weaknesses (2 marks)

Identification of and

comprehensive

justification for at least

five sales and

Identification of and

justification for at least

four sales and

receivables internal

Identification of and

justification for at least three

sales and receivables internal

control weaknesses.

Identification of but limited

explanation for at least three sales

and receivables internal control

weaknesses.

identification skills (2

marks).

information to provide

comprehensive

assessment of at least

four items of business

risk.

information to provide

assessment of at least

four items of business

risk.

at least three items of business

risk.

analytical procedures.

Question 2

Appraisal of the client's

internal control environment

and application to the audit

risk model (5 marks)

Identification of at least

four internal controls

that are potentially

effective, with

a comprehensive

explanation of the risk

each one could mitigate.

Tests of control

Identification of at

least four internal

controls that are

potentially effective,

with an explanation of

the risk each one could

mitigate.

Identification of at least three

internal controls that are

potentially effective, with an

explanation of the risk each

one could mitigate.

Identification of three internal

controls that are potentially

effective with basic explanation of

the risk each one could mitigate.

Development of a series of

audit steps that assess the

effectiveness of

internal controls (2 marks).

Development of a

comprehensive series of

audit steps designed

to assess the

effectiveness of internal

controls. This

demonstrates a deep

understanding of the

audit process.

Development of a

series of high quality

audit steps designed to

assess the effectiveness

of internal controls.

This demonstrates

a clear understanding

of the audit process.

Development of audit steps

designed to assess the

effectiveness of internal

controls. This demonstrates a

moderate understanding of the

audit process.

Development of basic audit steps

designed to assess the

effectiveness of internal controls.

This demonstrates a basic

understanding of the audit

process.

Identified internal control

weaknesses (2 marks)

Identification of and

comprehensive

justification for at least

five sales and

Identification of and

justification for at least

four sales and

receivables internal

Identification of and

justification for at least three

sales and receivables internal

control weaknesses.

Identification of but limited

explanation for at least three sales

and receivables internal control

weaknesses.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Criteria High Distinction Distinction Credit Pass

receivables internal

control weaknesses.

control weaknesses.

These last two criteria

relate to the whole of the

case study.

Professional communication

(Note: you are required to

space between paragraphs;

use Arial 10pt or TNR 12 pt;

use 1.5 or double line

spacing) (0.5 mark).

Work contains distinct

understandable

statements with no

errors.

Extremely well

organised. Content is

structured in a manner

that facilitates the

reader’s understanding.

Work contains distinct

understandable

statements with

minimal errors.

Answer is well

organised. Content is

structured in a manner

that facilitates the

reader’s understanding.

Minor spelling, grammar and

punctuation errors. Work

shows evidence of

proofreading. Well-structured

with one main idea or

argument provided per

paragraph.

Some spelling, grammar and

punctuation errors found but the

work is readable and structured.

Work may include too many ideas

in one paragraph.

Appropriate resources and

correct referencing

(0.5 mark).

Used a range of sources.

All work has been

referenced correctly as

per APA (6th edn)

requirements.

Used two or more

sources. All work has

been referenced

correctly as per APA

(6th edn) requirements.

Used one or more sources. All

work has been referenced

within the body of the answer

and in the reference list, with

some omissions or errors in

terms.

No additional sources used other

than the text. Others’ work is not

always acknowledged and there

are a number of errors or non-

compliance with the APA (6th

edn).

receivables internal

control weaknesses.

control weaknesses.

These last two criteria

relate to the whole of the

case study.

Professional communication

(Note: you are required to

space between paragraphs;

use Arial 10pt or TNR 12 pt;

use 1.5 or double line

spacing) (0.5 mark).

Work contains distinct

understandable

statements with no

errors.

Extremely well

organised. Content is

structured in a manner

that facilitates the

reader’s understanding.

Work contains distinct

understandable

statements with

minimal errors.

Answer is well

organised. Content is

structured in a manner

that facilitates the

reader’s understanding.

Minor spelling, grammar and

punctuation errors. Work

shows evidence of

proofreading. Well-structured

with one main idea or

argument provided per

paragraph.

Some spelling, grammar and

punctuation errors found but the

work is readable and structured.

Work may include too many ideas

in one paragraph.

Appropriate resources and

correct referencing

(0.5 mark).

Used a range of sources.

All work has been

referenced correctly as

per APA (6th edn)

requirements.

Used two or more

sources. All work has

been referenced

correctly as per APA

(6th edn) requirements.

Used one or more sources. All

work has been referenced

within the body of the answer

and in the reference list, with

some omissions or errors in

terms.

No additional sources used other

than the text. Others’ work is not

always acknowledged and there

are a number of errors or non-

compliance with the APA (6th

edn).

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.