Balance Scorecard: Concept, Assumptions, Critique and Examples

VerifiedAdded on 2023/06/15

|18

|3632

|485

AI Summary

This report analyses the process of balance scorecard usage in organisations. It summarises the concept of balance scorecard, assumptions it’s based on, and different perspectives it is used in companies. It also includes examples of usage of balance scorecard in different sectors like healthcare, manufacturing and software industries.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BALANCE SCORECARD

Balance Scorecard

Name of the Student:

Name of the University:

Author note:

Balance Scorecard

Name of the Student:

Name of the University:

Author note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BALANCE SCORECARD

Executive summary

The purpose of this report is to analyse the process of balance scorecard usage in

organisation. The discussion briefly summarises the concept of balance scorecard. The main

purpose is to criticise balance scorecard and the assumptions it’s based into. The report also

summarises different perspectives it is used in companies. Different sector like healthcare,

manufacturing and software industries uses this scorecard. It is also used in different

department of an organisation. Therefore, an example of Human resource balance scorecard

is used in this text and described briefly. Moreover the real life usage of balance scorecard in

Ethiopia industry and Tolko Industry’s usage of BSC is summarised in the discussion.

Executive summary

The purpose of this report is to analyse the process of balance scorecard usage in

organisation. The discussion briefly summarises the concept of balance scorecard. The main

purpose is to criticise balance scorecard and the assumptions it’s based into. The report also

summarises different perspectives it is used in companies. Different sector like healthcare,

manufacturing and software industries uses this scorecard. It is also used in different

department of an organisation. Therefore, an example of Human resource balance scorecard

is used in this text and described briefly. Moreover the real life usage of balance scorecard in

Ethiopia industry and Tolko Industry’s usage of BSC is summarised in the discussion.

2BALANCE SCORECARD

Table of Contents

Introduction................................................................................................................................3

Concept of balance scorecard.....................................................................................................3

Assumptions on which balance scorecard is based on...............................................................3

Critically review balance scorecard...........................................................................................7

Benefits......................................................................................................................................7

Drawbacks..................................................................................................................................8

Examples of usage of balance scorecard....................................................................................9

Real life examples of usage of balance scorecard....................................................................12

Conclusion................................................................................................................................13

Reference..................................................................................................................................14

Table of Contents

Introduction................................................................................................................................3

Concept of balance scorecard.....................................................................................................3

Assumptions on which balance scorecard is based on...............................................................3

Critically review balance scorecard...........................................................................................7

Benefits......................................................................................................................................7

Drawbacks..................................................................................................................................8

Examples of usage of balance scorecard....................................................................................9

Real life examples of usage of balance scorecard....................................................................12

Conclusion................................................................................................................................13

Reference..................................................................................................................................14

3BALANCE SCORECARD

Introduction

Kaplan invented the balance scorecard in 1992, which was later published by Norton

in 1996 in an upgraded version (Kaplan and Norton 2012). The performance measurement

tool is one of the most important part of organisation to predict the future. The industries

have also become competitive in nature with changing environment. To achieve success in

this competitive market the companies are also becoming more conscious about their

performance. After globalisation, competing in a global market has also become imperative.

Therefore, this tool of measurement has gain attention of several business personnel’s to

methodically use it according to the organisation’s requirements (Buller and McEvoy 2012).

The following discussion about balance scorecard and different examples from different

sector has been discussed. The balance scorecard comes under the strategic map of the four

perspectives (Casey and Peck 2014). This strategic map helps in drawing an overall

conclusion of from four different perspectives.

Concept of balance scorecard

This tool of measurement has originated to involve two different matters of

measurement and combining them in a proper manner. The age-old financial data to gain

insights in performance, as well as the effect of non-financial data. This also takes into

consideration of the different strategic agenda the company have or had (Pineno 2013.). This

is also known as the strategic linkage model because it takes into account of the strategic

advantage. The measurement features and version has flexibility to change with the different

factors of the organisations.

Introduction

Kaplan invented the balance scorecard in 1992, which was later published by Norton

in 1996 in an upgraded version (Kaplan and Norton 2012). The performance measurement

tool is one of the most important part of organisation to predict the future. The industries

have also become competitive in nature with changing environment. To achieve success in

this competitive market the companies are also becoming more conscious about their

performance. After globalisation, competing in a global market has also become imperative.

Therefore, this tool of measurement has gain attention of several business personnel’s to

methodically use it according to the organisation’s requirements (Buller and McEvoy 2012).

The following discussion about balance scorecard and different examples from different

sector has been discussed. The balance scorecard comes under the strategic map of the four

perspectives (Casey and Peck 2014). This strategic map helps in drawing an overall

conclusion of from four different perspectives.

Concept of balance scorecard

This tool of measurement has originated to involve two different matters of

measurement and combining them in a proper manner. The age-old financial data to gain

insights in performance, as well as the effect of non-financial data. This also takes into

consideration of the different strategic agenda the company have or had (Pineno 2013.). This

is also known as the strategic linkage model because it takes into account of the strategic

advantage. The measurement features and version has flexibility to change with the different

factors of the organisations.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BALANCE SCORECARD

Assumptions on which balance scorecard is based on

The basic scorecard consists of four different perspectives that affect the development

of the original business perspectives.

Financial – the success of the business or the organisation depends on the revenue or the

capital of the business. The financial performance of the company is calculated by the

financial metrics decided. This is one of the most important of the pillars of BSC. In this case,

the main aim is to gauge the financial perspectives of the company (Pineno 2013). To

improve the productivity of the company and incorporating growth strategy is main objective

of this process. It also involves the stakeholder’s satisfaction in the company (Rid 2016). It is

also monitors and evaluates the implemented process in the organisation. The generic metrics

or measurement of this is return of capital, economic value addition, sales growth and cash

flow (Casey and Peck 2004). The financial success of the business is also dependent upon the

operating cost and efficiency, capacity to utilisation ratio, capability constraints and

warranties and guarantee cost.

Customer – the customer perspective of the company is essential part of balance scorecard.

This factor was not considered in the previous measurement tools. With the product or

service offered by the company the cost to customers is very sensitive matter to consider.

Therefore, this element of organisations success is considered in this measurement tool. With

lowering the cost, more attraction of the customer and consistency in their buying behaviour

will be gained. In this customer, perspective element of balance scorecard the two most

important part of this factor is customer satisfaction and brand image of the company (Madah

et al. 2013). Therefore, to ensure the highest satisfaction score the generic metrics of the

company is lowering manufacturing cost by increasing operational efficiency, Sales delivery

efficiency, and direct pass rate and market feedback (Casey and Peck 2014). The other

primary factors are sales volume analysis with keeping in mind about the profitability

Assumptions on which balance scorecard is based on

The basic scorecard consists of four different perspectives that affect the development

of the original business perspectives.

Financial – the success of the business or the organisation depends on the revenue or the

capital of the business. The financial performance of the company is calculated by the

financial metrics decided. This is one of the most important of the pillars of BSC. In this case,

the main aim is to gauge the financial perspectives of the company (Pineno 2013). To

improve the productivity of the company and incorporating growth strategy is main objective

of this process. It also involves the stakeholder’s satisfaction in the company (Rid 2016). It is

also monitors and evaluates the implemented process in the organisation. The generic metrics

or measurement of this is return of capital, economic value addition, sales growth and cash

flow (Casey and Peck 2004). The financial success of the business is also dependent upon the

operating cost and efficiency, capacity to utilisation ratio, capability constraints and

warranties and guarantee cost.

Customer – the customer perspective of the company is essential part of balance scorecard.

This factor was not considered in the previous measurement tools. With the product or

service offered by the company the cost to customers is very sensitive matter to consider.

Therefore, this element of organisations success is considered in this measurement tool. With

lowering the cost, more attraction of the customer and consistency in their buying behaviour

will be gained. In this customer, perspective element of balance scorecard the two most

important part of this factor is customer satisfaction and brand image of the company (Madah

et al. 2013). Therefore, to ensure the highest satisfaction score the generic metrics of the

company is lowering manufacturing cost by increasing operational efficiency, Sales delivery

efficiency, and direct pass rate and market feedback (Casey and Peck 2014). The other

primary factors are sales volume analysis with keeping in mind about the profitability

5BALANCE SCORECARD

maximisation, increasing quality standards, product and service delivery excellence, ensuring

knowledge and skilled partner of the company, reinforcing customer satisfaction through

providing a proper brand image.

Internal business process - the internal perspective of the organisation involves the

operational and process excellence, which are the main factor of the internal process. In

conducting the internal process evaluation the main criteria is to alliance more with the

Strategic Business Units of the organisation (Awadallah and Allam 2015). On the other hand,

process innovation helps in increasing corporate social responsibility. In this perspective, the

generic indicators are productivity, delivery, rapid improvement, Performance identifiers as

well as safety and health and environmental factors are considered too (Casey and Peck

2014). For some process, in different organisations the things that are used are Cycle time,

which increases the efficiency of two consecutive process, work in Progress, kaizen costing

to increase the efficiency, lessening the number of industrial accidents, timely introduction

(Madah et al. 2013).

Learning and growth strategy – the development is also essential for the company to consider

the availability and of skills and strategic alignment with the proposed plan. The research and

development unit should be part of the procurement process of the company (Awadallah and

Allam 2015.). The information system availability of the company also considers the set up

and validation cost and communication process of the system (Ciuzaite 2012). The

effectiveness of this process relies in the system as well as the people. The employee

retention, training, skills and morale are also evaluated in this process. The availability of

critical real time for information need and employee need is also measured in this process.

Evaluation - The monitoring and evaluation should be parallelly implemented in the

systems. It may be daily, weekly; monthly monitoring service but it should be specifically

maximisation, increasing quality standards, product and service delivery excellence, ensuring

knowledge and skilled partner of the company, reinforcing customer satisfaction through

providing a proper brand image.

Internal business process - the internal perspective of the organisation involves the

operational and process excellence, which are the main factor of the internal process. In

conducting the internal process evaluation the main criteria is to alliance more with the

Strategic Business Units of the organisation (Awadallah and Allam 2015). On the other hand,

process innovation helps in increasing corporate social responsibility. In this perspective, the

generic indicators are productivity, delivery, rapid improvement, Performance identifiers as

well as safety and health and environmental factors are considered too (Casey and Peck

2014). For some process, in different organisations the things that are used are Cycle time,

which increases the efficiency of two consecutive process, work in Progress, kaizen costing

to increase the efficiency, lessening the number of industrial accidents, timely introduction

(Madah et al. 2013).

Learning and growth strategy – the development is also essential for the company to consider

the availability and of skills and strategic alignment with the proposed plan. The research and

development unit should be part of the procurement process of the company (Awadallah and

Allam 2015.). The information system availability of the company also considers the set up

and validation cost and communication process of the system (Ciuzaite 2012). The

effectiveness of this process relies in the system as well as the people. The employee

retention, training, skills and morale are also evaluated in this process. The availability of

critical real time for information need and employee need is also measured in this process.

Evaluation - The monitoring and evaluation should be parallelly implemented in the

systems. It may be daily, weekly; monthly monitoring service but it should be specifically

6BALANCE SCORECARD

implemented in the process. The flexibility of this measurement tool lies in the intended use

of this in all level of business process (Siddique and Shadbolt 2016.). There can be two

different evaluation processes, one is system performance evaluation and another is strategic

performance evaluation (Buller and McEvoy 2012). The system performance evaluation is

very methodical in nature, the evaluation report consist of the assessments, interview, online

surveys, executive survey and surveys of the internal stakeholders of the company. The

technical evaluation and behavioural evaluation of the company gets influenced by the

characteristics of the system and culture and norms of the organisation (Siddique and

Shadbolt 2016). The strategic performance evaluation of the company is another essential

role of balance scorecard evaluation process. After the evaluation, revalidation of the

company’s mission, vision and the strategic points should be given emphasis. The validity

and modification process is done in this organisation (Madah et al. 2013). The performance

measures and re-prioritisation of the initiatives is main objective of this process.

implemented in the process. The flexibility of this measurement tool lies in the intended use

of this in all level of business process (Siddique and Shadbolt 2016.). There can be two

different evaluation processes, one is system performance evaluation and another is strategic

performance evaluation (Buller and McEvoy 2012). The system performance evaluation is

very methodical in nature, the evaluation report consist of the assessments, interview, online

surveys, executive survey and surveys of the internal stakeholders of the company. The

technical evaluation and behavioural evaluation of the company gets influenced by the

characteristics of the system and culture and norms of the organisation (Siddique and

Shadbolt 2016). The strategic performance evaluation of the company is another essential

role of balance scorecard evaluation process. After the evaluation, revalidation of the

company’s mission, vision and the strategic points should be given emphasis. The validity

and modification process is done in this organisation (Madah et al. 2013). The performance

measures and re-prioritisation of the initiatives is main objective of this process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BALANCE SCORECARD

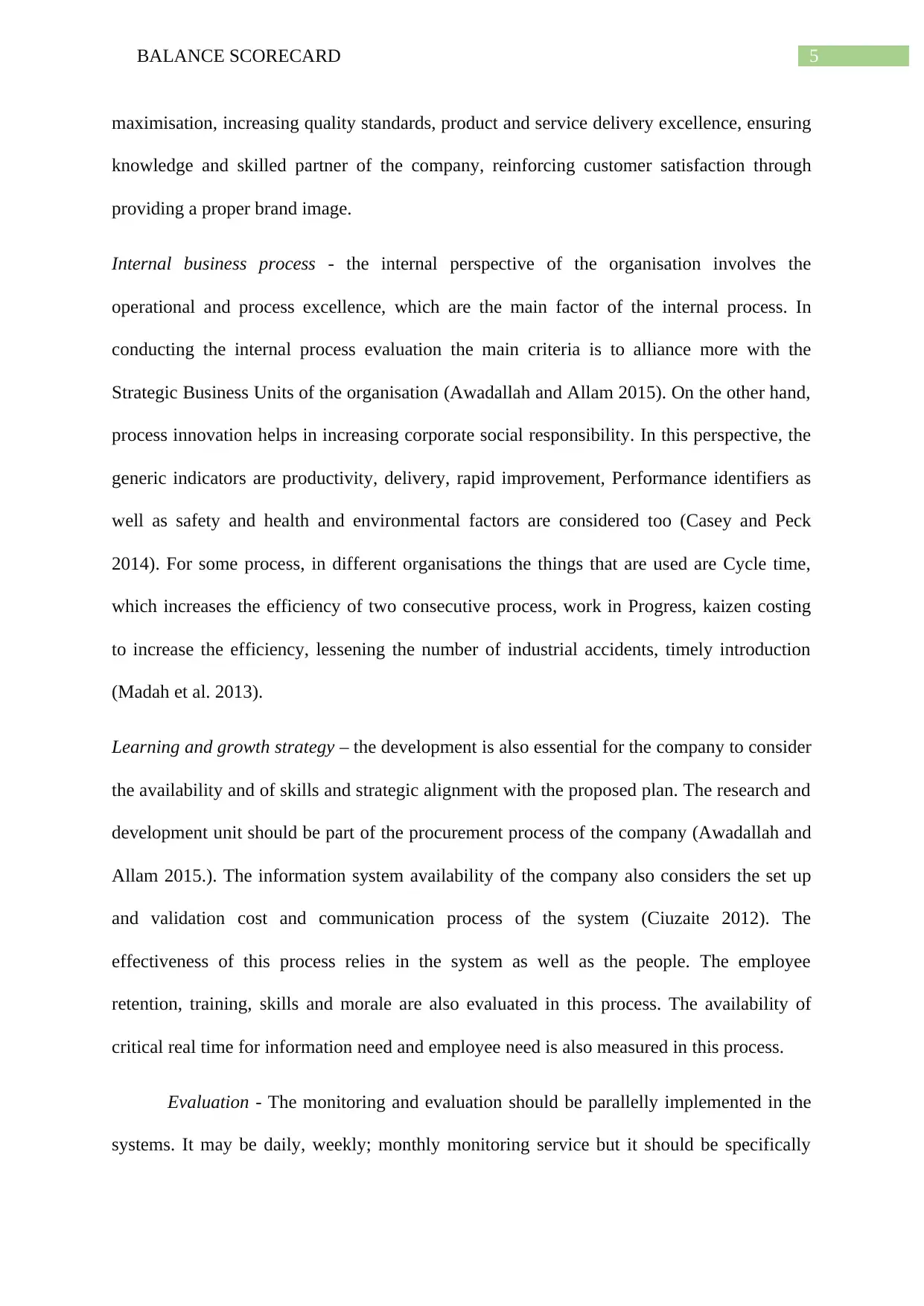

Figure: Balance Scorecard the nine-step success framework

Source: Buller and McEvoy 2012

The above system and strategic evaluation and monitor is used by companies in need of the

measuring their performance in any level.

Critically review balance scorecard

The balance scorecard was invented in order to balance between the positive and a

negative aspect of performance, which was at first was entirely dependent upon the

accounting measures. According to Nørreklit and Mitchell (2014), the aim was also to

broaden the financial perspective as well as to improve organisational performance by

incorporating different contributing factor that affects the performance. In addition, the aim

was to take into consideration, the strategic part of the company (Pineno 2013). It has become

essential that the company use different tools to particularly measure the outcome of their

performance. Balance scorecard consolidates the result of an organisation, which is complex

entity. Another benefit of this scorecard is that, it can be used in many context and different

nature of organisation. The casual relationship among the four dimensions is also argued to

be a main factor considered in the balance scorecard model.

Benefits

There are many advantages of using balance scorecard in the measuring performance

of organisation. According to Kurtzman and Urresta (2012) in the late nineties, the more than

50 % of the company used balance scorecard in different form. Government agencies military

units as well as the new non-profit organisations also used the balance scorecard (Siddique

and Shadbolt 2016). The modern balance scorecard is one of the most important tool to assess

the performance of the company. First, it gives structure to the strategy consolidating under a

Figure: Balance Scorecard the nine-step success framework

Source: Buller and McEvoy 2012

The above system and strategic evaluation and monitor is used by companies in need of the

measuring their performance in any level.

Critically review balance scorecard

The balance scorecard was invented in order to balance between the positive and a

negative aspect of performance, which was at first was entirely dependent upon the

accounting measures. According to Nørreklit and Mitchell (2014), the aim was also to

broaden the financial perspective as well as to improve organisational performance by

incorporating different contributing factor that affects the performance. In addition, the aim

was to take into consideration, the strategic part of the company (Pineno 2013). It has become

essential that the company use different tools to particularly measure the outcome of their

performance. Balance scorecard consolidates the result of an organisation, which is complex

entity. Another benefit of this scorecard is that, it can be used in many context and different

nature of organisation. The casual relationship among the four dimensions is also argued to

be a main factor considered in the balance scorecard model.

Benefits

There are many advantages of using balance scorecard in the measuring performance

of organisation. According to Kurtzman and Urresta (2012) in the late nineties, the more than

50 % of the company used balance scorecard in different form. Government agencies military

units as well as the new non-profit organisations also used the balance scorecard (Siddique

and Shadbolt 2016). The modern balance scorecard is one of the most important tool to assess

the performance of the company. First, it gives structure to the strategy consolidating under a

8BALANCE SCORECARD

single strategy. For example, the financial perspective can be interpreted from BSC by the

HR manager helping them incorporating re-evaluation of strategy of training needs and skill

development programs in a company, which may be a liability or cost to company. As

explained by (Siddique and Shadbolt 2016), A logical structure of balance scorecard also

helps in communicating strategies in a layman’s language, like clearing key individual goals

as well as how it is aligned with the company’s objectives. Aligning the individual

department’s or teams objectives with the enterprise is also part of the done through balance

scorecard. Like generic metrics like economic value addition is measured in the process to

align the social responsibility of the company towards regional or global economy. This value

addition links to the projects that the company takes in the future (Ciuzaite 2012). The most

reviewed part of balance scorecard is involving the intangible factors into strategic

management.

Drawbacks

Though this measurement tool has been adopted by many organisations, some of the critics

has shown many disadvantages of using this tool. The second-generation balance scorecard is

one of the most complex models and the casual links of this modified version is also

complicated in nature. The empirical nature of the framework is one of the most criticised

parts of balance scorecard by Grevinga (2013). Another limitation of this is that the tool can

be less effective in the service industry. The service industry consists of many intangible

factors that cannot be incorporated in the measurement thus reducing its effectiveness.

According to Kraaijenbrink (2012), it is more suited to the engineering firms. Many

organisations use this tool to get an overview of their performance and implementing the

strategy. But the in-depth insights are not gathered in this process. Moreover, according to

him, the more influence of the strategy can also be a matter to avoid the other contributing

single strategy. For example, the financial perspective can be interpreted from BSC by the

HR manager helping them incorporating re-evaluation of strategy of training needs and skill

development programs in a company, which may be a liability or cost to company. As

explained by (Siddique and Shadbolt 2016), A logical structure of balance scorecard also

helps in communicating strategies in a layman’s language, like clearing key individual goals

as well as how it is aligned with the company’s objectives. Aligning the individual

department’s or teams objectives with the enterprise is also part of the done through balance

scorecard. Like generic metrics like economic value addition is measured in the process to

align the social responsibility of the company towards regional or global economy. This value

addition links to the projects that the company takes in the future (Ciuzaite 2012). The most

reviewed part of balance scorecard is involving the intangible factors into strategic

management.

Drawbacks

Though this measurement tool has been adopted by many organisations, some of the critics

has shown many disadvantages of using this tool. The second-generation balance scorecard is

one of the most complex models and the casual links of this modified version is also

complicated in nature. The empirical nature of the framework is one of the most criticised

parts of balance scorecard by Grevinga (2013). Another limitation of this is that the tool can

be less effective in the service industry. The service industry consists of many intangible

factors that cannot be incorporated in the measurement thus reducing its effectiveness.

According to Kraaijenbrink (2012), it is more suited to the engineering firms. Many

organisations use this tool to get an overview of their performance and implementing the

strategy. But the in-depth insights are not gathered in this process. Moreover, according to

him, the more influence of the strategy can also be a matter to avoid the other contributing

9BALANCE SCORECARD

factor. Comparing two electrical firms, it has been seen that the two firms to gain similar net

and gross profit but one firm used the measurement tool and the other did not. Therefore, this

practical acquisition of the framework originated the negative effect in the usage and

adoption of balance scorecard (Swierk and Mulawa 2014). The positive financial result may

or may not be dependent on the balance scorecard implementation. Implementation of BSC in

the organisation is time consuming and it has been found that the employees got more

irritated in the process and claimed that they could have used the time in doing the assigned

responsibilities in the company. On several account it has been claimed that it does not take

into consideration of the important aspects of stakeholders issues (Madsen and Stenheim

2014). In fact, it is also cited that the importance of the key stakeholders like suppliers,

government and environmental factors are ignored as well as it fails to accommodate the

shareholders interests. Moreover, though the internal process and learning and growth

strategy includes employee in the framework but at times, it lacks explicit involvement of

employee engagement and

factor. Comparing two electrical firms, it has been seen that the two firms to gain similar net

and gross profit but one firm used the measurement tool and the other did not. Therefore, this

practical acquisition of the framework originated the negative effect in the usage and

adoption of balance scorecard (Swierk and Mulawa 2014). The positive financial result may

or may not be dependent on the balance scorecard implementation. Implementation of BSC in

the organisation is time consuming and it has been found that the employees got more

irritated in the process and claimed that they could have used the time in doing the assigned

responsibilities in the company. On several account it has been claimed that it does not take

into consideration of the important aspects of stakeholders issues (Madsen and Stenheim

2014). In fact, it is also cited that the importance of the key stakeholders like suppliers,

government and environmental factors are ignored as well as it fails to accommodate the

shareholders interests. Moreover, though the internal process and learning and growth

strategy includes employee in the framework but at times, it lacks explicit involvement of

employee engagement and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BALANCE SCORECARD

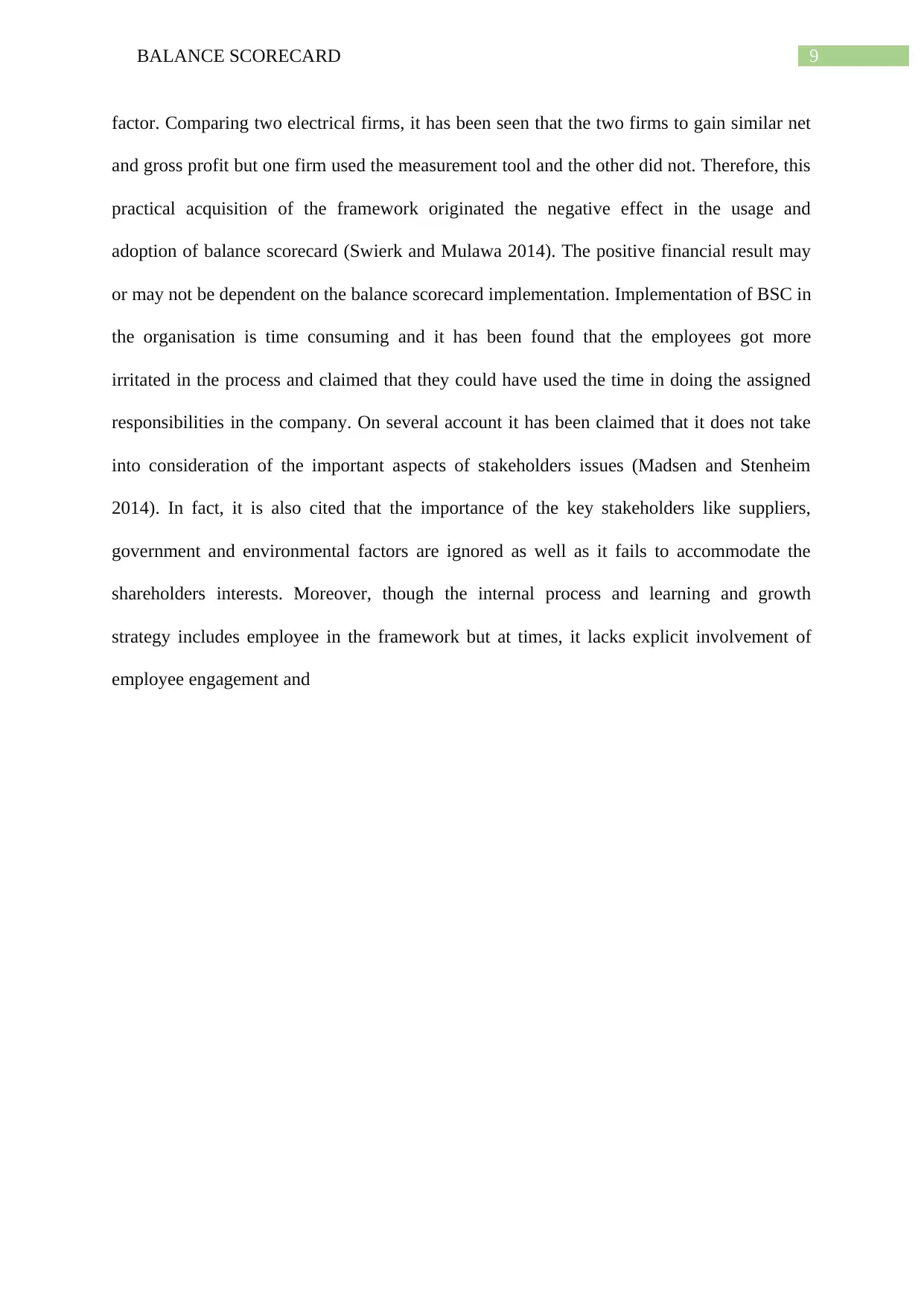

Examples of usage of balance scorecard

Figure: manufacturing scorecard

Source: Swierk and Mulawa 2014)

The manufacturing scorecard of the company consists of the volume profit and low cost

operations. Most of the time, the manufacturing companies are more concerned about their

operational efficiency (Swierk and Mulawa 2014). Increasing the output and decreasing the

production cost, with correctly pricing strategy should be obtained (Grevinga 2013). The

large emphasis should also be on the safety needs of the in a manufacturing camp. The

metrics that are given should be consolidated under the strategic framework. The main four

pillars of balance scorecard are separated in the process.

Examples of usage of balance scorecard

Figure: manufacturing scorecard

Source: Swierk and Mulawa 2014)

The manufacturing scorecard of the company consists of the volume profit and low cost

operations. Most of the time, the manufacturing companies are more concerned about their

operational efficiency (Swierk and Mulawa 2014). Increasing the output and decreasing the

production cost, with correctly pricing strategy should be obtained (Grevinga 2013). The

large emphasis should also be on the safety needs of the in a manufacturing camp. The

metrics that are given should be consolidated under the strategic framework. The main four

pillars of balance scorecard are separated in the process.

11BALANCE SCORECARD

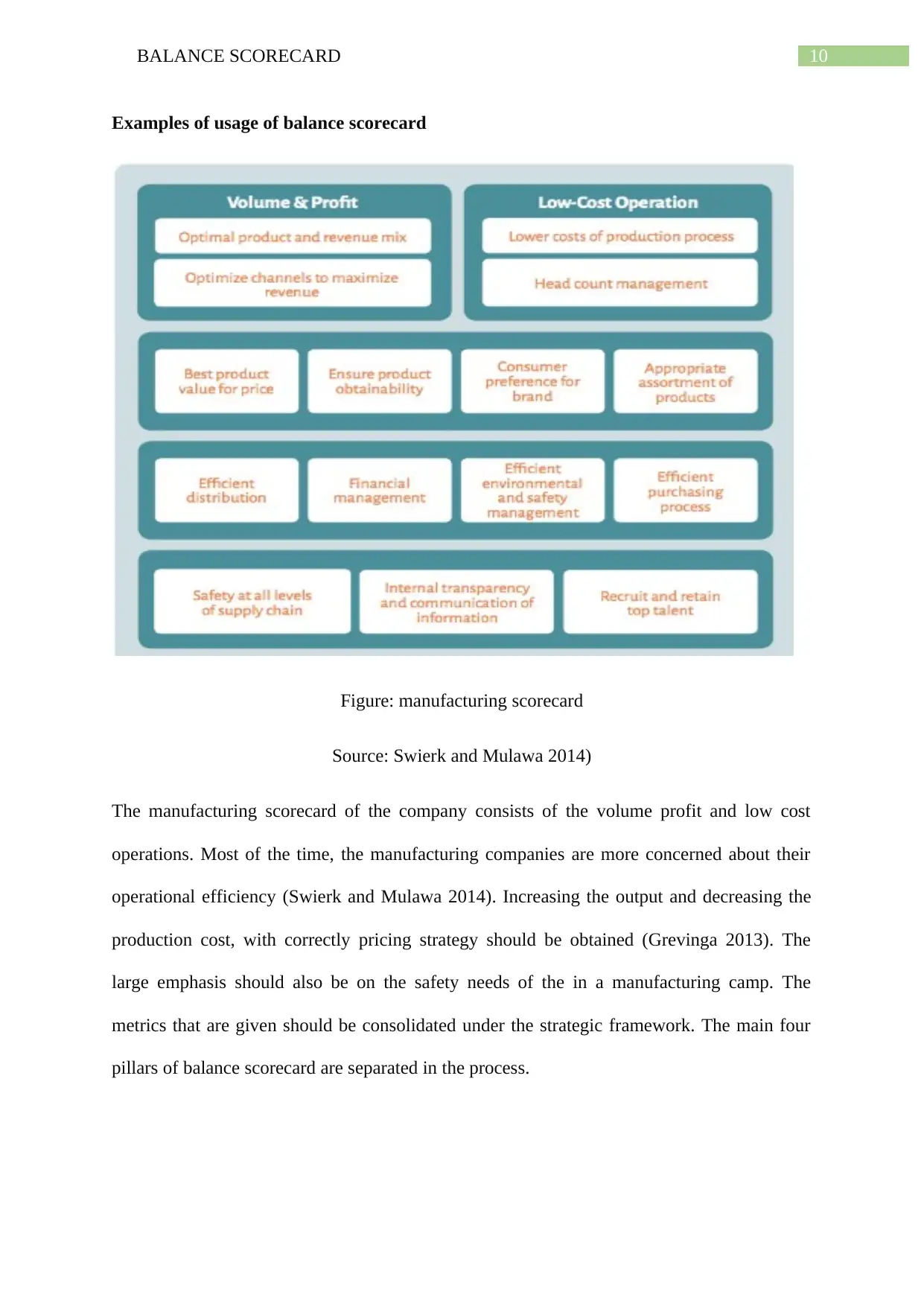

Figure: HR Balance score card

Source: (Poureisa et al. 2013).

An HR balance scorecard is given above that includes the financial perspectives of the

company. The main objective is to increase the profit and productivity per employee. At the

initial stage, there should be increase in the new hire, as that would increase the performance.

To alleviate the customer perspectives talent management and talent attraction strategy

should be increased as the structure suggests. The talent pool is essential to consider in the

Human resource management (Poureisa et al. 2013). The internal process the main aim is to

lowering the employee turnover by enhancing the work culture and work life balance. In the

fourth stage of learning and growth, aim is to maintain the ever-changing nature of

Figure: HR Balance score card

Source: (Poureisa et al. 2013).

An HR balance scorecard is given above that includes the financial perspectives of the

company. The main objective is to increase the profit and productivity per employee. At the

initial stage, there should be increase in the new hire, as that would increase the performance.

To alleviate the customer perspectives talent management and talent attraction strategy

should be increased as the structure suggests. The talent pool is essential to consider in the

Human resource management (Poureisa et al. 2013). The internal process the main aim is to

lowering the employee turnover by enhancing the work culture and work life balance. In the

fourth stage of learning and growth, aim is to maintain the ever-changing nature of

12BALANCE SCORECARD

organisation and incorporating that in the organisation. For the entire observed and identified

variable, the key performance indicators are decided.

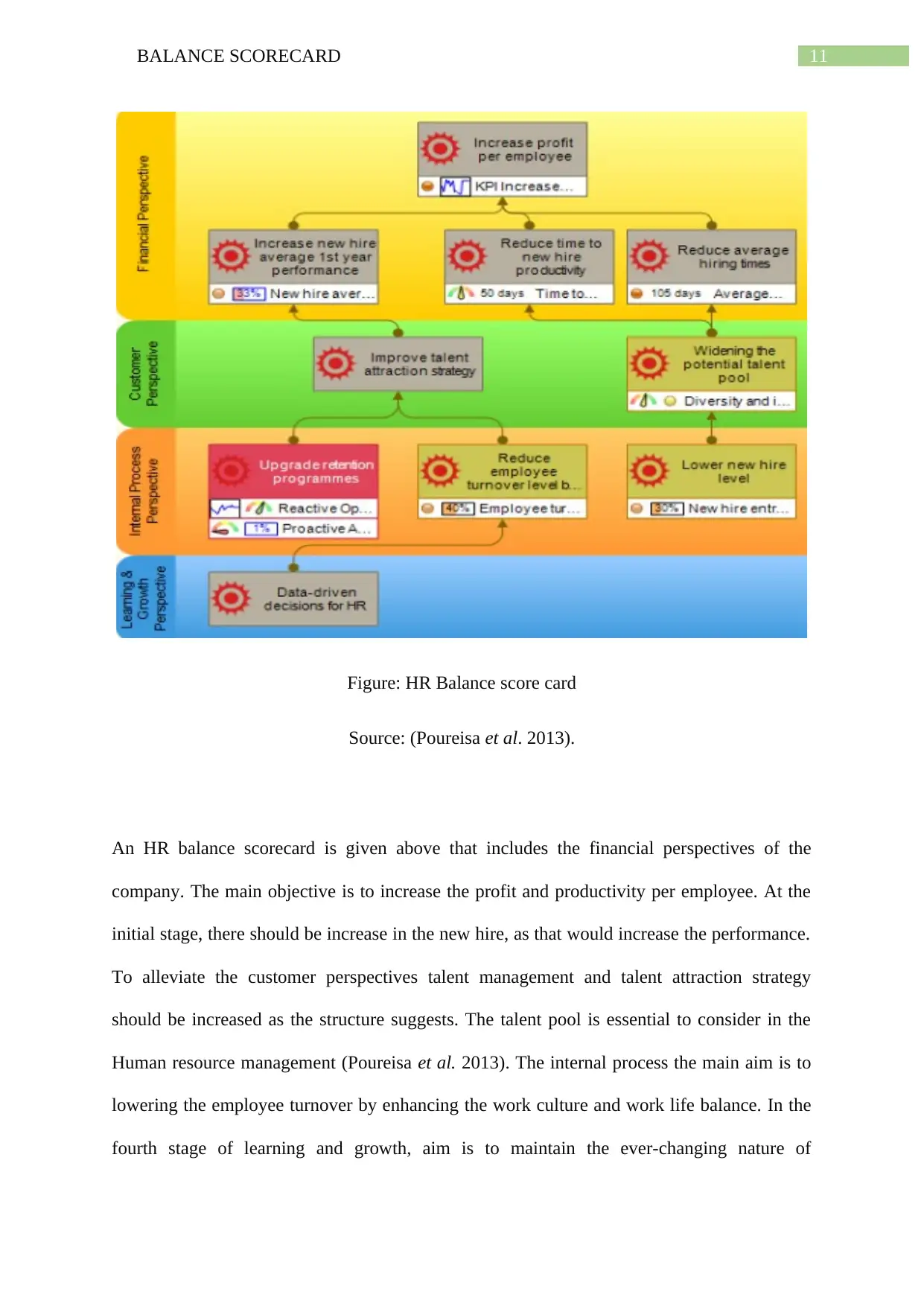

Figure: Generic Software industry scorecard

Source: (Swierk and Mulawa 2014)

In this, the internal perspectives are combined with the external need of the company. As this

customisation is very dependent on the services requirements of the product the it needs all

the Key Performance metrics to be incorporated in gaining market leadership, customer

relationship, Operational excellence (Swierk and Mulawa 2014).

organisation and incorporating that in the organisation. For the entire observed and identified

variable, the key performance indicators are decided.

Figure: Generic Software industry scorecard

Source: (Swierk and Mulawa 2014)

In this, the internal perspectives are combined with the external need of the company. As this

customisation is very dependent on the services requirements of the product the it needs all

the Key Performance metrics to be incorporated in gaining market leadership, customer

relationship, Operational excellence (Swierk and Mulawa 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BALANCE SCORECARD

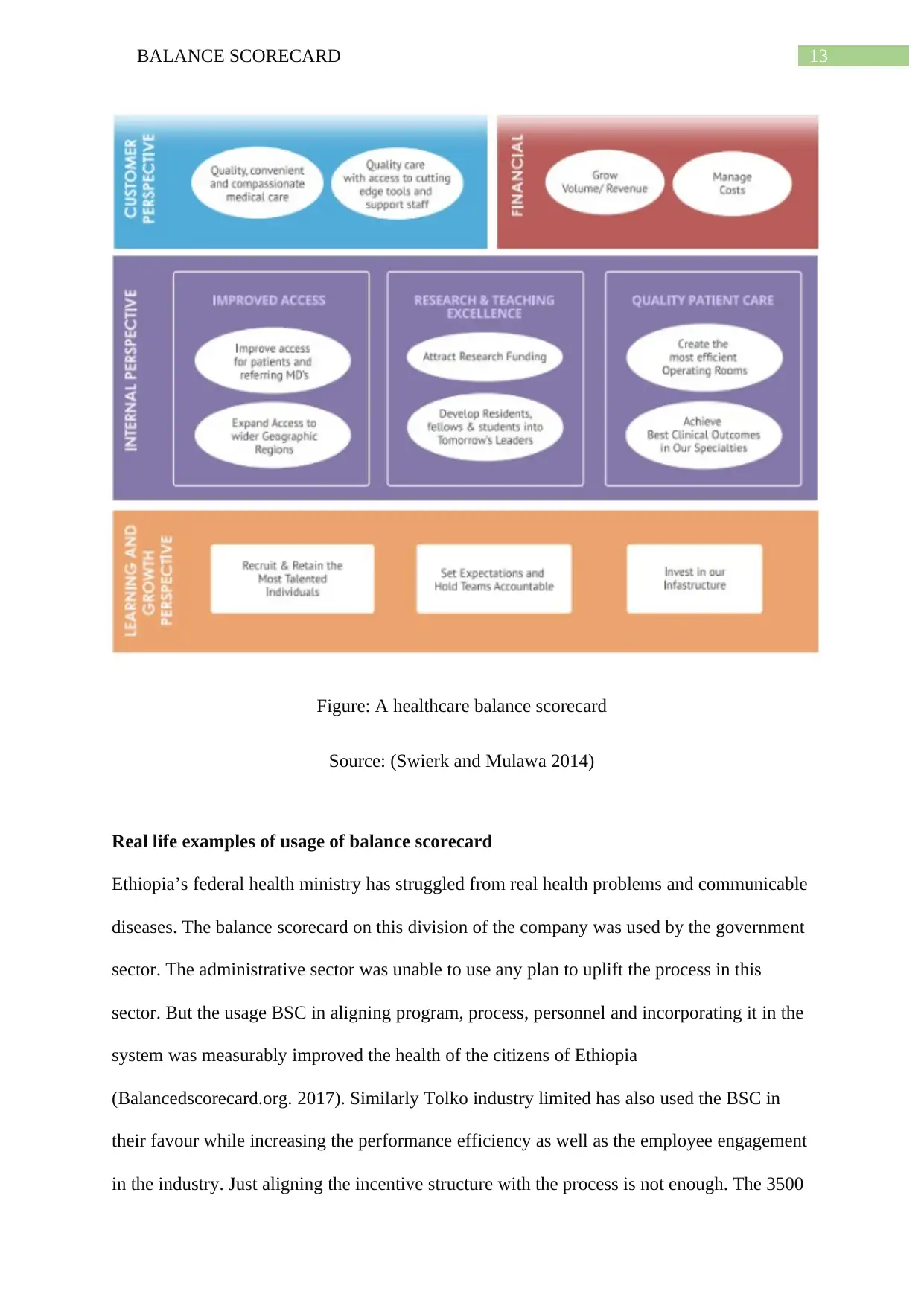

Figure: A healthcare balance scorecard

Source: (Swierk and Mulawa 2014)

Real life examples of usage of balance scorecard

Ethiopia’s federal health ministry has struggled from real health problems and communicable

diseases. The balance scorecard on this division of the company was used by the government

sector. The administrative sector was unable to use any plan to uplift the process in this

sector. But the usage BSC in aligning program, process, personnel and incorporating it in the

system was measurably improved the health of the citizens of Ethiopia

(Balancedscorecard.org. 2017). Similarly Tolko industry limited has also used the BSC in

their favour while increasing the performance efficiency as well as the employee engagement

in the industry. Just aligning the incentive structure with the process is not enough. The 3500

Figure: A healthcare balance scorecard

Source: (Swierk and Mulawa 2014)

Real life examples of usage of balance scorecard

Ethiopia’s federal health ministry has struggled from real health problems and communicable

diseases. The balance scorecard on this division of the company was used by the government

sector. The administrative sector was unable to use any plan to uplift the process in this

sector. But the usage BSC in aligning program, process, personnel and incorporating it in the

system was measurably improved the health of the citizens of Ethiopia

(Balancedscorecard.org. 2017). Similarly Tolko industry limited has also used the BSC in

their favour while increasing the performance efficiency as well as the employee engagement

in the industry. Just aligning the incentive structure with the process is not enough. The 3500

14BALANCE SCORECARD

employees of the company were engaged and made understand of the strategic plan and were

involved in the process which was only possible after the launch of balance scorecard and

nine step evaluation and monitoring of the process (Balancedscorecard.org. 2017).

Conclusion

Therefore, from the above the discussion it can be concluded that balance scorecard is one of

the most important tool for the company to check and measure the performance. The

changing environment and nature of organisation includes changing the method of viewing

success only in terms of profitability. The intangible factors must also be considered and

measured if possible to measure the success of the company. Balance scorecard helps in

reviewing process and incorporating all the contributing factor that makes the organisation

successful entity. Considering all the four factors and the secondary and primary key

performance indicators should also be incorporated in the balance scorecard’s identified

elements. As from the real life examples, it can be seen that this process has helped many

companies to identify their root cause of the problem and thus after evaluating and

implementing balance score card has helped them in solving strategic problems regarding the

four factors.

employees of the company were engaged and made understand of the strategic plan and were

involved in the process which was only possible after the launch of balance scorecard and

nine step evaluation and monitoring of the process (Balancedscorecard.org. 2017).

Conclusion

Therefore, from the above the discussion it can be concluded that balance scorecard is one of

the most important tool for the company to check and measure the performance. The

changing environment and nature of organisation includes changing the method of viewing

success only in terms of profitability. The intangible factors must also be considered and

measured if possible to measure the success of the company. Balance scorecard helps in

reviewing process and incorporating all the contributing factor that makes the organisation

successful entity. Considering all the four factors and the secondary and primary key

performance indicators should also be incorporated in the balance scorecard’s identified

elements. As from the real life examples, it can be seen that this process has helped many

companies to identify their root cause of the problem and thus after evaluating and

implementing balance score card has helped them in solving strategic problems regarding the

four factors.

15BALANCE SCORECARD

Reference

Awadallah, E., New Performance Measurement Models and Management Control Systems:

A Critique of the Literature.

Awadallah, E.A. and Allam, A., 2015. A critique of the balanced scorecard as a performance

measurement tool. International Journal of Business and Social Science, 6(7), pp.91-99.

Balancedscorecard.org. (2017). Balanced Scorecard Examples & Success Stories. [online]

Available at: http://www.balancedscorecard.org/BSC-Basics/Examples-Success-Stories

[Accessed 28 Nov. 2017].

Bhagwat, R. and Sharma, M.K., 2014. Performance measurement of supply chain

management: A balanced scorecard approach. Computers & Industrial Engineering, 53(1),

pp.43-62.

Boscia, M.W. and McAfee, R.B., 2014. Using the balance scorecard approach: A group

exercise. Developments in Business Simulation and Experiential Learning, 35.

Buller, P.F. and McEvoy, G.M., 2012. Strategy, human resource management and

performance: Sharpening line of sight. Human resource management review, 22(1), pp.43-

56.

Casey, W. and Peck, W., 2014. A balanced view of balanced scorecard. Executive Leadership

Group, White Paper: The Leadership Lighthouse Series.

Ciuzaite, E., 2012. Balanced scorecard development in Lithuanian companies: Cultural

implications, Balanced Scorecard development process framework and discussion on

interlink with employee incentive system (Doctoral dissertation, Thesis, University of Aarhus

Denmark).

Reference

Awadallah, E., New Performance Measurement Models and Management Control Systems:

A Critique of the Literature.

Awadallah, E.A. and Allam, A., 2015. A critique of the balanced scorecard as a performance

measurement tool. International Journal of Business and Social Science, 6(7), pp.91-99.

Balancedscorecard.org. (2017). Balanced Scorecard Examples & Success Stories. [online]

Available at: http://www.balancedscorecard.org/BSC-Basics/Examples-Success-Stories

[Accessed 28 Nov. 2017].

Bhagwat, R. and Sharma, M.K., 2014. Performance measurement of supply chain

management: A balanced scorecard approach. Computers & Industrial Engineering, 53(1),

pp.43-62.

Boscia, M.W. and McAfee, R.B., 2014. Using the balance scorecard approach: A group

exercise. Developments in Business Simulation and Experiential Learning, 35.

Buller, P.F. and McEvoy, G.M., 2012. Strategy, human resource management and

performance: Sharpening line of sight. Human resource management review, 22(1), pp.43-

56.

Casey, W. and Peck, W., 2014. A balanced view of balanced scorecard. Executive Leadership

Group, White Paper: The Leadership Lighthouse Series.

Ciuzaite, E., 2012. Balanced scorecard development in Lithuanian companies: Cultural

implications, Balanced Scorecard development process framework and discussion on

interlink with employee incentive system (Doctoral dissertation, Thesis, University of Aarhus

Denmark).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16BALANCE SCORECARD

Grevinga, K., 2013. Common measure bias in the balanced scorecard: an experiment with

undergraduate students(Master's thesis, University of Twente).

Kaplan, R.S. and Norton, D.P., 2012. The balanced scorecard: translating strategy into

action. Harvard Business Press.

Kurtzman, J. and Urresta, L.,2012. Is your company off course? Now you can find out

why. Fortune, 135(3), pp.128-130.

Madah, N.A., Ahmad, I.S. and Sultan, K., 2013. Building and Implementing a Balanced

Scorecard Model at Cihan University Requirements and Steps. Acad. of Contemp. Research

Journal, 2(III), pp.106-117.

Madsen, D.Ø. and Stenheim, T., 2014. Perceived benefits of balanced scorecard

implementation: some preliminary evidence.

Nørreklit, H. and Mitchell, F., 2014. Contemporary issues on the balance scorecard. Journal

of Accounting & Organizational Change, 10(4).

Nurhadi, D., 2016, October. Designing a balanced scorecard model to evaluate strategies of

engineering educational institution. In AIP Conference Proceedings (Vol. 1778, No. 1, p.

030031). AIP Publishing.

Pineno, C.J., 2013. Sustainability Reporting by Universities and Corporations: an Integrated

Approach or a Separate Category within the Balanced Scorecard. Journal of Business and

Accounting, 6(1), p.51.

Poureisa, A., Ahmadgourabi, M. and Efteghar, A., 2013. Balanced scorecard: A new tool for

performance evaluation. Interdisciplinary Journal of Contemporary Research in

Business, 5(1), pp.974-978.

Grevinga, K., 2013. Common measure bias in the balanced scorecard: an experiment with

undergraduate students(Master's thesis, University of Twente).

Kaplan, R.S. and Norton, D.P., 2012. The balanced scorecard: translating strategy into

action. Harvard Business Press.

Kurtzman, J. and Urresta, L.,2012. Is your company off course? Now you can find out

why. Fortune, 135(3), pp.128-130.

Madah, N.A., Ahmad, I.S. and Sultan, K., 2013. Building and Implementing a Balanced

Scorecard Model at Cihan University Requirements and Steps. Acad. of Contemp. Research

Journal, 2(III), pp.106-117.

Madsen, D.Ø. and Stenheim, T., 2014. Perceived benefits of balanced scorecard

implementation: some preliminary evidence.

Nørreklit, H. and Mitchell, F., 2014. Contemporary issues on the balance scorecard. Journal

of Accounting & Organizational Change, 10(4).

Nurhadi, D., 2016, October. Designing a balanced scorecard model to evaluate strategies of

engineering educational institution. In AIP Conference Proceedings (Vol. 1778, No. 1, p.

030031). AIP Publishing.

Pineno, C.J., 2013. Sustainability Reporting by Universities and Corporations: an Integrated

Approach or a Separate Category within the Balanced Scorecard. Journal of Business and

Accounting, 6(1), p.51.

Poureisa, A., Ahmadgourabi, M. and Efteghar, A., 2013. Balanced scorecard: A new tool for

performance evaluation. Interdisciplinary Journal of Contemporary Research in

Business, 5(1), pp.974-978.

17BALANCE SCORECARD

Rid, J., 2016. Efficiency and Effectiveness Differences between Organizations with Different

Ownership Status. An Outcome consideration.

Siddique, M.I. and Shadbolt, N., 2016. Strategy Implementation.

Swierk, J. and Mulawa, M., 2014. IT Balanced Scorecard as a Significant Component of

Competitive and Modern Company. In Management, Knowledge, and Learning International

Conference (pp. 822-825).

Rid, J., 2016. Efficiency and Effectiveness Differences between Organizations with Different

Ownership Status. An Outcome consideration.

Siddique, M.I. and Shadbolt, N., 2016. Strategy Implementation.

Swierk, J. and Mulawa, M., 2014. IT Balanced Scorecard as a Significant Component of

Competitive and Modern Company. In Management, Knowledge, and Learning International

Conference (pp. 822-825).

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.