Product and Process Improvement in a Bank: Improving Real-Time Feedback and Its Impact on Customer Satisfaction

VerifiedAdded on 2023/06/11

|13

|3213

|356

AI Summary

This study investigates the impact of product innovation, relationship management, customer feedback, turnaround time, and lining management on customer satisfaction in commercial banks. The study found that product innovation, relationship management, customer feedback, turnaround time, and lining management all have a positive impact on customer satisfaction. The study recommends that banks should frequently conduct customer satisfaction surveys to improve their services and products.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

PRODUCT AND PROCESS IMPROVEMENT IN A BANK

IMPROVING REAL-TIME FEEDBACK AND ITS IMPACT ON

CUSTOMER SATISFACTION

May 30, 2018

IMPROVING REAL-TIME FEEDBACK AND ITS IMPACT ON

CUSTOMER SATISFACTION

May 30, 2018

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ABSTRACT

The motivation behind this investigation was to build up inward factors influencing customer

satisfaction of business banks. This was accomplished by investigating the accompanying five

particular destinations: To decide the impact of business banks' item advancement on customer

satisfaction. Furthermore, to look at the impact of business banks' relationship administration on

customer satisfaction. Thirdly, is to discover the effect of business banks' customer criticism on

customer satisfaction. Fourthly, is to decide the impact of business banks' turnaround time on

customer satisfaction and to discover the impact of business banks' lining administration

framework on customer satisfaction. The investigation focused on an expected populace

comprising 650 dynamic customers.

Page 2 of 13

The motivation behind this investigation was to build up inward factors influencing customer

satisfaction of business banks. This was accomplished by investigating the accompanying five

particular destinations: To decide the impact of business banks' item advancement on customer

satisfaction. Furthermore, to look at the impact of business banks' relationship administration on

customer satisfaction. Thirdly, is to discover the effect of business banks' customer criticism on

customer satisfaction. Fourthly, is to decide the impact of business banks' turnaround time on

customer satisfaction and to discover the impact of business banks' lining administration

framework on customer satisfaction. The investigation focused on an expected populace

comprising 650 dynamic customers.

Page 2 of 13

Introduction

The most widely recognized method for measuring satisfaction is to look at the customer's view

of an affair, or some piece of it, with their desires. This is known as the desires disconfirmation

model of customer satisfaction. Utilizing this model, customer satisfaction can be sorted by level

of customer desire. This model proposes that if customers see their desires to be met, they are

fulfilled. In the event that their desires are failed to meet expectations, this is negative

disconfirmation, and they were disappointed. Through item development, organizations can

make profoundly fulfilled customers who are faithful to the association. This is valuable to the

association as the customers spread positive informal, basically, turning into a mobile talking

commercial for the firm. On the off chance that numerous charmed customers are spreading

positive informal correspondence, this at that point brings down the cost of advancement to draw

in new customers [1].

He additionally shows that profoundly fulfilled customers are more lenient than the unsatisfied

customers. It, consequently, interprets that the firm can once in a while goof and not lose

customers. Having very fulfilled customers at that point resembles having a protection strategy

against something turning out badly in the service experience. Essentially, customer satisfaction

can be viewed as a method for accomplishing business objectives and additionally being a

wellspring of reasonable upper hand or a competitive advantage [2].

Inside Elements

As indicated by Kaura [3], inward factors in a bank are factors inside the banking area which

impact the satisfaction of customers. The interior components prompting customer satisfaction in

a banking division incorporates; item offered by the bank, administration practices, customer

service, banks opening time, shutting time, the time taken to react to customers' objections and

Page 3 of 13

The most widely recognized method for measuring satisfaction is to look at the customer's view

of an affair, or some piece of it, with their desires. This is known as the desires disconfirmation

model of customer satisfaction. Utilizing this model, customer satisfaction can be sorted by level

of customer desire. This model proposes that if customers see their desires to be met, they are

fulfilled. In the event that their desires are failed to meet expectations, this is negative

disconfirmation, and they were disappointed. Through item development, organizations can

make profoundly fulfilled customers who are faithful to the association. This is valuable to the

association as the customers spread positive informal, basically, turning into a mobile talking

commercial for the firm. On the off chance that numerous charmed customers are spreading

positive informal correspondence, this at that point brings down the cost of advancement to draw

in new customers [1].

He additionally shows that profoundly fulfilled customers are more lenient than the unsatisfied

customers. It, consequently, interprets that the firm can once in a while goof and not lose

customers. Having very fulfilled customers at that point resembles having a protection strategy

against something turning out badly in the service experience. Essentially, customer satisfaction

can be viewed as a method for accomplishing business objectives and additionally being a

wellspring of reasonable upper hand or a competitive advantage [2].

Inside Elements

As indicated by Kaura [3], inward factors in a bank are factors inside the banking area which

impact the satisfaction of customers. The interior components prompting customer satisfaction in

a banking division incorporates; item offered by the bank, administration practices, customer

service, banks opening time, shutting time, the time taken to react to customers' objections and

Page 3 of 13

bank specialists state of mind towards customers. The significance of estimation of customer

satisfaction lies in the way that one key to customer maintenance is customer satisfaction. A

profoundly fulfilled customer by and large remains longer, purchases more as the organization

presents new items and services and redesigns existing items and services talks positively to

others about the organization give careful consideration to contending brands, offers item or

service thoughts to the organization, and costs less to serve than new customers on the grounds

that exchanges can wind up schedule. More prominent customer satisfaction has additionally

been connected to higher returns and speedier organization development [4].

The estimation of customer satisfaction isn't conceivable unless the elements prompting

customer satisfaction are resolved. There are both outer and inside variables. Outer variables are

those elements from outside the bank that influences customer satisfaction. Inner components are

those variables or impacting frameworks from and inside the bank; that somehow influence

customer satisfaction. There are different classes of those elements. Cases are item development

practices, relationship administration practices, customer input dealing with, banks' turnaround

time and line administration framework.

Item development practices are presently a need for directors of numerous business banking

associations and it is a driver of execution and a key of development as associations in this

industry work in a to a great degree aggressive and dynamic condition. There are numerous types

of banking advancements in the banking area which incorporate relationship banking, robotized

teller machines, phone banking, web banking, branch organizing, electronic assets exchange and

continuous (real-time) gross settlement framework [5].

Page 4 of 13

satisfaction lies in the way that one key to customer maintenance is customer satisfaction. A

profoundly fulfilled customer by and large remains longer, purchases more as the organization

presents new items and services and redesigns existing items and services talks positively to

others about the organization give careful consideration to contending brands, offers item or

service thoughts to the organization, and costs less to serve than new customers on the grounds

that exchanges can wind up schedule. More prominent customer satisfaction has additionally

been connected to higher returns and speedier organization development [4].

The estimation of customer satisfaction isn't conceivable unless the elements prompting

customer satisfaction are resolved. There are both outer and inside variables. Outer variables are

those elements from outside the bank that influences customer satisfaction. Inner components are

those variables or impacting frameworks from and inside the bank; that somehow influence

customer satisfaction. There are different classes of those elements. Cases are item development

practices, relationship administration practices, customer input dealing with, banks' turnaround

time and line administration framework.

Item development practices are presently a need for directors of numerous business banking

associations and it is a driver of execution and a key of development as associations in this

industry work in a to a great degree aggressive and dynamic condition. There are numerous types

of banking advancements in the banking area which incorporate relationship banking, robotized

teller machines, phone banking, web banking, branch organizing, electronic assets exchange and

continuous (real-time) gross settlement framework [5].

Page 4 of 13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Literature Review

A huge level of customer satisfaction is among the most basic pointers of the business' future.

Customers who are fulfilled are additionally faithful, and this guarantees a reliable income for

the undertaking later on. Also, fulfilled customers are regularly portrayed as not as price

sensitive as new clients, and they will probably spend more on getting items they have attempted

and tried previously. In addition, security in business relations is additionally gainful where the

positive quality picture limits the cost for a present customer. As indicated by Luciano et al [6],

satisfaction alludes to an inclination or a fleeting state of mind that can change inferable from

different conditions. It exists in the client's brain and is dissimilar to recognizable practices like

item decision, affirmations or repurchase [7].

In a related report, Mungányi [8] researched the connection that exists between the desires, real

execution, and the satisfaction. The discoveries built up that when a customer judges the

execution of an item, he, for the most part, thinks about an arrangement of execution results. The

item is then liable to be considered as dissatisfactory or tasteful. Item advancements are seen as

the "motor" driving the monetary framework towards achieving its objective of improving the

execution of what market analysts call the "genuine economy".

McDonald and Rundle-Thiele [9] refers to the US national home loan market, the advancement

of worldwide markets for money related subsidiaries and the development of shared reserve and

venture businesses as cases where developments have created huge benefits of social well-being.

Item advancements including subordinates can enhance effectiveness by extending open doors

for chance sharing, bringing down exchange expenses and decreasing unbalanced data and office

Page 5 of 13

A huge level of customer satisfaction is among the most basic pointers of the business' future.

Customers who are fulfilled are additionally faithful, and this guarantees a reliable income for

the undertaking later on. Also, fulfilled customers are regularly portrayed as not as price

sensitive as new clients, and they will probably spend more on getting items they have attempted

and tried previously. In addition, security in business relations is additionally gainful where the

positive quality picture limits the cost for a present customer. As indicated by Luciano et al [6],

satisfaction alludes to an inclination or a fleeting state of mind that can change inferable from

different conditions. It exists in the client's brain and is dissimilar to recognizable practices like

item decision, affirmations or repurchase [7].

In a related report, Mungányi [8] researched the connection that exists between the desires, real

execution, and the satisfaction. The discoveries built up that when a customer judges the

execution of an item, he, for the most part, thinks about an arrangement of execution results. The

item is then liable to be considered as dissatisfactory or tasteful. Item advancements are seen as

the "motor" driving the monetary framework towards achieving its objective of improving the

execution of what market analysts call the "genuine economy".

McDonald and Rundle-Thiele [9] refers to the US national home loan market, the advancement

of worldwide markets for money related subsidiaries and the development of shared reserve and

venture businesses as cases where developments have created huge benefits of social well-being.

Item advancements including subordinates can enhance effectiveness by extending open doors

for chance sharing, bringing down exchange expenses and decreasing unbalanced data and office

Page 5 of 13

costs. Item advancements advance monetary development by dispensing capital where it can be

generally profitable [10].

Petr, Jiri and Maria [11] called attention to that advancements enable markets to make particular

home loan contracts and to exchange dangers, and item developments have plainly profited

purchasers by driving down expenses. They brought up that since 1985; introductory expenses

for customary home loan advances have tumbled from approximately 2.5% of advance adjust to

around 0.5%. Furthermore, a mix of legitimate and item advancements has acquired a major

increment of the number of players in the home loan showcase, including intermediaries,

guarantors, and servicer agencies and rating organizations. Another favorable position noted by

the researcher was a decision. A couple of decades back, individuals were offered maybe a

couple diverse home loan items, yet now they can look over various instruments and payback

structures. Ultimately, customers gain from quicker advances choices [12].

Raza, Jawaid and Hassan [12] recognized trust as a fundamental component in keeping up and

upgrading the connection between a purchaser and a dealer. Trust can be built up through the

trading of data, proactive determination of grumblings and clashes, uprightness and unwavering

quality. Without a doubt, relationship advertising looks to set up and fortify collaboration

between an association and its customers by building an everlasting bond with them. The general

goal is to increment long-haul deals despite the fact that it likewise encourages item or service

repositioning, grabs customers from rivalry and helps with propelling new items or services. The

foremost reason for relationship showcasing is to set up, keep up, and upgrade the association

with customers that are beneficial. Consequently, it is imperative for relationship directors to

investigate the best relationship, which is justified regardless of the exertion, yet how to

distinguish the best relationship is the outside layer of the issue.

Page 6 of 13

generally profitable [10].

Petr, Jiri and Maria [11] called attention to that advancements enable markets to make particular

home loan contracts and to exchange dangers, and item developments have plainly profited

purchasers by driving down expenses. They brought up that since 1985; introductory expenses

for customary home loan advances have tumbled from approximately 2.5% of advance adjust to

around 0.5%. Furthermore, a mix of legitimate and item advancements has acquired a major

increment of the number of players in the home loan showcase, including intermediaries,

guarantors, and servicer agencies and rating organizations. Another favorable position noted by

the researcher was a decision. A couple of decades back, individuals were offered maybe a

couple diverse home loan items, yet now they can look over various instruments and payback

structures. Ultimately, customers gain from quicker advances choices [12].

Raza, Jawaid and Hassan [12] recognized trust as a fundamental component in keeping up and

upgrading the connection between a purchaser and a dealer. Trust can be built up through the

trading of data, proactive determination of grumblings and clashes, uprightness and unwavering

quality. Without a doubt, relationship advertising looks to set up and fortify collaboration

between an association and its customers by building an everlasting bond with them. The general

goal is to increment long-haul deals despite the fact that it likewise encourages item or service

repositioning, grabs customers from rivalry and helps with propelling new items or services. The

foremost reason for relationship showcasing is to set up, keep up, and upgrade the association

with customers that are beneficial. Consequently, it is imperative for relationship directors to

investigate the best relationship, which is justified regardless of the exertion, yet how to

distinguish the best relationship is the outside layer of the issue.

Page 6 of 13

Understanding the idea of the service one gives to customers permits to an energy about how the

customers see the services gave. As indicated by Rostami, Valmohammadi & Yousefpoo [13], in

any customer service cooperation, the view of customers is essential to one's capacity to

guarantee that they are satisfied past desire. This gives customers not what is evident but rather

additionally satisfy a large number of more subtle customer needs.

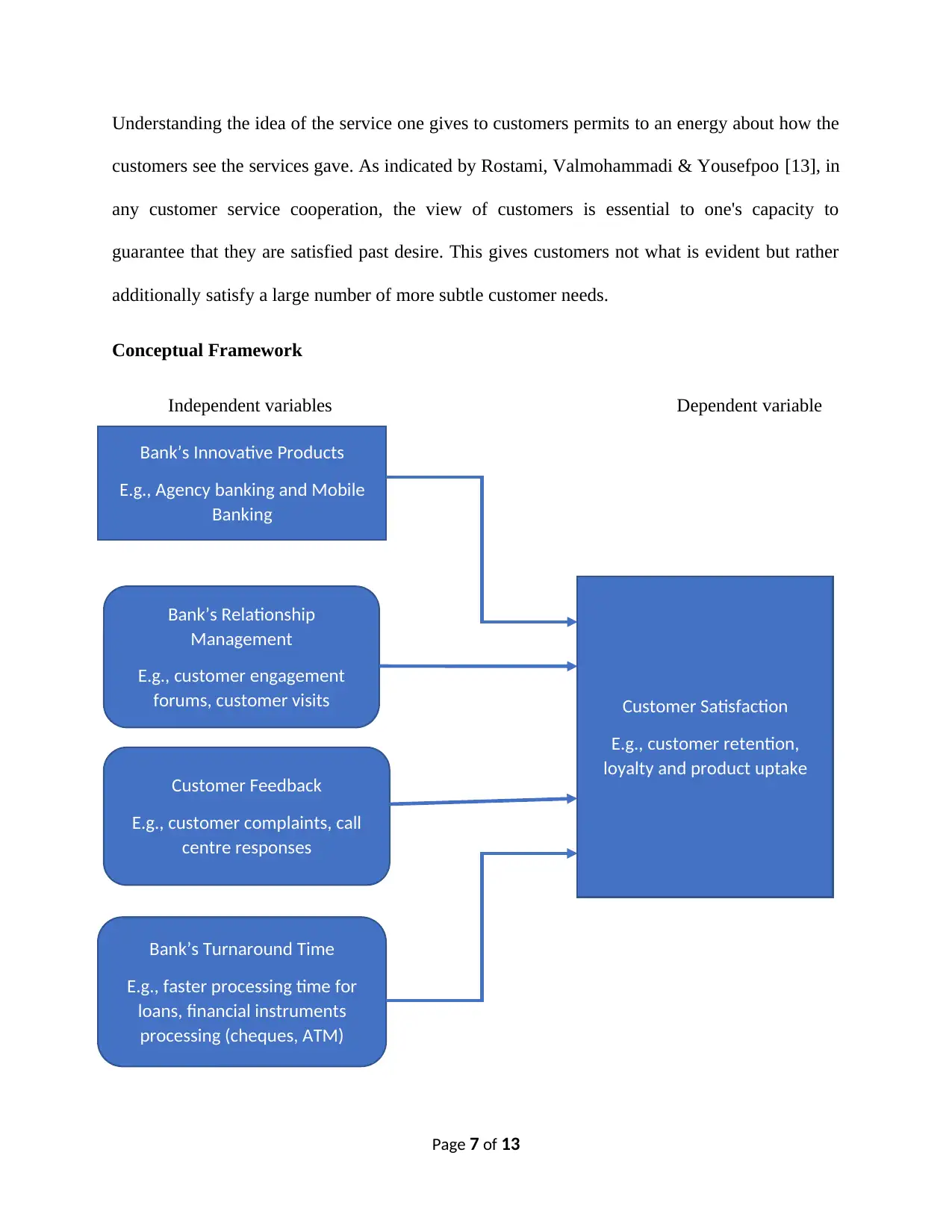

Conceptual Framework

Independent variables Dependent variable

Page 7 of 13

Bank’s Innovative Products

E.g., Agency banking and Mobile

Banking

Bank’s Relationship

Management

E.g., customer engagement

forums, customer visits

Customer Feedback

E.g., customer complaints, call

centre responses

Bank’s Turnaround Time

E.g., faster processing time for

loans, financial instruments

processing (cheques, ATM)

Customer Satisfaction

E.g., customer retention,

loyalty and product uptake

customers see the services gave. As indicated by Rostami, Valmohammadi & Yousefpoo [13], in

any customer service cooperation, the view of customers is essential to one's capacity to

guarantee that they are satisfied past desire. This gives customers not what is evident but rather

additionally satisfy a large number of more subtle customer needs.

Conceptual Framework

Independent variables Dependent variable

Page 7 of 13

Bank’s Innovative Products

E.g., Agency banking and Mobile

Banking

Bank’s Relationship

Management

E.g., customer engagement

forums, customer visits

Customer Feedback

E.g., customer complaints, call

centre responses

Bank’s Turnaround Time

E.g., faster processing time for

loans, financial instruments

processing (cheques, ATM)

Customer Satisfaction

E.g., customer retention,

loyalty and product uptake

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per Zeinalizadeh, Shojaie & Shariatmadari [14], the present banking industry has been

changed into an overcomplicated one. Throughout the last few of years, the monetary

organizations have grown quickly by acquisitions and mergers without a full usage of the

common services. The utilization of shared services incorporates a mix of new items, procedures,

and frameworks. The progress has prompted complex grid associations, and in addition, a wide

and modern item offering that is serviced by a grouping of incongruent data innovation (IT)

frameworks. Moreover, the banking business has made considerable interests in elective

circulation channels without a critical increment in value from its systems.

Turnaround time may not be plausible under a few conditions. In different settings, the

association may do not have the abilities or assets to execute suitable turnaround time accurately.

Regardless of whether connected accurately, in an appropriate setting, the hierarchical result of a

turnaround time still relies upon emanant factors, (for example, rivalry), which can avert or delay

in turnaround time. Components that impact the turnaround time incorporate seriousness of the

troubled state, firm size and free assets accessible.

Improvement of Waiting times in a Bank Branches

The rearrangements in getting service which will prompt lining are the typical issues in certain

conditions and even in regular day to day existence circumstances. The essential highlights of a

standard queuing framework comprised of the structure of the line, gatherings of interest, entry

and service procedures, and train of the line. In on-location service associations, for example,

banks, the failure to streamline the ability of the service will bring about long lines.

Consequently, the acknowledgment and comprehension of the client’s request and what the

client inclines toward is the underlying advance for the change of the service capacity.

Page 8 of 13

changed into an overcomplicated one. Throughout the last few of years, the monetary

organizations have grown quickly by acquisitions and mergers without a full usage of the

common services. The utilization of shared services incorporates a mix of new items, procedures,

and frameworks. The progress has prompted complex grid associations, and in addition, a wide

and modern item offering that is serviced by a grouping of incongruent data innovation (IT)

frameworks. Moreover, the banking business has made considerable interests in elective

circulation channels without a critical increment in value from its systems.

Turnaround time may not be plausible under a few conditions. In different settings, the

association may do not have the abilities or assets to execute suitable turnaround time accurately.

Regardless of whether connected accurately, in an appropriate setting, the hierarchical result of a

turnaround time still relies upon emanant factors, (for example, rivalry), which can avert or delay

in turnaround time. Components that impact the turnaround time incorporate seriousness of the

troubled state, firm size and free assets accessible.

Improvement of Waiting times in a Bank Branches

The rearrangements in getting service which will prompt lining are the typical issues in certain

conditions and even in regular day to day existence circumstances. The essential highlights of a

standard queuing framework comprised of the structure of the line, gatherings of interest, entry

and service procedures, and train of the line. In on-location service associations, for example,

banks, the failure to streamline the ability of the service will bring about long lines.

Consequently, the acknowledgment and comprehension of the client’s request and what the

client inclines toward is the underlying advance for the change of the service capacity.

Page 8 of 13

Banks, specifically, give careful consideration to service quality as the most critical capability. In

this manner, diverse methodologies have been connected with a specific end goal to enhance

service quality and consumer loyalty in the banking business. For example, Alhemoud [1]

received specialist recreation to decide the ideal asset setup of a bank, as concerns cost and

consumer loyalty. In a comparative report, he connected recreation to locate the best option as

far as lessening the service time of banks' counters considering the use rate of counters.

In any case, Luciano, Federica and Luisa [6] utilized reproduction for considering delays in an

arrangement of lines with associated service time at every hub, where service time for every

client at the principal hub is an irregular variable and the sequential service times are related with

the one at the main hub. Likewise, Kumar [4] attempted to propose a reproduction display, in

which some bank teller administration approaches were connected to accomplish the coveted

level of service quality. In other distinctive examinations, he connected the six-sigma system

with DMAIC ventures in banking services, going for upgrading service quality. Moreover, some

different researchers endeavored to fuse modern building strategies to enhance the service nature

of banks.

Future work

This inquiry demonstrates that a unit change in turnaround time will prompt a positive change in

customer satisfaction and that turnaround time has the best commitment to the model. Likewise,

a unit changes in customers lining administration will prompt a huge change in customer

satisfaction. A unit change in item relationship administration will prompt an adjustment in

customer satisfaction fundamentally. Similarly, a unit change in customer's criticism will bring

Page 9 of 13

this manner, diverse methodologies have been connected with a specific end goal to enhance

service quality and consumer loyalty in the banking business. For example, Alhemoud [1]

received specialist recreation to decide the ideal asset setup of a bank, as concerns cost and

consumer loyalty. In a comparative report, he connected recreation to locate the best option as

far as lessening the service time of banks' counters considering the use rate of counters.

In any case, Luciano, Federica and Luisa [6] utilized reproduction for considering delays in an

arrangement of lines with associated service time at every hub, where service time for every

client at the principal hub is an irregular variable and the sequential service times are related with

the one at the main hub. Likewise, Kumar [4] attempted to propose a reproduction display, in

which some bank teller administration approaches were connected to accomplish the coveted

level of service quality. In other distinctive examinations, he connected the six-sigma system

with DMAIC ventures in banking services, going for upgrading service quality. Moreover, some

different researchers endeavored to fuse modern building strategies to enhance the service nature

of banks.

Future work

This inquiry demonstrates that a unit change in turnaround time will prompt a positive change in

customer satisfaction and that turnaround time has the best commitment to the model. Likewise,

a unit changes in customers lining administration will prompt a huge change in customer

satisfaction. A unit change in item relationship administration will prompt an adjustment in

customer satisfaction fundamentally. Similarly, a unit change in customer's criticism will bring

Page 9 of 13

about a positive change in customer satisfaction while a unit change in item advancement will

prompt a positive change in customer satisfaction.

In view of the discoveries of this investigation, the expert finished up the accompanying: There

is a positive connection between banks' item development and customer' satisfaction. The banks'

item development fundamentally impacts customer satisfaction. This is on account of customers

need to grasp the utilization of new innovation which is brought by advancements. The banks'

relationship administration fundamentally impacts customer satisfaction. Customer’s input

fundamentally impacts the overall customer' satisfaction and that there is a positive banks

connection between customer' satisfaction. There is a positive connection between business

banks' turnaround time and customer satisfaction, also there is a positive connection between

business banks' line administration and customer satisfaction.

Banks ought to much of the time do customer satisfaction overviews to discover the feelings of

its customers. Their criticism can be utilized to enhance services and items advertised. They

ought to likewise enhance its turnaround time as this will help abbreviate lines and sitting tight

time for customers. Moreover, banks ought to shorten the time that it takes to settle on choices

on customer demands. This should be possible by enhancing the frameworks that are being used

or through rebuilding to dispose of what isn't required. The general goal of this investigation was

to discover the interior variables influencing customer satisfaction of commercial banks.

Additionally, research should be possible on the elements affecting banks development, factors

impacting the relationship administration, factors affecting turnaround time and outside elements

affecting customers' satisfaction.

Page 10 of 13

prompt a positive change in customer satisfaction.

In view of the discoveries of this investigation, the expert finished up the accompanying: There

is a positive connection between banks' item development and customer' satisfaction. The banks'

item development fundamentally impacts customer satisfaction. This is on account of customers

need to grasp the utilization of new innovation which is brought by advancements. The banks'

relationship administration fundamentally impacts customer satisfaction. Customer’s input

fundamentally impacts the overall customer' satisfaction and that there is a positive banks

connection between customer' satisfaction. There is a positive connection between business

banks' turnaround time and customer satisfaction, also there is a positive connection between

business banks' line administration and customer satisfaction.

Banks ought to much of the time do customer satisfaction overviews to discover the feelings of

its customers. Their criticism can be utilized to enhance services and items advertised. They

ought to likewise enhance its turnaround time as this will help abbreviate lines and sitting tight

time for customers. Moreover, banks ought to shorten the time that it takes to settle on choices

on customer demands. This should be possible by enhancing the frameworks that are being used

or through rebuilding to dispose of what isn't required. The general goal of this investigation was

to discover the interior variables influencing customer satisfaction of commercial banks.

Additionally, research should be possible on the elements affecting banks development, factors

impacting the relationship administration, factors affecting turnaround time and outside elements

affecting customers' satisfaction.

Page 10 of 13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page 11 of 13

References

[1] A. M. Alhemoud, "Banking in Kuwait: a customer satisfaction case study," Competitiveness Review:

An International Business Journal, vol. 20, no. 4, pp. 333-342, 2010.

[2] Dauda S.Y. & Lee J., "Quality of service and customer satisfaction: a conjoint analysis for the

Nigerian bank customers," International Journal of Bank Marketing, vol. 34, no. 6, pp. 841-867,

2016.

[3] V. Kaura, "Antecedents of customer satisfaction: a study of Indian public and private sector banks,"

International Journal of Bank Marketing, vol. 31, no. 3, pp. 167-186, 2013.

[4] V. Kumar, "Introduction: Is Customer Satisfaction (Ir)relevant as a Metric?. Journal of Marketing,"

Journal of Marketing, vol. 80, no. 5, pp. 108-109, 2016.

[5] Lin F.H, Tsai S.B, Lee Y.C, Hsiao C.F, Zhou J., Wang J. & Shang Z., "Empirical research on Kano’s

model and customer satisfaction," PLOS ONE, vol. 12, no. 9, pp. 1-22, 2017.

[6] Luciano M., Federica I. & Luisa B., "Customer Satisfaction Management in Italian Banks,"

Qualitative Research in Financial Markets, vol. 5, no. 2, pp. 139-160, 2013.

[7] Lundahl N., Vegholm F. & Silver L., "Technical and functional determinants of customer satisfaction

in the bank SME relationship,"‐ Managing Service Quality: An International Journal, vol. 19, no. 5,

pp. 581-594, 2009.

[8] Mang’unyi E.E., Khabala O.T & Govender K.K., "Bank customer loyalty and satisfaction: the

influence of virtual e-CRM," African Journal of Economic and Management Studies, vol. 9, no. 2, pp.

250-265, 2018.

[9] McDonald L.M. & Rundle Thiele S., "Corporate social responsibility and bank customer satisfaction:‐

A research agenda," International Journal of Bank Marketing, vol. 26, no. 3, pp. 170-182, 2008.

[10] Muhammad I., Shamsudin F. S. & Ul Hadi N., "How Important Is Customer Satisfaction?

Quantitative Evidence from Mobile Telecommunication Market," International Journal of Business

and Management, vol. 11, no. 6, pp. 57-69, 2016.

[11] Petr S., Jiří R., & Maria K., "Customer Satisfaction, Product Quality and Performance of Companies,"

Review of Economic Perspectives, vol. 14, no. 4, pp. 329-344, 2014.

[12] Raza S.A., Jawaid S.T. & Hassan A., "Internet banking and customer satisfaction in Pakistan,"

Qualitative Research in Financial Markets, vol. 7, no. 1, pp. 24-36, 2015.

[13] Rostami A.R., Valmohammadi C. & Yousefpoo J., "The relationship between customer satisfaction

and customer relationship management system; a case study of Ghavamin Bank," Industrial and

Commercial Training, vol. 46, no. 4, pp. 220-227, 2014.

Page 12 of 13

[1] A. M. Alhemoud, "Banking in Kuwait: a customer satisfaction case study," Competitiveness Review:

An International Business Journal, vol. 20, no. 4, pp. 333-342, 2010.

[2] Dauda S.Y. & Lee J., "Quality of service and customer satisfaction: a conjoint analysis for the

Nigerian bank customers," International Journal of Bank Marketing, vol. 34, no. 6, pp. 841-867,

2016.

[3] V. Kaura, "Antecedents of customer satisfaction: a study of Indian public and private sector banks,"

International Journal of Bank Marketing, vol. 31, no. 3, pp. 167-186, 2013.

[4] V. Kumar, "Introduction: Is Customer Satisfaction (Ir)relevant as a Metric?. Journal of Marketing,"

Journal of Marketing, vol. 80, no. 5, pp. 108-109, 2016.

[5] Lin F.H, Tsai S.B, Lee Y.C, Hsiao C.F, Zhou J., Wang J. & Shang Z., "Empirical research on Kano’s

model and customer satisfaction," PLOS ONE, vol. 12, no. 9, pp. 1-22, 2017.

[6] Luciano M., Federica I. & Luisa B., "Customer Satisfaction Management in Italian Banks,"

Qualitative Research in Financial Markets, vol. 5, no. 2, pp. 139-160, 2013.

[7] Lundahl N., Vegholm F. & Silver L., "Technical and functional determinants of customer satisfaction

in the bank SME relationship,"‐ Managing Service Quality: An International Journal, vol. 19, no. 5,

pp. 581-594, 2009.

[8] Mang’unyi E.E., Khabala O.T & Govender K.K., "Bank customer loyalty and satisfaction: the

influence of virtual e-CRM," African Journal of Economic and Management Studies, vol. 9, no. 2, pp.

250-265, 2018.

[9] McDonald L.M. & Rundle Thiele S., "Corporate social responsibility and bank customer satisfaction:‐

A research agenda," International Journal of Bank Marketing, vol. 26, no. 3, pp. 170-182, 2008.

[10] Muhammad I., Shamsudin F. S. & Ul Hadi N., "How Important Is Customer Satisfaction?

Quantitative Evidence from Mobile Telecommunication Market," International Journal of Business

and Management, vol. 11, no. 6, pp. 57-69, 2016.

[11] Petr S., Jiří R., & Maria K., "Customer Satisfaction, Product Quality and Performance of Companies,"

Review of Economic Perspectives, vol. 14, no. 4, pp. 329-344, 2014.

[12] Raza S.A., Jawaid S.T. & Hassan A., "Internet banking and customer satisfaction in Pakistan,"

Qualitative Research in Financial Markets, vol. 7, no. 1, pp. 24-36, 2015.

[13] Rostami A.R., Valmohammadi C. & Yousefpoo J., "The relationship between customer satisfaction

and customer relationship management system; a case study of Ghavamin Bank," Industrial and

Commercial Training, vol. 46, no. 4, pp. 220-227, 2014.

Page 12 of 13

[14] Zeinalizadeh N., Shojaie A.A & Shariatmadari M., "Modeling and analysis of bank customer

satisfaction using neural networks approach," International Journal of Bank Marketing, vol. 33, no.

6, pp. 717-732, 2015.

Page 13 of 13

satisfaction using neural networks approach," International Journal of Bank Marketing, vol. 33, no.

6, pp. 717-732, 2015.

Page 13 of 13

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.