Economics of Banking & Finance: OCBC Bank Financial Case Study

VerifiedAdded on 2023/06/15

|14

|4810

|228

Case Study

AI Summary

This case study examines OCBC Bank's role in Singapore's financial system, focusing on brokerage services and asset transformation. It critically evaluates the problems associated with relying on debt finance for financial surplus and deficit units, highlighting issues like maturity mismatch and credit risk exposure. The study also analyzes the impact of Basel III's capital adequacy, liquidity, and leverage requirements on OCBC, demonstrating the bank's adherence to these regulations. Furthermore, it discusses the processes of asset securitization and the implications of the global financial crisis on OCBC's financial performance, referencing OCBC's annual reports and IMF studies to support its findings. Desklib offers a wide range of solved assignments and past papers for students.

Running head: ECONOMICS OF BANKING AND FINANCE

Economics of Banking and Finance

Name of Student:

Name of University:

Author’s Note:

Economics of Banking and Finance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS OF BANKING AND FINANCE

Table of Contents

Two key roles of the bank in terms of its contributions to country’s financial system...................2

Critical Evaluation of problem with relying on debt finance for financial surplus unit and

financial deficit unit.........................................................................................................................4

Changes to the capital adequacy, liquidity and leverage requirements as stipulated by Basel III

and its impact on OCBC..................................................................................................................5

Processes of asset securitization......................................................................................................8

Implications of the global financial crisis on the bank’s financial performances.........................10

References......................................................................................................................................12

Table of Contents

Two key roles of the bank in terms of its contributions to country’s financial system...................2

Critical Evaluation of problem with relying on debt finance for financial surplus unit and

financial deficit unit.........................................................................................................................4

Changes to the capital adequacy, liquidity and leverage requirements as stipulated by Basel III

and its impact on OCBC..................................................................................................................5

Processes of asset securitization......................................................................................................8

Implications of the global financial crisis on the bank’s financial performances.........................10

References......................................................................................................................................12

2ECONOMICS OF BANKING AND FINANCE

Two key roles of the bank in terms of its contributions to country’s financial system

The developmental activities of a country are dependent on its economic growth which is

attained over a certain period. The economic growth considers the investment and the production

to the extent which illustrates that the investment and production is to the extent of GDP in a

country. This leads to improvement in the overall standard of living and economic development.

The two key contributions of the banks in terms of the financial system are stated below as

follows:

1. Brokerage Services - Banking assists in investing in listed securities in the capital market.

These services are discerned to be provided in accordance with registered financial

advisors who are able to provide a high level of professional assistance to their clients. In

the recent times, banking service is able to determine the long-term and short-term

financial goals along with risk tolerance limit. It is also able to examine the most suitable

alternative investments which might help in reaching the desired goal and execute trades

(Webb and Martin 2017). OCBC securities is considered as one of the first brokerage

service in Singapore to introduce “OCBC OneTouch on their iOCBC TradeMobile” app

for both Android and iPhone which enabled the users to evaluate their stock portfolio.

The bank took noteworthy initiative to launch app named Apple Watch. This service was

able to provide important “account information via wrist devices”. The bank is able to

make significant contribution to the financial system with continuous engagement with

prospective customers to initiate cross selling of the brokerage services. In addition to

this, OCBC launched “StockReports+ in September 2016”, which aggregates

independent research done by the brokers and provide quantitative analysis for the stocks

in “Singapore, Hong Kong, United States and Malaysia markets”. OCBC expanded the

contribution of brokerage services to the financial system by enabling trading on the

“Shenzhen ‘A’ market after the launch of the Shenzhen-Hong Kong Stock Connect in

November 2016”. This allowed the existing customers to trade over 15 global exchange

online (Ocbc.com. 2018). Some of the other brokerage services are identified in form of

providing opportunity to earn income on unvested cash in the brokerage account with

bank deposit program thereby assisting in dividend reinvestment plan, periodic

Two key roles of the bank in terms of its contributions to country’s financial system

The developmental activities of a country are dependent on its economic growth which is

attained over a certain period. The economic growth considers the investment and the production

to the extent which illustrates that the investment and production is to the extent of GDP in a

country. This leads to improvement in the overall standard of living and economic development.

The two key contributions of the banks in terms of the financial system are stated below as

follows:

1. Brokerage Services - Banking assists in investing in listed securities in the capital market.

These services are discerned to be provided in accordance with registered financial

advisors who are able to provide a high level of professional assistance to their clients. In

the recent times, banking service is able to determine the long-term and short-term

financial goals along with risk tolerance limit. It is also able to examine the most suitable

alternative investments which might help in reaching the desired goal and execute trades

(Webb and Martin 2017). OCBC securities is considered as one of the first brokerage

service in Singapore to introduce “OCBC OneTouch on their iOCBC TradeMobile” app

for both Android and iPhone which enabled the users to evaluate their stock portfolio.

The bank took noteworthy initiative to launch app named Apple Watch. This service was

able to provide important “account information via wrist devices”. The bank is able to

make significant contribution to the financial system with continuous engagement with

prospective customers to initiate cross selling of the brokerage services. In addition to

this, OCBC launched “StockReports+ in September 2016”, which aggregates

independent research done by the brokers and provide quantitative analysis for the stocks

in “Singapore, Hong Kong, United States and Malaysia markets”. OCBC expanded the

contribution of brokerage services to the financial system by enabling trading on the

“Shenzhen ‘A’ market after the launch of the Shenzhen-Hong Kong Stock Connect in

November 2016”. This allowed the existing customers to trade over 15 global exchange

online (Ocbc.com. 2018). Some of the other brokerage services are identified in form of

providing opportunity to earn income on unvested cash in the brokerage account with

bank deposit program thereby assisting in dividend reinvestment plan, periodic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS OF BANKING AND FINANCE

reinvestment plan and providing margin borrowing and option trading (Unionbank.com.

2018).

2. Asset Transformation - The process of asset transformation deals with creating new

asset from liabilities with different characteristics and conversion of small denomination,

“immediately available and relatively risk-free bank deposit into loans”. Asset

transformation in banks is used with deposits to produce revenue for pooling deposits to

fund loans. Henceforth, in a simple way the process of asset transformation involves

converting bank liabilities or deposits into bank assets or loans. The primary activities of

bank include withdrawal of deposits by the customers at the stipulated time and the

contract is made at the time of deposit agreement (Entrop et al. 2015). Bank loans are

considered as assets as the present money is the bank lends and expects to receive along

with interest payments. Very often, bank decides to undertake asset transformation via

lending long and borrowing short rate of interests with transformation of revenues. The

bank performs asset transformation by offering varieties of financial products in form of

“deposits, loan products and investment options” (Majd Bakir 2015). The asset

conversion cycle of OCBC shows that as there was an increase in the customer deposit by

6% in 2016 (“amounting to S$ 261 billion”), this comprised of 80% compensation for

funding of the group. This shows that 80% of the Banks’s liabilities (deposits) were

transformed into assets (loan). The sound assets transformation policies adopted by the

bank was further evident with a stable funding and liquidity position in 2016. In addition

to this, there was an increase in the “loans-to deposits ratio stood at 82.9%, as compared

with 84.5% a year ago”. However, bank is in a good position to cover any unforeseen

fund requirements due to the high asset transformation rate (Ocbc.com. 2018).

A study conducted by the IMF has implied that an increase in one percentage

point of the GDP is able to increase the output by 0.4% in the same year and after four

years by 1.5%. In general, the financial institutions are also able to bring economic

development in the infrastructure facilities in a country with asset conversion. The

financial services are discerned to play an important role in terms of providing growth to

the infrastructural facilities. The private sector finds it difficult for raising the capital

needed for setting up of the infrastructure industries. The development banks and the

reinvestment plan and providing margin borrowing and option trading (Unionbank.com.

2018).

2. Asset Transformation - The process of asset transformation deals with creating new

asset from liabilities with different characteristics and conversion of small denomination,

“immediately available and relatively risk-free bank deposit into loans”. Asset

transformation in banks is used with deposits to produce revenue for pooling deposits to

fund loans. Henceforth, in a simple way the process of asset transformation involves

converting bank liabilities or deposits into bank assets or loans. The primary activities of

bank include withdrawal of deposits by the customers at the stipulated time and the

contract is made at the time of deposit agreement (Entrop et al. 2015). Bank loans are

considered as assets as the present money is the bank lends and expects to receive along

with interest payments. Very often, bank decides to undertake asset transformation via

lending long and borrowing short rate of interests with transformation of revenues. The

bank performs asset transformation by offering varieties of financial products in form of

“deposits, loan products and investment options” (Majd Bakir 2015). The asset

conversion cycle of OCBC shows that as there was an increase in the customer deposit by

6% in 2016 (“amounting to S$ 261 billion”), this comprised of 80% compensation for

funding of the group. This shows that 80% of the Banks’s liabilities (deposits) were

transformed into assets (loan). The sound assets transformation policies adopted by the

bank was further evident with a stable funding and liquidity position in 2016. In addition

to this, there was an increase in the “loans-to deposits ratio stood at 82.9%, as compared

with 84.5% a year ago”. However, bank is in a good position to cover any unforeseen

fund requirements due to the high asset transformation rate (Ocbc.com. 2018).

A study conducted by the IMF has implied that an increase in one percentage

point of the GDP is able to increase the output by 0.4% in the same year and after four

years by 1.5%. In general, the financial institutions are also able to bring economic

development in the infrastructure facilities in a country with asset conversion. The

financial services are discerned to play an important role in terms of providing growth to

the infrastructural facilities. The private sector finds it difficult for raising the capital

needed for setting up of the infrastructure industries. The development banks and the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS OF BANKING AND FINANCE

merchant banks are able to contribute for raising capital in these industries. Banks have

the opportunity to work with multilateral developing organizations for setting up

financial and investment funds and other industrial platforms (Bhattacharya, Oppenheim

and Stern 2015). The multinational banks have been able to gather substantial amount of

information pertaining to “management, client, government and market-related

information” with the help of daily operations. They have been able to resolve several

types of the finding issues associated to infrastructural development. There is significant

scope of commercial financial institutions which may work with the multilateral

development organizations and financing funds. The global infrastructure is able to

embrace new opportunities. This is done by strengthening cooperation and resolving

investment issues faced in several countries, there is significant opportunity for

development of economy, infrastructure quality along with promotion of regional

connectivity (IMF 2014).

Critical Evaluation of problem with relying on debt finance for financial surplus unit and

financial deficit unit

There are number of problem associated to the financial deficit and financial surplus

units. For instance, the problem with financing to providing debt finance to financial surplus unit

was depicted with “maturity mismatch, size mismatch, return and risk” for OCBC in 2015. In

several instance OCBC struggled to meet the short maturity debts. As per the financial

revealing, OCBC has majority forms of Credit Exposure arising out of residual contract maturity

amounting to S$119152 in 2016. As per the depiction of annual report published on 31st

December 2016, the “absolute non-performing asset grew by $ 2.89 billion in compared to $ 2.04

billion”. This shows significant issues with the debt financing by bank to both financial deficit

and financial surplus units. The financial surplus units such as oil and gas support services

witnessed higher NPA because of the high “NPL ratio from 0.9% a year ago to 1.3% in 2016”.

However, the group had been able to maintain a strong funding position and capitalisation

options (Paligorova and Santos 2017).

merchant banks are able to contribute for raising capital in these industries. Banks have

the opportunity to work with multilateral developing organizations for setting up

financial and investment funds and other industrial platforms (Bhattacharya, Oppenheim

and Stern 2015). The multinational banks have been able to gather substantial amount of

information pertaining to “management, client, government and market-related

information” with the help of daily operations. They have been able to resolve several

types of the finding issues associated to infrastructural development. There is significant

scope of commercial financial institutions which may work with the multilateral

development organizations and financing funds. The global infrastructure is able to

embrace new opportunities. This is done by strengthening cooperation and resolving

investment issues faced in several countries, there is significant opportunity for

development of economy, infrastructure quality along with promotion of regional

connectivity (IMF 2014).

Critical Evaluation of problem with relying on debt finance for financial surplus unit and

financial deficit unit

There are number of problem associated to the financial deficit and financial surplus

units. For instance, the problem with financing to providing debt finance to financial surplus unit

was depicted with “maturity mismatch, size mismatch, return and risk” for OCBC in 2015. In

several instance OCBC struggled to meet the short maturity debts. As per the financial

revealing, OCBC has majority forms of Credit Exposure arising out of residual contract maturity

amounting to S$119152 in 2016. As per the depiction of annual report published on 31st

December 2016, the “absolute non-performing asset grew by $ 2.89 billion in compared to $ 2.04

billion”. This shows significant issues with the debt financing by bank to both financial deficit

and financial surplus units. The financial surplus units such as oil and gas support services

witnessed higher NPA because of the high “NPL ratio from 0.9% a year ago to 1.3% in 2016”.

However, the group had been able to maintain a strong funding position and capitalisation

options (Paligorova and Santos 2017).

5ECONOMICS OF BANKING AND FINANCE

The problem associated to debt financing for financial deficit units are seen with OCBC

issuing of unsecured debt. This is evident with “subordinate debt, Commercial papers and

Structured notes” increasing in 2016. Over time the bank is seen to issue more debt within “1

week, 1-week to1 month, 1 to 3 months and 3 to 12 months”. The increasing debt obligations

over the months, shows that the securities comprise of the equity securities, trading and

investment portfolio of government, debt and equity securities (Eichengreen and Panizza 2016).

Some of the other risks identified with debt financing for the financial deficit units are

identified with lending to the consumer, corporate or institutional customers. Some of the most

noted trading and investment banking activities are discerned with banking activities pertaining

to “trading of derivatives, debt securities, foreign exchange, commodities, securities

underwriting and the settlement of transactions” (Porter 2016). This has exposed the group to the

counterparty and issuer credit risk. OCBC credit risk exposure is quantified in terms of the

transaction’s present positive “mark-to-market value plus an appropriate add-on factor for

potential future exposure”. For example, a bondholder may sell the bond at any time, in order to

receive this privilege, the bond holder will be able to make a lump sum payment at the time of

purchasing the bond. The rate of interest on bonds are generally lower than the bank loans but

the accessing time of the bank loans are faster (Christensen et al. 2016).

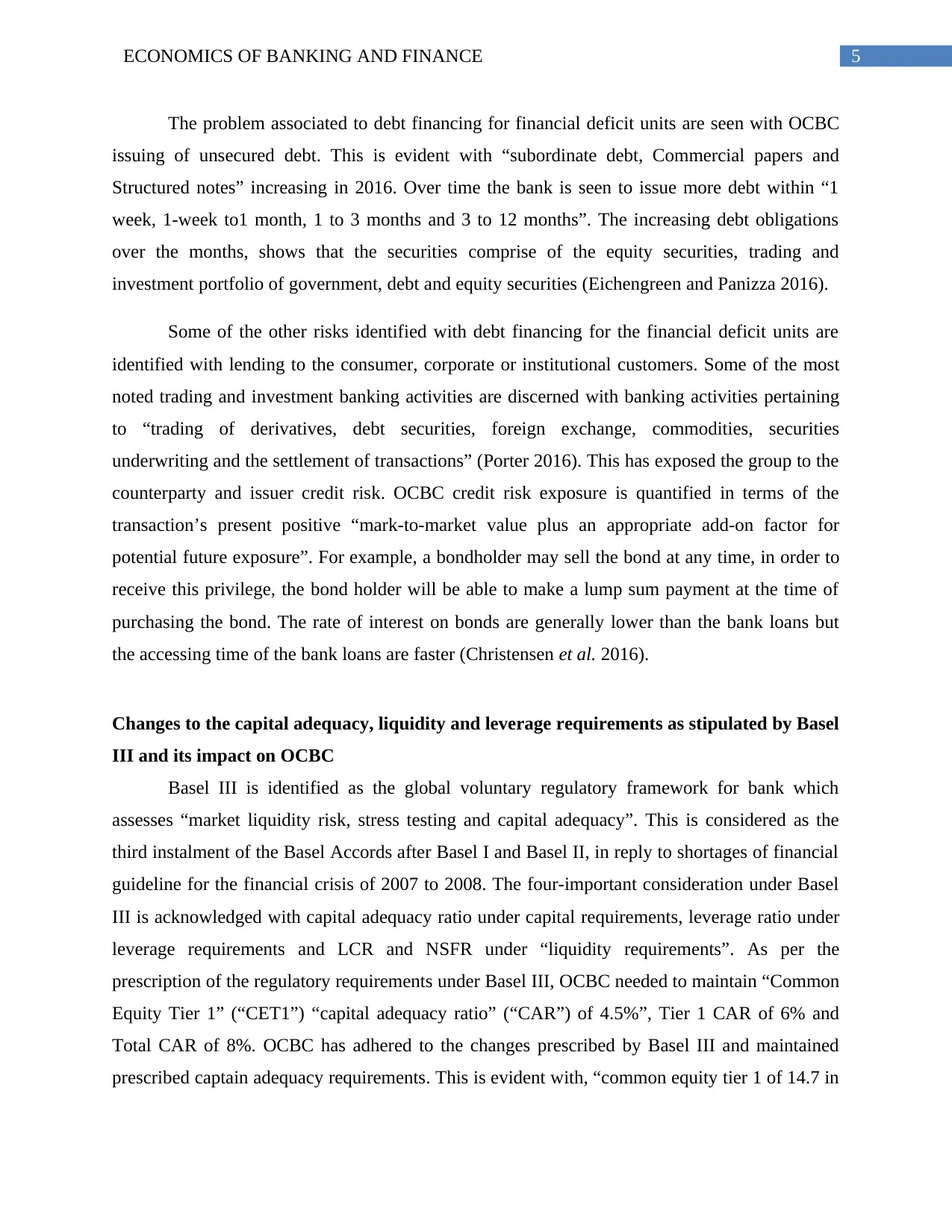

Changes to the capital adequacy, liquidity and leverage requirements as stipulated by Basel

III and its impact on OCBC

Basel III is identified as the global voluntary regulatory framework for bank which

assesses “market liquidity risk, stress testing and capital adequacy”. This is considered as the

third instalment of the Basel Accords after Basel I and Basel II, in reply to shortages of financial

guideline for the financial crisis of 2007 to 2008. The four-important consideration under Basel

III is acknowledged with capital adequacy ratio under capital requirements, leverage ratio under

leverage requirements and LCR and NSFR under “liquidity requirements”. As per the

prescription of the regulatory requirements under Basel III, OCBC needed to maintain “Common

Equity Tier 1” (“CET1”) “capital adequacy ratio” (“CAR”) of 4.5%”, Tier 1 CAR of 6% and

Total CAR of 8%. OCBC has adhered to the changes prescribed by Basel III and maintained

prescribed captain adequacy requirements. This is evident with, “common equity tier 1 of 14.7 in

The problem associated to debt financing for financial deficit units are seen with OCBC

issuing of unsecured debt. This is evident with “subordinate debt, Commercial papers and

Structured notes” increasing in 2016. Over time the bank is seen to issue more debt within “1

week, 1-week to1 month, 1 to 3 months and 3 to 12 months”. The increasing debt obligations

over the months, shows that the securities comprise of the equity securities, trading and

investment portfolio of government, debt and equity securities (Eichengreen and Panizza 2016).

Some of the other risks identified with debt financing for the financial deficit units are

identified with lending to the consumer, corporate or institutional customers. Some of the most

noted trading and investment banking activities are discerned with banking activities pertaining

to “trading of derivatives, debt securities, foreign exchange, commodities, securities

underwriting and the settlement of transactions” (Porter 2016). This has exposed the group to the

counterparty and issuer credit risk. OCBC credit risk exposure is quantified in terms of the

transaction’s present positive “mark-to-market value plus an appropriate add-on factor for

potential future exposure”. For example, a bondholder may sell the bond at any time, in order to

receive this privilege, the bond holder will be able to make a lump sum payment at the time of

purchasing the bond. The rate of interest on bonds are generally lower than the bank loans but

the accessing time of the bank loans are faster (Christensen et al. 2016).

Changes to the capital adequacy, liquidity and leverage requirements as stipulated by Basel

III and its impact on OCBC

Basel III is identified as the global voluntary regulatory framework for bank which

assesses “market liquidity risk, stress testing and capital adequacy”. This is considered as the

third instalment of the Basel Accords after Basel I and Basel II, in reply to shortages of financial

guideline for the financial crisis of 2007 to 2008. The four-important consideration under Basel

III is acknowledged with capital adequacy ratio under capital requirements, leverage ratio under

leverage requirements and LCR and NSFR under “liquidity requirements”. As per the

prescription of the regulatory requirements under Basel III, OCBC needed to maintain “Common

Equity Tier 1” (“CET1”) “capital adequacy ratio” (“CAR”) of 4.5%”, Tier 1 CAR of 6% and

Total CAR of 8%. OCBC has adhered to the changes prescribed by Basel III and maintained

prescribed captain adequacy requirements. This is evident with, “common equity tier 1 of 14.7 in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS OF BANKING AND FINANCE

2016 and 14.18 2015”. It has further able to maintain the minimum total capital requirements,

which is evident with total CAR of “15.90 in 2014, 16.8 in 2015 and 17.1 in 2016” (Ocbc.com.

2018).

The increasing nature of “capital adequacy ratio” is considered to be safe for the bank as OCBC

is in a better position to cover its financial obligations. (Ocbc.com. 2018).

Figure: Basel III Regulatory Capital Requirements

(Source: Tonse.in. 2018)

2016 and 14.18 2015”. It has further able to maintain the minimum total capital requirements,

which is evident with total CAR of “15.90 in 2014, 16.8 in 2015 and 17.1 in 2016” (Ocbc.com.

2018).

The increasing nature of “capital adequacy ratio” is considered to be safe for the bank as OCBC

is in a better position to cover its financial obligations. (Ocbc.com. 2018).

Figure: Basel III Regulatory Capital Requirements

(Source: Tonse.in. 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS OF BANKING AND FINANCE

The Basel III norms also strengthened the liquidity requirements by putting an augmented

effort to determine capital requirements for counterparty in case of credit default. The main

changes in the Basel III norms that are brought by strengthening the liquidity requirements in

form of LCR and NSFR. The introduction of NSFR was done to encourage the banks to utilize

stable sources while financing the operational activities. The LCR was introduced to ensure there

was sufficient stock for imaginative “high-value liquid asset” consisting of “cash or cash

equivalent units” for meeting liquidity obligations. Liquidity policies introduced under Basel III

(LCR) depicted that, the banks needed to consider “high-quality liquid asset” for covering “net

cash outflows” for more than 30 days. As per the NSFR requirement, the accessible sum for

stable funding is required to exceed the required amount of stable funding for more than one year

under extended stress. The objective of liquidity risk management of the bank was to confirm

that there are funds available to meet the contractual and regulatory obligations of finance and

OCBC is able to undertake new transactions. As per the fourth quarter result of 2016, the average

Singapore dollar (“SGD”) and “all-currency liquidity coverage ratios” (“LCR”)” for the group

thereby not considering OCBC Wing Hang which will be included in due course”) was depicted

with “284% and 145%” respectively. Balance sheet of the bank’s is able to demonstrate that

OCBC is recognized to prudently manage its risks and attain a healthy liquidity and funding

position. Based on the performance review the bank had to go through difficult operating

environment in 2016 (Chen, Dasgupta and Yu 2014). The availability of the sales national assets

is considered for infinite time and this may be held for selling the needs of liquidity or any

change in exchange policy, market prices or interest rate. The different types of expected

liquidity of the company are managed with combination of “treasury and asset liability practice

management”. However, OCBC is still working on its regulatory framework for applying the

regulatory reporting of Group-wide NSFR and “liquidity coverage ratio (LCR)” (Ocbc.com.

2018).

In several cases banks need robust risk-based ratio for capital as this helps in excessive

leverage build up. Basel III required the banks to maintain a minimum leverage ratio of 3%. This

is considered with leverage ratio as per risk and calculated by dividing Tier 1 capital by the

bank's average total consolidated assets”. In addition to this, The Basel Committee tested “a

minimum Tier 1 leverage ratio of 3% during the parallel run period from January 1, 2013 to

January 1, 2017”. The main changes brought in the leverage requirements had done to protect the

The Basel III norms also strengthened the liquidity requirements by putting an augmented

effort to determine capital requirements for counterparty in case of credit default. The main

changes in the Basel III norms that are brought by strengthening the liquidity requirements in

form of LCR and NSFR. The introduction of NSFR was done to encourage the banks to utilize

stable sources while financing the operational activities. The LCR was introduced to ensure there

was sufficient stock for imaginative “high-value liquid asset” consisting of “cash or cash

equivalent units” for meeting liquidity obligations. Liquidity policies introduced under Basel III

(LCR) depicted that, the banks needed to consider “high-quality liquid asset” for covering “net

cash outflows” for more than 30 days. As per the NSFR requirement, the accessible sum for

stable funding is required to exceed the required amount of stable funding for more than one year

under extended stress. The objective of liquidity risk management of the bank was to confirm

that there are funds available to meet the contractual and regulatory obligations of finance and

OCBC is able to undertake new transactions. As per the fourth quarter result of 2016, the average

Singapore dollar (“SGD”) and “all-currency liquidity coverage ratios” (“LCR”)” for the group

thereby not considering OCBC Wing Hang which will be included in due course”) was depicted

with “284% and 145%” respectively. Balance sheet of the bank’s is able to demonstrate that

OCBC is recognized to prudently manage its risks and attain a healthy liquidity and funding

position. Based on the performance review the bank had to go through difficult operating

environment in 2016 (Chen, Dasgupta and Yu 2014). The availability of the sales national assets

is considered for infinite time and this may be held for selling the needs of liquidity or any

change in exchange policy, market prices or interest rate. The different types of expected

liquidity of the company are managed with combination of “treasury and asset liability practice

management”. However, OCBC is still working on its regulatory framework for applying the

regulatory reporting of Group-wide NSFR and “liquidity coverage ratio (LCR)” (Ocbc.com.

2018).

In several cases banks need robust risk-based ratio for capital as this helps in excessive

leverage build up. Basel III required the banks to maintain a minimum leverage ratio of 3%. This

is considered with leverage ratio as per risk and calculated by dividing Tier 1 capital by the

bank's average total consolidated assets”. In addition to this, The Basel Committee tested “a

minimum Tier 1 leverage ratio of 3% during the parallel run period from January 1, 2013 to

January 1, 2017”. The main changes brought in the leverage requirements had done to protect the

8ECONOMICS OF BANKING AND FINANCE

bank from systemwide build-up of leverage due to financial stress during destabilization or

unwinding of a certain process. The leverage ratio of OCBC was 8.2%, which was above than a

least requirement of 3% as suggested by the “Basel III committee”. OCBC was also decided to

introduce more transparent measures for capital requirement by maintaining a high

"discretionary counter-cyclical buffer” (Ocbc.com. 2018).

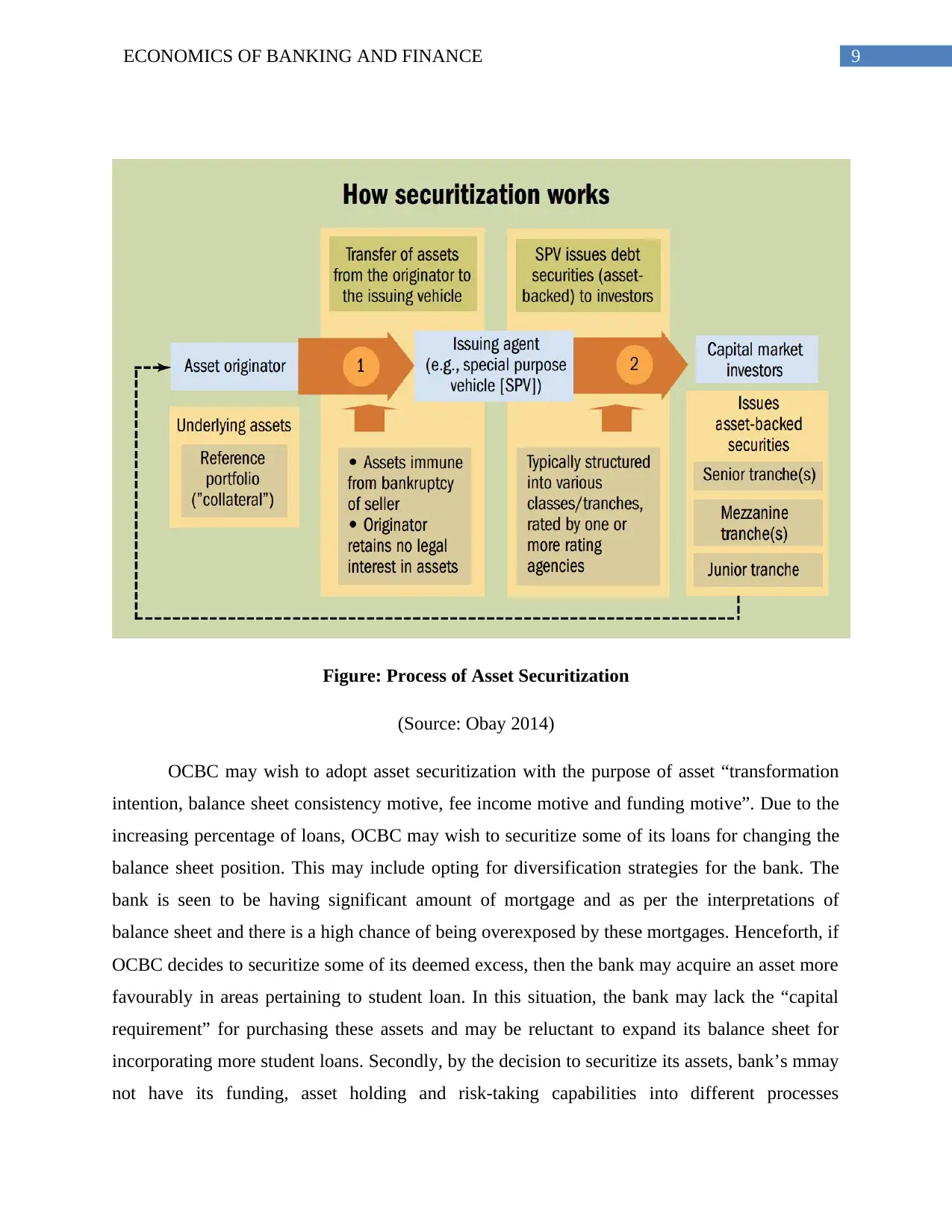

Processes of asset securitization and examine why OCBC may wish to securitize

The process of asset securitization is identified as practice for financial pooling different

types of contractual debts. These are identified with such as “auto loans, credit cards,

commercial mortgages and residential mortgages and sending the associated cash flows to the

“third-party investors” in form of securities”. These securities may be defined as “bonds, pass-

through securities, or collateralized debt obligations (CDOs)”. The associated investors are

recompensed from the “interest cash flows and principal” “collected from the underlying debt”

and redistributing the same with capital structure of new financing. The securities supported by

mortgage receivables are termed as “mortgage-backed securities” while securities backed by

“other receivables are termed as asset backed securities”. The procedure of asset “securitization”

is identified as a complex one which includes several actors. The diagram depicted below is

taken from IMF website which shows the rudimentary mechanism of creating securities and

transferring of asset. The entity which originally holds the asset, initiates the process by legal

entity which is known as SPV, specially created to limit the risk of the final investor in relation

to the issuer of the assets”. Based on the situation, SPV is either responsible for issuing the direct

securities or reselling the pool of assets to a trust (Agarwal et al. 2016).

SPV is a legal framework rather than the element which is responsible to play an active

role in the transaction process. The most noted character played by SPV is seen to be of that of

an arranger, which is typically a bank responsible for setting up the contract and evaluating the

“pool of assets”. It also determines the way in which this would be fed and characterized by

securities on like structure of fund. The main purpose of structuring is observed with the

postmodern “characteristics of securities”, in a way that they agree to the needs of final investor.

The arranger plays a significant role in distribution of the securities made for final “investors”.

This also enables refinancing of short-term debts with long-term bonds (Fimarkets.com. 2018).

bank from systemwide build-up of leverage due to financial stress during destabilization or

unwinding of a certain process. The leverage ratio of OCBC was 8.2%, which was above than a

least requirement of 3% as suggested by the “Basel III committee”. OCBC was also decided to

introduce more transparent measures for capital requirement by maintaining a high

"discretionary counter-cyclical buffer” (Ocbc.com. 2018).

Processes of asset securitization and examine why OCBC may wish to securitize

The process of asset securitization is identified as practice for financial pooling different

types of contractual debts. These are identified with such as “auto loans, credit cards,

commercial mortgages and residential mortgages and sending the associated cash flows to the

“third-party investors” in form of securities”. These securities may be defined as “bonds, pass-

through securities, or collateralized debt obligations (CDOs)”. The associated investors are

recompensed from the “interest cash flows and principal” “collected from the underlying debt”

and redistributing the same with capital structure of new financing. The securities supported by

mortgage receivables are termed as “mortgage-backed securities” while securities backed by

“other receivables are termed as asset backed securities”. The procedure of asset “securitization”

is identified as a complex one which includes several actors. The diagram depicted below is

taken from IMF website which shows the rudimentary mechanism of creating securities and

transferring of asset. The entity which originally holds the asset, initiates the process by legal

entity which is known as SPV, specially created to limit the risk of the final investor in relation

to the issuer of the assets”. Based on the situation, SPV is either responsible for issuing the direct

securities or reselling the pool of assets to a trust (Agarwal et al. 2016).

SPV is a legal framework rather than the element which is responsible to play an active

role in the transaction process. The most noted character played by SPV is seen to be of that of

an arranger, which is typically a bank responsible for setting up the contract and evaluating the

“pool of assets”. It also determines the way in which this would be fed and characterized by

securities on like structure of fund. The main purpose of structuring is observed with the

postmodern “characteristics of securities”, in a way that they agree to the needs of final investor.

The arranger plays a significant role in distribution of the securities made for final “investors”.

This also enables refinancing of short-term debts with long-term bonds (Fimarkets.com. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS OF BANKING AND FINANCE

Figure: Process of Asset Securitization

(Source: Obay 2014)

OCBC may wish to adopt asset securitization with the purpose of asset “transformation

intention, balance sheet consistency motive, fee income motive and funding motive”. Due to the

increasing percentage of loans, OCBC may wish to securitize some of its loans for changing the

balance sheet position. This may include opting for diversification strategies for the bank. The

bank is seen to be having significant amount of mortgage and as per the interpretations of

balance sheet and there is a high chance of being overexposed by these mortgages. Henceforth, if

OCBC decides to securitize some of its deemed excess, then the bank may acquire an asset more

favourably in areas pertaining to student loan. In this situation, the bank may lack the “capital

requirement” for purchasing these assets and may be reluctant to expand its balance sheet for

incorporating more student loans. Secondly, by the decision to securitize its assets, bank’s mmay

not have its funding, asset holding and risk-taking capabilities into different processes

Figure: Process of Asset Securitization

(Source: Obay 2014)

OCBC may wish to adopt asset securitization with the purpose of asset “transformation

intention, balance sheet consistency motive, fee income motive and funding motive”. Due to the

increasing percentage of loans, OCBC may wish to securitize some of its loans for changing the

balance sheet position. This may include opting for diversification strategies for the bank. The

bank is seen to be having significant amount of mortgage and as per the interpretations of

balance sheet and there is a high chance of being overexposed by these mortgages. Henceforth, if

OCBC decides to securitize some of its deemed excess, then the bank may acquire an asset more

favourably in areas pertaining to student loan. In this situation, the bank may lack the “capital

requirement” for purchasing these assets and may be reluctant to expand its balance sheet for

incorporating more student loans. Secondly, by the decision to securitize its assets, bank’s mmay

not have its funding, asset holding and risk-taking capabilities into different processes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS OF BANKING AND FINANCE

(Abdelsalam et al. 2017). Due to this, securities would be able to link parties which possesses

more comparative advantage and share mutual benefit. The bank is discerned to be having a

comparative advantage in terms of initializing the loans. Henceforth, OCBC may be able to

outsource its relatively weaker SPV’s to the eventual investors and specialize in terms of funding

and holding loans. Moreover, in case the “SPV is not a subsidiary of the bank” then it needs to

pay a fee to the bank for purchasing of the assets and this can create additional source of income

thereby potentially leading to increased “rate of return on equity”. The shifting of this “credit

risk” enhances the capacity of the bank for lending activities. Furthermore, this increased

capacity enhances the bank reputation this customer and able to build an approachable bond by

providing loans to those otherwise struggle to obtain (Ocbc.com. 2018).

OCBC may also want to encourage its funding activities which benefited asset

securitization of bank loans. By exercising securitization options, the bank would be able to

widen its fund sources and the investors who had previously sceptical will no longer have to

invest their funds in a bank which they don’t prefer (Le, Narayanan and Van Vo 2016).

Implications of the “global financial crisis” on the bank’s financial performances

“Global Financial Crisis (GFC)” was well-thought-out as the one of the worst downturn

in global economy followed by Great Depression in 1930. The implication of this crisis

originated from Lehman Brothers bankruptcy filed On September 15, 2008. This was one of the

largest bankruptcy in the history with “$639 billion in assets and $619 billion in debt”, thereby

surpassing previous bankrupt giants such as “Enron and WorldCom”. The demise of “fourth-

largest U.S. investment bank” -entities such as “financial crisis” which swept through GFC in

2008. This collapse was identified as a seminal event which greatly intensified financial erosion

off close to “10 trillion in market capitalization from global equity markets in October 2008”

(Ball 2016).

The impact of GFC during 2008-2009 did not had any severe implication on the

performance of the bank. OCBC was able to maintain a sturdy “balance sheet and capital

position”. These implications were attributed to the basic blueprint for banking with its emphasis

on the SME and retail banking unlike the strong proprietary trading gains recorded in some

“global financial institutions”. The core net profit after tax for OCBC (“excluding the onetime

(Abdelsalam et al. 2017). Due to this, securities would be able to link parties which possesses

more comparative advantage and share mutual benefit. The bank is discerned to be having a

comparative advantage in terms of initializing the loans. Henceforth, OCBC may be able to

outsource its relatively weaker SPV’s to the eventual investors and specialize in terms of funding

and holding loans. Moreover, in case the “SPV is not a subsidiary of the bank” then it needs to

pay a fee to the bank for purchasing of the assets and this can create additional source of income

thereby potentially leading to increased “rate of return on equity”. The shifting of this “credit

risk” enhances the capacity of the bank for lending activities. Furthermore, this increased

capacity enhances the bank reputation this customer and able to build an approachable bond by

providing loans to those otherwise struggle to obtain (Ocbc.com. 2018).

OCBC may also want to encourage its funding activities which benefited asset

securitization of bank loans. By exercising securitization options, the bank would be able to

widen its fund sources and the investors who had previously sceptical will no longer have to

invest their funds in a bank which they don’t prefer (Le, Narayanan and Van Vo 2016).

Implications of the “global financial crisis” on the bank’s financial performances

“Global Financial Crisis (GFC)” was well-thought-out as the one of the worst downturn

in global economy followed by Great Depression in 1930. The implication of this crisis

originated from Lehman Brothers bankruptcy filed On September 15, 2008. This was one of the

largest bankruptcy in the history with “$639 billion in assets and $619 billion in debt”, thereby

surpassing previous bankrupt giants such as “Enron and WorldCom”. The demise of “fourth-

largest U.S. investment bank” -entities such as “financial crisis” which swept through GFC in

2008. This collapse was identified as a seminal event which greatly intensified financial erosion

off close to “10 trillion in market capitalization from global equity markets in October 2008”

(Ball 2016).

The impact of GFC during 2008-2009 did not had any severe implication on the

performance of the bank. OCBC was able to maintain a sturdy “balance sheet and capital

position”. These implications were attributed to the basic blueprint for banking with its emphasis

on the SME and retail banking unlike the strong proprietary trading gains recorded in some

“global financial institutions”. The core net profit after tax for OCBC (“excluding the onetime

11ECONOMICS OF BANKING AND FINANCE

gains”) increased by “32% in 2009 to attain a new record of S$1,962 million. This was discerned

to be exceeded to the previous high of S$1,878 million in 2007”. The increase in the earnings in

2009 was recorded with higher amount of “non-interest income”, decrease in the allowances and

lower expenses. The allowed margin for adjustments and net interest income depicted a healthy

trend at the time of financial crisis. By the adaptation of a robust risk management framework,

active monitoring and prudent loan growth policy of the portfolios, OCBC was able to achieve

the best quality in terms of the asset and “credit loss” experience among the three banks based in

Singapore. In June 2009 the company’s Non-performing loan ratio peaked at “2.1%, compared to

1.7% in December 2007 and 1.5% in December 2008”. This value was depicted with an increase

of 1.7% in December 2009. The total amount of the assets and specific allowances for loan over

the average loan were discerned to be below 30 BPS in 2008 and 2009. The coverage ratio for

the allowances remained at a healthy level with “125% in December 2008 and 102% in

December 2009”. During the situation of crisis, OCBC continued to maintain a strong capital

cushion with a “Tier 1 ratio of 14.9% in 2008 and 15.9%”. This is seen to be even higher than

the non-financial crisis situation in 2007 when the ratio was only 11.5%. OCBC is considered as

the only bank in Singapore which did not reduce its DPS for the period (Bis.org 2018).

As Singapore is identified as a small and open economy with strong linkages with the

other countries, it severely got affected in terms of falling Global trade. The “Monetary Policy”

responses were graduated deliberately, which was underpinned with the objective of promoting

“price stability” in medium term. Singapore government intentionally did not respond to every

single development in the “economy or the financial markets” as this would have brought in

needless volatility and ambiguity. In response to the significant decline the external demand in

the late 2008, MAS was seen to support the domestic economy in the early 2010 thereby

consideration for strong recovery path of the rising economy. In the early 2010, the government

took a strong recovery route for addressing the rising “domestic cost pressures amidst high rates

of resource utilisation”. To address this concern, MAS was seen to shift its gradual and modest

appreciation towards “S$NEER policy band”. Subsequently a more stricter policy for MAS

tightening is seen from improving on the policy band slope (Bis.org. 2018).

gains”) increased by “32% in 2009 to attain a new record of S$1,962 million. This was discerned

to be exceeded to the previous high of S$1,878 million in 2007”. The increase in the earnings in

2009 was recorded with higher amount of “non-interest income”, decrease in the allowances and

lower expenses. The allowed margin for adjustments and net interest income depicted a healthy

trend at the time of financial crisis. By the adaptation of a robust risk management framework,

active monitoring and prudent loan growth policy of the portfolios, OCBC was able to achieve

the best quality in terms of the asset and “credit loss” experience among the three banks based in

Singapore. In June 2009 the company’s Non-performing loan ratio peaked at “2.1%, compared to

1.7% in December 2007 and 1.5% in December 2008”. This value was depicted with an increase

of 1.7% in December 2009. The total amount of the assets and specific allowances for loan over

the average loan were discerned to be below 30 BPS in 2008 and 2009. The coverage ratio for

the allowances remained at a healthy level with “125% in December 2008 and 102% in

December 2009”. During the situation of crisis, OCBC continued to maintain a strong capital

cushion with a “Tier 1 ratio of 14.9% in 2008 and 15.9%”. This is seen to be even higher than

the non-financial crisis situation in 2007 when the ratio was only 11.5%. OCBC is considered as

the only bank in Singapore which did not reduce its DPS for the period (Bis.org 2018).

As Singapore is identified as a small and open economy with strong linkages with the

other countries, it severely got affected in terms of falling Global trade. The “Monetary Policy”

responses were graduated deliberately, which was underpinned with the objective of promoting

“price stability” in medium term. Singapore government intentionally did not respond to every

single development in the “economy or the financial markets” as this would have brought in

needless volatility and ambiguity. In response to the significant decline the external demand in

the late 2008, MAS was seen to support the domestic economy in the early 2010 thereby

consideration for strong recovery path of the rising economy. In the early 2010, the government

took a strong recovery route for addressing the rising “domestic cost pressures amidst high rates

of resource utilisation”. To address this concern, MAS was seen to shift its gradual and modest

appreciation towards “S$NEER policy band”. Subsequently a more stricter policy for MAS

tightening is seen from improving on the policy band slope (Bis.org. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14