FIN203 Banking & Finance: AMP & CBA Share Price & Capital Budgeting

VerifiedAdded on 2023/06/07

|13

|3035

|159

Project

AI Summary

This finance project analyzes the share price trends of AMP and Commonwealth Bank (CBA) over the past five years, examining the impact of the Royal Commission on systematic and unsystematic risks. It also delves into capital budgeting, comparing the Internal Rate of Return (IRR) and Required Rate of Return (RRR), calculating Net Present Value (NPV) and IRR for hypothetical projects X and Y, and assessing the effect of changes in the required rate of return on project selection. The analysis reveals the impact of the Royal Commission's disclosures on the share prices of both AMP and CBA, highlighting the increased risk perception. Project Y is identified as the preferred investment based on both NPV and IRR calculations, even with adjustments to the required rate of return.

Running head: BANKING AND FINANCE

Banking and Finance

Name of the Student:

Name of the University:

Authors Note:

Banking and Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BANKING AND FINANCE

1

Table of Contents

Part A: AMP and CBA Share Price...........................................................................................2

1. Understanding the share price of CBA and AMP, whereas detecting their trend for past

five years:...................................................................................................................................2

2. Understanding the implications that Royal Commission enquiry has on systematic and

unsystematic risk of financial institutions, while detecting the share price movement of both

AMP and CBA with the reports of Royal Commission:............................................................4

Part B: Capital Budgeting..........................................................................................................6

1. Detecting the differences between the internal rate of return and required rate of return:....6

2. Understanding and calculating the current NPV value of Project X and Project Y:.............6

3. Calculating and detecting the internal rate of return of Project X and Project Y:.................7

4. Calculating the changes in NPV with the decline in required rate of return by 10%, while

determining any changes in the current decision:......................................................................8

5. Depicting the conditions under which Net Present Value and Internal Rate of Return offers

alternative recommendations:....................................................................................................9

References and Bibliography:..................................................................................................11

1

Table of Contents

Part A: AMP and CBA Share Price...........................................................................................2

1. Understanding the share price of CBA and AMP, whereas detecting their trend for past

five years:...................................................................................................................................2

2. Understanding the implications that Royal Commission enquiry has on systematic and

unsystematic risk of financial institutions, while detecting the share price movement of both

AMP and CBA with the reports of Royal Commission:............................................................4

Part B: Capital Budgeting..........................................................................................................6

1. Detecting the differences between the internal rate of return and required rate of return:....6

2. Understanding and calculating the current NPV value of Project X and Project Y:.............6

3. Calculating and detecting the internal rate of return of Project X and Project Y:.................7

4. Calculating the changes in NPV with the decline in required rate of return by 10%, while

determining any changes in the current decision:......................................................................8

5. Depicting the conditions under which Net Present Value and Internal Rate of Return offers

alternative recommendations:....................................................................................................9

References and Bibliography:..................................................................................................11

BANKING AND FINANCE

2

Part A: AMP and CBA Share Price

1. Understanding the share price of CBA and AMP, whereas detecting their trend for

past five years:

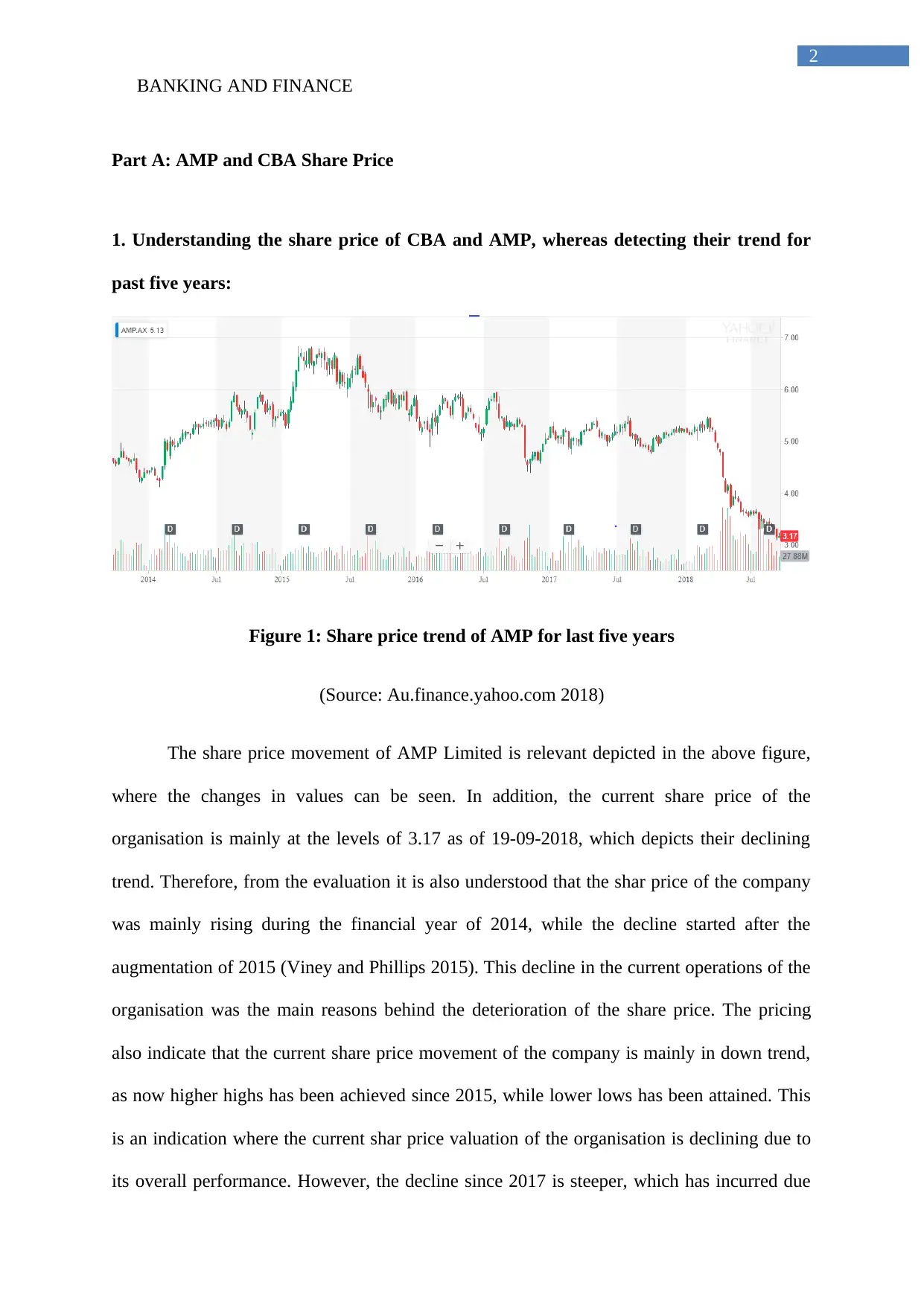

Figure 1: Share price trend of AMP for last five years

(Source: Au.finance.yahoo.com 2018)

The share price movement of AMP Limited is relevant depicted in the above figure,

where the changes in values can be seen. In addition, the current share price of the

organisation is mainly at the levels of 3.17 as of 19-09-2018, which depicts their declining

trend. Therefore, from the evaluation it is also understood that the shar price of the company

was mainly rising during the financial year of 2014, while the decline started after the

augmentation of 2015 (Viney and Phillips 2015). This decline in the current operations of the

organisation was the main reasons behind the deterioration of the share price. The pricing

also indicate that the current share price movement of the company is mainly in down trend,

as now higher highs has been achieved since 2015, while lower lows has been attained. This

is an indication where the current shar price valuation of the organisation is declining due to

its overall performance. However, the decline since 2017 is steeper, which has incurred due

2

Part A: AMP and CBA Share Price

1. Understanding the share price of CBA and AMP, whereas detecting their trend for

past five years:

Figure 1: Share price trend of AMP for last five years

(Source: Au.finance.yahoo.com 2018)

The share price movement of AMP Limited is relevant depicted in the above figure,

where the changes in values can be seen. In addition, the current share price of the

organisation is mainly at the levels of 3.17 as of 19-09-2018, which depicts their declining

trend. Therefore, from the evaluation it is also understood that the shar price of the company

was mainly rising during the financial year of 2014, while the decline started after the

augmentation of 2015 (Viney and Phillips 2015). This decline in the current operations of the

organisation was the main reasons behind the deterioration of the share price. The pricing

also indicate that the current share price movement of the company is mainly in down trend,

as now higher highs has been achieved since 2015, while lower lows has been attained. This

is an indication where the current shar price valuation of the organisation is declining due to

its overall performance. However, the decline since 2017 is steeper, which has incurred due

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BANKING AND FINANCE

3

to the augmentation of the Royal Commission that was assigned to view the current unethical

practices conducted in financial sectors. The new related to the current operations of AMP

has mainly declined its share values, as the company has been engulfed in unethical practices,

which was partially disclosed by the Royal Commission. On the contrary, Chandra (2017)

argued that investor using the technical analysis is not able to comprehend the investment

opportunity, which is detected from fundamental analysis.

Figure 1: Share price trend of CBA for last five years

(Source: Au.finance.yahoo.com 2018)

The current share price value of Commonwealth Bank is mainly at the levels of 72.09,

which has relevantly fallen from the highs of 96.08 achieved in 2015. However, increment in

valuation of the company was mainly at the levels of 73.08 during the start of 2014, while it

achieved the highs of 96.08 in 2015. This increment in share price was only witnessed once,

while rapid decline in the share price can be seen during the financial year of 2015. Since

2015 the share price of Commonwealth Bank has mainly declined exponentially, where the

support is seen within the levels of 70. The share price of the organisation has relevantly

increased during the financial year of 2017, while the disclosures conducted by the Royal

Commission directly have negative impact on valuation of the organisation. The share price

3

to the augmentation of the Royal Commission that was assigned to view the current unethical

practices conducted in financial sectors. The new related to the current operations of AMP

has mainly declined its share values, as the company has been engulfed in unethical practices,

which was partially disclosed by the Royal Commission. On the contrary, Chandra (2017)

argued that investor using the technical analysis is not able to comprehend the investment

opportunity, which is detected from fundamental analysis.

Figure 1: Share price trend of CBA for last five years

(Source: Au.finance.yahoo.com 2018)

The current share price value of Commonwealth Bank is mainly at the levels of 72.09,

which has relevantly fallen from the highs of 96.08 achieved in 2015. However, increment in

valuation of the company was mainly at the levels of 73.08 during the start of 2014, while it

achieved the highs of 96.08 in 2015. This increment in share price was only witnessed once,

while rapid decline in the share price can be seen during the financial year of 2015. Since

2015 the share price of Commonwealth Bank has mainly declined exponentially, where the

support is seen within the levels of 70. The share price of the organisation has relevantly

increased during the financial year of 2017, while the disclosures conducted by the Royal

Commission directly have negative impact on valuation of the organisation. The share price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BANKING AND FINANCE

4

valuation of the organisation has declined abruptly during the period of 2017, which indicates

the low valuation that has been conducted by the organisation. In this context, Edwards,

Magee and Bassetti (2018) mentioned that investors with the use of charts able to understand

the current trend of a share, which can be help in improving the level of income from

investment. Therefore, furthered decline in values of CBA below the price level of 70 will

indicate an initiation of a new downtrend.

2. Understanding the implications that Royal Commission enquiry has on systematic

and unsystematic risk of financial institutions, while detecting the share price

movement of both AMP and CBA with the reports of Royal Commission:

The Royal Commission was assigned during the fiscal year of 2017 for analysing the

current unethical practices, which are being conducted by the financial sector companies. The

results that is intended by the Royal Commission will directly have negative impact on the

performance of financial sector companies. This relevantly raises the level of concern for the

financial sector companies, as both the systematic and unsystematic risk has relevantly

increased for the financial institutions (Theguardian.com 2018). The rising concern for the

unethical measures, which were conducted by the financial sector companies was highlighted

by the Royal Commission. This relevantly raises the level of systematic (market) and

unsystematic (firm-specific) risk, present with the capital market. The rising concern for the

financial sector companies will directly affect the overall capital market and raises the

concern for price fluctuations. On the other hand, the rising concern for the financial sector

and the detection of unethical practises, which are being conducted raises the level of firm

specific risk and negatively affects the share price value of the companies.

AMP limited:

4

valuation of the organisation has declined abruptly during the period of 2017, which indicates

the low valuation that has been conducted by the organisation. In this context, Edwards,

Magee and Bassetti (2018) mentioned that investors with the use of charts able to understand

the current trend of a share, which can be help in improving the level of income from

investment. Therefore, furthered decline in values of CBA below the price level of 70 will

indicate an initiation of a new downtrend.

2. Understanding the implications that Royal Commission enquiry has on systematic

and unsystematic risk of financial institutions, while detecting the share price

movement of both AMP and CBA with the reports of Royal Commission:

The Royal Commission was assigned during the fiscal year of 2017 for analysing the

current unethical practices, which are being conducted by the financial sector companies. The

results that is intended by the Royal Commission will directly have negative impact on the

performance of financial sector companies. This relevantly raises the level of concern for the

financial sector companies, as both the systematic and unsystematic risk has relevantly

increased for the financial institutions (Theguardian.com 2018). The rising concern for the

unethical measures, which were conducted by the financial sector companies was highlighted

by the Royal Commission. This relevantly raises the level of systematic (market) and

unsystematic (firm-specific) risk, present with the capital market. The rising concern for the

financial sector companies will directly affect the overall capital market and raises the

concern for price fluctuations. On the other hand, the rising concern for the financial sector

and the detection of unethical practises, which are being conducted raises the level of firm

specific risk and negatively affects the share price value of the companies.

AMP limited:

BANKING AND FINANCE

5

The shar price movement of AMP Limited is directly influenced by the results and

disclosures, which are being conducted by the Royal Commission. In addition, the AMP

Limited share price has mainly declined during the financial year of 2018 due to the

disclosures of the scandal, which is being conducted by the Royal Commission. This directly

altered share price of AMP limited during the disclosures, where the share price declined

from the level of 5.43 to the current share price. This decline is directly reflecting the level of

unethical measures, which was being conceited by the company over the period. This

discloser contained the extra charges, which was imposed by AMP on their superannuation

fund investors. the compensation of $5 million was mainly distributed to 50,000

superannuation fund investors to comply with the unethical measures made previously by the

management. This disclosure directly reflected the problematic management decisions, which

were conducted in the organisation (Theguardian.com 2018).

Commonwealth Bank:

The disclosures that is being conducted by the Royal Commission against the current

operations of Commonwealth Bank are also raising concern for the investors and reducing tis

share valuation. In addition, the disclosures conducted during the fiscal year of 2017 and

2018 directly reflects the level of share price decline, which was conducted for

Commonwealth Bank. The Royal Commission has conducted allegations regarding the

current manipulations, which was being conducted by Commonwealth Bank. The Royal

Commission has adequately depicted that CBA has conducted malpractices in their

operations, which was going to be disclosed in future (Theguardian.com 2018).

5

The shar price movement of AMP Limited is directly influenced by the results and

disclosures, which are being conducted by the Royal Commission. In addition, the AMP

Limited share price has mainly declined during the financial year of 2018 due to the

disclosures of the scandal, which is being conducted by the Royal Commission. This directly

altered share price of AMP limited during the disclosures, where the share price declined

from the level of 5.43 to the current share price. This decline is directly reflecting the level of

unethical measures, which was being conceited by the company over the period. This

discloser contained the extra charges, which was imposed by AMP on their superannuation

fund investors. the compensation of $5 million was mainly distributed to 50,000

superannuation fund investors to comply with the unethical measures made previously by the

management. This disclosure directly reflected the problematic management decisions, which

were conducted in the organisation (Theguardian.com 2018).

Commonwealth Bank:

The disclosures that is being conducted by the Royal Commission against the current

operations of Commonwealth Bank are also raising concern for the investors and reducing tis

share valuation. In addition, the disclosures conducted during the fiscal year of 2017 and

2018 directly reflects the level of share price decline, which was conducted for

Commonwealth Bank. The Royal Commission has conducted allegations regarding the

current manipulations, which was being conducted by Commonwealth Bank. The Royal

Commission has adequately depicted that CBA has conducted malpractices in their

operations, which was going to be disclosed in future (Theguardian.com 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BANKING AND FINANCE

6

Part B: Capital Budgeting

1. Detecting the differences between the internal rate of return and required rate of

return:

The concept of IRR (Internal Rate of Return) and RRR (Required Rate of Return) has

some dissimilarities, which can be detected as follows.

The major difference between the IRR and RRR is its measure, which is used for

selecting the accurate project for investment. The use of IRR directly allows the

management to understand the level of returns, which can be provided by a single project.

On the contrary, the RRR is a percentage returns, which is used for calculating the NPV

of the project.

The second major difference is the usage and output between the IRR and RRR, which

relevantly allows the company to select a financially secure investment scope. The output

of IRR is different for all the projects, as it is determined from the level of cash outflows

and inflows conducted by the project. However, the RRR for each project is same, as the

organisation needs to evaluate different NPV value of the projects (Li and Trutnevyte

2017).

The last difference between eh IRR and RRR is its significance, which allows the

company to detect the accurate project for improving their current financial progress. The

RRR is mainly assumed by the company to evaluate the projects survival conditions,

while IRR is absolute, where the cash inflows and outflows remaining constant.

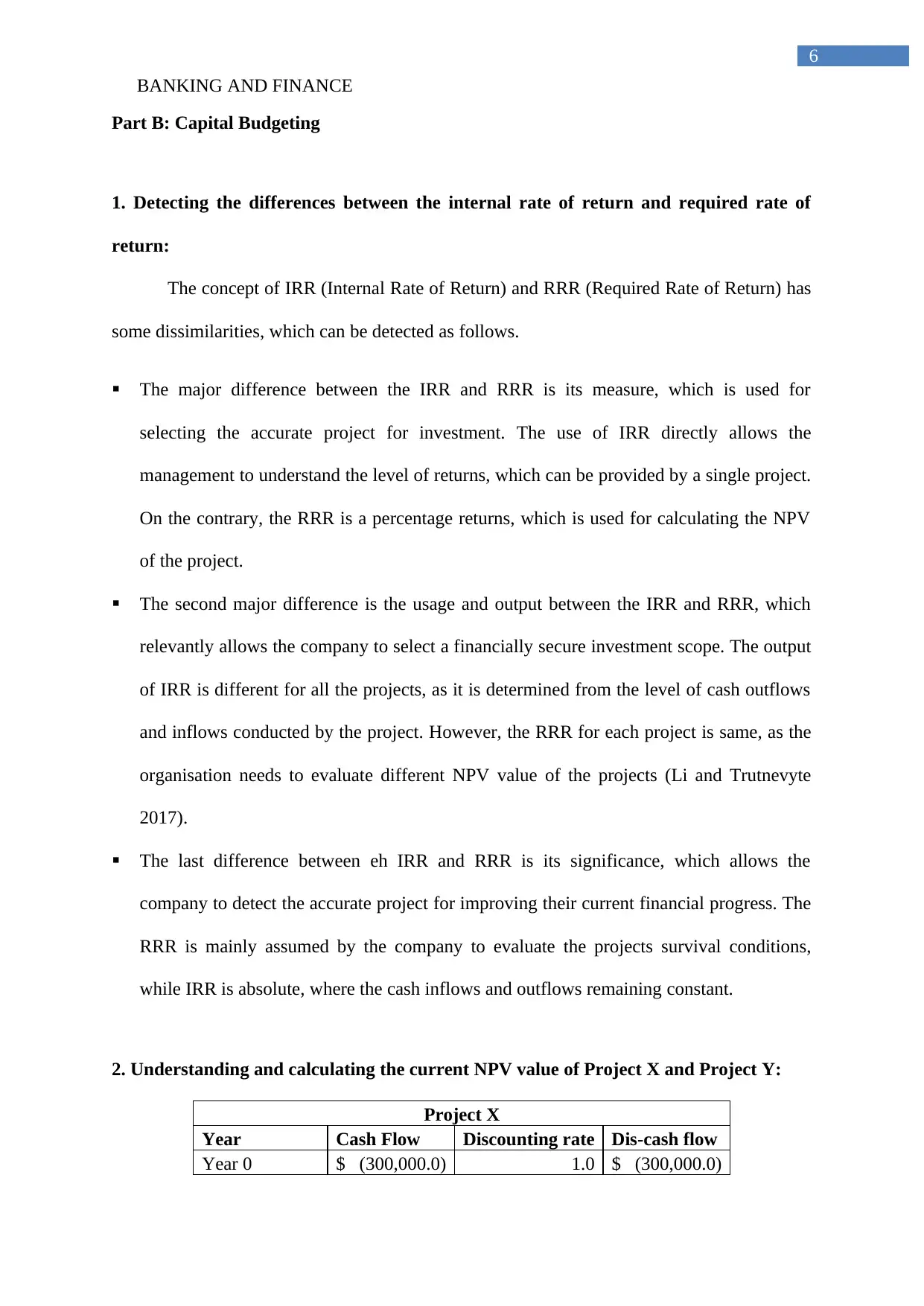

2. Understanding and calculating the current NPV value of Project X and Project Y:

Project X

Year Cash Flow Discounting rate Dis-cash flow

Year 0 $ (300,000.0) 1.0 $ (300,000.0)

6

Part B: Capital Budgeting

1. Detecting the differences between the internal rate of return and required rate of

return:

The concept of IRR (Internal Rate of Return) and RRR (Required Rate of Return) has

some dissimilarities, which can be detected as follows.

The major difference between the IRR and RRR is its measure, which is used for

selecting the accurate project for investment. The use of IRR directly allows the

management to understand the level of returns, which can be provided by a single project.

On the contrary, the RRR is a percentage returns, which is used for calculating the NPV

of the project.

The second major difference is the usage and output between the IRR and RRR, which

relevantly allows the company to select a financially secure investment scope. The output

of IRR is different for all the projects, as it is determined from the level of cash outflows

and inflows conducted by the project. However, the RRR for each project is same, as the

organisation needs to evaluate different NPV value of the projects (Li and Trutnevyte

2017).

The last difference between eh IRR and RRR is its significance, which allows the

company to detect the accurate project for improving their current financial progress. The

RRR is mainly assumed by the company to evaluate the projects survival conditions,

while IRR is absolute, where the cash inflows and outflows remaining constant.

2. Understanding and calculating the current NPV value of Project X and Project Y:

Project X

Year Cash Flow Discounting rate Dis-cash flow

Year 0 $ (300,000.0) 1.0 $ (300,000.0)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BANKING AND FINANCE

7

Year 1 $ 80,000.0 0.9 $ 71,428.6

Year 2 $ 140,000.0 0.8 $ 111,607.1

Year 3 $ 130,000.0 0.7 $ 92,531.4

Year 4 $ 160,000.0 0.6 $ 101,682.9

Discounted rate 12.0%

NPV $ 77,250.0

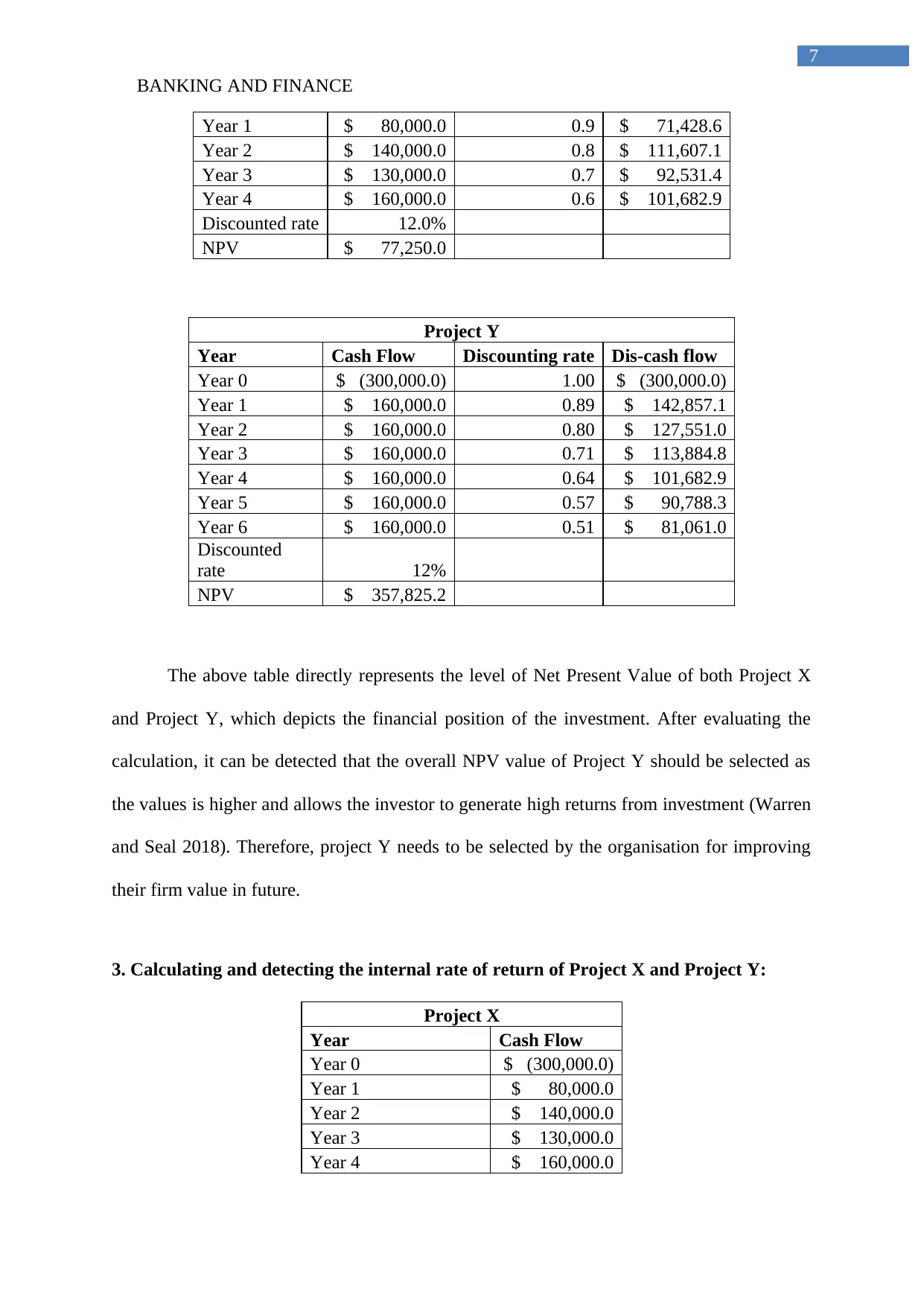

Project Y

Year Cash Flow Discounting rate Dis-cash flow

Year 0 $ (300,000.0) 1.00 $ (300,000.0)

Year 1 $ 160,000.0 0.89 $ 142,857.1

Year 2 $ 160,000.0 0.80 $ 127,551.0

Year 3 $ 160,000.0 0.71 $ 113,884.8

Year 4 $ 160,000.0 0.64 $ 101,682.9

Year 5 $ 160,000.0 0.57 $ 90,788.3

Year 6 $ 160,000.0 0.51 $ 81,061.0

Discounted

rate 12%

NPV $ 357,825.2

The above table directly represents the level of Net Present Value of both Project X

and Project Y, which depicts the financial position of the investment. After evaluating the

calculation, it can be detected that the overall NPV value of Project Y should be selected as

the values is higher and allows the investor to generate high returns from investment (Warren

and Seal 2018). Therefore, project Y needs to be selected by the organisation for improving

their firm value in future.

3. Calculating and detecting the internal rate of return of Project X and Project Y:

Project X

Year Cash Flow

Year 0 $ (300,000.0)

Year 1 $ 80,000.0

Year 2 $ 140,000.0

Year 3 $ 130,000.0

Year 4 $ 160,000.0

7

Year 1 $ 80,000.0 0.9 $ 71,428.6

Year 2 $ 140,000.0 0.8 $ 111,607.1

Year 3 $ 130,000.0 0.7 $ 92,531.4

Year 4 $ 160,000.0 0.6 $ 101,682.9

Discounted rate 12.0%

NPV $ 77,250.0

Project Y

Year Cash Flow Discounting rate Dis-cash flow

Year 0 $ (300,000.0) 1.00 $ (300,000.0)

Year 1 $ 160,000.0 0.89 $ 142,857.1

Year 2 $ 160,000.0 0.80 $ 127,551.0

Year 3 $ 160,000.0 0.71 $ 113,884.8

Year 4 $ 160,000.0 0.64 $ 101,682.9

Year 5 $ 160,000.0 0.57 $ 90,788.3

Year 6 $ 160,000.0 0.51 $ 81,061.0

Discounted

rate 12%

NPV $ 357,825.2

The above table directly represents the level of Net Present Value of both Project X

and Project Y, which depicts the financial position of the investment. After evaluating the

calculation, it can be detected that the overall NPV value of Project Y should be selected as

the values is higher and allows the investor to generate high returns from investment (Warren

and Seal 2018). Therefore, project Y needs to be selected by the organisation for improving

their firm value in future.

3. Calculating and detecting the internal rate of return of Project X and Project Y:

Project X

Year Cash Flow

Year 0 $ (300,000.0)

Year 1 $ 80,000.0

Year 2 $ 140,000.0

Year 3 $ 130,000.0

Year 4 $ 160,000.0

BANKING AND FINANCE

8

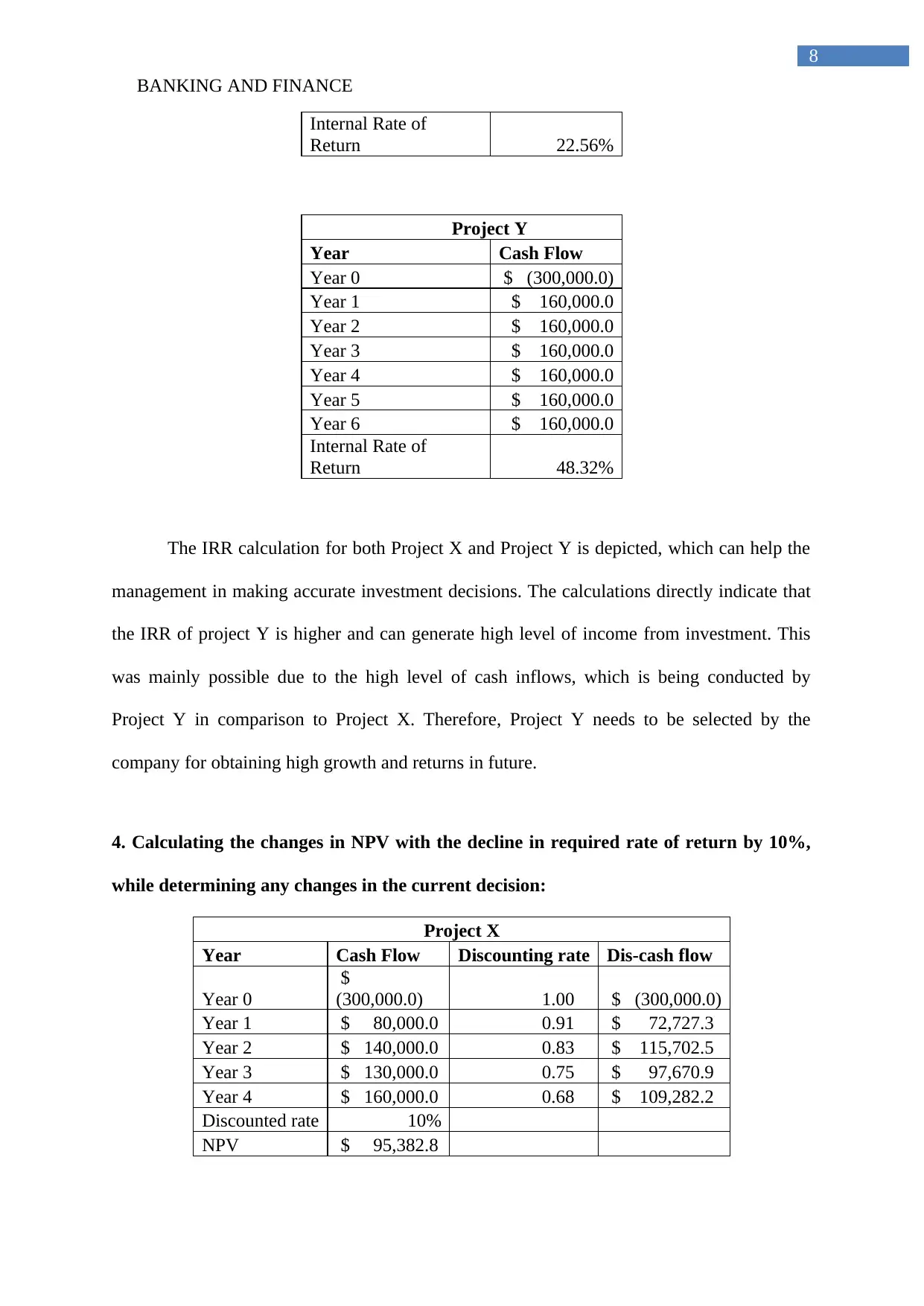

Internal Rate of

Return 22.56%

Project Y

Year Cash Flow

Year 0 $ (300,000.0)

Year 1 $ 160,000.0

Year 2 $ 160,000.0

Year 3 $ 160,000.0

Year 4 $ 160,000.0

Year 5 $ 160,000.0

Year 6 $ 160,000.0

Internal Rate of

Return 48.32%

The IRR calculation for both Project X and Project Y is depicted, which can help the

management in making accurate investment decisions. The calculations directly indicate that

the IRR of project Y is higher and can generate high level of income from investment. This

was mainly possible due to the high level of cash inflows, which is being conducted by

Project Y in comparison to Project X. Therefore, Project Y needs to be selected by the

company for obtaining high growth and returns in future.

4. Calculating the changes in NPV with the decline in required rate of return by 10%,

while determining any changes in the current decision:

Project X

Year Cash Flow Discounting rate Dis-cash flow

Year 0

$

(300,000.0) 1.00 $ (300,000.0)

Year 1 $ 80,000.0 0.91 $ 72,727.3

Year 2 $ 140,000.0 0.83 $ 115,702.5

Year 3 $ 130,000.0 0.75 $ 97,670.9

Year 4 $ 160,000.0 0.68 $ 109,282.2

Discounted rate 10%

NPV $ 95,382.8

8

Internal Rate of

Return 22.56%

Project Y

Year Cash Flow

Year 0 $ (300,000.0)

Year 1 $ 160,000.0

Year 2 $ 160,000.0

Year 3 $ 160,000.0

Year 4 $ 160,000.0

Year 5 $ 160,000.0

Year 6 $ 160,000.0

Internal Rate of

Return 48.32%

The IRR calculation for both Project X and Project Y is depicted, which can help the

management in making accurate investment decisions. The calculations directly indicate that

the IRR of project Y is higher and can generate high level of income from investment. This

was mainly possible due to the high level of cash inflows, which is being conducted by

Project Y in comparison to Project X. Therefore, Project Y needs to be selected by the

company for obtaining high growth and returns in future.

4. Calculating the changes in NPV with the decline in required rate of return by 10%,

while determining any changes in the current decision:

Project X

Year Cash Flow Discounting rate Dis-cash flow

Year 0

$

(300,000.0) 1.00 $ (300,000.0)

Year 1 $ 80,000.0 0.91 $ 72,727.3

Year 2 $ 140,000.0 0.83 $ 115,702.5

Year 3 $ 130,000.0 0.75 $ 97,670.9

Year 4 $ 160,000.0 0.68 $ 109,282.2

Discounted rate 10%

NPV $ 95,382.8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BANKING AND FINANCE

9

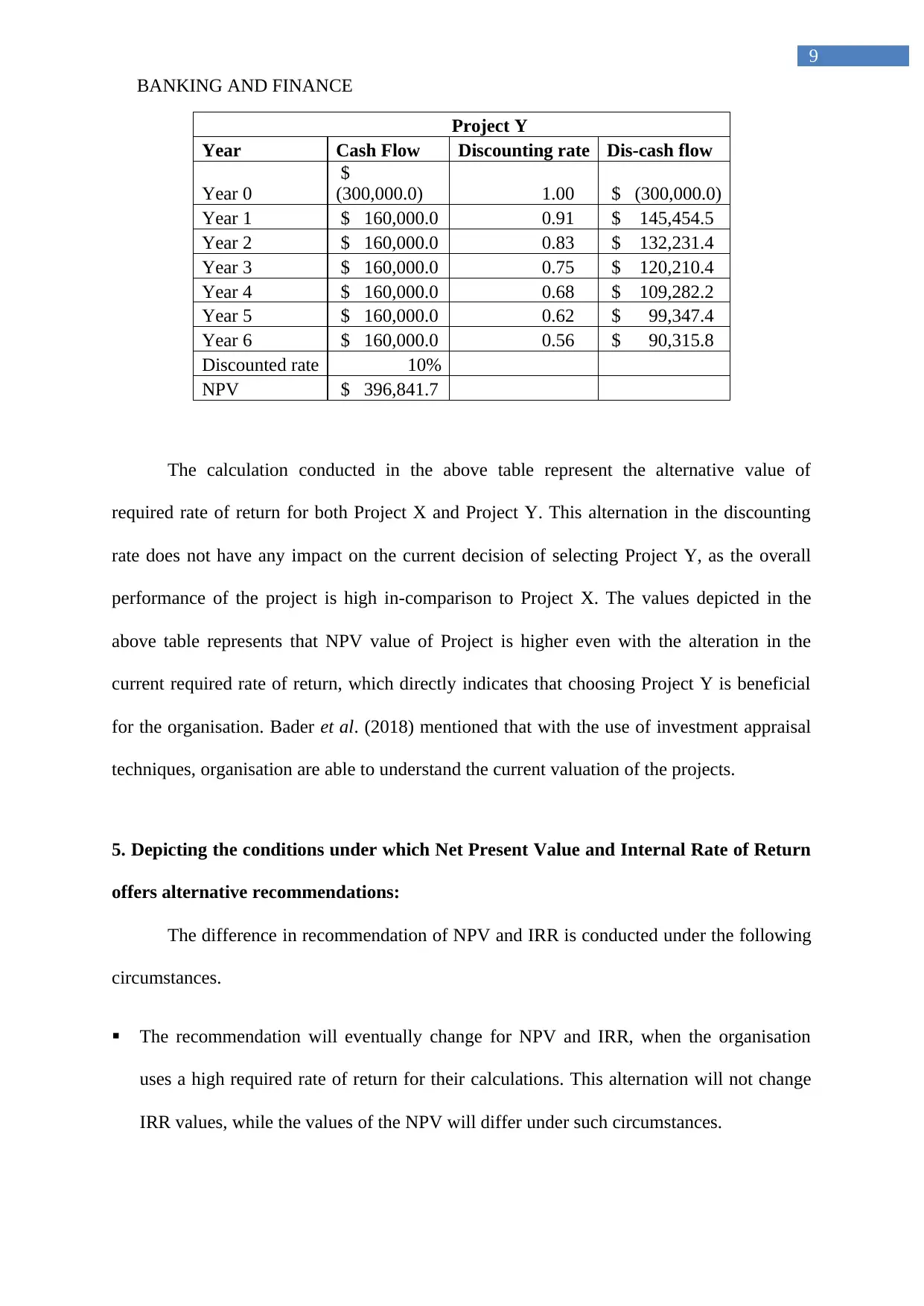

Project Y

Year Cash Flow Discounting rate Dis-cash flow

Year 0

$

(300,000.0) 1.00 $ (300,000.0)

Year 1 $ 160,000.0 0.91 $ 145,454.5

Year 2 $ 160,000.0 0.83 $ 132,231.4

Year 3 $ 160,000.0 0.75 $ 120,210.4

Year 4 $ 160,000.0 0.68 $ 109,282.2

Year 5 $ 160,000.0 0.62 $ 99,347.4

Year 6 $ 160,000.0 0.56 $ 90,315.8

Discounted rate 10%

NPV $ 396,841.7

The calculation conducted in the above table represent the alternative value of

required rate of return for both Project X and Project Y. This alternation in the discounting

rate does not have any impact on the current decision of selecting Project Y, as the overall

performance of the project is high in-comparison to Project X. The values depicted in the

above table represents that NPV value of Project is higher even with the alteration in the

current required rate of return, which directly indicates that choosing Project Y is beneficial

for the organisation. Bader et al. (2018) mentioned that with the use of investment appraisal

techniques, organisation are able to understand the current valuation of the projects.

5. Depicting the conditions under which Net Present Value and Internal Rate of Return

offers alternative recommendations:

The difference in recommendation of NPV and IRR is conducted under the following

circumstances.

The recommendation will eventually change for NPV and IRR, when the organisation

uses a high required rate of return for their calculations. This alternation will not change

IRR values, while the values of the NPV will differ under such circumstances.

9

Project Y

Year Cash Flow Discounting rate Dis-cash flow

Year 0

$

(300,000.0) 1.00 $ (300,000.0)

Year 1 $ 160,000.0 0.91 $ 145,454.5

Year 2 $ 160,000.0 0.83 $ 132,231.4

Year 3 $ 160,000.0 0.75 $ 120,210.4

Year 4 $ 160,000.0 0.68 $ 109,282.2

Year 5 $ 160,000.0 0.62 $ 99,347.4

Year 6 $ 160,000.0 0.56 $ 90,315.8

Discounted rate 10%

NPV $ 396,841.7

The calculation conducted in the above table represent the alternative value of

required rate of return for both Project X and Project Y. This alternation in the discounting

rate does not have any impact on the current decision of selecting Project Y, as the overall

performance of the project is high in-comparison to Project X. The values depicted in the

above table represents that NPV value of Project is higher even with the alteration in the

current required rate of return, which directly indicates that choosing Project Y is beneficial

for the organisation. Bader et al. (2018) mentioned that with the use of investment appraisal

techniques, organisation are able to understand the current valuation of the projects.

5. Depicting the conditions under which Net Present Value and Internal Rate of Return

offers alternative recommendations:

The difference in recommendation of NPV and IRR is conducted under the following

circumstances.

The recommendation will eventually change for NPV and IRR, when the organisation

uses a high required rate of return for their calculations. This alternation will not change

IRR values, while the values of the NPV will differ under such circumstances.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BANKING AND FINANCE

10

The cash flow timing will also have negative impact on the performance IRR, where the

alternations in the cash flow will alter the values of IRR and even lead it to negative

(Lindvall and Larsson 2017).

The third alternations that can affect the recommendation of IRR and NPV the is tenure

of the project. The time taken by the company in completing the project will directly alter

the output of IRR and NPV, which will differ the recommendations for each project.

10

The cash flow timing will also have negative impact on the performance IRR, where the

alternations in the cash flow will alter the values of IRR and even lead it to negative

(Lindvall and Larsson 2017).

The third alternations that can affect the recommendation of IRR and NPV the is tenure

of the project. The time taken by the company in completing the project will directly alter

the output of IRR and NPV, which will differ the recommendations for each project.

BANKING AND FINANCE

11

References and Bibliography:

Au.finance.yahoo.com. (2018). Yahoo is now a part of Oath. [online] Available at:

https://au.finance.yahoo.com/ [Accessed 16 Sep. 2018].

Bader, A., Al-Nawaiseh, H.N. and Nawaiseh, M.E., 2018. Capital Investment Appraisal

Practices of Jordan Industrial Companies: A Survey of Current Usage. International

Research Journal of Applied Finance, 9(4), pp.146-161.

Briston, R.J., 2017. The stock exchange and investment analysis. Routledge.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

DeBoeuf, D., Lee, H., Johnson, D. and Masharuev, M., 2018. Purchasing power return, a new

paradigm of capital investment appraisal. Managerial Finance, 44(2), pp.241-256.

Edwards, R.D., Magee, J. and Bassetti, W.H.C., 2018. Technical analysis of stock trends.

CRC Press.

Li, F.G. and Trutnevyte, E., 2017. Investment appraisal of cost-optimal and near-optimal

pathways for the UK electricity sector transition to 2050. Applied energy, 189, pp.89-109.

Lindvall, N. and Larsson, A., 2017. Investment Appraisal in the Public Sector–Incorporating

Flexibility and Environmental Impact. Journal of Advanced Management Science Vol, 5(3).

Lokman, S., Volker, D., Zijlstra-Vlasveld, M.C., Brouwers, E.P., Boon, B., Beekman, A.T.,

Smit, F. and Van der Feltz-Cornelis, C.M., 2017. Return-to-work intervention versus usual

care for sick-listed employees: health-economic investment appraisal alongside a cluster

randomised trial. BMJ open, 7(10), p.e016348.

11

References and Bibliography:

Au.finance.yahoo.com. (2018). Yahoo is now a part of Oath. [online] Available at:

https://au.finance.yahoo.com/ [Accessed 16 Sep. 2018].

Bader, A., Al-Nawaiseh, H.N. and Nawaiseh, M.E., 2018. Capital Investment Appraisal

Practices of Jordan Industrial Companies: A Survey of Current Usage. International

Research Journal of Applied Finance, 9(4), pp.146-161.

Briston, R.J., 2017. The stock exchange and investment analysis. Routledge.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

DeBoeuf, D., Lee, H., Johnson, D. and Masharuev, M., 2018. Purchasing power return, a new

paradigm of capital investment appraisal. Managerial Finance, 44(2), pp.241-256.

Edwards, R.D., Magee, J. and Bassetti, W.H.C., 2018. Technical analysis of stock trends.

CRC Press.

Li, F.G. and Trutnevyte, E., 2017. Investment appraisal of cost-optimal and near-optimal

pathways for the UK electricity sector transition to 2050. Applied energy, 189, pp.89-109.

Lindvall, N. and Larsson, A., 2017. Investment Appraisal in the Public Sector–Incorporating

Flexibility and Environmental Impact. Journal of Advanced Management Science Vol, 5(3).

Lokman, S., Volker, D., Zijlstra-Vlasveld, M.C., Brouwers, E.P., Boon, B., Beekman, A.T.,

Smit, F. and Van der Feltz-Cornelis, C.M., 2017. Return-to-work intervention versus usual

care for sick-listed employees: health-economic investment appraisal alongside a cluster

randomised trial. BMJ open, 7(10), p.e016348.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.