FIN20013 - Analyzing Banking Operations & Governance of Two Banks

VerifiedAdded on 2023/06/10

|16

|2137

|469

Report

AI Summary

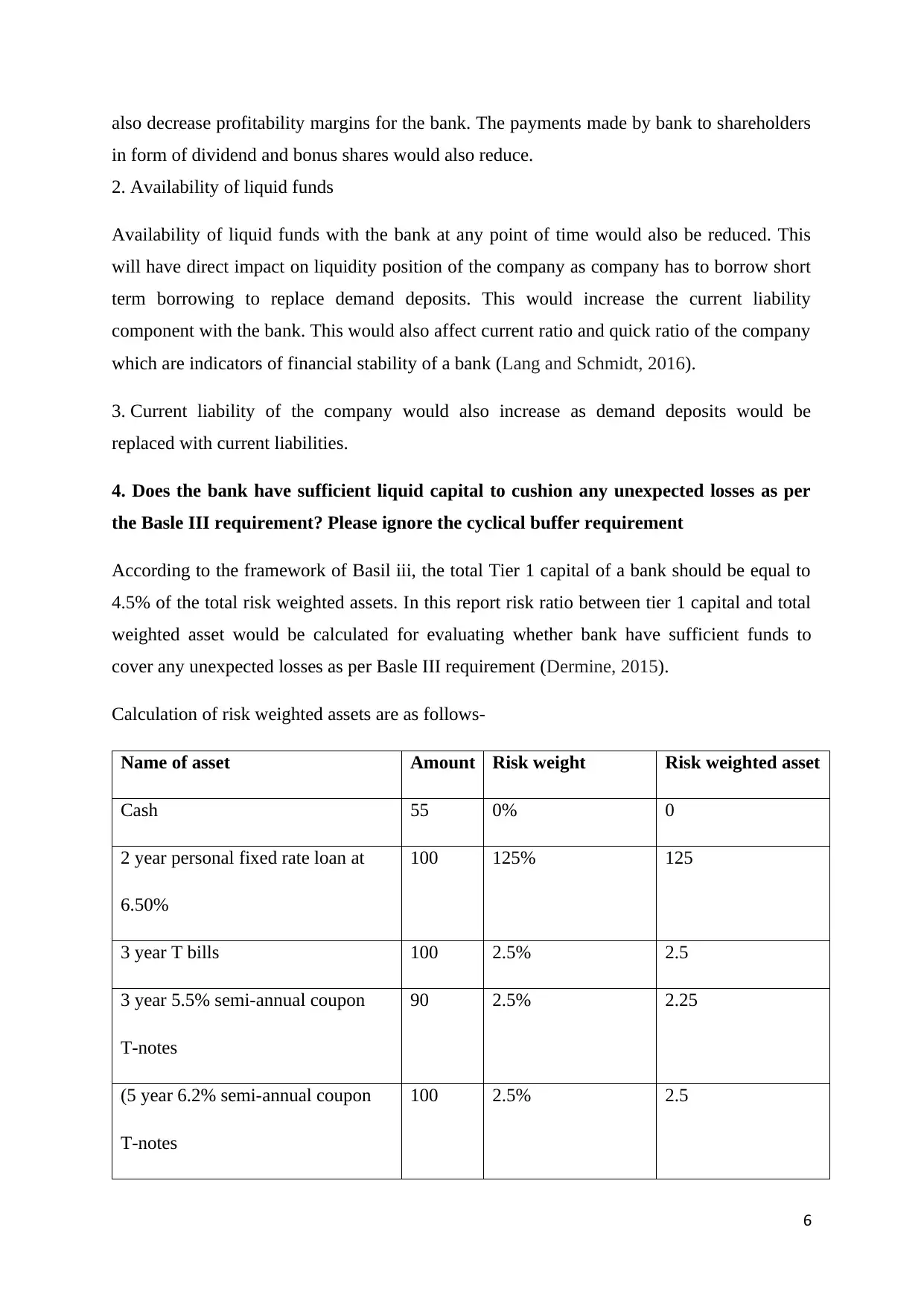

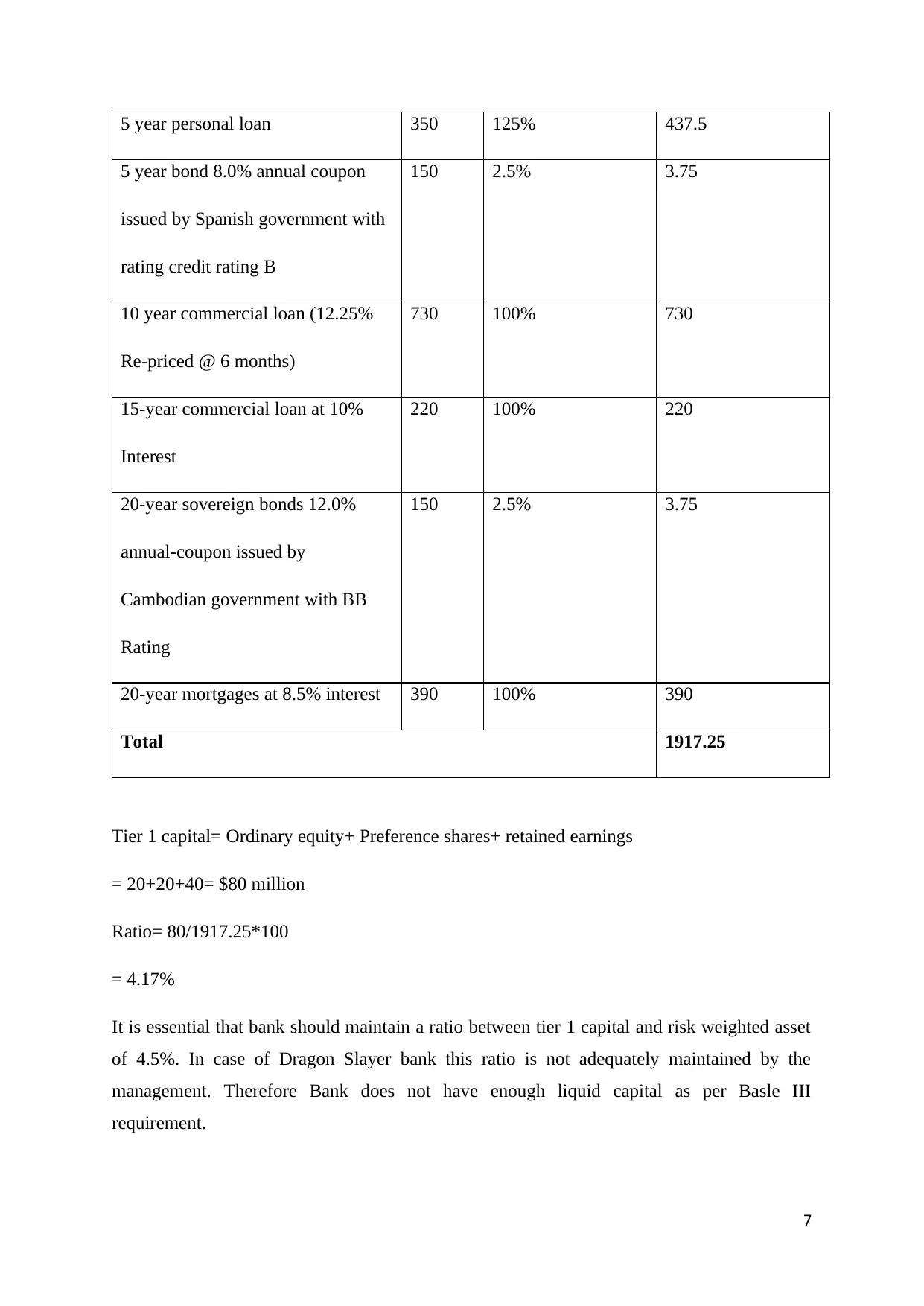

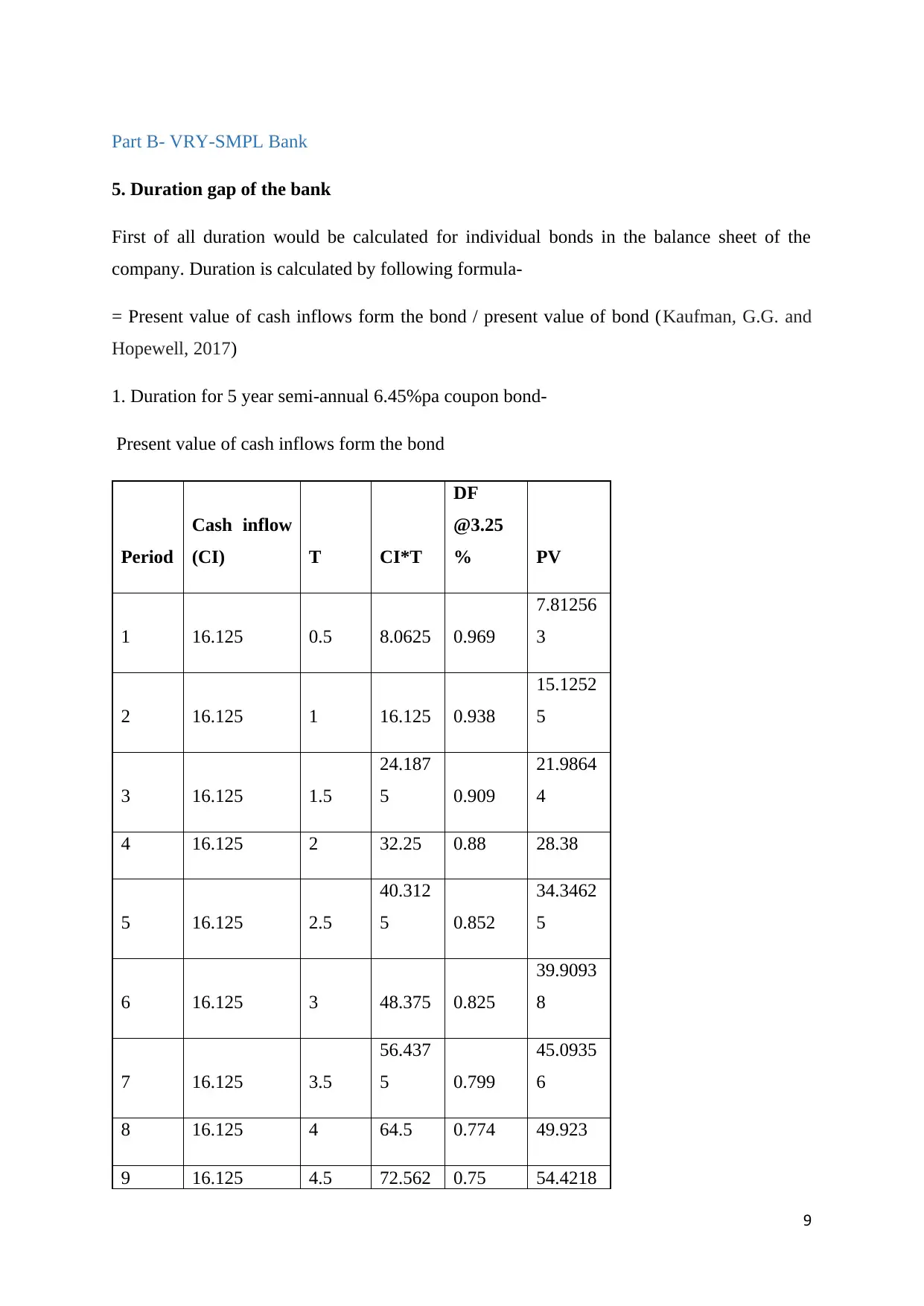

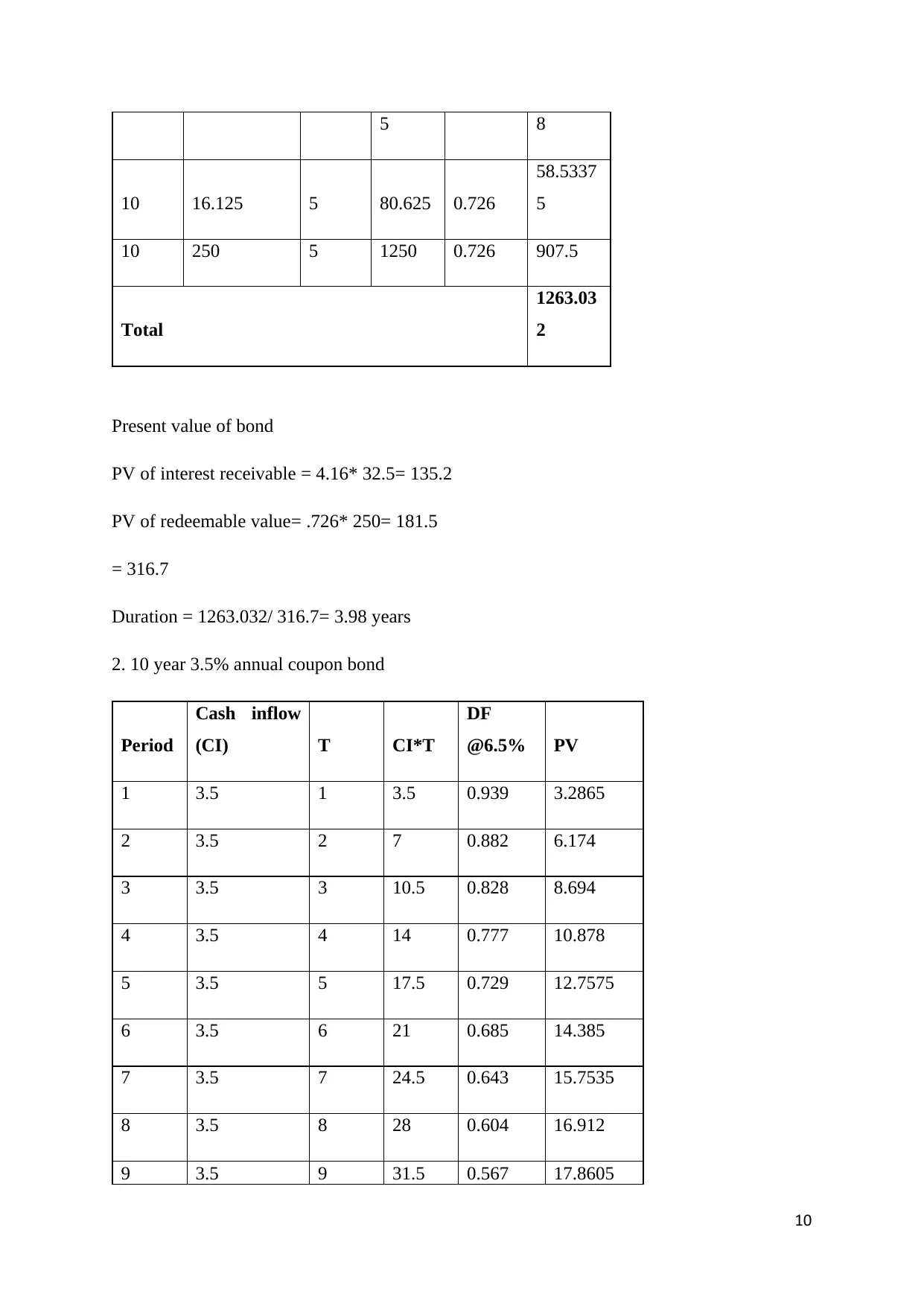

This report provides a comprehensive analysis of two banks, Dragon Slayer Bank and VRY-SMPL Bank, focusing on their banking operations and governance. For Dragon Slayer Bank, the analysis includes calculating the cumulative re-pricing gap for different planning periods, assessing the impact of interest rate changes on net income, evaluating the consequences of decreased demand deposits on asset-liability management, and determining the bank's compliance with Basel III liquidity requirements. The report calculates risk-weighted assets and the Tier 1 capital ratio to assess the bank's ability to cushion unexpected losses. For VRY-SMPL Bank, the report calculates the duration gap by determining the duration of various assets and liabilities, estimates the change in net worth resulting from changes in market yield, and calculates the maturity gap. The analysis uses financial formulas and frameworks to evaluate the financial health and risk management practices of both banks.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.