BAO2202 - Financial Accounting | Assignment

Added on 2020-03-01

17 Pages4922 Words183 Views

BAO2202Financial AccountingAssignment Semester 2 2017

TABLE OF CONTENTSPart I...........................................................................................................................................3Abstract..................................................................................................................................3Introduction............................................................................................................................3Part I.......................................................................................................................................3Conclusion..............................................................................................................................3Bibliography...........................................................................................................................3Part II..........................................................................................................................................4Abstract..................................................................................................................................4Introduction............................................................................................................................4Part II......................................................................................................................................4Conclusion..............................................................................................................................4Bibliography...........................................................................................................................4Part III........................................................................................................................................5Abstract..................................................................................................................................5Introduction............................................................................................................................5Part III....................................................................................................................................5Conclusion..............................................................................................................................5Bibliography...........................................................................................................................5

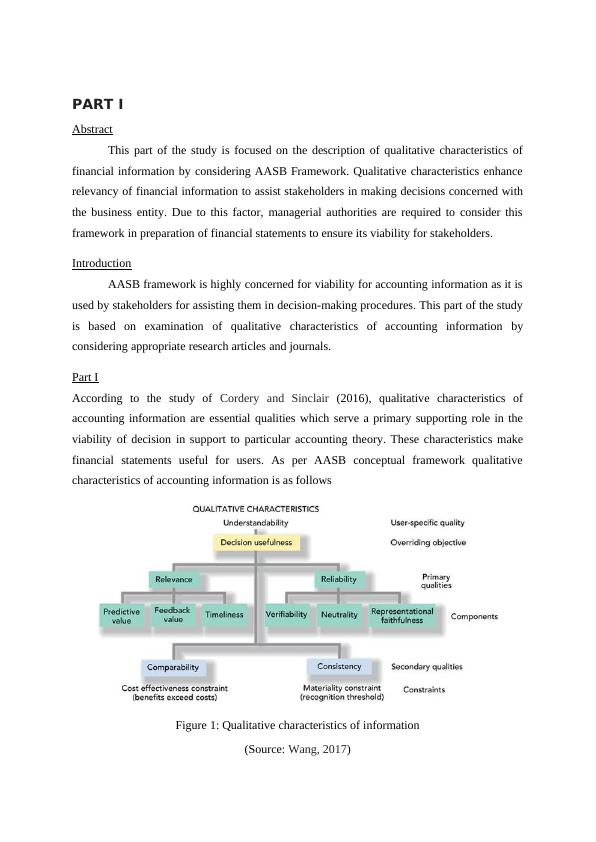

PART IAbstractThis part of the study is focused on the description of qualitative characteristics offinancial information by considering AASB Framework. Qualitative characteristics enhancerelevancy of financial information to assist stakeholders in making decisions concerned withthe business entity. Due to this factor, managerial authorities are required to consider thisframework in preparation of financial statements to ensure its viability for stakeholders. IntroductionAASB framework is highly concerned for viability for accounting information as it isused by stakeholders for assisting them in decision-making procedures. This part of the studyis based on examination of qualitative characteristics of accounting information byconsidering appropriate research articles and journals.Part IAccording to the study of Cordery and Sinclair (2016), qualitative characteristics ofaccounting information are essential qualities which serve a primary supporting role in theviability of decision in support to particular accounting theory. These characteristics makefinancial statements useful for users. As per AASB conceptual framework qualitativecharacteristics of accounting information is as followsFigure 1: Qualitative characteristics of information(Source: Wang, 2017)

The fundamental qualitative characteristic of accounting information is relevance andfaithful representation. Both of these qualities are important, if the information is 100%reliable but not relevant, then it will be of no use. On the other hand, accurate informationconsists less or no value if the same is not reliable (Amendments to the AustralianConceptual Framework, 2013). These qualities are enumerated as below and are inclusive ofthe elements which will make these qualities more desirable. In addition to two secondaryqualities are considers which are comparability and consistency. These characteristics mustbe steady to each other. The information must be relevant as it helps users to determine the past, current andfuture capacity of generating income of the business. Relevant information can makesignificant in the opinion of the user as decision requires either predictive or confirmatoryvalue or both. Relevance also consists a significant element which is timeliness. Informationmust be provided at the right time to the user to enable its use in the process of decisionmaking (Barker and Penman, 2016). Further, reliability is an amount on which theinformation is verifiable as it assists in assuring the users that the information shows exactlythe economic phenomenon that seeks to represent them. The word objectivity refers toverifiability. Verifiability of accounting information ensures faithful representation ofeconomic phenomena. Accounting information provided statements must be verifiablewhether it is by the direct or indirect method. It means information must be supported byreliable evidence and individuals are in a position to cross check that cited information isrepresented in a faithful manner. This quality takes place when both measure andphenomenon makes an agreement; it claims to be represented. In accordance with the viewpoint of Collier (2015), faithful representation does notrefer to complete accuracy of financial aspects but refers that provide information is free fromerrors and omissions. For example, estimation in disclosure or computation cannot beperfectly accurate, but representation can be faithful if complete information is providedalong with the limitation of the estimation process and providing assurance that process isfree from error and biases. Although, faithful representation does not necessarily imply usefulinformation. For a better understanding of this aspect, following example can be considered;in the case where estimation is to be made regarding the amount by which carrying amount ofassets is required to be adjusted to provide effective on impairment on the value of the asset(Amendments to the Australian Conceptual Framework, 2013). In this case is disclosure ofimpairment is faithful representation only if the entity has applied an appropriate process in a

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Qualitative Features of Accounting Informationlg...

|15

|4707

|162

Qualitative Characteristics of Accounting Informationlg...

|20

|5020

|158

Development in Accounting - Reportlg...

|9

|2584

|38

ACCT6007 Financial Accounting Theory and Practice Task 2022lg...

|9

|1864

|21

BAO2202 Accounting Assignment: Accounting Treatmentlg...

|20

|5195

|154

Report on Critical Analysis of PPElg...

|8

|1910

|149