Comparison of Barclays and Standard Chartered monthly stock return performance

VerifiedAdded on 2023/06/10

|16

|4094

|469

AI Summary

This article provides a brief description of Barclays and Standard Chartered Plc. It compares and contrasts their monthly stock return performance and provides stock recommendations. The article also includes portfolio formation and analysis, calculation of mean, variance, and standard deviation of portfolio returns, trade-off between mean return and standard deviation of the portfolio, and indicating efficient frontier in a trade-off graph. The subject of the article is finance and investments. No course code or college/university is mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INDIVIDUAL

ASSIGNMENT

ASSIGNMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

PART 1............................................................................................................................................3

Brief description of Company A and Company B.......................................................................3

Comparison and contrasting between Barclays and Standard Chartered monthly stock return

performance.................................................................................................................................4

Comment on result and Stock Recommendation.........................................................................5

2. Portfolio formation and analysis..............................................................................................5

a. Calculation of mean, variance and standard deviation of portfolio returns.............................5

b. Trade – Off between mean return and standard deviation of the portfolio.............................8

c. Indicating Efficient Frontier in a Trade – off graph................................................................9

d. Minimum Variance Portfolio.................................................................................................10

e. Advise to investor on the basis of above findings.................................................................12

PART 2..........................................................................................................................................13

1. Calculation of investor’s required rate of return on company A’s equity.............................13

2. Valuation of company A’s equity..........................................................................................14

3. Comparison of calculated equity value with market value (or current stock price) of the

company.....................................................................................................................................14

REFERENCES..............................................................................................................................15

Books and Journals....................................................................................................................15

PART 1............................................................................................................................................3

Brief description of Company A and Company B.......................................................................3

Comparison and contrasting between Barclays and Standard Chartered monthly stock return

performance.................................................................................................................................4

Comment on result and Stock Recommendation.........................................................................5

2. Portfolio formation and analysis..............................................................................................5

a. Calculation of mean, variance and standard deviation of portfolio returns.............................5

b. Trade – Off between mean return and standard deviation of the portfolio.............................8

c. Indicating Efficient Frontier in a Trade – off graph................................................................9

d. Minimum Variance Portfolio.................................................................................................10

e. Advise to investor on the basis of above findings.................................................................12

PART 2..........................................................................................................................................13

1. Calculation of investor’s required rate of return on company A’s equity.............................13

2. Valuation of company A’s equity..........................................................................................14

3. Comparison of calculated equity value with market value (or current stock price) of the

company.....................................................................................................................................14

REFERENCES..............................................................................................................................15

Books and Journals....................................................................................................................15

PART 1

Brief description of Company A and Company B

Company A: Barclays Plc

Barclays is a British multinational universal bank having its headquarter in London,

England which was founded in the year 1630. Barclay is basically operating as two divisions i.e.,

Barclays UK and Barclays International. The company is a public limited company and primarily

listed on London Stock Exchange (LSE). Secondly, Barclays is also listed on New York Stock

Exchange. The company generally operates in over 40 countries and provide employment to

more than 80000 people. It is one of the fifth largest bank in Europe because of its total assets

value of £1.384 trillion as per 2021 annual report (Augar, 2018). Basically, Barclays products &

comprises of retail banking, consumer credit cards, wealth management service, private banking,

wholesale banking, investment, commercial banking etc.

As per 2021 annual report, the total revenue of Barclays includes £21.940 billion which is

higher than the previous year total revenue of 21.766 billion. The net income and operating

income of the company in the year 2021 was £7.226 billion and 8.414 billion respectively.

Further, the earning per share of Barclays in the year 2021 is $2.01 that is higher than the year

2020 of $0.44 EPS. The company have market share of around 10.50% beside of the top

competitors such as HSBC, JP Morgan Securities Plc whose market shares is lower than

Barclays with 6.75% and 6.07% respectively (Nyanaro and Bett, 2018).

Company B: Standard Chartered Plc

Standard Chartered Plc is a British multinational banking and financial service public

limited company that was founded in the year 1853. The company have its headquarter in

London, England. The company basically operates a network of more than 1200 branches and

outlet in more than 70 countries in order to enhance their international presence. The products

and service of Standard Chartered Plc is comprising of credit cards, consumer banking, corporate

banking, investment, private, mortgage loan, wealth management etc. The company is primarily

listed on the London Stock Exchange (LSE). It is one of the largest international bank. The total

number of employees worked with Standard Chartered Plc is 85000 employees. The total

revenue of the company in the year 2021 is US$ 337 million which was higher than the year

Brief description of Company A and Company B

Company A: Barclays Plc

Barclays is a British multinational universal bank having its headquarter in London,

England which was founded in the year 1630. Barclay is basically operating as two divisions i.e.,

Barclays UK and Barclays International. The company is a public limited company and primarily

listed on London Stock Exchange (LSE). Secondly, Barclays is also listed on New York Stock

Exchange. The company generally operates in over 40 countries and provide employment to

more than 80000 people. It is one of the fifth largest bank in Europe because of its total assets

value of £1.384 trillion as per 2021 annual report (Augar, 2018). Basically, Barclays products &

comprises of retail banking, consumer credit cards, wealth management service, private banking,

wholesale banking, investment, commercial banking etc.

As per 2021 annual report, the total revenue of Barclays includes £21.940 billion which is

higher than the previous year total revenue of 21.766 billion. The net income and operating

income of the company in the year 2021 was £7.226 billion and 8.414 billion respectively.

Further, the earning per share of Barclays in the year 2021 is $2.01 that is higher than the year

2020 of $0.44 EPS. The company have market share of around 10.50% beside of the top

competitors such as HSBC, JP Morgan Securities Plc whose market shares is lower than

Barclays with 6.75% and 6.07% respectively (Nyanaro and Bett, 2018).

Company B: Standard Chartered Plc

Standard Chartered Plc is a British multinational banking and financial service public

limited company that was founded in the year 1853. The company have its headquarter in

London, England. The company basically operates a network of more than 1200 branches and

outlet in more than 70 countries in order to enhance their international presence. The products

and service of Standard Chartered Plc is comprising of credit cards, consumer banking, corporate

banking, investment, private, mortgage loan, wealth management etc. The company is primarily

listed on the London Stock Exchange (LSE). It is one of the largest international bank. The total

number of employees worked with Standard Chartered Plc is 85000 employees. The total

revenue of the company in the year 2021 is US$ 337 million which was higher than the year

2020 of US$227 million. Further, the net income and operating income of the company in the

year 2021 was US$2.313 billion and US$ 3.347 billion respectively (Jun and Yoon, 2020).

The closest competitors of Standard Chartered are HDFC but the average customer rating

of Standard Chartered is 4.6 and HDFC is 4.5. This indicate that the company are highly focused

towards their customer service enhancement. Standard Chartered Plc annual earnings per share

in the year 2021 was $0.6 which was 486.41% higher than previous year EPS of $0.5. The

largest shareholder of Standard Chartered Plc is Temasek Holdings (Private) Limited with the

17% of share holdings (Mbai, Ngui and Ndiao, 2018). It is systematically an important bank as

per Financial Stability Board.

Comparison and contrasting between Barclays and Standard Chartered monthly stock return

performance

On the basis of the computation of mean, variance and standard deviation of both company

such as Barclays and standard chartered stock return, it is analysed that both risk and return are

higher in purchasing Barclays stocks. It is because the standard deviation of Standard chartered

is 9.04% while the standard deviation of Barclays Plc is 10.38%. This means that the risk is

lower in Standard Chartered shares. However, on the other hand, despite of lower risk in shares,

the return from Standard chartered stocks is negative. It is because the mean of Standard

chartered monthly stock return is -0.33%. But on the other hand, the mean of Barclays Plc

monthly stock return is positive 0.68%. This indicate that by taking a little higher risk and

investing the fund in Barclays stocks will provide the investors with positive and higher return as

compared to the investment in Standard Chartered stocks. On the basis of the standard deviation

calculation of both stock, it is analysed that the risk is higher in Barclays Plc but on the same side

with the analysis of mean calculation of both stock, it is analysed that the return is also higher in

Standard Chartered (Chiang, 2019).

So, on this basis it can be said that there is a positive correlation exist between risk and

return. The greater the risk, the higher the potential return. If the investor take risk by investing

the money in Barclay Plc than they able to earn higher return from the investment. Further, on

the basis of monthly stock return calculation of both stock, it is identified that Barclays average

return are higher than the average return of Standard Chartered. Hence, it means that low level of

year 2021 was US$2.313 billion and US$ 3.347 billion respectively (Jun and Yoon, 2020).

The closest competitors of Standard Chartered are HDFC but the average customer rating

of Standard Chartered is 4.6 and HDFC is 4.5. This indicate that the company are highly focused

towards their customer service enhancement. Standard Chartered Plc annual earnings per share

in the year 2021 was $0.6 which was 486.41% higher than previous year EPS of $0.5. The

largest shareholder of Standard Chartered Plc is Temasek Holdings (Private) Limited with the

17% of share holdings (Mbai, Ngui and Ndiao, 2018). It is systematically an important bank as

per Financial Stability Board.

Comparison and contrasting between Barclays and Standard Chartered monthly stock return

performance

On the basis of the computation of mean, variance and standard deviation of both company

such as Barclays and standard chartered stock return, it is analysed that both risk and return are

higher in purchasing Barclays stocks. It is because the standard deviation of Standard chartered

is 9.04% while the standard deviation of Barclays Plc is 10.38%. This means that the risk is

lower in Standard Chartered shares. However, on the other hand, despite of lower risk in shares,

the return from Standard chartered stocks is negative. It is because the mean of Standard

chartered monthly stock return is -0.33%. But on the other hand, the mean of Barclays Plc

monthly stock return is positive 0.68%. This indicate that by taking a little higher risk and

investing the fund in Barclays stocks will provide the investors with positive and higher return as

compared to the investment in Standard Chartered stocks. On the basis of the standard deviation

calculation of both stock, it is analysed that the risk is higher in Barclays Plc but on the same side

with the analysis of mean calculation of both stock, it is analysed that the return is also higher in

Standard Chartered (Chiang, 2019).

So, on this basis it can be said that there is a positive correlation exist between risk and

return. The greater the risk, the higher the potential return. If the investor take risk by investing

the money in Barclay Plc than they able to earn higher return from the investment. Further, on

the basis of monthly stock return calculation of both stock, it is identified that Barclays average

return are higher than the average return of Standard Chartered. Hence, it means that low level of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

uncertainty is associated with low return and high level of uncertainty associated with higher

return.

Comment on result and Stock Recommendation

On the basis of monthly stock return calculation from period January 2017 to December

2021 and analysis of the result of mean, variance and standard deviation, it is identified that the

risk and return both are high in Barclays stock. While on the other hand, both risk and return are

low in Standard Chartered Plc as compared to Barclay. From the result, it is analysing that if

investors invest its fund in Standard Chartered Plc than the risk will be low but they will get

negative return. On the other hand, if the investor invests the same amount in the Barclays stock

than the risk will be high but they will get positive and higher return. Hence, on this basis, it is

recommendable or advisable to investors that they should invest in Barclays stock rather than

Standard Chartered stock. It is because they will get the average monthly return of 0.68% with

the investment of money in Barclays stocks (Chiang and Zhang, 2018). However, the risk is high

in Barclays stock but it is recommendable to investors on the basis that there is a direct relation

between stock risk and return. The higher level of risk with higher level of return.

2. Portfolio formation and analysis

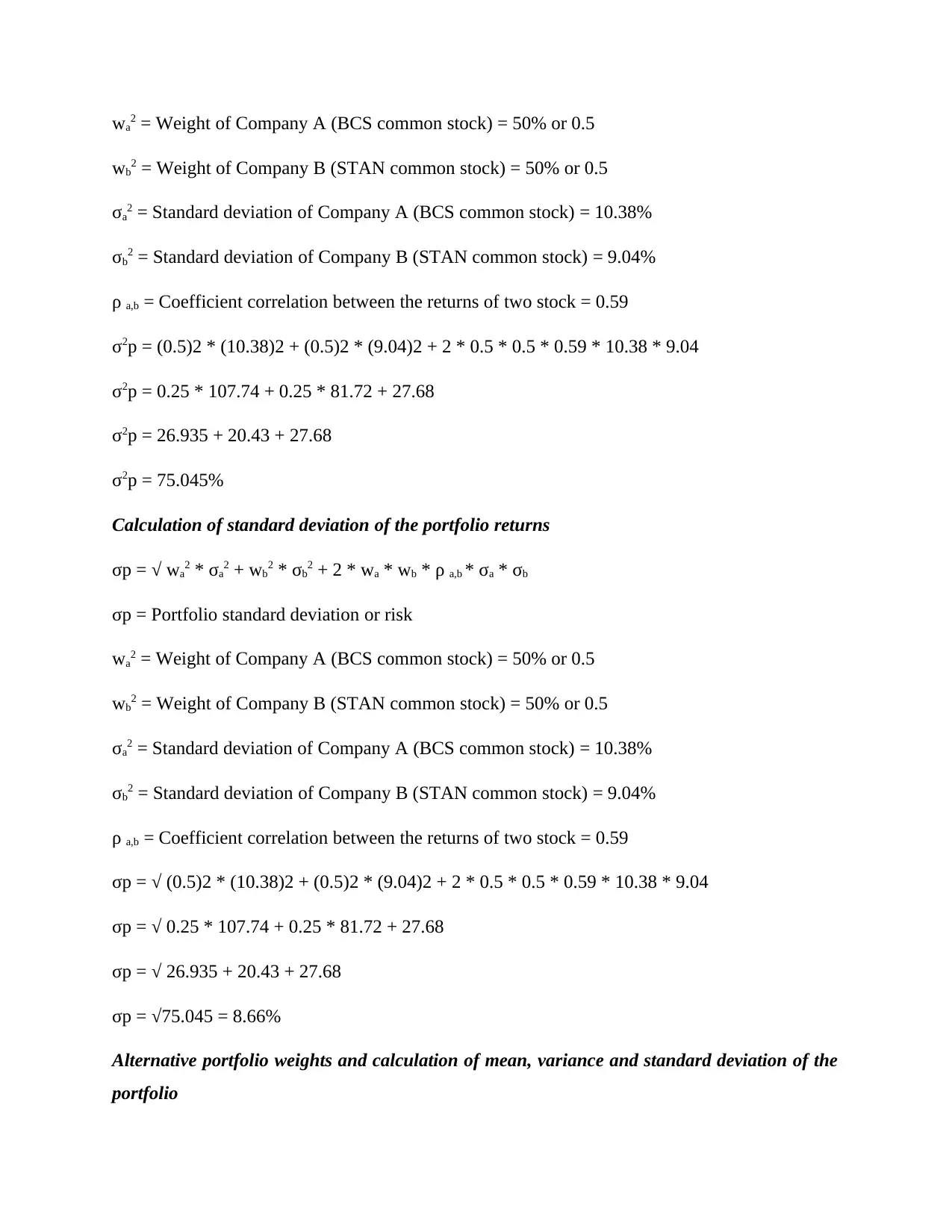

a. Calculation of mean, variance and standard deviation of portfolio returns

Calculation of mean or expected portfolio returns

Mean return or expected return of BCS stock = 0.68%

Weights assigned to BCS stock in the portfolio = 0.5

Mean return or expected return of STAN stock = -0.33%

Weights assigned to STAN stock in the portfolio = 0.5

Expected or Mean portfolio return = (0.68% * 0.5) + (-0.33% * 0.5) = 0.18%.

Calculation of Variance of the portfolio returns

σ2p = wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σ2p = Portfolio variance

return.

Comment on result and Stock Recommendation

On the basis of monthly stock return calculation from period January 2017 to December

2021 and analysis of the result of mean, variance and standard deviation, it is identified that the

risk and return both are high in Barclays stock. While on the other hand, both risk and return are

low in Standard Chartered Plc as compared to Barclay. From the result, it is analysing that if

investors invest its fund in Standard Chartered Plc than the risk will be low but they will get

negative return. On the other hand, if the investor invests the same amount in the Barclays stock

than the risk will be high but they will get positive and higher return. Hence, on this basis, it is

recommendable or advisable to investors that they should invest in Barclays stock rather than

Standard Chartered stock. It is because they will get the average monthly return of 0.68% with

the investment of money in Barclays stocks (Chiang and Zhang, 2018). However, the risk is high

in Barclays stock but it is recommendable to investors on the basis that there is a direct relation

between stock risk and return. The higher level of risk with higher level of return.

2. Portfolio formation and analysis

a. Calculation of mean, variance and standard deviation of portfolio returns

Calculation of mean or expected portfolio returns

Mean return or expected return of BCS stock = 0.68%

Weights assigned to BCS stock in the portfolio = 0.5

Mean return or expected return of STAN stock = -0.33%

Weights assigned to STAN stock in the portfolio = 0.5

Expected or Mean portfolio return = (0.68% * 0.5) + (-0.33% * 0.5) = 0.18%.

Calculation of Variance of the portfolio returns

σ2p = wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σ2p = Portfolio variance

wa2 = Weight of Company A (BCS common stock) = 50% or 0.5

wb2 = Weight of Company B (STAN common stock) = 50% or 0.5

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σ2p = (0.5)2 * (10.38)2 + (0.5)2 * (9.04)2 + 2 * 0.5 * 0.5 * 0.59 * 10.38 * 9.04

σ2p = 0.25 * 107.74 + 0.25 * 81.72 + 27.68

σ2p = 26.935 + 20.43 + 27.68

σ2p = 75.045%

Calculation of standard deviation of the portfolio returns

σp = √ wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σp = Portfolio standard deviation or risk

wa2 = Weight of Company A (BCS common stock) = 50% or 0.5

wb2 = Weight of Company B (STAN common stock) = 50% or 0.5

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σp = √ (0.5)2 * (10.38)2 + (0.5)2 * (9.04)2 + 2 * 0.5 * 0.5 * 0.59 * 10.38 * 9.04

σp = √ 0.25 * 107.74 + 0.25 * 81.72 + 27.68

σp = √ 26.935 + 20.43 + 27.68

σp = √75.045 = 8.66%

Alternative portfolio weights and calculation of mean, variance and standard deviation of the

portfolio

wb2 = Weight of Company B (STAN common stock) = 50% or 0.5

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σ2p = (0.5)2 * (10.38)2 + (0.5)2 * (9.04)2 + 2 * 0.5 * 0.5 * 0.59 * 10.38 * 9.04

σ2p = 0.25 * 107.74 + 0.25 * 81.72 + 27.68

σ2p = 26.935 + 20.43 + 27.68

σ2p = 75.045%

Calculation of standard deviation of the portfolio returns

σp = √ wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σp = Portfolio standard deviation or risk

wa2 = Weight of Company A (BCS common stock) = 50% or 0.5

wb2 = Weight of Company B (STAN common stock) = 50% or 0.5

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σp = √ (0.5)2 * (10.38)2 + (0.5)2 * (9.04)2 + 2 * 0.5 * 0.5 * 0.59 * 10.38 * 9.04

σp = √ 0.25 * 107.74 + 0.25 * 81.72 + 27.68

σp = √ 26.935 + 20.43 + 27.68

σp = √75.045 = 8.66%

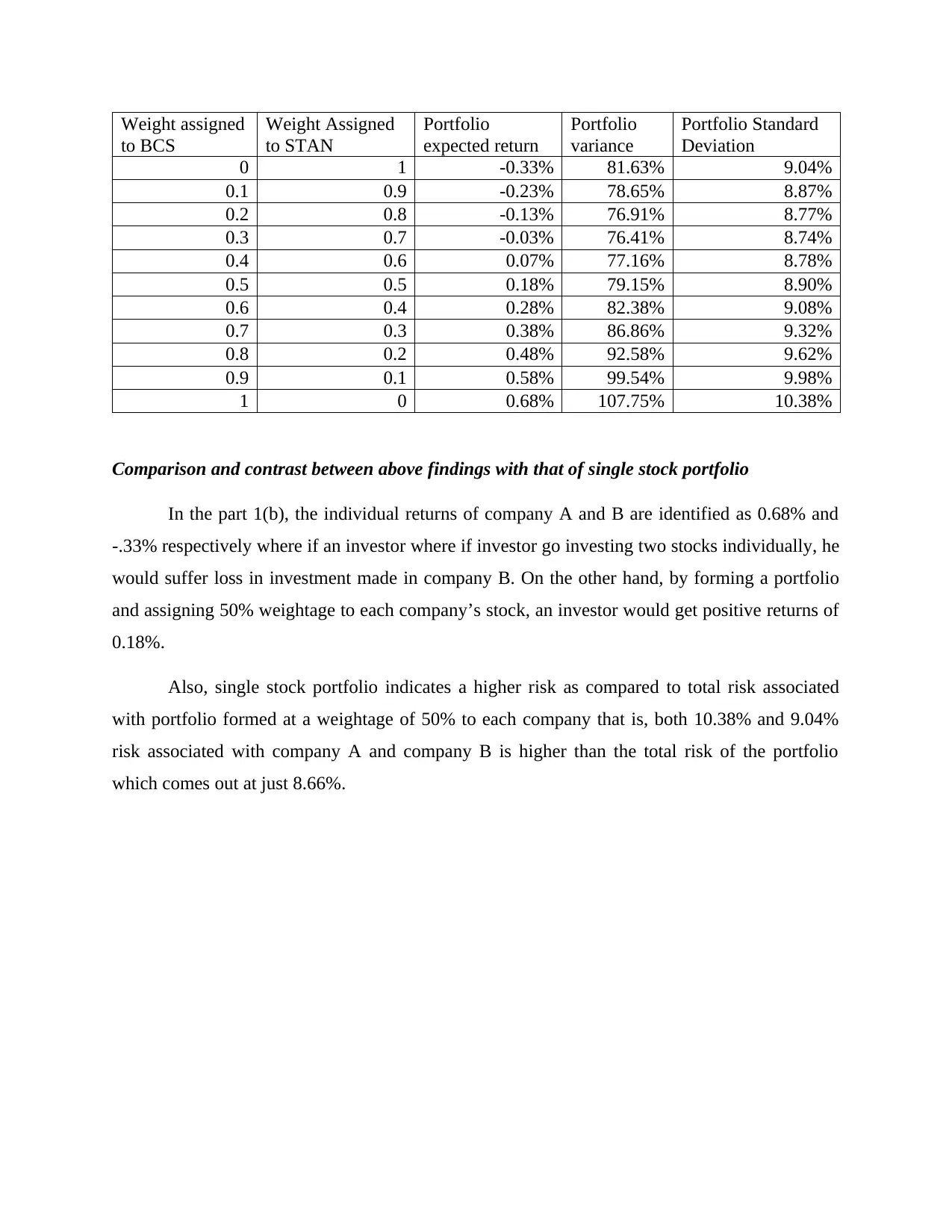

Alternative portfolio weights and calculation of mean, variance and standard deviation of the

portfolio

Weight assigned

to BCS

Weight Assigned

to STAN

Portfolio

expected return

Portfolio

variance

Portfolio Standard

Deviation

0 1 -0.33% 81.63% 9.04%

0.1 0.9 -0.23% 78.65% 8.87%

0.2 0.8 -0.13% 76.91% 8.77%

0.3 0.7 -0.03% 76.41% 8.74%

0.4 0.6 0.07% 77.16% 8.78%

0.5 0.5 0.18% 79.15% 8.90%

0.6 0.4 0.28% 82.38% 9.08%

0.7 0.3 0.38% 86.86% 9.32%

0.8 0.2 0.48% 92.58% 9.62%

0.9 0.1 0.58% 99.54% 9.98%

1 0 0.68% 107.75% 10.38%

Comparison and contrast between above findings with that of single stock portfolio

In the part 1(b), the individual returns of company A and B are identified as 0.68% and

-.33% respectively where if an investor where if investor go investing two stocks individually, he

would suffer loss in investment made in company B. On the other hand, by forming a portfolio

and assigning 50% weightage to each company’s stock, an investor would get positive returns of

0.18%.

Also, single stock portfolio indicates a higher risk as compared to total risk associated

with portfolio formed at a weightage of 50% to each company that is, both 10.38% and 9.04%

risk associated with company A and company B is higher than the total risk of the portfolio

which comes out at just 8.66%.

to BCS

Weight Assigned

to STAN

Portfolio

expected return

Portfolio

variance

Portfolio Standard

Deviation

0 1 -0.33% 81.63% 9.04%

0.1 0.9 -0.23% 78.65% 8.87%

0.2 0.8 -0.13% 76.91% 8.77%

0.3 0.7 -0.03% 76.41% 8.74%

0.4 0.6 0.07% 77.16% 8.78%

0.5 0.5 0.18% 79.15% 8.90%

0.6 0.4 0.28% 82.38% 9.08%

0.7 0.3 0.38% 86.86% 9.32%

0.8 0.2 0.48% 92.58% 9.62%

0.9 0.1 0.58% 99.54% 9.98%

1 0 0.68% 107.75% 10.38%

Comparison and contrast between above findings with that of single stock portfolio

In the part 1(b), the individual returns of company A and B are identified as 0.68% and

-.33% respectively where if an investor where if investor go investing two stocks individually, he

would suffer loss in investment made in company B. On the other hand, by forming a portfolio

and assigning 50% weightage to each company’s stock, an investor would get positive returns of

0.18%.

Also, single stock portfolio indicates a higher risk as compared to total risk associated

with portfolio formed at a weightage of 50% to each company that is, both 10.38% and 9.04%

risk associated with company A and company B is higher than the total risk of the portfolio

which comes out at just 8.66%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

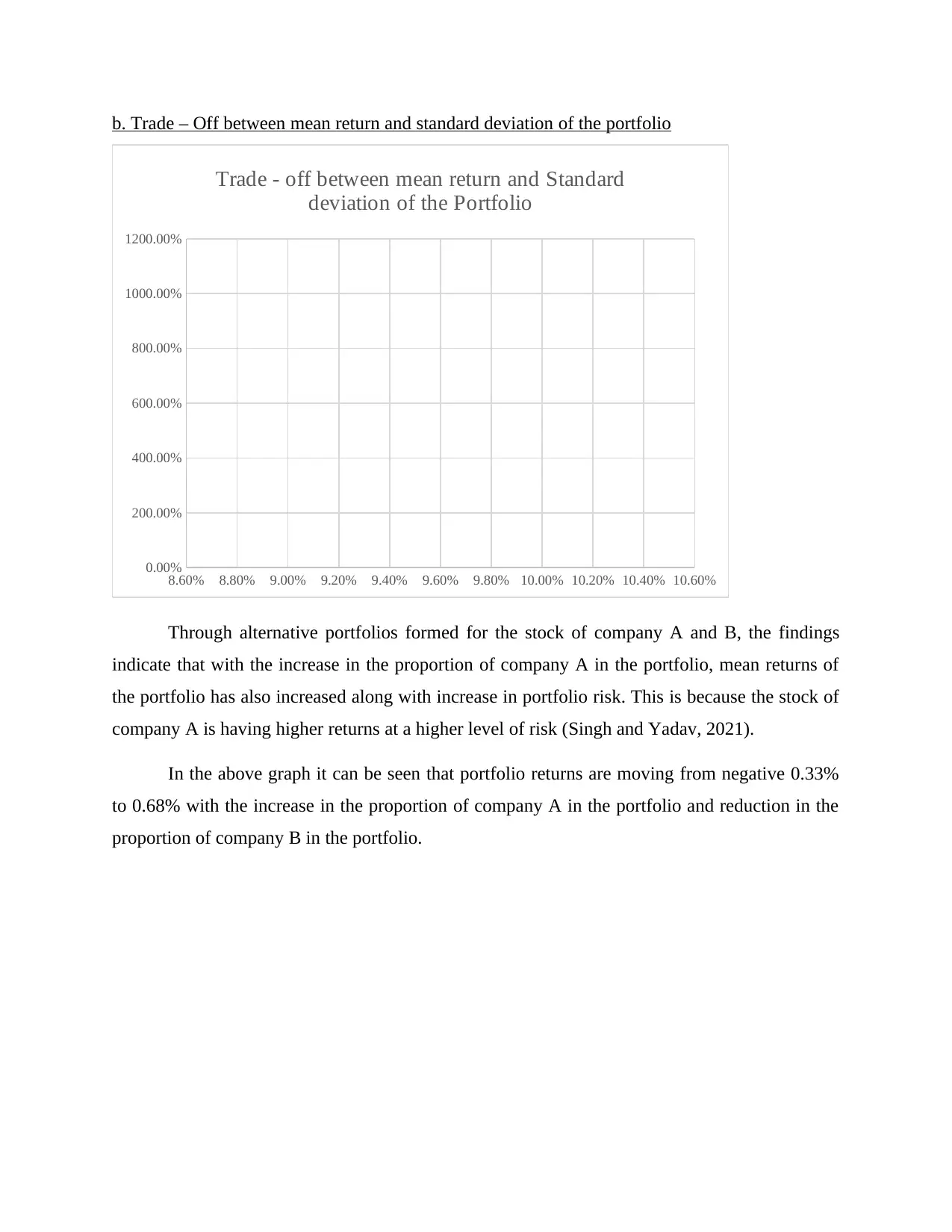

b. Trade – Off between mean return and standard deviation of the portfolio

8.60% 8.80% 9.00% 9.20% 9.40% 9.60% 9.80% 10.00% 10.20% 10.40% 10.60%

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

1200.00%

Trade - off between mean return and Standard

deviation of the Portfolio

Through alternative portfolios formed for the stock of company A and B, the findings

indicate that with the increase in the proportion of company A in the portfolio, mean returns of

the portfolio has also increased along with increase in portfolio risk. This is because the stock of

company A is having higher returns at a higher level of risk (Singh and Yadav, 2021).

In the above graph it can be seen that portfolio returns are moving from negative 0.33%

to 0.68% with the increase in the proportion of company A in the portfolio and reduction in the

proportion of company B in the portfolio.

8.60% 8.80% 9.00% 9.20% 9.40% 9.60% 9.80% 10.00% 10.20% 10.40% 10.60%

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

1200.00%

Trade - off between mean return and Standard

deviation of the Portfolio

Through alternative portfolios formed for the stock of company A and B, the findings

indicate that with the increase in the proportion of company A in the portfolio, mean returns of

the portfolio has also increased along with increase in portfolio risk. This is because the stock of

company A is having higher returns at a higher level of risk (Singh and Yadav, 2021).

In the above graph it can be seen that portfolio returns are moving from negative 0.33%

to 0.68% with the increase in the proportion of company A in the portfolio and reduction in the

proportion of company B in the portfolio.

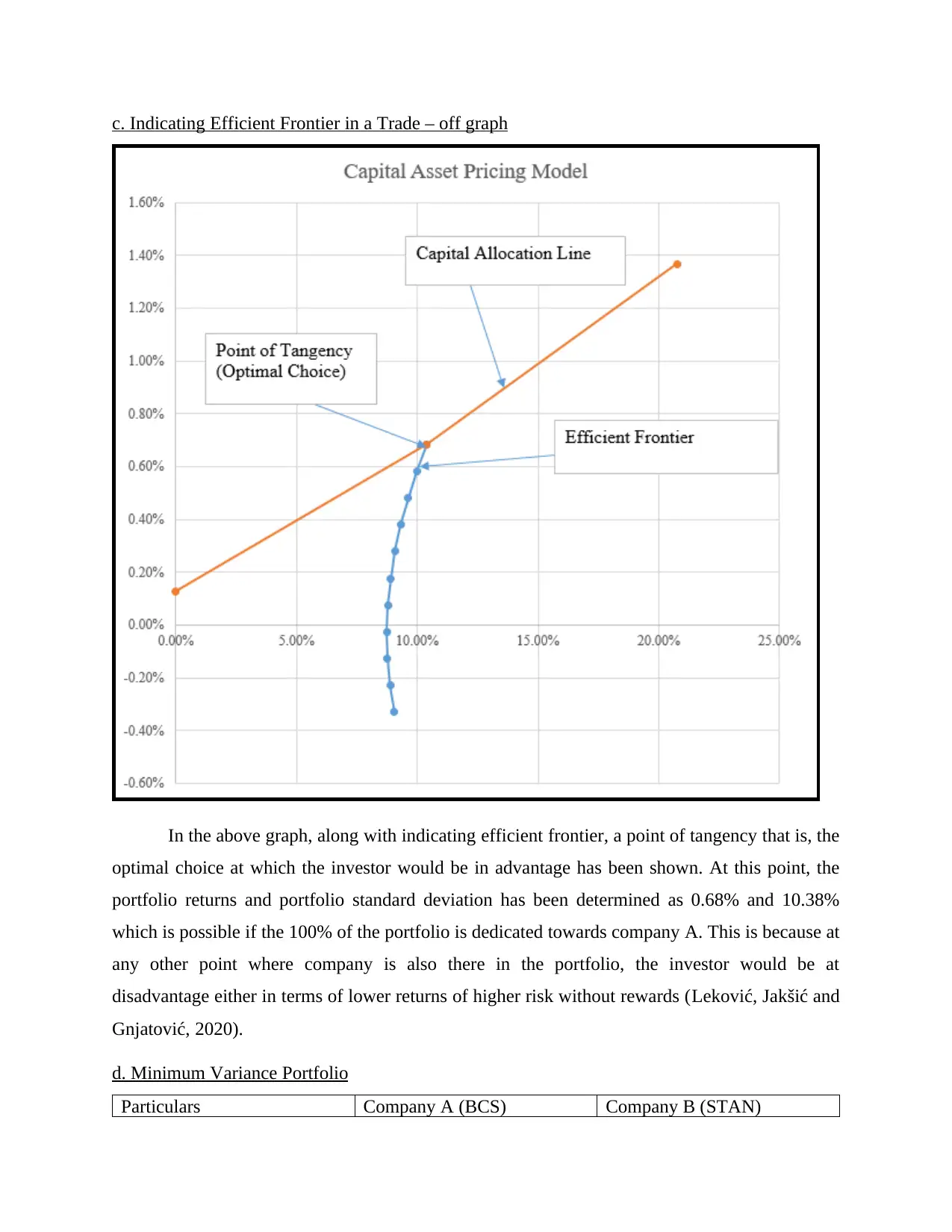

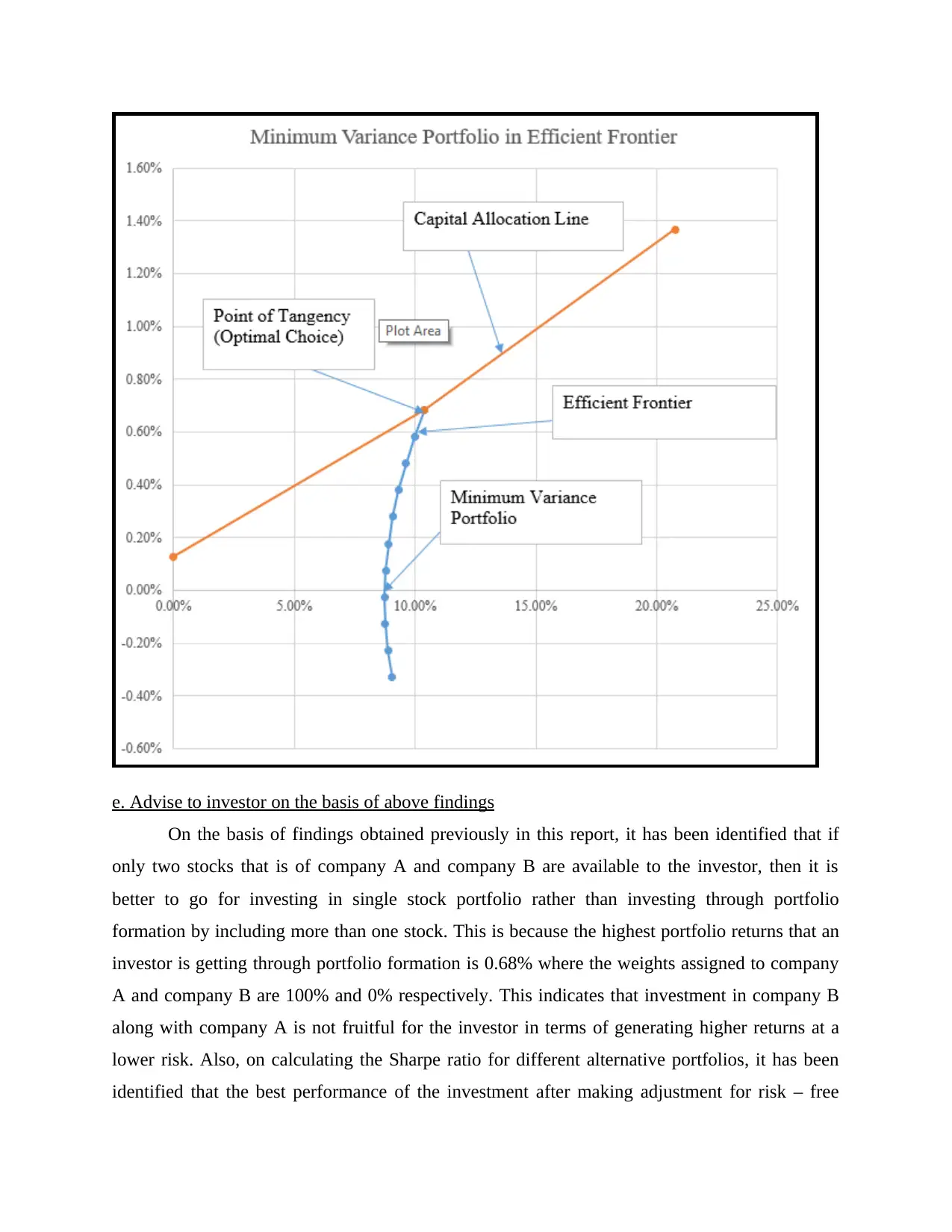

c. Indicating Efficient Frontier in a Trade – off graph

In the above graph, along with indicating efficient frontier, a point of tangency that is, the

optimal choice at which the investor would be in advantage has been shown. At this point, the

portfolio returns and portfolio standard deviation has been determined as 0.68% and 10.38%

which is possible if the 100% of the portfolio is dedicated towards company A. This is because at

any other point where company is also there in the portfolio, the investor would be at

disadvantage either in terms of lower returns of higher risk without rewards (Leković, Jakšić and

Gnjatović, 2020).

d. Minimum Variance Portfolio

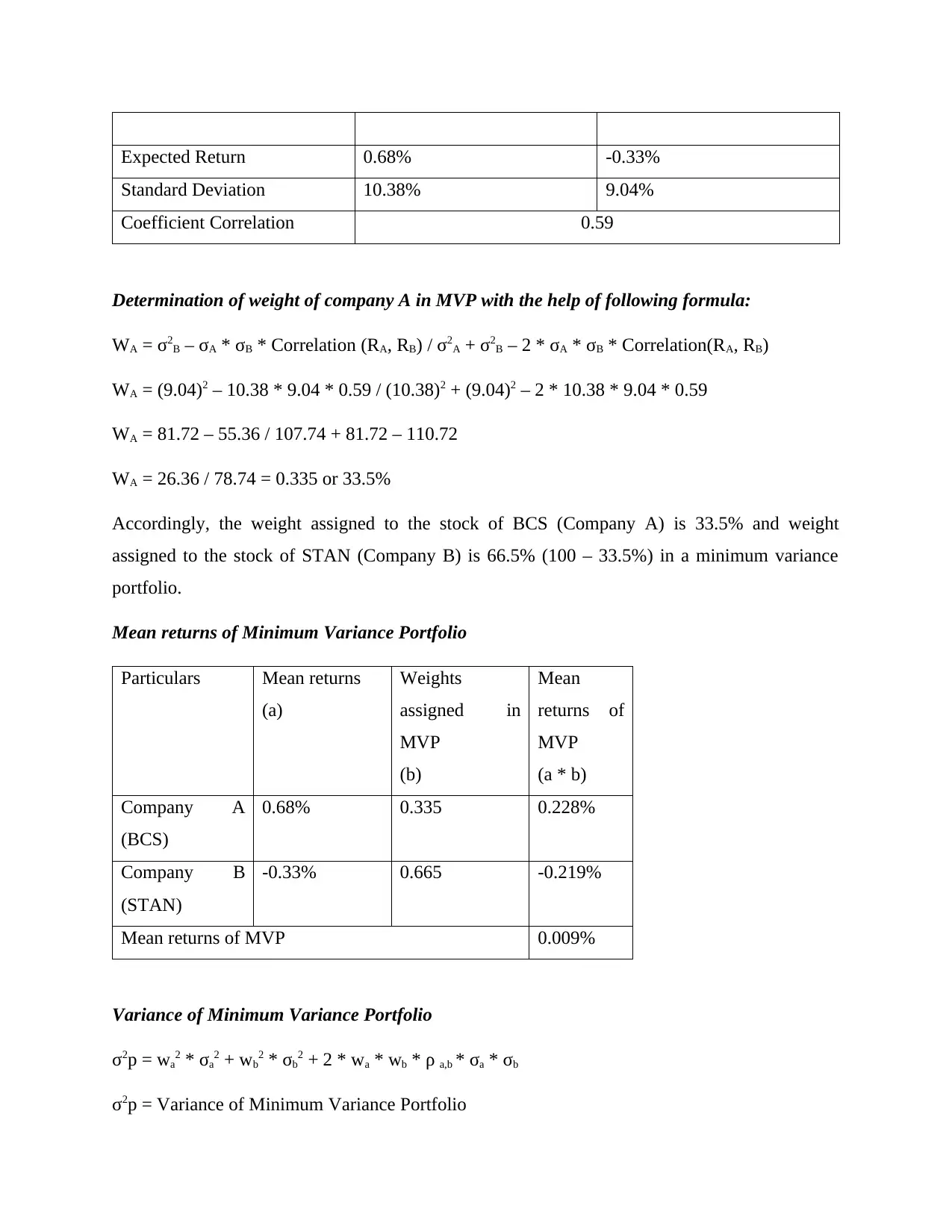

Particulars Company A (BCS) Company B (STAN)

In the above graph, along with indicating efficient frontier, a point of tangency that is, the

optimal choice at which the investor would be in advantage has been shown. At this point, the

portfolio returns and portfolio standard deviation has been determined as 0.68% and 10.38%

which is possible if the 100% of the portfolio is dedicated towards company A. This is because at

any other point where company is also there in the portfolio, the investor would be at

disadvantage either in terms of lower returns of higher risk without rewards (Leković, Jakšić and

Gnjatović, 2020).

d. Minimum Variance Portfolio

Particulars Company A (BCS) Company B (STAN)

Expected Return 0.68% -0.33%

Standard Deviation 10.38% 9.04%

Coefficient Correlation 0.59

Determination of weight of company A in MVP with the help of following formula:

WA = σ2B – σA * σB * Correlation (RA, RB) / σ2A + σ2B – 2 * σA * σB * Correlation(RA, RB)

WA = (9.04)2 – 10.38 * 9.04 * 0.59 / (10.38)2 + (9.04)2 – 2 * 10.38 * 9.04 * 0.59

WA = 81.72 – 55.36 / 107.74 + 81.72 – 110.72

WA = 26.36 / 78.74 = 0.335 or 33.5%

Accordingly, the weight assigned to the stock of BCS (Company A) is 33.5% and weight

assigned to the stock of STAN (Company B) is 66.5% (100 – 33.5%) in a minimum variance

portfolio.

Mean returns of Minimum Variance Portfolio

Particulars Mean returns

(a)

Weights

assigned in

MVP

(b)

Mean

returns of

MVP

(a * b)

Company A

(BCS)

0.68% 0.335 0.228%

Company B

(STAN)

-0.33% 0.665 -0.219%

Mean returns of MVP 0.009%

Variance of Minimum Variance Portfolio

σ2p = wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σ2p = Variance of Minimum Variance Portfolio

Standard Deviation 10.38% 9.04%

Coefficient Correlation 0.59

Determination of weight of company A in MVP with the help of following formula:

WA = σ2B – σA * σB * Correlation (RA, RB) / σ2A + σ2B – 2 * σA * σB * Correlation(RA, RB)

WA = (9.04)2 – 10.38 * 9.04 * 0.59 / (10.38)2 + (9.04)2 – 2 * 10.38 * 9.04 * 0.59

WA = 81.72 – 55.36 / 107.74 + 81.72 – 110.72

WA = 26.36 / 78.74 = 0.335 or 33.5%

Accordingly, the weight assigned to the stock of BCS (Company A) is 33.5% and weight

assigned to the stock of STAN (Company B) is 66.5% (100 – 33.5%) in a minimum variance

portfolio.

Mean returns of Minimum Variance Portfolio

Particulars Mean returns

(a)

Weights

assigned in

MVP

(b)

Mean

returns of

MVP

(a * b)

Company A

(BCS)

0.68% 0.335 0.228%

Company B

(STAN)

-0.33% 0.665 -0.219%

Mean returns of MVP 0.009%

Variance of Minimum Variance Portfolio

σ2p = wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σ2p = Variance of Minimum Variance Portfolio

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

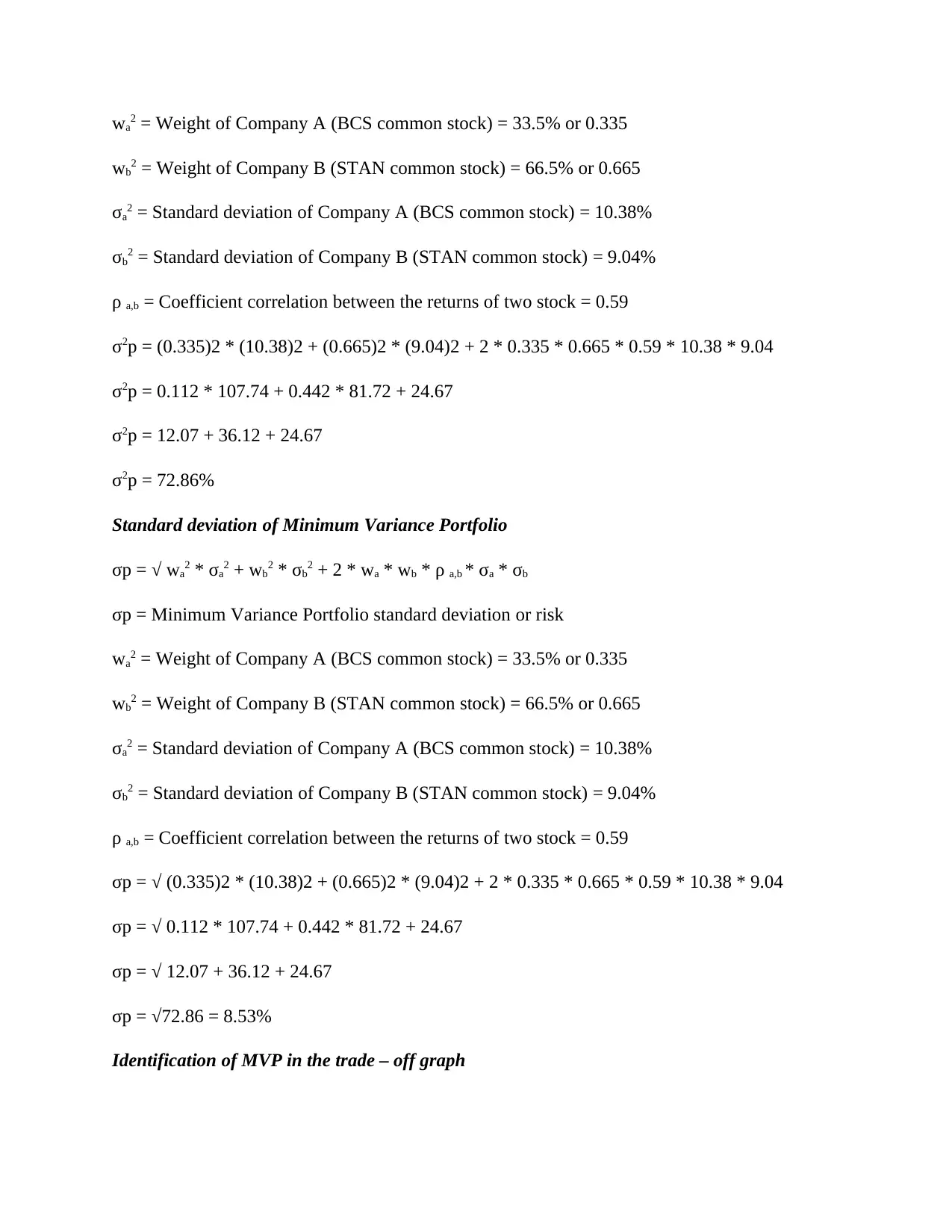

wa2 = Weight of Company A (BCS common stock) = 33.5% or 0.335

wb2 = Weight of Company B (STAN common stock) = 66.5% or 0.665

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σ2p = (0.335)2 * (10.38)2 + (0.665)2 * (9.04)2 + 2 * 0.335 * 0.665 * 0.59 * 10.38 * 9.04

σ2p = 0.112 * 107.74 + 0.442 * 81.72 + 24.67

σ2p = 12.07 + 36.12 + 24.67

σ2p = 72.86%

Standard deviation of Minimum Variance Portfolio

σp = √ wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σp = Minimum Variance Portfolio standard deviation or risk

wa2 = Weight of Company A (BCS common stock) = 33.5% or 0.335

wb2 = Weight of Company B (STAN common stock) = 66.5% or 0.665

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σp = √ (0.335)2 * (10.38)2 + (0.665)2 * (9.04)2 + 2 * 0.335 * 0.665 * 0.59 * 10.38 * 9.04

σp = √ 0.112 * 107.74 + 0.442 * 81.72 + 24.67

σp = √ 12.07 + 36.12 + 24.67

σp = √72.86 = 8.53%

Identification of MVP in the trade – off graph

wb2 = Weight of Company B (STAN common stock) = 66.5% or 0.665

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σ2p = (0.335)2 * (10.38)2 + (0.665)2 * (9.04)2 + 2 * 0.335 * 0.665 * 0.59 * 10.38 * 9.04

σ2p = 0.112 * 107.74 + 0.442 * 81.72 + 24.67

σ2p = 12.07 + 36.12 + 24.67

σ2p = 72.86%

Standard deviation of Minimum Variance Portfolio

σp = √ wa2 * σa2 + wb2 * σb2 + 2 * wa * wb * ρ a,b * σa * σb

σp = Minimum Variance Portfolio standard deviation or risk

wa2 = Weight of Company A (BCS common stock) = 33.5% or 0.335

wb2 = Weight of Company B (STAN common stock) = 66.5% or 0.665

σa2 = Standard deviation of Company A (BCS common stock) = 10.38%

σb2 = Standard deviation of Company B (STAN common stock) = 9.04%

ρ a,b = Coefficient correlation between the returns of two stock = 0.59

σp = √ (0.335)2 * (10.38)2 + (0.665)2 * (9.04)2 + 2 * 0.335 * 0.665 * 0.59 * 10.38 * 9.04

σp = √ 0.112 * 107.74 + 0.442 * 81.72 + 24.67

σp = √ 12.07 + 36.12 + 24.67

σp = √72.86 = 8.53%

Identification of MVP in the trade – off graph

e. Advise to investor on the basis of above findings

On the basis of findings obtained previously in this report, it has been identified that if

only two stocks that is of company A and company B are available to the investor, then it is

better to go for investing in single stock portfolio rather than investing through portfolio

formation by including more than one stock. This is because the highest portfolio returns that an

investor is getting through portfolio formation is 0.68% where the weights assigned to company

A and company B are 100% and 0% respectively. This indicates that investment in company B

along with company A is not fruitful for the investor in terms of generating higher returns at a

lower risk. Also, on calculating the Sharpe ratio for different alternative portfolios, it has been

identified that the best performance of the investment after making adjustment for risk – free

On the basis of findings obtained previously in this report, it has been identified that if

only two stocks that is of company A and company B are available to the investor, then it is

better to go for investing in single stock portfolio rather than investing through portfolio

formation by including more than one stock. This is because the highest portfolio returns that an

investor is getting through portfolio formation is 0.68% where the weights assigned to company

A and company B are 100% and 0% respectively. This indicates that investment in company B

along with company A is not fruitful for the investor in terms of generating higher returns at a

lower risk. Also, on calculating the Sharpe ratio for different alternative portfolios, it has been

identified that the best performance of the investment after making adjustment for risk – free

asset would be realised at a point where 100% allocation is being made to the stock of company

A keeping weight assigned to company B as 0%. This shows profitable and optimal investment

opportunity for an investor.

On including a risk free asset in the portfolio, investor would get comparatively higher

returns at no additional risk. Also, risk – free asset would provide safety to the investor’s wealth

and thus there are lower returns attached with such assets (Pavolova and et.al., 2021).

Accordingly, an investor would be better off in terms of securing higher risk – adjusted returns

as there is no correlation of risk – free asset with that of other risky assets in the portfolio.

PART 2

1. Calculation of investor’s required rate of return on company A’s equity

With the help of CAPM, the required rate of return for an investor can be calculated through

following formula:

E(r) = Rf + Beta * (Market return – Risk- free rate)

Rf = risk – free rate = 1.53%

Beta of Company A (BCS) = Covariance between stock returns and market returns / variance of

market return

Covariance (BCS, FTSE 100) = 0.0068

Variance of FTSE 100 returns = 0.0073

Beta = 0.0068 / 0.0073 = 0.93

Mean Market return = -0.08%

Accordingly,

E(r) = 1.53% + 0.93 * (-0.08% - 1.53%)

E(r) = 1.53% + 0.93 * (-1.61%)

E(r) = 1.53% - 1.50%

E(r) = 0.03%

A keeping weight assigned to company B as 0%. This shows profitable and optimal investment

opportunity for an investor.

On including a risk free asset in the portfolio, investor would get comparatively higher

returns at no additional risk. Also, risk – free asset would provide safety to the investor’s wealth

and thus there are lower returns attached with such assets (Pavolova and et.al., 2021).

Accordingly, an investor would be better off in terms of securing higher risk – adjusted returns

as there is no correlation of risk – free asset with that of other risky assets in the portfolio.

PART 2

1. Calculation of investor’s required rate of return on company A’s equity

With the help of CAPM, the required rate of return for an investor can be calculated through

following formula:

E(r) = Rf + Beta * (Market return – Risk- free rate)

Rf = risk – free rate = 1.53%

Beta of Company A (BCS) = Covariance between stock returns and market returns / variance of

market return

Covariance (BCS, FTSE 100) = 0.0068

Variance of FTSE 100 returns = 0.0073

Beta = 0.0068 / 0.0073 = 0.93

Mean Market return = -0.08%

Accordingly,

E(r) = 1.53% + 0.93 * (-0.08% - 1.53%)

E(r) = 1.53% + 0.93 * (-1.61%)

E(r) = 1.53% - 1.50%

E(r) = 0.03%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Valuation of company A’s equity

In order to determine the equity value of company A, dividend discount model has been

chosen. It is the method of stock evaluation where by predicting future dividends and

discounting them at an investor’s required rate of return, the present value of company’s equity

can be determined (Bulkley and et.al., 2021). The dividend policy of the company is such where

dividends are declared on half yearly basis that is in February & August, while the payment of

this declared dividend is done on annual basis at the end of year. Also, the company has variable

dividend growth model which get changed with the market and company own condition.

Therefore, the expected dividend to be declared by Barclays for the year 2022 is 6p. On the

basis of this dividend, the present equity value of company can be determined as follows:

PV0 = D1 / (1 + r)1

D1 = 6p

r = investor’s required rate of return = 0.03%

PV0 = = 6 / (1 + 0.03%)1

PV0 = 6 / 1.0003 = 5.998 or 6.

Therefore, the equity value of company A based on their expected dividend payment for the

upcoming year is 6.

3. Comparison of calculated equity value with market value (or current stock price) of the

company

The determined equity value of company A on the basis of dividend discount model is $6

while the current market price of company A’s stock is 7.28. Therefore, it can be said that the

stock is little bit overvalued. This indicates that investors are ready to pay more for company’s

stock may be due to their earning potential or better growth prospects in the future (Liu, 2021).

In order to determine the equity value of company A, dividend discount model has been

chosen. It is the method of stock evaluation where by predicting future dividends and

discounting them at an investor’s required rate of return, the present value of company’s equity

can be determined (Bulkley and et.al., 2021). The dividend policy of the company is such where

dividends are declared on half yearly basis that is in February & August, while the payment of

this declared dividend is done on annual basis at the end of year. Also, the company has variable

dividend growth model which get changed with the market and company own condition.

Therefore, the expected dividend to be declared by Barclays for the year 2022 is 6p. On the

basis of this dividend, the present equity value of company can be determined as follows:

PV0 = D1 / (1 + r)1

D1 = 6p

r = investor’s required rate of return = 0.03%

PV0 = = 6 / (1 + 0.03%)1

PV0 = 6 / 1.0003 = 5.998 or 6.

Therefore, the equity value of company A based on their expected dividend payment for the

upcoming year is 6.

3. Comparison of calculated equity value with market value (or current stock price) of the

company

The determined equity value of company A on the basis of dividend discount model is $6

while the current market price of company A’s stock is 7.28. Therefore, it can be said that the

stock is little bit overvalued. This indicates that investors are ready to pay more for company’s

stock may be due to their earning potential or better growth prospects in the future (Liu, 2021).

REFERENCES

Books and Journals

Augar, P., 2018. The bank that lived a little: Barclays in the age of the very free market. Penguin

UK.

Bulkley, K. E., and et.al., 2021. Challenging the One Best System: The portfolio management

model and urban school governance. Harvard Education Press.

Chiang, T. C. and Zhang, Y., 2018. An empirical investigation of risk-return relations in chinese

equity markets: Evidence from aggregate and sectoral data. International Journal of

Financial Studies. 6(2). p.35.

Chiang, T. C., 2019. Economic policy uncertainty, risk and stock returns: Evidence from G7

stock markets. Finance Research Letters. 29(C). pp.41-49.

Jun, B. W. and Yoon, S. M., 2020. Foreign banks acquisition strategy and the business approach

of domestic bank: a case of standard chartered bank. Asian Economic and Financial

Review. 10(7). pp.861-874.

Leković, M., Jakšić, M. M. and Gnjatović, D., 2020. Portfolio performance evaluation of mutual

funds in the Republic of Serbia. Serbian Journal of Management.

Liu, W., 2021. Risk-Aware Financial Portfolio Management with Distributional Deep

Deterministic Policy Gradient (Doctoral dissertation, University of Toronto (Canada)).

Mbai, E., Ngui, T. and Ndiao, O., 2018. Competitive strategies implementation and quality

service delivery in Standard Chartered Bank (K) Ltd. International Academic Journal of

Human Resource and Business Administration. 3(1). pp.246-265.

Nyanaro, N. N. and Bett, S., 2018. Influence of strategic planning on performance of commercial

banks in Kenya: Case of Barclays Bank of Kenya. International Academic Journal of

Human Resource and Business Administration. 3(2). pp.235-255.

Pavolova, H., and et.al., 2021. The analysis of investment into industries based on portfolio

managers. Acta Montanistica Slovaca, 26(1).

Books and Journals

Augar, P., 2018. The bank that lived a little: Barclays in the age of the very free market. Penguin

UK.

Bulkley, K. E., and et.al., 2021. Challenging the One Best System: The portfolio management

model and urban school governance. Harvard Education Press.

Chiang, T. C. and Zhang, Y., 2018. An empirical investigation of risk-return relations in chinese

equity markets: Evidence from aggregate and sectoral data. International Journal of

Financial Studies. 6(2). p.35.

Chiang, T. C., 2019. Economic policy uncertainty, risk and stock returns: Evidence from G7

stock markets. Finance Research Letters. 29(C). pp.41-49.

Jun, B. W. and Yoon, S. M., 2020. Foreign banks acquisition strategy and the business approach

of domestic bank: a case of standard chartered bank. Asian Economic and Financial

Review. 10(7). pp.861-874.

Leković, M., Jakšić, M. M. and Gnjatović, D., 2020. Portfolio performance evaluation of mutual

funds in the Republic of Serbia. Serbian Journal of Management.

Liu, W., 2021. Risk-Aware Financial Portfolio Management with Distributional Deep

Deterministic Policy Gradient (Doctoral dissertation, University of Toronto (Canada)).

Mbai, E., Ngui, T. and Ndiao, O., 2018. Competitive strategies implementation and quality

service delivery in Standard Chartered Bank (K) Ltd. International Academic Journal of

Human Resource and Business Administration. 3(1). pp.246-265.

Nyanaro, N. N. and Bett, S., 2018. Influence of strategic planning on performance of commercial

banks in Kenya: Case of Barclays Bank of Kenya. International Academic Journal of

Human Resource and Business Administration. 3(2). pp.235-255.

Pavolova, H., and et.al., 2021. The analysis of investment into industries based on portfolio

managers. Acta Montanistica Slovaca, 26(1).

Singh, S. and Yadav, S. S., 2021. Diversification of Risk. In Security Analysis and Portfolio

Management (pp. 255-294). Springer, Singapore.

Management (pp. 255-294). Springer, Singapore.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.