Financial Analysis and Performance of Barkes Computers (ACC01)

VerifiedAdded on 2023/06/03

|12

|3137

|293

Case Study

AI Summary

This report analyzes the financial performance of Barkes Computers from 2013 to 2017, utilizing ratio analysis (profitability, liquidity, and leverage) and trend analysis (vertical and horizontal). The analysis reveals declining gross and net profit ratios, while return on equity and assets show improvement. Asset turnover and debt-to-equity ratios also indicate trends. The current ratio shows a deteriorating liquidity position. Trend analysis further highlights changes in sales, COGS, expenses, and net profit, as well as shifts in asset and liability compositions. The report concludes with an evaluation of the company's financial position and offers recommendations based on the findings.

Running head: ACC01

ACC01

Name of the student

Name of the university

Student ID

Author note

ACC01

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACC01

Table of Contents

Introduction................................................................................................................................2

Performance analysis of the company........................................................................................2

Conclusion and recommendation...............................................................................................8

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Performance analysis of the company........................................................................................2

Conclusion and recommendation...............................................................................................8

References................................................................................................................................10

2ACC01

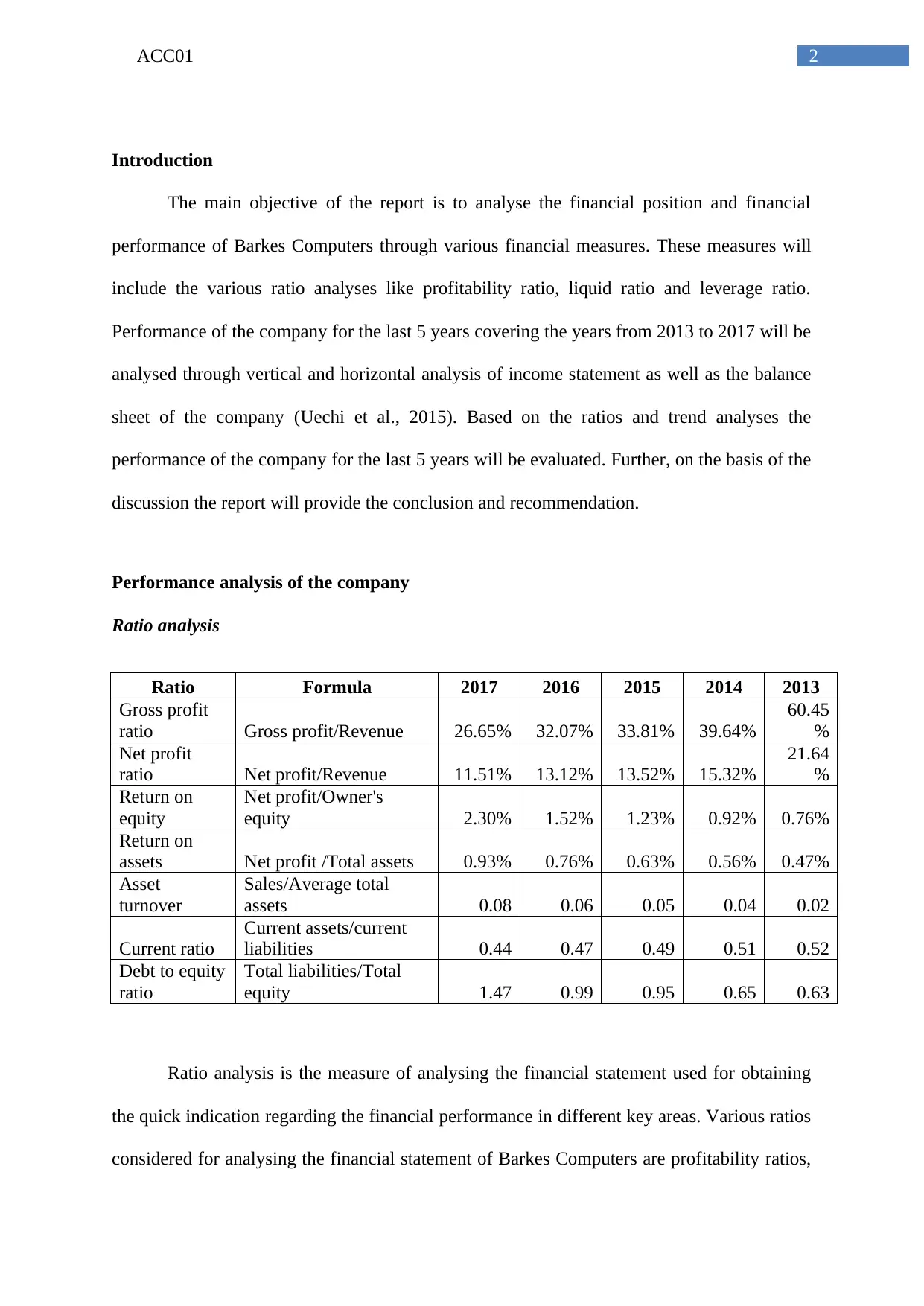

Introduction

The main objective of the report is to analyse the financial position and financial

performance of Barkes Computers through various financial measures. These measures will

include the various ratio analyses like profitability ratio, liquid ratio and leverage ratio.

Performance of the company for the last 5 years covering the years from 2013 to 2017 will be

analysed through vertical and horizontal analysis of income statement as well as the balance

sheet of the company (Uechi et al., 2015). Based on the ratios and trend analyses the

performance of the company for the last 5 years will be evaluated. Further, on the basis of the

discussion the report will provide the conclusion and recommendation.

Performance analysis of the company

Ratio analysis

Ratio Formula 2017 2016 2015 2014 2013

Gross profit

ratio Gross profit/Revenue 26.65% 32.07% 33.81% 39.64%

60.45

%

Net profit

ratio Net profit/Revenue 11.51% 13.12% 13.52% 15.32%

21.64

%

Return on

equity

Net profit/Owner's

equity 2.30% 1.52% 1.23% 0.92% 0.76%

Return on

assets Net profit /Total assets 0.93% 0.76% 0.63% 0.56% 0.47%

Asset

turnover

Sales/Average total

assets 0.08 0.06 0.05 0.04 0.02

Current ratio

Current assets/current

liabilities 0.44 0.47 0.49 0.51 0.52

Debt to equity

ratio

Total liabilities/Total

equity 1.47 0.99 0.95 0.65 0.63

Ratio analysis is the measure of analysing the financial statement used for obtaining

the quick indication regarding the financial performance in different key areas. Various ratios

considered for analysing the financial statement of Barkes Computers are profitability ratios,

Introduction

The main objective of the report is to analyse the financial position and financial

performance of Barkes Computers through various financial measures. These measures will

include the various ratio analyses like profitability ratio, liquid ratio and leverage ratio.

Performance of the company for the last 5 years covering the years from 2013 to 2017 will be

analysed through vertical and horizontal analysis of income statement as well as the balance

sheet of the company (Uechi et al., 2015). Based on the ratios and trend analyses the

performance of the company for the last 5 years will be evaluated. Further, on the basis of the

discussion the report will provide the conclusion and recommendation.

Performance analysis of the company

Ratio analysis

Ratio Formula 2017 2016 2015 2014 2013

Gross profit

ratio Gross profit/Revenue 26.65% 32.07% 33.81% 39.64%

60.45

%

Net profit

ratio Net profit/Revenue 11.51% 13.12% 13.52% 15.32%

21.64

%

Return on

equity

Net profit/Owner's

equity 2.30% 1.52% 1.23% 0.92% 0.76%

Return on

assets Net profit /Total assets 0.93% 0.76% 0.63% 0.56% 0.47%

Asset

turnover

Sales/Average total

assets 0.08 0.06 0.05 0.04 0.02

Current ratio

Current assets/current

liabilities 0.44 0.47 0.49 0.51 0.52

Debt to equity

ratio

Total liabilities/Total

equity 1.47 0.99 0.95 0.65 0.63

Ratio analysis is the measure of analysing the financial statement used for obtaining

the quick indication regarding the financial performance in different key areas. Various ratios

considered for analysing the financial statement of Barkes Computers are profitability ratios,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACC01

liquid ratio and leverage ratio or solvency ratio (Weygandt, Kimmel & Kieso, 2015). As the

data presented in the financial statement of the company are available readily it assists in

comparing the performance of the company with previous years or with the competitors in

the industry. However, the ratio analysis can be used as the 1st step of analysis as it is based

on the accounting information available through the financial statement of the company and

does not justify the true and fairness of the information provided (Wahlen, Baginski &

Bradshaw, 2014).

Gross profit ratio – it establishes a relationship among the net revenue earned by the

company and the amount left with it after spending the amount towards manufacturing and

selling of the goods or providing the services. This is a profitability ratio and expressed in the

percentage form. The net sales considered here is the total of cash sales as well as credit

sales. It assists in ascertaining the optimum sales price and enhances the efficiencies of the

trading activities. High gross profit ratio indicates that the net sales of the company are high

with consistent cost of the sales. On the other hand, low sales with increasing COGS results

into falling trend of the gross profit (Easton & Sommers, 2018). It can be identified from the

ratio calculation table that the gross profit of the company is in falling trend and it is reduced

from 60.45% to 26.65% over the years from 2013 to 2017.

Net profit ratio – It is the sales percentage left with the company after paying off all the

operating expenses and financial and tax expenses. Net profit does not indicate the cash flows

as the net profits incorporate various non-cash expenses like depreciation and amortization.

However, the major issue associated with net profit margin is it is considered for short term

performance measure as does not reveal any measure for maintaining the profitability over

the long run. It establishes a relationship among the net revenue earned by the company and

the amount left with it after paying taxes, operational and financial expenses. It can be

identified from the ratio calculation table that the net profit of the company is in falling trend

liquid ratio and leverage ratio or solvency ratio (Weygandt, Kimmel & Kieso, 2015). As the

data presented in the financial statement of the company are available readily it assists in

comparing the performance of the company with previous years or with the competitors in

the industry. However, the ratio analysis can be used as the 1st step of analysis as it is based

on the accounting information available through the financial statement of the company and

does not justify the true and fairness of the information provided (Wahlen, Baginski &

Bradshaw, 2014).

Gross profit ratio – it establishes a relationship among the net revenue earned by the

company and the amount left with it after spending the amount towards manufacturing and

selling of the goods or providing the services. This is a profitability ratio and expressed in the

percentage form. The net sales considered here is the total of cash sales as well as credit

sales. It assists in ascertaining the optimum sales price and enhances the efficiencies of the

trading activities. High gross profit ratio indicates that the net sales of the company are high

with consistent cost of the sales. On the other hand, low sales with increasing COGS results

into falling trend of the gross profit (Easton & Sommers, 2018). It can be identified from the

ratio calculation table that the gross profit of the company is in falling trend and it is reduced

from 60.45% to 26.65% over the years from 2013 to 2017.

Net profit ratio – It is the sales percentage left with the company after paying off all the

operating expenses and financial and tax expenses. Net profit does not indicate the cash flows

as the net profits incorporate various non-cash expenses like depreciation and amortization.

However, the major issue associated with net profit margin is it is considered for short term

performance measure as does not reveal any measure for maintaining the profitability over

the long run. It establishes a relationship among the net revenue earned by the company and

the amount left with it after paying taxes, operational and financial expenses. It can be

identified from the ratio calculation table that the net profit of the company is in falling trend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACC01

and it is reduced from 21.64% to 11.51% over the years from 2013 to 2017 (Cakici,

Chatterjee & Tang, 2017).

Return on equity – return on equity measures the return rate that will be received by the

stock holders on their investment. ROE further indicates the efficiency of the company

regarding generating the returns on investment received from the shareholders. It is computed

through dividing the net profit of the company by total equities of the company . Hence, if the

ROE of the company is 1 it indicates that the shareholders investment earn earning of $ 1.

From the investor’s perspective this ratio is very important as this ratio is used it is used for

judging the efficiency of the company with regard to the generation of additional income

from the investment (Kriplani, Shrishrimal & Bhide, 2017). It can be identified from the ratio

calculation table that the return on equity of the company is in rising trend and it is increased

from 0.76% to 2.30% over the years from 2013 to 2017.

Return on assets – ROA is a profitability measure used for measuring the business

profitability as compared to its assets. It indicates the efficiencies with regard to the

generation of capital invested in the assets. higher return indicates that the company is more

efficient and productive with regard to utilization of the economic resources. Conversely,

falling trend of ROA indicates that there is some issues with regard to generation of earning

from the assets of the company. However, as ROA does not consider the liabilities of the

company the return computed may not actually reveal the position of the entity. It can be

identified from the ratio calculation table that the return on asset of the company is in rising

trend and it is increased from 0.47% to 0.93% over the years from 2013 to 2017.

Asset turnover – it is an efficiency ratio used to measure the efficiency of the company for

generating sales from the assets. It compares the value of sales generated by the company as

compared to its average assets. It is used as an indication for efficiency regarding deployment

and it is reduced from 21.64% to 11.51% over the years from 2013 to 2017 (Cakici,

Chatterjee & Tang, 2017).

Return on equity – return on equity measures the return rate that will be received by the

stock holders on their investment. ROE further indicates the efficiency of the company

regarding generating the returns on investment received from the shareholders. It is computed

through dividing the net profit of the company by total equities of the company . Hence, if the

ROE of the company is 1 it indicates that the shareholders investment earn earning of $ 1.

From the investor’s perspective this ratio is very important as this ratio is used it is used for

judging the efficiency of the company with regard to the generation of additional income

from the investment (Kriplani, Shrishrimal & Bhide, 2017). It can be identified from the ratio

calculation table that the return on equity of the company is in rising trend and it is increased

from 0.76% to 2.30% over the years from 2013 to 2017.

Return on assets – ROA is a profitability measure used for measuring the business

profitability as compared to its assets. It indicates the efficiencies with regard to the

generation of capital invested in the assets. higher return indicates that the company is more

efficient and productive with regard to utilization of the economic resources. Conversely,

falling trend of ROA indicates that there is some issues with regard to generation of earning

from the assets of the company. However, as ROA does not consider the liabilities of the

company the return computed may not actually reveal the position of the entity. It can be

identified from the ratio calculation table that the return on asset of the company is in rising

trend and it is increased from 0.47% to 0.93% over the years from 2013 to 2017.

Asset turnover – it is an efficiency ratio used to measure the efficiency of the company for

generating sales from the assets. It compares the value of sales generated by the company as

compared to its average assets. It is used as an indication for efficiency regarding deployment

5ACC01

of its assets for income generation. It is computed on annual basis and higher ratio indicates

that the company is performing well. However. the ROA is considered as useful when the

comparison is made for various entities in the same industry or with the company’s past

performance. It can be identified from the ratio calculation table that the asset turnover of the

company is in rising trend and it is increased from 0.02 to 0.08 over the years from 2013 to

2017.

Current ratio – it is used for measuring the efficiency as well as the liquidity with regard to

payment of the short term liabilities with the available current assets of the company. This

ratio is considered as an important measure for measuring the liquidity position as the short

term obligations becomes payable within one year time period. the entity has limited time for

arranging payment for meeting its short term obligations. Current assets such as inventories,

cash, receivable and marketable securities can be converted into cash quickly. Hence, the

companies with large amount of current assets as compared to its current obligations are

strong in terms of liquidity. It can be identified from the ratio calculation table that the

current ratio of the company is in falling trend and it is reduced from 0.52 to 0.02 over the

years from 2013 to 2017. Hence, the liquidity position of the company has been deteriorated.

Further, for all over the last 5 years the company never had current ratio of more than 1 that

indicates that the company never had sufficient current assets to meet its short-term

obligations (Sari, Nurlaela & Titisari, 2018).

Debt to equity ratio – it is a leverage ratio used to measure the total debt of the company as

compared to its equities. It reveals the proportion of funds raised through borrowing and

raised from the investors. Ratio of 1 indicates that the company has equal proportion of debt

and equities. If the debt to equity ratio of the company is high it indicates that the company is

highly leveraged and major portion of the fund is raised through borrowing. Higher debt to

equity ratio is considered as risky from the creditor’s perspective as significant amount of the

of its assets for income generation. It is computed on annual basis and higher ratio indicates

that the company is performing well. However. the ROA is considered as useful when the

comparison is made for various entities in the same industry or with the company’s past

performance. It can be identified from the ratio calculation table that the asset turnover of the

company is in rising trend and it is increased from 0.02 to 0.08 over the years from 2013 to

2017.

Current ratio – it is used for measuring the efficiency as well as the liquidity with regard to

payment of the short term liabilities with the available current assets of the company. This

ratio is considered as an important measure for measuring the liquidity position as the short

term obligations becomes payable within one year time period. the entity has limited time for

arranging payment for meeting its short term obligations. Current assets such as inventories,

cash, receivable and marketable securities can be converted into cash quickly. Hence, the

companies with large amount of current assets as compared to its current obligations are

strong in terms of liquidity. It can be identified from the ratio calculation table that the

current ratio of the company is in falling trend and it is reduced from 0.52 to 0.02 over the

years from 2013 to 2017. Hence, the liquidity position of the company has been deteriorated.

Further, for all over the last 5 years the company never had current ratio of more than 1 that

indicates that the company never had sufficient current assets to meet its short-term

obligations (Sari, Nurlaela & Titisari, 2018).

Debt to equity ratio – it is a leverage ratio used to measure the total debt of the company as

compared to its equities. It reveals the proportion of funds raised through borrowing and

raised from the investors. Ratio of 1 indicates that the company has equal proportion of debt

and equities. If the debt to equity ratio of the company is high it indicates that the company is

highly leveraged and major portion of the fund is raised through borrowing. Higher debt to

equity ratio is considered as risky from the creditor’s perspective as significant amount of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACC01

company will be spend for paying the interest expenses on borrowing. It can be identified

from the ratio calculation table that the debt to equity ratio of the company is in rising trend

and it significantly increased from 0.63 to 1.47 over the years from 2013 to 2017. It is

signifying that the funding of the company through borrowing over the last 5 years has been

increased which in turn will expose the company towards interest risk and solvency risk

(Barth & Miller, 2018).

Trend analysis

This is a method of analysing the performance of the company for predicting the

future based on the past performance and trends. It takes into account the past years data

movement and based on that the performance of the company is analysed (Saeed, Majid,

Zahra & Akram, 2018).

Vertical analysis

2017 2016 2015 2014 2013

Sales

350.00

%

255.97

%

209.70

%

165.67

% 100%

COGS

649.06

%

439.62

%

350.94

%

252.83

% 100%

Gross Profit

154.32

%

135.80

%

117.28

%

108.64

% 100%

Expenses

120.00

%

115.00

%

102.50

%

100.00

% 100%

EBIT

187.80

%

156.10

%

131.71

%

117.07

% 100%

Tax

191.67

%

158.33

%

133.33

%

116.67

% 100%

Net Profit

186.21

%

155.17

%

131.03

%

117.24

% 100%

2017 2016 2015 2014 2013

Current Assets 90.91% 93.18% 95.45% 97.73% 100%

company will be spend for paying the interest expenses on borrowing. It can be identified

from the ratio calculation table that the debt to equity ratio of the company is in rising trend

and it significantly increased from 0.63 to 1.47 over the years from 2013 to 2017. It is

signifying that the funding of the company through borrowing over the last 5 years has been

increased which in turn will expose the company towards interest risk and solvency risk

(Barth & Miller, 2018).

Trend analysis

This is a method of analysing the performance of the company for predicting the

future based on the past performance and trends. It takes into account the past years data

movement and based on that the performance of the company is analysed (Saeed, Majid,

Zahra & Akram, 2018).

Vertical analysis

2017 2016 2015 2014 2013

Sales

350.00

%

255.97

%

209.70

%

165.67

% 100%

COGS

649.06

%

439.62

%

350.94

%

252.83

% 100%

Gross Profit

154.32

%

135.80

%

117.28

%

108.64

% 100%

Expenses

120.00

%

115.00

%

102.50

%

100.00

% 100%

EBIT

187.80

%

156.10

%

131.71

%

117.07

% 100%

Tax

191.67

%

158.33

%

133.33

%

116.67

% 100%

Net Profit

186.21

%

155.17

%

131.03

%

117.24

% 100%

2017 2016 2015 2014 2013

Current Assets 90.91% 93.18% 95.45% 97.73% 100%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACC01

Non-current Assets 93.33% 95.00% 96.67% 98.33% 100%

Total Assets 93.25% 94.94% 96.62% 98.31% 100%

Current Liabilities

107.14

%

104.76

%

102.38

%

100.00

% 100%

Non-current Liabilities

150.00

%

125.00

%

125.00

%

100.00

% 100%

Total Liabilities

143.15

%

121.99

%

121.58

%

100.41

% 100%

Owners Equity 61.68% 77.82% 80.84% 96.98% 100%

From the vertical analysis of the income statement it can be identified that the sales as

well as COGS of the company both are in rising trend. Hence, the gross profit of the

company has been increased to 154.32%. The operating expenses of the company has been

increased to 120%. Further, the net profit of the company has been increased to 186.21%. All

these trends have been analysed taking into consideration 2013 as base year (Greenbaum,

Thakor & Boot, 2015).

If the balance sheet is analysed it can be found that total assets of the company along

with current assets as well as non-current assets are in falling trend. however, the liabilities of

the company including current liabilities and non-current liabilities are in rising trend. it

states that the liquidity position as well as the solvency position of the company has been

deteriorated over the last 5 years. Further, the owner’s equity of the company has been

reduced to 61.68% in 2017 if 2013 is considered as the base year (Al Nimer, Warrad & Al

Omari, 2015).

Horizontal analysis

2017 2016 2015 2014 2013

Sales

100.00

%

100.00

%

100.00

%

100.00

%

100.00

%

COGS 73.35% 67.93% 66.19% 60.36% 39.55%

Gross Profit 26.65% 32.07% 33.81% 39.64% 60.45%

Expenses 10.23% 13.41% 14.59% 18.02% 29.85%

Non-current Assets 93.33% 95.00% 96.67% 98.33% 100%

Total Assets 93.25% 94.94% 96.62% 98.31% 100%

Current Liabilities

107.14

%

104.76

%

102.38

%

100.00

% 100%

Non-current Liabilities

150.00

%

125.00

%

125.00

%

100.00

% 100%

Total Liabilities

143.15

%

121.99

%

121.58

%

100.41

% 100%

Owners Equity 61.68% 77.82% 80.84% 96.98% 100%

From the vertical analysis of the income statement it can be identified that the sales as

well as COGS of the company both are in rising trend. Hence, the gross profit of the

company has been increased to 154.32%. The operating expenses of the company has been

increased to 120%. Further, the net profit of the company has been increased to 186.21%. All

these trends have been analysed taking into consideration 2013 as base year (Greenbaum,

Thakor & Boot, 2015).

If the balance sheet is analysed it can be found that total assets of the company along

with current assets as well as non-current assets are in falling trend. however, the liabilities of

the company including current liabilities and non-current liabilities are in rising trend. it

states that the liquidity position as well as the solvency position of the company has been

deteriorated over the last 5 years. Further, the owner’s equity of the company has been

reduced to 61.68% in 2017 if 2013 is considered as the base year (Al Nimer, Warrad & Al

Omari, 2015).

Horizontal analysis

2017 2016 2015 2014 2013

Sales

100.00

%

100.00

%

100.00

%

100.00

%

100.00

%

COGS 73.35% 67.93% 66.19% 60.36% 39.55%

Gross Profit 26.65% 32.07% 33.81% 39.64% 60.45%

Expenses 10.23% 13.41% 14.59% 18.02% 29.85%

8ACC01

EBIT 16.42% 18.66% 19.22% 21.62% 30.60%

Tax 4.90% 5.54% 5.69% 6.31% 8.96%

Net Profit 11.51% 13.12% 13.52% 15.32% 21.64%

2017 2016 2015 2014 2013

Current Assets 3.45% 3.47% 3.49% 3.52% 3.54%

Non-current Assets 96.55%

96.53

% 96.51% 96.48% 96.46%

Total Assets

100.00

% 100%

100.00

% 100.00%

100.00

%

Current Liabilities 7.76% 7.45% 7.15% 6.87% 6.75%

Non-current Liabilities 51.72%

42.34

% 41.60% 32.71% 32.15%

Total Liabilities 59.48%

49.79

% 48.75% 39.57% 38.75%

Owners Equity 40.52%

50.21

% 51.25% 60.43% 61.25%

From the horizontal analysis of the company’s income statement it can be identified

that the gross profit percentage of the company over the last 5 years fell in from 60.45% to

26.65%. The EBIT of the company further reduced from 30.60% to 16.42%. finally it is

identified that the net profit of the company was also in reducing trend and reached to

11.51% in 2017 from 21.64% in 2013 (Chalermchatvichien et al., 2014).

If the balance is considered it can be identified that the liability portion of the

company as compared to asset over the last 5 years has been increased from 38.75% to

59.48%. Conversely, the equity portion of the company as compared to asset over the last 5

years has been reduced from 61.25% to 40.52%. It is signifying that the funding of the

company through borrowing over the last 5 years has been increased which in turn will

expose the company towards interest risk and solvency risk (Gitman, Juchau & Flanagan,

2015).

EBIT 16.42% 18.66% 19.22% 21.62% 30.60%

Tax 4.90% 5.54% 5.69% 6.31% 8.96%

Net Profit 11.51% 13.12% 13.52% 15.32% 21.64%

2017 2016 2015 2014 2013

Current Assets 3.45% 3.47% 3.49% 3.52% 3.54%

Non-current Assets 96.55%

96.53

% 96.51% 96.48% 96.46%

Total Assets

100.00

% 100%

100.00

% 100.00%

100.00

%

Current Liabilities 7.76% 7.45% 7.15% 6.87% 6.75%

Non-current Liabilities 51.72%

42.34

% 41.60% 32.71% 32.15%

Total Liabilities 59.48%

49.79

% 48.75% 39.57% 38.75%

Owners Equity 40.52%

50.21

% 51.25% 60.43% 61.25%

From the horizontal analysis of the company’s income statement it can be identified

that the gross profit percentage of the company over the last 5 years fell in from 60.45% to

26.65%. The EBIT of the company further reduced from 30.60% to 16.42%. finally it is

identified that the net profit of the company was also in reducing trend and reached to

11.51% in 2017 from 21.64% in 2013 (Chalermchatvichien et al., 2014).

If the balance is considered it can be identified that the liability portion of the

company as compared to asset over the last 5 years has been increased from 38.75% to

59.48%. Conversely, the equity portion of the company as compared to asset over the last 5

years has been reduced from 61.25% to 40.52%. It is signifying that the funding of the

company through borrowing over the last 5 years has been increased which in turn will

expose the company towards interest risk and solvency risk (Gitman, Juchau & Flanagan,

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACC01

Conclusion and recommendation

From the above calculation and interpretation it can be concluded that the profitability

position of the company with regard to the gross profit and net profit has been deteriorated

over the last 5 years. however, the company has improved its position with regard to

generation of profit from the assets as well as deploying its assets. Further, if the liquidity

position of the company for the last 5 years in considered it can be stated that the company

never had current ratio of more than 1. It indicates that the company never had sufficient

current assets to meet its short-term obligations. Further, the debt equity ratio trend is

indicating the the leverage position of the company over the last 5 years has been

deteriorated.

Therefore, it is recommended that to improve the profitability position the company

shall take necessary steps for reducing its COGS as well as other expenses, wherever possible

to improve the gross profit as well as net profit position. Further, the liquidity position of the

company can be improved through paying off the current obligations. Moreover, it is

recommended that for further requirement of fund the company shall raise the fund through

equities instead of borrowings.

Conclusion and recommendation

From the above calculation and interpretation it can be concluded that the profitability

position of the company with regard to the gross profit and net profit has been deteriorated

over the last 5 years. however, the company has improved its position with regard to

generation of profit from the assets as well as deploying its assets. Further, if the liquidity

position of the company for the last 5 years in considered it can be stated that the company

never had current ratio of more than 1. It indicates that the company never had sufficient

current assets to meet its short-term obligations. Further, the debt equity ratio trend is

indicating the the leverage position of the company over the last 5 years has been

deteriorated.

Therefore, it is recommended that to improve the profitability position the company

shall take necessary steps for reducing its COGS as well as other expenses, wherever possible

to improve the gross profit as well as net profit position. Further, the liquidity position of the

company can be improved through paying off the current obligations. Moreover, it is

recommended that for further requirement of fund the company shall raise the fund through

equities instead of borrowings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACC01

References

Al Nimer, M., Warrad, L., & Al Omari, R. (2015). The impact of liquidity on Jordanian

banks profitability through return on assets. European Journal of Business and

Management, 7(7), 229-232.

Barth, J. R., & Miller, S. M. (2018). Benefits and costs of a higher bank “leverage

ratio”. Journal of Financial Stability, 38, 37-52.

Cakici, N., Chatterjee, S., & Tang, Y. (2017). Alternative Profitability Measures and Cross

Section of Expected Stock Returns: International Evidence.

Chalermchatvichien, P., Jumreornvong, S., Jiraporn, P., & Singh, M. (2014). The effect of

bank ownership concentration on capital adequacy, liquidity, and capital

stability. Journal of Financial Services Research, 45(2), 219-240.

Easton, M., & Sommers, Z. (2018). Financial Statement Analysis & Valuation, 5e.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Greenbaum, S. I., Thakor, A. V., & Boot, A. (Eds.). (2015). Contemporary financial

intermediation. Academic Press.

Kriplani, P., Shrishrimal, P., & Bhide, S. (2017, July). Granulation of financial time series for

trend analysis and recognition. In Fuzzy Systems (FUZZ-IEEE), 2017 IEEE

International Conference on (pp. 1-6). IEEE.

Saeed, S., Majid, S., Zahra, I., & Akram, S. (2018). Impact of Leverage on Profitability (A

case of Pakistani Textile Companies). Pakistan Research Journal of Management

Sciences, 1(1).

References

Al Nimer, M., Warrad, L., & Al Omari, R. (2015). The impact of liquidity on Jordanian

banks profitability through return on assets. European Journal of Business and

Management, 7(7), 229-232.

Barth, J. R., & Miller, S. M. (2018). Benefits and costs of a higher bank “leverage

ratio”. Journal of Financial Stability, 38, 37-52.

Cakici, N., Chatterjee, S., & Tang, Y. (2017). Alternative Profitability Measures and Cross

Section of Expected Stock Returns: International Evidence.

Chalermchatvichien, P., Jumreornvong, S., Jiraporn, P., & Singh, M. (2014). The effect of

bank ownership concentration on capital adequacy, liquidity, and capital

stability. Journal of Financial Services Research, 45(2), 219-240.

Easton, M., & Sommers, Z. (2018). Financial Statement Analysis & Valuation, 5e.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Greenbaum, S. I., Thakor, A. V., & Boot, A. (Eds.). (2015). Contemporary financial

intermediation. Academic Press.

Kriplani, P., Shrishrimal, P., & Bhide, S. (2017, July). Granulation of financial time series for

trend analysis and recognition. In Fuzzy Systems (FUZZ-IEEE), 2017 IEEE

International Conference on (pp. 1-6). IEEE.

Saeed, S., Majid, S., Zahra, I., & Akram, S. (2018). Impact of Leverage on Profitability (A

case of Pakistani Textile Companies). Pakistan Research Journal of Management

Sciences, 1(1).

11ACC01

Sari, R. K., Nurlaela, S., & Titisari, K. H. (2018, August). The Effect of Liquidity Ratio,

Profitability Ratio, Company Size, and Leverage on Bond Rating in Construction and

Real Estate Company. In PROCEEDING ICTESS (Internasional Conference on

Technology, Education and Social Sciences).

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J., & Kenett, D. Y. (2015). Sector

dominance ratio analysis of financial markets. Physica A: Statistical Mechanics and

its Applications, 421, 488-509.

Wahlen, J., Baginski, S., & Bradshaw, M. (2014). Financial reporting, financial statement

analysis and valuation. Nelson Education.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

Sari, R. K., Nurlaela, S., & Titisari, K. H. (2018, August). The Effect of Liquidity Ratio,

Profitability Ratio, Company Size, and Leverage on Bond Rating in Construction and

Real Estate Company. In PROCEEDING ICTESS (Internasional Conference on

Technology, Education and Social Sciences).

Uechi, L., Akutsu, T., Stanley, H. E., Marcus, A. J., & Kenett, D. Y. (2015). Sector

dominance ratio analysis of financial markets. Physica A: Statistical Mechanics and

its Applications, 421, 488-509.

Wahlen, J., Baginski, S., & Bradshaw, M. (2014). Financial reporting, financial statement

analysis and valuation. Nelson Education.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.