Analyzing BEGA Cheese Limited: Financial Performance through Ratios

VerifiedAdded on 2023/06/04

|10

|2181

|235

Report

AI Summary

This report provides a comprehensive financial analysis of BEGA Cheese Limited, examining its performance from 2021 to 2022 using various financial ratios. It calculates and interprets key metrics, including current ratio, quick ratio, receivables turnover, return on equity (ROE), return on assets (...

BEGA Cheese Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................1

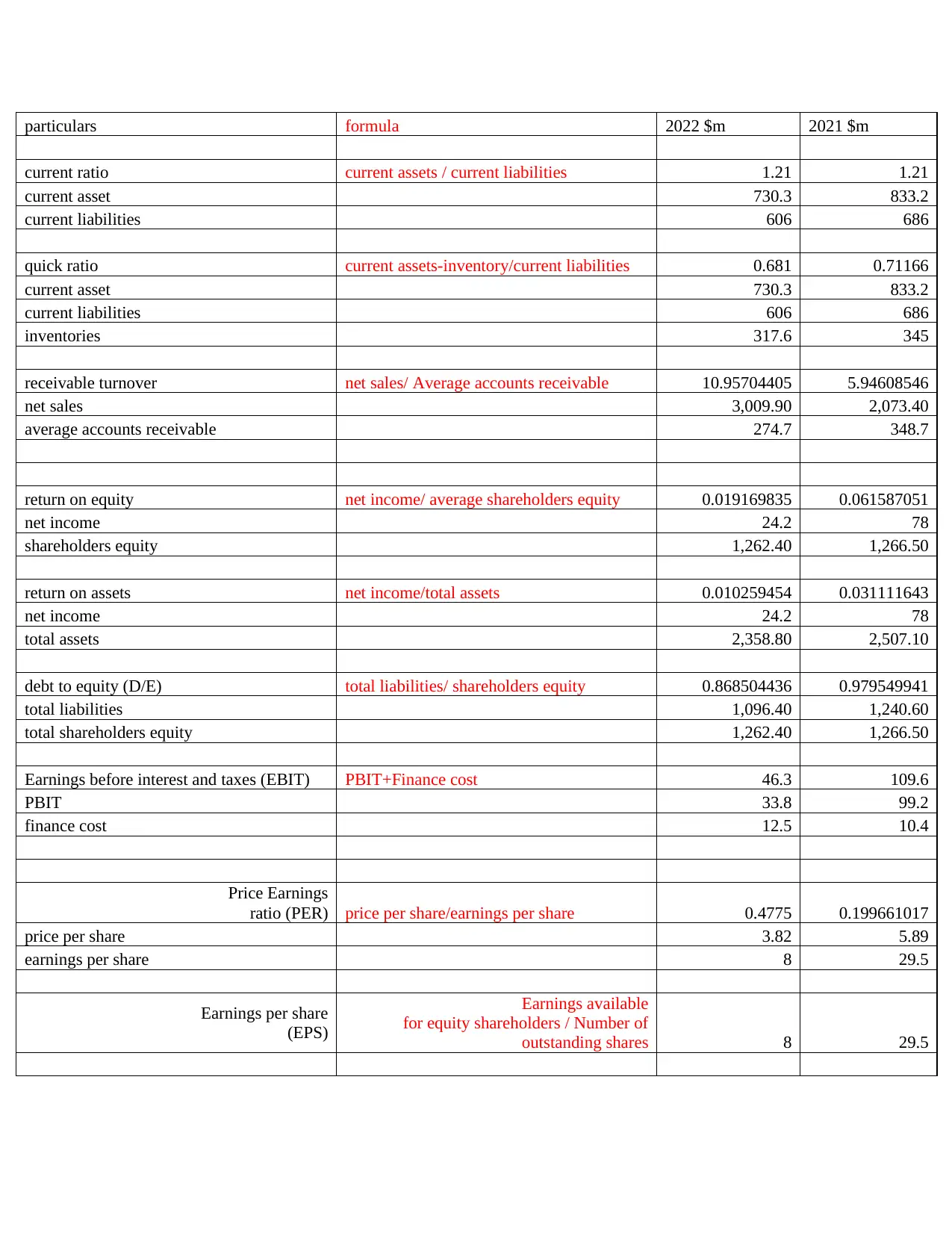

particulars formula 2022 $m 2021 $m

current ratio current assets / current liabilities 1.21 1.21

current asset 730.3 833.2

current liabilities 606 686

quick ratio current assets-inventory/current liabilities 0.681 0.71166

current asset 730.3 833.2

current liabilities 606 686

inventories 317.6 345

receivable turnover net sales/ Average accounts receivable 10.95704405 5.94608546

net sales 3,009.90 2,073.40

average accounts receivable 274.7 348.7

return on equity net income/ average shareholders equity 0.019169835 0.061587051

net income 24.2 78

shareholders equity 1,262.40 1,266.50

return on assets net income/total assets 0.010259454 0.031111643

net income 24.2 78

total assets 2,358.80 2,507.10

debt to equity (D/E) total liabilities/ shareholders equity 0.868504436 0.979549941

total liabilities 1,096.40 1,240.60

total shareholders equity 1,262.40 1,266.50

Earnings before interest and taxes (EBIT) PBIT+Finance cost 46.3 109.6

PBIT 33.8 99.2

finance cost 12.5 10.4

Price Earnings

ratio (PER) price per share/earnings per share 0.4775 0.199661017

price per share 3.82 5.89

earnings per share 8 29.5

Earnings per share

(EPS)

Earnings available

for equity shareholders / Number of

outstanding shares 8 29.5

current ratio current assets / current liabilities 1.21 1.21

current asset 730.3 833.2

current liabilities 606 686

quick ratio current assets-inventory/current liabilities 0.681 0.71166

current asset 730.3 833.2

current liabilities 606 686

inventories 317.6 345

receivable turnover net sales/ Average accounts receivable 10.95704405 5.94608546

net sales 3,009.90 2,073.40

average accounts receivable 274.7 348.7

return on equity net income/ average shareholders equity 0.019169835 0.061587051

net income 24.2 78

shareholders equity 1,262.40 1,266.50

return on assets net income/total assets 0.010259454 0.031111643

net income 24.2 78

total assets 2,358.80 2,507.10

debt to equity (D/E) total liabilities/ shareholders equity 0.868504436 0.979549941

total liabilities 1,096.40 1,240.60

total shareholders equity 1,262.40 1,266.50

Earnings before interest and taxes (EBIT) PBIT+Finance cost 46.3 109.6

PBIT 33.8 99.2

finance cost 12.5 10.4

Price Earnings

ratio (PER) price per share/earnings per share 0.4775 0.199661017

price per share 3.82 5.89

earnings per share 8 29.5

Earnings per share

(EPS)

Earnings available

for equity shareholders / Number of

outstanding shares 8 29.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

current ratio

By calculating current ratio, company can easily know about its ability to pay short term

obligations or those amount which is due in one year. Basically, this ratio is used by creditors in

order to know whether a firm can be offered short term debts or not (Nuryani and Sunarsi, 2020).

By using this ratio, company can easily provide information about its operating cycle. from the

above calculation, it has been evaluated that current ratio of BEGA cheese limited in the year

2022 is 1.21 and in the year 2021 it is 1.21, which indicates that the firm is able to meet its short

term obligations. From this calculation it can be said that company can maximize the current

assets on its balance sheet in order to satisfy payables as well as current debt. It is interpreted that

the company is in good position and healthy in terms of paying debts. The company has good

management of its working capital. From this it can also be said that company is properly

utilizing its assets and focusing on financial well-being in a correct manner. Hence, company is

able to convert its assets into cash for paying short term debts. From maintaining and improving

current ratio in the future, the company needs to reduce any unnecessary expenses, personal draw

on the business. In addition, it is recommended to sell off all the assets which is not generating a

return to the business and which are of no use.

Acid-test (quick) ratio

The obligation of the payment of the short term debt through the most liquid assets by the

company is termed as quick ratio. Compare to the other liquid ratios the more values were hold

by the quick ratio. The quick ratio of the Cheese Limited company in 2022 is 0.68 and in 2021 it

is 0.71 which indicates that the business has more liquidity and fewer liquid assets (Wijaya and

Sedana, 2020). Due to the decrease in the sales, poor account receivable the quick ratio of the

company decreased from previous year. The idle quick ratio is 1:1. Thus, the business should

increase its inventory turnover and the sales in the future to improve the ratio. Increasing in the

marketing and providing the incentive to the sales staff leads in increase in the sales which will

help in increasing the inventory turnover.

Receivables turnover ratio: This ratio measures the company’s efficiency in terms of

collecting its dues from the debtors and accordingly measure the number of times the receivables

have been converted to cash during the given period (Dance and Imade, 2019). In the given case,

the ratio has increased from 5.94 to 10.96 between 2021 & 2022 indicating that the efficiency of

By calculating current ratio, company can easily know about its ability to pay short term

obligations or those amount which is due in one year. Basically, this ratio is used by creditors in

order to know whether a firm can be offered short term debts or not (Nuryani and Sunarsi, 2020).

By using this ratio, company can easily provide information about its operating cycle. from the

above calculation, it has been evaluated that current ratio of BEGA cheese limited in the year

2022 is 1.21 and in the year 2021 it is 1.21, which indicates that the firm is able to meet its short

term obligations. From this calculation it can be said that company can maximize the current

assets on its balance sheet in order to satisfy payables as well as current debt. It is interpreted that

the company is in good position and healthy in terms of paying debts. The company has good

management of its working capital. From this it can also be said that company is properly

utilizing its assets and focusing on financial well-being in a correct manner. Hence, company is

able to convert its assets into cash for paying short term debts. From maintaining and improving

current ratio in the future, the company needs to reduce any unnecessary expenses, personal draw

on the business. In addition, it is recommended to sell off all the assets which is not generating a

return to the business and which are of no use.

Acid-test (quick) ratio

The obligation of the payment of the short term debt through the most liquid assets by the

company is termed as quick ratio. Compare to the other liquid ratios the more values were hold

by the quick ratio. The quick ratio of the Cheese Limited company in 2022 is 0.68 and in 2021 it

is 0.71 which indicates that the business has more liquidity and fewer liquid assets (Wijaya and

Sedana, 2020). Due to the decrease in the sales, poor account receivable the quick ratio of the

company decreased from previous year. The idle quick ratio is 1:1. Thus, the business should

increase its inventory turnover and the sales in the future to improve the ratio. Increasing in the

marketing and providing the incentive to the sales staff leads in increase in the sales which will

help in increasing the inventory turnover.

Receivables turnover ratio: This ratio measures the company’s efficiency in terms of

collecting its dues from the debtors and accordingly measure the number of times the receivables

have been converted to cash during the given period (Dance and Imade, 2019). In the given case,

the ratio has increased from 5.94 to 10.96 between 2021 & 2022 indicating that the efficiency of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company has increased in terms of collecting outstanding amount from its accounts

receivables because of having quality customers who usually make payment quickly.

Return on Equity (ROE)

Return of equity ratio reflects the ability of an organization to maintain and organize the capital

of the shareholders. Higher roe ratio states that a firm is highly capable to manage funds. From

the above table it can be stated that the ability of the organization to maintain the capital has

decreased from the past year (Al‐Hadi & et.al., 2019). For improvement the return on equity of

Dega cheese Ltd. it has been recommended to increase the profit margins on the products and

services of the firm. This can give. Firm can work on increasing the efficiency of the supply

chain to reduce the variable cost that can reduce the total cost of the product. Reduction in the

procurement of raw material can help the firm to increase the profits. Moreover, the organization

can focus on improvement of asset turnover to gain higher capability. Idle cash hold by the

company can be distributed to the shareholders to get a leverage. It can boost the return on equity

as the variable of shareholders equity increases with the distribution. The distribution of the cash

also influences the investors towards the company as they see lucrative returns.

Return on Assets (ROA)

The profitability of the company in relation with the assets possessed by them is depicted by the

return of assets ratio. This ratio helps the management to determine the efficiency of the

organization to earn profits through proper allocation of resources (Wu & et.al., 2020). Higher

ROA reflects the higher efficiency of the business to organize assets. The table has shown a

decline in the ability of firm to organize assets as the return on asset ratio has decreased from the

previous year. For improving this ratio the organization can focus on increasing the efficiency of

current and fixed assets. Current assets include cash, bills receivable etc. whose allocation and

usage can be done properly so that the firm can achieve higher profits from it. Receivable are of

high importance to the organization which can be managed thoroughly. Working on the credit

policy and collection process of receivable can help in doing so. For improving the return on

assets, entity can opt for leasing the assets instead of purchasing it. It will eliminate the cost

incurred on the wear and tear of assets or the depreciation on it.

Debt equity ratio: This ratio is helpful to determine the financial risk for the company by

showing the proportion of debt and equity in the overall capital structure of the company. In case

receivables because of having quality customers who usually make payment quickly.

Return on Equity (ROE)

Return of equity ratio reflects the ability of an organization to maintain and organize the capital

of the shareholders. Higher roe ratio states that a firm is highly capable to manage funds. From

the above table it can be stated that the ability of the organization to maintain the capital has

decreased from the past year (Al‐Hadi & et.al., 2019). For improvement the return on equity of

Dega cheese Ltd. it has been recommended to increase the profit margins on the products and

services of the firm. This can give. Firm can work on increasing the efficiency of the supply

chain to reduce the variable cost that can reduce the total cost of the product. Reduction in the

procurement of raw material can help the firm to increase the profits. Moreover, the organization

can focus on improvement of asset turnover to gain higher capability. Idle cash hold by the

company can be distributed to the shareholders to get a leverage. It can boost the return on equity

as the variable of shareholders equity increases with the distribution. The distribution of the cash

also influences the investors towards the company as they see lucrative returns.

Return on Assets (ROA)

The profitability of the company in relation with the assets possessed by them is depicted by the

return of assets ratio. This ratio helps the management to determine the efficiency of the

organization to earn profits through proper allocation of resources (Wu & et.al., 2020). Higher

ROA reflects the higher efficiency of the business to organize assets. The table has shown a

decline in the ability of firm to organize assets as the return on asset ratio has decreased from the

previous year. For improving this ratio the organization can focus on increasing the efficiency of

current and fixed assets. Current assets include cash, bills receivable etc. whose allocation and

usage can be done properly so that the firm can achieve higher profits from it. Receivable are of

high importance to the organization which can be managed thoroughly. Working on the credit

policy and collection process of receivable can help in doing so. For improving the return on

assets, entity can opt for leasing the assets instead of purchasing it. It will eliminate the cost

incurred on the wear and tear of assets or the depreciation on it.

Debt equity ratio: This ratio is helpful to determine the financial risk for the company by

showing the proportion of debt and equity in the overall capital structure of the company. In case

of higher debt – equity ratio, this means the firm have more of debt capital as compared to equity

capital in its overall capital and accordingly, the firm must be having more financial risk in terms

of meeting interest as well as repayment of principal obligations from time to time. The ideal

ratio that is considered to be good is between 2 or 2.5. By determining this ratio, company

indicates how much of debt and equity they have used for financing their assets. In the given

case of Bega Cheese, the ratio has been calculated for two years which comes out as 0.97 and

0.86 for 2021 and 2022 respectively. Accordingly, this figures for debt – equity ratio shows that

the company is having low financial risk as they have included less of debt and more of equity

towards financing their assets. In other words, low debt to equity ratio is the indicator of

company having more owned capital against borrowed capital. Therefore, the financial risk of

Bega Cheese is very low (Rahman and Shamsuddin, 2019).

EBIT or Earnings Before Interest & tax: This metrics shows the operating profit of the

company by excluding the tax and interest costs bear by the company and thus indicates

profitability of the company. In the year 2021, the EBIT of the company was found out as $109.6

million while in 2022, it has reduced to $46.3 million despite of rising revenue of the company.

Therefore, this difference in the profitability of the company can be attributed to the rise in

expenses of the company which it had incurred towards generating sales both directly &

indirectly (Almeida ,2019).

Price earnings ratio: It is measured for the company’s valuation by comparing the

market price and earnings per share and accordingly indicate the willingness of market for

paying towards the company’s stock based on their past or potential future earnings. In the given

case, the p/e ratio has increased from 0.19 to 0.48 between 2021 and 2022 and accordingly, it can

be said that market’s willingness to pay for the company’s share has increased. The determined

p/e ratio is quite low which indicates the current price of the stock is undervalued as compared to

the earnings.

Earnings per share (EPS)

The number of the outstanding common share of the company was divided by the net

profit to identify the earning per share. Generally, the ratio is between 13 and 15. The earning per

share of the Cheese Limited was decreased by 21.5 from the previous year. Decrease in the ratio

indicates that shareholder will get lower return on the investment and poor health of the

capital in its overall capital and accordingly, the firm must be having more financial risk in terms

of meeting interest as well as repayment of principal obligations from time to time. The ideal

ratio that is considered to be good is between 2 or 2.5. By determining this ratio, company

indicates how much of debt and equity they have used for financing their assets. In the given

case of Bega Cheese, the ratio has been calculated for two years which comes out as 0.97 and

0.86 for 2021 and 2022 respectively. Accordingly, this figures for debt – equity ratio shows that

the company is having low financial risk as they have included less of debt and more of equity

towards financing their assets. In other words, low debt to equity ratio is the indicator of

company having more owned capital against borrowed capital. Therefore, the financial risk of

Bega Cheese is very low (Rahman and Shamsuddin, 2019).

EBIT or Earnings Before Interest & tax: This metrics shows the operating profit of the

company by excluding the tax and interest costs bear by the company and thus indicates

profitability of the company. In the year 2021, the EBIT of the company was found out as $109.6

million while in 2022, it has reduced to $46.3 million despite of rising revenue of the company.

Therefore, this difference in the profitability of the company can be attributed to the rise in

expenses of the company which it had incurred towards generating sales both directly &

indirectly (Almeida ,2019).

Price earnings ratio: It is measured for the company’s valuation by comparing the

market price and earnings per share and accordingly indicate the willingness of market for

paying towards the company’s stock based on their past or potential future earnings. In the given

case, the p/e ratio has increased from 0.19 to 0.48 between 2021 and 2022 and accordingly, it can

be said that market’s willingness to pay for the company’s share has increased. The determined

p/e ratio is quite low which indicates the current price of the stock is undervalued as compared to

the earnings.

Earnings per share (EPS)

The number of the outstanding common share of the company was divided by the net

profit to identify the earning per share. Generally, the ratio is between 13 and 15. The earning per

share of the Cheese Limited was decreased by 21.5 from the previous year. Decrease in the ratio

indicates that shareholder will get lower return on the investment and poor health of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. Due to the decrease in the income of the company also leads to decrease in the ratio

(Almira and Wiagustini, 2020). The growth in the future will be impacted if there will be the

decrease in the ratio. Cheese limited can decrease the cut cost and the expenses to increase the

earning per share ratio. The ratio can also be improved by increasing the sales of the company in

the future. Decreasing the outstanding share through the process of buyback will help the

company in increasing the earning per share. Due to the repurchase of the share it can be

increased.

(Almira and Wiagustini, 2020). The growth in the future will be impacted if there will be the

decrease in the ratio. Cheese limited can decrease the cut cost and the expenses to increase the

earning per share ratio. The ratio can also be improved by increasing the sales of the company in

the future. Decreasing the outstanding share through the process of buyback will help the

company in increasing the earning per share. Due to the repurchase of the share it can be

increased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Wijaya, D. P., & Sedana, I. B. P. (2020). Effects of quick ratio, return on assets and exchange

rates on stock returns. Am. J. Humanities Soc. Sci. Res. 4. 323-329.

Almira, N. P. A. K., & Wiagustini, N. L. P. (2020). Return on asset, return on equity, dan

earning per share berpengaruh terhadap return saham. E-Jurnal Manajemen Universitas

Udayana, 9(3). 1069.

Nuryani, Y., & Sunarsi, D. (2020). The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi

Akuntansi). 4(2). 304-312.

Almeida, H. (2019). Is it time to get rid of earnings-per-share (EPS)?. Review of Corporate

Finance Studies. 8(1). 174-206.

Rahman, M. L., & Shamsuddin, A. (2019). Investor sentiment and the price-earnings ratio in the

G7 stock markets. Pacific-Basin Finance Journal. 55. 46-62.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress

in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic

Sciences, 86(2), pp.155-165.

Campisi, D., and et.al., 2019. Efficiency assessment of knowledge intensive business services

industry in Italy: Data envelopment analysis (DEA) and financial ratio

analysis. Measuring Business Excellence, 23(4), pp.484-495.

Islami, I.N. and Rio, W., 2019. Financial ratio analysis to predict financial distress on property

and real estate company listed in indonesia stock exchange. JAAF (Journal of Applied

Accounting and Finance), 2(2), pp.125-137.

Wu, J. & et.al., (2020). The economic policy uncertainty and firm investment in

Australia. Applied Economics, 52(31), 3354-3378.

Al‐Hadi, A. & et.al., (2019). Corporate social responsibility performance, financial distress and

firm life cycle: evidence from Australia. Accounting & Finance, 59(2), 961-989.

Books and Journals

Wijaya, D. P., & Sedana, I. B. P. (2020). Effects of quick ratio, return on assets and exchange

rates on stock returns. Am. J. Humanities Soc. Sci. Res. 4. 323-329.

Almira, N. P. A. K., & Wiagustini, N. L. P. (2020). Return on asset, return on equity, dan

earning per share berpengaruh terhadap return saham. E-Jurnal Manajemen Universitas

Udayana, 9(3). 1069.

Nuryani, Y., & Sunarsi, D. (2020). The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi

Akuntansi). 4(2). 304-312.

Almeida, H. (2019). Is it time to get rid of earnings-per-share (EPS)?. Review of Corporate

Finance Studies. 8(1). 174-206.

Rahman, M. L., & Shamsuddin, A. (2019). Investor sentiment and the price-earnings ratio in the

G7 stock markets. Pacific-Basin Finance Journal. 55. 46-62.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress

in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic

Sciences, 86(2), pp.155-165.

Campisi, D., and et.al., 2019. Efficiency assessment of knowledge intensive business services

industry in Italy: Data envelopment analysis (DEA) and financial ratio

analysis. Measuring Business Excellence, 23(4), pp.484-495.

Islami, I.N. and Rio, W., 2019. Financial ratio analysis to predict financial distress on property

and real estate company listed in indonesia stock exchange. JAAF (Journal of Applied

Accounting and Finance), 2(2), pp.125-137.

Wu, J. & et.al., (2020). The economic policy uncertainty and firm investment in

Australia. Applied Economics, 52(31), 3354-3378.

Al‐Hadi, A. & et.al., (2019). Corporate social responsibility performance, financial distress and

firm life cycle: evidence from Australia. Accounting & Finance, 59(2), 961-989.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.