MS FM Behavioral Finance Report: Prospect Theory and Biases Analysis

VerifiedAdded on 2022/10/11

|20

|4631

|29

Report

AI Summary

This report, prepared for Shefrain Consulting, delves into behavioral finance, examining prospect theory and its contrast with expected utility theory. It identifies various cognitive biases, including hindsight bias, and explores their impact on investment decisions and corporate finance. The report provides a detailed analysis of prospect theory's value function, loss aversion, and the equity premium puzzle. Furthermore, it explores the application of behavioral finance in investment strategies and portfolio allocation, considering the influence of behavioral factors on key financial decisions. The report also discusses the implications of behavioral finance on the author's career and the prospects for Shefrain Consulting, offering a comprehensive understanding of the field.

Running head : BEHAVIOURAL FINANCE

BEHAVIOURAL FINANCE

Name of the Student

Name of the University

Author Note

BEHAVIOURAL FINANCE

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BEHAVIOURAL FINANCE

Table of Contents

Executive Summary...................................................................................................................2

White paper on Prospect Theory................................................................................................3

Bias Identification....................................................................................................................10

Behavioral Finance and Investments.......................................................................................11

Behavioural Corporate Finance................................................................................................13

Future and Behavioural Finance Post 2008.............................................................................14

References................................................................................................................................16

Table of Contents

Executive Summary...................................................................................................................2

White paper on Prospect Theory................................................................................................3

Bias Identification....................................................................................................................10

Behavioral Finance and Investments.......................................................................................11

Behavioural Corporate Finance................................................................................................13

Future and Behavioural Finance Post 2008.............................................................................14

References................................................................................................................................16

BEHAVIOURAL FINANCE

Executive Summary

The aim of the study is to deliver six parts for the new employer, Shefrain Consulting

for the purpose of demonstration of the competence in the area of the Behavioural Finance.

The report further aims towards a matured knowledge regarding the Prospect theory and the

areas where it implies, on the traditional theory of making of decisions. Apart from that, the

report gives knowledge on the various behaviour biases, and where can they be implemented.

It provides a brief demonstration on the theory of behaviour finance with respect to an

investment decision of a particular client as well as the allocation of its portfolio. The various

essential financial decisions, which may be impacted by the behavioural factors, are also

taken into consideration. It articulates the essential aspects of behaviour finance that may

have an impact on my career plus prospects for Shefrain Consulting.

Executive Summary

The aim of the study is to deliver six parts for the new employer, Shefrain Consulting

for the purpose of demonstration of the competence in the area of the Behavioural Finance.

The report further aims towards a matured knowledge regarding the Prospect theory and the

areas where it implies, on the traditional theory of making of decisions. Apart from that, the

report gives knowledge on the various behaviour biases, and where can they be implemented.

It provides a brief demonstration on the theory of behaviour finance with respect to an

investment decision of a particular client as well as the allocation of its portfolio. The various

essential financial decisions, which may be impacted by the behavioural factors, are also

taken into consideration. It articulates the essential aspects of behaviour finance that may

have an impact on my career plus prospects for Shefrain Consulting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEHAVIOURAL FINANCE

White paper on Prospect Theory

1. Prospect theory vs. expected utility theory

Prospect Theory

(Barberis, Nicholas, Abhiroop Mukherjee, and Baolian Wang 2016)Prospect Theory

goes on an assumption that losses and the gains are estimated on the distinctly and

therefore the making of an individual’s decisions, which are on the basis of perceived

profits in place of the perceived losses(Deshmukh, G. K., and Sanskrity Joseph 2016).

The Prospect Theory is also called as the Loss Aversion theory( Ramiah, V., Zhao, Y.,

Moosa, I., & Graham, M. 2016). The general conception behind the Prospect theory is

that of two alternatives are taken together in front of a particular individual, both having

equality in the presentation in terms of the possible profits and the rest in terms of

potential losses, the first alternative being taken into consideration (Joo, Bashir Ahmad,

and Kokab Durri.2015).

The working of the Prospect theory

According to Baker, H. Kent, Greg Filbeck, and Victor Ricciardi (2017) The

Prospect theory can be defined as the theory which is a part of subgroup of Behavioural

Economics, which describes how the individuals can make a choice between the

probabilistic Alternative, which involves risks, and the possibility of distinct outputs id

not known to the individual. The underlying explanation for the behaviour of an

individual under the Behavioural Finance theory or the Prospect theory can be that due to

the choices that are independent and singular, the possibility of the profit or losses is

reasonably taken into the assumption as being the half possibility that is actually

presented. Significantly, the possibility of the profit is generally taken into perception as

much greater (Hsu, Dan K., Johan Wiklund, and Richard D. Cotton 2017). A proposal

White paper on Prospect Theory

1. Prospect theory vs. expected utility theory

Prospect Theory

(Barberis, Nicholas, Abhiroop Mukherjee, and Baolian Wang 2016)Prospect Theory

goes on an assumption that losses and the gains are estimated on the distinctly and

therefore the making of an individual’s decisions, which are on the basis of perceived

profits in place of the perceived losses(Deshmukh, G. K., and Sanskrity Joseph 2016).

The Prospect Theory is also called as the Loss Aversion theory( Ramiah, V., Zhao, Y.,

Moosa, I., & Graham, M. 2016). The general conception behind the Prospect theory is

that of two alternatives are taken together in front of a particular individual, both having

equality in the presentation in terms of the possible profits and the rest in terms of

potential losses, the first alternative being taken into consideration (Joo, Bashir Ahmad,

and Kokab Durri.2015).

The working of the Prospect theory

According to Baker, H. Kent, Greg Filbeck, and Victor Ricciardi (2017) The

Prospect theory can be defined as the theory which is a part of subgroup of Behavioural

Economics, which describes how the individuals can make a choice between the

probabilistic Alternative, which involves risks, and the possibility of distinct outputs id

not known to the individual. The underlying explanation for the behaviour of an

individual under the Behavioural Finance theory or the Prospect theory can be that due to

the choices that are independent and singular, the possibility of the profit or losses is

reasonably taken into the assumption as being the half possibility that is actually

presented. Significantly, the possibility of the profit is generally taken into perception as

much greater (Hsu, Dan K., Johan Wiklund, and Richard D. Cotton 2017). A proposal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BEHAVIOURAL FINANCE

from Tversky and Kahneman came that losses may lead to a greater emotional influence

on an individual compared to the one who does an equivalent amount of gain so given

alternatives presented in two ways. One with both offering the same outputs- an

individuals will choose the option which offers perceived profits (Tuyon, Jasman, and

Zamri Ahmad 2016 : Clark, William AV, and William Lisowski 2017).

Utility Theory

The utility theory is the theory which talks about the utility that is derived from a

certain commodity (goods or services). However, it is not possible to evaluate the amount

of utility that can be derived from a certain commodity. Therefore, in the utility theory the

alternatives are ordered in the ranks of their preferences to the consumer. As this

alternative, is limited by the price and the earnings of the consumers, the rational

consumer will not be spending the amount on an additional unit of the certain commodity

unless and until he receives the marginal or the additional utility from the consumption of

that commodity. Hence there is a relation to the marginal utility and the consumer will be

ranking the his or her preferences in accordance with that (Baddeley, Michelle 2018).

The utility theory in economics refers to the concept of the utility that can be derived

from the usage of a product. The moral philosophers like Jeremy Bentham and John

Stuart Mill also know it as the theory of Utilitarianism (Raj, and Supriya Maheshwari

2016).

Application

The application of Utility is where the economists undergo the construction of the

indifference curve that plot the bundles of the goods and services that an individual or a

society would take into acceptance the satisfaction at a given level. Indifferences and

utility curves are used by the economists for the understanding of the underpinnings of

from Tversky and Kahneman came that losses may lead to a greater emotional influence

on an individual compared to the one who does an equivalent amount of gain so given

alternatives presented in two ways. One with both offering the same outputs- an

individuals will choose the option which offers perceived profits (Tuyon, Jasman, and

Zamri Ahmad 2016 : Clark, William AV, and William Lisowski 2017).

Utility Theory

The utility theory is the theory which talks about the utility that is derived from a

certain commodity (goods or services). However, it is not possible to evaluate the amount

of utility that can be derived from a certain commodity. Therefore, in the utility theory the

alternatives are ordered in the ranks of their preferences to the consumer. As this

alternative, is limited by the price and the earnings of the consumers, the rational

consumer will not be spending the amount on an additional unit of the certain commodity

unless and until he receives the marginal or the additional utility from the consumption of

that commodity. Hence there is a relation to the marginal utility and the consumer will be

ranking the his or her preferences in accordance with that (Baddeley, Michelle 2018).

The utility theory in economics refers to the concept of the utility that can be derived

from the usage of a product. The moral philosophers like Jeremy Bentham and John

Stuart Mill also know it as the theory of Utilitarianism (Raj, and Supriya Maheshwari

2016).

Application

The application of Utility is where the economists undergo the construction of the

indifference curve that plot the bundles of the goods and services that an individual or a

society would take into acceptance the satisfaction at a given level. Indifferences and

utility curves are used by the economists for the understanding of the underpinnings of

BEHAVIOURAL FINANCE

the demand curves, that are half of the supply and demand analysis that is used for the

analysis of the workings of the good markets (Prashanth, L. A., et al 2016).

Prospect theory versus Utility theory

Utility Theory is considered one of the best normative theory in which it provides the

description on how the people are supposed to behave. It refers to the branch of homo

economics, which is the rationale, that is taken into assumption, as the consumer of the

classical economic theory. The theory also takes into assumptions the final results and the

of the wealth condition regarding risks that are linked to the proposed results (Kumar,

Satish, and Nisha Goyal 2015).

Contrasting to the Utility theory, the Prospect theory is a theory which is explanatory

in nature (Ebert, Sebastian, and Philipp Strack 2015). It seeks to provide description on

how the people actually behave, if they are given their bounds of rationality as well as the

calculations which are perfectly cognitive. It takes into assumptions which the individuals

take decision that are based on the profits and losses though some imaginary starting

points rather than the final outcomes that are obtained from those profits and losses.

The performances of trials by Tversky and Kahneman in developing of the prospect

theory showed that the tendency of people is to limitlessly weight the results with the

small possibilities and the underweight higher possible results (Li, Yongjian, and

Chengqing Wang 2017).

2. Example of the violation of Utility theory

Independent axiom

The derivation of the Von Neumann and Morgenstern’s utility theory refers to the

theory that is taken from three axioms, which are order, independence and continuity. The

the demand curves, that are half of the supply and demand analysis that is used for the

analysis of the workings of the good markets (Prashanth, L. A., et al 2016).

Prospect theory versus Utility theory

Utility Theory is considered one of the best normative theory in which it provides the

description on how the people are supposed to behave. It refers to the branch of homo

economics, which is the rationale, that is taken into assumption, as the consumer of the

classical economic theory. The theory also takes into assumptions the final results and the

of the wealth condition regarding risks that are linked to the proposed results (Kumar,

Satish, and Nisha Goyal 2015).

Contrasting to the Utility theory, the Prospect theory is a theory which is explanatory

in nature (Ebert, Sebastian, and Philipp Strack 2015). It seeks to provide description on

how the people actually behave, if they are given their bounds of rationality as well as the

calculations which are perfectly cognitive. It takes into assumptions which the individuals

take decision that are based on the profits and losses though some imaginary starting

points rather than the final outcomes that are obtained from those profits and losses.

The performances of trials by Tversky and Kahneman in developing of the prospect

theory showed that the tendency of people is to limitlessly weight the results with the

small possibilities and the underweight higher possible results (Li, Yongjian, and

Chengqing Wang 2017).

2. Example of the violation of Utility theory

Independent axiom

The derivation of the Von Neumann and Morgenstern’s utility theory refers to the

theory that is taken from three axioms, which are order, independence and continuity. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEHAVIOURAL FINANCE

independent axiom states, “if an alternative is non optimal for a leadership decision

problem, it cannot be made optimal by adding new alternatives to the problem.” The

independent axiom, which is also called the “principle of independence of irrelevant

alternatives” (LTUNTAŞ, Semra T., Vedat Sarikovanlik, and Nertil Mera 2017).

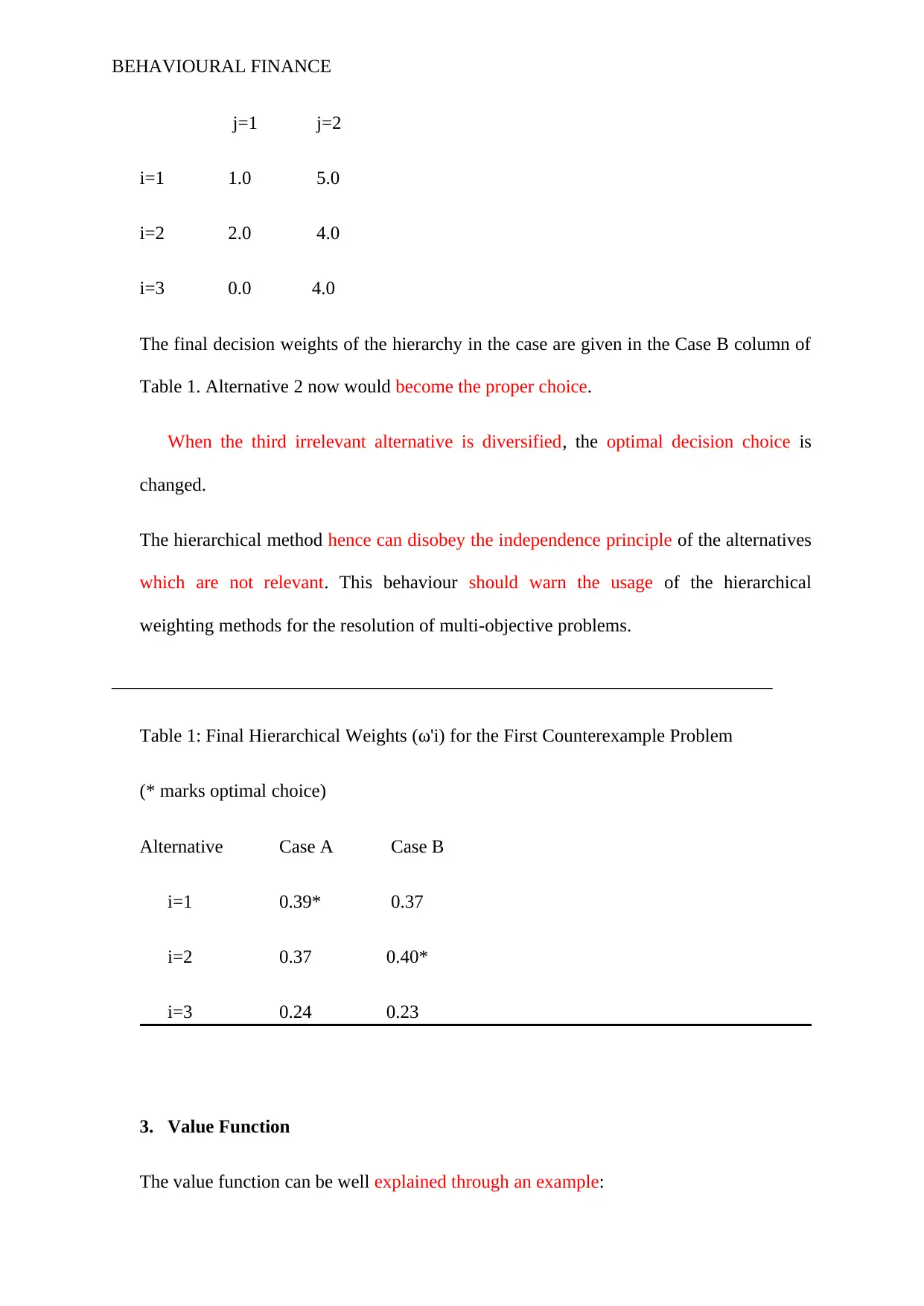

The defying of the independent axiom by the hierarchical weighting methods’ application

to select a single best option, which is explained with the help of an example.

The objective weights possess values β1 = 0.25 and β2 = 0.75

First, case of three trials with performances are taken into consideration, Pij, given by:

j=1 j=2

i=1 1.0 5.0

i=2 2.0 4.0

i=3 2.0 2.0

It is to be noted that the initial two alternative are the members of a non-dominated set

of solutions in which the third alternative is clearly inferior. To cite an example the final

decision weights that is provided by the applying Equation 1 that come in the case A

column of table 1.

For this case, alternative

1 is the proper choice.

Next, we should consider the same issue, apart from the third (inferior) Alternative has

been altered, but the inferiority of the alternative remains at place. The performances, Pij,

are now:

independent axiom states, “if an alternative is non optimal for a leadership decision

problem, it cannot be made optimal by adding new alternatives to the problem.” The

independent axiom, which is also called the “principle of independence of irrelevant

alternatives” (LTUNTAŞ, Semra T., Vedat Sarikovanlik, and Nertil Mera 2017).

The defying of the independent axiom by the hierarchical weighting methods’ application

to select a single best option, which is explained with the help of an example.

The objective weights possess values β1 = 0.25 and β2 = 0.75

First, case of three trials with performances are taken into consideration, Pij, given by:

j=1 j=2

i=1 1.0 5.0

i=2 2.0 4.0

i=3 2.0 2.0

It is to be noted that the initial two alternative are the members of a non-dominated set

of solutions in which the third alternative is clearly inferior. To cite an example the final

decision weights that is provided by the applying Equation 1 that come in the case A

column of table 1.

For this case, alternative

1 is the proper choice.

Next, we should consider the same issue, apart from the third (inferior) Alternative has

been altered, but the inferiority of the alternative remains at place. The performances, Pij,

are now:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BEHAVIOURAL FINANCE

j=1 j=2

i=1 1.0 5.0

i=2 2.0 4.0

i=3 0.0 4.0

The final decision weights of the hierarchy in the case are given in the Case B column of

Table 1. Alternative 2 now would become the proper choice.

When the third irrelevant alternative is diversified, the optimal decision choice is

changed.

The hierarchical method hence can disobey the independence principle of the alternatives

which are not relevant. This behaviour should warn the usage of the hierarchical

weighting methods for the resolution of multi-objective problems.

_______________________________________________________________________

Table 1: Final Hierarchical Weights (ω'i) for the First Counterexample Problem

(* marks optimal choice)

Alternative Case A Case B

i=1 0.39* 0.37

i=2 0.37 0.40*

i=3 0.24 0.23

3. Value Function

The value function can be well explained through an example:

j=1 j=2

i=1 1.0 5.0

i=2 2.0 4.0

i=3 0.0 4.0

The final decision weights of the hierarchy in the case are given in the Case B column of

Table 1. Alternative 2 now would become the proper choice.

When the third irrelevant alternative is diversified, the optimal decision choice is

changed.

The hierarchical method hence can disobey the independence principle of the alternatives

which are not relevant. This behaviour should warn the usage of the hierarchical

weighting methods for the resolution of multi-objective problems.

_______________________________________________________________________

Table 1: Final Hierarchical Weights (ω'i) for the First Counterexample Problem

(* marks optimal choice)

Alternative Case A Case B

i=1 0.39* 0.37

i=2 0.37 0.40*

i=3 0.24 0.23

3. Value Function

The value function can be well explained through an example:

BEHAVIOURAL FINANCE

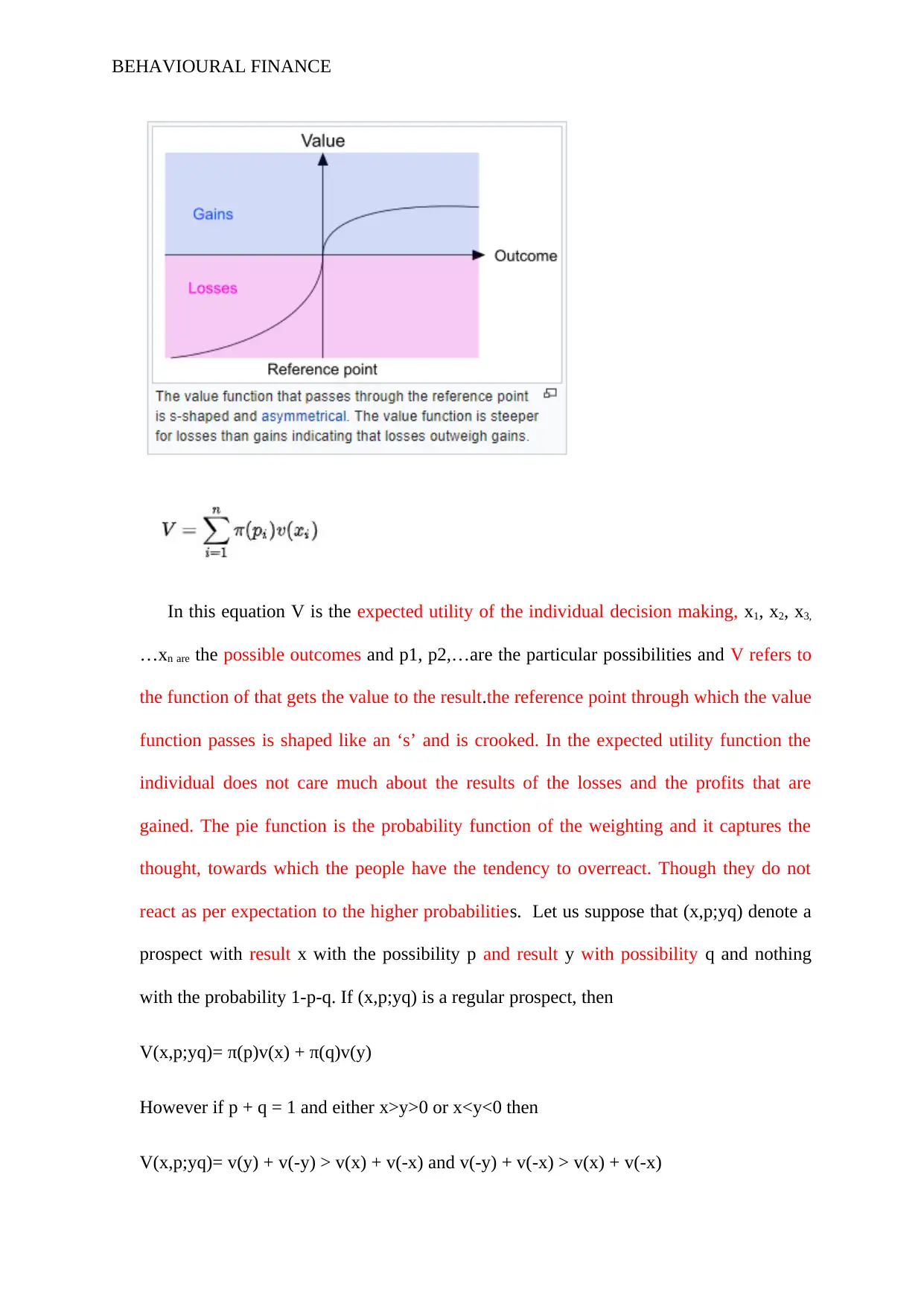

In this equation V is the expected utility of the individual decision making, x1, x2, x3,

…xn are the possible outcomes and p1, p2,…are the particular possibilities and V refers to

the function of that gets the value to the result.the reference point through which the value

function passes is shaped like an ‘s’ and is crooked. In the expected utility function the

individual does not care much about the results of the losses and the profits that are

gained. The pie function is the probability function of the weighting and it captures the

thought, towards which the people have the tendency to overreact. Though they do not

react as per expectation to the higher probabilities. Let us suppose that (x,p;yq) denote a

prospect with result x with the possibility p and result y with possibility q and nothing

with the probability 1-p-q. If (x,p;yq) is a regular prospect, then

V(x,p;yq)= π(p)v(x) + π(q)v(y)

However if p + q = 1 and either x>y>0 or x<y<0 then

V(x,p;yq)= v(y) + v(-y) > v(x) + v(-x) and v(-y) + v(-x) > v(x) + v(-x)

In this equation V is the expected utility of the individual decision making, x1, x2, x3,

…xn are the possible outcomes and p1, p2,…are the particular possibilities and V refers to

the function of that gets the value to the result.the reference point through which the value

function passes is shaped like an ‘s’ and is crooked. In the expected utility function the

individual does not care much about the results of the losses and the profits that are

gained. The pie function is the probability function of the weighting and it captures the

thought, towards which the people have the tendency to overreact. Though they do not

react as per expectation to the higher probabilities. Let us suppose that (x,p;yq) denote a

prospect with result x with the possibility p and result y with possibility q and nothing

with the probability 1-p-q. If (x,p;yq) is a regular prospect, then

V(x,p;yq)= π(p)v(x) + π(q)v(y)

However if p + q = 1 and either x>y>0 or x<y<0 then

V(x,p;yq)= v(y) + v(-y) > v(x) + v(-x) and v(-y) + v(-x) > v(x) + v(-x)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEHAVIOURAL FINANCE

Value function therefore refers to the divergence from the points of reference that are

concave for the profits and commonly convex for the losses and steeper for losses than

for the gains (Benveniste, Elie, and Gordon Ritter 2017).

4. Implications of prospect theory

1) Value is relative to a reference point

The perception of the value depends on the relative deviation. It does not depend on

the absolute value.

Importance

In Von Neumann Morgenstern utility, that serves as the base for expected utility

theory (EUT), the last outcome of a speculation is the final determining factor of the

utility. Under the expected utility theory whether the speculation is arranged as a

profit or a loss is not at all relevant. In opposition to it the prospect theory holds the

value which is defined on the basis of the relative change in the wealth in replacement

of resultant levels of wealth.

5. Anomaly by prospect theory

The equity premium puzzle, which comes under the anomaly by the prospect theory,

can be defined as the lack of ability of a significant class of models of economics. It is for

the explanation of the premium of a modified United States equity portfolio over the

United States treasury bills that are under the observation for not less than 100 years.

Rajnish Mehra and Edward C. Prescott invented the term equity premium puzzle during a

study that was published in the year 1985 which possessed the title The Equity Premium:

A Puzzle. An initial version of the study was presented in the year 1982 which had the

title A test of the intertemporal asset pricing model. The writers had concluded that a

uniform general equilibrium model underwent the process of calibration to the display

key United States business cycle fluctuations, which generated an Equity premium of less

Value function therefore refers to the divergence from the points of reference that are

concave for the profits and commonly convex for the losses and steeper for losses than

for the gains (Benveniste, Elie, and Gordon Ritter 2017).

4. Implications of prospect theory

1) Value is relative to a reference point

The perception of the value depends on the relative deviation. It does not depend on

the absolute value.

Importance

In Von Neumann Morgenstern utility, that serves as the base for expected utility

theory (EUT), the last outcome of a speculation is the final determining factor of the

utility. Under the expected utility theory whether the speculation is arranged as a

profit or a loss is not at all relevant. In opposition to it the prospect theory holds the

value which is defined on the basis of the relative change in the wealth in replacement

of resultant levels of wealth.

5. Anomaly by prospect theory

The equity premium puzzle, which comes under the anomaly by the prospect theory,

can be defined as the lack of ability of a significant class of models of economics. It is for

the explanation of the premium of a modified United States equity portfolio over the

United States treasury bills that are under the observation for not less than 100 years.

Rajnish Mehra and Edward C. Prescott invented the term equity premium puzzle during a

study that was published in the year 1985 which possessed the title The Equity Premium:

A Puzzle. An initial version of the study was presented in the year 1982 which had the

title A test of the intertemporal asset pricing model. The writers had concluded that a

uniform general equilibrium model underwent the process of calibration to the display

key United States business cycle fluctuations, which generated an Equity premium of less

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BEHAVIOURAL FINANCE

than 1 % for an answerable risk aversion levels. This outcome stood in sharp opposition

with the average equity premium of six percent that was observed during the historical

period (Dickason-Koekemoer, Z., and S. J. Ferreira. 2018).

Bias Identification

The concept for the first conversation

The concept of behavioural finance that is followed in the first conversation is the

hindsight Bias. In this concept the people are more likely to make predictions. If they find

out that, their prediction is coming true they would stick to the same decision making in the

next investment (Heaton, J. B.2019). However no one is confident of the future possibilities.

They tend to make decisions based on predictions. In this model, just because he knows the

industry well, he thinks that whatever predictions he would make, will fetch him better

returns, which is absolutely a sign of poor decision making skills(Lane, Anthony, et al 2016).

The concept for the second conversation

The concept of behavioural finance that is followed in the second conversation is the

Illusion of Control. There are many investors, who make their decision under the illusion of

control. In this concept if a person had invested some amount in stocks or shares and earns

profits thereafter, he goes on an assumption that the strategy that he uses to get the profits

year after year is the only strategy that exists in order to earn the similar amounts of profits

for the subsequent years. They consider themselves very superior. They have a thought

procedure that taking assistance from the external sources is not of much help.

With reference to the case, the person takes undue advantage of the losses, that are not

being showcased. He thinks that the way he is carrying on his operations is right. However he

refuses to take opinions from others. Therefore Illusion of Control concept is appropriate for

this case.

than 1 % for an answerable risk aversion levels. This outcome stood in sharp opposition

with the average equity premium of six percent that was observed during the historical

period (Dickason-Koekemoer, Z., and S. J. Ferreira. 2018).

Bias Identification

The concept for the first conversation

The concept of behavioural finance that is followed in the first conversation is the

hindsight Bias. In this concept the people are more likely to make predictions. If they find

out that, their prediction is coming true they would stick to the same decision making in the

next investment (Heaton, J. B.2019). However no one is confident of the future possibilities.

They tend to make decisions based on predictions. In this model, just because he knows the

industry well, he thinks that whatever predictions he would make, will fetch him better

returns, which is absolutely a sign of poor decision making skills(Lane, Anthony, et al 2016).

The concept for the second conversation

The concept of behavioural finance that is followed in the second conversation is the

Illusion of Control. There are many investors, who make their decision under the illusion of

control. In this concept if a person had invested some amount in stocks or shares and earns

profits thereafter, he goes on an assumption that the strategy that he uses to get the profits

year after year is the only strategy that exists in order to earn the similar amounts of profits

for the subsequent years. They consider themselves very superior. They have a thought

procedure that taking assistance from the external sources is not of much help.

With reference to the case, the person takes undue advantage of the losses, that are not

being showcased. He thinks that the way he is carrying on his operations is right. However he

refuses to take opinions from others. Therefore Illusion of Control concept is appropriate for

this case.

BEHAVIOURAL FINANCE

The concept for the third conversation

The concept of behavioural finance that has been used in the third conversation is the

confirmation Bias. In this concept, they have their inclination towards a specific information

that they have in their mind. These people do perform research works, and if the research that

they preform passes by them, they believe that the decision that they took is the one and only

decision that can be taken ion such an occurrence. They don’t do any kind of further research

work regarding the matter.

Behavioral Finance and Investments

1) Siosan’s Utility Function

The Siosan’s utility function can be defined as the combination of investments, which

will be generating maximum returns to her investment portfolio. It can be observed that, she

is a risk-averse investor and makes an optimum combination of short-term money market and

security market instruments in her investment portfolio. Therefore, she constructs and defines

all her investment and debt combinations, which will maximize her return with a lower risk

assumption.

Contrastingly, the traditional finance theory has two concepts and the most important

of them is the wealth maximization approach. In traditional finance theory, more focus is

given on the pay-outs or the return from an investment and less focus is given on the risk

aspect of the investment. The wealth maximization concept of traditional finance theory

requires making such investment strategies, which will maximize the value of the investment

or the overall wealth of the investor. In this case study, if Siosan follows the traditional

finance approach, then she would have constructed her investment portfolio with an objective

of increasing the value of total investment. In achieving such target, more growth securities

could have been included in her investment portfolio.

The concept for the third conversation

The concept of behavioural finance that has been used in the third conversation is the

confirmation Bias. In this concept, they have their inclination towards a specific information

that they have in their mind. These people do perform research works, and if the research that

they preform passes by them, they believe that the decision that they took is the one and only

decision that can be taken ion such an occurrence. They don’t do any kind of further research

work regarding the matter.

Behavioral Finance and Investments

1) Siosan’s Utility Function

The Siosan’s utility function can be defined as the combination of investments, which

will be generating maximum returns to her investment portfolio. It can be observed that, she

is a risk-averse investor and makes an optimum combination of short-term money market and

security market instruments in her investment portfolio. Therefore, she constructs and defines

all her investment and debt combinations, which will maximize her return with a lower risk

assumption.

Contrastingly, the traditional finance theory has two concepts and the most important

of them is the wealth maximization approach. In traditional finance theory, more focus is

given on the pay-outs or the return from an investment and less focus is given on the risk

aspect of the investment. The wealth maximization concept of traditional finance theory

requires making such investment strategies, which will maximize the value of the investment

or the overall wealth of the investor. In this case study, if Siosan follows the traditional

finance approach, then she would have constructed her investment portfolio with an objective

of increasing the value of total investment. In achieving such target, more growth securities

could have been included in her investment portfolio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.