Bell Studio Systems: Analysis of Information Systems and Controls

VerifiedAdded on 2023/01/23

|15

|3059

|69

Report

AI Summary

This report provides a comprehensive analysis of Bell Studio Systems' strategic information systems. It begins with an executive summary outlining the core findings, followed by an introduction that highlights the importance of enterprise resource planning systems and the need for system analysis. The report then delves into the system description, utilizing data flow diagrams and system flowcharts to represent the purchasing, cash disbursement, and payroll systems. Key internal control weaknesses are identified within each subsystem, including a lack of authorization, poorly defined procurement processes, poor task assignment, and a lack of oversight and payment review processes. The report meticulously details the risks associated with each weakness and offers recommendations for improvement, such as implementing authorization processes, defining clear procurement procedures, and improving task segregation to mitigate fraud and financial mismanagement risks. The analysis underscores the critical need for robust internal controls to ensure the effectiveness and reliability of the company's operations.

Bell Studio Systems 1

STRATEGIC INFORMATION SYSTEMS FOR BUSINESS AND ENTERPRISE

By [Name] [Number]

Course

Name of Course Professor

University

Location of University

Date of Submission

STRATEGIC INFORMATION SYSTEMS FOR BUSINESS AND ENTERPRISE

By [Name] [Number]

Course

Name of Course Professor

University

Location of University

Date of Submission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bell Studio Systems 2

Contents

1.0. Introduction...............................................................................................................................2

2.0. System Description....................................................................................................................3

2.1. Data Flow Diagrams...............................................................................................................3

2.1.1. Purchases and Cash Disbursement Systems..................................................................3

2.1.2. Payroll System....................................................................................................................5

2.2. System Flowchart..................................................................................................................6

2.2.1. Purchases System..........................................................................................................6

2.2.2. Cash Disbursement System............................................................................................8

2.2.3. Payroll System Flowchart...............................................................................................8

3.0. Internal Control.........................................................................................................................9

3.1. Purchases System................................................................................................................10

3.1.1. Authorization...............................................................................................................10

3.1.2. Procurement process...................................................................................................10

3.1.3. Assignment of tasks.....................................................................................................11

3.2. Cash Disbursement System..................................................................................................11

3.2.1. Lack of oversight..........................................................................................................11

3.2.2. Lack of Payment Review process.................................................................................11

3.3. Payroll System.....................................................................................................................11

3.3.1. Manual data input.......................................................................................................12

Contents

1.0. Introduction...............................................................................................................................2

2.0. System Description....................................................................................................................3

2.1. Data Flow Diagrams...............................................................................................................3

2.1.1. Purchases and Cash Disbursement Systems..................................................................3

2.1.2. Payroll System....................................................................................................................5

2.2. System Flowchart..................................................................................................................6

2.2.1. Purchases System..........................................................................................................6

2.2.2. Cash Disbursement System............................................................................................8

2.2.3. Payroll System Flowchart...............................................................................................8

3.0. Internal Control.........................................................................................................................9

3.1. Purchases System................................................................................................................10

3.1.1. Authorization...............................................................................................................10

3.1.2. Procurement process...................................................................................................10

3.1.3. Assignment of tasks.....................................................................................................11

3.2. Cash Disbursement System..................................................................................................11

3.2.1. Lack of oversight..........................................................................................................11

3.2.2. Lack of Payment Review process.................................................................................11

3.3. Payroll System.....................................................................................................................11

3.3.1. Manual data input.......................................................................................................12

Bell Studio Systems 3

Executive Summary

Bell Studio, an Adelaide art wholesaler hired an analyst to assist in analyzing the

various transaction cycles, financial reporting, and management reporting of its enterprise

system. Consequently, the system was divided into various subsystems that interact with

each other. These subsystems were the purchasing modules, cash disbursement, and payroll

modules. Each was represented using data flow diagrams and system flowcharts. After this

undertaking, each was analyzed for various internal control weaknesses. As a result, several

weaknesses were discovered in each of the subsystem. For this reason, the risk associated

with each internal control weakness was described. Weaknesses found include the lack of

properly defined procurement process, lack of managerial oversight and authorization, lack of

user authentication and lack of transaction monitoring process.

1.0. Introduction

Enterprise resource planning systems enable businesses to integrate various resources

and business processes towards achievement of the company’s goals. This helps address

various business concerns than cannot be addressed by other types of information systems

(Alrawashdeh, Muhairat and Qatawneh, 2014). This leads to cost reductions in operations

and ability to respond to users needs. However, due to uniqueness of each business’

processes, there is no one standardized model of implementing business information systems.

Therefore, analysis of each system becomes crucial in determining whether the system works

as expected. Additionally, it becomes imperative to determine whether the system exposes

the company to any risks associated with dependence on such a system. For this reason, this

report analyzes the Bell Studio Inc. information management system. This process will

include a discussion of various internal control weaknesses and their associated risk

implications to the company.

Executive Summary

Bell Studio, an Adelaide art wholesaler hired an analyst to assist in analyzing the

various transaction cycles, financial reporting, and management reporting of its enterprise

system. Consequently, the system was divided into various subsystems that interact with

each other. These subsystems were the purchasing modules, cash disbursement, and payroll

modules. Each was represented using data flow diagrams and system flowcharts. After this

undertaking, each was analyzed for various internal control weaknesses. As a result, several

weaknesses were discovered in each of the subsystem. For this reason, the risk associated

with each internal control weakness was described. Weaknesses found include the lack of

properly defined procurement process, lack of managerial oversight and authorization, lack of

user authentication and lack of transaction monitoring process.

1.0. Introduction

Enterprise resource planning systems enable businesses to integrate various resources

and business processes towards achievement of the company’s goals. This helps address

various business concerns than cannot be addressed by other types of information systems

(Alrawashdeh, Muhairat and Qatawneh, 2014). This leads to cost reductions in operations

and ability to respond to users needs. However, due to uniqueness of each business’

processes, there is no one standardized model of implementing business information systems.

Therefore, analysis of each system becomes crucial in determining whether the system works

as expected. Additionally, it becomes imperative to determine whether the system exposes

the company to any risks associated with dependence on such a system. For this reason, this

report analyzes the Bell Studio Inc. information management system. This process will

include a discussion of various internal control weaknesses and their associated risk

implications to the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bell Studio Systems 4

2.0. System Description

System analysts use various methods in describing computer information systems.

However, Data Flow diagrams and System flowcharts are commonly used to describe

computer systems. A data flow diagram (DFD) is a diagrammatic representation of the flow

of various processes and data across the system (Dobesova, 2014). This provides a visual

understanding of the system (Yakubu et al., 2011). Similarly, system flowchart is a visual

representation of the data flow in the system and hence the system process model (Ibrahim

and Yen, 2010). The main difference is that the system flowchart focuses on the flow control

and execution sequence of the process while DFDs focus on flow of data.

2.1. Data Flow Diagrams

2.1.1. Purchases and Cash Disbursement Systems

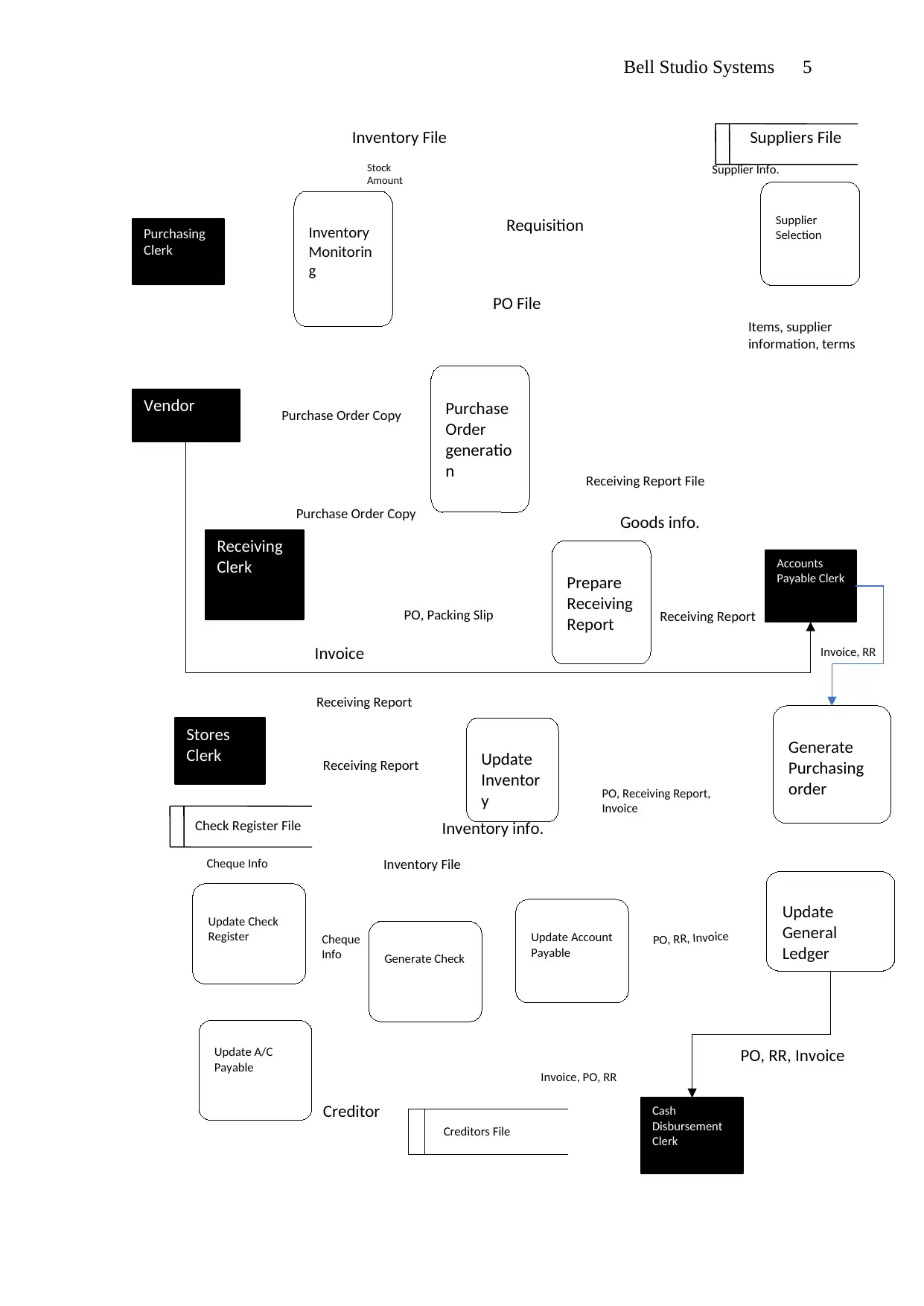

Purchasing systems are crucial in managing inventory and monitoring of stock. This

assists companies in understanding what to buy, when and from whom. Cash disbursement

system enables companies to handle payments effectively. The two systems are closely

related since the purchasing system depends on the latter to settle payments for goods

acquired. Similarly, the cash disbursement depends on the purchasing system to determine

what needs to be paid for and the amount. The two systems form a subsystem that can be

accurately represented using data flow diagrams. Data involved in this subsystem include

vendors, purchase orders, receiving reports, accounts payables, and inventory lists

2.0. System Description

System analysts use various methods in describing computer information systems.

However, Data Flow diagrams and System flowcharts are commonly used to describe

computer systems. A data flow diagram (DFD) is a diagrammatic representation of the flow

of various processes and data across the system (Dobesova, 2014). This provides a visual

understanding of the system (Yakubu et al., 2011). Similarly, system flowchart is a visual

representation of the data flow in the system and hence the system process model (Ibrahim

and Yen, 2010). The main difference is that the system flowchart focuses on the flow control

and execution sequence of the process while DFDs focus on flow of data.

2.1. Data Flow Diagrams

2.1.1. Purchases and Cash Disbursement Systems

Purchasing systems are crucial in managing inventory and monitoring of stock. This

assists companies in understanding what to buy, when and from whom. Cash disbursement

system enables companies to handle payments effectively. The two systems are closely

related since the purchasing system depends on the latter to settle payments for goods

acquired. Similarly, the cash disbursement depends on the purchasing system to determine

what needs to be paid for and the amount. The two systems form a subsystem that can be

accurately represented using data flow diagrams. Data involved in this subsystem include

vendors, purchase orders, receiving reports, accounts payables, and inventory lists

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supplier Info.

Inventory info.

Creditor

Stock

Amount

Receiving Report File

Inventory

Monitorin

g

Inventory File

Supplier

Selection

Purchase

Order

generatio

n

Purchasing

Clerk

Vendor

Receiving

Clerk Prepare

Receiving

Report

Stores

Clerk Update

Inventor

y

Accounts

Payable Clerk

Generate

Purchasing

order

Update Account

Payable

Update

General

Ledger

Cash

Disbursement

Clerk

Generate Check

Update Check

Register

Items, supplier

information, terms

Purchase Order Copy

PO, Packing Slip

Invoice

Receiving Report

Inventory File

PO, Receiving Report,

Invoice

Invoice, PO, RR

PO, RR, Invoice

Creditors File

Suppliers File

Purchase Order Copy

PO File

Requisition

Receiving Report

Receiving Report

Invoice, RR

Update A/C

Payable

Cheque

Info

Cheque Info

PO, RR, Invoice

Goods info.

Bell Studio Systems 5

Check Register File

Inventory info.

Creditor

Stock

Amount

Receiving Report File

Inventory

Monitorin

g

Inventory File

Supplier

Selection

Purchase

Order

generatio

n

Purchasing

Clerk

Vendor

Receiving

Clerk Prepare

Receiving

Report

Stores

Clerk Update

Inventor

y

Accounts

Payable Clerk

Generate

Purchasing

order

Update Account

Payable

Update

General

Ledger

Cash

Disbursement

Clerk

Generate Check

Update Check

Register

Items, supplier

information, terms

Purchase Order Copy

PO, Packing Slip

Invoice

Receiving Report

Inventory File

PO, Receiving Report,

Invoice

Invoice, PO, RR

PO, RR, Invoice

Creditors File

Suppliers File

Purchase Order Copy

PO File

Requisition

Receiving Report

Receiving Report

Invoice, RR

Update A/C

Payable

Cheque

Info

Cheque Info

PO, RR, Invoice

Goods info.

Bell Studio Systems 5

Check Register File

Payment Register

Payroll

Clerk

Time Card data

Entry

Time Card File

Update

Employees

records

Employee File

Process

Disbursement

voucher

Accounts

Payable

Clerk

General

Ledger

Clerk

Update

general Ledger

General Ledger file

Time Card,

Payroll

Register

Payment

Register

Disbursement

voucher

Hours worked

Payment Register

Salary expense

Work Data

Bell Studio Systems 6

Figure 1. Purchases and cash disbursement flow of data

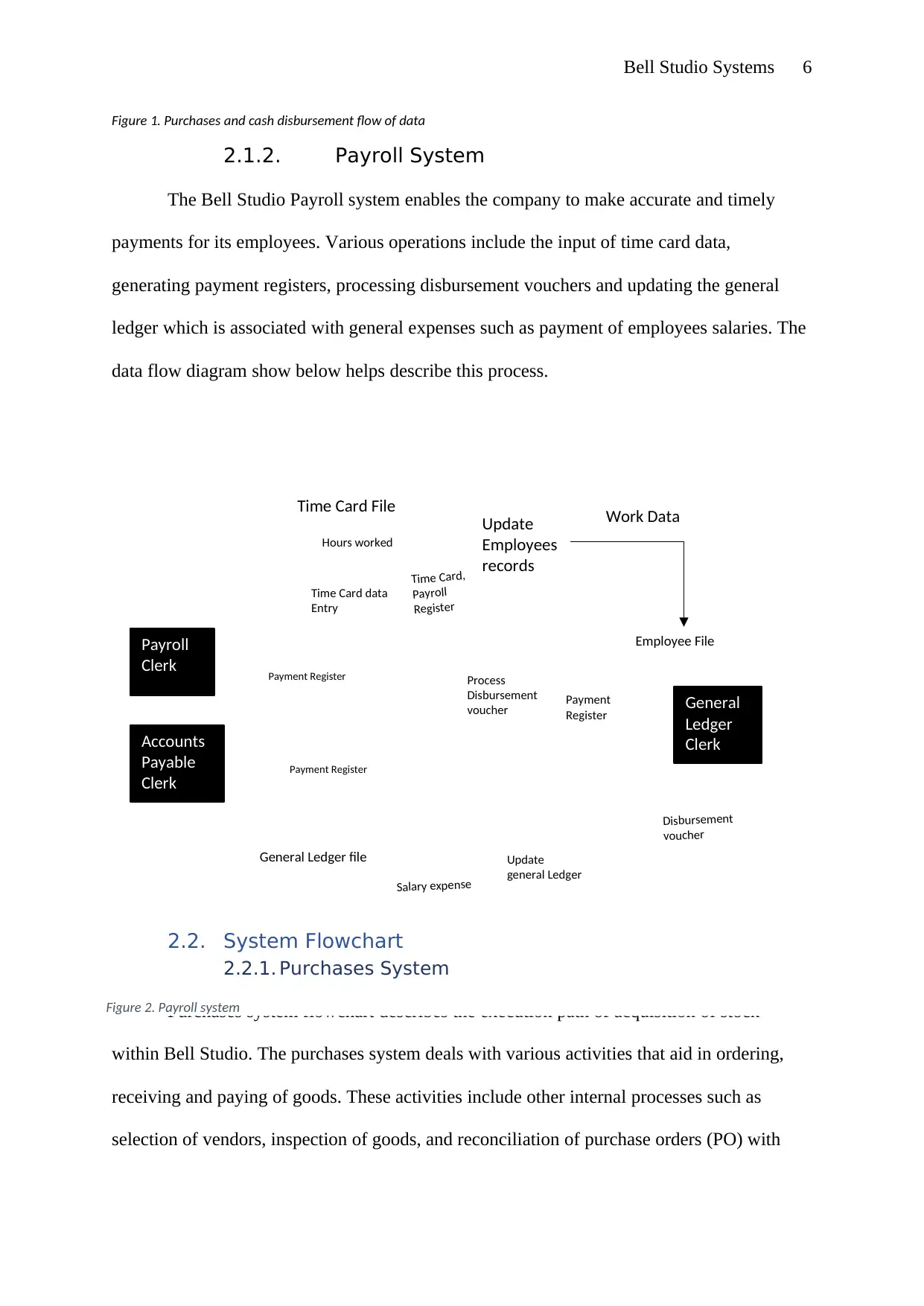

2.1.2. Payroll System

The Bell Studio Payroll system enables the company to make accurate and timely

payments for its employees. Various operations include the input of time card data,

generating payment registers, processing disbursement vouchers and updating the general

ledger which is associated with general expenses such as payment of employees salaries. The

data flow diagram show below helps describe this process.

2.2. System Flowchart

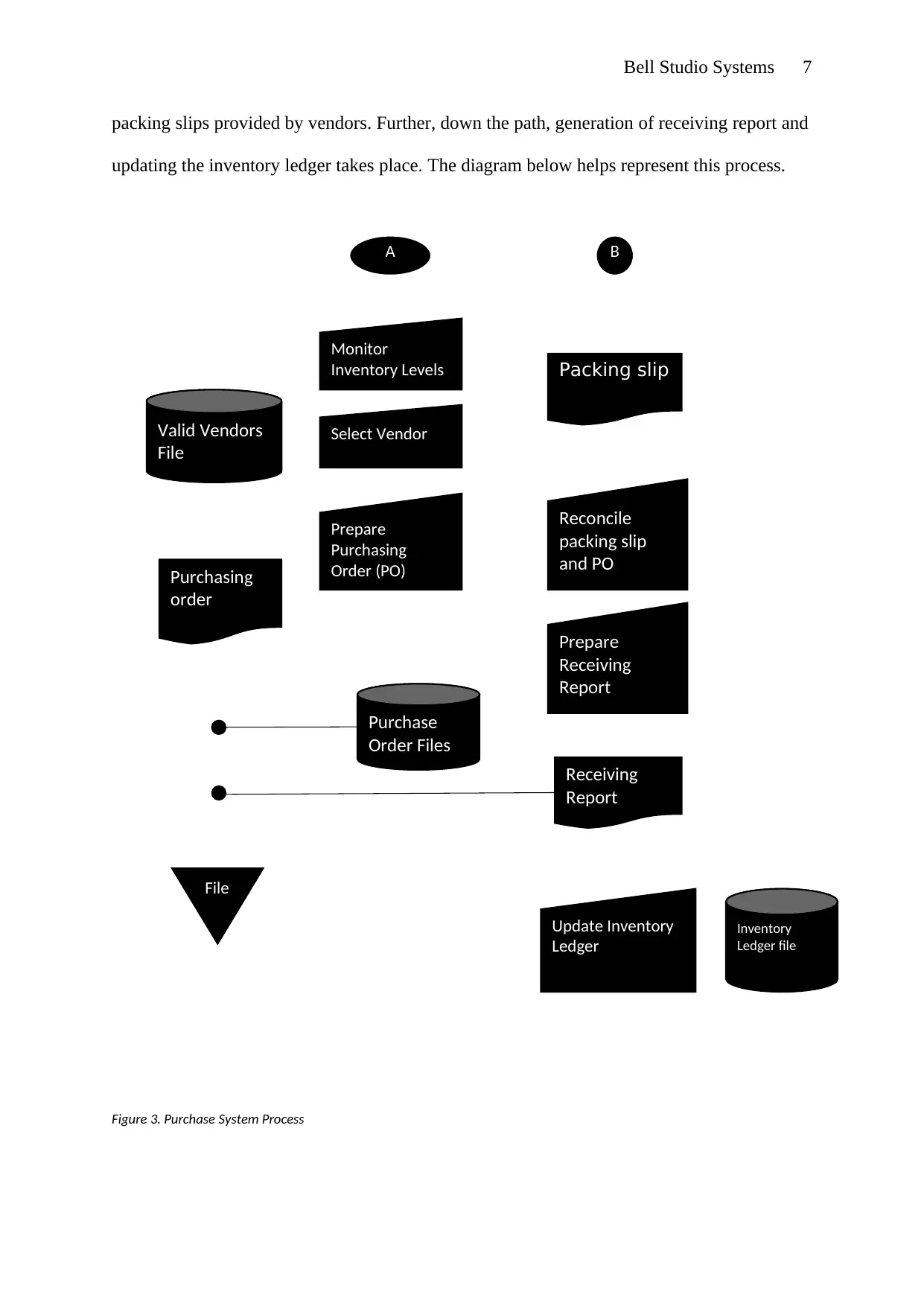

2.2.1. Purchases System

Purchases system flowchart describes the execution path of acquisition of stock

within Bell Studio. The purchases system deals with various activities that aid in ordering,

receiving and paying of goods. These activities include other internal processes such as

selection of vendors, inspection of goods, and reconciliation of purchase orders (PO) with

Figure 2. Payroll system

Payroll

Clerk

Time Card data

Entry

Time Card File

Update

Employees

records

Employee File

Process

Disbursement

voucher

Accounts

Payable

Clerk

General

Ledger

Clerk

Update

general Ledger

General Ledger file

Time Card,

Payroll

Register

Payment

Register

Disbursement

voucher

Hours worked

Payment Register

Salary expense

Work Data

Bell Studio Systems 6

Figure 1. Purchases and cash disbursement flow of data

2.1.2. Payroll System

The Bell Studio Payroll system enables the company to make accurate and timely

payments for its employees. Various operations include the input of time card data,

generating payment registers, processing disbursement vouchers and updating the general

ledger which is associated with general expenses such as payment of employees salaries. The

data flow diagram show below helps describe this process.

2.2. System Flowchart

2.2.1. Purchases System

Purchases system flowchart describes the execution path of acquisition of stock

within Bell Studio. The purchases system deals with various activities that aid in ordering,

receiving and paying of goods. These activities include other internal processes such as

selection of vendors, inspection of goods, and reconciliation of purchase orders (PO) with

Figure 2. Payroll system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A

Monitor

Inventory Levels

Valid Vendors

File

Select Vendor

Prepare

Purchasing

Order (PO)Purchasing

order

Purchase

Order Files

B

Packing slip

Prepare

Receiving

Report

Receiving

Report

Update Inventory

Ledger

Inventory

Ledger file

Reconcile

packing slip

and PO

File

Bell Studio Systems 7

packing slips provided by vendors. Further, down the path, generation of receiving report and

updating the inventory ledger takes place. The diagram below helps represent this process.

Figure 3. Purchase System Process

Monitor

Inventory Levels

Valid Vendors

File

Select Vendor

Prepare

Purchasing

Order (PO)Purchasing

order

Purchase

Order Files

B

Packing slip

Prepare

Receiving

Report

Receiving

Report

Update Inventory

Ledger

Inventory

Ledger file

Reconcile

packing slip

and PO

File

Bell Studio Systems 7

packing slips provided by vendors. Further, down the path, generation of receiving report and

updating the inventory ledger takes place. The diagram below helps represent this process.

Figure 3. Purchase System Process

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A

Process Check

PO

Invoice

Receiving

Report

Update Check

Register

Check

Register File

Update Account

Payable

Cash Payable

Ledger File

File

Bell Studio Systems 8

2.2.2. Cash Disbursement System

The cash disbursement system allows the company to make payments for goods received or

services rendered. Therefore understanding the working of the system is crucial. The following

diagram shows the cash disbursement flowchart.

Figure 4. Cash Disbursement Process

2.2.3. Payroll System Flowchart

The Bell Studio payroll system enables companies to calculate employees earnings

based on hours worked. Description of the system using flowchart enable use to understand

Process Check

PO

Invoice

Receiving

Report

Update Check

Register

Check

Register File

Update Account

Payable

Cash Payable

Ledger File

File

Bell Studio Systems 8

2.2.2. Cash Disbursement System

The cash disbursement system allows the company to make payments for goods received or

services rendered. Therefore understanding the working of the system is crucial. The following

diagram shows the cash disbursement flowchart.

Figure 4. Cash Disbursement Process

2.2.3. Payroll System Flowchart

The Bell Studio payroll system enables companies to calculate employees earnings

based on hours worked. Description of the system using flowchart enable use to understand

A

Input Hours Worked

Employees

Records

B

Prepare

Disbursement

Voucher

Update General

Ledger

General

Ledger File

File

Payroll

Registers

Bell Studio Systems 9

the process of handling employees’ remuneration within the company. The following system

flowchart enables us to understand the payroll system for Bell Studio Inc.

Figure 5. Payroll system process

3.0. Internal Control Weaknesses and Associated Risks

Internal control are the systematic processes that exists within a company to ensure

effectiveness and reliability of operations. These processes exist to prevent the occurrence of

events that may jeopardize the integrity of the company’s finances. For this reason, the

computer systems used are supposed to ensure this rules are observed. Closer analysis of the

Input Hours Worked

Employees

Records

B

Prepare

Disbursement

Voucher

Update General

Ledger

General

Ledger File

File

Payroll

Registers

Bell Studio Systems 9

the process of handling employees’ remuneration within the company. The following system

flowchart enables us to understand the payroll system for Bell Studio Inc.

Figure 5. Payroll system process

3.0. Internal Control Weaknesses and Associated Risks

Internal control are the systematic processes that exists within a company to ensure

effectiveness and reliability of operations. These processes exist to prevent the occurrence of

events that may jeopardize the integrity of the company’s finances. For this reason, the

computer systems used are supposed to ensure this rules are observed. Closer analysis of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bell Studio Systems 10

Bell studio system reveals that there exists various internal control weaknesses in various

subsystems.

3.1. Purchases System

Purchases and disbursement subsystem exhibits various weaknesses that pose threats

to the system.

3.1.1. Lack of Authorization

The purchases system lacks a means of authorizing the purchase clerk’s activities. For

this reason, the purchase orders created by the purchasing clerk are able to advance to the

next step without being authorized by the department’s manager or supervisor. The clerk is

able to create purchase orders and print them immediately.

The lack of authorization exposes the system to the possibility of creation of

unnecessary orders. Additionally, this puts the company at the risk of acquiring goods not

related to the operations of the company. In order to control this behavior, the company

should implement the system such that all orders created by the purchases clerk undergo

through an approval process by the manager. This can be achieved by having the manager log

in to the system and manually approve the orders before the clerk is allowed to print them.

3.1.2. Lack of a Defined Procurement process

The purchases system lack clearly defined procurement process. This leads to the

situation where orders are placed without checking the prevailing prices of goods. The

purchasing clerk checks the goods and places an order without investigating the prices of

good being procured. Additionally, the suppliers are not vetted on their ability to deliver the

particular goods in required form at the current moment.

Lack of a defined procurement process exposes the company to the risk of

exaggeration of prices of goods. This would lead to the company paying higher for prices of

goods. In addition, the company would fail to take advantage of offers and mass discounts

that are available during purchases. This would lead to the company losing money

Bell studio system reveals that there exists various internal control weaknesses in various

subsystems.

3.1. Purchases System

Purchases and disbursement subsystem exhibits various weaknesses that pose threats

to the system.

3.1.1. Lack of Authorization

The purchases system lacks a means of authorizing the purchase clerk’s activities. For

this reason, the purchase orders created by the purchasing clerk are able to advance to the

next step without being authorized by the department’s manager or supervisor. The clerk is

able to create purchase orders and print them immediately.

The lack of authorization exposes the system to the possibility of creation of

unnecessary orders. Additionally, this puts the company at the risk of acquiring goods not

related to the operations of the company. In order to control this behavior, the company

should implement the system such that all orders created by the purchases clerk undergo

through an approval process by the manager. This can be achieved by having the manager log

in to the system and manually approve the orders before the clerk is allowed to print them.

3.1.2. Lack of a Defined Procurement process

The purchases system lack clearly defined procurement process. This leads to the

situation where orders are placed without checking the prevailing prices of goods. The

purchasing clerk checks the goods and places an order without investigating the prices of

good being procured. Additionally, the suppliers are not vetted on their ability to deliver the

particular goods in required form at the current moment.

Lack of a defined procurement process exposes the company to the risk of

exaggeration of prices of goods. This would lead to the company paying higher for prices of

goods. In addition, the company would fail to take advantage of offers and mass discounts

that are available during purchases. This would lead to the company losing money

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bell Studio Systems 11

unnecessarily. The recommendation for this problem is that the purchases clerk should only

deal with identifying the goods that require to be acquired and then another person carries on

with the process. The person charged with this process should be able to check prices and

discounts available. The current system has an order placed before a procurement process is

carried out. Placing an order before procurement is a major contributor to purchases fraud

(Murray, 2014). This exposes the company to potential of fraud through collusion involving

the purchasing clerk and suppliers.

3.1.3. Poor Assignment of Tasks

In the procurement process, the purchases officer is responsible of making orders and

selecting suppliers. The purchasing officer has the power to determine which goods are to be

bought. Similarly, the purchasing officer has the power to determine which supplier delivers

the goods. This gives him or her direct control in the complete purchasing process.

Having one person execute more than one task related to supply of goods creates a

room for fraud. This is because suppliers could influence purchasing officer into selecting

them or ordering goods that they supply. This could be in done with the promise of kickbacks

and other favors. Such as process should be carried out by various people to eliminate the

possibility of collusion. One person could select the goods to be ordered while another person

could be charged with the process of selecting the suppliers.

3.2. Cash Disbursement System

3.2.1. Lack of oversight

In the process of cash disbursement, there lacks the process of checking the

correctness and accuracy of cheques written. There is no officer who verifies that the cheques

written by the cash disbursement clerk is backed up by an expenditure. Additionally, there is

no other document related to the expense being paid for accompanies the cheque. The cash

disbursement clerk just creates a cheque and sends it for signing without any proof of

transaction.

unnecessarily. The recommendation for this problem is that the purchases clerk should only

deal with identifying the goods that require to be acquired and then another person carries on

with the process. The person charged with this process should be able to check prices and

discounts available. The current system has an order placed before a procurement process is

carried out. Placing an order before procurement is a major contributor to purchases fraud

(Murray, 2014). This exposes the company to potential of fraud through collusion involving

the purchasing clerk and suppliers.

3.1.3. Poor Assignment of Tasks

In the procurement process, the purchases officer is responsible of making orders and

selecting suppliers. The purchasing officer has the power to determine which goods are to be

bought. Similarly, the purchasing officer has the power to determine which supplier delivers

the goods. This gives him or her direct control in the complete purchasing process.

Having one person execute more than one task related to supply of goods creates a

room for fraud. This is because suppliers could influence purchasing officer into selecting

them or ordering goods that they supply. This could be in done with the promise of kickbacks

and other favors. Such as process should be carried out by various people to eliminate the

possibility of collusion. One person could select the goods to be ordered while another person

could be charged with the process of selecting the suppliers.

3.2. Cash Disbursement System

3.2.1. Lack of oversight

In the process of cash disbursement, there lacks the process of checking the

correctness and accuracy of cheques written. There is no officer who verifies that the cheques

written by the cash disbursement clerk is backed up by an expenditure. Additionally, there is

no other document related to the expense being paid for accompanies the cheque. The cash

disbursement clerk just creates a cheque and sends it for signing without any proof of

transaction.

Bell Studio Systems 12

Lack of oversight exposes the disbursement procedure to the risk of fraud. This is

because the cash disbursement clerk could potentially write a fictitious cheque and send it for

signing without anyone noticing the potential fraud. Additionally, the clerk could also be able

to write a cheque for higher amount than the actual amount being paid. This creates a

loophole for financial mismanagement and fraud. The best method to address this would be

to have a cheque prepared and accompanied by documentation of the payment. The treasurer

would then verify the cheque against the transactions before signing the cheque. This would

reduce the possibility of fraud or errors being made by the disbursement clerk.

3.2.2. Lack of Payment Review process

The cash disbursement system lacks the payment review process. There does not exist

any process or department to review outgoing payments. All transactions go ahead without

any review. The cash disbursement clerk writes a cheque and the treasurer signs it. This

allows the payment to take place without the input of any other person within the company.

The managers or directors are not required to authorize or review payments. For this reason,

the disbursement clerk and the treasurer could collude to have payments take place

fraudulently. This exposes the system to the risk of fraud. A proper payment process would

require more people to authorize the payment to safeguard against fraud. However, the

system fails to have such controls therefore exposing it to the risk of fraud.

3.3. Payroll System

The payroll system contributes to one of the biggest expenses in most of the

companies. Ability to secure the payroll system would reduce the risk of losing a lot of

money through fraud and manipulation. However, the Bell Studio payroll system has been

identified to contain some internal control weaknesses. This create an environment where

various people are able to exploit the system for their own benefit.

Lack of oversight exposes the disbursement procedure to the risk of fraud. This is

because the cash disbursement clerk could potentially write a fictitious cheque and send it for

signing without anyone noticing the potential fraud. Additionally, the clerk could also be able

to write a cheque for higher amount than the actual amount being paid. This creates a

loophole for financial mismanagement and fraud. The best method to address this would be

to have a cheque prepared and accompanied by documentation of the payment. The treasurer

would then verify the cheque against the transactions before signing the cheque. This would

reduce the possibility of fraud or errors being made by the disbursement clerk.

3.2.2. Lack of Payment Review process

The cash disbursement system lacks the payment review process. There does not exist

any process or department to review outgoing payments. All transactions go ahead without

any review. The cash disbursement clerk writes a cheque and the treasurer signs it. This

allows the payment to take place without the input of any other person within the company.

The managers or directors are not required to authorize or review payments. For this reason,

the disbursement clerk and the treasurer could collude to have payments take place

fraudulently. This exposes the system to the risk of fraud. A proper payment process would

require more people to authorize the payment to safeguard against fraud. However, the

system fails to have such controls therefore exposing it to the risk of fraud.

3.3. Payroll System

The payroll system contributes to one of the biggest expenses in most of the

companies. Ability to secure the payroll system would reduce the risk of losing a lot of

money through fraud and manipulation. However, the Bell Studio payroll system has been

identified to contain some internal control weaknesses. This create an environment where

various people are able to exploit the system for their own benefit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.