ACC200: Evaluating Costing Methods and Ethical Issues at Beztec

VerifiedAdded on 2023/06/07

|10

|2394

|433

Report

AI Summary

This report analyzes Beztec Limited's costing methods, particularly comparing traditional costing with activity-based costing (ABC). It calculates cost driver rates and the cost of each printer model (Lexon and Protox) under ABC, followed by a profitability analysis determining gross profit and gross profit percentage per unit. The report addresses the ethical dilemma faced by the management accountant regarding altering ABC results, referencing the APES 110 Code of Ethics, and suggests recommendations. Finally, it outlines techniques for disposing of over or under-applied overhead costs within the ABC system. Desklib provides a platform for students to access similar solved assignments and past papers for their studies.

Introduction to Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The present report is developed for providing an analysis of the case study of Beztec

Limited that is involved in manufacturing of two models of printers, that is, Lexon and Protox.

The company is initially following the traditional method of costing and is facing issues in

realizing profits from its product line of Lexon. The company has thus decided to introduce a

new product line, Protox, that they believe to generate much higher profit as compared to that of

Lexon. The management accountant, Smith, has advised the management for adopting the use of

ABC (Activity-based Costing) system so that it can accurate measure both direct and indirect

cost involved in production. However, ABC method has depicted that its new product line also

does not seem to be profitable and thus Kay, CEO of the company has advised Smith to alter the

results produced. In this context, the report has discussed the benefits of using the method of

accurate product costing over traditional method of costing to provide accurate results that

facilitates in taking correct decision. Also, it has provided a calculation regarding the cost driver

rates for various activities under the ABC system and the cost of each model of printer of

company under the activity based costing. The report has also conducted a profitability analysis

by calculating the gross profit and gross profit percentage per unit for both model as per the ABC

system. In addition to this, it has also provided recommendations to Smith for resolving the

ethical dilemma faced of altering the results derived with the use of ABC systems. At last, it has

also sated the technique to dispose the amount of over or under applied overhead costs with the

use of system of activity based costing.

Answer 1:

Product costing can be regarded as the process of allocating costs to the inventory and

production based on expenditure incurred during these processes while manufacturing of a

product. There is need for accurate estimation of the product cost to take important decisions for

improving the profitability position of a company by reduction in the operational costs. The

major goals that can be achieved by estimation of product costs are developing strategies for

reducing material cost, labor cost or the subcontractor cost. The major benefit of determination

of accurate product costing is achieving accuracy for keeping a track of operational expenses.

The use of product costing helps in assigning the cost to the value created by them for the

business. It also proves to be very useful in developing budgets by determination of overall

2

The present report is developed for providing an analysis of the case study of Beztec

Limited that is involved in manufacturing of two models of printers, that is, Lexon and Protox.

The company is initially following the traditional method of costing and is facing issues in

realizing profits from its product line of Lexon. The company has thus decided to introduce a

new product line, Protox, that they believe to generate much higher profit as compared to that of

Lexon. The management accountant, Smith, has advised the management for adopting the use of

ABC (Activity-based Costing) system so that it can accurate measure both direct and indirect

cost involved in production. However, ABC method has depicted that its new product line also

does not seem to be profitable and thus Kay, CEO of the company has advised Smith to alter the

results produced. In this context, the report has discussed the benefits of using the method of

accurate product costing over traditional method of costing to provide accurate results that

facilitates in taking correct decision. Also, it has provided a calculation regarding the cost driver

rates for various activities under the ABC system and the cost of each model of printer of

company under the activity based costing. The report has also conducted a profitability analysis

by calculating the gross profit and gross profit percentage per unit for both model as per the ABC

system. In addition to this, it has also provided recommendations to Smith for resolving the

ethical dilemma faced of altering the results derived with the use of ABC systems. At last, it has

also sated the technique to dispose the amount of over or under applied overhead costs with the

use of system of activity based costing.

Answer 1:

Product costing can be regarded as the process of allocating costs to the inventory and

production based on expenditure incurred during these processes while manufacturing of a

product. There is need for accurate estimation of the product cost to take important decisions for

improving the profitability position of a company by reduction in the operational costs. The

major goals that can be achieved by estimation of product costs are developing strategies for

reducing material cost, labor cost or the subcontractor cost. The major benefit of determination

of accurate product costing is achieving accuracy for keeping a track of operational expenses.

The use of product costing helps in assigning the cost to the value created by them for the

business. It also proves to be very useful in developing budgets by determination of overall

2

expenses that will be involved in completion of a project. The development of budget helps in

assessing whether the various stages of a project are meeting the cost expectations and

identifying the variances easily. This helps in keeping a track of project cost and resolving the

costing issues in advance for ensuring successful completion of a project. The lack of accurate

product costing can lead to difficulty in analyzing the cash flows and determining the success of

a project (Maingi, 2013).

The determination of accurate product cost is very useful in making important decision

involving return realized on capital invested and estimating the profit to be achieved from an

action. For example, business managers adopt the use of absorption costing that involves

segregating the overall cost involved in production into different products manufactured.

Therefore, it can be said that there is high importance of estimating the accurate cost for taking

significant decisions in developing a new product line using methods for reduction in the

operational costs. It is required for controlling the expenses in current production process,

preventing the overruns of future jobs and developing a cost history for estimating the success of

a future product or service planning to be launched (Hansen, 2007).

The business managers at present are emphasizing on adopting the use of accurate

product methods as compared to the traditional method of costing. For example, management of

Beztec has adopted the sue of activity based costing for determination of overhead costs for its

product lines. The method of activity based costing helps in determination the accurate cost

incurred in developing a product by identifying the overall activities involved in production and

then allocating the cost based on actual consumption. The use of accurate product costing is

becoming important for business entities due to problems associated with the traditional costing

system that has been used by Beztec previously. The traditional cost methods do not seem to be

adequate in estimating the overhead costs involved in manufacturing of a product as it allocates

the cost based on volume such as total products manufactured, direct labor hours consumed or

number of machine hours involved. Therefore, the allocation of indirect costs that are not

incurred due to volume is not possible under the method of traditional costing system. This

weakness of the traditional costing system is causing the business entities such as Beztec to

adopt the use of accurate product costing methods (Emblemsvåg and Bras, 2012).

Answer 2:

3

assessing whether the various stages of a project are meeting the cost expectations and

identifying the variances easily. This helps in keeping a track of project cost and resolving the

costing issues in advance for ensuring successful completion of a project. The lack of accurate

product costing can lead to difficulty in analyzing the cash flows and determining the success of

a project (Maingi, 2013).

The determination of accurate product cost is very useful in making important decision

involving return realized on capital invested and estimating the profit to be achieved from an

action. For example, business managers adopt the use of absorption costing that involves

segregating the overall cost involved in production into different products manufactured.

Therefore, it can be said that there is high importance of estimating the accurate cost for taking

significant decisions in developing a new product line using methods for reduction in the

operational costs. It is required for controlling the expenses in current production process,

preventing the overruns of future jobs and developing a cost history for estimating the success of

a future product or service planning to be launched (Hansen, 2007).

The business managers at present are emphasizing on adopting the use of accurate

product methods as compared to the traditional method of costing. For example, management of

Beztec has adopted the sue of activity based costing for determination of overhead costs for its

product lines. The method of activity based costing helps in determination the accurate cost

incurred in developing a product by identifying the overall activities involved in production and

then allocating the cost based on actual consumption. The use of accurate product costing is

becoming important for business entities due to problems associated with the traditional costing

system that has been used by Beztec previously. The traditional cost methods do not seem to be

adequate in estimating the overhead costs involved in manufacturing of a product as it allocates

the cost based on volume such as total products manufactured, direct labor hours consumed or

number of machine hours involved. Therefore, the allocation of indirect costs that are not

incurred due to volume is not possible under the method of traditional costing system. This

weakness of the traditional costing system is causing the business entities such as Beztec to

adopt the use of accurate product costing methods (Emblemsvåg and Bras, 2012).

Answer 2:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

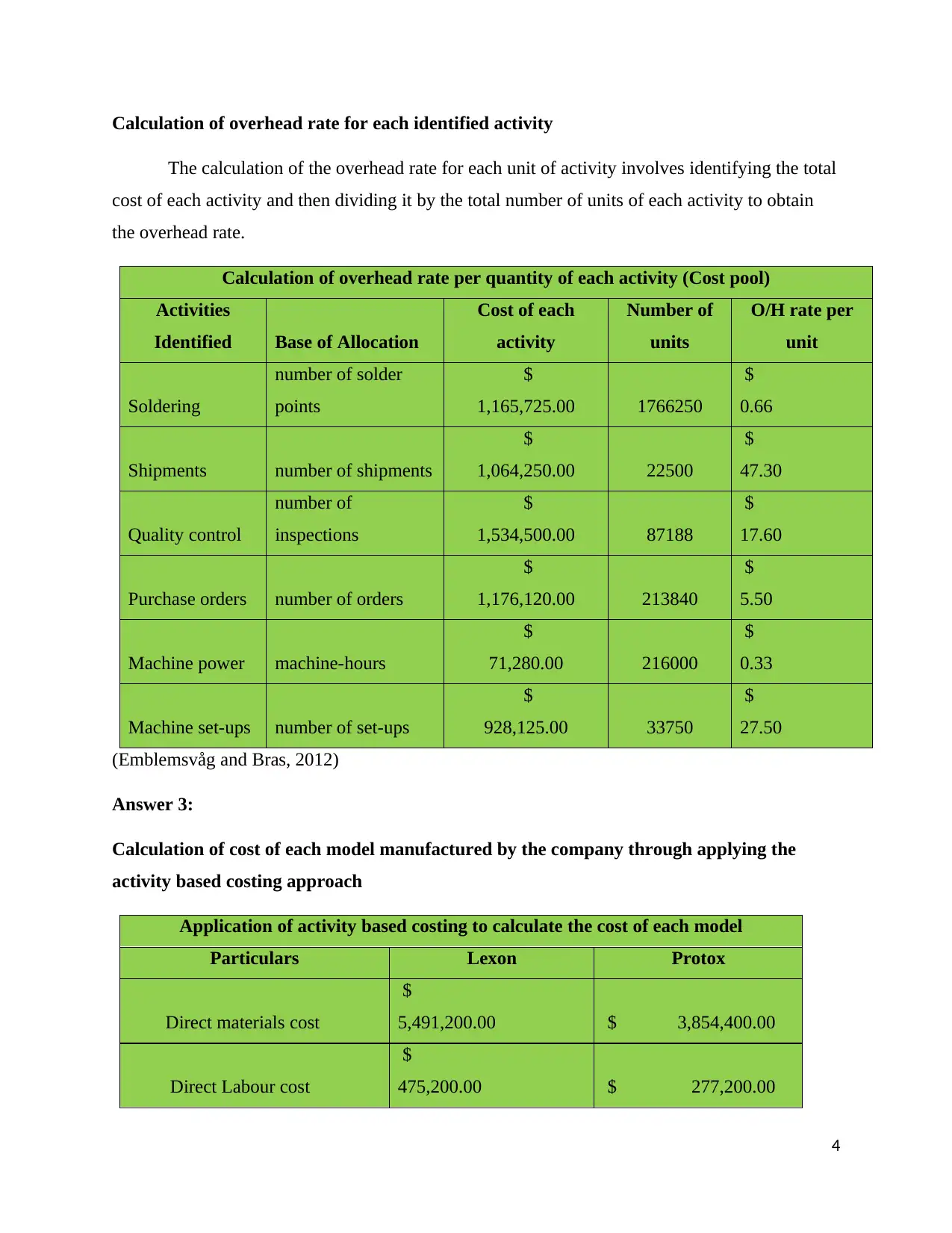

Calculation of overhead rate for each identified activity

The calculation of the overhead rate for each unit of activity involves identifying the total

cost of each activity and then dividing it by the total number of units of each activity to obtain

the overhead rate.

Calculation of overhead rate per quantity of each activity (Cost pool)

Activities

Identified Base of Allocation

Cost of each

activity

Number of

units

O/H rate per

unit

Soldering

number of solder

points

$

1,165,725.00 1766250

$

0.66

Shipments number of shipments

$

1,064,250.00 22500

$

47.30

Quality control

number of

inspections

$

1,534,500.00 87188

$

17.60

Purchase orders number of orders

$

1,176,120.00 213840

$

5.50

Machine power machine-hours

$

71,280.00 216000

$

0.33

Machine set-ups number of set-ups

$

928,125.00 33750

$

27.50

(Emblemsvåg and Bras, 2012)

Answer 3:

Calculation of cost of each model manufactured by the company through applying the

activity based costing approach

Application of activity based costing to calculate the cost of each model

Particulars Lexon Protox

Direct materials cost

$

5,491,200.00 $ 3,854,400.00

Direct Labour cost

$

475,200.00 $ 277,200.00

4

The calculation of the overhead rate for each unit of activity involves identifying the total

cost of each activity and then dividing it by the total number of units of each activity to obtain

the overhead rate.

Calculation of overhead rate per quantity of each activity (Cost pool)

Activities

Identified Base of Allocation

Cost of each

activity

Number of

units

O/H rate per

unit

Soldering

number of solder

points

$

1,165,725.00 1766250

$

0.66

Shipments number of shipments

$

1,064,250.00 22500

$

47.30

Quality control

number of

inspections

$

1,534,500.00 87188

$

17.60

Purchase orders number of orders

$

1,176,120.00 213840

$

5.50

Machine power machine-hours

$

71,280.00 216000

$

0.33

Machine set-ups number of set-ups

$

928,125.00 33750

$

27.50

(Emblemsvåg and Bras, 2012)

Answer 3:

Calculation of cost of each model manufactured by the company through applying the

activity based costing approach

Application of activity based costing to calculate the cost of each model

Particulars Lexon Protox

Direct materials cost

$

5,491,200.00 $ 3,854,400.00

Direct Labour cost

$

475,200.00 $ 277,200.00

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

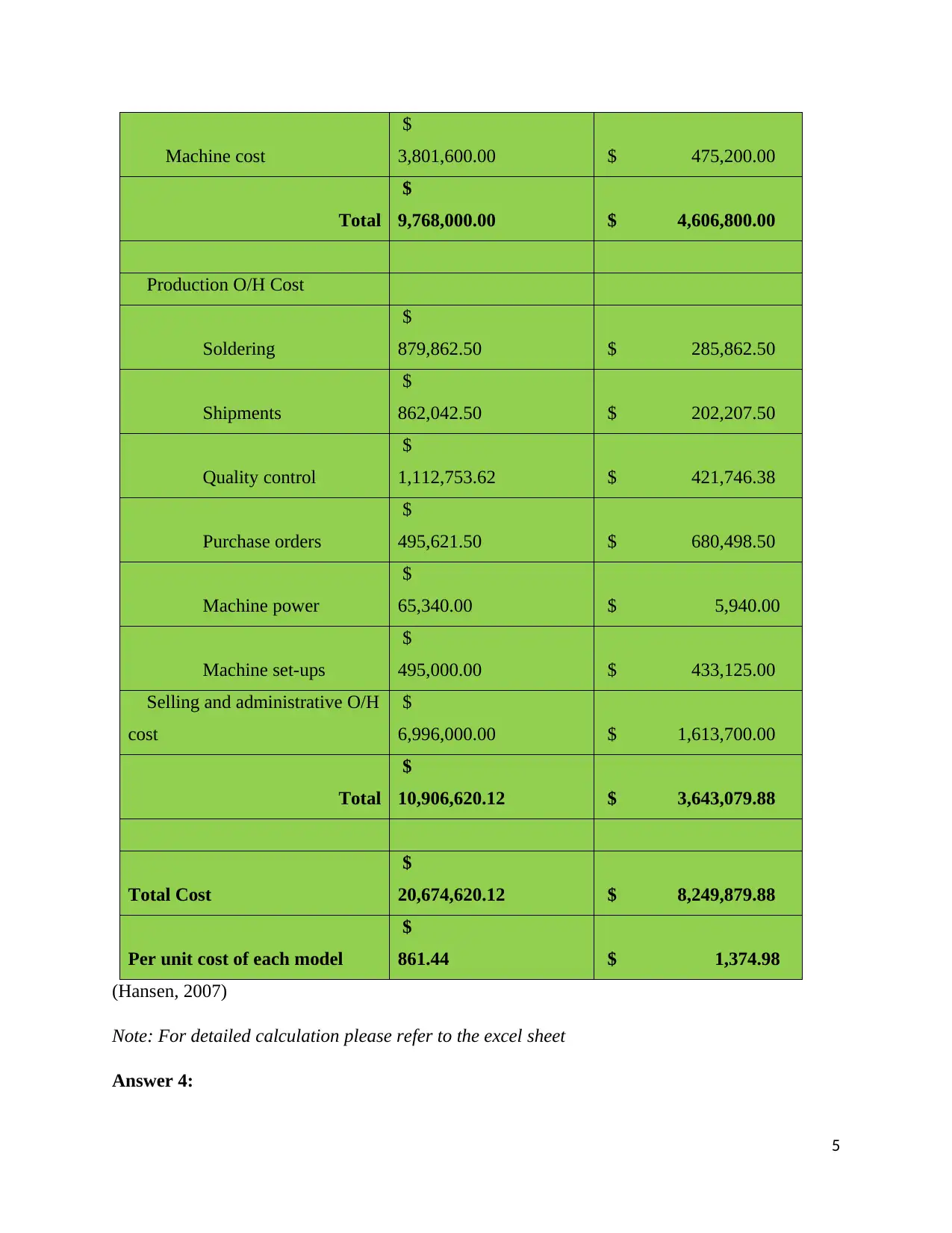

Machine cost

$

3,801,600.00 $ 475,200.00

Total

$

9,768,000.00 $ 4,606,800.00

Production O/H Cost

Soldering

$

879,862.50 $ 285,862.50

Shipments

$

862,042.50 $ 202,207.50

Quality control

$

1,112,753.62 $ 421,746.38

Purchase orders

$

495,621.50 $ 680,498.50

Machine power

$

65,340.00 $ 5,940.00

Machine set-ups

$

495,000.00 $ 433,125.00

Selling and administrative O/H

cost

$

6,996,000.00 $ 1,613,700.00

Total

$

10,906,620.12 $ 3,643,079.88

Total Cost

$

20,674,620.12 $ 8,249,879.88

Per unit cost of each model

$

861.44 $ 1,374.98

(Hansen, 2007)

Note: For detailed calculation please refer to the excel sheet

Answer 4:

5

$

3,801,600.00 $ 475,200.00

Total

$

9,768,000.00 $ 4,606,800.00

Production O/H Cost

Soldering

$

879,862.50 $ 285,862.50

Shipments

$

862,042.50 $ 202,207.50

Quality control

$

1,112,753.62 $ 421,746.38

Purchase orders

$

495,621.50 $ 680,498.50

Machine power

$

65,340.00 $ 5,940.00

Machine set-ups

$

495,000.00 $ 433,125.00

Selling and administrative O/H

cost

$

6,996,000.00 $ 1,613,700.00

Total

$

10,906,620.12 $ 3,643,079.88

Total Cost

$

20,674,620.12 $ 8,249,879.88

Per unit cost of each model

$

861.44 $ 1,374.98

(Hansen, 2007)

Note: For detailed calculation please refer to the excel sheet

Answer 4:

5

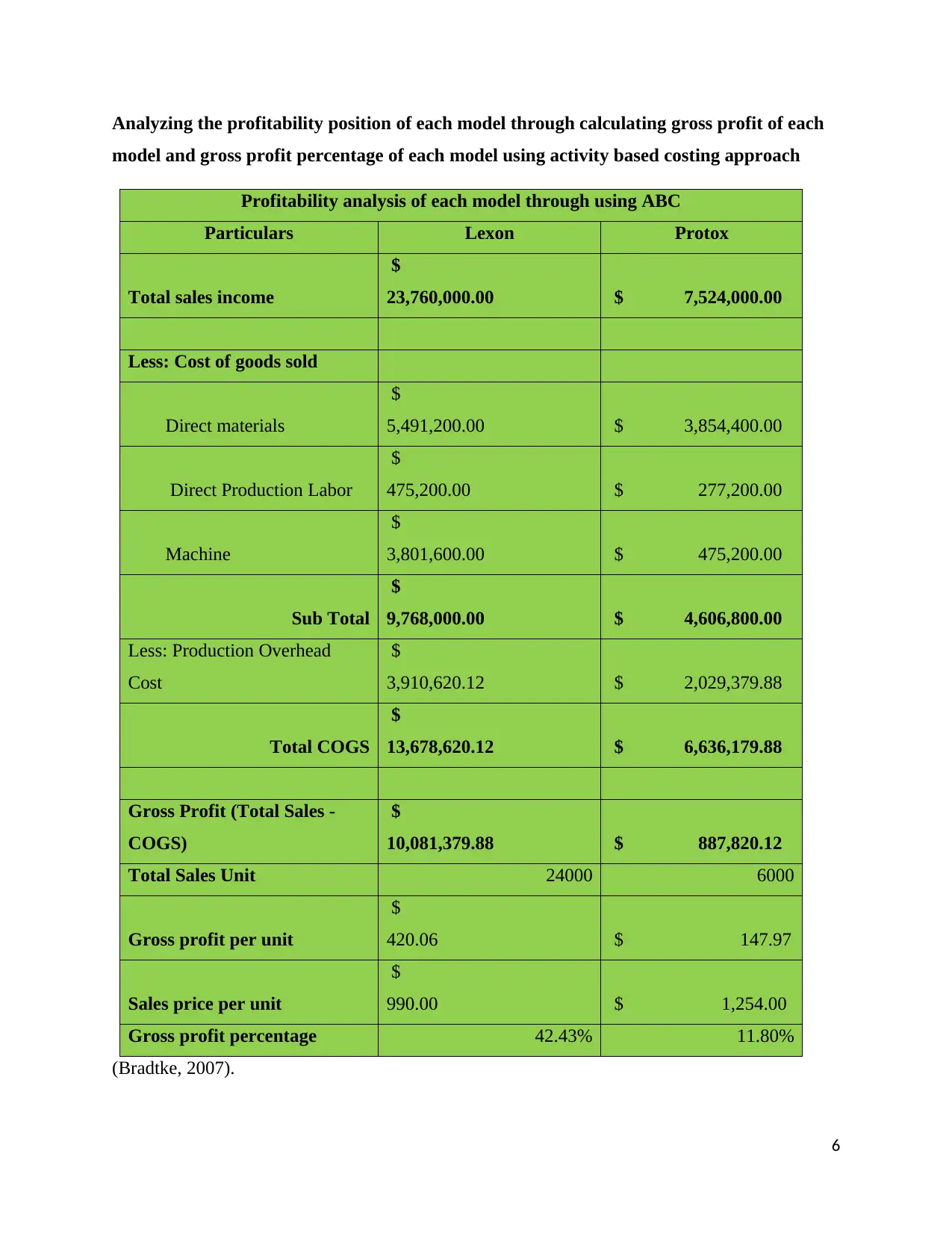

Analyzing the profitability position of each model through calculating gross profit of each

model and gross profit percentage of each model using activity based costing approach

Profitability analysis of each model through using ABC

Particulars Lexon Protox

Total sales income

$

23,760,000.00 $ 7,524,000.00

Less: Cost of goods sold

Direct materials

$

5,491,200.00 $ 3,854,400.00

Direct Production Labor

$

475,200.00 $ 277,200.00

Machine

$

3,801,600.00 $ 475,200.00

Sub Total

$

9,768,000.00 $ 4,606,800.00

Less: Production Overhead

Cost

$

3,910,620.12 $ 2,029,379.88

Total COGS

$

13,678,620.12 $ 6,636,179.88

Gross Profit (Total Sales -

COGS)

$

10,081,379.88 $ 887,820.12

Total Sales Unit 24000 6000

Gross profit per unit

$

420.06 $ 147.97

Sales price per unit

$

990.00 $ 1,254.00

Gross profit percentage 42.43% 11.80%

(Bradtke, 2007).

6

model and gross profit percentage of each model using activity based costing approach

Profitability analysis of each model through using ABC

Particulars Lexon Protox

Total sales income

$

23,760,000.00 $ 7,524,000.00

Less: Cost of goods sold

Direct materials

$

5,491,200.00 $ 3,854,400.00

Direct Production Labor

$

475,200.00 $ 277,200.00

Machine

$

3,801,600.00 $ 475,200.00

Sub Total

$

9,768,000.00 $ 4,606,800.00

Less: Production Overhead

Cost

$

3,910,620.12 $ 2,029,379.88

Total COGS

$

13,678,620.12 $ 6,636,179.88

Gross Profit (Total Sales -

COGS)

$

10,081,379.88 $ 887,820.12

Total Sales Unit 24000 6000

Gross profit per unit

$

420.06 $ 147.97

Sales price per unit

$

990.00 $ 1,254.00

Gross profit percentage 42.43% 11.80%

(Bradtke, 2007).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer 5:

Smith, the management accountant of Beztec, has advocated the use of activity-based

costing method for gathering the information related to overhead costs involved in each of its

product line of Protox and Lexon. This has been done as the use of traditional method of costing

is not proving to be adequate for identifying the overhead costs. As such, the initial product line

of Beztec, lexon, has not generated profitable results due to inadequate identification of the

indirect costs with the sue of traditional costing method. As such, Smith has emphasized on the

use of ABC system for identifying the overhead costs so that its new product line Proton

becomes profitable. The use of ABC system has depicted that the new product line of Beztec,

Protox, is also not profitable. Smith has depicted these results to Steven Kay, the CEO of the

company, and he has advised Smith to alter the results derived with the use of ABC system. This

is because Smith believes they cannot show these results to the headquarters as initially the

product line of Lexon was not profitable and now their new product line Protox has also depicted

negative costing results.

However, Smith has re-checked the results derived with the use of ABC system and have

found them to be accurate. As such, Smith is facing ethical dilemma for deciding the ways she

should respond to the suggestion of Kay as it would be unethical on her part to alter the results

derived with the use of ABC system according to APES 110 Code of Ethics. Accounting

Professional & Ethical Standards Board Limited (APESB) has stated that it’s the responsibility

of the accountancy professional to act in the direction of maximizing the public interest. As per

the code, an accounting professional need to give the professional judgment without any biasness

and should provide a fair view of the financial performance of an entity to its stakeholders. It is

the responsibility of accounting professional to apply the safeguards for eliminating the threats to

an acceptable level. Therefore, as per the code of ethics Smith has the responsibility of

presenting true and fair view of the financial results to the headquarters so that they can take

accurate decisions for its future growth and development. The manipulation of costing results

would be unethical on the part of Smith as it could lead to misleading the Board about its actual

financial position as well as can have a negative impact on its future growth prospects. As such,

it is advised to Smith to develop an understanding to Kay about the future implications of such

an alteration caused in the results produced by ABC system. The importance of depicting true

7

Smith, the management accountant of Beztec, has advocated the use of activity-based

costing method for gathering the information related to overhead costs involved in each of its

product line of Protox and Lexon. This has been done as the use of traditional method of costing

is not proving to be adequate for identifying the overhead costs. As such, the initial product line

of Beztec, lexon, has not generated profitable results due to inadequate identification of the

indirect costs with the sue of traditional costing method. As such, Smith has emphasized on the

use of ABC system for identifying the overhead costs so that its new product line Proton

becomes profitable. The use of ABC system has depicted that the new product line of Beztec,

Protox, is also not profitable. Smith has depicted these results to Steven Kay, the CEO of the

company, and he has advised Smith to alter the results derived with the use of ABC system. This

is because Smith believes they cannot show these results to the headquarters as initially the

product line of Lexon was not profitable and now their new product line Protox has also depicted

negative costing results.

However, Smith has re-checked the results derived with the use of ABC system and have

found them to be accurate. As such, Smith is facing ethical dilemma for deciding the ways she

should respond to the suggestion of Kay as it would be unethical on her part to alter the results

derived with the use of ABC system according to APES 110 Code of Ethics. Accounting

Professional & Ethical Standards Board Limited (APESB) has stated that it’s the responsibility

of the accountancy professional to act in the direction of maximizing the public interest. As per

the code, an accounting professional need to give the professional judgment without any biasness

and should provide a fair view of the financial performance of an entity to its stakeholders. It is

the responsibility of accounting professional to apply the safeguards for eliminating the threats to

an acceptable level. Therefore, as per the code of ethics Smith has the responsibility of

presenting true and fair view of the financial results to the headquarters so that they can take

accurate decisions for its future growth and development. The manipulation of costing results

would be unethical on the part of Smith as it could lead to misleading the Board about its actual

financial position as well as can have a negative impact on its future growth prospects. As such,

it is advised to Smith to develop an understanding to Kay about the future implications of such

an alteration caused in the results produced by ABC system. The importance of depicting true

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

result before the headquarters should be explained to Kay for taking significant decisions for

reducing the operating costs to make Protox profitable (APES 110 Code of Ethics for

Professional Accountants, 2010).

Answer 6:

The use of a predetermined overhead rate can result in over or under allocation of

overhead costs. This is because of the occurrence of variances due to difference between the

actual overhead incurred and the estimated overhead cost calculated based on a predetermined

overhead rate incurred during the manufacturing process. The predetermined overhead rate is

calculated based on estimated hours of labor or machine. However, the rate determined varies as

the actual hours of labor or machine varies at the end of production period. Therefore, such

variances can result in causing overhead or under applied overhead (CCH Australia Limited,

2009). The three ways that can be used for disposing the amount of over or under applied

overhead costs are as follows:

Assigning the over or under applied overhead cost to work in progress, finished goods or

cost of goods sold

Transferring the complete cost in over or under applied overhead to the cost of goods

sold

Developing distinct account for over or under applied overhead cost and then transferring

it afterwards (Bhimani, 2006).

Conclusion

It can be stated from the analysis of the case study issues that has been carried out in this

report that determination of accurate product costs is of utmost significant for sustaining the

future growth prospects of a company. This is because it facilitates in taking accurate decision

relating to developing strategies for controlling and monitoring the overhead costs that is not

determined with the sue of traditional costing method. Beztec has also adopted the use of ABC

model for estimating the overhead cost of its new product line of Protox that is not possible with

the use of traditional method of costing. The differences resulting between the overhead cost

determined and that incurred can be used to calculate the overhead cost. It is also recommended

based on overall analysis of the case study issues that accounting professionals must adopt the

8

reducing the operating costs to make Protox profitable (APES 110 Code of Ethics for

Professional Accountants, 2010).

Answer 6:

The use of a predetermined overhead rate can result in over or under allocation of

overhead costs. This is because of the occurrence of variances due to difference between the

actual overhead incurred and the estimated overhead cost calculated based on a predetermined

overhead rate incurred during the manufacturing process. The predetermined overhead rate is

calculated based on estimated hours of labor or machine. However, the rate determined varies as

the actual hours of labor or machine varies at the end of production period. Therefore, such

variances can result in causing overhead or under applied overhead (CCH Australia Limited,

2009). The three ways that can be used for disposing the amount of over or under applied

overhead costs are as follows:

Assigning the over or under applied overhead cost to work in progress, finished goods or

cost of goods sold

Transferring the complete cost in over or under applied overhead to the cost of goods

sold

Developing distinct account for over or under applied overhead cost and then transferring

it afterwards (Bhimani, 2006).

Conclusion

It can be stated from the analysis of the case study issues that has been carried out in this

report that determination of accurate product costs is of utmost significant for sustaining the

future growth prospects of a company. This is because it facilitates in taking accurate decision

relating to developing strategies for controlling and monitoring the overhead costs that is not

determined with the sue of traditional costing method. Beztec has also adopted the use of ABC

model for estimating the overhead cost of its new product line of Protox that is not possible with

the use of traditional method of costing. The differences resulting between the overhead cost

determined and that incurred can be used to calculate the overhead cost. It is also recommended

based on overall analysis of the case study issues that accounting professionals must adopt the

8

use of techniques of accurate product costing to depict the accurate results to the management so

that they can take effective decisions regarding the future growth strategies of a company. APES

110 code of ethics provides guidance to the accounting professionals for maintaining integrity,

honesty and transparency in developing financial results to protect the interest of the

stakeholders.

9

that they can take effective decisions regarding the future growth strategies of a company. APES

110 code of ethics provides guidance to the accounting professionals for maintaining integrity,

honesty and transparency in developing financial results to protect the interest of the

stakeholders.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

APES 110 Code of Ethics for Professional Accountants. 2010. [Online]. Available at:

https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf [Accessed on: 15

September 2018].

Bhimani, A. 2006. Contemporary Issues in Management Accounting. Oxford University Press.

Emblemsvåg, J. and Bras, B. 2012. Activity-Based Cost and Environmental Management: A

Different Approach to ISO 14000 Compliance. Springer Science & Business Media.

Maingi, J. 2013. Advantages & Disadvantages of activity based costing with reference to

economic value addition. GRIN Verlag.

Hansen, D. 2007. Cost Management: Accounting and Control. Cengage Learning.

Bradtke, D. 2007. Activity-Based-Costing. GRIN Verlag.

CCH Australia Limited. 2009. Australian Master Accountants Guide. CCH Australia Limited.

10

APES 110 Code of Ethics for Professional Accountants. 2010. [Online]. Available at:

https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf [Accessed on: 15

September 2018].

Bhimani, A. 2006. Contemporary Issues in Management Accounting. Oxford University Press.

Emblemsvåg, J. and Bras, B. 2012. Activity-Based Cost and Environmental Management: A

Different Approach to ISO 14000 Compliance. Springer Science & Business Media.

Maingi, J. 2013. Advantages & Disadvantages of activity based costing with reference to

economic value addition. GRIN Verlag.

Hansen, D. 2007. Cost Management: Accounting and Control. Cengage Learning.

Bradtke, D. 2007. Activity-Based-Costing. GRIN Verlag.

CCH Australia Limited. 2009. Australian Master Accountants Guide. CCH Australia Limited.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.