Differentiate between Long Futures hedge and Short Futures hedge

32 Pages3543 Words32 Views

Added on 2022-01-22

Differentiate between Long Futures hedge and Short Futures hedge

Added on 2022-01-22

ShareRelated Documents

BFW2751 - Derivatives 1

S1, 2021

Lecture Week 2

Hedging Strategies using Futures Contracts

Chapter 3 in text book

S1, 2021

Lecture Week 2

Hedging Strategies using Futures Contracts

Chapter 3 in text book

Lecture 2: Learning objectives

▪ Understand the concept of “hedging”.

▪ Differentiate between “Long Futures hedge” and “Short Futures hedge”.

▪ Be able to perform hedging strategies using Futures contracts

▪ Appreciate that real world hedge is typically “imperfect”, leading to the

need for an optimal hedge strategy.

3/16/2021 BFW2751 S2 2020 AP Jothee 2

▪ Understand the concept of “hedging”.

▪ Differentiate between “Long Futures hedge” and “Short Futures hedge”.

▪ Be able to perform hedging strategies using Futures contracts

▪ Appreciate that real world hedge is typically “imperfect”, leading to the

need for an optimal hedge strategy.

3/16/2021 BFW2751 S2 2020 AP Jothee 2

Learning structure

▪ Issues in hedging using futures

▪ Types of hedge

▪ Basis risk

▪ The optimal hedge ratio (OHR), optimal number of hedging contracts and

hedging effectiveness

3/16/2021 BFW2751 S2 2020 AP Jothee 3

▪ Issues in hedging using futures

▪ Types of hedge

▪ Basis risk

▪ The optimal hedge ratio (OHR), optimal number of hedging contracts and

hedging effectiveness

3/16/2021 BFW2751 S2 2020 AP Jothee 3

What is hedging ?

▪ Hedging is about reducing the volatility (risk) of future cash flows associated with

commitments in cash/physical market.

▪ Commitments in cash/physical market means existing positions in some instruments /

commodities or equities or planning to buy or sell any of these in the future time in physical

market.

▪ The concept is to take some position in derivative contracts that neutralizes the risk as much

as possible. (if you lose in cash market, you will gain in derivative market, and vis a vis)

▪ In most of the cases, hedging involves the use of some financial derivatives like Futures or

Options contracts.

▪ Hedgers identify the risk factor and take a position in a derivative such as to benefits from the

adverse movements in the underlying asset prices.

3/16/2021 BFW2751 S2 2020 AP Jothee 4

▪ Hedging is about reducing the volatility (risk) of future cash flows associated with

commitments in cash/physical market.

▪ Commitments in cash/physical market means existing positions in some instruments /

commodities or equities or planning to buy or sell any of these in the future time in physical

market.

▪ The concept is to take some position in derivative contracts that neutralizes the risk as much

as possible. (if you lose in cash market, you will gain in derivative market, and vis a vis)

▪ In most of the cases, hedging involves the use of some financial derivatives like Futures or

Options contracts.

▪ Hedgers identify the risk factor and take a position in a derivative such as to benefits from the

adverse movements in the underlying asset prices.

3/16/2021 BFW2751 S2 2020 AP Jothee 4

Examples of Hedging

Farmers want to lock-in the price they can sell their future crops. Producers of goods

will hedge their future product delivery prices by going into short hedge (i.e. to short sell

in Futures contracts to gain in the Futures market if their product / crop prices fall by the

time it could be delivered in the physical market.

Gold producers want to ensure the sale price they’ll get from their gold will not fall below

a certain level in the future supply.

Jewellery makers want to lock in the price of gold they’re going to buy as raw materials

for their business in future dates.

Importers of products wish to fix the price they pay for the next shipment.

A bank just sold a forward contract and wishes to hedge against that risk of its underlying

falling.

3/16/2021 BFW2751 S2 2020 AP Jothee 5

Farmers want to lock-in the price they can sell their future crops. Producers of goods

will hedge their future product delivery prices by going into short hedge (i.e. to short sell

in Futures contracts to gain in the Futures market if their product / crop prices fall by the

time it could be delivered in the physical market.

Gold producers want to ensure the sale price they’ll get from their gold will not fall below

a certain level in the future supply.

Jewellery makers want to lock in the price of gold they’re going to buy as raw materials

for their business in future dates.

Importers of products wish to fix the price they pay for the next shipment.

A bank just sold a forward contract and wishes to hedge against that risk of its underlying

falling.

3/16/2021 BFW2751 S2 2020 AP Jothee 5

Long & Short Futures hedges

▪ A Long Futures hedge is appropriate when you want to purchase an asset

in the future date and intend to neutralize the risk of increase in price of the

asset by taking a long position in the Futures market. (Long Futures hedge

when asset price may rise at future time).

▪ A Short Futures hedge is appropriate when you want to sell an asset in the

future date and intend to neutralize the risk of fall in price of the asset by

taking a short position in the Futures market. (Short Futures hedge when

asset price may fall in future time).

3/16/2021 BFW2751 S2 2020 AP Jothee 6

▪ A Long Futures hedge is appropriate when you want to purchase an asset

in the future date and intend to neutralize the risk of increase in price of the

asset by taking a long position in the Futures market. (Long Futures hedge

when asset price may rise at future time).

▪ A Short Futures hedge is appropriate when you want to sell an asset in the

future date and intend to neutralize the risk of fall in price of the asset by

taking a short position in the Futures market. (Short Futures hedge when

asset price may fall in future time).

3/16/2021 BFW2751 S2 2020 AP Jothee 6

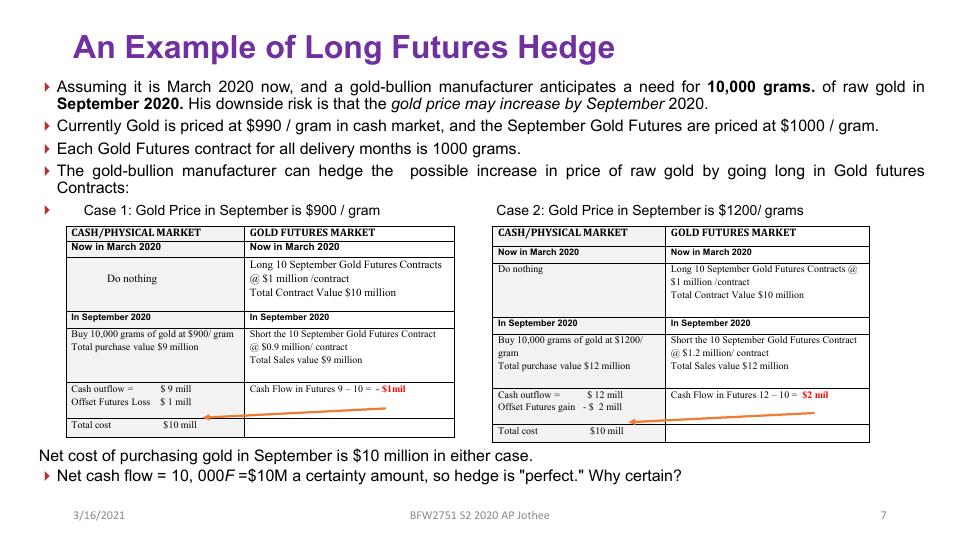

An Example of Long Futures Hedge

Assuming it is March 2020 now, and a gold-bullion manufacturer anticipates a need for 10,000 grams. of raw gold in

September 2020. His downside risk is that the gold price may increase by September 2020.

Currently Gold is priced at $990 / gram in cash market, and the September Gold Futures are priced at $1000 / gram.

Each Gold Futures contract for all delivery months is 1000 grams.

The gold-bullion manufacturer can hedge the possible increase in price of raw gold by going long in Gold futures

Contracts:

Case 1: Gold Price in September is $900 / gram Case 2: Gold Price in September is $1200/ grams

Net cost of purchasing gold in September is $10 million in either case.

Net cash flow = 10, 000F =$10M a certainty amount, so hedge is "perfect." Why certain?

3/16/2021 BFW2751 S2 2020 AP Jothee 7

CASH/PHYSICAL MARKET GOLD FUTURES MARKET

Now in March 2020 Now in March 2020

Do nothing

Long 10 September Gold Futures Contracts

@ $1 million /contract

Total Contract Value $10 million

In September 2020 In September 2020

Buy 10,000 grams of gold at $900/ gram

Total purchase value $9 million

Short the 10 September Gold Futures Contract

@ $0.9 million/ contract

Total Sales value $9 million

Cash outflow = $ 9 mill

Offset Futures Loss $ 1 mill

Cash Flow in Futures 9 – 10 = - $1mil

Total cost $10 mill

CASH/PHYSICAL MARKET GOLD FUTURES MARKET

Now in March 2020 Now in March 2020

Do nothing Long 10 September Gold Futures Contracts @

$1 million /contract

Total Contract Value $10 million

In September 2020 In September 2020

Buy 10,000 grams of gold at $1200/

gram

Total purchase value $12 million

Short the 10 September Gold Futures Contract

@ $1.2 million/ contract

Total Sales value $12 million

Cash outflow = $ 12 mill

Offset Futures gain - $ 2 mill

Cash Flow in Futures 12 – 10 = $2 mil

Total cost $10 mill

Assuming it is March 2020 now, and a gold-bullion manufacturer anticipates a need for 10,000 grams. of raw gold in

September 2020. His downside risk is that the gold price may increase by September 2020.

Currently Gold is priced at $990 / gram in cash market, and the September Gold Futures are priced at $1000 / gram.

Each Gold Futures contract for all delivery months is 1000 grams.

The gold-bullion manufacturer can hedge the possible increase in price of raw gold by going long in Gold futures

Contracts:

Case 1: Gold Price in September is $900 / gram Case 2: Gold Price in September is $1200/ grams

Net cost of purchasing gold in September is $10 million in either case.

Net cash flow = 10, 000F =$10M a certainty amount, so hedge is "perfect." Why certain?

3/16/2021 BFW2751 S2 2020 AP Jothee 7

CASH/PHYSICAL MARKET GOLD FUTURES MARKET

Now in March 2020 Now in March 2020

Do nothing

Long 10 September Gold Futures Contracts

@ $1 million /contract

Total Contract Value $10 million

In September 2020 In September 2020

Buy 10,000 grams of gold at $900/ gram

Total purchase value $9 million

Short the 10 September Gold Futures Contract

@ $0.9 million/ contract

Total Sales value $9 million

Cash outflow = $ 9 mill

Offset Futures Loss $ 1 mill

Cash Flow in Futures 9 – 10 = - $1mil

Total cost $10 mill

CASH/PHYSICAL MARKET GOLD FUTURES MARKET

Now in March 2020 Now in March 2020

Do nothing Long 10 September Gold Futures Contracts @

$1 million /contract

Total Contract Value $10 million

In September 2020 In September 2020

Buy 10,000 grams of gold at $1200/

gram

Total purchase value $12 million

Short the 10 September Gold Futures Contract

@ $1.2 million/ contract

Total Sales value $12 million

Cash outflow = $ 12 mill

Offset Futures gain - $ 2 mill

Cash Flow in Futures 12 – 10 = $2 mil

Total cost $10 mill

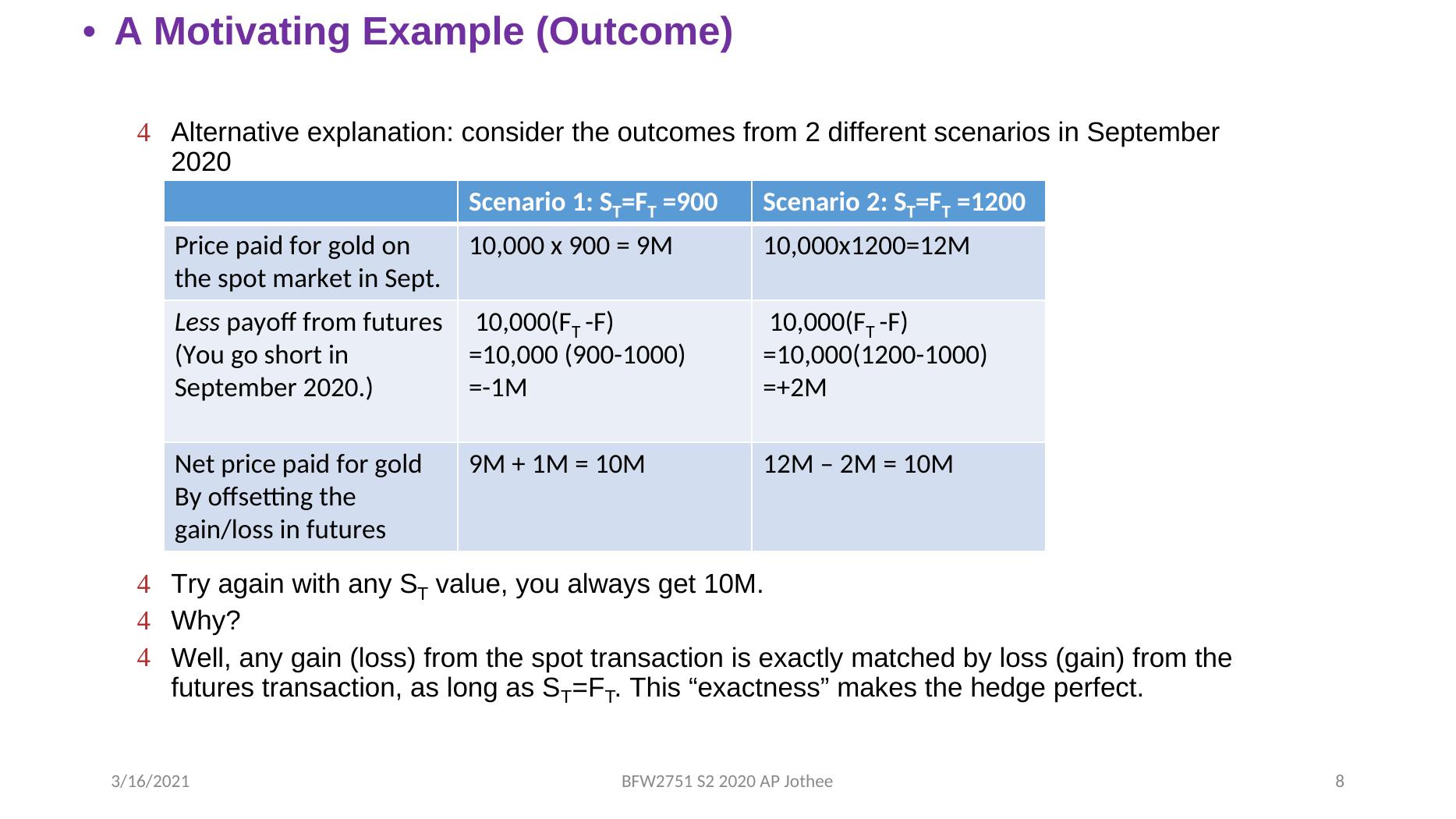

• A Motivating Example (Outcome)

Alternative explanation: consider the outcomes from 2 different scenarios in September

2020

Try again with any ST value, you always get 10M.

Why?

Well, any gain (loss) from the spot transaction is exactly matched by loss (gain) from the

futures transaction, as long as ST=FT. This “exactness” makes the hedge perfect.

Scenario 1: ST=FT =900 Scenario 2: ST=FT =1200

Price paid for gold on

the spot market in Sept.

10,000 x 900 = 9M 10,000x1200=12M

Less payoff from futures

(You go short in

September 2020.)

10,000(FT -F)

=10,000 (900-1000)

=-1M

10,000(FT -F)

=10,000(1200-1000)

=+2M

Net price paid for gold

By offsetting the

gain/loss in futures

9M + 1M = 10M 12M – 2M = 10M

3/16/2021 BFW2751 S2 2020 AP Jothee 8

Alternative explanation: consider the outcomes from 2 different scenarios in September

2020

Try again with any ST value, you always get 10M.

Why?

Well, any gain (loss) from the spot transaction is exactly matched by loss (gain) from the

futures transaction, as long as ST=FT. This “exactness” makes the hedge perfect.

Scenario 1: ST=FT =900 Scenario 2: ST=FT =1200

Price paid for gold on

the spot market in Sept.

10,000 x 900 = 9M 10,000x1200=12M

Less payoff from futures

(You go short in

September 2020.)

10,000(FT -F)

=10,000 (900-1000)

=-1M

10,000(FT -F)

=10,000(1200-1000)

=+2M

Net price paid for gold

By offsetting the

gain/loss in futures

9M + 1M = 10M 12M – 2M = 10M

3/16/2021 BFW2751 S2 2020 AP Jothee 8

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Futures Contracts Question Answer 2022lg...

|5

|1558

|13

Benefits And Limitations of Hedging Analysislg...

|8

|1533

|18