Analyzing BHP Billiton's Contemporary Accounting Issues & Framework

VerifiedAdded on 2023/06/12

|15

|2734

|128

Report

AI Summary

This report provides an analysis of BHP Billiton's compliance with the conceptual framework of accounting, focusing on its annual report and effectiveness in fulfilling related obligations. The assessment includes consideration of the company's adherence to the objectives of the conceptual framework, recognition criteria for revenue, taxation, trade receivables, plant, property, and equipment, goodwill, and closure and rehabilitation provisions. Furthermore, the report evaluates BHP Billiton's fundamental and enhancing guidelines, such as independence rules for directors, reporting processes, adherence to the JORC Code, and risk management practices, in relation to qualitative characteristics like relevance, reliability, and timeliness. The analysis concludes with recommendations for improvement, emphasizing the importance of disclosing only key financial and non-financial performance methods to enhance the meaningfulness of financial information for stakeholders. Desklib provides access to this and other solved assignments for students.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmrtyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

CONTEMPORARY ISSUES

IN ACCOUNTING

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmrtyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

CONTEMPORARY ISSUES

IN ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BHP Billiton

Executive summary

Conceptual framework has become crucial in the modern corporate environment because it

paves a path for companies to enjoy a good market reputation and enhance organizational

effectiveness respectively. With the help of this report, the annual report of BHP has been

considered. Moreover, it will be evaluated whether the company has been efficient in

fulfilling its conceptual framework obligations. For such purpose, consideration of the

company’s fulfillment of conceptual framework objective will be assessed. This will be

followed by its recognition criteria and fundamental and enhancing guidelines.

2

Executive summary

Conceptual framework has become crucial in the modern corporate environment because it

paves a path for companies to enjoy a good market reputation and enhance organizational

effectiveness respectively. With the help of this report, the annual report of BHP has been

considered. Moreover, it will be evaluated whether the company has been efficient in

fulfilling its conceptual framework obligations. For such purpose, consideration of the

company’s fulfillment of conceptual framework objective will be assessed. This will be

followed by its recognition criteria and fundamental and enhancing guidelines.

2

BHP Billiton

Contents

Introduction...........................................................................................................................................3

Consideration of objective of the conceptual framework.....................................................................4

Recognition criteria...............................................................................................................................5

Recognition of revenue.........................................................................................................................5

Taxation.................................................................................................................................................5

Trade receivables..................................................................................................................................6

Plant, property, and equipment............................................................................................................6

Goodwill and other intangibles.............................................................................................................6

Closure and rehabilitation.....................................................................................................................6

Fundamental and enhancing guidelines................................................................................................7

Recommendation..................................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

Contents

Introduction...........................................................................................................................................3

Consideration of objective of the conceptual framework.....................................................................4

Recognition criteria...............................................................................................................................5

Recognition of revenue.........................................................................................................................5

Taxation.................................................................................................................................................5

Trade receivables..................................................................................................................................6

Plant, property, and equipment............................................................................................................6

Goodwill and other intangibles.............................................................................................................6

Closure and rehabilitation.....................................................................................................................6

Fundamental and enhancing guidelines................................................................................................7

Recommendation..................................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BHP Billiton

Introduction

In the modern corporate environment, there are several complexities in the financial

transactions that occur on daily basis, and that necessitates fulfillment of conceptual

framework obligations of accounting. The reason behind this ideology can be attributed to the

fact that conceptual framework obligations allow an organization enhance its fundamental

and enhancing qualitative characteristics like materiality, relevance, reliability, faithful

representation, etc of financial reporting, thereby assisting both users and preparers in making

effective decisions for future developments (BHP Billiton, 2017). Furthermore, in the

absence of a conceptual framework of accounting, interpretation of financial information will

become difficult for the users and they may fail in making proper decisions based on such

information, thereby creating a topsy-turvy scenario for the entire organization (Carmichael

& Graham, 2012). With the help of this report, the effectiveness of BHP Billiton in fulfilling

the obligations of the conceptual framework of accounting will be analyzed taking into

consideration its recognition criteria, fundamental and enhancing guidelines, and

consideration of objectives of conceptual framework.

4

Introduction

In the modern corporate environment, there are several complexities in the financial

transactions that occur on daily basis, and that necessitates fulfillment of conceptual

framework obligations of accounting. The reason behind this ideology can be attributed to the

fact that conceptual framework obligations allow an organization enhance its fundamental

and enhancing qualitative characteristics like materiality, relevance, reliability, faithful

representation, etc of financial reporting, thereby assisting both users and preparers in making

effective decisions for future developments (BHP Billiton, 2017). Furthermore, in the

absence of a conceptual framework of accounting, interpretation of financial information will

become difficult for the users and they may fail in making proper decisions based on such

information, thereby creating a topsy-turvy scenario for the entire organization (Carmichael

& Graham, 2012). With the help of this report, the effectiveness of BHP Billiton in fulfilling

the obligations of the conceptual framework of accounting will be analyzed taking into

consideration its recognition criteria, fundamental and enhancing guidelines, and

consideration of objectives of conceptual framework.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BHP Billiton

Consideration of objective of the conceptual framework

BHP Billiton has efficiently considered the objective of conceptual framework by disclosing

relevant financial information to the stakeholders and other shareholders in order to assist

them in understanding and interpreting such information prepared in accordance with the

IFRS standards. Besides, the company has also explained its underlying performance through

disclosure of alternate performance measures. Moreover, the company has also excluded

certain details from its financial statements to the extent offered by Australian Law and the

United Kingdom. The reason behind this can be attributed to the fact that any such matter that

is associated with impending developments and matters in the negotiation course can cause

serious harm to the prejudicial interests of the company (Peirson et. al, 2015). Nevertheless,

this is because such disclosure can be misleading owing to the fact that it is preliminary or

premature in nature, associated to commercially sensitive contracts, may undermine

confidentiality between the clients or suppliers and the company, or may otherwise

unreasonably spoil the entire business (Freeman & Alexander, 2013). Overall, the

information categories excluded from the annual report of BHP Billiton Group comprises of

forward-looking projections and estimates prepared for the management of internal purposes,

information associated with the projects and assets of the company that is susceptible and

developing to change, and details related to pricing modules and commercial contracts

(Caradonna, 2014). All these inclusions and exclusions in the financial statements of the

Group clearly shed light on the fact that BHP has effectively considered the ideology of

proper disclosure strategies that can, in turn, assist its stakeholders in their decision-making

processes.

With respect to the corporate governance affairs, BHP Billiton Group has been committed to

highest standards of corporate governance by undertaking its business based on the ASX

recommendations listed in the third edition of the ASX (Australian Stock Exchange)

Corporate Governance Principles and Recommendations. In addition to this, BHP Billiton

has also furnished their reports in accordance with the UK Corporate Governance Code that

also comprises of the Turnbull Guidance. Furthermore, in order to consider the objectives of

the conceptual framework of accounting, the Group has offered material information in

relation to its investments in low-emission technologies for reducing fossil fuel emissions

(Deegan, 2011). With the provision of such material information, the stakeholders can be

easily guided on whether to invest their funds into the company or get associated with the

5

Consideration of objective of the conceptual framework

BHP Billiton has efficiently considered the objective of conceptual framework by disclosing

relevant financial information to the stakeholders and other shareholders in order to assist

them in understanding and interpreting such information prepared in accordance with the

IFRS standards. Besides, the company has also explained its underlying performance through

disclosure of alternate performance measures. Moreover, the company has also excluded

certain details from its financial statements to the extent offered by Australian Law and the

United Kingdom. The reason behind this can be attributed to the fact that any such matter that

is associated with impending developments and matters in the negotiation course can cause

serious harm to the prejudicial interests of the company (Peirson et. al, 2015). Nevertheless,

this is because such disclosure can be misleading owing to the fact that it is preliminary or

premature in nature, associated to commercially sensitive contracts, may undermine

confidentiality between the clients or suppliers and the company, or may otherwise

unreasonably spoil the entire business (Freeman & Alexander, 2013). Overall, the

information categories excluded from the annual report of BHP Billiton Group comprises of

forward-looking projections and estimates prepared for the management of internal purposes,

information associated with the projects and assets of the company that is susceptible and

developing to change, and details related to pricing modules and commercial contracts

(Caradonna, 2014). All these inclusions and exclusions in the financial statements of the

Group clearly shed light on the fact that BHP has effectively considered the ideology of

proper disclosure strategies that can, in turn, assist its stakeholders in their decision-making

processes.

With respect to the corporate governance affairs, BHP Billiton Group has been committed to

highest standards of corporate governance by undertaking its business based on the ASX

recommendations listed in the third edition of the ASX (Australian Stock Exchange)

Corporate Governance Principles and Recommendations. In addition to this, BHP Billiton

has also furnished their reports in accordance with the UK Corporate Governance Code that

also comprises of the Turnbull Guidance. Furthermore, in order to consider the objectives of

the conceptual framework of accounting, the Group has offered material information in

relation to its investments in low-emission technologies for reducing fossil fuel emissions

(Deegan, 2011). With the provision of such material information, the stakeholders can be

easily guided on whether to invest their funds into the company or get associated with the

5

BHP Billiton

company in any scenario. Overall, every type of information that is required by stakeholders

for addressing their decision-making process is appropriately taken into account by BHP

Billiton and the reason behind this fact can be attributed to the company’s prior significance

towards materiality segments (BHP Billiton, 2017). Hence, the business model of BHP

Group has assisted it in disclosing every type of information that is required to the

stakeholders and for such purpose, the company has not shown any negligence.

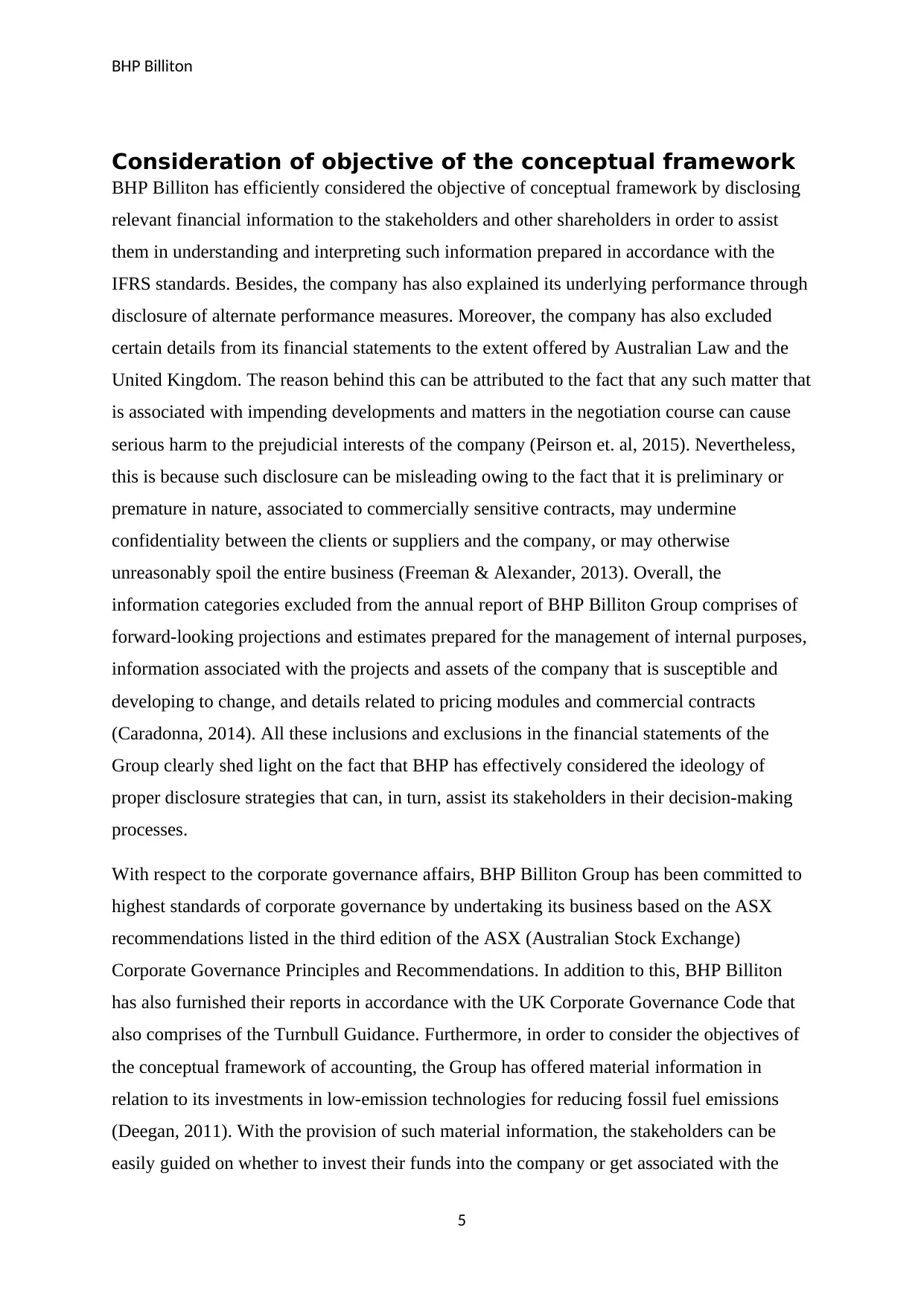

Recognition criteria

The accounting policies of the company have been prepared in accordance with the IASB,

AASB, AAS, IFRS, and requirements of Corporations Act 2001 that has facilitated in

enhancing the meaningfulness of its financial information. Furthermore, for the purpose of

corporate governance, the company has adhered to the UK Corporate Governance Code for

enhancing its recognition criteria as a whole (BHP Billiton, 2017).

Recognition of revenue

The company’s revenue is measured at the fair value of the obtained consideration. In

association with the sale of goods, revenue is recognized when the rewards and risks of goods

ownership have been passed to the buyer in accordance with agreed delivery terms. Further,

in relation to provisionally priced sales, revenue is recognized at the expected fair value of

receivable consideration in relation to contractual or/and forward price and ascertained

hydrocarbon or mineral specifications (BHP Billiton, 2017). Overall, the income of the

6

company in any scenario. Overall, every type of information that is required by stakeholders

for addressing their decision-making process is appropriately taken into account by BHP

Billiton and the reason behind this fact can be attributed to the company’s prior significance

towards materiality segments (BHP Billiton, 2017). Hence, the business model of BHP

Group has assisted it in disclosing every type of information that is required to the

stakeholders and for such purpose, the company has not shown any negligence.

Recognition criteria

The accounting policies of the company have been prepared in accordance with the IASB,

AASB, AAS, IFRS, and requirements of Corporations Act 2001 that has facilitated in

enhancing the meaningfulness of its financial information. Furthermore, for the purpose of

corporate governance, the company has adhered to the UK Corporate Governance Code for

enhancing its recognition criteria as a whole (BHP Billiton, 2017).

Recognition of revenue

The company’s revenue is measured at the fair value of the obtained consideration. In

association with the sale of goods, revenue is recognized when the rewards and risks of goods

ownership have been passed to the buyer in accordance with agreed delivery terms. Further,

in relation to provisionally priced sales, revenue is recognized at the expected fair value of

receivable consideration in relation to contractual or/and forward price and ascertained

hydrocarbon or mineral specifications (BHP Billiton, 2017). Overall, the income of the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BHP Billiton

Group is recognized when it becomes feasible that the financial benefits related to a

transaction will flow to it and they can be measured effectively or reliably. Moreover,

dividends are recognized upon their declaration (Parrino et. al, 2012).

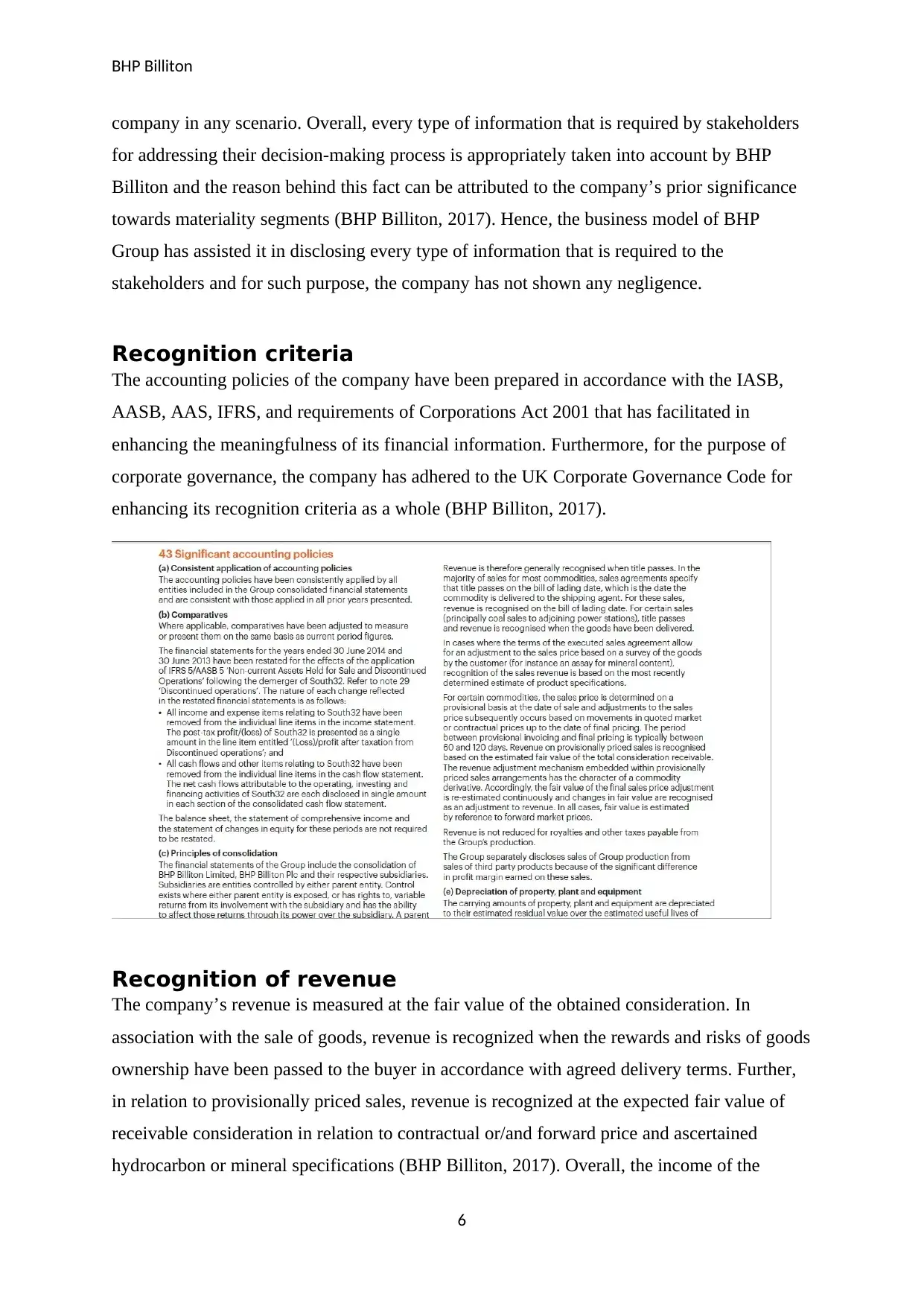

Taxation

Taxation on the loss or profit for the year consists of deferred and current tax. Moreover,

taxation of the company is recognized in the income statement except to the level that it is

associated with the items recognized directly in equity wherein the tax effect is also identified

in equity (BHP Billiton, 2017). Furthermore, recognition of deferred tax assets are done to

level that it is feasible that future tax revenues will be prevalent in contrast to the utilization

of temporary differences.

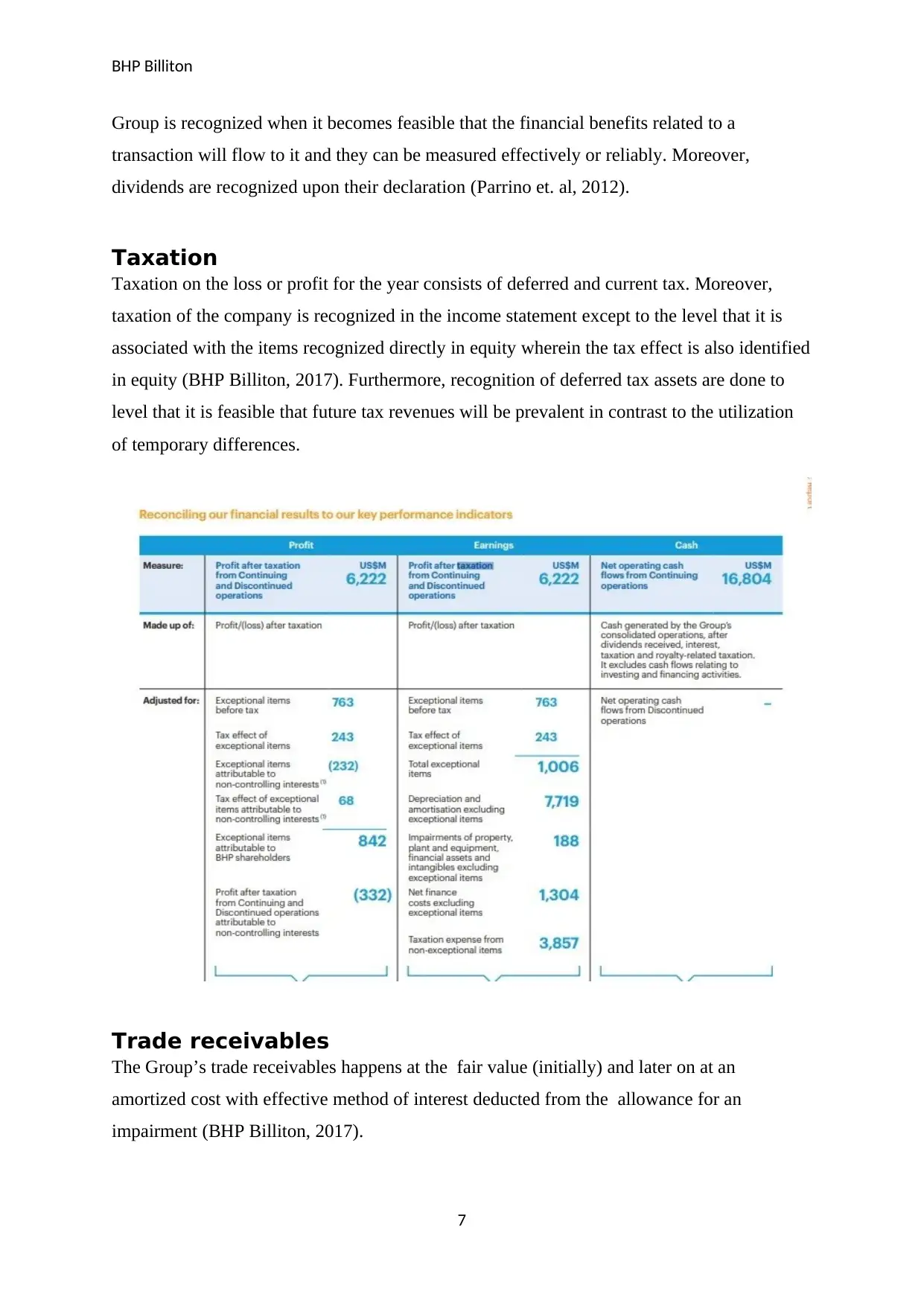

Trade receivables

The Group’s trade receivables happens at the fair value (initially) and later on at an

amortized cost with effective method of interest deducted from the allowance for an

impairment (BHP Billiton, 2017).

7

Group is recognized when it becomes feasible that the financial benefits related to a

transaction will flow to it and they can be measured effectively or reliably. Moreover,

dividends are recognized upon their declaration (Parrino et. al, 2012).

Taxation

Taxation on the loss or profit for the year consists of deferred and current tax. Moreover,

taxation of the company is recognized in the income statement except to the level that it is

associated with the items recognized directly in equity wherein the tax effect is also identified

in equity (BHP Billiton, 2017). Furthermore, recognition of deferred tax assets are done to

level that it is feasible that future tax revenues will be prevalent in contrast to the utilization

of temporary differences.

Trade receivables

The Group’s trade receivables happens at the fair value (initially) and later on at an

amortized cost with effective method of interest deducted from the allowance for an

impairment (BHP Billiton, 2017).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BHP Billiton

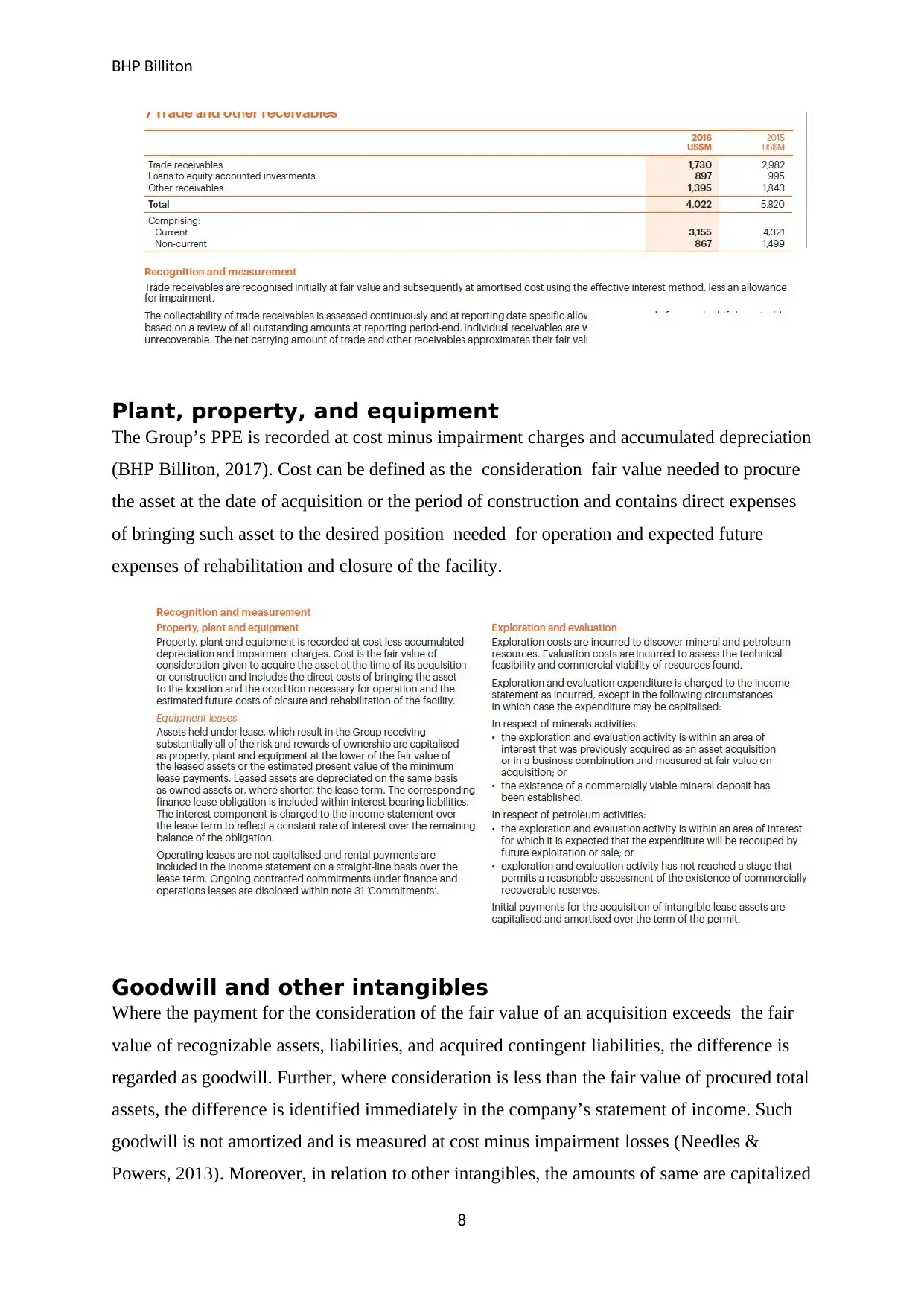

Plant, property, and equipment

The Group’s PPE is recorded at cost minus impairment charges and accumulated depreciation

(BHP Billiton, 2017). Cost can be defined as the consideration fair value needed to procure

the asset at the date of acquisition or the period of construction and contains direct expenses

of bringing such asset to the desired position needed for operation and expected future

expenses of rehabilitation and closure of the facility.

Goodwill and other intangibles

Where the payment for the consideration of the fair value of an acquisition exceeds the fair

value of recognizable assets, liabilities, and acquired contingent liabilities, the difference is

regarded as goodwill. Further, where consideration is less than the fair value of procured total

assets, the difference is identified immediately in the company’s statement of income. Such

goodwill is not amortized and is measured at cost minus impairment losses (Needles &

Powers, 2013). Moreover, in relation to other intangibles, the amounts of same are capitalized

8

Plant, property, and equipment

The Group’s PPE is recorded at cost minus impairment charges and accumulated depreciation

(BHP Billiton, 2017). Cost can be defined as the consideration fair value needed to procure

the asset at the date of acquisition or the period of construction and contains direct expenses

of bringing such asset to the desired position needed for operation and expected future

expenses of rehabilitation and closure of the facility.

Goodwill and other intangibles

Where the payment for the consideration of the fair value of an acquisition exceeds the fair

value of recognizable assets, liabilities, and acquired contingent liabilities, the difference is

regarded as goodwill. Further, where consideration is less than the fair value of procured total

assets, the difference is identified immediately in the company’s statement of income. Such

goodwill is not amortized and is measured at cost minus impairment losses (Needles &

Powers, 2013). Moreover, in relation to other intangibles, the amounts of same are capitalized

8

BHP Billiton

for the procurement of recognizable intangibles like licenses, software, and initial payments

for procurement of mineral lease assets wherein it is regarded that the same will assist in

contributing to future tenures through the generation of revenue or reduction in expenses as a

whole (BHP Billiton, 2017).

Closure and rehabilitation

The Group’s provisions for rehabilitation and closure are recognized when the amount can be

estimated reliably, when it pursues a constructive or legal obligation as an outcome of the

events that happened in the past and when it is more feasible the resources outflow is

essential to cover the obligations (BHP Billiton, 2017).

9

for the procurement of recognizable intangibles like licenses, software, and initial payments

for procurement of mineral lease assets wherein it is regarded that the same will assist in

contributing to future tenures through the generation of revenue or reduction in expenses as a

whole (BHP Billiton, 2017).

Closure and rehabilitation

The Group’s provisions for rehabilitation and closure are recognized when the amount can be

estimated reliably, when it pursues a constructive or legal obligation as an outcome of the

events that happened in the past and when it is more feasible the resources outflow is

essential to cover the obligations (BHP Billiton, 2017).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BHP Billiton

Fundamental and enhancing guidelines

In relation to the effectiveness of BHP’s obligations in fulfilling the requirements of

conceptual framework, it can be seen that the company has various fundamental and

enhancing guidelines contained within the operations enabling it to sustain a competitive

advantage in the market and provide accurate and adequate information to the stakeholders

for enhancements of their decision-making process. The company’s guidelines for the

independence rules and regulations of the directors allow it to comply with the faithful

representation qualitative characteristic of the conceptual framework because the directors’

independence is guided by fulfillment of rules like UK rules, US rules, and Australia rules.

Moreover, these directors are also bound to reflect an authentic view of the financial

statements of the company by complying with the requirements of Corporations Act 2001

(Davies & Crawford, 2012). In addition, the company also has a guideline that allows it set

reporting processes and controls for the purpose of the release of significant information to

the stakeholders. In relation to this, BHP is committed towards highest disclosure standards

by signalling that all potential investors contains a link to relevant, proper information in a

timely and accessible way for the purpose of making informed decisions (BHP Billiton,

2017). With the help or prevalence of such fundamental guideline within the Group’s

framework, qualitative characteristics of the conceptual framework like relevance, reliability,

and timeliness are also easily taken into consideration, thereby facilitating in enhancing the

meaningfulness of financial information present in the statements (Hemmer & Labro, 2008).

Another significant and enhancing guideline within the Group is the adherence to JORC

Code (Joint Ore Reserves Committee). With the help of such guideline, the company ensures

both external and internal users regarding its effectiveness of operations. This guideline is for

public reporting in relation to mineral resources, reserves of ore, and exploration results in

Australia that is accurately fulfilled by the Group and that can allow stakeholders rely upon

the same for making effective decisions (BHP Billiton, 2017). In addition, the Group also has

a risk management guideline within its affairs that allows it in managing and identifying

opportunities and risks for creating long-term value for the shareholders. Moreover, the

presence of internal control functions for mitigating the effects of risk allows BHP to comply

with the legal requirements and internal guidelines (Levine & Prietula, 2013). Such control

function can provide an opportunity to the Group in reducing the possibilities of risks and

further surveillance of overall processes (Brigham & Daves, 2012). These guidelines have not

10

Fundamental and enhancing guidelines

In relation to the effectiveness of BHP’s obligations in fulfilling the requirements of

conceptual framework, it can be seen that the company has various fundamental and

enhancing guidelines contained within the operations enabling it to sustain a competitive

advantage in the market and provide accurate and adequate information to the stakeholders

for enhancements of their decision-making process. The company’s guidelines for the

independence rules and regulations of the directors allow it to comply with the faithful

representation qualitative characteristic of the conceptual framework because the directors’

independence is guided by fulfillment of rules like UK rules, US rules, and Australia rules.

Moreover, these directors are also bound to reflect an authentic view of the financial

statements of the company by complying with the requirements of Corporations Act 2001

(Davies & Crawford, 2012). In addition, the company also has a guideline that allows it set

reporting processes and controls for the purpose of the release of significant information to

the stakeholders. In relation to this, BHP is committed towards highest disclosure standards

by signalling that all potential investors contains a link to relevant, proper information in a

timely and accessible way for the purpose of making informed decisions (BHP Billiton,

2017). With the help or prevalence of such fundamental guideline within the Group’s

framework, qualitative characteristics of the conceptual framework like relevance, reliability,

and timeliness are also easily taken into consideration, thereby facilitating in enhancing the

meaningfulness of financial information present in the statements (Hemmer & Labro, 2008).

Another significant and enhancing guideline within the Group is the adherence to JORC

Code (Joint Ore Reserves Committee). With the help of such guideline, the company ensures

both external and internal users regarding its effectiveness of operations. This guideline is for

public reporting in relation to mineral resources, reserves of ore, and exploration results in

Australia that is accurately fulfilled by the Group and that can allow stakeholders rely upon

the same for making effective decisions (BHP Billiton, 2017). In addition, the Group also has

a risk management guideline within its affairs that allows it in managing and identifying

opportunities and risks for creating long-term value for the shareholders. Moreover, the

presence of internal control functions for mitigating the effects of risk allows BHP to comply

with the legal requirements and internal guidelines (Levine & Prietula, 2013). Such control

function can provide an opportunity to the Group in reducing the possibilities of risks and

further surveillance of overall processes (Brigham & Daves, 2012). These guidelines have not

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BHP Billiton

only assisted the company in fulfilling its disclosure requirements but have also catered to the

obligations of the conceptual framework of accounting (Siraj et. al, 2011).

11

only assisted the company in fulfilling its disclosure requirements but have also catered to the

obligations of the conceptual framework of accounting (Siraj et. al, 2011).

11

BHP Billiton

Recommendation

After a critical assessment of the financial statement of BHP Billiton, it is observable that the

company’s disclosures are of relevant nature and this is the reason why stakeholders have

been able to make proper decisions based on the same. However, it is recommended to the

company that only key financial and non-financial performance methods be disclosed to the

users (Douma & Hein, 2013). This means that information that is not relevant in nature must

be discarded. Further, the discussion be spread to the matter that the provision of non-

significant information may only create troubles and complications for the users in making

informed decisions, thereby spoiling the overall significance of conceptual framework of

accounting.

12

Recommendation

After a critical assessment of the financial statement of BHP Billiton, it is observable that the

company’s disclosures are of relevant nature and this is the reason why stakeholders have

been able to make proper decisions based on the same. However, it is recommended to the

company that only key financial and non-financial performance methods be disclosed to the

users (Douma & Hein, 2013). This means that information that is not relevant in nature must

be discarded. Further, the discussion be spread to the matter that the provision of non-

significant information may only create troubles and complications for the users in making

informed decisions, thereby spoiling the overall significance of conceptual framework of

accounting.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.