Crystal Hotel Financial Analysis: Performance and Industry Comparison

VerifiedAdded on 2023/01/16

|12

|2593

|82

Report

AI Summary

This report conducts a comprehensive financial analysis of Crystal Hotel, focusing on its performance in 2015. It begins with an executive summary and introduction, followed by a comparative analysis of the hotel's income statement against industry benchmarks, utilizing vertical analysis to highlight revenue streams and cost structures. The report delves into a detailed ratio analysis, examining profitability (gross profit margin, net profit margin, ROA, ROE), efficiency (inventory turnover, accounts receivable collection), liquidity (current ratio, quick ratio), and solvency ratios. The analysis compares Crystal Hotel's performance against industry averages, identifying areas of strength and weakness. Findings suggest the hotel excels in managing personnel costs and generating net profit, but needs improvement in cost of sales, inventory turnover, and accounts receivable collection. The report also uses other industry benchmarks like occupancy rates and average daily rates to further evaluate the hotel's operational efficiency and financial standing, concluding with recommendations for improvement.

BIZ201 Accounting for Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The purpose of this report is to address the financial issues faced by Crystal Hotel and to

make comparison of company performance with industry benchmark through use ratios and

vertical analysis. Vertical comparative analysis of company with industry benchmark shows that

company had been successful in saving must of its cost but it lack behind in reducing the cost of

sales and unallocated operating cost. It might be possible that company provide extra services

free of cost to their customer that adds to operating cost that no other hotel provide.

The purpose of this report is to address the financial issues faced by Crystal Hotel and to

make comparison of company performance with industry benchmark through use ratios and

vertical analysis. Vertical comparative analysis of company with industry benchmark shows that

company had been successful in saving must of its cost but it lack behind in reducing the cost of

sales and unallocated operating cost. It might be possible that company provide extra services

free of cost to their customer that adds to operating cost that no other hotel provide.

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Comparative Analysis of income statement of Crystal Hotel with its industry benchmarks..........4

Ratio Analysis of Crystal Hotel and comparative analysis with the industry values......................6

Use of other industry benchmark to compare company performance with that of industry.........10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Comparative Analysis of income statement of Crystal Hotel with its industry benchmarks..........4

Ratio Analysis of Crystal Hotel and comparative analysis with the industry values......................6

Use of other industry benchmark to compare company performance with that of industry.........10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

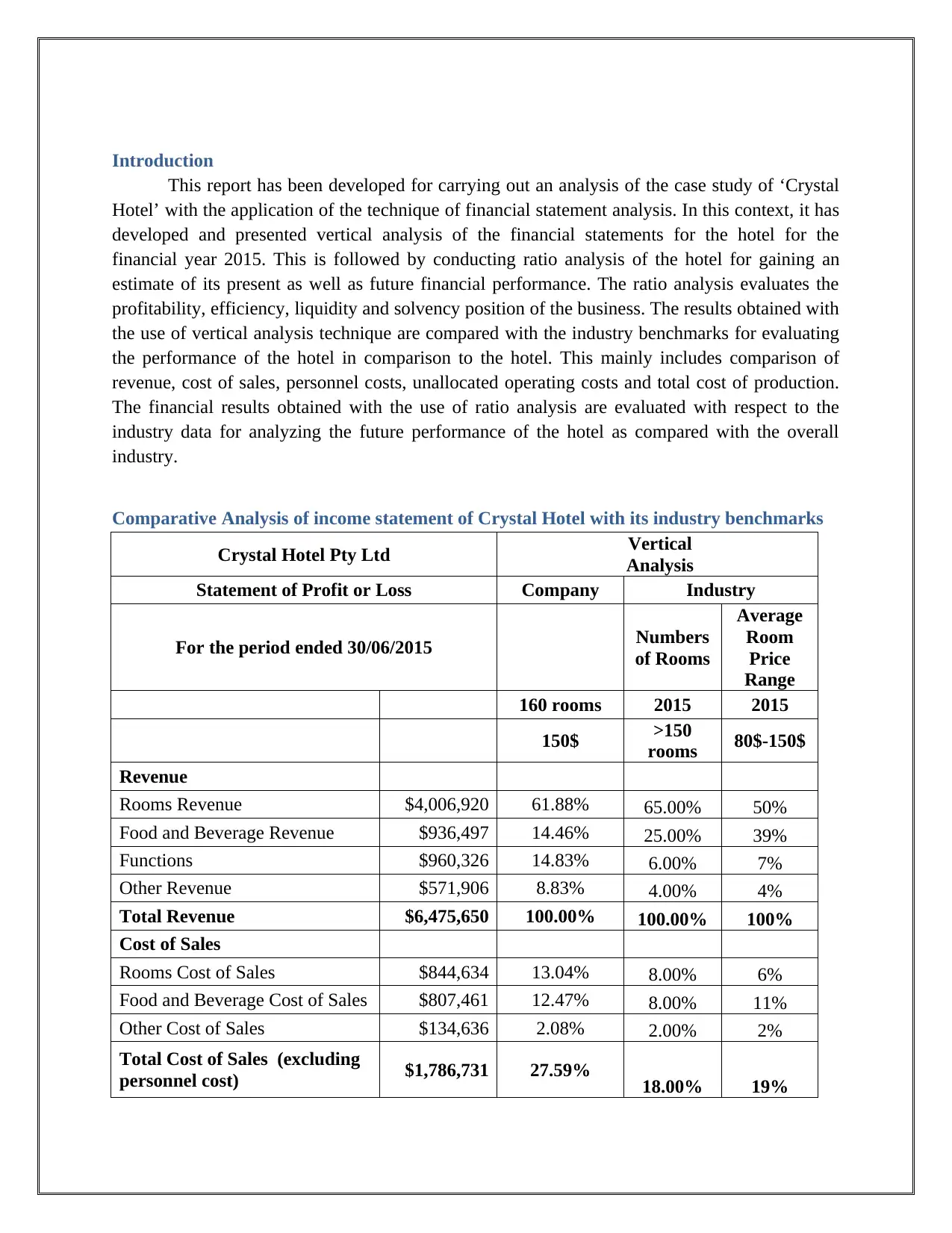

Introduction

This report has been developed for carrying out an analysis of the case study of ‘Crystal

Hotel’ with the application of the technique of financial statement analysis. In this context, it has

developed and presented vertical analysis of the financial statements for the hotel for the

financial year 2015. This is followed by conducting ratio analysis of the hotel for gaining an

estimate of its present as well as future financial performance. The ratio analysis evaluates the

profitability, efficiency, liquidity and solvency position of the business. The results obtained with

the use of vertical analysis technique are compared with the industry benchmarks for evaluating

the performance of the hotel in comparison to the hotel. This mainly includes comparison of

revenue, cost of sales, personnel costs, unallocated operating costs and total cost of production.

The financial results obtained with the use of ratio analysis are evaluated with respect to the

industry data for analyzing the future performance of the hotel as compared with the overall

industry.

Comparative Analysis of income statement of Crystal Hotel with its industry benchmarks

Crystal Hotel Pty Ltd Vertical

Analysis

Statement of Profit or Loss Company Industry

For the period ended 30/06/2015 Numbers

of Rooms

Average

Room

Price

Range

160 rooms 2015 2015

150$ >150

rooms 80$-150$

Revenue

Rooms Revenue $4,006,920 61.88% 65.00% 50%

Food and Beverage Revenue $936,497 14.46% 25.00% 39%

Functions $960,326 14.83% 6.00% 7%

Other Revenue $571,906 8.83% 4.00% 4%

Total Revenue $6,475,650 100.00% 100.00% 100%

Cost of Sales

Rooms Cost of Sales $844,634 13.04% 8.00% 6%

Food and Beverage Cost of Sales $807,461 12.47% 8.00% 11%

Other Cost of Sales $134,636 2.08% 2.00% 2%

Total Cost of Sales (excluding

personnel cost) $1,786,731 27.59% 18.00% 19%

This report has been developed for carrying out an analysis of the case study of ‘Crystal

Hotel’ with the application of the technique of financial statement analysis. In this context, it has

developed and presented vertical analysis of the financial statements for the hotel for the

financial year 2015. This is followed by conducting ratio analysis of the hotel for gaining an

estimate of its present as well as future financial performance. The ratio analysis evaluates the

profitability, efficiency, liquidity and solvency position of the business. The results obtained with

the use of vertical analysis technique are compared with the industry benchmarks for evaluating

the performance of the hotel in comparison to the hotel. This mainly includes comparison of

revenue, cost of sales, personnel costs, unallocated operating costs and total cost of production.

The financial results obtained with the use of ratio analysis are evaluated with respect to the

industry data for analyzing the future performance of the hotel as compared with the overall

industry.

Comparative Analysis of income statement of Crystal Hotel with its industry benchmarks

Crystal Hotel Pty Ltd Vertical

Analysis

Statement of Profit or Loss Company Industry

For the period ended 30/06/2015 Numbers

of Rooms

Average

Room

Price

Range

160 rooms 2015 2015

150$ >150

rooms 80$-150$

Revenue

Rooms Revenue $4,006,920 61.88% 65.00% 50%

Food and Beverage Revenue $936,497 14.46% 25.00% 39%

Functions $960,326 14.83% 6.00% 7%

Other Revenue $571,906 8.83% 4.00% 4%

Total Revenue $6,475,650 100.00% 100.00% 100%

Cost of Sales

Rooms Cost of Sales $844,634 13.04% 8.00% 6%

Food and Beverage Cost of Sales $807,461 12.47% 8.00% 11%

Other Cost of Sales $134,636 2.08% 2.00% 2%

Total Cost of Sales (excluding

personnel cost) $1,786,731 27.59% 18.00% 19%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

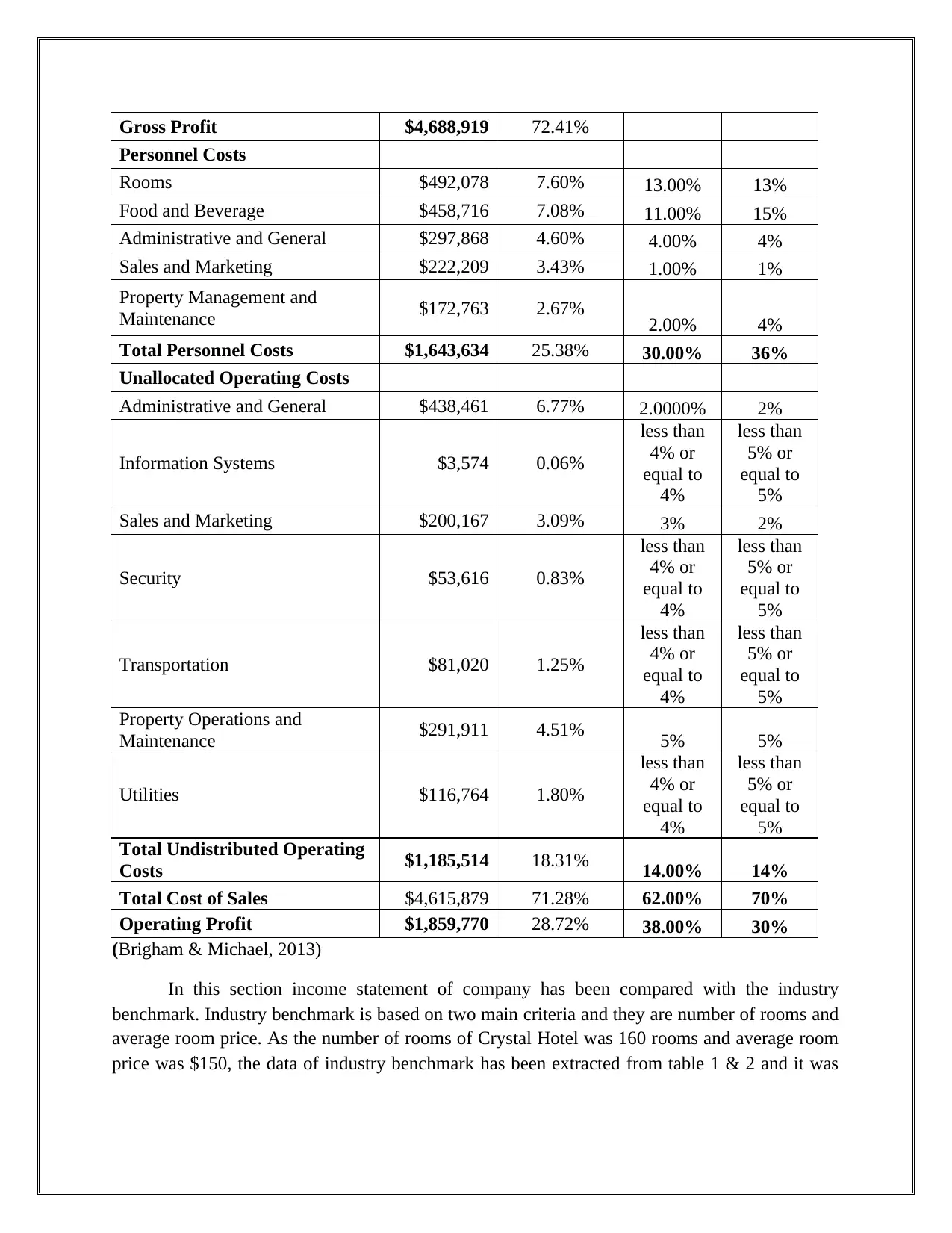

Gross Profit $4,688,919 72.41%

Personnel Costs

Rooms $492,078 7.60% 13.00% 13%

Food and Beverage $458,716 7.08% 11.00% 15%

Administrative and General $297,868 4.60% 4.00% 4%

Sales and Marketing $222,209 3.43% 1.00% 1%

Property Management and

Maintenance $172,763 2.67% 2.00% 4%

Total Personnel Costs $1,643,634 25.38% 30.00% 36%

Unallocated Operating Costs

Administrative and General $438,461 6.77% 2.0000% 2%

Information Systems $3,574 0.06%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Sales and Marketing $200,167 3.09% 3% 2%

Security $53,616 0.83%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Transportation $81,020 1.25%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Property Operations and

Maintenance $291,911 4.51% 5% 5%

Utilities $116,764 1.80%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Total Undistributed Operating

Costs $1,185,514 18.31% 14.00% 14%

Total Cost of Sales $4,615,879 71.28% 62.00% 70%

Operating Profit $1,859,770 28.72% 38.00% 30%

(Brigham & Michael, 2013)

In this section income statement of company has been compared with the industry

benchmark. Industry benchmark is based on two main criteria and they are number of rooms and

average room price. As the number of rooms of Crystal Hotel was 160 rooms and average room

price was $150, the data of industry benchmark has been extracted from table 1 & 2 and it was

Personnel Costs

Rooms $492,078 7.60% 13.00% 13%

Food and Beverage $458,716 7.08% 11.00% 15%

Administrative and General $297,868 4.60% 4.00% 4%

Sales and Marketing $222,209 3.43% 1.00% 1%

Property Management and

Maintenance $172,763 2.67% 2.00% 4%

Total Personnel Costs $1,643,634 25.38% 30.00% 36%

Unallocated Operating Costs

Administrative and General $438,461 6.77% 2.0000% 2%

Information Systems $3,574 0.06%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Sales and Marketing $200,167 3.09% 3% 2%

Security $53,616 0.83%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Transportation $81,020 1.25%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Property Operations and

Maintenance $291,911 4.51% 5% 5%

Utilities $116,764 1.80%

less than

4% or

equal to

4%

less than

5% or

equal to

5%

Total Undistributed Operating

Costs $1,185,514 18.31% 14.00% 14%

Total Cost of Sales $4,615,879 71.28% 62.00% 70%

Operating Profit $1,859,770 28.72% 38.00% 30%

(Brigham & Michael, 2013)

In this section income statement of company has been compared with the industry

benchmark. Industry benchmark is based on two main criteria and they are number of rooms and

average room price. As the number of rooms of Crystal Hotel was 160 rooms and average room

price was $150, the data of industry benchmark has been extracted from table 1 & 2 and it was

compared with company vertical analysis of income statement above. Some important points of

comparison have been discussed below:

Revenue: When revenue percentage of different streams have been compared with

industry benchmark it has been found that company focus functions and other revenue in

addition to room revenue and sale of food & beverages. Industry benchmark is very low

for both functions and other revenue that supports that Crystal Hotels make organization

of functions at large scale as compared to competitors in same industry. On the basis of

average room price industry benchmark, Crystal Hotel had outperformed the other

companies. It means Crystal Hotel have high occupancy ratios as compared to

competitors. On the basis of number of rooms, company has slightly low revenue

percentage from rooms as compared to industry benchmark which indicates company

follows competitive pricing strategy to allow to maximum occupancy of rooms. Crystal

hotel earned approx 15% from sale of food & beverages but it very low as compared to

industry. Overall it is recommended to focus on sale of food & beverages through use of

attractive offers (Damodaran, 2011).

Cost of Sales: Overall cost of sales of company was very high as compared to industry

benchmark in both cases (Number of rooms and average room price). It means there is

need to focus on reducing the cost of sales through reducing the offering made to

customers and use of value proposition measures to control the cost.

Personnel costs: Personnel cost of company have been charged relatively low as

compared to industry benchmark that allows company to save some cost and use such

money for improvement of hotel overall facilities.

Unallocated operating cost: These cost are fixed in nature and they are very important

for providing the main services but it is very important company should allow only such

cost that add value to the revenue. These costs add 18% of overall revenue while average

industry benchmark limits it 14% that indicates company is providing additional services

that no hotel is providing (Davies & Crawford, 2011).

Ratio Analysis of Crystal Hotel and comparative analysis with the industry values

This section of the report has presented the financial results in context of the profitability,

efficiency, liquidity and solvency position of the Crystal Hotel Pvt Ltd. The outcomes achieved

with the use of ratio analysis technique are evaluated as per the industry benchmarks in order to

evaluate the financial performance of the hotel as compared with the industry benchmarks.

Profitability Analysis

The analysis is carried out for determining the ability of a business to generate profit after

meeting all its expenses related to carrying out its operational activities. It is calculated by the

use of following ratios:

comparison have been discussed below:

Revenue: When revenue percentage of different streams have been compared with

industry benchmark it has been found that company focus functions and other revenue in

addition to room revenue and sale of food & beverages. Industry benchmark is very low

for both functions and other revenue that supports that Crystal Hotels make organization

of functions at large scale as compared to competitors in same industry. On the basis of

average room price industry benchmark, Crystal Hotel had outperformed the other

companies. It means Crystal Hotel have high occupancy ratios as compared to

competitors. On the basis of number of rooms, company has slightly low revenue

percentage from rooms as compared to industry benchmark which indicates company

follows competitive pricing strategy to allow to maximum occupancy of rooms. Crystal

hotel earned approx 15% from sale of food & beverages but it very low as compared to

industry. Overall it is recommended to focus on sale of food & beverages through use of

attractive offers (Damodaran, 2011).

Cost of Sales: Overall cost of sales of company was very high as compared to industry

benchmark in both cases (Number of rooms and average room price). It means there is

need to focus on reducing the cost of sales through reducing the offering made to

customers and use of value proposition measures to control the cost.

Personnel costs: Personnel cost of company have been charged relatively low as

compared to industry benchmark that allows company to save some cost and use such

money for improvement of hotel overall facilities.

Unallocated operating cost: These cost are fixed in nature and they are very important

for providing the main services but it is very important company should allow only such

cost that add value to the revenue. These costs add 18% of overall revenue while average

industry benchmark limits it 14% that indicates company is providing additional services

that no hotel is providing (Davies & Crawford, 2011).

Ratio Analysis of Crystal Hotel and comparative analysis with the industry values

This section of the report has presented the financial results in context of the profitability,

efficiency, liquidity and solvency position of the Crystal Hotel Pvt Ltd. The outcomes achieved

with the use of ratio analysis technique are evaluated as per the industry benchmarks in order to

evaluate the financial performance of the hotel as compared with the industry benchmarks.

Profitability Analysis

The analysis is carried out for determining the ability of a business to generate profit after

meeting all its expenses related to carrying out its operational activities. It is calculated by the

use of following ratios:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

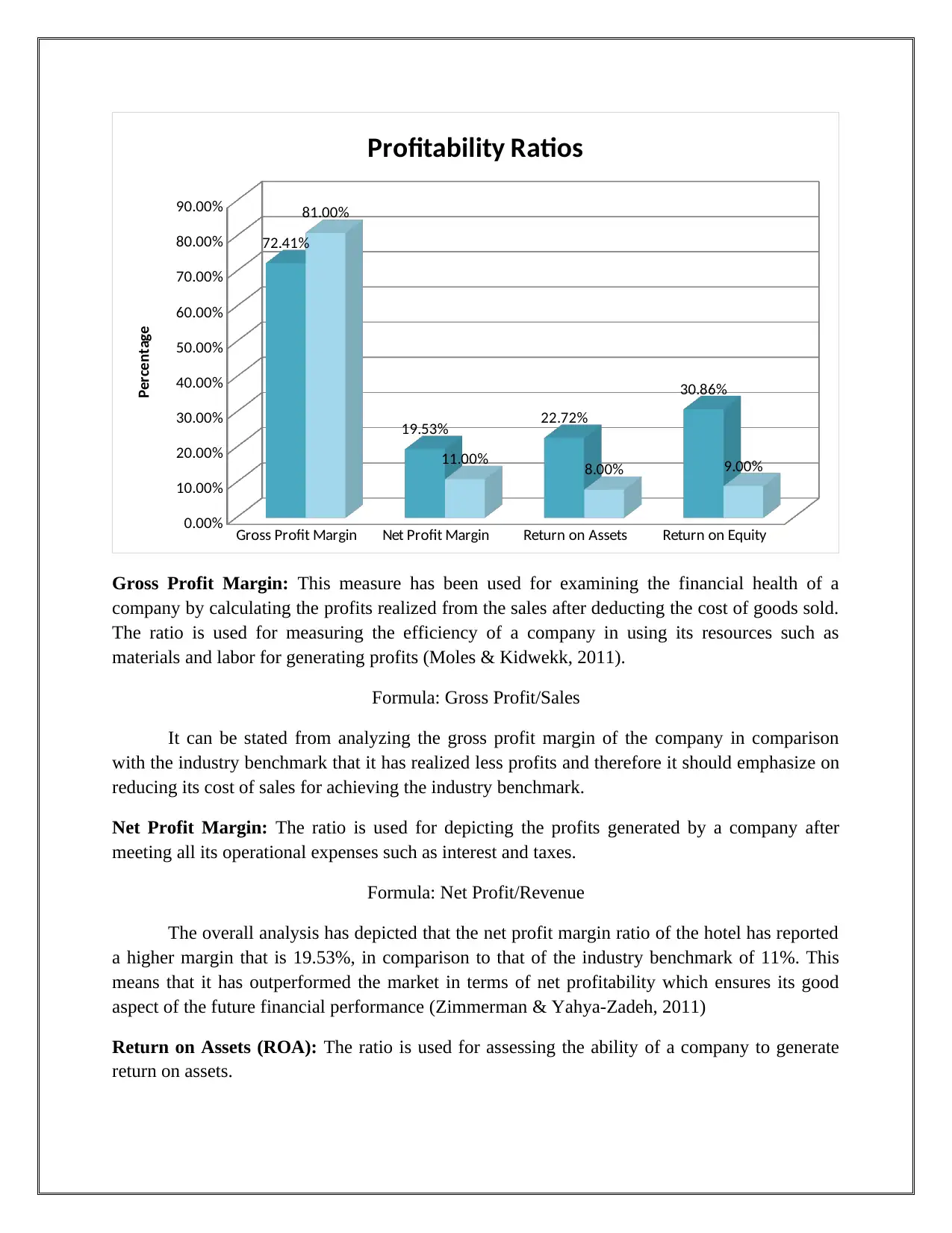

Gross Profit Margin Net Profit Margin Return on Assets Return on Equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

72.41%

19.53% 22.72%

30.86%

81.00%

11.00% 8.00% 9.00%

Profitability Ratios

Percentage

Gross Profit Margin: This measure has been used for examining the financial health of a

company by calculating the profits realized from the sales after deducting the cost of goods sold.

The ratio is used for measuring the efficiency of a company in using its resources such as

materials and labor for generating profits (Moles & Kidwekk, 2011).

Formula: Gross Profit/Sales

It can be stated from analyzing the gross profit margin of the company in comparison

with the industry benchmark that it has realized less profits and therefore it should emphasize on

reducing its cost of sales for achieving the industry benchmark.

Net Profit Margin: The ratio is used for depicting the profits generated by a company after

meeting all its operational expenses such as interest and taxes.

Formula: Net Profit/Revenue

The overall analysis has depicted that the net profit margin ratio of the hotel has reported

a higher margin that is 19.53%, in comparison to that of the industry benchmark of 11%. This

means that it has outperformed the market in terms of net profitability which ensures its good

aspect of the future financial performance (Zimmerman & Yahya-Zadeh, 2011)

Return on Assets (ROA): The ratio is used for assessing the ability of a company to generate

return on assets.

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

72.41%

19.53% 22.72%

30.86%

81.00%

11.00% 8.00% 9.00%

Profitability Ratios

Percentage

Gross Profit Margin: This measure has been used for examining the financial health of a

company by calculating the profits realized from the sales after deducting the cost of goods sold.

The ratio is used for measuring the efficiency of a company in using its resources such as

materials and labor for generating profits (Moles & Kidwekk, 2011).

Formula: Gross Profit/Sales

It can be stated from analyzing the gross profit margin of the company in comparison

with the industry benchmark that it has realized less profits and therefore it should emphasize on

reducing its cost of sales for achieving the industry benchmark.

Net Profit Margin: The ratio is used for depicting the profits generated by a company after

meeting all its operational expenses such as interest and taxes.

Formula: Net Profit/Revenue

The overall analysis has depicted that the net profit margin ratio of the hotel has reported

a higher margin that is 19.53%, in comparison to that of the industry benchmark of 11%. This

means that it has outperformed the market in terms of net profitability which ensures its good

aspect of the future financial performance (Zimmerman & Yahya-Zadeh, 2011)

Return on Assets (ROA): The ratio is used for assessing the ability of a company to generate

return on assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Formula: Net Income/Total value of assets

It can be stated from analyzing the financial results of the hotel that it has realized higher

returns, that is, 22.72% from the use of its asset base in comparison to the overall industry

benchmark that is 8%. The performance of the hotel business can be stated as very good as

compared with its competitors that ensures its good future prospects.

Return on Equity (ROE): It provides an assessment regarding the profits realized by a

company for generating income from the equity base. The formula used for the calculation is as

follows:

ROE=Net Income/Shareholders Equity

ROE of the hotel, that is, 30.86%, as compared with the industry benchmark of 9% that

states that the hotel has outperformed the industry by realizing higher returns on equity as

compared with its competitor base.

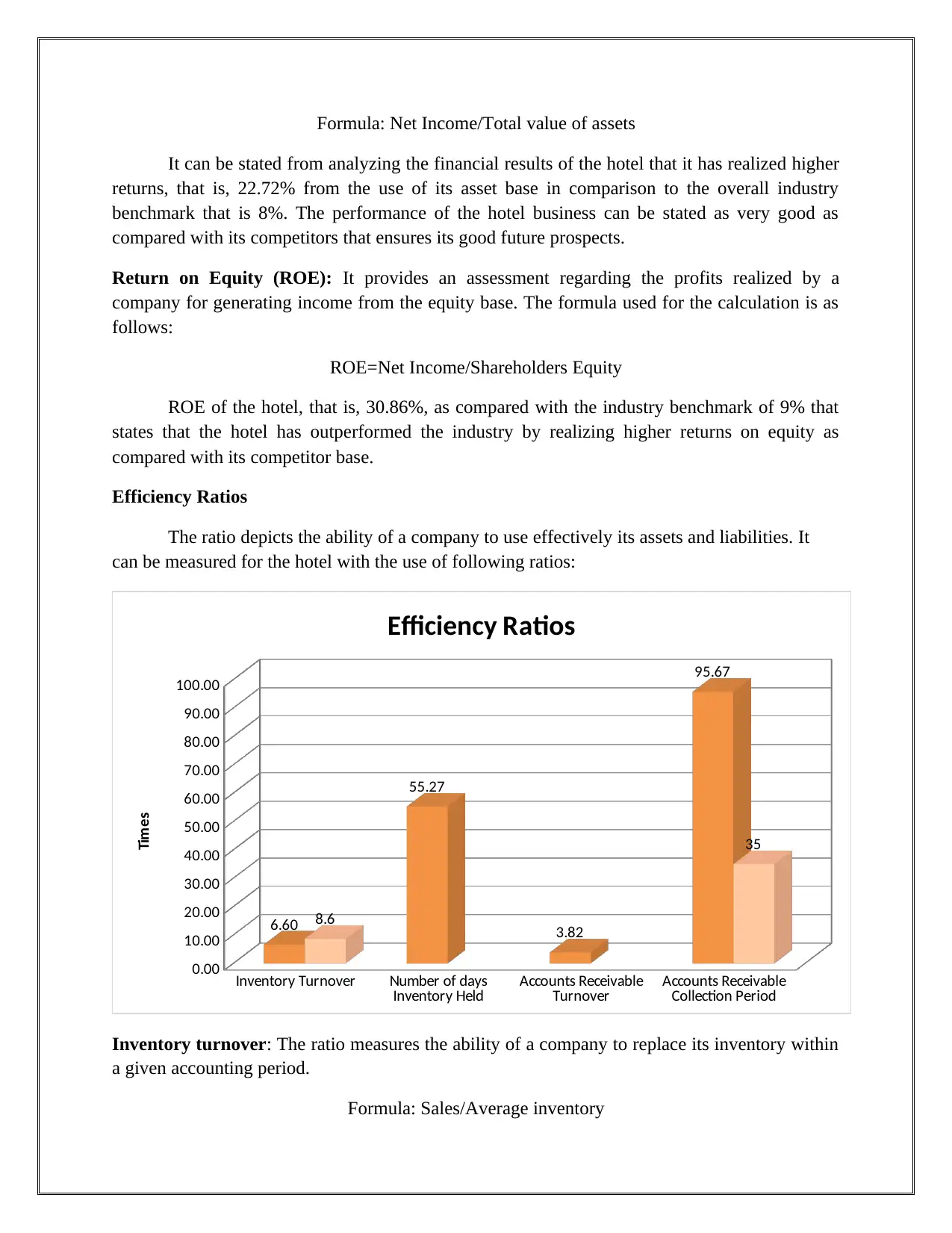

Efficiency Ratios

The ratio depicts the ability of a company to use effectively its assets and liabilities. It

can be measured for the hotel with the use of following ratios:

Inventory Turnover Number of days

Inventory Held Accounts Receivable

Turnover Accounts Receivable

Collection Period

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

6.60

55.27

3.82

95.67

8.6

35

Efficiency Ratios

Times

Inventory turnover: The ratio measures the ability of a company to replace its inventory within

a given accounting period.

Formula: Sales/Average inventory

It can be stated from analyzing the financial results of the hotel that it has realized higher

returns, that is, 22.72% from the use of its asset base in comparison to the overall industry

benchmark that is 8%. The performance of the hotel business can be stated as very good as

compared with its competitors that ensures its good future prospects.

Return on Equity (ROE): It provides an assessment regarding the profits realized by a

company for generating income from the equity base. The formula used for the calculation is as

follows:

ROE=Net Income/Shareholders Equity

ROE of the hotel, that is, 30.86%, as compared with the industry benchmark of 9% that

states that the hotel has outperformed the industry by realizing higher returns on equity as

compared with its competitor base.

Efficiency Ratios

The ratio depicts the ability of a company to use effectively its assets and liabilities. It

can be measured for the hotel with the use of following ratios:

Inventory Turnover Number of days

Inventory Held Accounts Receivable

Turnover Accounts Receivable

Collection Period

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

6.60

55.27

3.82

95.67

8.6

35

Efficiency Ratios

Times

Inventory turnover: The ratio measures the ability of a company to replace its inventory within

a given accounting period.

Formula: Sales/Average inventory

The ratio for the company, that is, 6.60% is significant lower as compared with that of the

industry of 8.60% which means that it need to improve its ability for replacing inventory.

Accounts Receivable collection period: It measures the ability of a company to covert sales into

profits (Arnold, 2013)

Formula: Outstanding Receivables/Total sales

The ratio for the hotel, that is, 95.67% is higher as compared with the industry benchmark

of 35% which means that it need to improve its ability to covert credit sales as compared with the

competitors.

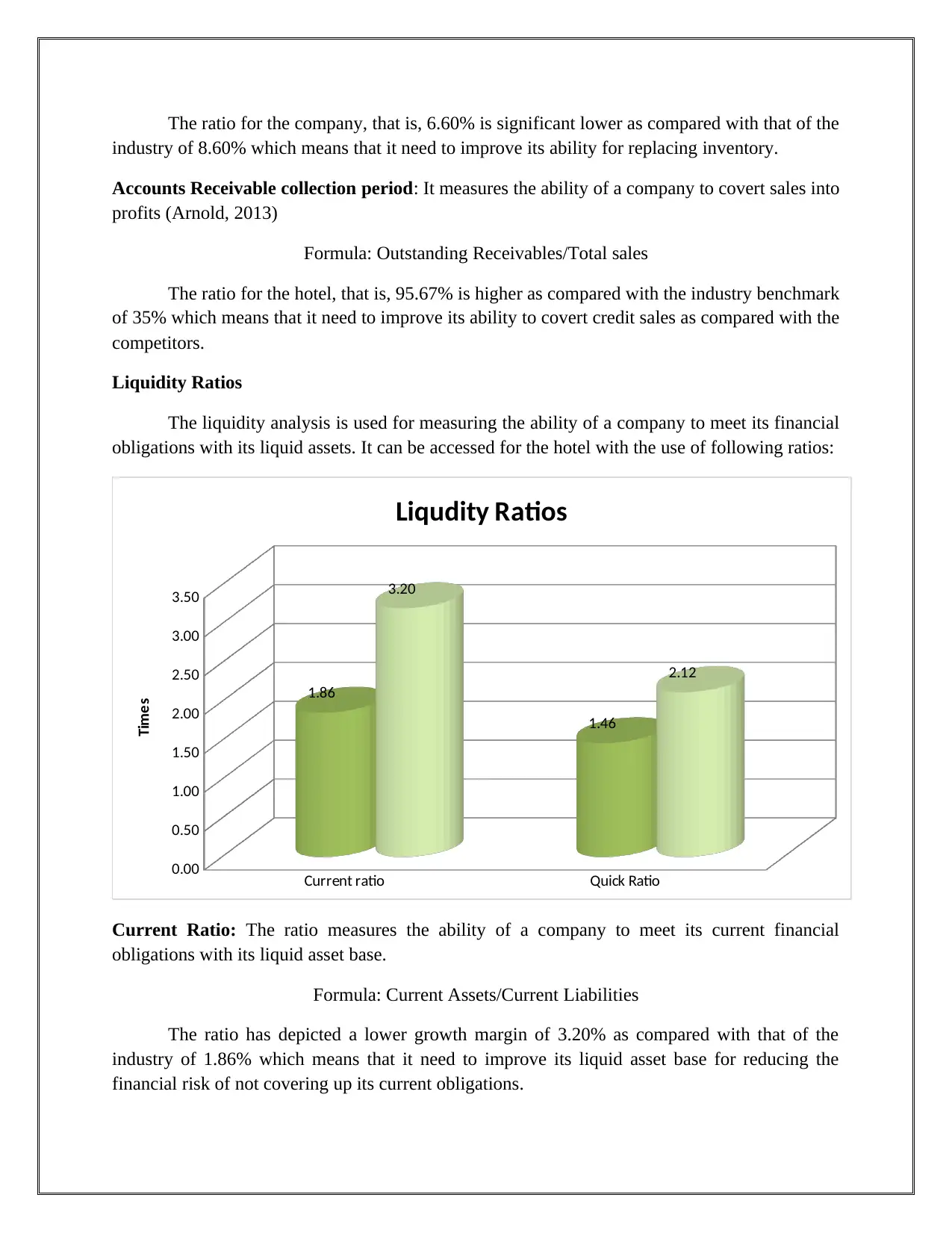

Liquidity Ratios

The liquidity analysis is used for measuring the ability of a company to meet its financial

obligations with its liquid assets. It can be accessed for the hotel with the use of following ratios:

Current ratio Quick Ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1.86

1.46

3.20

2.12

Liqudity Ratios

Times

Current Ratio: The ratio measures the ability of a company to meet its current financial

obligations with its liquid asset base.

Formula: Current Assets/Current Liabilities

The ratio has depicted a lower growth margin of 3.20% as compared with that of the

industry of 1.86% which means that it need to improve its liquid asset base for reducing the

financial risk of not covering up its current obligations.

industry of 8.60% which means that it need to improve its ability for replacing inventory.

Accounts Receivable collection period: It measures the ability of a company to covert sales into

profits (Arnold, 2013)

Formula: Outstanding Receivables/Total sales

The ratio for the hotel, that is, 95.67% is higher as compared with the industry benchmark

of 35% which means that it need to improve its ability to covert credit sales as compared with the

competitors.

Liquidity Ratios

The liquidity analysis is used for measuring the ability of a company to meet its financial

obligations with its liquid assets. It can be accessed for the hotel with the use of following ratios:

Current ratio Quick Ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1.86

1.46

3.20

2.12

Liqudity Ratios

Times

Current Ratio: The ratio measures the ability of a company to meet its current financial

obligations with its liquid asset base.

Formula: Current Assets/Current Liabilities

The ratio has depicted a lower growth margin of 3.20% as compared with that of the

industry of 1.86% which means that it need to improve its liquid asset base for reducing the

financial risk of not covering up its current obligations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick Ratio: The ratio depicts the ability of a company to meet its financial obligations with its

most liquid asset base such as cash in hand, accounts receivable and others.

Formula: (Cash + marketable securities+ Accounts Receivables)/Current liabilities

The hotel has reported a lower quick ratio of 1.46 % as compared with the industrial

benchmark of 2.12% which means that it need to improve its cash flow position for meeting the

current financial obligations (Baker & Powell, 2009).

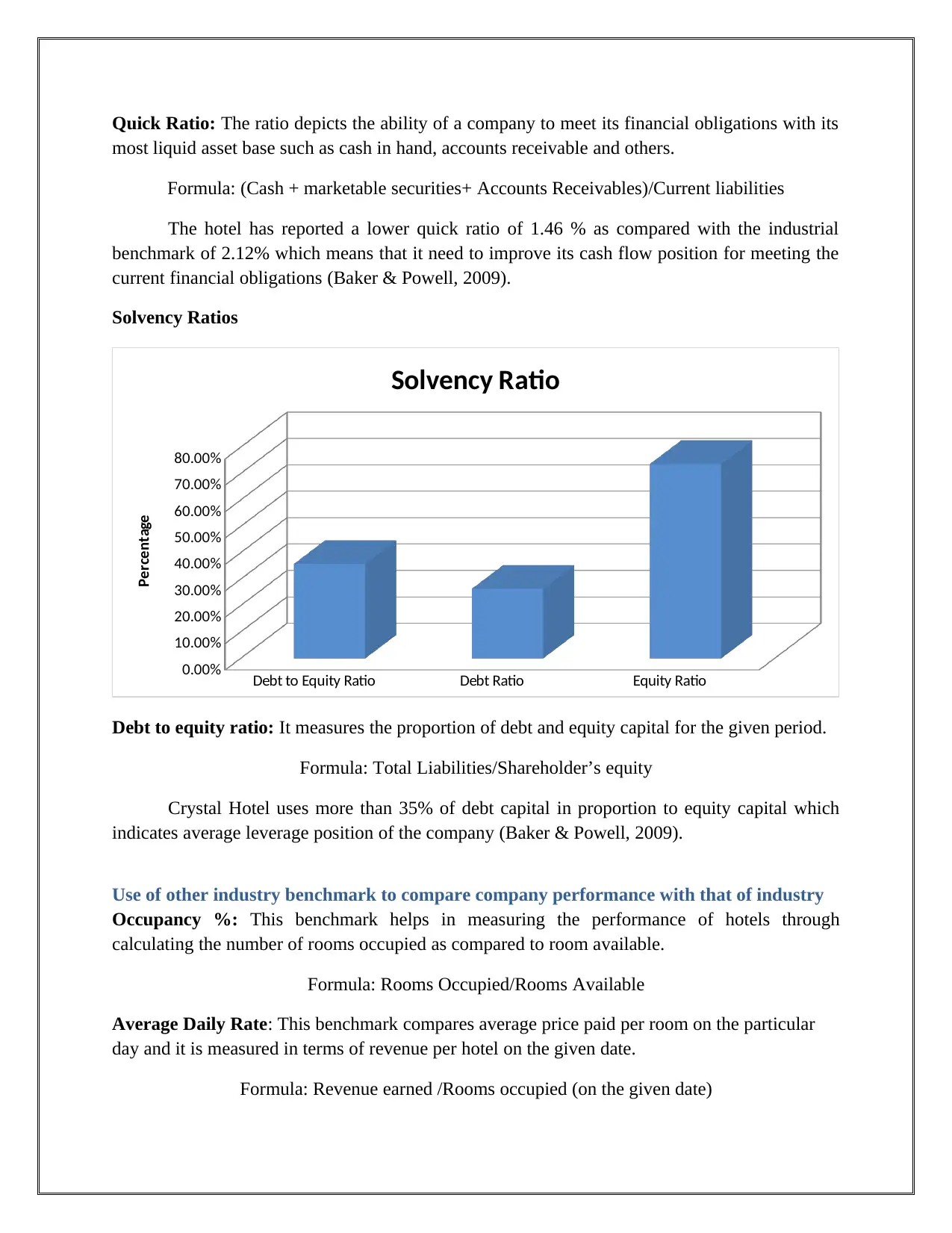

Solvency Ratios

Debt to Equity Ratio Debt Ratio Equity Ratio

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Solvency Ratio

Percentage

Debt to equity ratio: It measures the proportion of debt and equity capital for the given period.

Formula: Total Liabilities/Shareholder’s equity

Crystal Hotel uses more than 35% of debt capital in proportion to equity capital which

indicates average leverage position of the company (Baker & Powell, 2009).

Use of other industry benchmark to compare company performance with that of industry

Occupancy %: This benchmark helps in measuring the performance of hotels through

calculating the number of rooms occupied as compared to room available.

Formula: Rooms Occupied/Rooms Available

Average Daily Rate: This benchmark compares average price paid per room on the particular

day and it is measured in terms of revenue per hotel on the given date.

Formula: Revenue earned /Rooms occupied (on the given date)

most liquid asset base such as cash in hand, accounts receivable and others.

Formula: (Cash + marketable securities+ Accounts Receivables)/Current liabilities

The hotel has reported a lower quick ratio of 1.46 % as compared with the industrial

benchmark of 2.12% which means that it need to improve its cash flow position for meeting the

current financial obligations (Baker & Powell, 2009).

Solvency Ratios

Debt to Equity Ratio Debt Ratio Equity Ratio

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Solvency Ratio

Percentage

Debt to equity ratio: It measures the proportion of debt and equity capital for the given period.

Formula: Total Liabilities/Shareholder’s equity

Crystal Hotel uses more than 35% of debt capital in proportion to equity capital which

indicates average leverage position of the company (Baker & Powell, 2009).

Use of other industry benchmark to compare company performance with that of industry

Occupancy %: This benchmark helps in measuring the performance of hotels through

calculating the number of rooms occupied as compared to room available.

Formula: Rooms Occupied/Rooms Available

Average Daily Rate: This benchmark compares average price paid per room on the particular

day and it is measured in terms of revenue per hotel on the given date.

Formula: Revenue earned /Rooms occupied (on the given date)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue per available room REVPAR: Unlikely this benchmark is similar to average daily

rate but the criteria defined by this ratio is somewhat different as it measures average daily

revenue earned on number of rooms available (Krantz, 2016).

Formula: Total Room Revenue/Rooms available

Conclusion

On the basis of overall comparative analysis Crystal Hotel performance with that of

industry benchmarks it can be said company had performed well as compared to its competitor.

There are some recommendations provided with regards to each ratio and company must

implement those recommendations in order to improve the performance.

rate but the criteria defined by this ratio is somewhat different as it measures average daily

revenue earned on number of rooms available (Krantz, 2016).

Formula: Total Room Revenue/Rooms available

Conclusion

On the basis of overall comparative analysis Crystal Hotel performance with that of

industry benchmarks it can be said company had performed well as compared to its competitor.

There are some recommendations provided with regards to each ratio and company must

implement those recommendations in order to improve the performance.

References

Arnold, G., 2013. Corporate financial management. USA: Pearson Higher Ed.

Baker, K. & Powell, G. 2009. Understanding Financial Management: A Practical Guide. USA:

John Wiley & Sons.

Brigham, F., & Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. & Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. & Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Zimmerman, J.L. & Yahya-Zadeh, M., 2011. Accounting for decision making and control. Issues

in Accounting Education, 26(1), pp.258-259.

Arnold, G., 2013. Corporate financial management. USA: Pearson Higher Ed.

Baker, K. & Powell, G. 2009. Understanding Financial Management: A Practical Guide. USA:

John Wiley & Sons.

Brigham, F., & Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. & Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. & Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Zimmerman, J.L. & Yahya-Zadeh, M., 2011. Accounting for decision making and control. Issues

in Accounting Education, 26(1), pp.258-259.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.