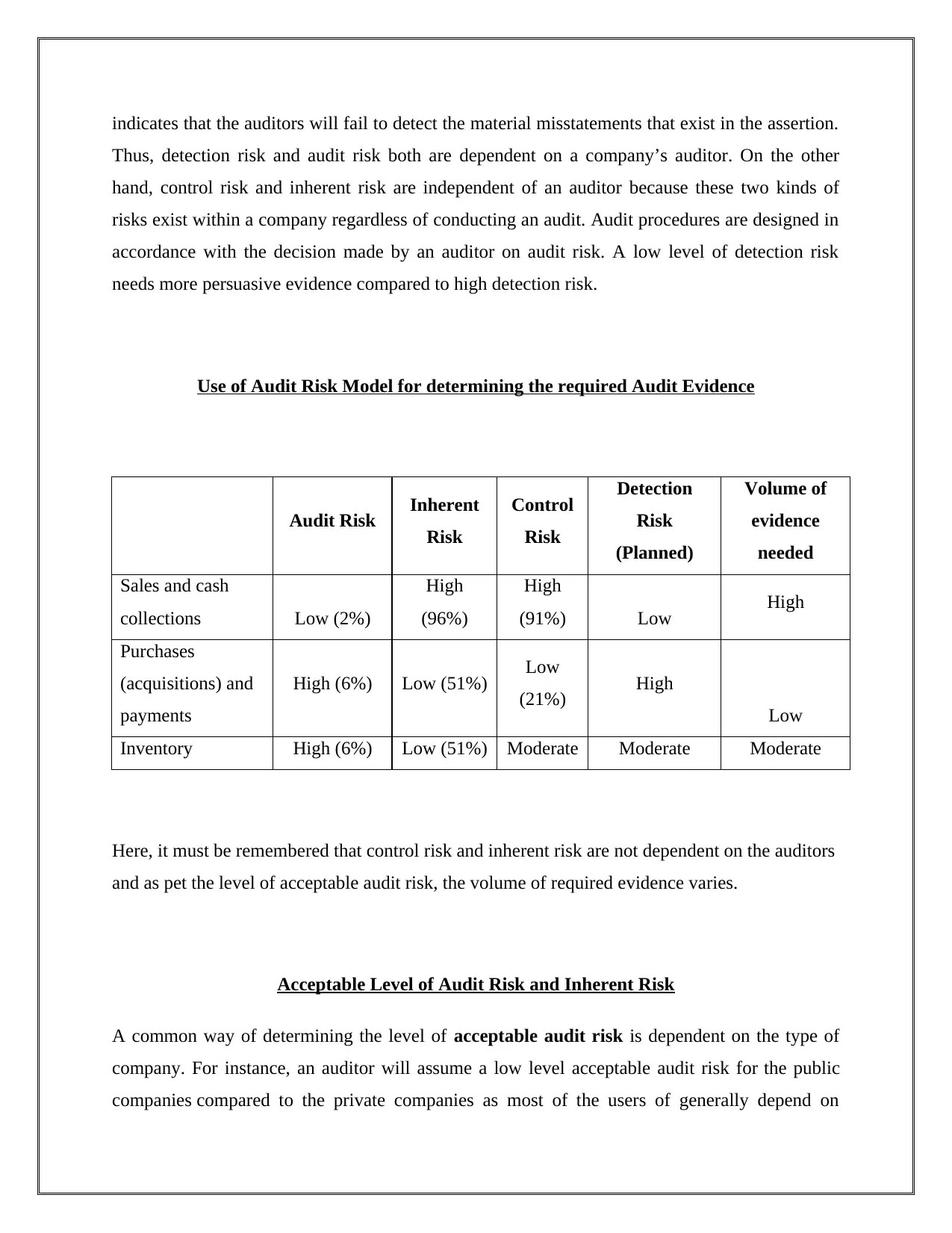

The assignment content is about ABC Limited, an Information Technology company that operates with its own auditors and uses suspected control risk. The acceptable level of audit risk for the company is below or equal to 8%. Oliver identifies both inherent risk and control risk while reviewing the company's financial statements. He assumes the inherent risk is 30% and control risk is 40%, which means the detection risk will be 67%. The total audit risk is calculated to be 8%. The assignment also discusses the model of audit risk, which includes inherent risk, control risk, and detection risk. It highlights that control risk and inherent risk are independent of an auditor, while detection risk depends on the auditor. The acceptable level of audit risk varies based on factors such as the type of company, chances of financial failure, reliance by external users, and the integrity of management.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)