Understanding Marginal Cost in Business Decision-Making

VerifiedAdded on 2019/09/26

|7

|2202

|354

Essay

AI Summary

Marginal cost is a crucial concept in economics that represents the rate at which total cost changes with respect to an increase in production by one unit. It is unrelated to a company's fixed costs and varies depending on the change in variable costs. The marginal cost of producing each additional unit is calculated by subtracting the total cost of producing zero units (fixed costs) from the total cost of producing one unit. The example provided illustrates how marginal cost changes as production volume increases, with some instances of decreasing and then increasing marginal cost. Marginal cost has several features, including its ability to gauge variable cost impact on production volume, classify costs into fixed and variable, and assist in calculating break-even points. However, it also has limitations, such as the potential for inaccurate calculation due to technical difficulties.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BLOG: MARGINAL COST

WHAT IS MARGINAL COST?

WHAT IS MARGINAL COST?

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MARGINAL COST

1st August 2019

In research, production, retail, accounting and other operating activities of an organisation,

a cost stands as the value of money which has been incurred for producing something or

delivering a service. Hence, cost is a one-time element to be used and once it used for the first

time, it becomes unavailable to use anymore. In businesses, cost comes as an element used for

acquiring something i.e. a particular amount of liquid cash spend for acquiring an asset or

something else is treated as a cost. In this particular case, money acts as the input which is gone

in the process of acquiring a tangible thing, sometimes intangible too. This type of acquisition

cost refers as the sum of production cost which is incurred by a product’s original producer.

Though a sum of money is incurred while acquiring an asset (income-generating asset), it is not

treated as cost whereas it is treated as an expense. In more generalised term and considering the

economics, cost refers to a metric which is totaling-up as a result of a particular process.

A particular amount that must be given up or paid for getting something tangible or intangible is

called cost. In business operation, cost stands as a valuation, monetary in form, of effort,

material, resources, utilities and time consumed, cash and risks incurred, as well as the

opportunity gave up in the practice of production of products or services and its delivery. All

kinds of expenses are treated as costs, but not all types of costs are considered as expenses. Cost

or costs are often described on the basis of their applicability and timing. In accounting as well as

in economics, there are a number of costs such as accounting cost, historical cost, opportunity

cost, marginal cost, transaction cost, and sunk cost. All these costs are considered by businesses

while computing cost of products, pricing of final products, profit from business and more.

Moreover, these are also taken into account by a company’s management personnel while they

tend to make business related decisions.

Meaning of Marginal Cost with Example

Marginal cost refers to the change in the total cost which comes from producing or making one

more additional item. It is an additional cost a producer or manufacturer incurs for producing an

1st August 2019

In research, production, retail, accounting and other operating activities of an organisation,

a cost stands as the value of money which has been incurred for producing something or

delivering a service. Hence, cost is a one-time element to be used and once it used for the first

time, it becomes unavailable to use anymore. In businesses, cost comes as an element used for

acquiring something i.e. a particular amount of liquid cash spend for acquiring an asset or

something else is treated as a cost. In this particular case, money acts as the input which is gone

in the process of acquiring a tangible thing, sometimes intangible too. This type of acquisition

cost refers as the sum of production cost which is incurred by a product’s original producer.

Though a sum of money is incurred while acquiring an asset (income-generating asset), it is not

treated as cost whereas it is treated as an expense. In more generalised term and considering the

economics, cost refers to a metric which is totaling-up as a result of a particular process.

A particular amount that must be given up or paid for getting something tangible or intangible is

called cost. In business operation, cost stands as a valuation, monetary in form, of effort,

material, resources, utilities and time consumed, cash and risks incurred, as well as the

opportunity gave up in the practice of production of products or services and its delivery. All

kinds of expenses are treated as costs, but not all types of costs are considered as expenses. Cost

or costs are often described on the basis of their applicability and timing. In accounting as well as

in economics, there are a number of costs such as accounting cost, historical cost, opportunity

cost, marginal cost, transaction cost, and sunk cost. All these costs are considered by businesses

while computing cost of products, pricing of final products, profit from business and more.

Moreover, these are also taken into account by a company’s management personnel while they

tend to make business related decisions.

Meaning of Marginal Cost with Example

Marginal cost refers to the change in the total cost which comes from producing or making one

more additional item. It is an additional cost a producer or manufacturer incurs for producing an

additional unit of output. The marginal cost of production is analyses with the purpose of

determining the exact point at which a company can achieve economies of scale. More

specifically, the decrease or increase in a company’s total cost of production to make only one

more i.e. an additional unit of a product is the marginal cost. Marginal cost is computed by a

company when it becomes able to reach break-even point where the total fixed costs is been

absorbed by the items that are already produced and the direct or variable costs left for being

accounted.

The calculation of marginal cost is done by applying the following formula –

Marginal Cost = Change in total cost / the change in output

Marginal costs elements are variable in nature, which consist of material costs, labour cost along

with an estimated part of a company’s fixed costs related to its products such as selling expenses

and administration overheads. In those companies, where average costs remain fairly constant

i.e. almost fixed, marginal cost becomes equal to the average cost. Moreover, in heavy industries

such as in automobile plants, mines, and airlines which require a large amount of capital

investment and have huge average costs, marginal cost remains very low compared to other

industries which are not involved or require large capital investments. The calculation of the

marginal cost of production is mostly used by manufacturers in order to isolate an optimum level

of production. It is often found, that manufacturers examine the costs of adding an additional unit

to their existing production schedules. The reason behind this is, at some points of time, the

benefit attached to the production of one extra unit of product or service and generating income

from that extra item brings the total cost of production of the product-line down.

In production, marginal cost includes all kinds of costs which use to vary according to the level

or unit of production. For instance, when a company tends to establish a new production unit or

factory with the aim of producing more products, the cost incurred by the company for

establishing the new factory is treated as marginal cost. Furthermore, the amount in relation to

marginal cost uses to vary in accordance with the production volume that is being produced.

There are a number of economic factors responsible for creating an impact on the marginal cost.

These economic factors include information asymmetries, negative and positive externalities,

determining the exact point at which a company can achieve economies of scale. More

specifically, the decrease or increase in a company’s total cost of production to make only one

more i.e. an additional unit of a product is the marginal cost. Marginal cost is computed by a

company when it becomes able to reach break-even point where the total fixed costs is been

absorbed by the items that are already produced and the direct or variable costs left for being

accounted.

The calculation of marginal cost is done by applying the following formula –

Marginal Cost = Change in total cost / the change in output

Marginal costs elements are variable in nature, which consist of material costs, labour cost along

with an estimated part of a company’s fixed costs related to its products such as selling expenses

and administration overheads. In those companies, where average costs remain fairly constant

i.e. almost fixed, marginal cost becomes equal to the average cost. Moreover, in heavy industries

such as in automobile plants, mines, and airlines which require a large amount of capital

investment and have huge average costs, marginal cost remains very low compared to other

industries which are not involved or require large capital investments. The calculation of the

marginal cost of production is mostly used by manufacturers in order to isolate an optimum level

of production. It is often found, that manufacturers examine the costs of adding an additional unit

to their existing production schedules. The reason behind this is, at some points of time, the

benefit attached to the production of one extra unit of product or service and generating income

from that extra item brings the total cost of production of the product-line down.

In production, marginal cost includes all kinds of costs which use to vary according to the level

or unit of production. For instance, when a company tends to establish a new production unit or

factory with the aim of producing more products, the cost incurred by the company for

establishing the new factory is treated as marginal cost. Furthermore, the amount in relation to

marginal cost uses to vary in accordance with the production volume that is being produced.

There are a number of economic factors responsible for creating an impact on the marginal cost.

These economic factors include information asymmetries, negative and positive externalities,

price discrimination and transaction costs. Marginal cost of production is unrelated to a

company’s fixed costs of production. In the economic theory, marginal cost is considered as an

important factor because an organisation which is looking for maximising its profits needs to

produce products up to the point of production where MC (marginal cost) becomes equal to MR

(marginal revenue).

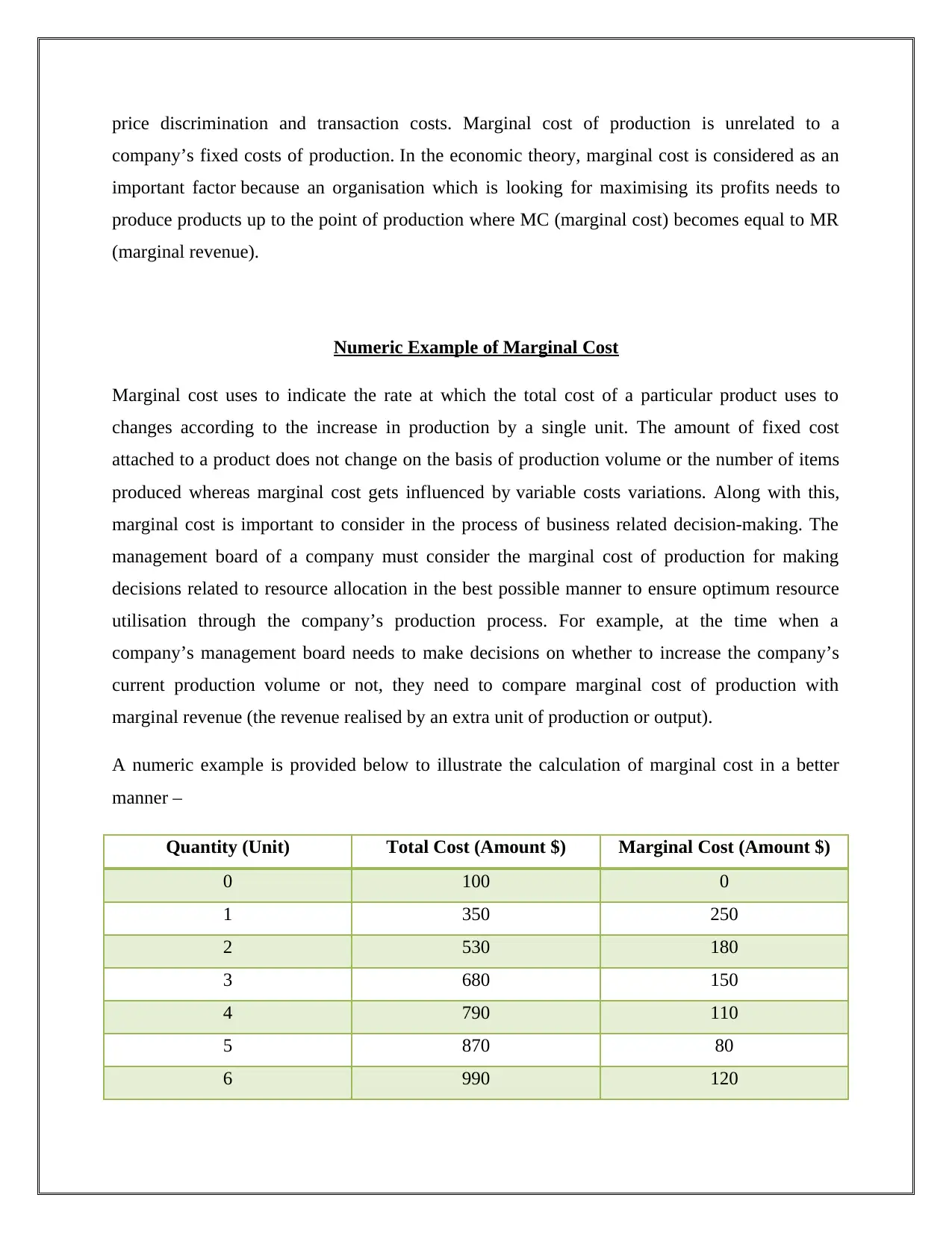

Numeric Example of Marginal Cost

Marginal cost uses to indicate the rate at which the total cost of a particular product uses to

changes according to the increase in production by a single unit. The amount of fixed cost

attached to a product does not change on the basis of production volume or the number of items

produced whereas marginal cost gets influenced by variable costs variations. Along with this,

marginal cost is important to consider in the process of business related decision-making. The

management board of a company must consider the marginal cost of production for making

decisions related to resource allocation in the best possible manner to ensure optimum resource

utilisation through the company’s production process. For example, at the time when a

company’s management board needs to make decisions on whether to increase the company’s

current production volume or not, they need to compare marginal cost of production with

marginal revenue (the revenue realised by an extra unit of production or output).

A numeric example is provided below to illustrate the calculation of marginal cost in a better

manner –

Quantity (Unit) Total Cost (Amount $) Marginal Cost (Amount $)

0 100 0

1 350 250

2 530 180

3 680 150

4 790 110

5 870 80

6 990 120

company’s fixed costs of production. In the economic theory, marginal cost is considered as an

important factor because an organisation which is looking for maximising its profits needs to

produce products up to the point of production where MC (marginal cost) becomes equal to MR

(marginal revenue).

Numeric Example of Marginal Cost

Marginal cost uses to indicate the rate at which the total cost of a particular product uses to

changes according to the increase in production by a single unit. The amount of fixed cost

attached to a product does not change on the basis of production volume or the number of items

produced whereas marginal cost gets influenced by variable costs variations. Along with this,

marginal cost is important to consider in the process of business related decision-making. The

management board of a company must consider the marginal cost of production for making

decisions related to resource allocation in the best possible manner to ensure optimum resource

utilisation through the company’s production process. For example, at the time when a

company’s management board needs to make decisions on whether to increase the company’s

current production volume or not, they need to compare marginal cost of production with

marginal revenue (the revenue realised by an extra unit of production or output).

A numeric example is provided below to illustrate the calculation of marginal cost in a better

manner –

Quantity (Unit) Total Cost (Amount $) Marginal Cost (Amount $)

0 100 0

1 350 250

2 530 180

3 680 150

4 790 110

5 870 80

6 990 120

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

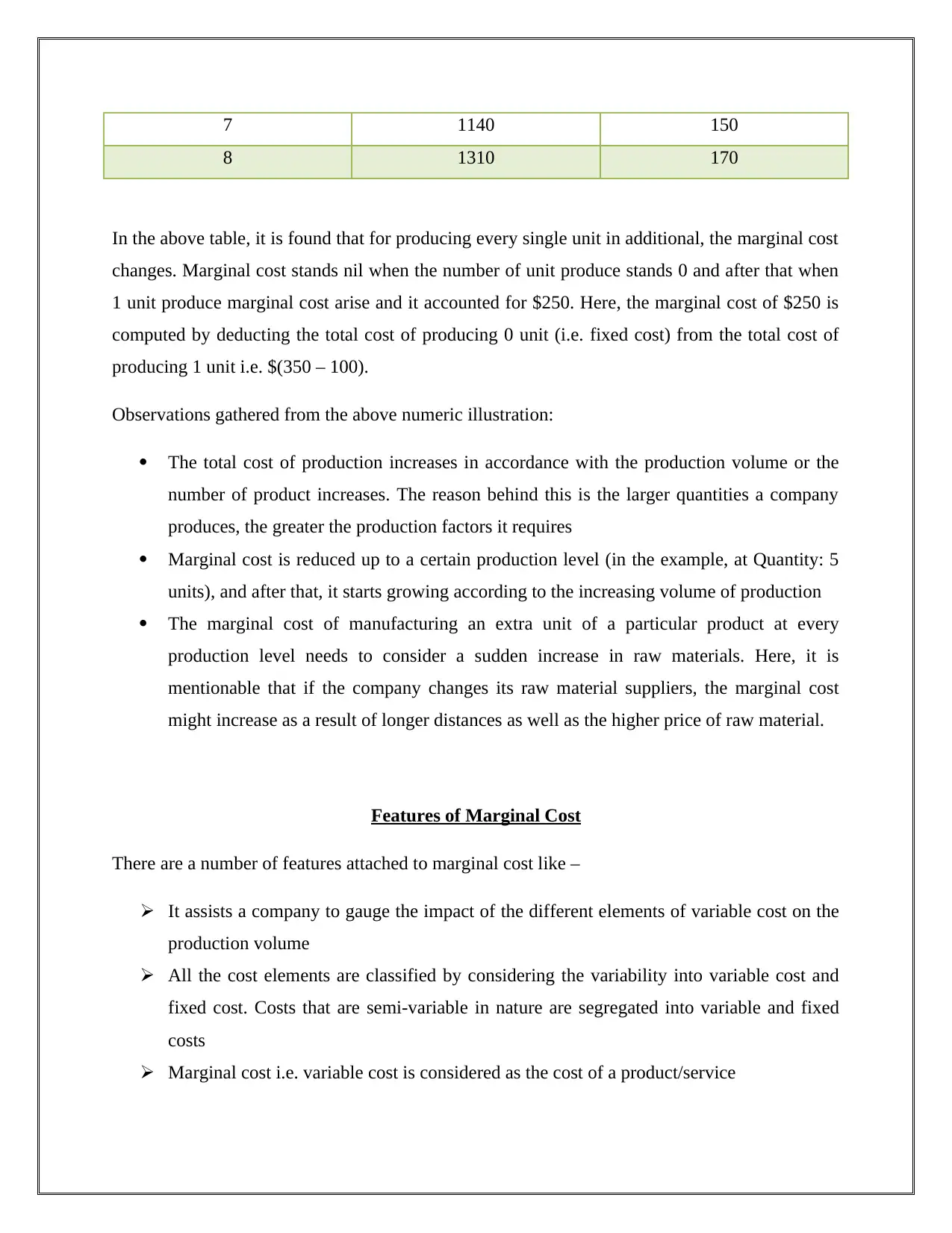

7 1140 150

8 1310 170

In the above table, it is found that for producing every single unit in additional, the marginal cost

changes. Marginal cost stands nil when the number of unit produce stands 0 and after that when

1 unit produce marginal cost arise and it accounted for $250. Here, the marginal cost of $250 is

computed by deducting the total cost of producing 0 unit (i.e. fixed cost) from the total cost of

producing 1 unit i.e. $(350 – 100).

Observations gathered from the above numeric illustration:

The total cost of production increases in accordance with the production volume or the

number of product increases. The reason behind this is the larger quantities a company

produces, the greater the production factors it requires

Marginal cost is reduced up to a certain production level (in the example, at Quantity: 5

units), and after that, it starts growing according to the increasing volume of production

The marginal cost of manufacturing an extra unit of a particular product at every

production level needs to consider a sudden increase in raw materials. Here, it is

mentionable that if the company changes its raw material suppliers, the marginal cost

might increase as a result of longer distances as well as the higher price of raw material.

Features of Marginal Cost

There are a number of features attached to marginal cost like –

It assists a company to gauge the impact of the different elements of variable cost on the

production volume

All the cost elements are classified by considering the variability into variable cost and

fixed cost. Costs that are semi-variable in nature are segregated into variable and fixed

costs

Marginal cost i.e. variable cost is considered as the cost of a product/service

8 1310 170

In the above table, it is found that for producing every single unit in additional, the marginal cost

changes. Marginal cost stands nil when the number of unit produce stands 0 and after that when

1 unit produce marginal cost arise and it accounted for $250. Here, the marginal cost of $250 is

computed by deducting the total cost of producing 0 unit (i.e. fixed cost) from the total cost of

producing 1 unit i.e. $(350 – 100).

Observations gathered from the above numeric illustration:

The total cost of production increases in accordance with the production volume or the

number of product increases. The reason behind this is the larger quantities a company

produces, the greater the production factors it requires

Marginal cost is reduced up to a certain production level (in the example, at Quantity: 5

units), and after that, it starts growing according to the increasing volume of production

The marginal cost of manufacturing an extra unit of a particular product at every

production level needs to consider a sudden increase in raw materials. Here, it is

mentionable that if the company changes its raw material suppliers, the marginal cost

might increase as a result of longer distances as well as the higher price of raw material.

Features of Marginal Cost

There are a number of features attached to marginal cost like –

It assists a company to gauge the impact of the different elements of variable cost on the

production volume

All the cost elements are classified by considering the variability into variable cost and

fixed cost. Costs that are semi-variable in nature are segregated into variable and fixed

costs

Marginal cost i.e. variable cost is considered as the cost of a product/service

Stocks that include work-in-progress and finished goods are valued by considering

marginal costs attached to them

Break-even point is known as a part of marginal cost

The profitability of a company associated with a product is computed on the basis of

contribution and contribution is computed by deducting marginal cost of a product from

the selling price of that product

Marginal cost helps in conducting cost-volume-profit (CVP) analysis

Advantages and Disadvantages of Marginal Cost

Advantages of marginal cost are –

The technique of identifying marginal cost element is easy and simple to understand

because it does not include any complexity of apportioning fixed costs

It uses to avoid the carry-forward of a part of fixed overhead attached to the current

period's production cost to the next or subsequent period.

It makes cost comparisons more meaningful

Marginal cost uses to provide useful data and information to the management of a

company in order to help it in managerial decision-making

It shows the fluctuation of sales and its impact on a company's profit in a clear manner

The stock of work-in-progress and finished goods are valued by considering marginal

cost remain uniform

It assists a company to make profit planning

It helps the management to find out both break-even point and break-even ratio

It helps the management of a company to gauge the different departments’ performance

It does not include any problem attached to under or over-absorption of production

oriented overhead costs

It helps management in budgetary control and standard costing

It uses to establish a clear and understandable relationship between sales, the volume of

output, cost, and break-even analysis

marginal costs attached to them

Break-even point is known as a part of marginal cost

The profitability of a company associated with a product is computed on the basis of

contribution and contribution is computed by deducting marginal cost of a product from

the selling price of that product

Marginal cost helps in conducting cost-volume-profit (CVP) analysis

Advantages and Disadvantages of Marginal Cost

Advantages of marginal cost are –

The technique of identifying marginal cost element is easy and simple to understand

because it does not include any complexity of apportioning fixed costs

It uses to avoid the carry-forward of a part of fixed overhead attached to the current

period's production cost to the next or subsequent period.

It makes cost comparisons more meaningful

Marginal cost uses to provide useful data and information to the management of a

company in order to help it in managerial decision-making

It shows the fluctuation of sales and its impact on a company's profit in a clear manner

The stock of work-in-progress and finished goods are valued by considering marginal

cost remain uniform

It assists a company to make profit planning

It helps the management to find out both break-even point and break-even ratio

It helps the management of a company to gauge the different departments’ performance

It does not include any problem attached to under or over-absorption of production

oriented overhead costs

It helps management in budgetary control and standard costing

It uses to establish a clear and understandable relationship between sales, the volume of

output, cost, and break-even analysis

Disadvantages of marginal cost are –

Marginal cost is considered as a variable cost and segregation of a product’s production

costs into variable and fixed elements involve technical difficulty which often leads a

company to compute the marginal cost of a product inaccurately

Cost control can be done in a better way in standard costing or budgetary control

The practice of computing marginal cost is not been applied in contract costing because

in contract costing the cost of work-in-progress always stands high

Pricing decisions are not been made only by considering marginal cost and contribution

which is computed by deducting the marginal cost of a product from its selling price

Segregation of costs in variable and fixed cost become difficult in long-run which causes

difficulties in computing the marginal cost

The Way Marginal Cost of Production Works

Production costs include fixed costs as well as variable costs. Here, variable cost stands as the

costs elements that are required for producing every single unit of a product and fixed costs stand

as the overhead costs which are distributed across the total unit of output. For instance, consider

a shoe maker. For producing each pair of shoe the show maker requires raw materials like fabric

and plastic which costs $0.75 in total. The show maker incurs fixed costs of $100 per month. If

the shoe maker makes 50 pair of shoe in every month, then the show maker needs to consider $2

($100 / $50) as fixed costs per unit i.e. per pair of shoe. Here, the total cost per pair of shoe

(including the cost of fabric and plastic) would be $2.75 [$0.75 + ($100/50)]. But if the shoe

maker cranked up the production volume and starts producing 100 pair of shoe every month,

then for per pair of shoe the shoe maker will start incurring $1 as fixed costs. The reason behind

this is that fixed costs are distributed across every unit of production. In this situation, the

total cost per pair of shoe will drop and it becomes $1.75 [$0.75 + ($100/100)]. In this particular

situation, by increasing the volume of production the shoe maker becomes able to reduce

marginal costs of production.

Marginal cost is considered as a variable cost and segregation of a product’s production

costs into variable and fixed elements involve technical difficulty which often leads a

company to compute the marginal cost of a product inaccurately

Cost control can be done in a better way in standard costing or budgetary control

The practice of computing marginal cost is not been applied in contract costing because

in contract costing the cost of work-in-progress always stands high

Pricing decisions are not been made only by considering marginal cost and contribution

which is computed by deducting the marginal cost of a product from its selling price

Segregation of costs in variable and fixed cost become difficult in long-run which causes

difficulties in computing the marginal cost

The Way Marginal Cost of Production Works

Production costs include fixed costs as well as variable costs. Here, variable cost stands as the

costs elements that are required for producing every single unit of a product and fixed costs stand

as the overhead costs which are distributed across the total unit of output. For instance, consider

a shoe maker. For producing each pair of shoe the show maker requires raw materials like fabric

and plastic which costs $0.75 in total. The show maker incurs fixed costs of $100 per month. If

the shoe maker makes 50 pair of shoe in every month, then the show maker needs to consider $2

($100 / $50) as fixed costs per unit i.e. per pair of shoe. Here, the total cost per pair of shoe

(including the cost of fabric and plastic) would be $2.75 [$0.75 + ($100/50)]. But if the shoe

maker cranked up the production volume and starts producing 100 pair of shoe every month,

then for per pair of shoe the shoe maker will start incurring $1 as fixed costs. The reason behind

this is that fixed costs are distributed across every unit of production. In this situation, the

total cost per pair of shoe will drop and it becomes $1.75 [$0.75 + ($100/100)]. In this particular

situation, by increasing the volume of production the shoe maker becomes able to reduce

marginal costs of production.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.