Bond Covenants in the Italian Legal System: An Analysis

VerifiedAdded on 2023/05/30

|59

|28850

|117

AI Summary

This study proposes an analysis of bond covenants in the Italian legal system, their benefits, and possible reasons for their adoption. The study also provides an overview of bond features and current regulations for bondholder protection.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INTRODUZIONE + PRIMA PARTE CAPITOLO 1

Introduction

This study proposes that the introductory analysis of a particular category of contractual clauses still

uncommon in the Italian legal system, contrary to international financial practices, particularly Anglo-Saxon,

where the so-called bond covenants characterize many of the statutes of issue of bonds .

The favor of those same contractual instruments in markets across the border, finds its justification in the

greater control that they are able to provide bondholders with regard to the issuing company, forcing the

latter to advance compensation for the loan or the payment of a best interests if the conditions attached to the

loan are not met. The benefit associated with the adoption of this contractual technique is twofold: the more

intense assurance gained from creditors is to pay a smaller financial commitment of the company, which will

to satisfy their need for financing on better terms than those normally taken.

The process of investigation opens presented outlining a brief glimpse of the current regulations for the

protection of the bondholder investor unprofessional, fruit of the union, perhaps not always consistent, the

recent reform of company law and the subsequent legislative intervention conducted in the protection

savings.

In connection with the outlined legal framework, the second section will address the issue of the possible

reasons of interest to the adoption of the bond covenants within the Italian financial scene, with special

attention to the singularity and the unique needs presented by the national economy.

AN OVERVIEW ON BOND COVENANTS

Bond's Features

Following the entry into force of the new company law, the traditional dichotomy between equity capital and

borrowed capital does not appear to be numbered among the key points of the regulatory framework of the

spa's many ties that unite the current discipline focus on action, to bonds and other financial vehicles

envisaged by the reform in fact they tend to align the positions of the subject in various capacities participate

collective undertaking, making it difficult for a reconstruction of the profiles that characterize these figures

clearly before surgery operated by the news. Excluding dating sharing experiences from the specialized

agencies in the provision of industrial credit, as well as the fracture accomplished with the introduction of

savings shares and drift aticipi titles of 70 years, the Italian corporate law has always kept separate different

role assumed by the creditor of the corporation than the shareholder thereof; Since 2003 this certainty seems

however definitely crack, not only due to a more intense shade of the figure of the shareholder, operated by

the insertion of share classes particularly flexible and adaptable, but also thanks to the introduction of special

funds and, above all, "chameleon-like" instruments referred to in the sixth co. art. 2346 cc, ie securities

actually endowed with the ability to take on much of its shades of shares as of the bonds. The Italian

Introduction

This study proposes that the introductory analysis of a particular category of contractual clauses still

uncommon in the Italian legal system, contrary to international financial practices, particularly Anglo-Saxon,

where the so-called bond covenants characterize many of the statutes of issue of bonds .

The favor of those same contractual instruments in markets across the border, finds its justification in the

greater control that they are able to provide bondholders with regard to the issuing company, forcing the

latter to advance compensation for the loan or the payment of a best interests if the conditions attached to the

loan are not met. The benefit associated with the adoption of this contractual technique is twofold: the more

intense assurance gained from creditors is to pay a smaller financial commitment of the company, which will

to satisfy their need for financing on better terms than those normally taken.

The process of investigation opens presented outlining a brief glimpse of the current regulations for the

protection of the bondholder investor unprofessional, fruit of the union, perhaps not always consistent, the

recent reform of company law and the subsequent legislative intervention conducted in the protection

savings.

In connection with the outlined legal framework, the second section will address the issue of the possible

reasons of interest to the adoption of the bond covenants within the Italian financial scene, with special

attention to the singularity and the unique needs presented by the national economy.

AN OVERVIEW ON BOND COVENANTS

Bond's Features

Following the entry into force of the new company law, the traditional dichotomy between equity capital and

borrowed capital does not appear to be numbered among the key points of the regulatory framework of the

spa's many ties that unite the current discipline focus on action, to bonds and other financial vehicles

envisaged by the reform in fact they tend to align the positions of the subject in various capacities participate

collective undertaking, making it difficult for a reconstruction of the profiles that characterize these figures

clearly before surgery operated by the news. Excluding dating sharing experiences from the specialized

agencies in the provision of industrial credit, as well as the fracture accomplished with the introduction of

savings shares and drift aticipi titles of 70 years, the Italian corporate law has always kept separate different

role assumed by the creditor of the corporation than the shareholder thereof; Since 2003 this certainty seems

however definitely crack, not only due to a more intense shade of the figure of the shareholder, operated by

the insertion of share classes particularly flexible and adaptable, but also thanks to the introduction of special

funds and, above all, "chameleon-like" instruments referred to in the sixth co. art. 2346 cc, ie securities

actually endowed with the ability to take on much of its shades of shares as of the bonds. The Italian

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

company law has always kept separate different role assumed by the creditor of the corporation than the

shareholder thereof; Since 2003 this certainty seems however definitely crack, not only due to a more intense

shade of the figure of the shareholder, operated by the insertion of share classes particularly flexible and

adaptable, but also thanks to the introduction of special funds and, above all, "chameleon-like" instruments

referred to in the sixth co. art. 2346 cc, ie securities actually endowed with the ability to take on much of its

shades of shares as of the bonds. The Italian company law has always kept separate different role assumed

by the creditor of the corporation than the shareholder thereof; Since 2003 this certainty seems however

definitely crack, not only due to a more intense shade of the figure of the shareholder, operated by the

insertion of share classes particularly flexible and adaptable, but also thanks to the introduction of special

funds and, above all, "chameleon-like" instruments referred to in the sixth co. art. 2346 cc, ie securities

actually endowed with the ability to take on much of its shades of shares as of the bonds. not only due to a

more intense shade of the figure of the shareholder, operated by the insertion of share classes particularly

flexible and adaptable, but also thanks to the introduction of special funds and, above all, the "chameleon-

like" instruments referred to in the sixth co . art. 2346 cc, ie securities actually endowed with the ability to

take on much of its shades of shares as of the bonds. not only due to a more intense shade of the figure of the

shareholder, operated by the insertion of share classes particularly flexible and adaptable, but also thanks to

the introduction of special funds and, above all, the "chameleon-like" instruments referred to in the sixth co .

art. 2346 cc, ie securities actually endowed with the ability to take on much of its shades of shares as of the

bonds.

In this context of reform measures, the regulation of bonds do not think I deserved - at least until the

worsening of the known financial scandals - a particular attention by the legislator. Already through the

second corrective action operated the company reform, the legislator seems to have partly changed the

content of the initial project, trying, on the one hand, to confirm the possible government intervention in the

economy in the form of government guarantees to issue bonds, on the other, to defend the weak positions of

the non-professional investors through the changes made by the first Legislative Decree no. 310 of 28

December 2004, now partly revised and relocated from the savings contained in d.lgs reform. 262 of 28

December 2005. Despite undergoing substantial alterations, from the point of view of the possible overlap of

the holding company plans adopted by other financial instruments of the spa, the bonds do not come

however to the "excesses" dictated by the sixth co. art. 2346 cc, while maintaining substantially the nature of

debt securities, albeit postergabili or redeemable.

Among the actions undertaken at the seventh section of the fifth title, however it occupies a prominent place

in accordance with the new co. art. 2412 cc, which normally provides for the possible exceedance of the

emission limit charged to the spa not acceding to the regulated market to the cost of the guarantee assumed

by the financial intermediary subject to prudential supervision first subscriber - or even later? - in favor of

the next non-professional investors borrowers. The forecast is clearly to encourage an expansion of the

Italian high-yield bond market cd, seeking a difficult balance between the requirements for diversification of

shareholder thereof; Since 2003 this certainty seems however definitely crack, not only due to a more intense

shade of the figure of the shareholder, operated by the insertion of share classes particularly flexible and

adaptable, but also thanks to the introduction of special funds and, above all, "chameleon-like" instruments

referred to in the sixth co. art. 2346 cc, ie securities actually endowed with the ability to take on much of its

shades of shares as of the bonds. The Italian company law has always kept separate different role assumed

by the creditor of the corporation than the shareholder thereof; Since 2003 this certainty seems however

definitely crack, not only due to a more intense shade of the figure of the shareholder, operated by the

insertion of share classes particularly flexible and adaptable, but also thanks to the introduction of special

funds and, above all, "chameleon-like" instruments referred to in the sixth co. art. 2346 cc, ie securities

actually endowed with the ability to take on much of its shades of shares as of the bonds. not only due to a

more intense shade of the figure of the shareholder, operated by the insertion of share classes particularly

flexible and adaptable, but also thanks to the introduction of special funds and, above all, the "chameleon-

like" instruments referred to in the sixth co . art. 2346 cc, ie securities actually endowed with the ability to

take on much of its shades of shares as of the bonds. not only due to a more intense shade of the figure of the

shareholder, operated by the insertion of share classes particularly flexible and adaptable, but also thanks to

the introduction of special funds and, above all, the "chameleon-like" instruments referred to in the sixth co .

art. 2346 cc, ie securities actually endowed with the ability to take on much of its shades of shares as of the

bonds.

In this context of reform measures, the regulation of bonds do not think I deserved - at least until the

worsening of the known financial scandals - a particular attention by the legislator. Already through the

second corrective action operated the company reform, the legislator seems to have partly changed the

content of the initial project, trying, on the one hand, to confirm the possible government intervention in the

economy in the form of government guarantees to issue bonds, on the other, to defend the weak positions of

the non-professional investors through the changes made by the first Legislative Decree no. 310 of 28

December 2004, now partly revised and relocated from the savings contained in d.lgs reform. 262 of 28

December 2005. Despite undergoing substantial alterations, from the point of view of the possible overlap of

the holding company plans adopted by other financial instruments of the spa, the bonds do not come

however to the "excesses" dictated by the sixth co. art. 2346 cc, while maintaining substantially the nature of

debt securities, albeit postergabili or redeemable.

Among the actions undertaken at the seventh section of the fifth title, however it occupies a prominent place

in accordance with the new co. art. 2412 cc, which normally provides for the possible exceedance of the

emission limit charged to the spa not acceding to the regulated market to the cost of the guarantee assumed

by the financial intermediary subject to prudential supervision first subscriber - or even later? - in favor of

the next non-professional investors borrowers. The forecast is clearly to encourage an expansion of the

Italian high-yield bond market cd, seeking a difficult balance between the requirements for diversification of

credit sources of non-listed companies of limited size and the need for better protection of investors that

direct part of their assets to sub-entry of such financial instruments. While shared aim, the practical side - in

particular interest in view of the financial intermediary - the norm, however, reveals the considerable

roughness; It seems all too obvious, in fact, as the endorsement imposed on this subject constitutes an

insurmountable obstacle to the fulfillment of any IPO enlarged to the public of non-professional investors,

thereby heavily delimiting the area of financing small to medium businesses ,

The application problems related to the intermediary's warranty does not appear to have been warned by the

legislature, which, in contrast, wanted to repeat the same mechanism of protection even in art. 11, according

to co., Lett. c) of Legislative Decree no. 262 of 2005: despite having the advantage of having repealed the

last co. art. 2412 cc, the savings reform has thus entered into the TUF a new provision, Article. 100-te,

which is aligned in large part to the second co. art. 2412 cc The amendment made specularly provides that,

without prejudice to the codicistic limit of capital and reserves for unlisted emissions, the guarantee of the

first subscriber in favor of borrowers next savers extends to all securities offered to the public only by

professional investors for one year from the placement, even if carried out abroad n. The dictated closing

repeats the questions already raised at with regard to Article doctrine. 2412 cc; doubts intended to scupper

the hypothesis of an immediate redeployment between

the public of the securities having a denomination of less than € 50,000, according to the established patterns

of private placements, normally made by a consortium of banks led by one or more lead managers.

It should also be highlighted by the reading of Article. 100-bis of the Consolidated Finance Act, as the norm,

while referring to the entire category of financial instruments, imposes a guarantee limited to "... the

solvency of the issuer ...", thereby including the debt and excluding evidently equity. The solution is

consistent with the traditional division between risk capital and credit, only by giving owners the latter a

more intensive protection as external social enterprise subjects; the status of partner, or positions anyway

participatory provided by the reform, even if they are based on a minimal stake, in fact justify the idea that

the rights related to the same give the possibility (even theoretical) to address the business dynamics, or at

least , provide adequate supervisory tools.

Possible reasons for interest in the study of the clauses covenants

The obvious benefit related to a more closely with corporate events has long led foreign financial practice, in

particular the US high yield bond market, to develop so-called bond covenants, or insert clauses in the loan

agreements bond with the function to impose conditions to the loan in favor of the holders of the debt

securities. This solution allows the mass of creditors of the company to more thoroughly monitor the trend of

the undertaking funded, as well as to target under certain aspects of the same, obtaining the guarantee of

early repayment or a higher rate of interest due to the occurrence of the condition. In economic terms,

direct part of their assets to sub-entry of such financial instruments. While shared aim, the practical side - in

particular interest in view of the financial intermediary - the norm, however, reveals the considerable

roughness; It seems all too obvious, in fact, as the endorsement imposed on this subject constitutes an

insurmountable obstacle to the fulfillment of any IPO enlarged to the public of non-professional investors,

thereby heavily delimiting the area of financing small to medium businesses ,

The application problems related to the intermediary's warranty does not appear to have been warned by the

legislature, which, in contrast, wanted to repeat the same mechanism of protection even in art. 11, according

to co., Lett. c) of Legislative Decree no. 262 of 2005: despite having the advantage of having repealed the

last co. art. 2412 cc, the savings reform has thus entered into the TUF a new provision, Article. 100-te,

which is aligned in large part to the second co. art. 2412 cc The amendment made specularly provides that,

without prejudice to the codicistic limit of capital and reserves for unlisted emissions, the guarantee of the

first subscriber in favor of borrowers next savers extends to all securities offered to the public only by

professional investors for one year from the placement, even if carried out abroad n. The dictated closing

repeats the questions already raised at with regard to Article doctrine. 2412 cc; doubts intended to scupper

the hypothesis of an immediate redeployment between

the public of the securities having a denomination of less than € 50,000, according to the established patterns

of private placements, normally made by a consortium of banks led by one or more lead managers.

It should also be highlighted by the reading of Article. 100-bis of the Consolidated Finance Act, as the norm,

while referring to the entire category of financial instruments, imposes a guarantee limited to "... the

solvency of the issuer ...", thereby including the debt and excluding evidently equity. The solution is

consistent with the traditional division between risk capital and credit, only by giving owners the latter a

more intensive protection as external social enterprise subjects; the status of partner, or positions anyway

participatory provided by the reform, even if they are based on a minimal stake, in fact justify the idea that

the rights related to the same give the possibility (even theoretical) to address the business dynamics, or at

least , provide adequate supervisory tools.

Possible reasons for interest in the study of the clauses covenants

The obvious benefit related to a more closely with corporate events has long led foreign financial practice, in

particular the US high yield bond market, to develop so-called bond covenants, or insert clauses in the loan

agreements bond with the function to impose conditions to the loan in favor of the holders of the debt

securities. This solution allows the mass of creditors of the company to more thoroughly monitor the trend of

the undertaking funded, as well as to target under certain aspects of the same, obtaining the guarantee of

early repayment or a higher rate of interest due to the occurrence of the condition. In economic terms,

For a comparison of the market for speculative debt of America and Europe, see. C. and A. Cesari Rusconi,

International context, II in the corporate bond market in Italy, edited by C, M, Pinardi, cit., P. 32 ss. and 45 s.

The figure was confirmed by M. Bradley and MR Roberts, bond covenants priced Are ?, Fuqua School of

Business, Duke University, November 2004, available at websitewww.ideas.repec.org, P. 4. AA. We put in

evidence as "We find a negative relation between the inclusion of a bond covenants and the promised yield

on corporate debt."

"In the US, lenders who wish to protect themselves from opportunistic behavior of shareholders must rely on

the contractual instrument"; Enriques so L. and J. Macey, venture capital and creditor protection Collection:

a radical critique of the European rules on share capital, in "Riv. Soc. ", 2002, I, p. 86. Notes however R.

Rordorf, importance and limits of information in the financial markets, "Jur. comm. ", 2003, I, p. 774, as

"self-regulation is able to give real benefits only when it succeeds in harmoniously coordinating with the

primary sources general law [...] carving out their own space in the interstices that that sort should be the

guarantee." On this point, see. Also F. Fimmanò, cit., p. 98 ff .; MC Brescia Morra, financing of limited

liability companies and debt securities,www.dircomm.it2003, XI, 2.

In addition to satisfying this primary financial reason, the adoption of clauses within the Italian system could

find specific reasons for interest in the peculiarities of our economy. Their use might indeed be strongly

encouraged by the underwriters intermediaries are obliged to guarantee the solvency for the next assigns

savers: it is clear that the introduction of such clauses would be to reduce the financial risk suffered by the

borrower 'guarantor', you would see thus better secured against the issuer for at least the first year of life of

the title - or for the warranty period imposed by article 100-bis of the Consolidated Finance Act - during

which it is expected that the securities remain in the portfolio from ' intermediary,

In the aftermath of the financial cracks occurred, the introduction of covenants clauses in contracts of

emission of bonds could also be a response to investors 'private' the supplementary to the strong public

demand for greater protection of risparmio24, unfortunately evaded request by the legislature only after a

long legislative stasis.

From a strictly legal point of view, the settled practice foreign contracts relating to covenants could stir some

attention, representing a valid reference point in the study of possible participatory content of the bonds, the

instruments referred to in the sixth co. art. 2346 cc and those issued on the occasion of the creation of

segregated assets and debt securities Ltd., and securities of Cooperatives: waiting for a consolidation of the

practice com- reholders', point out that in reality the "bondholders ... Also require protection When there are

conflicts between all agency managers and outside investors. " On this point, see. SM Bainbri- dge, Dead

Hand and No Hand Pills: precommitment strategies in corporate law, UCLA School of Law, Law and

Economics Research Paper no. 02-02, available to websitewww.ssrn.com, P. 3:05 ss.

Since the works by Jensen and Meckling (1976), Myers (1977), and Smith and Warner (1979), it has been

possible to distinguish costs of value transfer and costs related to agreement mechanisms for mitigating

International context, II in the corporate bond market in Italy, edited by C, M, Pinardi, cit., P. 32 ss. and 45 s.

The figure was confirmed by M. Bradley and MR Roberts, bond covenants priced Are ?, Fuqua School of

Business, Duke University, November 2004, available at websitewww.ideas.repec.org, P. 4. AA. We put in

evidence as "We find a negative relation between the inclusion of a bond covenants and the promised yield

on corporate debt."

"In the US, lenders who wish to protect themselves from opportunistic behavior of shareholders must rely on

the contractual instrument"; Enriques so L. and J. Macey, venture capital and creditor protection Collection:

a radical critique of the European rules on share capital, in "Riv. Soc. ", 2002, I, p. 86. Notes however R.

Rordorf, importance and limits of information in the financial markets, "Jur. comm. ", 2003, I, p. 774, as

"self-regulation is able to give real benefits only when it succeeds in harmoniously coordinating with the

primary sources general law [...] carving out their own space in the interstices that that sort should be the

guarantee." On this point, see. Also F. Fimmanò, cit., p. 98 ff .; MC Brescia Morra, financing of limited

liability companies and debt securities,www.dircomm.it2003, XI, 2.

In addition to satisfying this primary financial reason, the adoption of clauses within the Italian system could

find specific reasons for interest in the peculiarities of our economy. Their use might indeed be strongly

encouraged by the underwriters intermediaries are obliged to guarantee the solvency for the next assigns

savers: it is clear that the introduction of such clauses would be to reduce the financial risk suffered by the

borrower 'guarantor', you would see thus better secured against the issuer for at least the first year of life of

the title - or for the warranty period imposed by article 100-bis of the Consolidated Finance Act - during

which it is expected that the securities remain in the portfolio from ' intermediary,

In the aftermath of the financial cracks occurred, the introduction of covenants clauses in contracts of

emission of bonds could also be a response to investors 'private' the supplementary to the strong public

demand for greater protection of risparmio24, unfortunately evaded request by the legislature only after a

long legislative stasis.

From a strictly legal point of view, the settled practice foreign contracts relating to covenants could stir some

attention, representing a valid reference point in the study of possible participatory content of the bonds, the

instruments referred to in the sixth co. art. 2346 cc and those issued on the occasion of the creation of

segregated assets and debt securities Ltd., and securities of Cooperatives: waiting for a consolidation of the

practice com- reholders', point out that in reality the "bondholders ... Also require protection When there are

conflicts between all agency managers and outside investors. " On this point, see. SM Bainbri- dge, Dead

Hand and No Hand Pills: precommitment strategies in corporate law, UCLA School of Law, Law and

Economics Research Paper no. 02-02, available to websitewww.ssrn.com, P. 3:05 ss.

Since the works by Jensen and Meckling (1976), Myers (1977), and Smith and Warner (1979), it has been

possible to distinguish costs of value transfer and costs related to agreement mechanisms for mitigating

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

conflicts between shareholders and creditors. Regarding the transfer of value, when managers seek to

maximize shareholder value rather than maximize value for the company, there is the possibility of

overinvestment or underinvestment in future growth opportunities. Thus, the loss of value to the company

resulting from this attitude is characterized as an agency cost. Moreover, mechanisms that help reduce

conflict of interests and possible reductions capital cost (debt covenants and short-term debt) also have costs

related to its accession. After studies by Jensen and Meckling (1976) and Myers (1977), Smith and Warner

(1979) realized that the choice of covenants in a contract may indirectly and simultaneously affect an

enterprise’s other activities, such as investment decisions, payout policy and leverage.

As mentioned by Billet et al. (2007), although it is possible to reduce such agency conflicts without changing

the existing level of debt through the use of short-term debt and restrictive covenants, there are some

precautions related to a growth opportunity scenario that a company should take. In a growth opportunity

scenario, the use of covenants in debt agreements may limit the opportunities perceived in the future and the

use of short-term debt can bring the company liquidity risk problems. As these instruments may limit future

investments by firms, the logical solution is to decrease the current level of indebtedness or to use less debt

to raise funds in need of funding (Silva, Saito and Barbi, 2013). Therefore, the expected prediction is that

firms with greater growth opportunities are less leveraged. As debt covenants and short-term debt may limit

future opportunities, some companies might prefer not to raise debt instruments when they face growth

opportunities. That is the reason for predicting that growth opportunities and leverage have a negative

relation. In this situation, both covenants and short-term debt could be analyzed as possible tools to reduce

the negative relationship between growth opportunities and long-term debt.

Studies have shown that reducing debt maturity (i.e. issuing short-term debt) can help treatment of the

agency problem. Myers (1977) found that if the debt matures before the exercise growth option, maximizing

value to the business can be conducted. Then, it is possible to reduce the incentive for achievement of

underinvestment. According to Barclay and Smith (1995), in the event named contracting-cost, investors

tend to refuse investment when there is possibility of transferring wealth to creditors. One way to alleviate

the problem presented in the contracting-cost hypothesis would be reducing the maturity of debt owned and

using short-term debt in subsequent issues.

The hypothesis is far from unreal if we assume that the rate of bond interest can be modulated, being able to

guarantee for the first year of life of the title a particularly big chunk of that justifies the increased risk of the

first subscriber, in addition to covering the public placement of the subsequent costs.

"With a view to strengthening investor protection, the search for more efficient governance structures is not

just about the issuers, but also involves the lenders and brokers who, on behalf of the same issuer, are

concerned with the market finding resources» : F. Velia so, new rules of corporate governance and investor

protection, in this journal, 2004, III, p. 468; On this point, see. Also S. Fortunato, the "failures" in the system

of controls in the financial markets (on the sidelines of the bill on the protection of savings), in "Company",

maximize shareholder value rather than maximize value for the company, there is the possibility of

overinvestment or underinvestment in future growth opportunities. Thus, the loss of value to the company

resulting from this attitude is characterized as an agency cost. Moreover, mechanisms that help reduce

conflict of interests and possible reductions capital cost (debt covenants and short-term debt) also have costs

related to its accession. After studies by Jensen and Meckling (1976) and Myers (1977), Smith and Warner

(1979) realized that the choice of covenants in a contract may indirectly and simultaneously affect an

enterprise’s other activities, such as investment decisions, payout policy and leverage.

As mentioned by Billet et al. (2007), although it is possible to reduce such agency conflicts without changing

the existing level of debt through the use of short-term debt and restrictive covenants, there are some

precautions related to a growth opportunity scenario that a company should take. In a growth opportunity

scenario, the use of covenants in debt agreements may limit the opportunities perceived in the future and the

use of short-term debt can bring the company liquidity risk problems. As these instruments may limit future

investments by firms, the logical solution is to decrease the current level of indebtedness or to use less debt

to raise funds in need of funding (Silva, Saito and Barbi, 2013). Therefore, the expected prediction is that

firms with greater growth opportunities are less leveraged. As debt covenants and short-term debt may limit

future opportunities, some companies might prefer not to raise debt instruments when they face growth

opportunities. That is the reason for predicting that growth opportunities and leverage have a negative

relation. In this situation, both covenants and short-term debt could be analyzed as possible tools to reduce

the negative relationship between growth opportunities and long-term debt.

Studies have shown that reducing debt maturity (i.e. issuing short-term debt) can help treatment of the

agency problem. Myers (1977) found that if the debt matures before the exercise growth option, maximizing

value to the business can be conducted. Then, it is possible to reduce the incentive for achievement of

underinvestment. According to Barclay and Smith (1995), in the event named contracting-cost, investors

tend to refuse investment when there is possibility of transferring wealth to creditors. One way to alleviate

the problem presented in the contracting-cost hypothesis would be reducing the maturity of debt owned and

using short-term debt in subsequent issues.

The hypothesis is far from unreal if we assume that the rate of bond interest can be modulated, being able to

guarantee for the first year of life of the title a particularly big chunk of that justifies the increased risk of the

first subscriber, in addition to covering the public placement of the subsequent costs.

"With a view to strengthening investor protection, the search for more efficient governance structures is not

just about the issuers, but also involves the lenders and brokers who, on behalf of the same issuer, are

concerned with the market finding resources» : F. Velia so, new rules of corporate governance and investor

protection, in this journal, 2004, III, p. 468; On this point, see. Also S. Fortunato, the "failures" in the system

of controls in the financial markets (on the sidelines of the bill on the protection of savings), in "Company",

2004, VIII, p. 932 s; R. Pardolesi, AMP, A. Portolano, milk, tears (crocodile) and blood (of investors), in

"Mere. conc. reg. ", 2004, p. 200 s.

For a glimpse of the possible financing instruments of cooperative societies, their nature, see. P. Marchetti,

direct financing Technical forms of cooperative societies, in "Riv. coop. ", 2004, II, p. 26; R. costs, financial

instruments in new cooperatives: discipline problems, "Bank purse, tit. cred. ", 2005, II, p. 124 ss.

In this direction a significant boost to the material translation of the solutions provided by the legislature

could come from the current strengthening of the presence of foreign banks in the domestic capital market,

as well as the consolidation of synergies between Italians and European operators. The complexity of the

instruments now in the reformed code may in fact be more appreciated by the operators can already boast a

solid experience in the field of financial engineering1. These subjects may be so assigned the task of 'lead' a

market that has never particularly excelled in creating opportunities for a direct link between savings and

finance companies, also due to the limited size of the latter.

Finally, it must consider how, as a result of physiological aggregation operations of the numerous pieces of

the national bank mosaic, the actual decrease in the number of competitors subjects could force institutions

to reconsider, at least in part, the traditional operational strategies: if in fact until today the weight of

financial investments dished out in favor of individual company - itself usually not excessive, given the

limited size of Italian companies - is greatly reduced result from the breakdown of total debt in multiple lines

of credit opened by the various competing institutions, all ' opposite a concentration of the latter in a few

macro subjects could lead to a greater incidence of the possible suffering of the assets of institutions

(especially if concomitant with esposition to the guarantee of art. 100-bis TUF), forcing them to transfer a

greater part of the risk directly on risparmiatori25. In this regard the entry into force of the Basel II

agreements could play a decisive role in rationalizing the volume of direct investments, containing those

directed to the segment of companies with less financial strength and favoring, on the contrary, the pure

brokerage business capital.

The hope that the Italian banking world can "move ... corporate lending approach towards an approach of

corporate finance ...", "it is extremely present in the face of this historic moment, characterized by a

stagnation of national production system: the recovery in investor confidence and a more prompt and

attentive response to the financial needs of businesses, including in the interests of transnational

development of the same, therefore, seem to represent irreplaceable pieces in order to compose a credible

response to the phase slowdown that has unfortunately addressed our economy.

Starting from these premises may therefore be useful groped an analysis of the possible solutions to the

problem of a greater involvement in the management of the debt or, at least, supervision of the firm

(solutions that the new articles of the civil code transpire leave in determined operational flexibility that

themselves seek), comparing with the same practices contrattuamotive industry experience across the border,

1

"Mere. conc. reg. ", 2004, p. 200 s.

For a glimpse of the possible financing instruments of cooperative societies, their nature, see. P. Marchetti,

direct financing Technical forms of cooperative societies, in "Riv. coop. ", 2004, II, p. 26; R. costs, financial

instruments in new cooperatives: discipline problems, "Bank purse, tit. cred. ", 2005, II, p. 124 ss.

In this direction a significant boost to the material translation of the solutions provided by the legislature

could come from the current strengthening of the presence of foreign banks in the domestic capital market,

as well as the consolidation of synergies between Italians and European operators. The complexity of the

instruments now in the reformed code may in fact be more appreciated by the operators can already boast a

solid experience in the field of financial engineering1. These subjects may be so assigned the task of 'lead' a

market that has never particularly excelled in creating opportunities for a direct link between savings and

finance companies, also due to the limited size of the latter.

Finally, it must consider how, as a result of physiological aggregation operations of the numerous pieces of

the national bank mosaic, the actual decrease in the number of competitors subjects could force institutions

to reconsider, at least in part, the traditional operational strategies: if in fact until today the weight of

financial investments dished out in favor of individual company - itself usually not excessive, given the

limited size of Italian companies - is greatly reduced result from the breakdown of total debt in multiple lines

of credit opened by the various competing institutions, all ' opposite a concentration of the latter in a few

macro subjects could lead to a greater incidence of the possible suffering of the assets of institutions

(especially if concomitant with esposition to the guarantee of art. 100-bis TUF), forcing them to transfer a

greater part of the risk directly on risparmiatori25. In this regard the entry into force of the Basel II

agreements could play a decisive role in rationalizing the volume of direct investments, containing those

directed to the segment of companies with less financial strength and favoring, on the contrary, the pure

brokerage business capital.

The hope that the Italian banking world can "move ... corporate lending approach towards an approach of

corporate finance ...", "it is extremely present in the face of this historic moment, characterized by a

stagnation of national production system: the recovery in investor confidence and a more prompt and

attentive response to the financial needs of businesses, including in the interests of transnational

development of the same, therefore, seem to represent irreplaceable pieces in order to compose a credible

response to the phase slowdown that has unfortunately addressed our economy.

Starting from these premises may therefore be useful groped an analysis of the possible solutions to the

problem of a greater involvement in the management of the debt or, at least, supervision of the firm

(solutions that the new articles of the civil code transpire leave in determined operational flexibility that

themselves seek), comparing with the same practices contrattuamotive industry experience across the border,

1

in order to identify some of the possible scenarios that the framework of targeted funding Italian industry in

the future will come to contemplate.

BOND FEATURES

The term Yield is the percentage of the amount invested, as income result of a financial investment. Fixed-

income securities effective yield is the interest rate that exactly the stock price to the sum of the present

values formed by the cash flows that the title will generate in the future. The yield of a share is instead

calculated as the ratio of the annual dividend of the stock and the stock's market price.

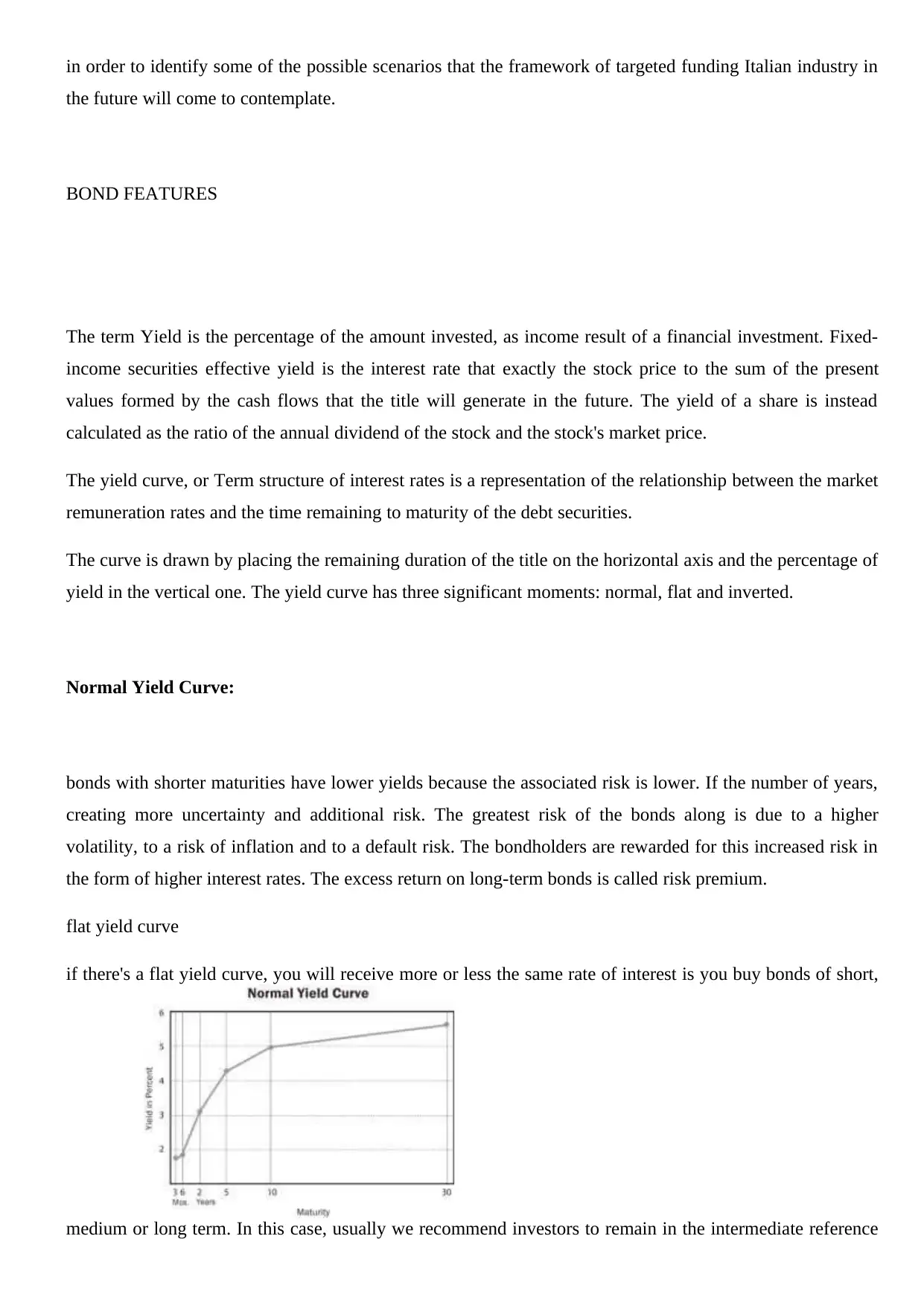

The yield curve, or Term structure of interest rates is a representation of the relationship between the market

remuneration rates and the time remaining to maturity of the debt securities.

The curve is drawn by placing the remaining duration of the title on the horizontal axis and the percentage of

yield in the vertical one. The yield curve has three significant moments: normal, flat and inverted.

Normal Yield Curve:

bonds with shorter maturities have lower yields because the associated risk is lower. If the number of years,

creating more uncertainty and additional risk. The greatest risk of the bonds along is due to a higher

volatility, to a risk of inflation and to a default risk. The bondholders are rewarded for this increased risk in

the form of higher interest rates. The excess return on long-term bonds is called risk premium.

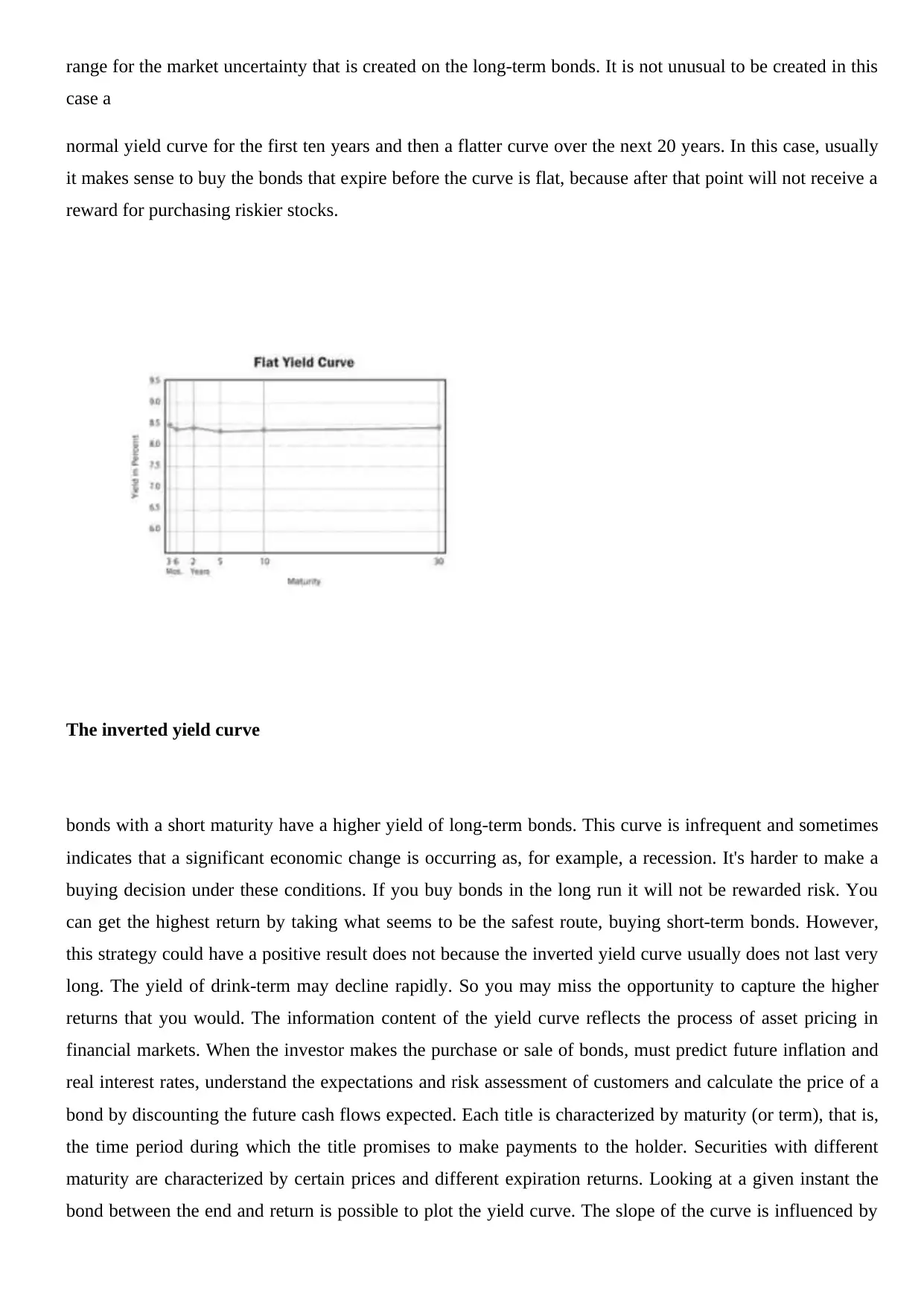

flat yield curve

if there's a flat yield curve, you will receive more or less the same rate of interest is you buy bonds of short,

medium or long term. In this case, usually we recommend investors to remain in the intermediate reference

the future will come to contemplate.

BOND FEATURES

The term Yield is the percentage of the amount invested, as income result of a financial investment. Fixed-

income securities effective yield is the interest rate that exactly the stock price to the sum of the present

values formed by the cash flows that the title will generate in the future. The yield of a share is instead

calculated as the ratio of the annual dividend of the stock and the stock's market price.

The yield curve, or Term structure of interest rates is a representation of the relationship between the market

remuneration rates and the time remaining to maturity of the debt securities.

The curve is drawn by placing the remaining duration of the title on the horizontal axis and the percentage of

yield in the vertical one. The yield curve has three significant moments: normal, flat and inverted.

Normal Yield Curve:

bonds with shorter maturities have lower yields because the associated risk is lower. If the number of years,

creating more uncertainty and additional risk. The greatest risk of the bonds along is due to a higher

volatility, to a risk of inflation and to a default risk. The bondholders are rewarded for this increased risk in

the form of higher interest rates. The excess return on long-term bonds is called risk premium.

flat yield curve

if there's a flat yield curve, you will receive more or less the same rate of interest is you buy bonds of short,

medium or long term. In this case, usually we recommend investors to remain in the intermediate reference

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

range for the market uncertainty that is created on the long-term bonds. It is not unusual to be created in this

case a

normal yield curve for the first ten years and then a flatter curve over the next 20 years. In this case, usually

it makes sense to buy the bonds that expire before the curve is flat, because after that point will not receive a

reward for purchasing riskier stocks.

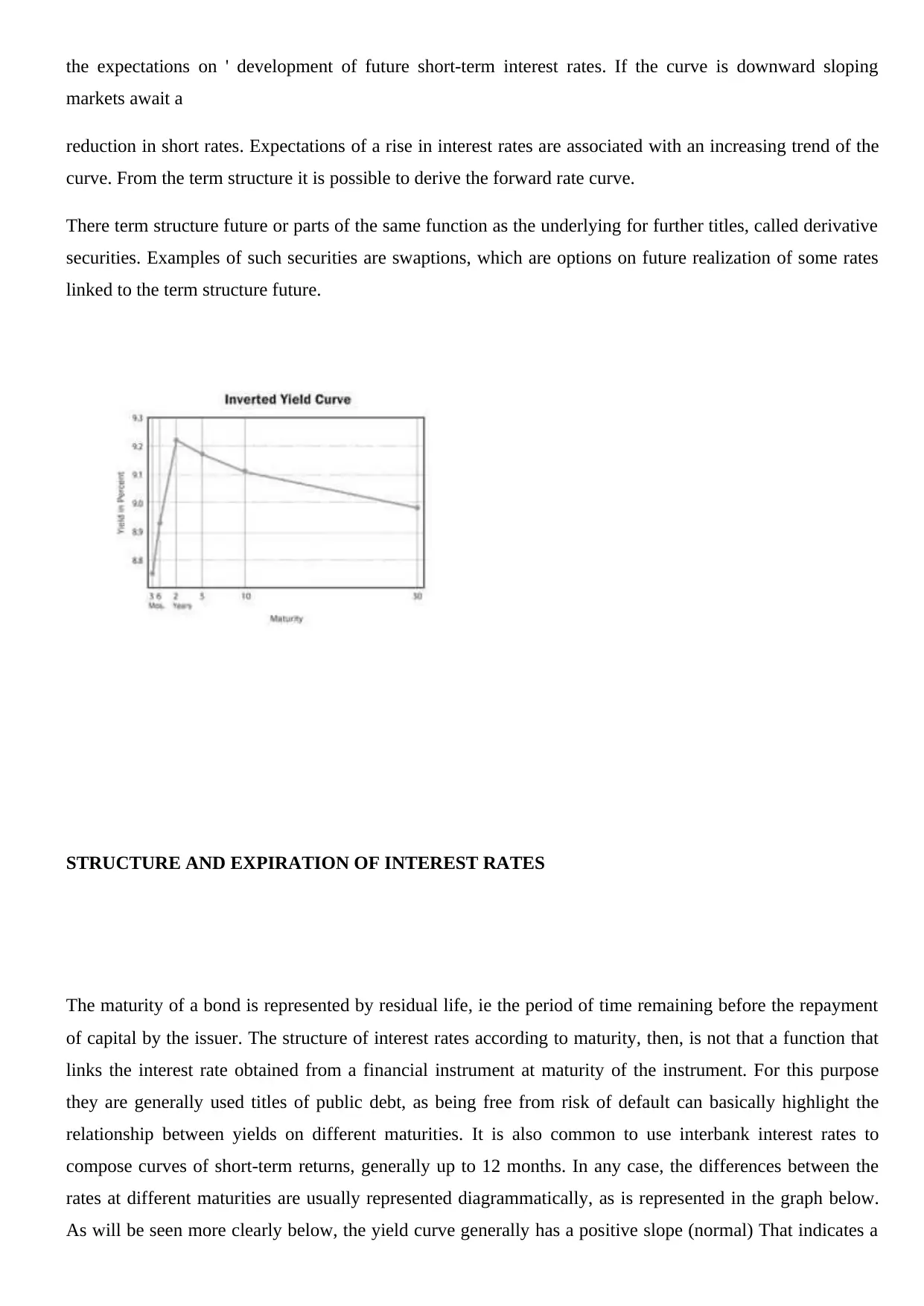

The inverted yield curve

bonds with a short maturity have a higher yield of long-term bonds. This curve is infrequent and sometimes

indicates that a significant economic change is occurring as, for example, a recession. It's harder to make a

buying decision under these conditions. If you buy bonds in the long run it will not be rewarded risk. You

can get the highest return by taking what seems to be the safest route, buying short-term bonds. However,

this strategy could have a positive result does not because the inverted yield curve usually does not last very

long. The yield of drink-term may decline rapidly. So you may miss the opportunity to capture the higher

returns that you would. The information content of the yield curve reflects the process of asset pricing in

financial markets. When the investor makes the purchase or sale of bonds, must predict future inflation and

real interest rates, understand the expectations and risk assessment of customers and calculate the price of a

bond by discounting the future cash flows expected. Each title is characterized by maturity (or term), that is,

the time period during which the title promises to make payments to the holder. Securities with different

maturity are characterized by certain prices and different expiration returns. Looking at a given instant the

bond between the end and return is possible to plot the yield curve. The slope of the curve is influenced by

case a

normal yield curve for the first ten years and then a flatter curve over the next 20 years. In this case, usually

it makes sense to buy the bonds that expire before the curve is flat, because after that point will not receive a

reward for purchasing riskier stocks.

The inverted yield curve

bonds with a short maturity have a higher yield of long-term bonds. This curve is infrequent and sometimes

indicates that a significant economic change is occurring as, for example, a recession. It's harder to make a

buying decision under these conditions. If you buy bonds in the long run it will not be rewarded risk. You

can get the highest return by taking what seems to be the safest route, buying short-term bonds. However,

this strategy could have a positive result does not because the inverted yield curve usually does not last very

long. The yield of drink-term may decline rapidly. So you may miss the opportunity to capture the higher

returns that you would. The information content of the yield curve reflects the process of asset pricing in

financial markets. When the investor makes the purchase or sale of bonds, must predict future inflation and

real interest rates, understand the expectations and risk assessment of customers and calculate the price of a

bond by discounting the future cash flows expected. Each title is characterized by maturity (or term), that is,

the time period during which the title promises to make payments to the holder. Securities with different

maturity are characterized by certain prices and different expiration returns. Looking at a given instant the

bond between the end and return is possible to plot the yield curve. The slope of the curve is influenced by

the expectations on ' development of future short-term interest rates. If the curve is downward sloping

markets await a

reduction in short rates. Expectations of a rise in interest rates are associated with an increasing trend of the

curve. From the term structure it is possible to derive the forward rate curve.

There term structure future or parts of the same function as the underlying for further titles, called derivative

securities. Examples of such securities are swaptions, which are options on future realization of some rates

linked to the term structure future.

STRUCTURE AND EXPIRATION OF INTEREST RATES

The maturity of a bond is represented by residual life, ie the period of time remaining before the repayment

of capital by the issuer. The structure of interest rates according to maturity, then, is not that a function that

links the interest rate obtained from a financial instrument at maturity of the instrument. For this purpose

they are generally used titles of public debt, as being free from risk of default can basically highlight the

relationship between yields on different maturities. It is also common to use interbank interest rates to

compose curves of short-term returns, generally up to 12 months. In any case, the differences between the

rates at different maturities are usually represented diagrammatically, as is represented in the graph below.

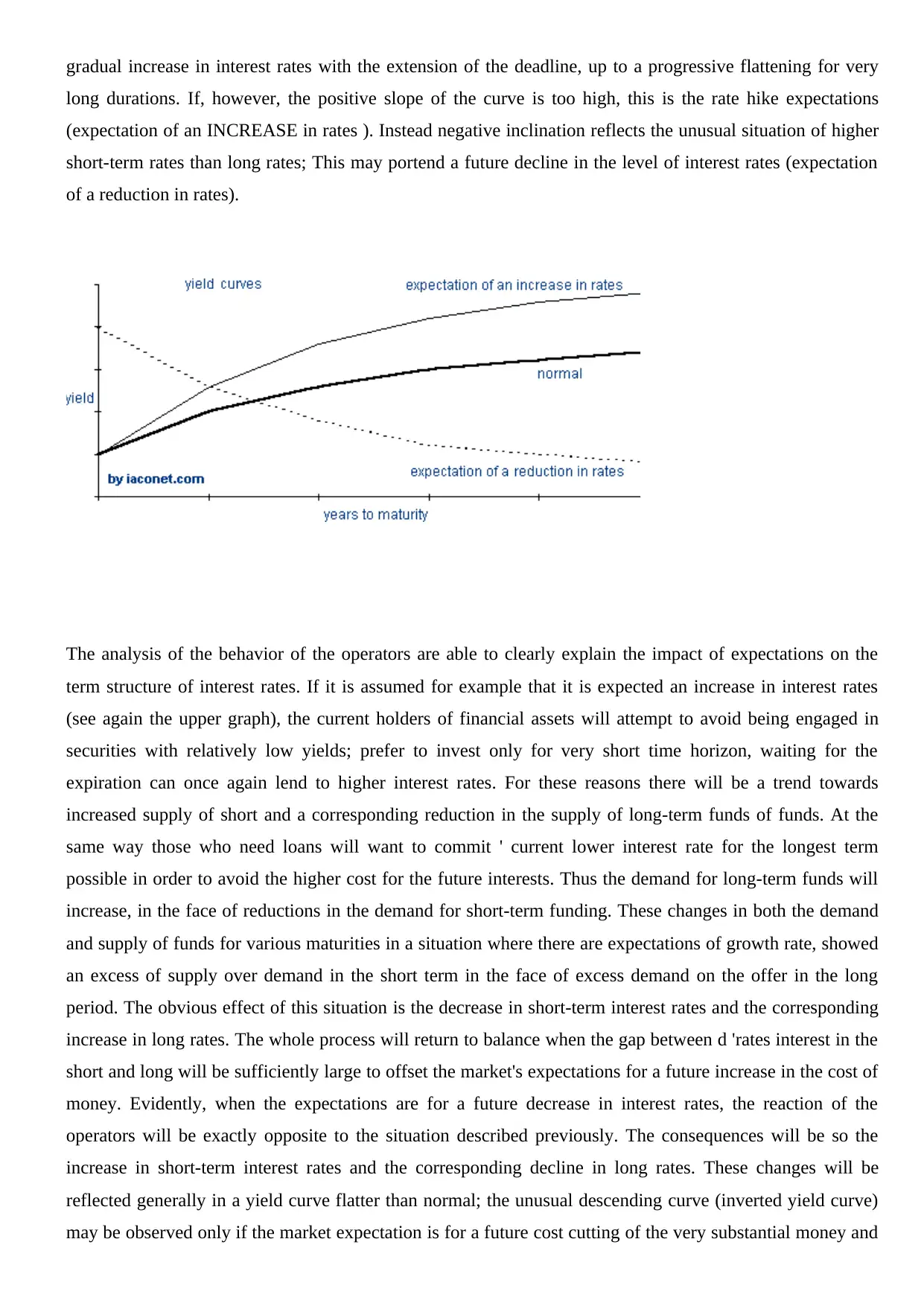

As will be seen more clearly below, the yield curve generally has a positive slope (normal) That indicates a

markets await a

reduction in short rates. Expectations of a rise in interest rates are associated with an increasing trend of the

curve. From the term structure it is possible to derive the forward rate curve.

There term structure future or parts of the same function as the underlying for further titles, called derivative

securities. Examples of such securities are swaptions, which are options on future realization of some rates

linked to the term structure future.

STRUCTURE AND EXPIRATION OF INTEREST RATES

The maturity of a bond is represented by residual life, ie the period of time remaining before the repayment

of capital by the issuer. The structure of interest rates according to maturity, then, is not that a function that

links the interest rate obtained from a financial instrument at maturity of the instrument. For this purpose

they are generally used titles of public debt, as being free from risk of default can basically highlight the

relationship between yields on different maturities. It is also common to use interbank interest rates to

compose curves of short-term returns, generally up to 12 months. In any case, the differences between the

rates at different maturities are usually represented diagrammatically, as is represented in the graph below.

As will be seen more clearly below, the yield curve generally has a positive slope (normal) That indicates a

gradual increase in interest rates with the extension of the deadline, up to a progressive flattening for very

long durations. If, however, the positive slope of the curve is too high, this is the rate hike expectations

(expectation of an INCREASE in rates ). Instead negative inclination reflects the unusual situation of higher

short-term rates than long rates; This may portend a future decline in the level of interest rates (expectation

of a reduction in rates).

The analysis of the behavior of the operators are able to clearly explain the impact of expectations on the

term structure of interest rates. If it is assumed for example that it is expected an increase in interest rates

(see again the upper graph), the current holders of financial assets will attempt to avoid being engaged in

securities with relatively low yields; prefer to invest only for very short time horizon, waiting for the

expiration can once again lend to higher interest rates. For these reasons there will be a trend towards

increased supply of short and a corresponding reduction in the supply of long-term funds of funds. At the

same way those who need loans will want to commit ' current lower interest rate for the longest term

possible in order to avoid the higher cost for the future interests. Thus the demand for long-term funds will

increase, in the face of reductions in the demand for short-term funding. These changes in both the demand

and supply of funds for various maturities in a situation where there are expectations of growth rate, showed

an excess of supply over demand in the short term in the face of excess demand on the offer in the long

period. The obvious effect of this situation is the decrease in short-term interest rates and the corresponding

increase in long rates. The whole process will return to balance when the gap between d 'rates interest in the

short and long will be sufficiently large to offset the market's expectations for a future increase in the cost of

money. Evidently, when the expectations are for a future decrease in interest rates, the reaction of the

operators will be exactly opposite to the situation described previously. The consequences will be so the

increase in short-term interest rates and the corresponding decline in long rates. These changes will be

reflected generally in a yield curve flatter than normal; the unusual descending curve (inverted yield curve)

may be observed only if the market expectation is for a future cost cutting of the very substantial money and

long durations. If, however, the positive slope of the curve is too high, this is the rate hike expectations

(expectation of an INCREASE in rates ). Instead negative inclination reflects the unusual situation of higher

short-term rates than long rates; This may portend a future decline in the level of interest rates (expectation

of a reduction in rates).

The analysis of the behavior of the operators are able to clearly explain the impact of expectations on the

term structure of interest rates. If it is assumed for example that it is expected an increase in interest rates

(see again the upper graph), the current holders of financial assets will attempt to avoid being engaged in

securities with relatively low yields; prefer to invest only for very short time horizon, waiting for the

expiration can once again lend to higher interest rates. For these reasons there will be a trend towards

increased supply of short and a corresponding reduction in the supply of long-term funds of funds. At the

same way those who need loans will want to commit ' current lower interest rate for the longest term

possible in order to avoid the higher cost for the future interests. Thus the demand for long-term funds will

increase, in the face of reductions in the demand for short-term funding. These changes in both the demand

and supply of funds for various maturities in a situation where there are expectations of growth rate, showed

an excess of supply over demand in the short term in the face of excess demand on the offer in the long

period. The obvious effect of this situation is the decrease in short-term interest rates and the corresponding

increase in long rates. The whole process will return to balance when the gap between d 'rates interest in the

short and long will be sufficiently large to offset the market's expectations for a future increase in the cost of

money. Evidently, when the expectations are for a future decrease in interest rates, the reaction of the

operators will be exactly opposite to the situation described previously. The consequences will be so the

increase in short-term interest rates and the corresponding decline in long rates. These changes will be

reflected generally in a yield curve flatter than normal; the unusual descending curve (inverted yield curve)

may be observed only if the market expectation is for a future cost cutting of the very substantial money and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

this expectation proves to be very well founded. In this case the influence and risk appetite Evidently, when

the expectations are for a future decrease in interest rates, the reaction of the operators will be exactly

opposite to the situation described previously. The consequences will be so the increase in short-term

interest rates and the corresponding decline in long rates. These changes will be reflected generally in a yield

curve flatter than normal; the unusual descending curve (inverted yield curve) may be observed only if the

market expectation is for a future cost cutting of the very substantial money and this expectation proves to be

very well founded. In this case the influence and risk appetite Evidently, when the expectations are for a

future decrease in interest rates, the reaction of the operators will be exactly opposite to the situation

described previously. The consequences will be so the increase in short-term interest rates and the

corresponding decline in long rates. These changes will be reflected generally in a yield curve flatter than

normal; the unusual descending curve (inverted yield curve) may be observed only if the market expectation

is for a future cost cutting of the very substantial money and this expectation proves to be very well founded.

In this case the influence and risk appetite The consequences will be so the increase in short-term interest

rates and the corresponding decline in long rates. These changes will be reflected generally in a yield curve

flatter than normal; the unusual descending curve (inverted yield curve) may be observed only if the market

expectation is for a future cost cutting of the very substantial money and this expectation proves to be very

well founded. In this case the influence and risk appetite The consequences will be so the increase in short-

term interest rates and the corresponding decline in long rates. These changes will be reflected generally in a

yield curve flatter than normal; the unusual descending curve (inverted yield curve) may be observed only if

the market expectation is for a future cost cutting of the very substantial money and this expectation proves

to be very well founded. In this case the influence and risk appetite market expectation is for a very

significant future cost of money and cutting this expectation proves to be very well founded. In this case the

influence and risk appetite market expectation is for a very significant future cost of money and cutting this

expectation proves to be very well founded. In this case the influence and risk appetite

the expectations are for a future decrease in interest rates, the reaction of the operators will be exactly

opposite to the situation described previously. The consequences will be so the increase in short-term

interest rates and the corresponding decline in long rates. These changes will be reflected generally in a yield

curve flatter than normal; the unusual descending curve (inverted yield curve) may be observed only if the

market expectation is for a future cost cutting of the very substantial money and this expectation proves to be

very well founded. In this case the influence and risk appetite Evidently, when the expectations are for a

future decrease in interest rates, the reaction of the operators will be exactly opposite to the situation

described previously. The consequences will be so the increase in short-term interest rates and the

corresponding decline in long rates. These changes will be reflected generally in a yield curve flatter than

normal; the unusual descending curve (inverted yield curve) may be observed only if the market expectation

is for a future cost cutting of the very substantial money and this expectation proves to be very well founded.

In this case the influence and risk appetite The consequences will be so the increase in short-term interest

rates and the corresponding decline in long rates. These changes will be reflected generally in a yield curve

flatter than normal; the unusual descending curve (inverted yield curve) may be observed only if the market

expectation is for a future cost cutting of the very substantial money and this expectation proves to be very

well founded. In this case the influence and risk appetite The consequences will be so the increase in short-

term interest rates and the corresponding decline in long rates. These changes will be reflected generally in a

yield curve flatter than normal; the unusual descending curve (inverted yield curve) may be observed only if

the market expectation is for a future cost cutting of the very substantial money and this expectation proves

to be very well founded. In this case the influence and risk appetite market expectation is for a very

significant future cost of money and cutting this expectation proves to be very well founded. In this case the

influence and risk appetite market expectation is for a very significant future cost of money and cutting this

expectation proves to be very well founded. In this case the influence and risk appetite

12

liquidity is not sufficient to offset this ingrained belief of a future sharp decline in interest rates.

TWO CURVES PERFORMANCE OF CREDIT RISK

Daily are calculated and published two maturing facilities. That pricipale is estimated on the prices

of government bonds with credit rating (Fitch) AAA, which signifies the structure for risk-free

maturing of the euro. A second is calculated from prices of all euro area government bonds. In both

cases are considered only euro-denominated securities, stakes deterministic (a coupon securities

nothing and fixed coupon bonds), life at maturity from 3 months to 30 years, issued nominal value

of at least € 5 billion and actually traded that day , with bid-ask spread of no more than 3 basis

points. The prices considered are those of the end of the day (closed).

The value of bonds, namely their price, can be obtained as the current value of their flows by

applying the principles of the RIC discounting, at an interest rate that we consider the constant (on a

period basis) for each maturity.

The types of covenants

As mentioned, the main reason for the development of the covenants bonds phenomenon in foreign

financial practice, primarily in the US market for high yield, it resides, in a nutshell, in the need to

contain the natural elapsing conflict between shareholders and bondholders, thereby reducing the

cost of financing. "it is clear as the venture capital (or often the only villages linked by a control

agreement), particularly in societies with little financial credit, it is naturally pushed to undertake

financial transactions that produce the higher profit achieved in order of payment of dividends,

almost always in the short course of a few financial years. These policies clearly clash with the

interests of creditors,aimed at the preservation of a constant profitability, and against a division of

assets to address the entire duration of the loan. "

A similar mechanism of protection is also known for bank loans: indeed it can be said that in reality

the Italian contractual practice of the conditions to the industrial mortgage operations will be

liquidity is not sufficient to offset this ingrained belief of a future sharp decline in interest rates.

TWO CURVES PERFORMANCE OF CREDIT RISK

Daily are calculated and published two maturing facilities. That pricipale is estimated on the prices

of government bonds with credit rating (Fitch) AAA, which signifies the structure for risk-free

maturing of the euro. A second is calculated from prices of all euro area government bonds. In both

cases are considered only euro-denominated securities, stakes deterministic (a coupon securities

nothing and fixed coupon bonds), life at maturity from 3 months to 30 years, issued nominal value

of at least € 5 billion and actually traded that day , with bid-ask spread of no more than 3 basis

points. The prices considered are those of the end of the day (closed).

The value of bonds, namely their price, can be obtained as the current value of their flows by

applying the principles of the RIC discounting, at an interest rate that we consider the constant (on a

period basis) for each maturity.

The types of covenants

As mentioned, the main reason for the development of the covenants bonds phenomenon in foreign

financial practice, primarily in the US market for high yield, it resides, in a nutshell, in the need to

contain the natural elapsing conflict between shareholders and bondholders, thereby reducing the

cost of financing. "it is clear as the venture capital (or often the only villages linked by a control

agreement), particularly in societies with little financial credit, it is naturally pushed to undertake

financial transactions that produce the higher profit achieved in order of payment of dividends,

almost always in the short course of a few financial years. These policies clearly clash with the

interests of creditors,aimed at the preservation of a constant profitability, and against a division of

assets to address the entire duration of the loan. "

A similar mechanism of protection is also known for bank loans: indeed it can be said that in reality

the Italian contractual practice of the conditions to the industrial mortgage operations will be

13

developed first in this field, in view of the increased specialization of credit institutions; However,

even the practice of loan covenants cd appears to now especially widespread in the national credit

reality: only a part of the few loans implemented by banking consortia can indeed detect a certain

use of such clausesSun''. A probable reason you possibly can find not only in the modeste size of

most Italian spa, in the absence of a real interest on the part of lenders, given the tight weave that

often unites the leading companies in the Italian banking sector and making it unnecessary to

impose such control mechanisms. The participation of many institutions to the social structure, or at

least the strong commercial relationship between banks normally the funded companies, are in fact

the instruments that was already more than enough for the exercise of a power monitoring, if not

sometimes indirect management of the enterprise, with the consequent risk of having generated the

distorting effects related to a constraint of this nature.

Conversely, not being able to realize such an intense relationship between the issuer and the mass of

the holders of the debt securities, are easy to understand the benefits of the use of such terms within

the contracts for bond financing: in this so the bondholders are strengthened to obtain a guarantee

against social enterprise, being able, on the one hand, to target certain operational choices, on the

other, coming to enjoy a right to control strengthened with respect to what expected from the

common discipline. Likewise the company is facilitated in search of capital, being able to pay a

lower interest in the face of reduced economic risk to which they are exposed and to be creditors of

the same. In order to satisfy this double requirement,

the indebtedness limitation clauses;

the limitation clauses to payments to certain entities;

the limitation clauses to lease back transactions;

the limitation clauses in the sale of corporate assets;

the limitation to the merger clauses;

the limitation on the change in the shareholding control clauses;

the limitation clauses in transactions with affiliates or parent companies;

clauses containing an obligation to specific information in favor of bondholders

Apart from the simple classification between positive and negative covenants - or respectively

based on obligations to do and not do - the enumeration can be split into two distinct subsets: the

first, comprising the first four categories, it is characterized by having a common denominator l

developed first in this field, in view of the increased specialization of credit institutions; However,

even the practice of loan covenants cd appears to now especially widespread in the national credit

reality: only a part of the few loans implemented by banking consortia can indeed detect a certain

use of such clausesSun''. A probable reason you possibly can find not only in the modeste size of

most Italian spa, in the absence of a real interest on the part of lenders, given the tight weave that

often unites the leading companies in the Italian banking sector and making it unnecessary to

impose such control mechanisms. The participation of many institutions to the social structure, or at

least the strong commercial relationship between banks normally the funded companies, are in fact

the instruments that was already more than enough for the exercise of a power monitoring, if not

sometimes indirect management of the enterprise, with the consequent risk of having generated the

distorting effects related to a constraint of this nature.

Conversely, not being able to realize such an intense relationship between the issuer and the mass of

the holders of the debt securities, are easy to understand the benefits of the use of such terms within

the contracts for bond financing: in this so the bondholders are strengthened to obtain a guarantee

against social enterprise, being able, on the one hand, to target certain operational choices, on the

other, coming to enjoy a right to control strengthened with respect to what expected from the

common discipline. Likewise the company is facilitated in search of capital, being able to pay a

lower interest in the face of reduced economic risk to which they are exposed and to be creditors of

the same. In order to satisfy this double requirement,

the indebtedness limitation clauses;

the limitation clauses to payments to certain entities;

the limitation clauses to lease back transactions;

the limitation clauses in the sale of corporate assets;

the limitation to the merger clauses;

the limitation on the change in the shareholding control clauses;

the limitation clauses in transactions with affiliates or parent companies;

clauses containing an obligation to specific information in favor of bondholders

Apart from the simple classification between positive and negative covenants - or respectively

based on obligations to do and not do - the enumeration can be split into two distinct subsets: the

first, comprising the first four categories, it is characterized by having a common denominator l

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

'imposition of operational limits aimed at direct protection of corporate assets "; the second, formed

by the remaining types, is instead characterized by putting in place a guarantee only mediated,

realized through the imposition of operating limitations that implement only indirectly a defense of

company '' active.

CAPITOLO 2 CONTINUAZIONE

the indebtedness limitation clauses

Among the figures outlined above that of more immediate understanding resides certainly in the

covenants relating to the imposition of a limitation of the issuer's debt. "In our sorting such creditors

guarantee mechanism is to operate only ex lege for spa unlisted not with popular tools among the

public with the fixation of emission limit calculated as twice the reserves and the existing capital

pursuant to art. 2412 cc the adoption of such a clause seems to configurable towards acceding spa to

the public capital markets wishing to put a conventional debt brake - as well as against other

companies - if they want to further reduce the limit already fixed by the legislature. Nothing then

exclude that this measure may also be accepted in issuing contracts the instruments referred to in

Articles. 2346, sixth co., 2483 to 2526 cc

In foreign financial practice the weighting between the active and the passive to the base of the

present covenants normally takes into consideration the relationship between Ebitda or EBTDA

"and the amount of the overall exposure of the individual exercise, relating respectively to the total

debt or interest only. Unlike the mechanism provided for by national law, it then configures a

substantially dynamic evaluation of the economic undertaking funded, mainly anchored to chaste

flow values that the latter is able to produce '' '. a further possible variant the issuer's indebtedness

direct calculation is given by the lowering of opinion expressed by the rating agencies. This practice

has to bind to an immediate perception parameter and knowable by the mass of the bondholders,

however, not free from the danger of errors, being tied to a questionable estimate prepared by a

private entity: in this sense are decidedly important for a correct application of the content of the

rules contained in the new art clause. 69- decies of Consob Resolution 11971 of May 14, 1999, the

Issuer Regulation, to ensure a fair presentation of the creditworthiness assessment enjoyed by the

'imposition of operational limits aimed at direct protection of corporate assets "; the second, formed

by the remaining types, is instead characterized by putting in place a guarantee only mediated,

realized through the imposition of operating limitations that implement only indirectly a defense of

company '' active.

CAPITOLO 2 CONTINUAZIONE

the indebtedness limitation clauses

Among the figures outlined above that of more immediate understanding resides certainly in the

covenants relating to the imposition of a limitation of the issuer's debt. "In our sorting such creditors

guarantee mechanism is to operate only ex lege for spa unlisted not with popular tools among the

public with the fixation of emission limit calculated as twice the reserves and the existing capital

pursuant to art. 2412 cc the adoption of such a clause seems to configurable towards acceding spa to

the public capital markets wishing to put a conventional debt brake - as well as against other

companies - if they want to further reduce the limit already fixed by the legislature. Nothing then

exclude that this measure may also be accepted in issuing contracts the instruments referred to in

Articles. 2346, sixth co., 2483 to 2526 cc

In foreign financial practice the weighting between the active and the passive to the base of the

present covenants normally takes into consideration the relationship between Ebitda or EBTDA

"and the amount of the overall exposure of the individual exercise, relating respectively to the total

debt or interest only. Unlike the mechanism provided for by national law, it then configures a

substantially dynamic evaluation of the economic undertaking funded, mainly anchored to chaste

flow values that the latter is able to produce '' '. a further possible variant the issuer's indebtedness

direct calculation is given by the lowering of opinion expressed by the rating agencies. This practice

has to bind to an immediate perception parameter and knowable by the mass of the bondholders,

however, not free from the danger of errors, being tied to a questionable estimate prepared by a