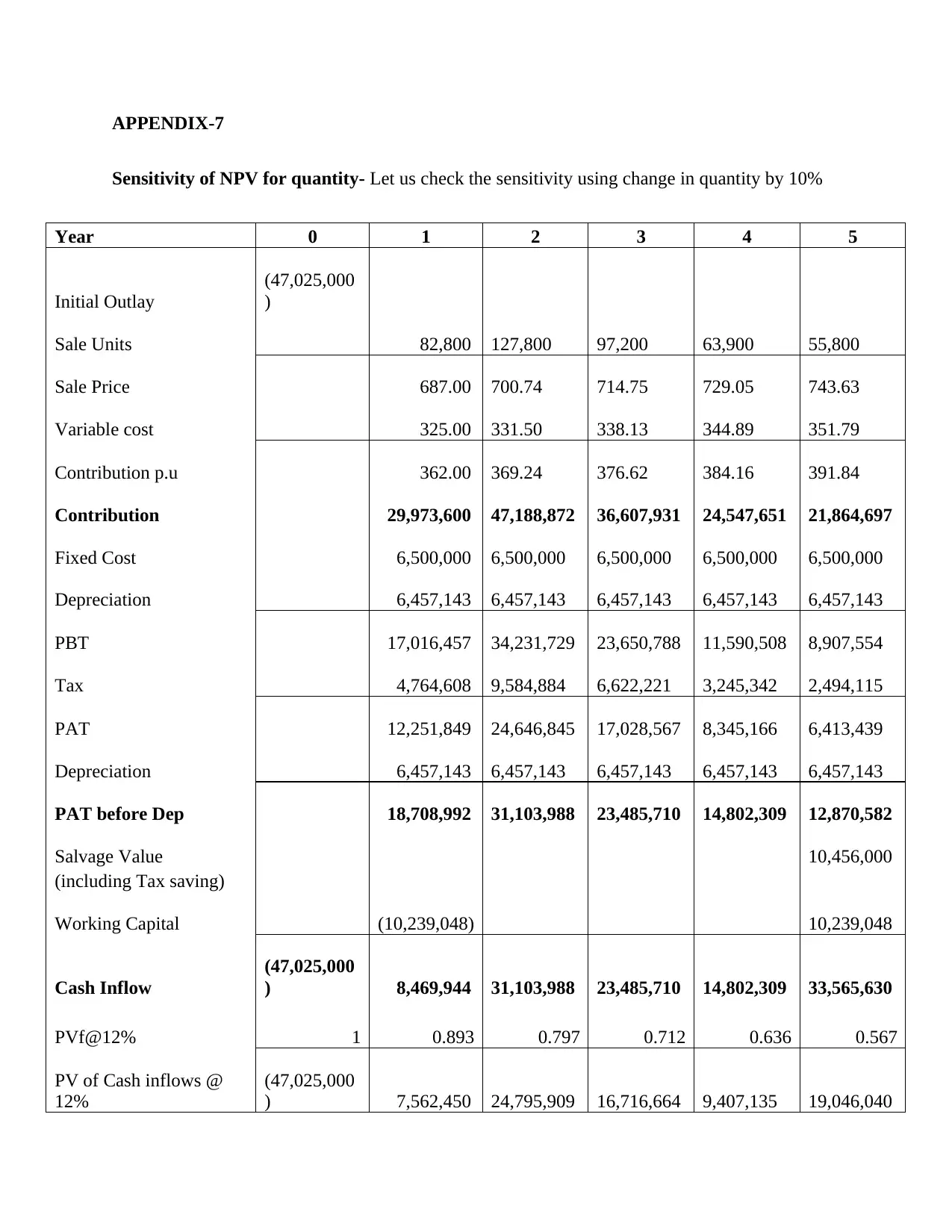

Sensitivity Analysis for Changes in Quantity by 10%

VerifiedAdded on 2019/09/25

|8

|1120

|102

Report

AI Summary

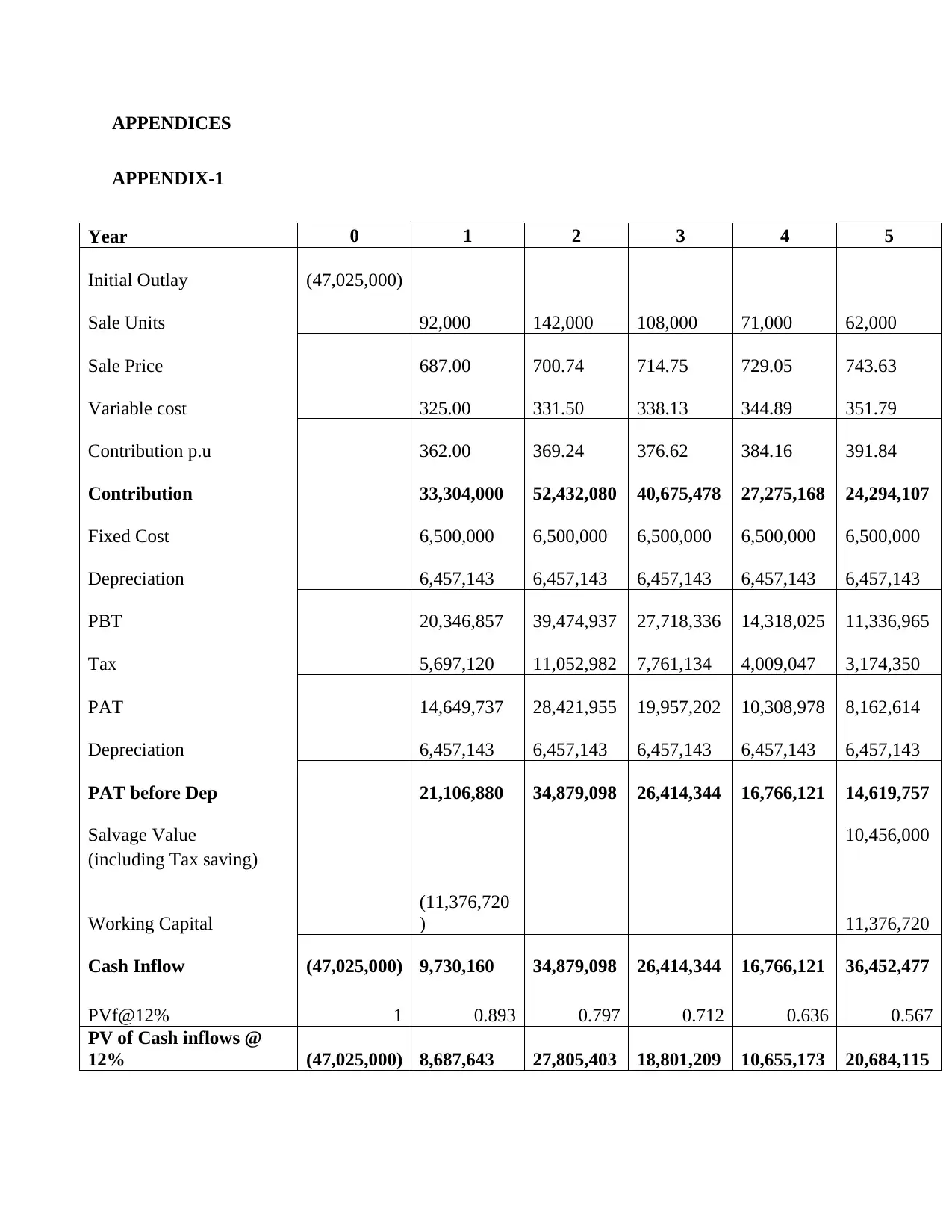

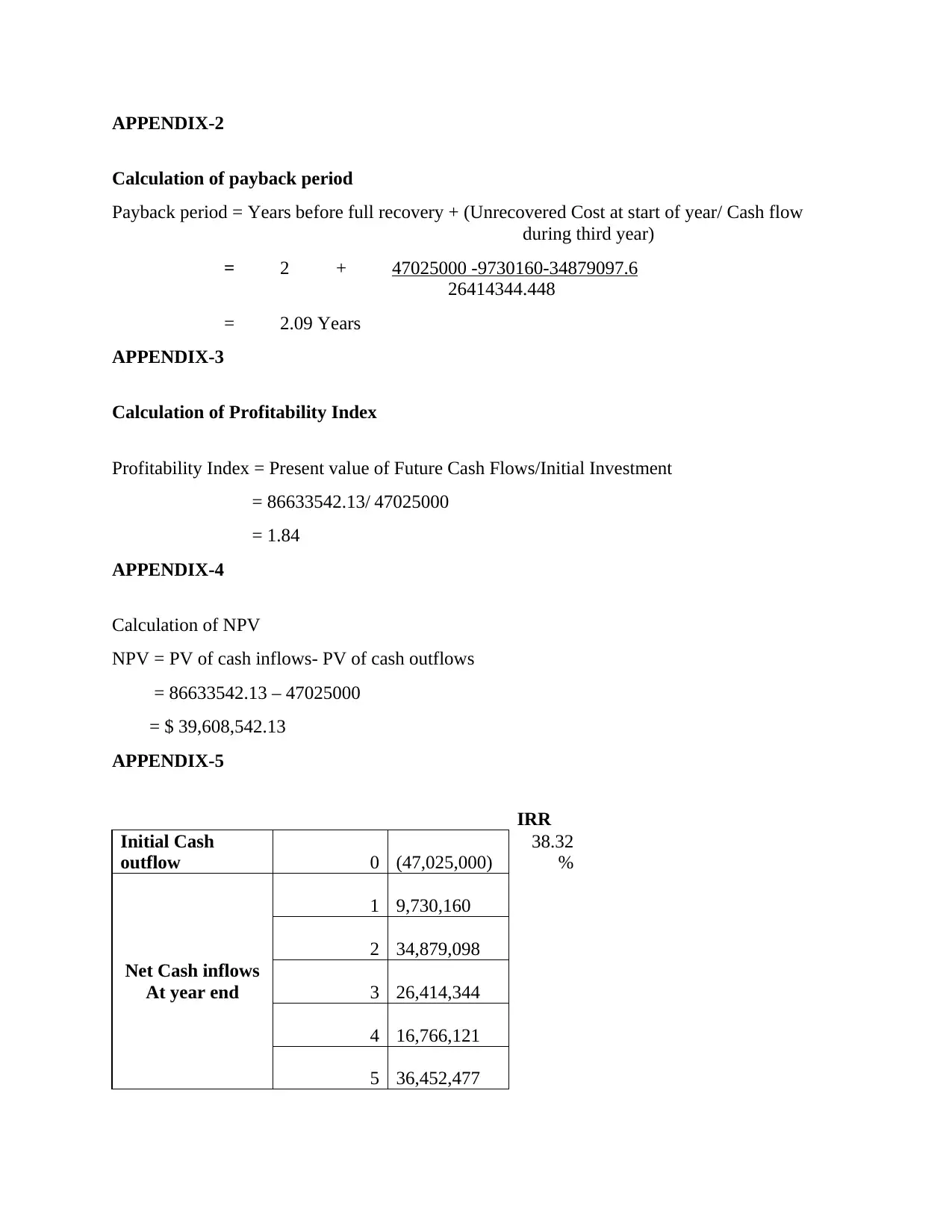

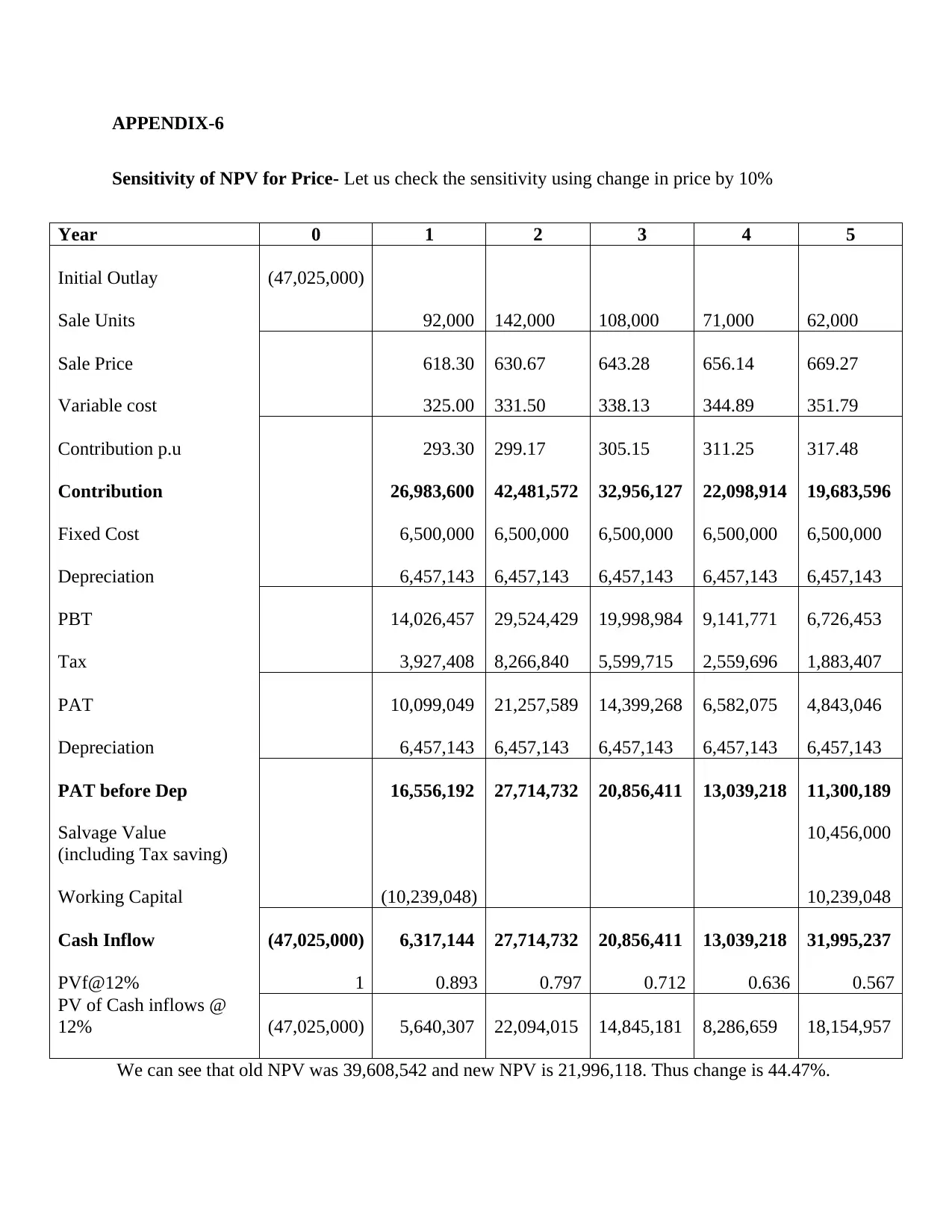

The assignment content presents a financial analysis of a project. The data provided shows the contribution, fixed cost, depreciation, PBT (Profit Before Tax), PAT (Profit After Tax), and working capital for different years. The sensitivity of NPV to quantity change is also analyzed by increasing the quantity by 10%. The results show an initial outlay of $47,025,000 and a new NPV of $21,996,118, indicating a 44.47% change from the old NPV of $39,608,542.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.