Analyzing Brazil's Macroeconomy: GDP, Unemployment, and Inflation

VerifiedAdded on 2023/05/30

|12

|2874

|203

Report

AI Summary

This report provides a macroeconomic snapshot of Brazil, examining the country's economic volatility over recent years, from periods of expansion to recession. It analyzes key factors contributing to Brazil's underperformance compared to other BRIC nations. The report covers real GDP, unemployment rates, and inflation, offering forecasts and policy recommendations for economic revival. It also discusses the nominal and real effective exchange rates and analyzes the risk premium of Brazilian government bonds compared to US Treasury bills, considering factors like credit risk, GDP growth forecasts, political uncertainty, and exchange rates. The report concludes with suggestions for implementing fiscal and monetary policies and addressing inequality to foster economic expansion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Macro Ecomic Snap Shot of Brazil

Executive Summary

Brazil has seen a period of great macro-economic volatility in the last few years. It has gone

from years of economic expansion to a long period of unprecedented economic recession. In

the past, was being touted one of the most exciting countries and was apart of a special group

of countries that were witnessing high growth i.e. Brazil, Russia, India, China . This led to the

formation of the nomenclature of BRIC countries while India and China have sustained

economic expansion, Brazilian economy has disappointed, to some extent. This reports

explores few of the key factors to unndertans the underperformance of the Brazilian economy

Part A...................................................................................................................................... 3

Real Gross Domestic Product.............................................................................................3

Unemployment Rate...........................................................................................................3

Inflation............................................................................................................................... 4

PART B................................................................................................................................... 5

PART C................................................................................................................................... 6

Question 2................................................................................................................................... 6

Part A...................................................................................................................................... 6

Part B...................................................................................................................................... 7

Question 3................................................................................................................................... 8

Part A...................................................................................................................................... 8

Part B.................................................................................................................................... 10

Appendix.................................................................................................................................... 10

References................................................................................................................................ 11

Executive Summary

Brazil has seen a period of great macro-economic volatility in the last few years. It has gone

from years of economic expansion to a long period of unprecedented economic recession. In

the past, was being touted one of the most exciting countries and was apart of a special group

of countries that were witnessing high growth i.e. Brazil, Russia, India, China . This led to the

formation of the nomenclature of BRIC countries while India and China have sustained

economic expansion, Brazilian economy has disappointed, to some extent. This reports

explores few of the key factors to unndertans the underperformance of the Brazilian economy

Part A...................................................................................................................................... 3

Real Gross Domestic Product.............................................................................................3

Unemployment Rate...........................................................................................................3

Inflation............................................................................................................................... 4

PART B................................................................................................................................... 5

PART C................................................................................................................................... 6

Question 2................................................................................................................................... 6

Part A...................................................................................................................................... 6

Part B...................................................................................................................................... 7

Question 3................................................................................................................................... 8

Part A...................................................................................................................................... 8

Part B.................................................................................................................................... 10

Appendix.................................................................................................................................... 10

References................................................................................................................................ 11

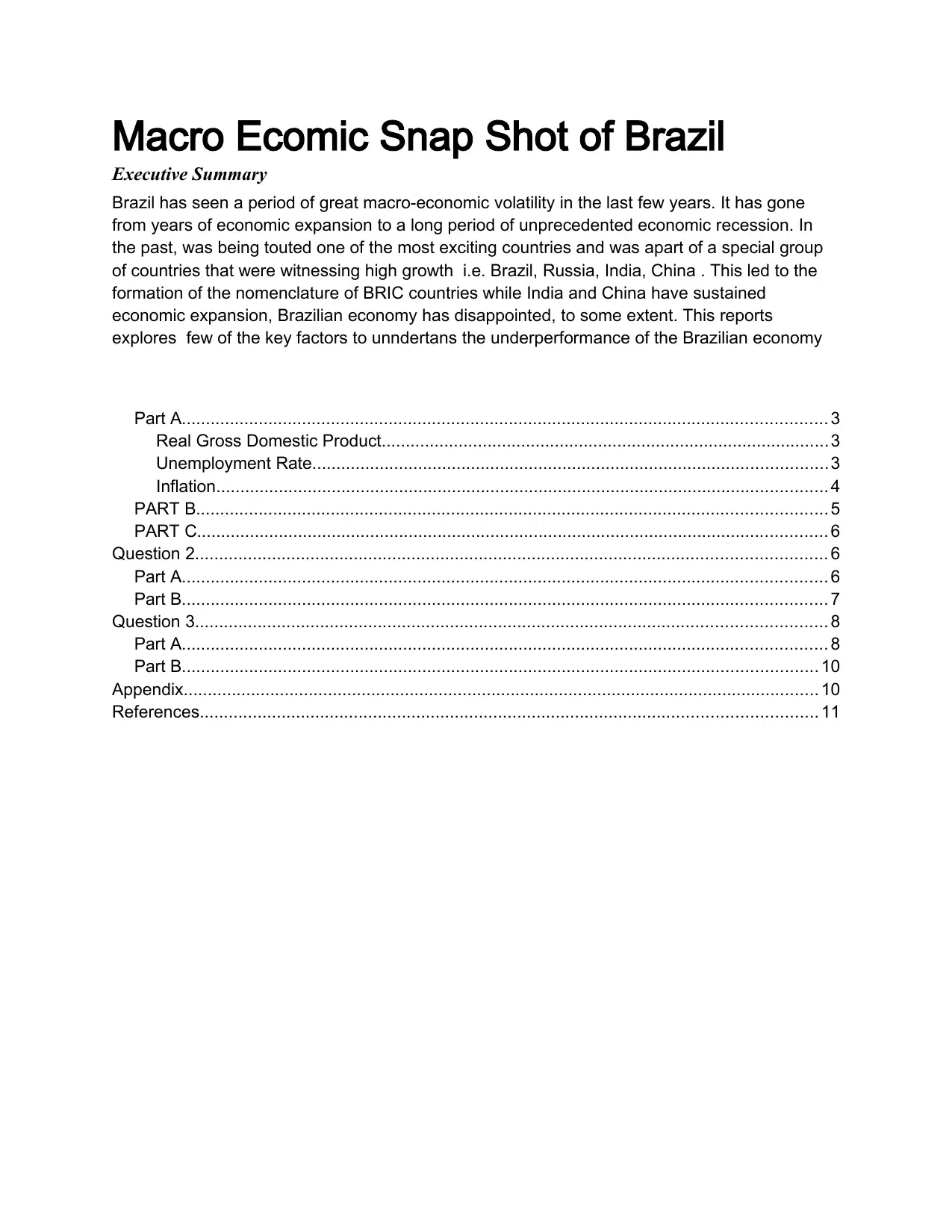

Part A

Real Gross Domestic Product

Brazil experienced a sustained period of GDP expansion prior to 2012, a trend that continued

until 2012 (Organisation for Economic Co-operation and Development, 2018)/ However, this

trend began to change in 2013. (Please refer to Table 1 in Appendix) In 2013, the GDP growth

rate of Brazil, at 2.86 was higher than the world average. However, following 2013, Brazil

started to slip in a recession. According to Organization of Economic Co-operation and

Development “a combination of rising fiscal imbalances, increasingly interventionist economic

policies and unaddressed structural weaknesses have led to a sharp erosion of confidence, which

ultimately led into the economy's strongest recession on record.” (Organisation for Economic

Co-operation and Development, 2018)

This period was characterised by rising budget deficit and high government borrowing.

However, the economy picked up in 2017 owing to a strong harvest, among other factors.

Graph 1.1 GDP Growth Rate. Source: (OECD, 2018) Prepared by Author

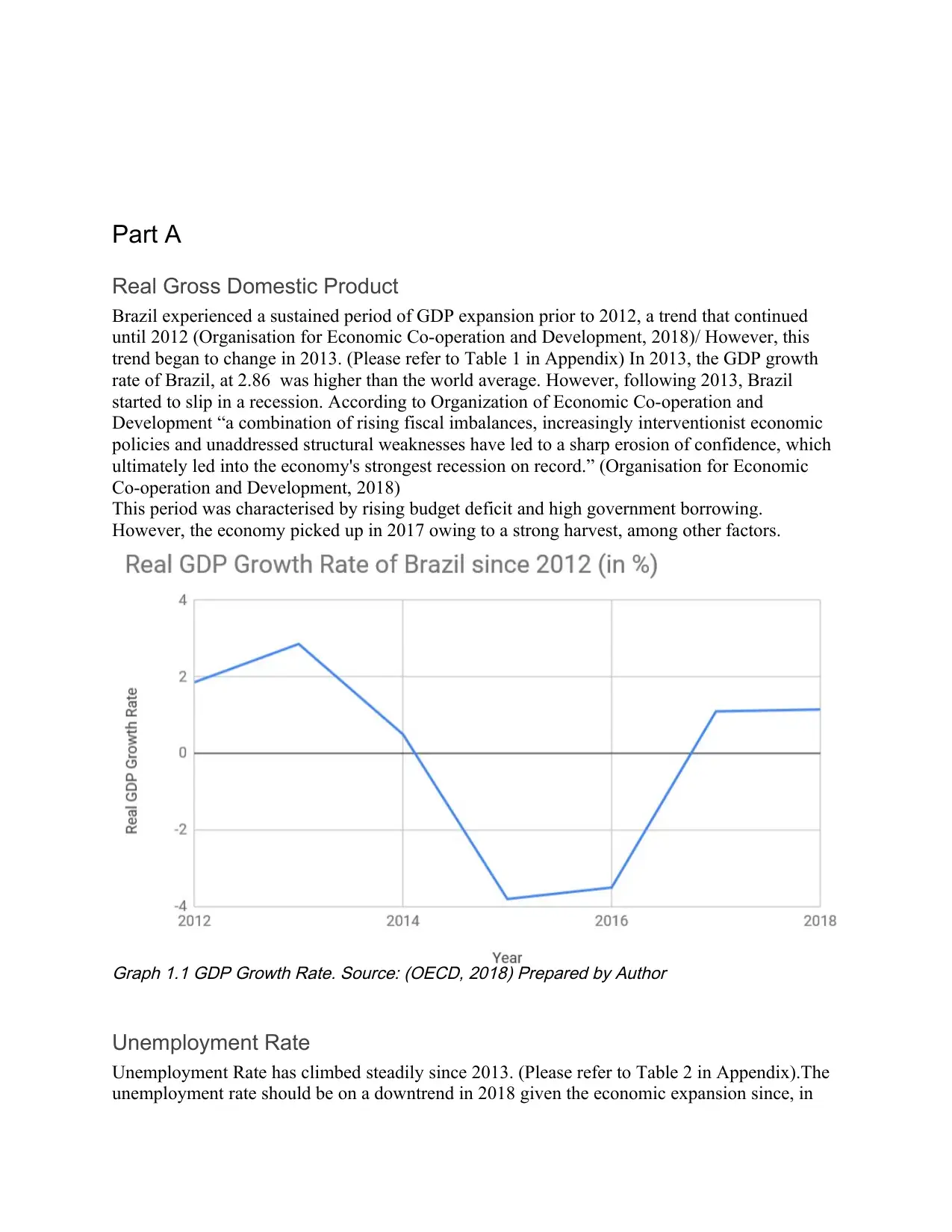

Unemployment Rate

Unemployment Rate has climbed steadily since 2013. (Please refer to Table 2 in Appendix).The

unemployment rate should be on a downtrend in 2018 given the economic expansion since, in

Real Gross Domestic Product

Brazil experienced a sustained period of GDP expansion prior to 2012, a trend that continued

until 2012 (Organisation for Economic Co-operation and Development, 2018)/ However, this

trend began to change in 2013. (Please refer to Table 1 in Appendix) In 2013, the GDP growth

rate of Brazil, at 2.86 was higher than the world average. However, following 2013, Brazil

started to slip in a recession. According to Organization of Economic Co-operation and

Development “a combination of rising fiscal imbalances, increasingly interventionist economic

policies and unaddressed structural weaknesses have led to a sharp erosion of confidence, which

ultimately led into the economy's strongest recession on record.” (Organisation for Economic

Co-operation and Development, 2018)

This period was characterised by rising budget deficit and high government borrowing.

However, the economy picked up in 2017 owing to a strong harvest, among other factors.

Graph 1.1 GDP Growth Rate. Source: (OECD, 2018) Prepared by Author

Unemployment Rate

Unemployment Rate has climbed steadily since 2013. (Please refer to Table 2 in Appendix).The

unemployment rate should be on a downtrend in 2018 given the economic expansion since, in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the past the high unemployment Brazil was in a recession for 2014, 2015 and 2016. (OECD,

2018) High unemployment leads to a vicious circle of low employment- low aggregate demand -

low employment. (Samuelson and Nordhaus, 2010)

Graph 1.2 Unemployment Rate. Source: (OECD, 2018) Prepared by Author

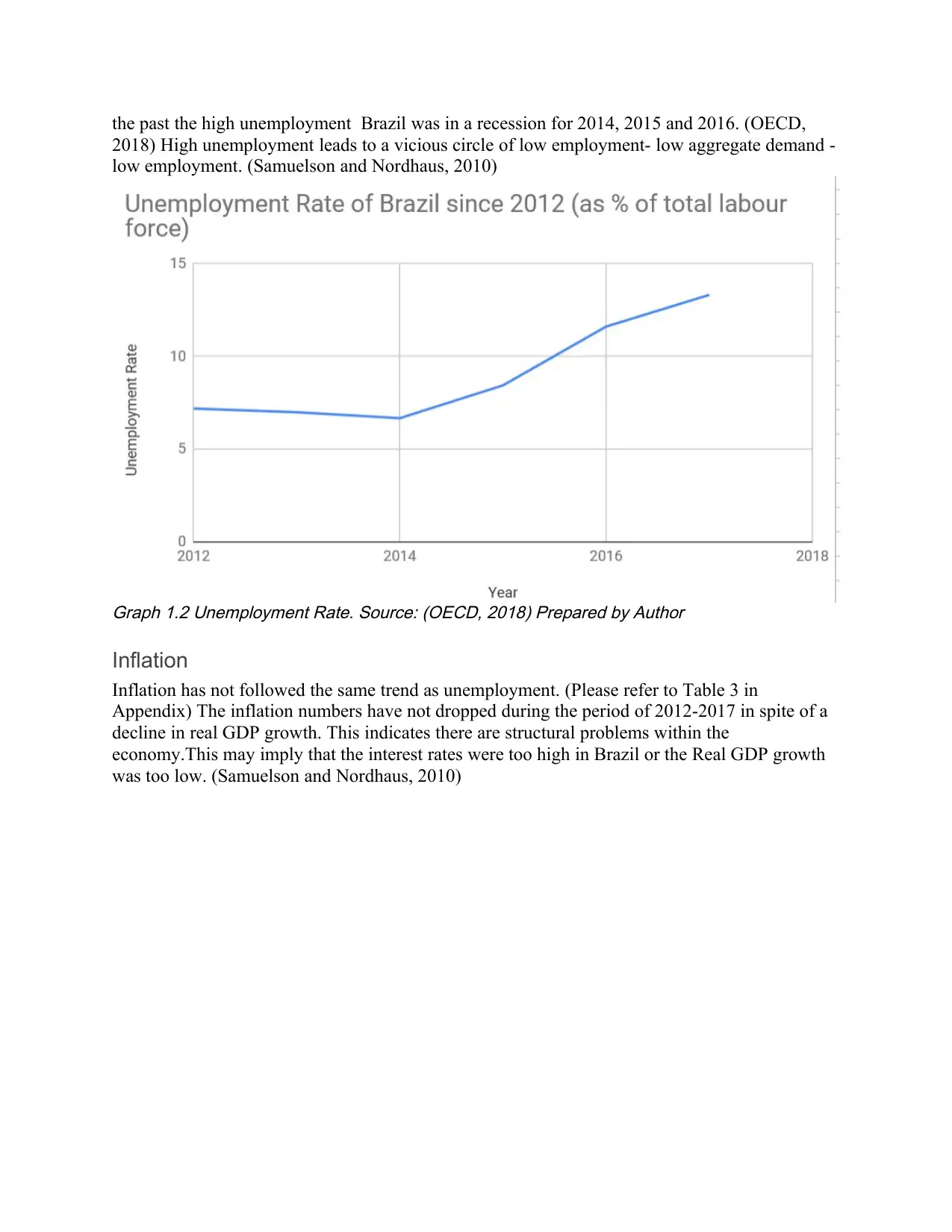

Inflation

Inflation has not followed the same trend as unemployment. (Please refer to Table 3 in

Appendix) The inflation numbers have not dropped during the period of 2012-2017 in spite of a

decline in real GDP growth. This indicates there are structural problems within the

economy.This may imply that the interest rates were too high in Brazil or the Real GDP growth

was too low. (Samuelson and Nordhaus, 2010)

2018) High unemployment leads to a vicious circle of low employment- low aggregate demand -

low employment. (Samuelson and Nordhaus, 2010)

Graph 1.2 Unemployment Rate. Source: (OECD, 2018) Prepared by Author

Inflation

Inflation has not followed the same trend as unemployment. (Please refer to Table 3 in

Appendix) The inflation numbers have not dropped during the period of 2012-2017 in spite of a

decline in real GDP growth. This indicates there are structural problems within the

economy.This may imply that the interest rates were too high in Brazil or the Real GDP growth

was too low. (Samuelson and Nordhaus, 2010)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Graph 1.3 Inflation Rate. Source: (OECD, 2018) Prepared by Author

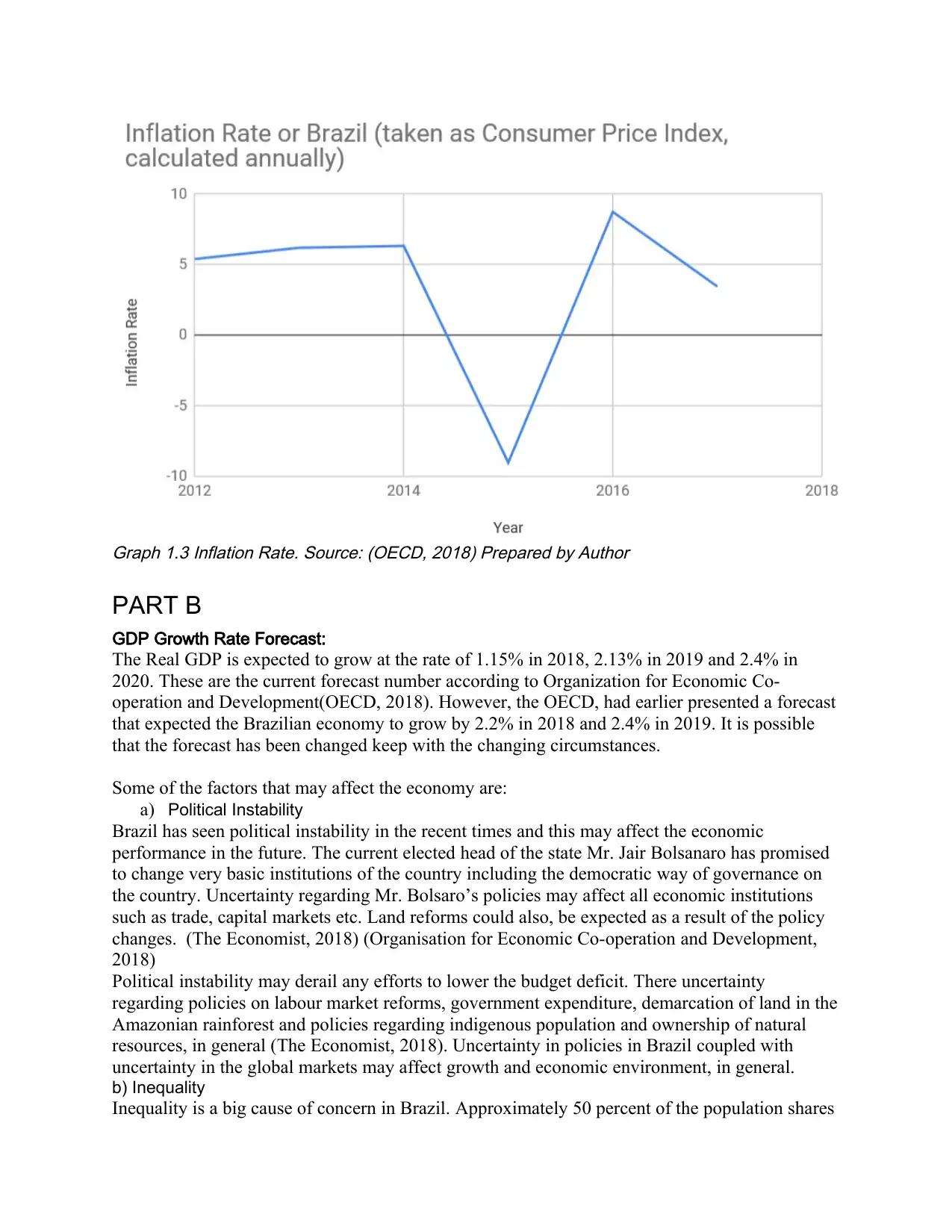

PART B

GDP Growth Rate Forecast:

The Real GDP is expected to grow at the rate of 1.15% in 2018, 2.13% in 2019 and 2.4% in

2020. These are the current forecast number according to Organization for Economic Co-

operation and Development(OECD, 2018). However, the OECD, had earlier presented a forecast

that expected the Brazilian economy to grow by 2.2% in 2018 and 2.4% in 2019. It is possible

that the forecast has been changed keep with the changing circumstances.

Some of the factors that may affect the economy are:

a) Political Instability

Brazil has seen political instability in the recent times and this may affect the economic

performance in the future. The current elected head of the state Mr. Jair Bolsanaro has promised

to change very basic institutions of the country including the democratic way of governance on

the country. Uncertainty regarding Mr. Bolsaro’s policies may affect all economic institutions

such as trade, capital markets etc. Land reforms could also, be expected as a result of the policy

changes. (The Economist, 2018) (Organisation for Economic Co-operation and Development,

2018)

Political instability may derail any efforts to lower the budget deficit. There uncertainty

regarding policies on labour market reforms, government expenditure, demarcation of land in the

Amazonian rainforest and policies regarding indigenous population and ownership of natural

resources, in general (The Economist, 2018). Uncertainty in policies in Brazil coupled with

uncertainty in the global markets may affect growth and economic environment, in general.

b) Inequality

Inequality is a big cause of concern in Brazil. Approximately 50 percent of the population shares

PART B

GDP Growth Rate Forecast:

The Real GDP is expected to grow at the rate of 1.15% in 2018, 2.13% in 2019 and 2.4% in

2020. These are the current forecast number according to Organization for Economic Co-

operation and Development(OECD, 2018). However, the OECD, had earlier presented a forecast

that expected the Brazilian economy to grow by 2.2% in 2018 and 2.4% in 2019. It is possible

that the forecast has been changed keep with the changing circumstances.

Some of the factors that may affect the economy are:

a) Political Instability

Brazil has seen political instability in the recent times and this may affect the economic

performance in the future. The current elected head of the state Mr. Jair Bolsanaro has promised

to change very basic institutions of the country including the democratic way of governance on

the country. Uncertainty regarding Mr. Bolsaro’s policies may affect all economic institutions

such as trade, capital markets etc. Land reforms could also, be expected as a result of the policy

changes. (The Economist, 2018) (Organisation for Economic Co-operation and Development,

2018)

Political instability may derail any efforts to lower the budget deficit. There uncertainty

regarding policies on labour market reforms, government expenditure, demarcation of land in the

Amazonian rainforest and policies regarding indigenous population and ownership of natural

resources, in general (The Economist, 2018). Uncertainty in policies in Brazil coupled with

uncertainty in the global markets may affect growth and economic environment, in general.

b) Inequality

Inequality is a big cause of concern in Brazil. Approximately 50 percent of the population shares

10% of the total household incomes, while other half holds 90%. Inequality also, persists in the

form of gender gap in wages. Gender Pay disparity is higher than the OECD average with male

workers being paid approximately, 50% more than female counterparts (in the formal sector), a

gap that is 10 percentage points higher than the OECD average. (Organisation for Economic Co-

operation and Development, 2018)

One of the reasons for the recent recession in Brazil has been cited as structural inefficiencies in

Brazil. (Organisation for Economic Co-operation and Development, 2018) In order to go remove

structural problems, Brazil must address the problem of inequality.

PART C

The following are some strong suggestions, in order to revive the economic expansion of Brazil

in the near term.

1) Implementation of mildly contractionary Fiscal and Monetary Policy measures:

Economic Expansion is expected in Brazil.(Organisation for Economic Co-operation and

Development, 2018)

Hence, raising taxes on the wealthiest class (to be defined) will help reduce the budget

deficit. Inflation would also, be expected to rise, given the expected rise in the real GDP

of the country. Hence, there is no need to increase interest rates. Increasing interest rates

marginally will allow further savings. Further, increasing interest rates may indirectly

help in raising the value of Brazilian Real. It is important to note here that the

recommendation is to increase the interest rates and taxes, only marginally, in order to

ensure that the economic expansion is not arrested.

2) Lower Government Spending: In the last couple of years, lowering government spending

was not possible due to the recession. (Organisation for Economic Co-operation and

Development, 2018), However, the economy is out of the recession. Hence, efforts must

be made of lower government spending, in order to reduce budget deficit and service

government debt.

Question 2

Part A

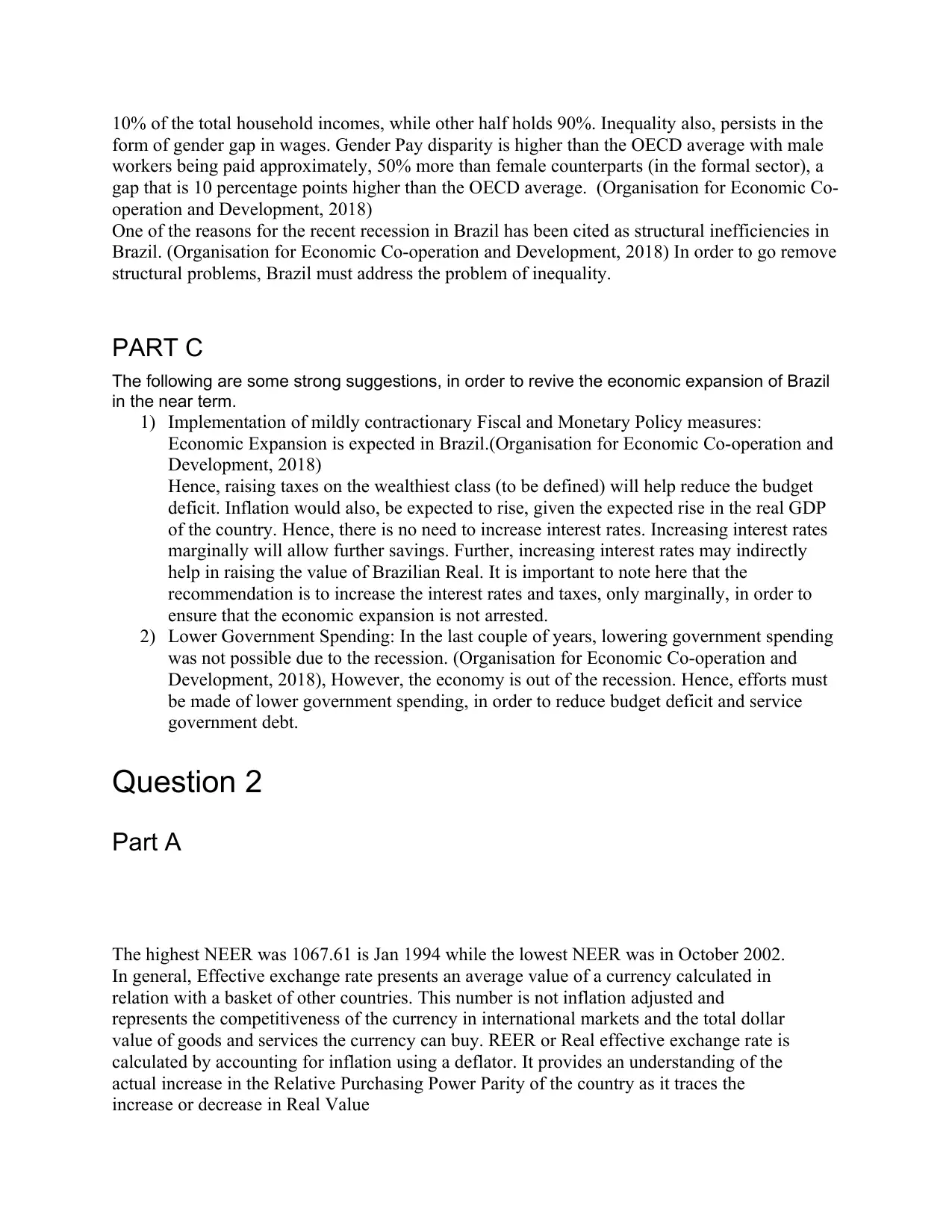

The highest NEER was 1067.61 is Jan 1994 while the lowest NEER was in October 2002.

In general, Effective exchange rate presents an average value of a currency calculated in

relation with a basket of other countries. This number is not inflation adjusted and

represents the competitiveness of the currency in international markets and the total dollar

value of goods and services the currency can buy. REER or Real effective exchange rate is

calculated by accounting for inflation using a deflator. It provides an understanding of the

actual increase in the Relative Purchasing Power Parity of the country as it traces the

increase or decrease in Real Value

form of gender gap in wages. Gender Pay disparity is higher than the OECD average with male

workers being paid approximately, 50% more than female counterparts (in the formal sector), a

gap that is 10 percentage points higher than the OECD average. (Organisation for Economic Co-

operation and Development, 2018)

One of the reasons for the recent recession in Brazil has been cited as structural inefficiencies in

Brazil. (Organisation for Economic Co-operation and Development, 2018) In order to go remove

structural problems, Brazil must address the problem of inequality.

PART C

The following are some strong suggestions, in order to revive the economic expansion of Brazil

in the near term.

1) Implementation of mildly contractionary Fiscal and Monetary Policy measures:

Economic Expansion is expected in Brazil.(Organisation for Economic Co-operation and

Development, 2018)

Hence, raising taxes on the wealthiest class (to be defined) will help reduce the budget

deficit. Inflation would also, be expected to rise, given the expected rise in the real GDP

of the country. Hence, there is no need to increase interest rates. Increasing interest rates

marginally will allow further savings. Further, increasing interest rates may indirectly

help in raising the value of Brazilian Real. It is important to note here that the

recommendation is to increase the interest rates and taxes, only marginally, in order to

ensure that the economic expansion is not arrested.

2) Lower Government Spending: In the last couple of years, lowering government spending

was not possible due to the recession. (Organisation for Economic Co-operation and

Development, 2018), However, the economy is out of the recession. Hence, efforts must

be made of lower government spending, in order to reduce budget deficit and service

government debt.

Question 2

Part A

The highest NEER was 1067.61 is Jan 1994 while the lowest NEER was in October 2002.

In general, Effective exchange rate presents an average value of a currency calculated in

relation with a basket of other countries. This number is not inflation adjusted and

represents the competitiveness of the currency in international markets and the total dollar

value of goods and services the currency can buy. REER or Real effective exchange rate is

calculated by accounting for inflation using a deflator. It provides an understanding of the

actual increase in the Relative Purchasing Power Parity of the country as it traces the

increase or decrease in Real Value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Graph 1: Nominal and Real Effective Exchange Rates. Source: (Bank of International

Settlements, 2018) . Prepared by author

Part B

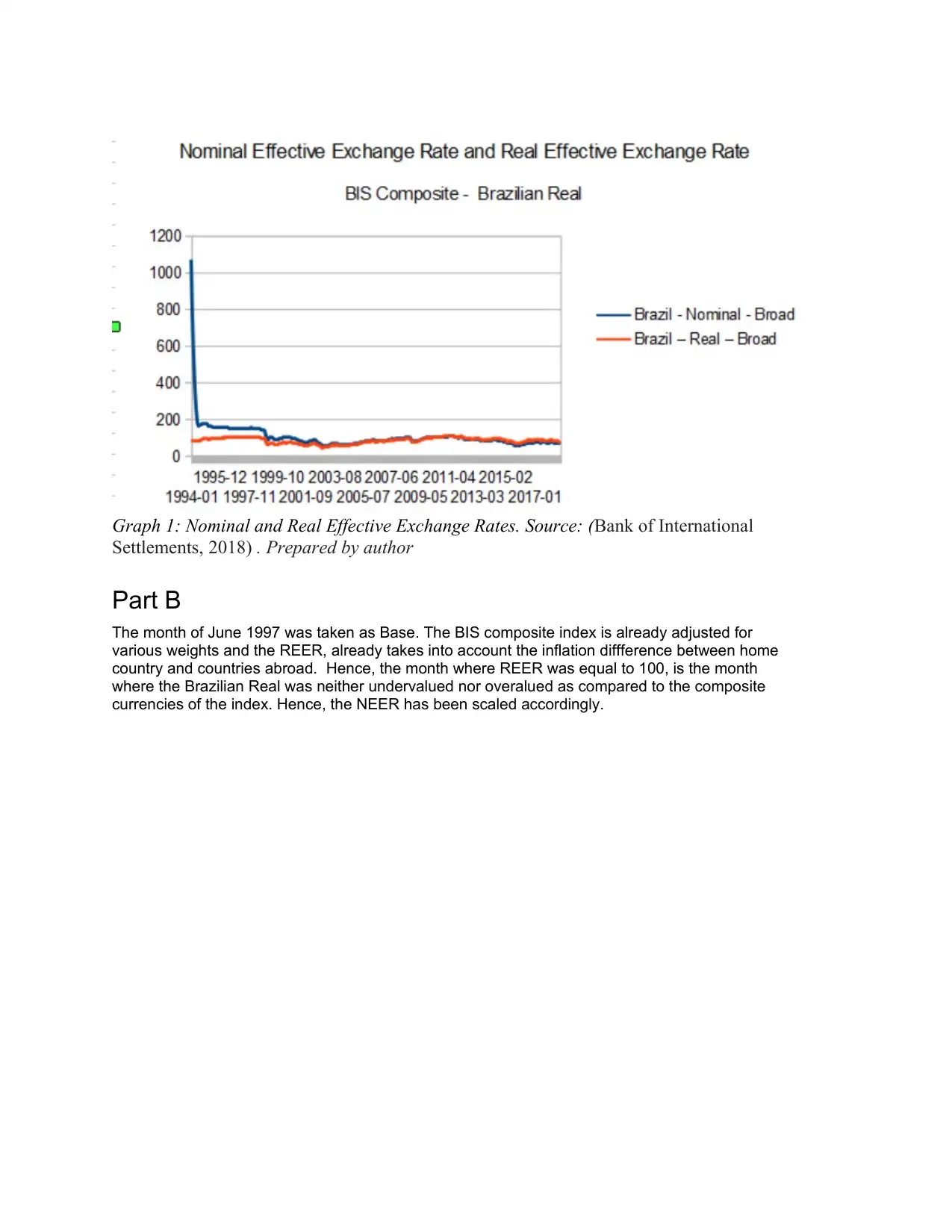

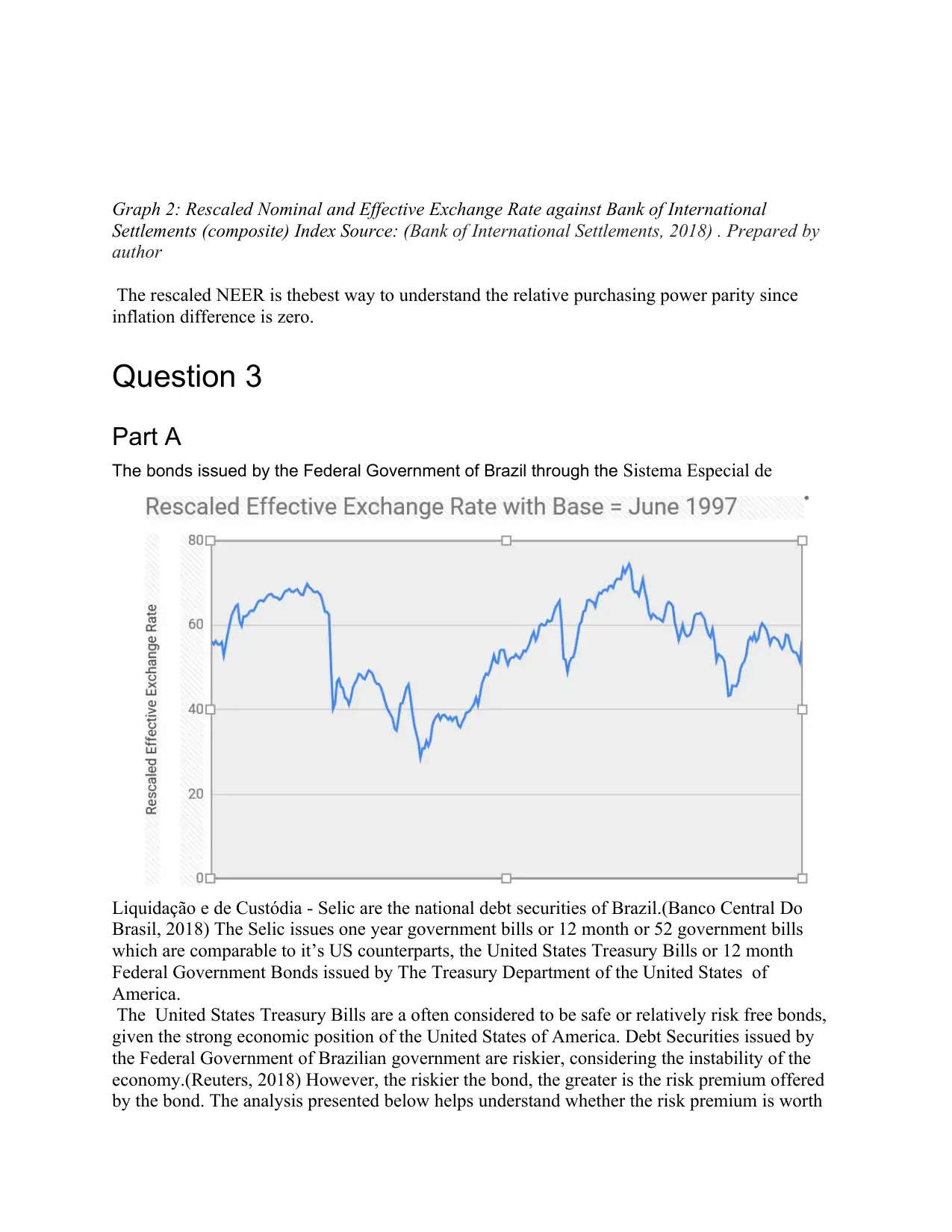

The month of June 1997 was taken as Base. The BIS composite index is already adjusted for

various weights and the REER, already takes into account the inflation diffference between home

country and countries abroad. Hence, the month where REER was equal to 100, is the month

where the Brazilian Real was neither undervalued nor overalued as compared to the composite

currencies of the index. Hence, the NEER has been scaled accordingly.

Settlements, 2018) . Prepared by author

Part B

The month of June 1997 was taken as Base. The BIS composite index is already adjusted for

various weights and the REER, already takes into account the inflation diffference between home

country and countries abroad. Hence, the month where REER was equal to 100, is the month

where the Brazilian Real was neither undervalued nor overalued as compared to the composite

currencies of the index. Hence, the NEER has been scaled accordingly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Graph 2: Rescaled Nominal and Effective Exchange Rate against Bank of International

Settlements (composite) Index Source: (Bank of International Settlements, 2018) . Prepared by

author

The rescaled NEER is thebest way to understand the relative purchasing power parity since

inflation difference is zero.

Question 3

Part A

The bonds issued by the Federal Government of Brazil through the Sistema Especial de

Liquidação e de Custódia - Selic are the national debt securities of Brazil.(Banco Central Do

Brasil, 2018) The Selic issues one year government bills or 12 month or 52 government bills

which are comparable to it’s US counterparts, the United States Treasury Bills or 12 month

Federal Government Bonds issued by The Treasury Department of the United States of

America.

The United States Treasury Bills are a often considered to be safe or relatively risk free bonds,

given the strong economic position of the United States of America. Debt Securities issued by

the Federal Government of Brazilian government are riskier, considering the instability of the

economy.(Reuters, 2018) However, the riskier the bond, the greater is the risk premium offered

by the bond. The analysis presented below helps understand whether the risk premium is worth

Settlements (composite) Index Source: (Bank of International Settlements, 2018) . Prepared by

author

The rescaled NEER is thebest way to understand the relative purchasing power parity since

inflation difference is zero.

Question 3

Part A

The bonds issued by the Federal Government of Brazil through the Sistema Especial de

Liquidação e de Custódia - Selic are the national debt securities of Brazil.(Banco Central Do

Brasil, 2018) The Selic issues one year government bills or 12 month or 52 government bills

which are comparable to it’s US counterparts, the United States Treasury Bills or 12 month

Federal Government Bonds issued by The Treasury Department of the United States of

America.

The United States Treasury Bills are a often considered to be safe or relatively risk free bonds,

given the strong economic position of the United States of America. Debt Securities issued by

the Federal Government of Brazilian government are riskier, considering the instability of the

economy.(Reuters, 2018) However, the riskier the bond, the greater is the risk premium offered

by the bond. The analysis presented below helps understand whether the risk premium is worth

the investment:

The Consensus Rate or CDI rate or Selic rate for 52 weeks Selic debt security is currently over

6% per annum (6.50 pcpa on December 1, 2018). Conversely, the US Treasury bills have

remained between 2% per annum and 2.5 % per annum. (‘Board of Governors of the Federal

Reserve System (USA)’, 2018) in the secondary market.

Some of the factors that influence the investment decision are as follows:

a) Credit Risk Ratings: Credit risks directly indicate the risk of default of payment by the

issuer of the debt security. Credit Risk ratings published by various financial firms such

as Standard and Poor’s Inc, Moody’s Investor Service, often calculate the risks and

provide ratings to such securities. Poor ratings suggest higher default risks. Hence, these

ratings are important in assessment of investment. (Moody’s Investor Services, 2018)

b) Real GDP growth rate forecast of Brazil and USA for the next 12 months: The

Real GDP forecast will determine all other factors such as inflation, government debt, fiscal and

monetary policy etc. All of these factors affect the yield of the security. Hence, the projected

GDP for 2019 is a major factor. (OECD, 2018)

c) Political and Economic Uncertainty: Certainty regarding policies, especially those related to

economics, help decide the direction of thee economy. In the absence of an understanding of

which direction the economy will take investment decisions. (Organisation for Economic Co-

operation and Development, 2018)

d) Effective Exchange Rate: The projected forward curve of the exchange rates for the

Brazilian Real i.e the forecast of Nominal Effective Exchange Rate and real Effective Exchange

Rate(International Monetary Fund, 2018) The forecasted exchange rates, especially, against the

US Dollar will help determine the investment, even though this is a minor factor. Exchange rates

help determine the total Dollar bill of exports and imports to a great extent. For example, coffee

is one of the key exports of Brazil. Apart from coffee prices, the exchange rate of Brazil may

affect the export bill. This is turn, affects budget deficit of Brazil which in turn affects

government spending in the economy. This will directly affect the Aggregate Demand, inflation,

interest rates and government debt. (Organisation for Economic Co-operation and Development,

2018)

Favourable Factors:

a) GDP forecast: The project GDP growth rate for Brazil is 1.15 in 2018 and 2.13 in 2019.

The projected growth rate for United States in 2019 is 2.1%.(OECD, 2018) The

forecasted real growth rates for both countries are more or less similar. Hence, it is

difficult to favour investment in Brazil based on this factor alone.

Unfavourable Factors:

a) Credit Risk: Standard and Poor awarded the debt securities of the Federal Government

of Brazil, especial the short term Selic securities a rating of “BB” in January 2018

indicating high default risk.(Reuters, 2018) The credit risk ratings also factor in the

The Consensus Rate or CDI rate or Selic rate for 52 weeks Selic debt security is currently over

6% per annum (6.50 pcpa on December 1, 2018). Conversely, the US Treasury bills have

remained between 2% per annum and 2.5 % per annum. (‘Board of Governors of the Federal

Reserve System (USA)’, 2018) in the secondary market.

Some of the factors that influence the investment decision are as follows:

a) Credit Risk Ratings: Credit risks directly indicate the risk of default of payment by the

issuer of the debt security. Credit Risk ratings published by various financial firms such

as Standard and Poor’s Inc, Moody’s Investor Service, often calculate the risks and

provide ratings to such securities. Poor ratings suggest higher default risks. Hence, these

ratings are important in assessment of investment. (Moody’s Investor Services, 2018)

b) Real GDP growth rate forecast of Brazil and USA for the next 12 months: The

Real GDP forecast will determine all other factors such as inflation, government debt, fiscal and

monetary policy etc. All of these factors affect the yield of the security. Hence, the projected

GDP for 2019 is a major factor. (OECD, 2018)

c) Political and Economic Uncertainty: Certainty regarding policies, especially those related to

economics, help decide the direction of thee economy. In the absence of an understanding of

which direction the economy will take investment decisions. (Organisation for Economic Co-

operation and Development, 2018)

d) Effective Exchange Rate: The projected forward curve of the exchange rates for the

Brazilian Real i.e the forecast of Nominal Effective Exchange Rate and real Effective Exchange

Rate(International Monetary Fund, 2018) The forecasted exchange rates, especially, against the

US Dollar will help determine the investment, even though this is a minor factor. Exchange rates

help determine the total Dollar bill of exports and imports to a great extent. For example, coffee

is one of the key exports of Brazil. Apart from coffee prices, the exchange rate of Brazil may

affect the export bill. This is turn, affects budget deficit of Brazil which in turn affects

government spending in the economy. This will directly affect the Aggregate Demand, inflation,

interest rates and government debt. (Organisation for Economic Co-operation and Development,

2018)

Favourable Factors:

a) GDP forecast: The project GDP growth rate for Brazil is 1.15 in 2018 and 2.13 in 2019.

The projected growth rate for United States in 2019 is 2.1%.(OECD, 2018) The

forecasted real growth rates for both countries are more or less similar. Hence, it is

difficult to favour investment in Brazil based on this factor alone.

Unfavourable Factors:

a) Credit Risk: Standard and Poor awarded the debt securities of the Federal Government

of Brazil, especial the short term Selic securities a rating of “BB” in January 2018

indicating high default risk.(Reuters, 2018) The credit risk ratings also factor in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

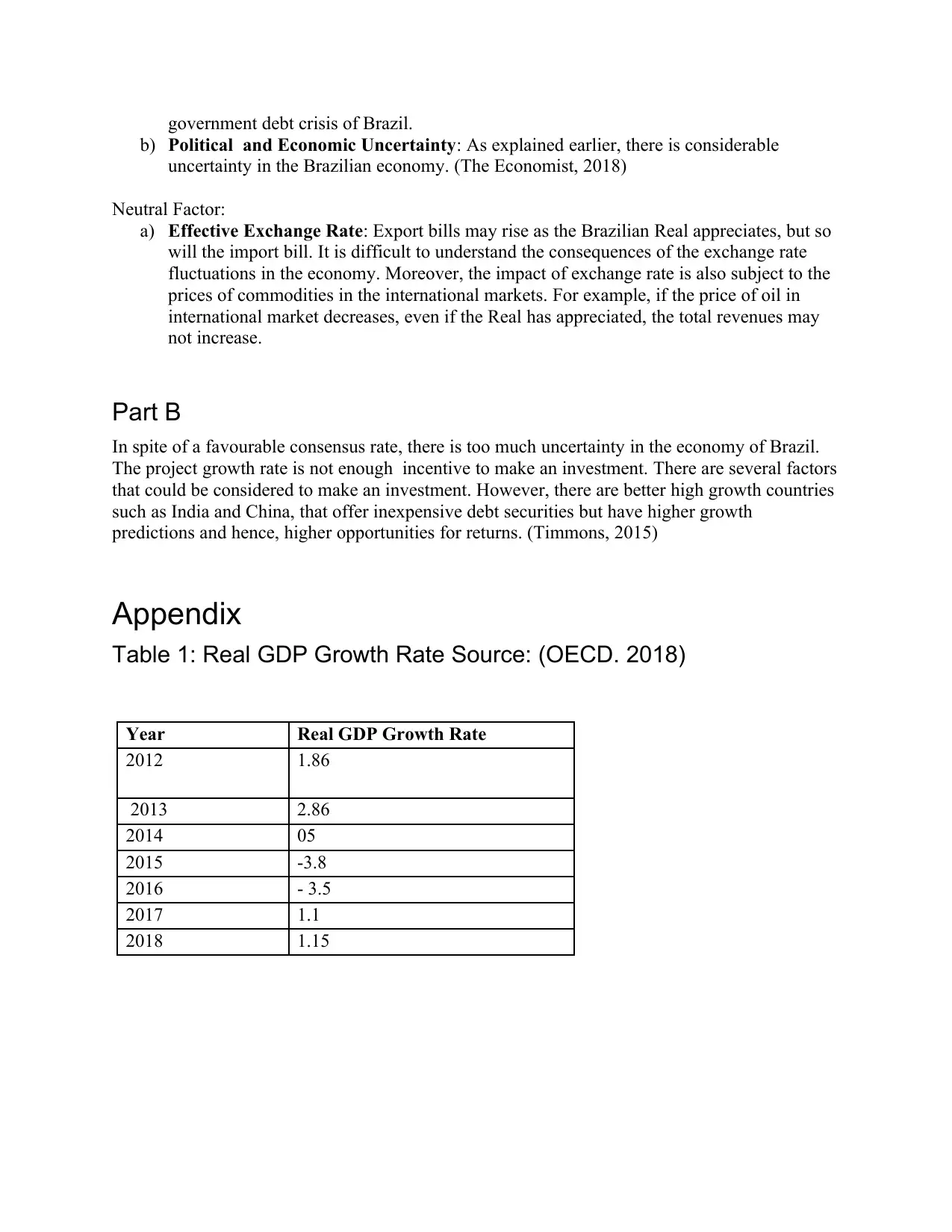

government debt crisis of Brazil.

b) Political and Economic Uncertainty: As explained earlier, there is considerable

uncertainty in the Brazilian economy. (The Economist, 2018)

Neutral Factor:

a) Effective Exchange Rate: Export bills may rise as the Brazilian Real appreciates, but so

will the import bill. It is difficult to understand the consequences of the exchange rate

fluctuations in the economy. Moreover, the impact of exchange rate is also subject to the

prices of commodities in the international markets. For example, if the price of oil in

international market decreases, even if the Real has appreciated, the total revenues may

not increase.

Part B

In spite of a favourable consensus rate, there is too much uncertainty in the economy of Brazil.

The project growth rate is not enough incentive to make an investment. There are several factors

that could be considered to make an investment. However, there are better high growth countries

such as India and China, that offer inexpensive debt securities but have higher growth

predictions and hence, higher opportunities for returns. (Timmons, 2015)

Appendix

Table 1: Real GDP Growth Rate Source: (OECD. 2018)

Year Real GDP Growth Rate

2012 1.86

2013 2.86

2014 05

2015 -3.8

2016 - 3.5

2017 1.1

2018 1.15

b) Political and Economic Uncertainty: As explained earlier, there is considerable

uncertainty in the Brazilian economy. (The Economist, 2018)

Neutral Factor:

a) Effective Exchange Rate: Export bills may rise as the Brazilian Real appreciates, but so

will the import bill. It is difficult to understand the consequences of the exchange rate

fluctuations in the economy. Moreover, the impact of exchange rate is also subject to the

prices of commodities in the international markets. For example, if the price of oil in

international market decreases, even if the Real has appreciated, the total revenues may

not increase.

Part B

In spite of a favourable consensus rate, there is too much uncertainty in the economy of Brazil.

The project growth rate is not enough incentive to make an investment. There are several factors

that could be considered to make an investment. However, there are better high growth countries

such as India and China, that offer inexpensive debt securities but have higher growth

predictions and hence, higher opportunities for returns. (Timmons, 2015)

Appendix

Table 1: Real GDP Growth Rate Source: (OECD. 2018)

Year Real GDP Growth Rate

2012 1.86

2013 2.86

2014 05

2015 -3.8

2016 - 3.5

2017 1.1

2018 1.15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

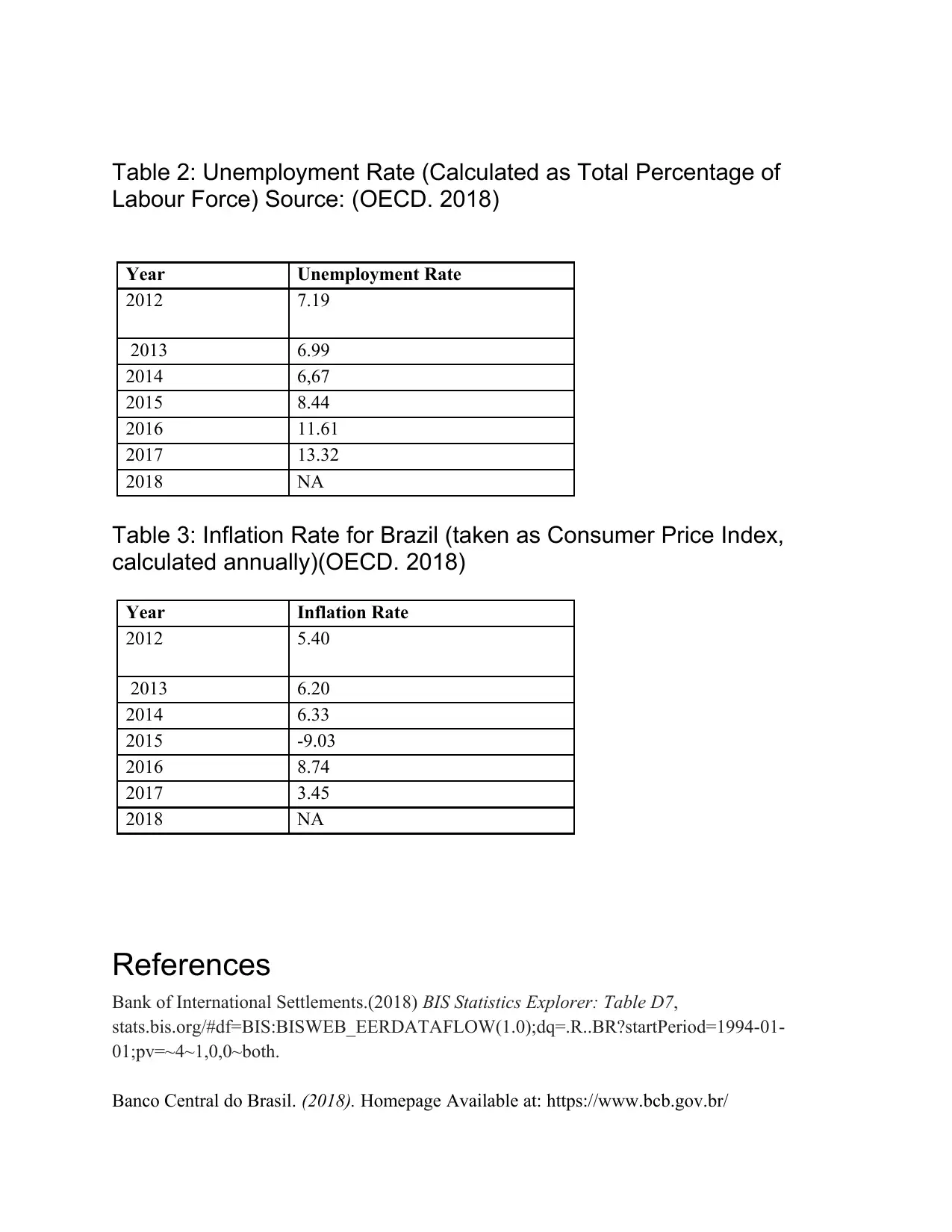

Table 2: Unemployment Rate (Calculated as Total Percentage of

Labour Force) Source: (OECD. 2018)

Year Unemployment Rate

2012 7.19

2013 6.99

2014 6,67

2015 8.44

2016 11.61

2017 13.32

2018 NA

Table 3: Inflation Rate for Brazil (taken as Consumer Price Index,

calculated annually)(OECD. 2018)

Year Inflation Rate

2012 5.40

2013 6.20

2014 6.33

2015 -9.03

2016 8.74

2017 3.45

2018 NA

References

Bank of International Settlements.(2018) BIS Statistics Explorer: Table D7,

stats.bis.org/#df=BIS:BISWEB_EERDATAFLOW(1.0);dq=.R..BR?startPeriod=1994-01-

01;pv=~4~1,0,0~both.

Banco Central do Brasil. (2018). Homepage Available at: https://www.bcb.gov.br/

Labour Force) Source: (OECD. 2018)

Year Unemployment Rate

2012 7.19

2013 6.99

2014 6,67

2015 8.44

2016 11.61

2017 13.32

2018 NA

Table 3: Inflation Rate for Brazil (taken as Consumer Price Index,

calculated annually)(OECD. 2018)

Year Inflation Rate

2012 5.40

2013 6.20

2014 6.33

2015 -9.03

2016 8.74

2017 3.45

2018 NA

References

Bank of International Settlements.(2018) BIS Statistics Explorer: Table D7,

stats.bis.org/#df=BIS:BISWEB_EERDATAFLOW(1.0);dq=.R..BR?startPeriod=1994-01-

01;pv=~4~1,0,0~both.

Banco Central do Brasil. (2018). Homepage Available at: https://www.bcb.gov.br/

Banco Central do Brasil.(2018) Selic - Introduction. Available at: https://www.bcb.gov.br/.

Board of Governors of the Federal Reserve System (USA), 1-Year Treasury Bill: Secondary

Market Rate [TB1YR], retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/TB1YR, December 2, 2018.

International Monetary Fund (2018) What is real effective exchange rate (REER)? IMF DATA

Help. Available at: http://datahelp.imf.org/knowledgebase/articles/537472-what-is-real-effective-

exchange-rate-reer.

Moody’s Investor Services (2018) Rating Symbols and Definitions. redirecting. Available at:

https://www.moodys.com/Pages/amr0

OECD (2018), Inflation (CPI) (indicator). doi: 10.1787/eee82e6e-en (Accessed on 01 December

2018)

OECD (2018), Real GDP forecast (indicator). doi: 10.1787/1f84150b-en (Accessed on 30

November 2018)

Organization for Economic Co-operation and Development (2018), Economic Survey of Brazil

2018. Estadísticas - OECD. Available at: http://www.oecd.org/eco/surveys/economic-survey-

brazil.htm.

Reuters (2018). S&P cuts Brazil credit rating as pension reform doubts grow. Reuters. Available

at: https://www.reuters.com/article/brazil-sovereign-downgrade/sp-cuts-brazil-credit-rating-as-

pension-reform-doubts-grow-idUSL1N1P628Y.

Samuelson, P.A. & Nordhaus, W.D., 2010. Economics, McGraw-Hill.

The Economist (2018): „Containing Jair Bolsonaro“. The Economist, Print Edition. The

Economist Newspaper Retrieved am from

https://www.economist.com/leaders/2018/10/27/containing-jair-bolsonaro.

Timmons, H., 2015. The BRICs era is over, even at Goldman Sachs. Quartz. Available at:

https://qz.com/544410/the-brics-era-is-over-even-at-goldman-sachs/.

Board of Governors of the Federal Reserve System (USA), 1-Year Treasury Bill: Secondary

Market Rate [TB1YR], retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/TB1YR, December 2, 2018.

International Monetary Fund (2018) What is real effective exchange rate (REER)? IMF DATA

Help. Available at: http://datahelp.imf.org/knowledgebase/articles/537472-what-is-real-effective-

exchange-rate-reer.

Moody’s Investor Services (2018) Rating Symbols and Definitions. redirecting. Available at:

https://www.moodys.com/Pages/amr0

OECD (2018), Inflation (CPI) (indicator). doi: 10.1787/eee82e6e-en (Accessed on 01 December

2018)

OECD (2018), Real GDP forecast (indicator). doi: 10.1787/1f84150b-en (Accessed on 30

November 2018)

Organization for Economic Co-operation and Development (2018), Economic Survey of Brazil

2018. Estadísticas - OECD. Available at: http://www.oecd.org/eco/surveys/economic-survey-

brazil.htm.

Reuters (2018). S&P cuts Brazil credit rating as pension reform doubts grow. Reuters. Available

at: https://www.reuters.com/article/brazil-sovereign-downgrade/sp-cuts-brazil-credit-rating-as-

pension-reform-doubts-grow-idUSL1N1P628Y.

Samuelson, P.A. & Nordhaus, W.D., 2010. Economics, McGraw-Hill.

The Economist (2018): „Containing Jair Bolsonaro“. The Economist, Print Edition. The

Economist Newspaper Retrieved am from

https://www.economist.com/leaders/2018/10/27/containing-jair-bolsonaro.

Timmons, H., 2015. The BRICs era is over, even at Goldman Sachs. Quartz. Available at:

https://qz.com/544410/the-brics-era-is-over-even-at-goldman-sachs/.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.