AFE7002-A: Corporate Finance Project - British American Tobacco

VerifiedAdded on 2023/06/07

|25

|5160

|204

Report

AI Summary

This report presents a valuation study of British American Tobacco, employing methods such as the economic valuation model, net asset valuation model, total shareholder return (TSR), comparable ratio analysis, and discounted cash flow (DCF) to assess the company's investment position. The EVA analysis indicates a current value of $4,743,796.77, while the total shareholder return over the past five years is 28.39%, reflecting a strong market position. However, the DCF valuation suggests that the intrinsic value is lower than the market value, implying the stock is overvalued. Based on this analysis, the report concludes that the stock price of British American Tobacco is overvalued, making it a less favorable investment choice.

Running Head: Corporate Finance

1

Project Report: Corporate Finance

1

Project Report: Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

2

Executive summary

A valuation study has been performed on the British American Tobacco in the report.

It focuses on the economic valuation model, net asset valuation model, total share holder

return, comparable ratio, discounted cash flows etc methods to identify the position of the

business in terms of the investment. The EVA analysis express that the current EVA of the

company is $ 4743796.77. the total shareholder return of last 5 years are 28.39%. the position

of TSR is highest in the current market.

Further, the DCF valuation method expresses that the intrinsic value of the company

is lower than the market value which means the stock is overvalued. On the basis of the

study, the stock price of the company is undervalued and thus the company is not a good

choice for the purpose of investment.

2

Executive summary

A valuation study has been performed on the British American Tobacco in the report.

It focuses on the economic valuation model, net asset valuation model, total share holder

return, comparable ratio, discounted cash flows etc methods to identify the position of the

business in terms of the investment. The EVA analysis express that the current EVA of the

company is $ 4743796.77. the total shareholder return of last 5 years are 28.39%. the position

of TSR is highest in the current market.

Further, the DCF valuation method expresses that the intrinsic value of the company

is lower than the market value which means the stock is overvalued. On the basis of the

study, the stock price of the company is undervalued and thus the company is not a good

choice for the purpose of investment.

Corporate Finance

3

Contents

Introduction...........................................................................................................................................4

Company overview................................................................................................................................4

EVA analysis.........................................................................................................................................4

Total shareholder return.........................................................................................................................5

Net asset value.......................................................................................................................................7

Comparable ratios..................................................................................................................................7

Discounted cash flow............................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Appendix.............................................................................................................................................13

3

Contents

Introduction...........................................................................................................................................4

Company overview................................................................................................................................4

EVA analysis.........................................................................................................................................4

Total shareholder return.........................................................................................................................5

Net asset value.......................................................................................................................................7

Comparable ratios..................................................................................................................................7

Discounted cash flow............................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Appendix.............................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Finance

4

Introduction:

The report has been prepared to identify the various tools to identify the value of a

business in the marketplace. A business and the investors are required to identify various

tools and techniques on the basis of which the correct worth of the business could be

recognized. In this report, BRITISH AMERICAN TOBACCO PLC has been taken into the

concern and various financial tools such as EVA analysis, total shareholder return, net asset

value, ratios, discounted cash flows etc have been calculated on the company to reach over a

conclusion about the overall performance of the company in the market and the investment

position of the company (Lumby and Jones, 2007).

Company overview:

BRITISH AMERICAN TOBACCO PLC is a British multinational company which

operates its activities under tobacco industry in the US market. Headquarter of the company

is in London. The company services its products and revises at worldwide. It is one of the

leading companies in around 50 countries in tobacco industry. The company has managed

better strategies and financial planning to improve the overall performance of the business in

the industry (Home, 2018).

EVA analysis:

Economic value added is a measurement tool to identify the residual value of an

organization. It valuates the financial performance of the business on the basis of the

operating profits and the cost of capita of the business. It briefs the exact economic value of

the business (Madura, 2014). The EVA analysis has been done on BRITISH AMERICAN

TOBACCO PLC to identify the economic worth of the business.

For analyzing the EVA figures of the business, the operating profit of the business has

been collected form the annual report of the company. The US corporate tax which is 20%

has been taken into the context further. The WACC of each year has been calculated through

collecting the data from various authentic websites and the US official websites. On the basis

of the overall EVA analysis, it has been found that the EVA position of the company as

enough strong in the year of 2013. But along with the time, a decrement has been seen in the

economic profit position of the company (lord, 2007).

4

Introduction:

The report has been prepared to identify the various tools to identify the value of a

business in the marketplace. A business and the investors are required to identify various

tools and techniques on the basis of which the correct worth of the business could be

recognized. In this report, BRITISH AMERICAN TOBACCO PLC has been taken into the

concern and various financial tools such as EVA analysis, total shareholder return, net asset

value, ratios, discounted cash flows etc have been calculated on the company to reach over a

conclusion about the overall performance of the company in the market and the investment

position of the company (Lumby and Jones, 2007).

Company overview:

BRITISH AMERICAN TOBACCO PLC is a British multinational company which

operates its activities under tobacco industry in the US market. Headquarter of the company

is in London. The company services its products and revises at worldwide. It is one of the

leading companies in around 50 countries in tobacco industry. The company has managed

better strategies and financial planning to improve the overall performance of the business in

the industry (Home, 2018).

EVA analysis:

Economic value added is a measurement tool to identify the residual value of an

organization. It valuates the financial performance of the business on the basis of the

operating profits and the cost of capita of the business. It briefs the exact economic value of

the business (Madura, 2014). The EVA analysis has been done on BRITISH AMERICAN

TOBACCO PLC to identify the economic worth of the business.

For analyzing the EVA figures of the business, the operating profit of the business has

been collected form the annual report of the company. The US corporate tax which is 20%

has been taken into the context further. The WACC of each year has been calculated through

collecting the data from various authentic websites and the US official websites. On the basis

of the overall EVA analysis, it has been found that the EVA position of the company as

enough strong in the year of 2013. But along with the time, a decrement has been seen in the

economic profit position of the company (lord, 2007).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

5

The current year performance of BRITISH AMERICAN TOBACCO PLC explains

that the economic profit level of the company is highest and thus the company is performing

better in the market. The investment level of the company has also been improved.

Figure 1: Economic Value analysis

(Morningstar, 2018)

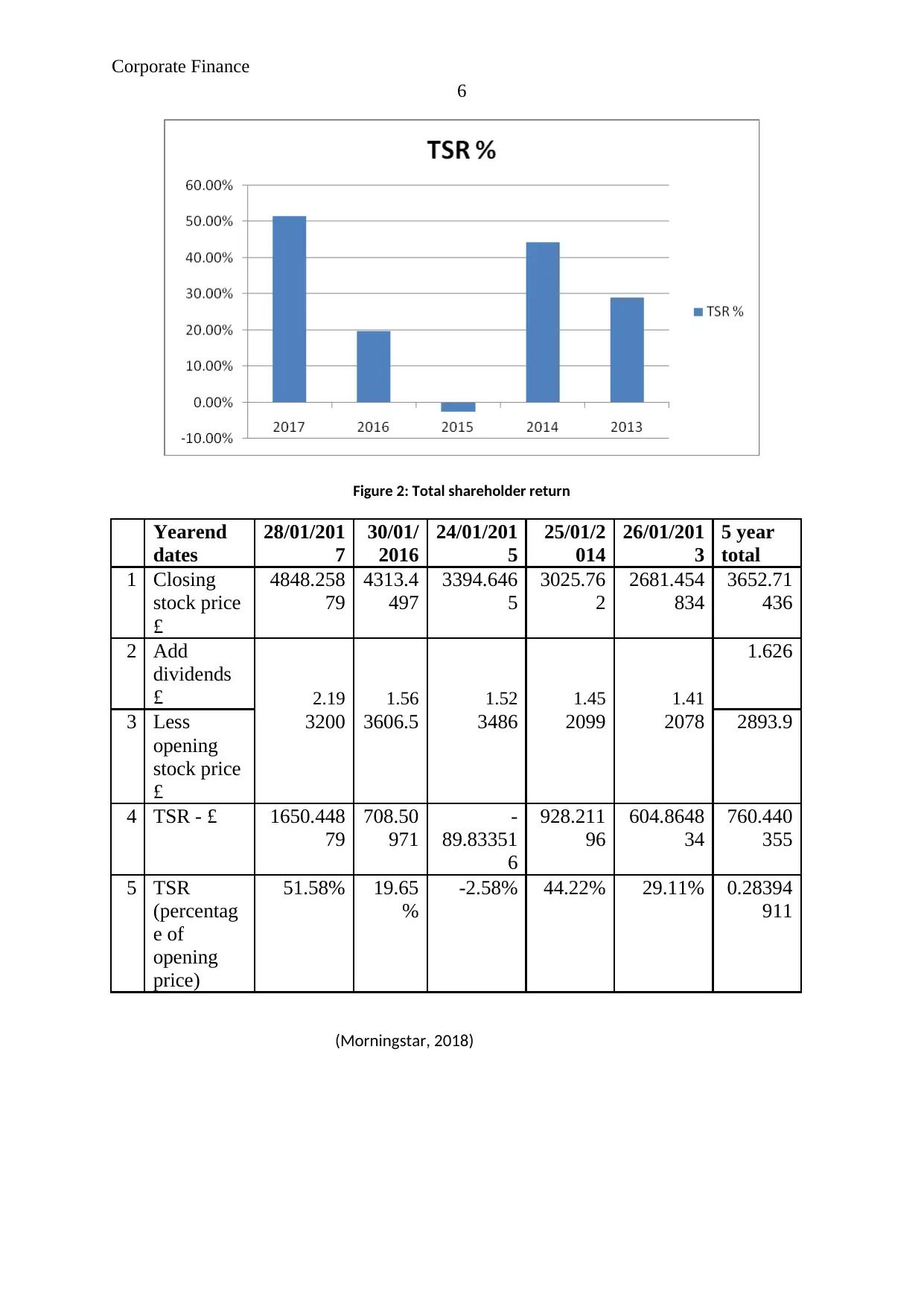

Total shareholder return:

Further, the study has been done on the total shareholder return of the company (Lord,

2007). Total shareholder return (TSR) is a measurement tool which evaluates the

performance of the stock of a business, it combines the share price, and dividend paid etc

items of the company to identify the total return to shareholder which is mainly expressed in

the percentage form (Lee and Lee, 2006).

In case of BRITISH AMERICAN TOBACCO PLC, it has been found that the total

shareholder return of the company was 51.58%, 19.65%, -2.58%, 44.22% and 29.11%

respectively in the year of 2017, 2016, 2015, 2014 and 2013. It expresses that the worth of

the shareholders in the business was highest in the year of 2017. The huge changes have

occurred due to the great increment in the stock price of the company in the year of 2017

(Morningstar, 2018). Further, it has been found that the overall position of the company is

improving constantly and because of it, the total shareholder return of the company is also

showing positive result. It briefs a better investment position in the company.

5

The current year performance of BRITISH AMERICAN TOBACCO PLC explains

that the economic profit level of the company is highest and thus the company is performing

better in the market. The investment level of the company has also been improved.

Figure 1: Economic Value analysis

(Morningstar, 2018)

Total shareholder return:

Further, the study has been done on the total shareholder return of the company (Lord,

2007). Total shareholder return (TSR) is a measurement tool which evaluates the

performance of the stock of a business, it combines the share price, and dividend paid etc

items of the company to identify the total return to shareholder which is mainly expressed in

the percentage form (Lee and Lee, 2006).

In case of BRITISH AMERICAN TOBACCO PLC, it has been found that the total

shareholder return of the company was 51.58%, 19.65%, -2.58%, 44.22% and 29.11%

respectively in the year of 2017, 2016, 2015, 2014 and 2013. It expresses that the worth of

the shareholders in the business was highest in the year of 2017. The huge changes have

occurred due to the great increment in the stock price of the company in the year of 2017

(Morningstar, 2018). Further, it has been found that the overall position of the company is

improving constantly and because of it, the total shareholder return of the company is also

showing positive result. It briefs a better investment position in the company.

Corporate Finance

6

Figure 2: Total shareholder return

Yearend

dates

28/01/201

7

30/01/

2016

24/01/201

5

25/01/2

014

26/01/201

3

5 year

total

1 Closing

stock price

£

4848.258

79

4313.4

497

3394.646

5

3025.76

2

2681.454

834

3652.71

436

2 Add

dividends

£ 2.19 1.56 1.52 1.45 1.41

1.626

3 Less

opening

stock price

£

3200 3606.5 3486 2099 2078 2893.9

4 TSR - £ 1650.448

79

708.50

971

-

89.83351

6

928.211

96

604.8648

34

760.440

355

5 TSR

(percentag

e of

opening

price)

51.58% 19.65

%

-2.58% 44.22% 29.11% 0.28394

911

(Morningstar, 2018)

6

Figure 2: Total shareholder return

Yearend

dates

28/01/201

7

30/01/

2016

24/01/201

5

25/01/2

014

26/01/201

3

5 year

total

1 Closing

stock price

£

4848.258

79

4313.4

497

3394.646

5

3025.76

2

2681.454

834

3652.71

436

2 Add

dividends

£ 2.19 1.56 1.52 1.45 1.41

1.626

3 Less

opening

stock price

£

3200 3606.5 3486 2099 2078 2893.9

4 TSR - £ 1650.448

79

708.50

971

-

89.83351

6

928.211

96

604.8648

34

760.440

355

5 TSR

(percentag

e of

opening

price)

51.58% 19.65

%

-2.58% 44.22% 29.11% 0.28394

911

(Morningstar, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Finance

7

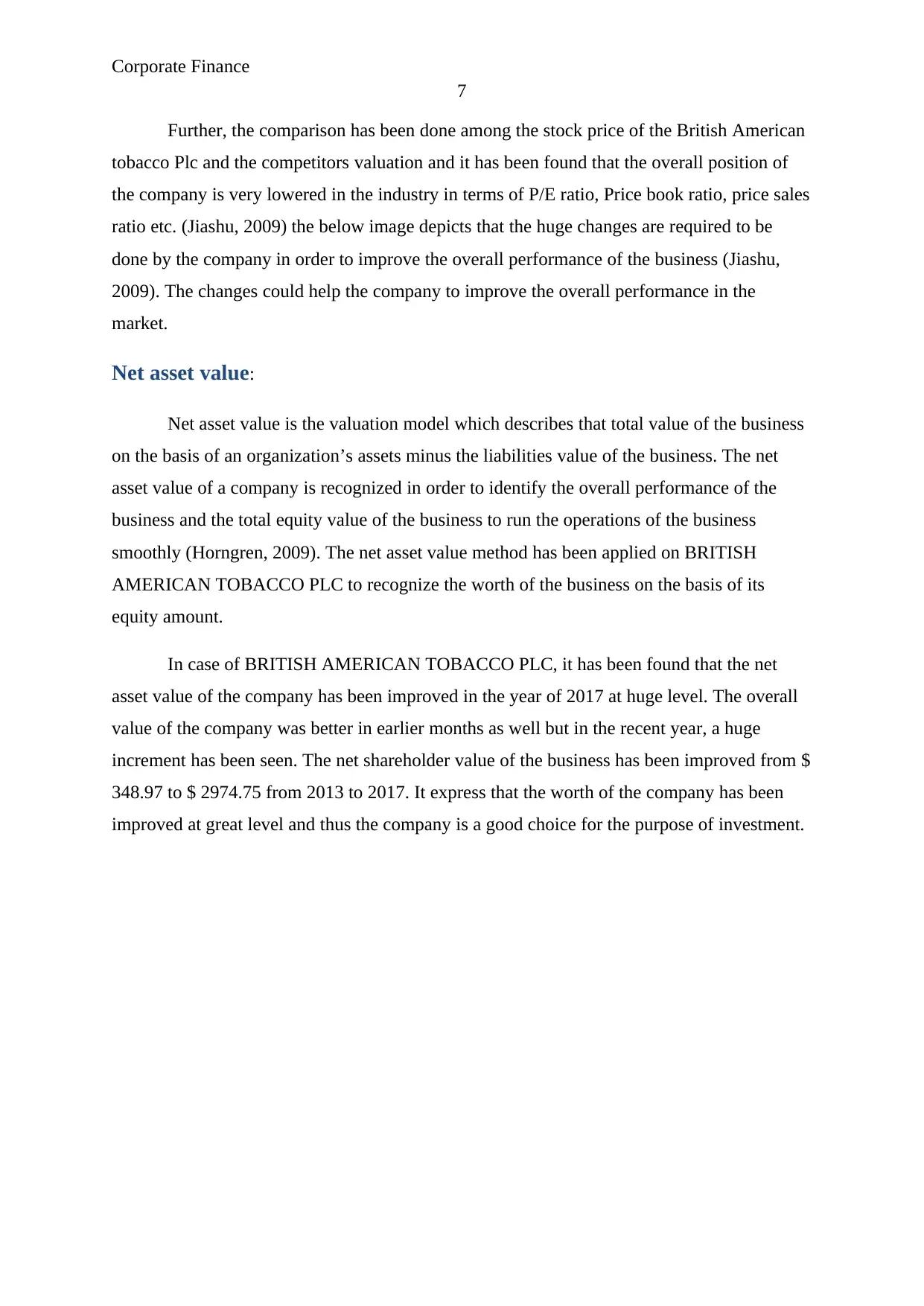

Further, the comparison has been done among the stock price of the British American

tobacco Plc and the competitors valuation and it has been found that the overall position of

the company is very lowered in the industry in terms of P/E ratio, Price book ratio, price sales

ratio etc. (Jiashu, 2009) the below image depicts that the huge changes are required to be

done by the company in order to improve the overall performance of the business (Jiashu,

2009). The changes could help the company to improve the overall performance in the

market.

Net asset value:

Net asset value is the valuation model which describes that total value of the business

on the basis of an organization’s assets minus the liabilities value of the business. The net

asset value of a company is recognized in order to identify the overall performance of the

business and the total equity value of the business to run the operations of the business

smoothly (Horngren, 2009). The net asset value method has been applied on BRITISH

AMERICAN TOBACCO PLC to recognize the worth of the business on the basis of its

equity amount.

In case of BRITISH AMERICAN TOBACCO PLC, it has been found that the net

asset value of the company has been improved in the year of 2017 at huge level. The overall

value of the company was better in earlier months as well but in the recent year, a huge

increment has been seen. The net shareholder value of the business has been improved from $

348.97 to $ 2974.75 from 2013 to 2017. It express that the worth of the company has been

improved at great level and thus the company is a good choice for the purpose of investment.

7

Further, the comparison has been done among the stock price of the British American

tobacco Plc and the competitors valuation and it has been found that the overall position of

the company is very lowered in the industry in terms of P/E ratio, Price book ratio, price sales

ratio etc. (Jiashu, 2009) the below image depicts that the huge changes are required to be

done by the company in order to improve the overall performance of the business (Jiashu,

2009). The changes could help the company to improve the overall performance in the

market.

Net asset value:

Net asset value is the valuation model which describes that total value of the business

on the basis of an organization’s assets minus the liabilities value of the business. The net

asset value of a company is recognized in order to identify the overall performance of the

business and the total equity value of the business to run the operations of the business

smoothly (Horngren, 2009). The net asset value method has been applied on BRITISH

AMERICAN TOBACCO PLC to recognize the worth of the business on the basis of its

equity amount.

In case of BRITISH AMERICAN TOBACCO PLC, it has been found that the net

asset value of the company has been improved in the year of 2017 at huge level. The overall

value of the company was better in earlier months as well but in the recent year, a huge

increment has been seen. The net shareholder value of the business has been improved from $

348.97 to $ 2974.75 from 2013 to 2017. It express that the worth of the company has been

improved at great level and thus the company is a good choice for the purpose of investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

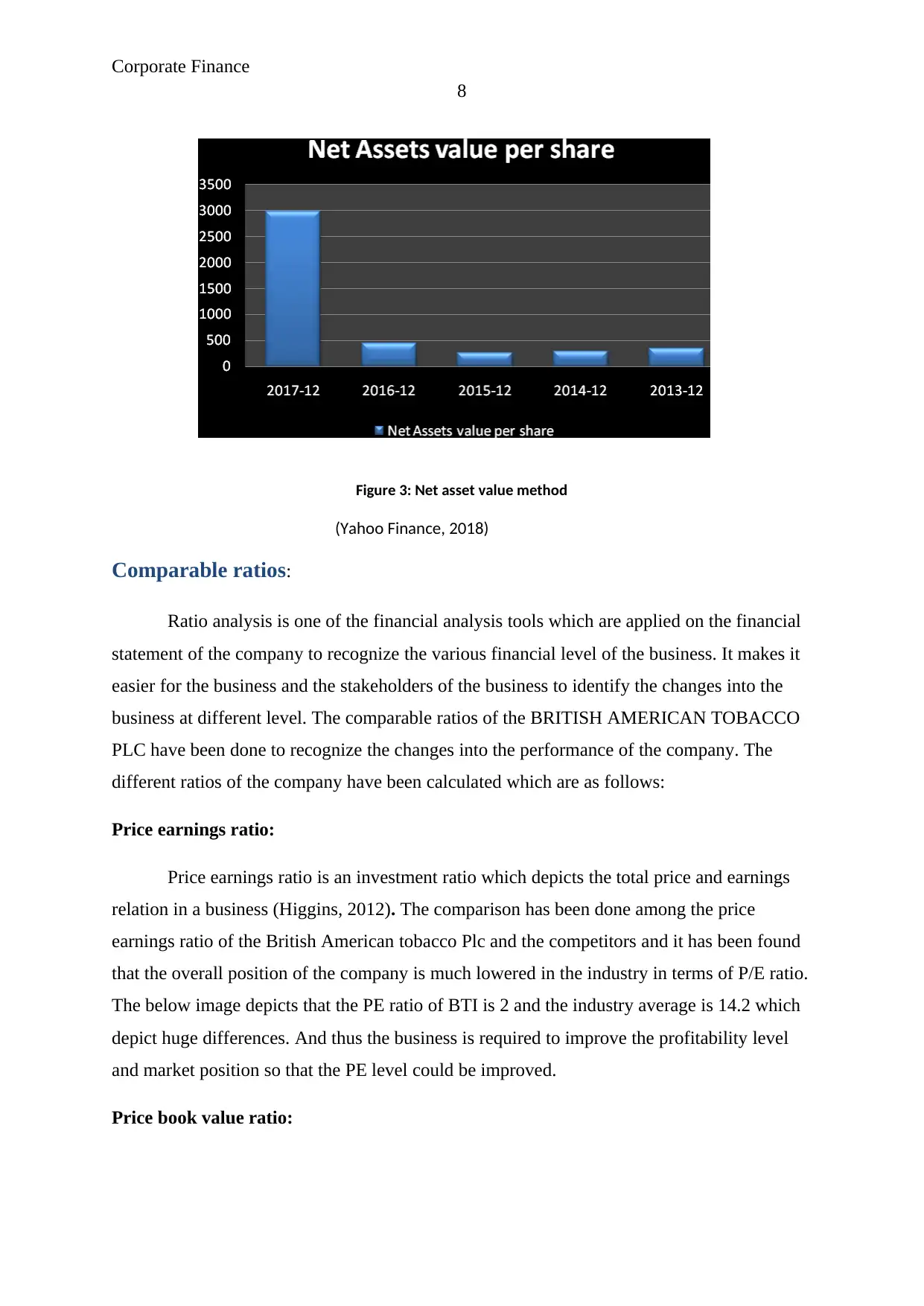

8

Figure 3: Net asset value method

(Yahoo Finance, 2018)

Comparable ratios:

Ratio analysis is one of the financial analysis tools which are applied on the financial

statement of the company to recognize the various financial level of the business. It makes it

easier for the business and the stakeholders of the business to identify the changes into the

business at different level. The comparable ratios of the BRITISH AMERICAN TOBACCO

PLC have been done to recognize the changes into the performance of the company. The

different ratios of the company have been calculated which are as follows:

Price earnings ratio:

Price earnings ratio is an investment ratio which depicts the total price and earnings

relation in a business (Higgins, 2012). The comparison has been done among the price

earnings ratio of the British American tobacco Plc and the competitors and it has been found

that the overall position of the company is much lowered in the industry in terms of P/E ratio.

The below image depicts that the PE ratio of BTI is 2 and the industry average is 14.2 which

depict huge differences. And thus the business is required to improve the profitability level

and market position so that the PE level could be improved.

Price book value ratio:

8

Figure 3: Net asset value method

(Yahoo Finance, 2018)

Comparable ratios:

Ratio analysis is one of the financial analysis tools which are applied on the financial

statement of the company to recognize the various financial level of the business. It makes it

easier for the business and the stakeholders of the business to identify the changes into the

business at different level. The comparable ratios of the BRITISH AMERICAN TOBACCO

PLC have been done to recognize the changes into the performance of the company. The

different ratios of the company have been calculated which are as follows:

Price earnings ratio:

Price earnings ratio is an investment ratio which depicts the total price and earnings

relation in a business (Higgins, 2012). The comparison has been done among the price

earnings ratio of the British American tobacco Plc and the competitors and it has been found

that the overall position of the company is much lowered in the industry in terms of P/E ratio.

The below image depicts that the PE ratio of BTI is 2 and the industry average is 14.2 which

depict huge differences. And thus the business is required to improve the profitability level

and market position so that the PE level could be improved.

Price book value ratio:

Corporate Finance

9

Further, the Price book ratio has been calculated which is also an investment ratio and

depicts the total market price of a stock against the book stock price of the company. The

comparison has been done among the price book ratio of the British American tobacco Plc

and the competitors and it has been found that the overall position of the company is very

lowered in the industry in terms of price book ratio (Horngren, 2009). The below image

depicts that the Price book ratio of BTI is 1.3 and the industry average is 7.2 which depict

huge differences. And thus the business is required to improve the market position so that the

PE level could be improved.

EV/EBITDA:

Further, the EV/EBITDA ratio has been calculated which is also an investment ratio

and depicts the total enterprise value of a business against the earnings before the interest,

taxes, dividend and the amortization of the company (Hillier, Grinblatt and Titman, 2011).

The comparison has been done among the price book ratio of the British American tobacco

Plc and the competitors and it has been found that the overall position of the company is very

lowered in the industry in terms of managing the enterprise value against the EBITDA. The

company is required to make the changes into the financial strategies and policies so that the

profitability level of the company could be improved and the company get succeed to make a

better position in the market.

Discounted cash flow:

Discounted cash flow method is one of the crucial business valuation models. It takes

the concern on the historical cash flows position of the business to estimate the future cash

flows of the business. On the basis of which an intrinsic value of the business is calculated

and it is compared to the market book price of the company to identify that how much

changes have taken place into the overall position of the company in a given period of time

(Higgins, 2012).

The discounted cash flow method has been applied on BRITISH AMERICAN

TOBACCO PLC. Firstly, the future cash flows of the business have been calculated on the

basis of the last 5 years cash flows of the business. It has been found that the FCFF of the

company is $ 34,27,444.60. the growth rate among the dividends of the company are 12.67%

which is quite higher in the industry and thus the industry data has been taken to measure the

overall growth of the business which s 3.33% (Appendix).

9

Further, the Price book ratio has been calculated which is also an investment ratio and

depicts the total market price of a stock against the book stock price of the company. The

comparison has been done among the price book ratio of the British American tobacco Plc

and the competitors and it has been found that the overall position of the company is very

lowered in the industry in terms of price book ratio (Horngren, 2009). The below image

depicts that the Price book ratio of BTI is 1.3 and the industry average is 7.2 which depict

huge differences. And thus the business is required to improve the market position so that the

PE level could be improved.

EV/EBITDA:

Further, the EV/EBITDA ratio has been calculated which is also an investment ratio

and depicts the total enterprise value of a business against the earnings before the interest,

taxes, dividend and the amortization of the company (Hillier, Grinblatt and Titman, 2011).

The comparison has been done among the price book ratio of the British American tobacco

Plc and the competitors and it has been found that the overall position of the company is very

lowered in the industry in terms of managing the enterprise value against the EBITDA. The

company is required to make the changes into the financial strategies and policies so that the

profitability level of the company could be improved and the company get succeed to make a

better position in the market.

Discounted cash flow:

Discounted cash flow method is one of the crucial business valuation models. It takes

the concern on the historical cash flows position of the business to estimate the future cash

flows of the business. On the basis of which an intrinsic value of the business is calculated

and it is compared to the market book price of the company to identify that how much

changes have taken place into the overall position of the company in a given period of time

(Higgins, 2012).

The discounted cash flow method has been applied on BRITISH AMERICAN

TOBACCO PLC. Firstly, the future cash flows of the business have been calculated on the

basis of the last 5 years cash flows of the business. It has been found that the FCFF of the

company is $ 34,27,444.60. the growth rate among the dividends of the company are 12.67%

which is quite higher in the industry and thus the industry data has been taken to measure the

overall growth of the business which s 3.33% (Appendix).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Finance

10

In addition, firstly the future cash flows of the next 10 years have been calculated and

it has been found that the terminal cash flow of the business is $ 49,14,644.57. The present

value method has been applied on the future cash flows and the terminal cash flows of the

business to identify the current worth of the business (Appendix). The WACC i.e. 1.17% rate

has been applied on the future cash flows and terminal cash flows of the business and it has

been found that the total PV of next 10 year cash outflows of the business are $

38,569,707.91 (Investing, 2018).

The present value of terminal cash flows of the business is $ 52,622,162.78 which

was earlier $ 4,914,644.57. On the basis of present value of terminal cash flows of the

business, the valuation process has been applied on the financial figures of the company.

Firstly, the total worth of the business has been calculated through adding the terminal cash

flows and the PV of future cash flows of the business (Appendix). The total value of the firm

is $ 91,191,870.68. Further, the total debt amount of the company has been deducted from the

total value of the firm to recognize the value of the equity of the business.

The total value of equity of the business has been estimated $ 26.501,870.98. The

total stock price of the company has been dividend by the outstanding shares of the company

i.e. 20,440 to identify the per share value of equity off the business which is 1296.57. It

express that the intrinsic value of the company is $ 1296.57. However, the market price of the

company is $ 4848 (Yahoo Finance, 2018). It express that the market position of the

company is overvalued.

Conclusion:

On the basis of the various valuation model of the company, it has been found that the

BRITISH AMERICAN TOBACCO PLC has made various changes into the financial

strategies and policies in last 5 years which impact could be seen in the valuation process of

the business. However, on the basis of the overall financial valuation model, it has been

found that the stock price of the company is undervalued. The market price of the company is

$ 4848 in current market. On the other hand, the intrinsic value of the company from the

entire valuation model is lower the market value and thus it is concluded that the stock price

of the company is undervalued.

10

In addition, firstly the future cash flows of the next 10 years have been calculated and

it has been found that the terminal cash flow of the business is $ 49,14,644.57. The present

value method has been applied on the future cash flows and the terminal cash flows of the

business to identify the current worth of the business (Appendix). The WACC i.e. 1.17% rate

has been applied on the future cash flows and terminal cash flows of the business and it has

been found that the total PV of next 10 year cash outflows of the business are $

38,569,707.91 (Investing, 2018).

The present value of terminal cash flows of the business is $ 52,622,162.78 which

was earlier $ 4,914,644.57. On the basis of present value of terminal cash flows of the

business, the valuation process has been applied on the financial figures of the company.

Firstly, the total worth of the business has been calculated through adding the terminal cash

flows and the PV of future cash flows of the business (Appendix). The total value of the firm

is $ 91,191,870.68. Further, the total debt amount of the company has been deducted from the

total value of the firm to recognize the value of the equity of the business.

The total value of equity of the business has been estimated $ 26.501,870.98. The

total stock price of the company has been dividend by the outstanding shares of the company

i.e. 20,440 to identify the per share value of equity off the business which is 1296.57. It

express that the intrinsic value of the company is $ 1296.57. However, the market price of the

company is $ 4848 (Yahoo Finance, 2018). It express that the market position of the

company is overvalued.

Conclusion:

On the basis of the various valuation model of the company, it has been found that the

BRITISH AMERICAN TOBACCO PLC has made various changes into the financial

strategies and policies in last 5 years which impact could be seen in the valuation process of

the business. However, on the basis of the overall financial valuation model, it has been

found that the stock price of the company is undervalued. The market price of the company is

$ 4848 in current market. On the other hand, the intrinsic value of the company from the

entire valuation model is lower the market value and thus it is concluded that the stock price

of the company is undervalued.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

11

The valuation method makes it easier for the investors and the financial analyst to

identify the economical profit and worth of the business and make better decision about the

investment level of the business.

11

The valuation method makes it easier for the investors and the financial analyst to

identify the economical profit and worth of the business and make better decision about the

investment level of the business.

Corporate Finance

12

References:

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Government publications. 2018. Rates and allowances. [online]. Available at:

https://www.gov.uk/government/publications/rates-and-allowances-corporation-tax/rates-

and-allowances-corporation-tax (accessed 17/9/18).

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Home. 2018.Britsih American tobacco plc. [online]. Available at: http://www.bat.com/

(accessed 17/9/18).

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Investing. 2018.Bond rates. [online]. Available at: https://uk.investing.com/rates-bonds/uk-5-

year-bond-yield-historical-data (accessed 17/9/18).

Jiashu, G., 2009. Study on Fair Value Accounting——on the essential characteristics of

financial accounting [J]. Accounting Research, 5, p.003.

Lee.C.F and Lee, A, C,.2006. Encyclopedia of finance, Springer science, new York

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3

(2). P. 17.

Lumby,S and Jones,C,.2007. Corporate finance theory & practice, 7th edition, Thomson,

London

Madura, J. 2014. Financial Markets and Institutions. Cengage Learning.

Morningstar. 2018.Britsih American tobacco plc. [online]. Available at:

http://investors.morningstar.com/ownership/shareholders-overview.html?

t=BTI®ion=usa&culture=en-US (accessed 17/9/18).

12

References:

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Government publications. 2018. Rates and allowances. [online]. Available at:

https://www.gov.uk/government/publications/rates-and-allowances-corporation-tax/rates-

and-allowances-corporation-tax (accessed 17/9/18).

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Home. 2018.Britsih American tobacco plc. [online]. Available at: http://www.bat.com/

(accessed 17/9/18).

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Investing. 2018.Bond rates. [online]. Available at: https://uk.investing.com/rates-bonds/uk-5-

year-bond-yield-historical-data (accessed 17/9/18).

Jiashu, G., 2009. Study on Fair Value Accounting——on the essential characteristics of

financial accounting [J]. Accounting Research, 5, p.003.

Lee.C.F and Lee, A, C,.2006. Encyclopedia of finance, Springer science, new York

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3

(2). P. 17.

Lumby,S and Jones,C,.2007. Corporate finance theory & practice, 7th edition, Thomson,

London

Madura, J. 2014. Financial Markets and Institutions. Cengage Learning.

Morningstar. 2018.Britsih American tobacco plc. [online]. Available at:

http://investors.morningstar.com/ownership/shareholders-overview.html?

t=BTI®ion=usa&culture=en-US (accessed 17/9/18).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.