BSBFIM501 Manage Budgets and Financial Plans - Assessment Task 1

VerifiedAdded on 2024/06/10

|23

|5214

|396

AI Summary

This assessment task covers the key concepts and skills required to manage budgets and financial plans effectively. It includes tasks related to developing a master budget, creating a contingency plan, understanding the role of petty cash, and analyzing financial data to identify areas for improvement. The assessment also explores the importance of accounting principles and concepts in financial management.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BSBFIM501

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Assessment Task 1.........................................................................................................................3

Task A.........................................................................................................................................3

Task B.........................................................................................................................................5

Assessment Task 2.........................................................................................................................6

Task A.........................................................................................................................................6

Task B.........................................................................................................................................7

Assessment Task 3.........................................................................................................................8

Part A..........................................................................................................................................8

Part B........................................................................................................................................11

Assessment Task 4.......................................................................................................................13

Task A.......................................................................................................................................13

Task B.......................................................................................................................................15

Task C.......................................................................................................................................17

Task D.......................................................................................................................................19

Task E.......................................................................................................................................20

References.....................................................................................................................................22

2

Assessment Task 1.........................................................................................................................3

Task A.........................................................................................................................................3

Task B.........................................................................................................................................5

Assessment Task 2.........................................................................................................................6

Task A.........................................................................................................................................6

Task B.........................................................................................................................................7

Assessment Task 3.........................................................................................................................8

Part A..........................................................................................................................................8

Part B........................................................................................................................................11

Assessment Task 4.......................................................................................................................13

Task A.......................................................................................................................................13

Task B.......................................................................................................................................15

Task C.......................................................................................................................................17

Task D.......................................................................................................................................19

Task E.......................................................................................................................................20

References.....................................................................................................................................22

2

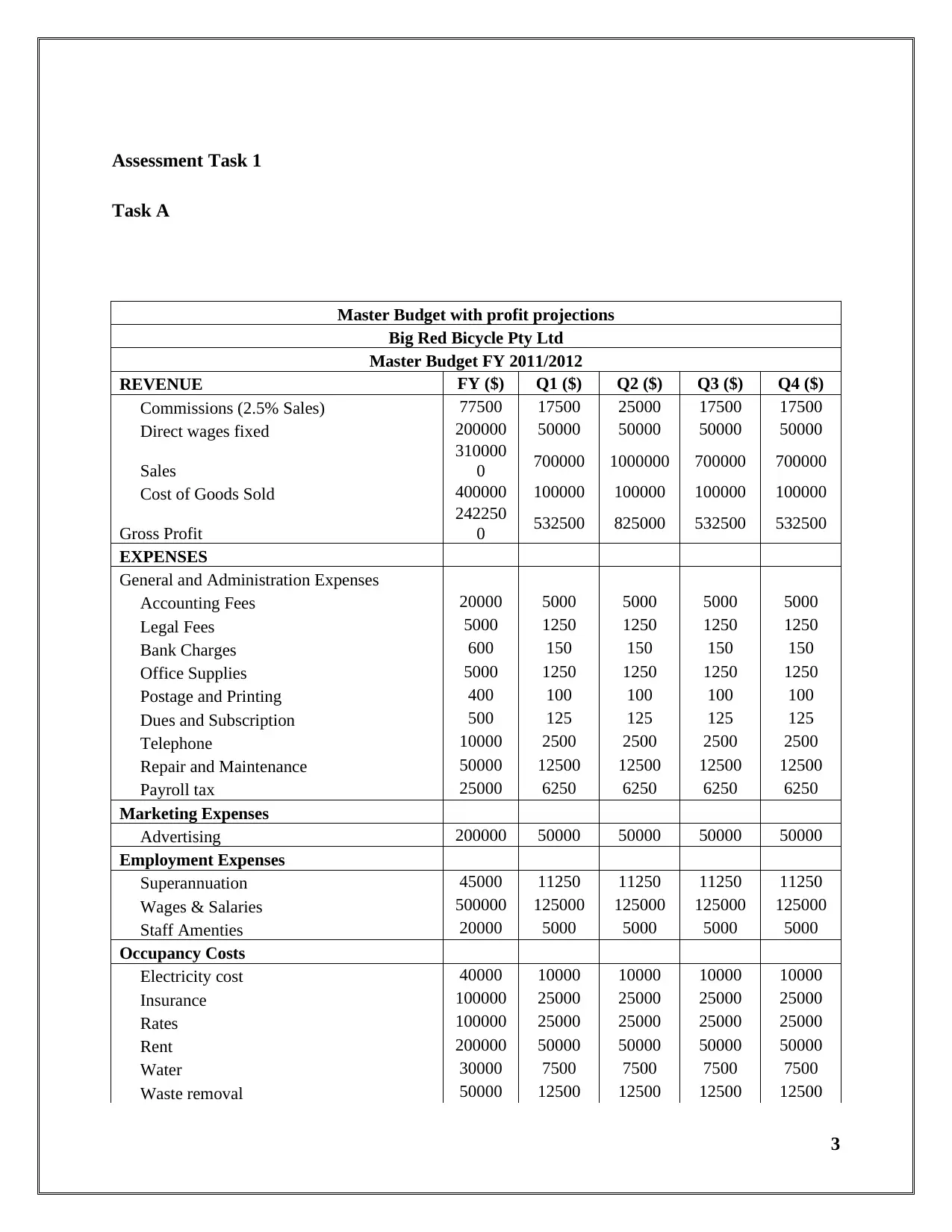

Assessment Task 1

Task A

Master Budget with profit projections

Big Red Bicycle Pty Ltd

Master Budget FY 2011/2012

REVENUE FY ($) Q1 ($) Q2 ($) Q3 ($) Q4 ($)

Commissions (2.5% Sales) 77500 17500 25000 17500 17500

Direct wages fixed 200000 50000 50000 50000 50000

Sales

310000

0 700000 1000000 700000 700000

Cost of Goods Sold 400000 100000 100000 100000 100000

Gross Profit

242250

0 532500 825000 532500 532500

EXPENSES

General and Administration Expenses

Accounting Fees 20000 5000 5000 5000 5000

Legal Fees 5000 1250 1250 1250 1250

Bank Charges 600 150 150 150 150

Office Supplies 5000 1250 1250 1250 1250

Postage and Printing 400 100 100 100 100

Dues and Subscription 500 125 125 125 125

Telephone 10000 2500 2500 2500 2500

Repair and Maintenance 50000 12500 12500 12500 12500

Payroll tax 25000 6250 6250 6250 6250

Marketing Expenses

Advertising 200000 50000 50000 50000 50000

Employment Expenses

Superannuation 45000 11250 11250 11250 11250

Wages & Salaries 500000 125000 125000 125000 125000

Staff Amenties 20000 5000 5000 5000 5000

Occupancy Costs

Electricity cost 40000 10000 10000 10000 10000

Insurance 100000 25000 25000 25000 25000

Rates 100000 25000 25000 25000 25000

Rent 200000 50000 50000 50000 50000

Water 30000 7500 7500 7500 7500

Waste removal 50000 12500 12500 12500 12500

3

Task A

Master Budget with profit projections

Big Red Bicycle Pty Ltd

Master Budget FY 2011/2012

REVENUE FY ($) Q1 ($) Q2 ($) Q3 ($) Q4 ($)

Commissions (2.5% Sales) 77500 17500 25000 17500 17500

Direct wages fixed 200000 50000 50000 50000 50000

Sales

310000

0 700000 1000000 700000 700000

Cost of Goods Sold 400000 100000 100000 100000 100000

Gross Profit

242250

0 532500 825000 532500 532500

EXPENSES

General and Administration Expenses

Accounting Fees 20000 5000 5000 5000 5000

Legal Fees 5000 1250 1250 1250 1250

Bank Charges 600 150 150 150 150

Office Supplies 5000 1250 1250 1250 1250

Postage and Printing 400 100 100 100 100

Dues and Subscription 500 125 125 125 125

Telephone 10000 2500 2500 2500 2500

Repair and Maintenance 50000 12500 12500 12500 12500

Payroll tax 25000 6250 6250 6250 6250

Marketing Expenses

Advertising 200000 50000 50000 50000 50000

Employment Expenses

Superannuation 45000 11250 11250 11250 11250

Wages & Salaries 500000 125000 125000 125000 125000

Staff Amenties 20000 5000 5000 5000 5000

Occupancy Costs

Electricity cost 40000 10000 10000 10000 10000

Insurance 100000 25000 25000 25000 25000

Rates 100000 25000 25000 25000 25000

Rent 200000 50000 50000 50000 50000

Water 30000 7500 7500 7500 7500

Waste removal 50000 12500 12500 12500 12500

3

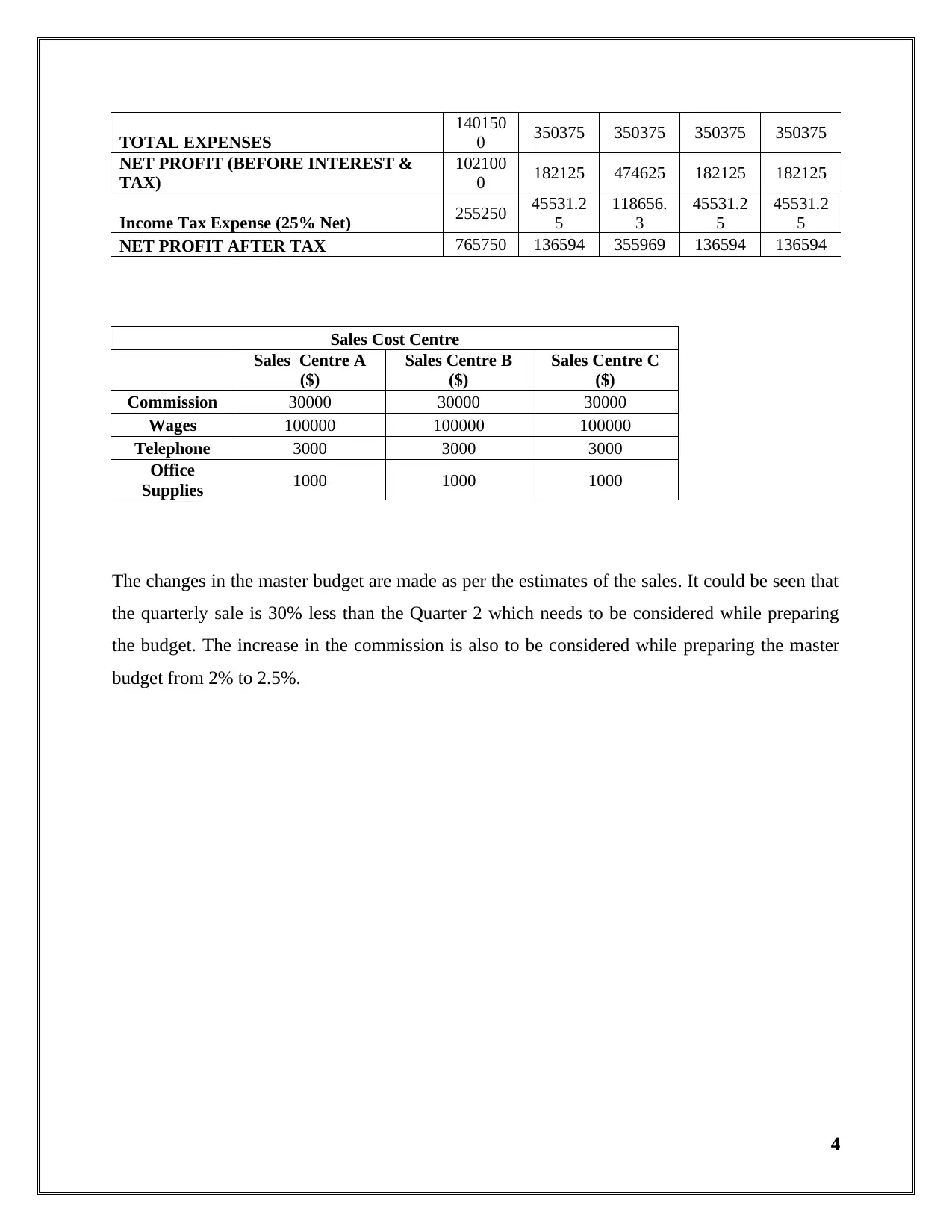

TOTAL EXPENSES

140150

0 350375 350375 350375 350375

NET PROFIT (BEFORE INTEREST &

TAX)

102100

0 182125 474625 182125 182125

Income Tax Expense (25% Net) 255250 45531.2

5

118656.

3

45531.2

5

45531.2

5

NET PROFIT AFTER TAX 765750 136594 355969 136594 136594

Sales Cost Centre

Sales Centre A

($)

Sales Centre B

($)

Sales Centre C

($)

Commission 30000 30000 30000

Wages 100000 100000 100000

Telephone 3000 3000 3000

Office

Supplies 1000 1000 1000

The changes in the master budget are made as per the estimates of the sales. It could be seen that

the quarterly sale is 30% less than the Quarter 2 which needs to be considered while preparing

the budget. The increase in the commission is also to be considered while preparing the master

budget from 2% to 2.5%.

4

140150

0 350375 350375 350375 350375

NET PROFIT (BEFORE INTEREST &

TAX)

102100

0 182125 474625 182125 182125

Income Tax Expense (25% Net) 255250 45531.2

5

118656.

3

45531.2

5

45531.2

5

NET PROFIT AFTER TAX 765750 136594 355969 136594 136594

Sales Cost Centre

Sales Centre A

($)

Sales Centre B

($)

Sales Centre C

($)

Commission 30000 30000 30000

Wages 100000 100000 100000

Telephone 3000 3000 3000

Office

Supplies 1000 1000 1000

The changes in the master budget are made as per the estimates of the sales. It could be seen that

the quarterly sale is 30% less than the Quarter 2 which needs to be considered while preparing

the budget. The increase in the commission is also to be considered while preparing the master

budget from 2% to 2.5%.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

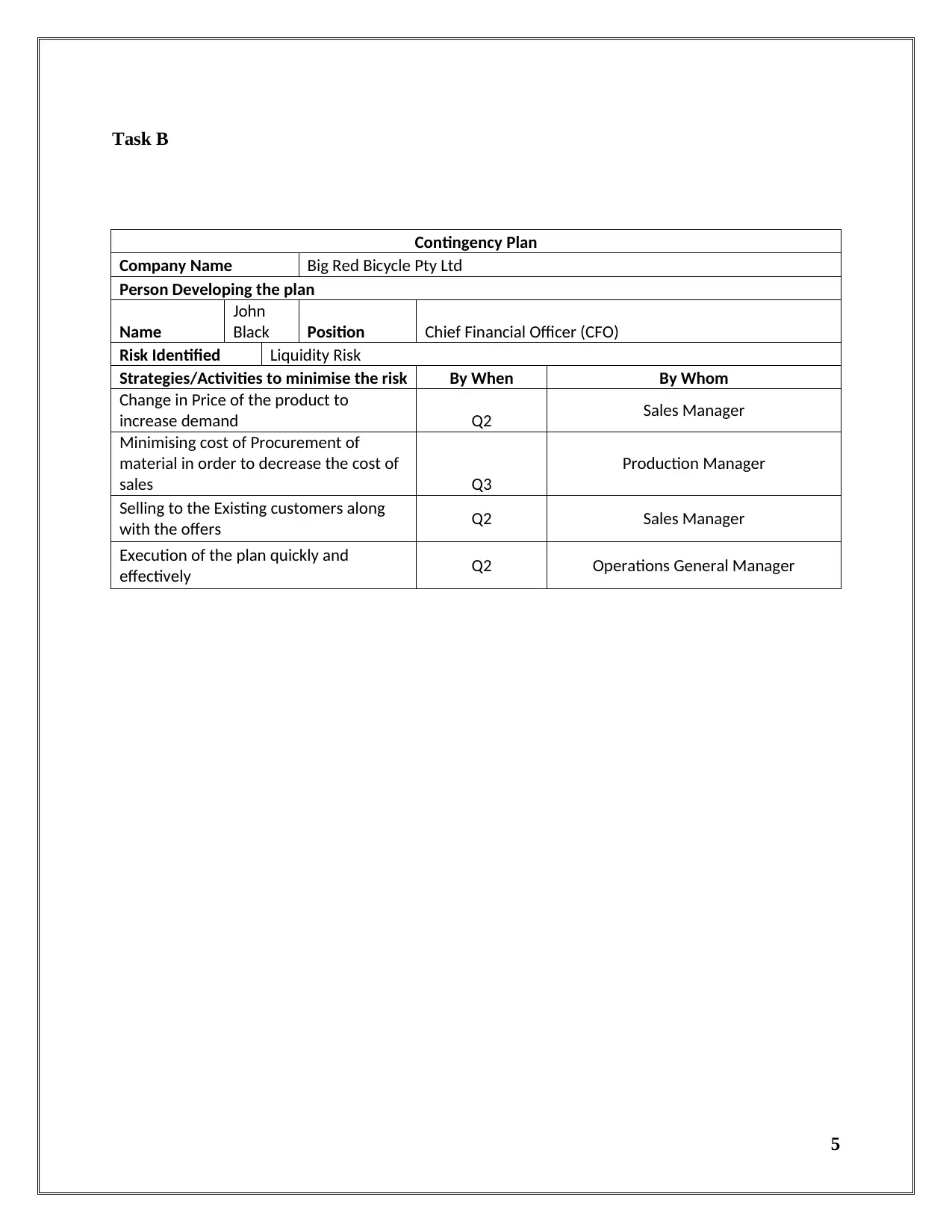

Task B

Contingency Plan

Company Name Big Red Bicycle Pty Ltd

Person Developing the plan

Name

John

Black Position Chief Financial Officer (CFO)

Risk Identified Liquidity Risk

Strategies/Activities to minimise the risk By When By Whom

Change in Price of the product to

increase demand Q2 Sales Manager

Minimising cost of Procurement of

material in order to decrease the cost of

sales Q3

Production Manager

Selling to the Existing customers along

with the offers Q2 Sales Manager

Execution of the plan quickly and

effectively Q2 Operations General Manager

5

Contingency Plan

Company Name Big Red Bicycle Pty Ltd

Person Developing the plan

Name

John

Black Position Chief Financial Officer (CFO)

Risk Identified Liquidity Risk

Strategies/Activities to minimise the risk By When By Whom

Change in Price of the product to

increase demand Q2 Sales Manager

Minimising cost of Procurement of

material in order to decrease the cost of

sales Q3

Production Manager

Selling to the Existing customers along

with the offers Q2 Sales Manager

Execution of the plan quickly and

effectively Q2 Operations General Manager

5

Assessment Task 2

Task A

The overall objective of the company is to diversify the product line in order to minimize the risk

involved with the decrease in sales of one product. The company is also looking forward to

expanding their business and get the advantage of the reduced cost. The reduced cost will result

in increasing profit making the financial position and liquidity strong.

The budget can be defined as the estimate of various components such as sales, direct cost etc.

depending upon various factors surrounding the organisation and can affect them. The budget

can be divided into 4 Phases that are Preparing of the budget, Approving the budget, executing

the budget, evaluating the budget (Lander, 2018). The preparing of the budget is based on the

various estimates and thought at the basic level with the objective and the way to complete them.

There are various things which need to be considered while preparation of the budget being

expected revenues, expenses such as direct material, wages and salaries etc. It is important to

have proper approval for the budget that is being prepared so that acceptance of the same can be

at each and every level. The executing and evaluation of the budget is then important so that

there can be the effective achievement of the goals and objectives (Lander, 2018). There can be

an allocation of the resources available on the basis of the budget that is being prepared. The

tactics and strategy can be implemented as per the formation of the budget.

There are different types of the budget that can be prepared as per the requirement of the

organisation such as master budget, operational budget, cash flow budget, financial budget and

static budget. The master budget consists of all the aspect of the business being base to set the

objectives and goals of the organisation (Shpak, 2018). The master budget is also useful to

evaluate the overall performance of the business. Operational budgets are concerned with the day

to day activities consisting of revenues and expenses. The financial budget is more of concerned

with the expenditure and revenue that the company may earn or incur as well as the capital

expenditure. In case of the static budget, there are no changes as per the deviations in the sales

figure.

6

Task A

The overall objective of the company is to diversify the product line in order to minimize the risk

involved with the decrease in sales of one product. The company is also looking forward to

expanding their business and get the advantage of the reduced cost. The reduced cost will result

in increasing profit making the financial position and liquidity strong.

The budget can be defined as the estimate of various components such as sales, direct cost etc.

depending upon various factors surrounding the organisation and can affect them. The budget

can be divided into 4 Phases that are Preparing of the budget, Approving the budget, executing

the budget, evaluating the budget (Lander, 2018). The preparing of the budget is based on the

various estimates and thought at the basic level with the objective and the way to complete them.

There are various things which need to be considered while preparation of the budget being

expected revenues, expenses such as direct material, wages and salaries etc. It is important to

have proper approval for the budget that is being prepared so that acceptance of the same can be

at each and every level. The executing and evaluation of the budget is then important so that

there can be the effective achievement of the goals and objectives (Lander, 2018). There can be

an allocation of the resources available on the basis of the budget that is being prepared. The

tactics and strategy can be implemented as per the formation of the budget.

There are different types of the budget that can be prepared as per the requirement of the

organisation such as master budget, operational budget, cash flow budget, financial budget and

static budget. The master budget consists of all the aspect of the business being base to set the

objectives and goals of the organisation (Shpak, 2018). The master budget is also useful to

evaluate the overall performance of the business. Operational budgets are concerned with the day

to day activities consisting of revenues and expenses. The financial budget is more of concerned

with the expenditure and revenue that the company may earn or incur as well as the capital

expenditure. In case of the static budget, there are no changes as per the deviations in the sales

figure.

6

Task B

The petty cash consists of postage, small items of stationary, casual labour, window cleaning,

travel expenses, donations. The expenses which are made for private are not being considered in

the petty cash. It is important to have a record of the petty cash book in which there is a

recording of each and every transaction which can be considered at the time of Auditing. There

must be the proper preparation of the vouchers for each claim that has been made during the

period (Peavler, 2018). These petty expenses can be defined as the small expenses that are being

incurred during the year. The petty cash is listed in the current assets in the balance sheet. These

are also recorded under the head cash and cash equivalent in the larger companies. The petty

cash book is debited whereas the cash account is credited. The variance in the fund provided for

the petty cash book can be audited and any fraud or misstatement can be identified (Accounting

Tools, 2017). The reconciliation of each and every transaction can be done with the cash book so

that there can be no chances of theft or misconduct.

7

The petty cash consists of postage, small items of stationary, casual labour, window cleaning,

travel expenses, donations. The expenses which are made for private are not being considered in

the petty cash. It is important to have a record of the petty cash book in which there is a

recording of each and every transaction which can be considered at the time of Auditing. There

must be the proper preparation of the vouchers for each claim that has been made during the

period (Peavler, 2018). These petty expenses can be defined as the small expenses that are being

incurred during the year. The petty cash is listed in the current assets in the balance sheet. These

are also recorded under the head cash and cash equivalent in the larger companies. The petty

cash book is debited whereas the cash account is credited. The variance in the fund provided for

the petty cash book can be audited and any fraud or misstatement can be identified (Accounting

Tools, 2017). The reconciliation of each and every transaction can be done with the cash book so

that there can be no chances of theft or misconduct.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

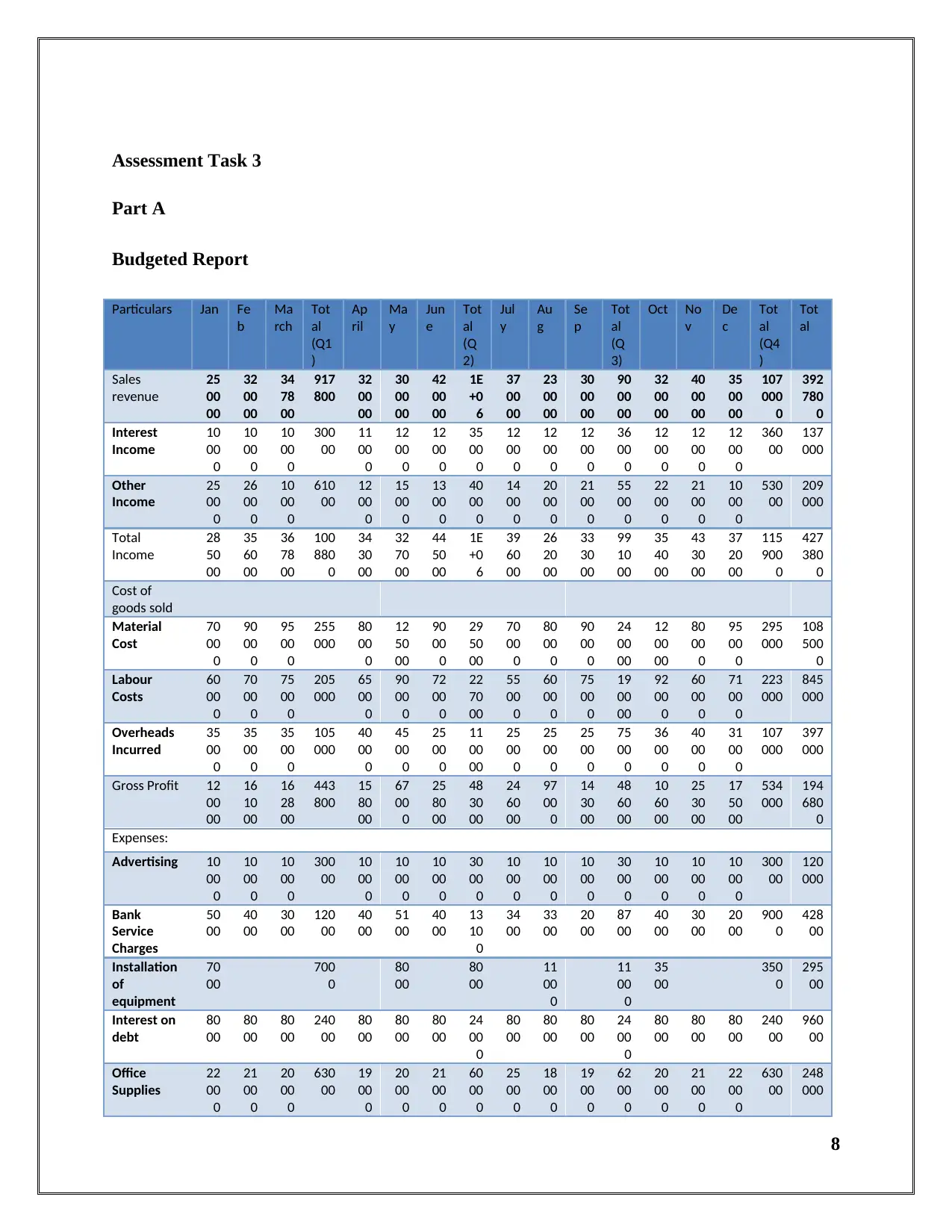

Assessment Task 3

Part A

Budgeted Report

Particulars Jan Fe

b

Ma

rch

Tot

al

(Q1

)

Ap

ril

Ma

y

Jun

e

Tot

al

(Q

2)

Jul

y

Au

g

Se

p

Tot

al

(Q

3)

Oct No

v

De

c

Tot

al

(Q4

)

Tot

al

Sales

revenue

25

00

00

32

00

00

34

78

00

917

800

32

00

00

30

00

00

42

00

00

1E

+0

6

37

00

00

23

00

00

30

00

00

90

00

00

32

00

00

40

00

00

35

00

00

107

000

0

392

780

0

Interest

Income

10

00

0

10

00

0

10

00

0

300

00

11

00

0

12

00

0

12

00

0

35

00

0

12

00

0

12

00

0

12

00

0

36

00

0

12

00

0

12

00

0

12

00

0

360

00

137

000

Other

Income

25

00

0

26

00

0

10

00

0

610

00

12

00

0

15

00

0

13

00

0

40

00

0

14

00

0

20

00

0

21

00

0

55

00

0

22

00

0

21

00

0

10

00

0

530

00

209

000

Total

Income

28

50

00

35

60

00

36

78

00

100

880

0

34

30

00

32

70

00

44

50

00

1E

+0

6

39

60

00

26

20

00

33

30

00

99

10

00

35

40

00

43

30

00

37

20

00

115

900

0

427

380

0

Cost of

goods sold

Material

Cost

70

00

0

90

00

0

95

00

0

255

000

80

00

0

12

50

00

90

00

0

29

50

00

70

00

0

80

00

0

90

00

0

24

00

00

12

00

00

80

00

0

95

00

0

295

000

108

500

0

Labour

Costs

60

00

0

70

00

0

75

00

0

205

000

65

00

0

90

00

0

72

00

0

22

70

00

55

00

0

60

00

0

75

00

0

19

00

00

92

00

0

60

00

0

71

00

0

223

000

845

000

Overheads

Incurred

35

00

0

35

00

0

35

00

0

105

000

40

00

0

45

00

0

25

00

0

11

00

00

25

00

0

25

00

0

25

00

0

75

00

0

36

00

0

40

00

0

31

00

0

107

000

397

000

Gross Profit 12

00

00

16

10

00

16

28

00

443

800

15

80

00

67

00

0

25

80

00

48

30

00

24

60

00

97

00

0

14

30

00

48

60

00

10

60

00

25

30

00

17

50

00

534

000

194

680

0

Expenses:

Advertising 10

00

0

10

00

0

10

00

0

300

00

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

300

00

120

000

Bank

Service

Charges

50

00

40

00

30

00

120

00

40

00

51

00

40

00

13

10

0

34

00

33

00

20

00

87

00

40

00

30

00

20

00

900

0

428

00

Installation

of

equipment

70

00

700

0

80

00

80

00

11

00

0

11

00

0

35

00

350

0

295

00

Interest on

debt

80

00

80

00

80

00

240

00

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

240

00

960

00

Office

Supplies

22

00

0

21

00

0

20

00

0

630

00

19

00

0

20

00

0

21

00

0

60

00

0

25

00

0

18

00

0

19

00

0

62

00

0

20

00

0

21

00

0

22

00

0

630

00

248

000

8

Part A

Budgeted Report

Particulars Jan Fe

b

Ma

rch

Tot

al

(Q1

)

Ap

ril

Ma

y

Jun

e

Tot

al

(Q

2)

Jul

y

Au

g

Se

p

Tot

al

(Q

3)

Oct No

v

De

c

Tot

al

(Q4

)

Tot

al

Sales

revenue

25

00

00

32

00

00

34

78

00

917

800

32

00

00

30

00

00

42

00

00

1E

+0

6

37

00

00

23

00

00

30

00

00

90

00

00

32

00

00

40

00

00

35

00

00

107

000

0

392

780

0

Interest

Income

10

00

0

10

00

0

10

00

0

300

00

11

00

0

12

00

0

12

00

0

35

00

0

12

00

0

12

00

0

12

00

0

36

00

0

12

00

0

12

00

0

12

00

0

360

00

137

000

Other

Income

25

00

0

26

00

0

10

00

0

610

00

12

00

0

15

00

0

13

00

0

40

00

0

14

00

0

20

00

0

21

00

0

55

00

0

22

00

0

21

00

0

10

00

0

530

00

209

000

Total

Income

28

50

00

35

60

00

36

78

00

100

880

0

34

30

00

32

70

00

44

50

00

1E

+0

6

39

60

00

26

20

00

33

30

00

99

10

00

35

40

00

43

30

00

37

20

00

115

900

0

427

380

0

Cost of

goods sold

Material

Cost

70

00

0

90

00

0

95

00

0

255

000

80

00

0

12

50

00

90

00

0

29

50

00

70

00

0

80

00

0

90

00

0

24

00

00

12

00

00

80

00

0

95

00

0

295

000

108

500

0

Labour

Costs

60

00

0

70

00

0

75

00

0

205

000

65

00

0

90

00

0

72

00

0

22

70

00

55

00

0

60

00

0

75

00

0

19

00

00

92

00

0

60

00

0

71

00

0

223

000

845

000

Overheads

Incurred

35

00

0

35

00

0

35

00

0

105

000

40

00

0

45

00

0

25

00

0

11

00

00

25

00

0

25

00

0

25

00

0

75

00

0

36

00

0

40

00

0

31

00

0

107

000

397

000

Gross Profit 12

00

00

16

10

00

16

28

00

443

800

15

80

00

67

00

0

25

80

00

48

30

00

24

60

00

97

00

0

14

30

00

48

60

00

10

60

00

25

30

00

17

50

00

534

000

194

680

0

Expenses:

Advertising 10

00

0

10

00

0

10

00

0

300

00

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

300

00

120

000

Bank

Service

Charges

50

00

40

00

30

00

120

00

40

00

51

00

40

00

13

10

0

34

00

33

00

20

00

87

00

40

00

30

00

20

00

900

0

428

00

Installation

of

equipment

70

00

700

0

80

00

80

00

11

00

0

11

00

0

35

00

350

0

295

00

Interest on

debt

80

00

80

00

80

00

240

00

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

240

00

960

00

Office

Supplies

22

00

0

21

00

0

20

00

0

630

00

19

00

0

20

00

0

21

00

0

60

00

0

25

00

0

18

00

0

19

00

0

62

00

0

20

00

0

21

00

0

22

00

0

630

00

248

000

8

Payroll

Taxes

20

00

20

00

20

00

600

0

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

20

00

20

00

20

00

600

0

240

00

Printing 50

00

50

00

50

00

150

00

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

150

00

600

00

Professiona

l Fees

15

00

0

14

00

0

10

00

0

390

00

11

00

0

12

00

0

13

00

0

36

00

0

10

00

0

12

00

0

13

00

0

35

00

0

15

00

0

14

00

0

13

50

0

425

00

152

500

Telephone

expenses

35

00

35

00

35

00

105

00

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

105

00

420

00

Vehicle

expense

12

00

0

10

00

0

11

00

0

330

00

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

330

00

132

000

Total

expenses

89

50

0

77

50

0

72

50

0

239

500

74

50

0

83

60

0

77

50

0

23

56

00

78

90

0

82

80

0

73

50

0

23

52

00

83

00

0

76

50

0

77

00

0

236

500

946

800

Net Profit

before taxes

30

50

0

83

50

0

90

30

0

204

300

83

50

0

-

16

60

0

18

05

00

24

74

00

16

71

00

14

20

0

69

50

0

25

08

00

23

00

0

17

65

00

98

00

0

297

500

100

000

0

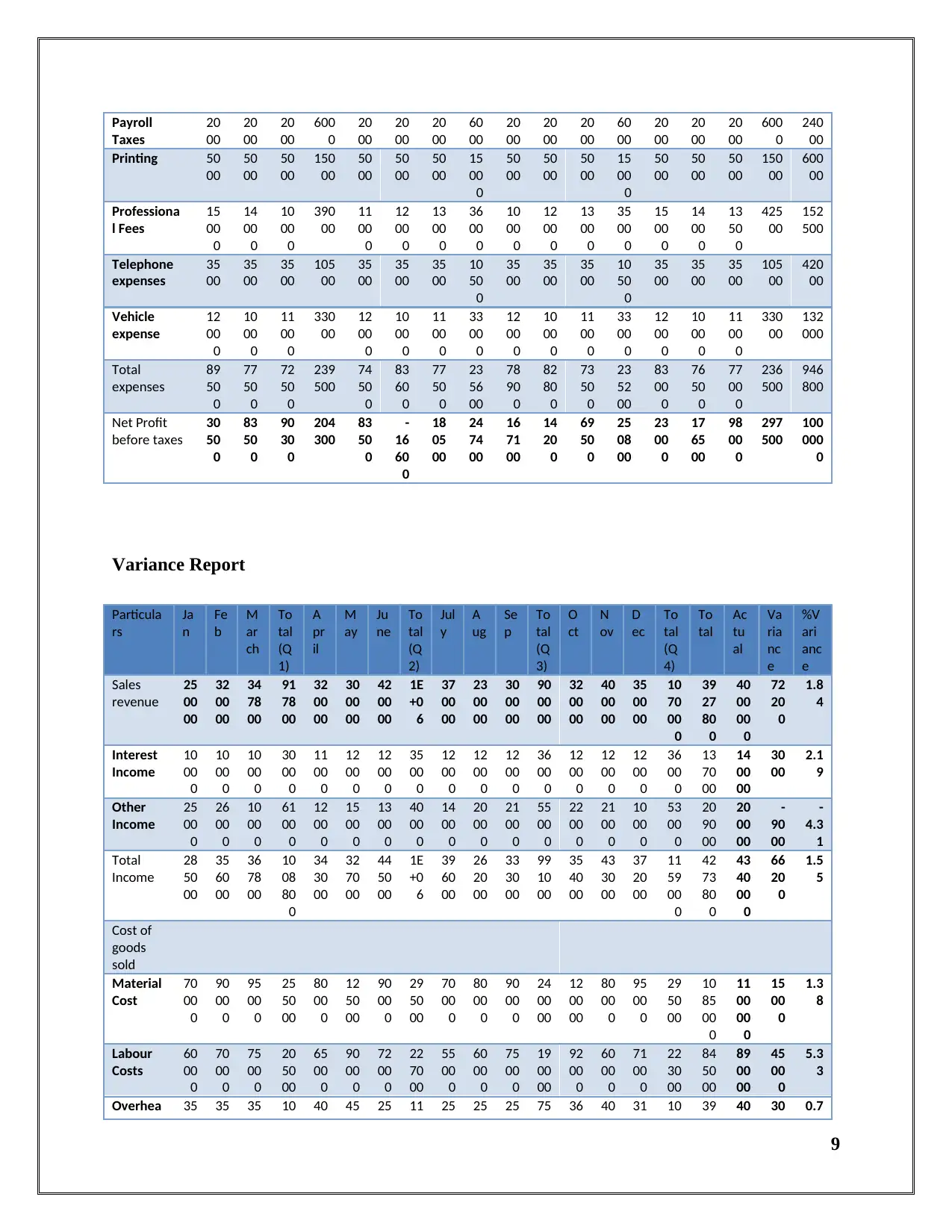

Variance Report

Particula

rs

Ja

n

Fe

b

M

ar

ch

To

tal

(Q

1)

A

pr

il

M

ay

Ju

ne

To

tal

(Q

2)

Jul

y

A

ug

Se

p

To

tal

(Q

3)

O

ct

N

ov

D

ec

To

tal

(Q

4)

To

tal

Ac

tu

al

Va

ria

nc

e

%V

ari

anc

e

Sales

revenue

25

00

00

32

00

00

34

78

00

91

78

00

32

00

00

30

00

00

42

00

00

1E

+0

6

37

00

00

23

00

00

30

00

00

90

00

00

32

00

00

40

00

00

35

00

00

10

70

00

0

39

27

80

0

40

00

00

0

72

20

0

1.8

4

Interest

Income

10

00

0

10

00

0

10

00

0

30

00

0

11

00

0

12

00

0

12

00

0

35

00

0

12

00

0

12

00

0

12

00

0

36

00

0

12

00

0

12

00

0

12

00

0

36

00

0

13

70

00

14

00

00

30

00

2.1

9

Other

Income

25

00

0

26

00

0

10

00

0

61

00

0

12

00

0

15

00

0

13

00

0

40

00

0

14

00

0

20

00

0

21

00

0

55

00

0

22

00

0

21

00

0

10

00

0

53

00

0

20

90

00

20

00

00

-

90

00

-

4.3

1

Total

Income

28

50

00

35

60

00

36

78

00

10

08

80

0

34

30

00

32

70

00

44

50

00

1E

+0

6

39

60

00

26

20

00

33

30

00

99

10

00

35

40

00

43

30

00

37

20

00

11

59

00

0

42

73

80

0

43

40

00

0

66

20

0

1.5

5

Cost of

goods

sold

Material

Cost

70

00

0

90

00

0

95

00

0

25

50

00

80

00

0

12

50

00

90

00

0

29

50

00

70

00

0

80

00

0

90

00

0

24

00

00

12

00

00

80

00

0

95

00

0

29

50

00

10

85

00

0

11

00

00

0

15

00

0

1.3

8

Labour

Costs

60

00

0

70

00

0

75

00

0

20

50

00

65

00

0

90

00

0

72

00

0

22

70

00

55

00

0

60

00

0

75

00

0

19

00

00

92

00

0

60

00

0

71

00

0

22

30

00

84

50

00

89

00

00

45

00

0

5.3

3

Overhea 35 35 35 10 40 45 25 11 25 25 25 75 36 40 31 10 39 40 30 0.7

9

Taxes

20

00

20

00

20

00

600

0

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

20

00

20

00

20

00

600

0

240

00

Printing 50

00

50

00

50

00

150

00

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

150

00

600

00

Professiona

l Fees

15

00

0

14

00

0

10

00

0

390

00

11

00

0

12

00

0

13

00

0

36

00

0

10

00

0

12

00

0

13

00

0

35

00

0

15

00

0

14

00

0

13

50

0

425

00

152

500

Telephone

expenses

35

00

35

00

35

00

105

00

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

105

00

420

00

Vehicle

expense

12

00

0

10

00

0

11

00

0

330

00

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

330

00

132

000

Total

expenses

89

50

0

77

50

0

72

50

0

239

500

74

50

0

83

60

0

77

50

0

23

56

00

78

90

0

82

80

0

73

50

0

23

52

00

83

00

0

76

50

0

77

00

0

236

500

946

800

Net Profit

before taxes

30

50

0

83

50

0

90

30

0

204

300

83

50

0

-

16

60

0

18

05

00

24

74

00

16

71

00

14

20

0

69

50

0

25

08

00

23

00

0

17

65

00

98

00

0

297

500

100

000

0

Variance Report

Particula

rs

Ja

n

Fe

b

M

ar

ch

To

tal

(Q

1)

A

pr

il

M

ay

Ju

ne

To

tal

(Q

2)

Jul

y

A

ug

Se

p

To

tal

(Q

3)

O

ct

N

ov

D

ec

To

tal

(Q

4)

To

tal

Ac

tu

al

Va

ria

nc

e

%V

ari

anc

e

Sales

revenue

25

00

00

32

00

00

34

78

00

91

78

00

32

00

00

30

00

00

42

00

00

1E

+0

6

37

00

00

23

00

00

30

00

00

90

00

00

32

00

00

40

00

00

35

00

00

10

70

00

0

39

27

80

0

40

00

00

0

72

20

0

1.8

4

Interest

Income

10

00

0

10

00

0

10

00

0

30

00

0

11

00

0

12

00

0

12

00

0

35

00

0

12

00

0

12

00

0

12

00

0

36

00

0

12

00

0

12

00

0

12

00

0

36

00

0

13

70

00

14

00

00

30

00

2.1

9

Other

Income

25

00

0

26

00

0

10

00

0

61

00

0

12

00

0

15

00

0

13

00

0

40

00

0

14

00

0

20

00

0

21

00

0

55

00

0

22

00

0

21

00

0

10

00

0

53

00

0

20

90

00

20

00

00

-

90

00

-

4.3

1

Total

Income

28

50

00

35

60

00

36

78

00

10

08

80

0

34

30

00

32

70

00

44

50

00

1E

+0

6

39

60

00

26

20

00

33

30

00

99

10

00

35

40

00

43

30

00

37

20

00

11

59

00

0

42

73

80

0

43

40

00

0

66

20

0

1.5

5

Cost of

goods

sold

Material

Cost

70

00

0

90

00

0

95

00

0

25

50

00

80

00

0

12

50

00

90

00

0

29

50

00

70

00

0

80

00

0

90

00

0

24

00

00

12

00

00

80

00

0

95

00

0

29

50

00

10

85

00

0

11

00

00

0

15

00

0

1.3

8

Labour

Costs

60

00

0

70

00

0

75

00

0

20

50

00

65

00

0

90

00

0

72

00

0

22

70

00

55

00

0

60

00

0

75

00

0

19

00

00

92

00

0

60

00

0

71

00

0

22

30

00

84

50

00

89

00

00

45

00

0

5.3

3

Overhea 35 35 35 10 40 45 25 11 25 25 25 75 36 40 31 10 39 40 30 0.7

9

ds

Incurred

00

0

00

0

00

0

50

00

00

0

00

0

00

0

00

00

00

0

00

0

00

0

00

0

00

0

00

0

00

0

70

00

70

00

00

00

00 6

Gross

Profit

12

00

00

16

10

00

16

28

00

44

38

00

15

80

00

67

00

0

25

80

00

48

30

00

24

60

00

97

00

0

14

30

00

48

60

00

10

60

00

25

30

00

17

50

00

53

40

00

19

46

80

0

19

50

00

0

32

00

0.1

6

Expenses

:

Advertisi

ng

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

12

00

00

13

00

00

10

00

0

8.3

3

Bank

Service

Charges

50

00

40

00

30

00

12

00

0

40

00

51

00

40

00

13

10

0

34

00

33

00

20

00

87

00

40

00

30

00

20

00

90

00

42

80

0

45

00

0

22

00

5.1

4

Installati

on of

equipme

nt

70

00

70

00

80

00

80

00

11

00

0

11

00

0

35

00

35

00

29

50

0

28

00

0

-

15

00

-

5.0

8

Interest

on debt

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

96

00

0

10

00

00

40

00

4.1

7

Office

Supplies

22

00

0

21

00

0

20

00

0

63

00

0

19

00

0

20

00

0

21

00

0

60

00

0

25

00

0

18

00

0

19

00

0

62

00

0

20

00

0

21

00

0

22

00

0

63

00

0

24

80

00

20

00

00

-

48

00

0

-

19.

35

Payroll

Taxes

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

24

00

0

20

00

0

-

40

00

-

16.

67

Printing 50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

60

00

0

50

00

0

-

10

00

0

-

16.

67

Professi

onal

Fees

15

00

0

14

00

0

10

00

0

39

00

0

11

00

0

12

00

0

13

00

0

36

00

0

10

00

0

12

00

0

13

00

0

35

00

0

15

00

0

14

00

0

13

50

0

42

50

0

15

25

00

15

00

00

-

25

00

-

1.6

4

Telepho

ne

expense

s

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

42

00

0

40

00

0

-

20

00

-

4.7

6

Vehicle

expense

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

13

20

00

13

00

00

-

20

00

-

1.5

2

Total

expenses

89

50

0

77

50

0

72

50

0

23

95

00

74

50

0

83

60

0

77

50

0

23

56

00

78

90

0

82

80

0

73

50

0

23

52

00

83

00

0

76

50

0

77

00

0

23

65

00

94

68

00

89

30

00

-

53

80

0

-

5.6

8

Net

Profit

before

taxes

30

50

0

83

50

0

90

30

0

20

43

00

83

50

0

-

16

60

0

18

05

00

24

74

00

16

71

00

14

20

0

69

50

0

25

08

00

23

00

0

17

65

00

98

00

0

29

75

00

10

00

00

0

10

57

00

0

57

00

0

5.7

0

10

Incurred

00

0

00

0

00

0

50

00

00

0

00

0

00

0

00

00

00

0

00

0

00

0

00

0

00

0

00

0

00

0

70

00

70

00

00

00

00 6

Gross

Profit

12

00

00

16

10

00

16

28

00

44

38

00

15

80

00

67

00

0

25

80

00

48

30

00

24

60

00

97

00

0

14

30

00

48

60

00

10

60

00

25

30

00

17

50

00

53

40

00

19

46

80

0

19

50

00

0

32

00

0.1

6

Expenses

:

Advertisi

ng

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

10

00

0

10

00

0

10

00

0

30

00

0

12

00

00

13

00

00

10

00

0

8.3

3

Bank

Service

Charges

50

00

40

00

30

00

12

00

0

40

00

51

00

40

00

13

10

0

34

00

33

00

20

00

87

00

40

00

30

00

20

00

90

00

42

80

0

45

00

0

22

00

5.1

4

Installati

on of

equipme

nt

70

00

70

00

80

00

80

00

11

00

0

11

00

0

35

00

35

00

29

50

0

28

00

0

-

15

00

-

5.0

8

Interest

on debt

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

80

00

80

00

80

00

24

00

0

96

00

0

10

00

00

40

00

4.1

7

Office

Supplies

22

00

0

21

00

0

20

00

0

63

00

0

19

00

0

20

00

0

21

00

0

60

00

0

25

00

0

18

00

0

19

00

0

62

00

0

20

00

0

21

00

0

22

00

0

63

00

0

24

80

00

20

00

00

-

48

00

0

-

19.

35

Payroll

Taxes

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

20

00

20

00

20

00

60

00

24

00

0

20

00

0

-

40

00

-

16.

67

Printing 50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

50

00

50

00

50

00

15

00

0

60

00

0

50

00

0

-

10

00

0

-

16.

67

Professi

onal

Fees

15

00

0

14

00

0

10

00

0

39

00

0

11

00

0

12

00

0

13

00

0

36

00

0

10

00

0

12

00

0

13

00

0

35

00

0

15

00

0

14

00

0

13

50

0

42

50

0

15

25

00

15

00

00

-

25

00

-

1.6

4

Telepho

ne

expense

s

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

35

00

35

00

35

00

10

50

0

42

00

0

40

00

0

-

20

00

-

4.7

6

Vehicle

expense

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

12

00

0

10

00

0

11

00

0

33

00

0

13

20

00

13

00

00

-

20

00

-

1.5

2

Total

expenses

89

50

0

77

50

0

72

50

0

23

95

00

74

50

0

83

60

0

77

50

0

23

56

00

78

90

0

82

80

0

73

50

0

23

52

00

83

00

0

76

50

0

77

00

0

23

65

00

94

68

00

89

30

00

-

53

80

0

-

5.6

8

Net

Profit

before

taxes

30

50

0

83

50

0

90

30

0

20

43

00

83

50

0

-

16

60

0

18

05

00

24

74

00

16

71

00

14

20

0

69

50

0

25

08

00

23

00

0

17

65

00

98

00

0

29

75

00

10

00

00

0

10

57

00

0

57

00

0

5.7

0

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

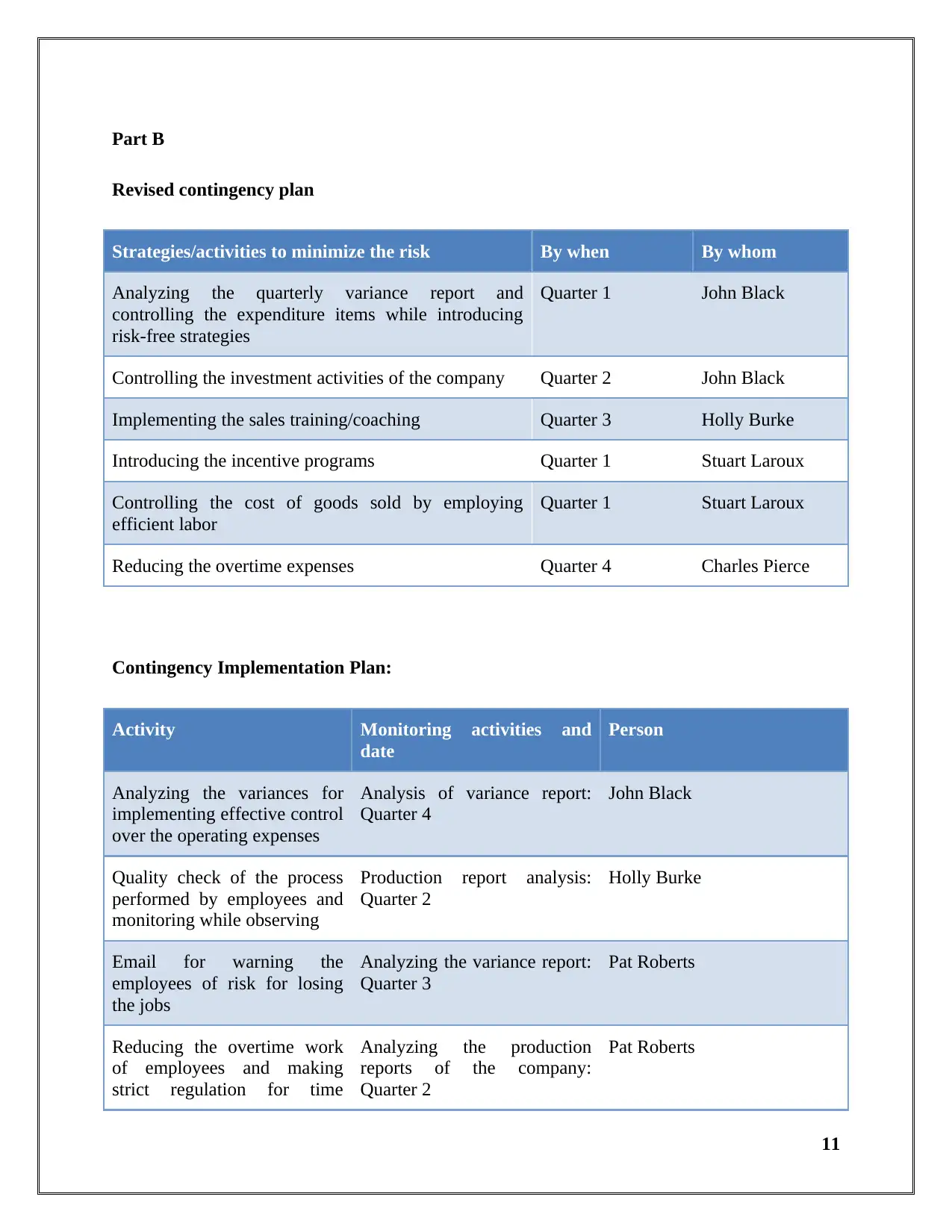

Part B

Revised contingency plan

Strategies/activities to minimize the risk By when By whom

Analyzing the quarterly variance report and

controlling the expenditure items while introducing

risk-free strategies

Quarter 1 John Black

Controlling the investment activities of the company Quarter 2 John Black

Implementing the sales training/coaching Quarter 3 Holly Burke

Introducing the incentive programs Quarter 1 Stuart Laroux

Controlling the cost of goods sold by employing

efficient labor

Quarter 1 Stuart Laroux

Reducing the overtime expenses Quarter 4 Charles Pierce

Contingency Implementation Plan:

Activity Monitoring activities and

date

Person

Analyzing the variances for

implementing effective control

over the operating expenses

Analysis of variance report:

Quarter 4

John Black

Quality check of the process

performed by employees and

monitoring while observing

Production report analysis:

Quarter 2

Holly Burke

Email for warning the

employees of risk for losing

the jobs

Analyzing the variance report:

Quarter 3

Pat Roberts

Reducing the overtime work

of employees and making

strict regulation for time

Analyzing the production

reports of the company:

Quarter 2

Pat Roberts

11

Revised contingency plan

Strategies/activities to minimize the risk By when By whom

Analyzing the quarterly variance report and

controlling the expenditure items while introducing

risk-free strategies

Quarter 1 John Black

Controlling the investment activities of the company Quarter 2 John Black

Implementing the sales training/coaching Quarter 3 Holly Burke

Introducing the incentive programs Quarter 1 Stuart Laroux

Controlling the cost of goods sold by employing

efficient labor

Quarter 1 Stuart Laroux

Reducing the overtime expenses Quarter 4 Charles Pierce

Contingency Implementation Plan:

Activity Monitoring activities and

date

Person

Analyzing the variances for

implementing effective control

over the operating expenses

Analysis of variance report:

Quarter 4

John Black

Quality check of the process

performed by employees and

monitoring while observing

Production report analysis:

Quarter 2

Holly Burke

Email for warning the

employees of risk for losing

the jobs

Analyzing the variance report:

Quarter 3

Pat Roberts

Reducing the overtime work

of employees and making

strict regulation for time

Analyzing the production

reports of the company:

Quarter 2

Pat Roberts

11

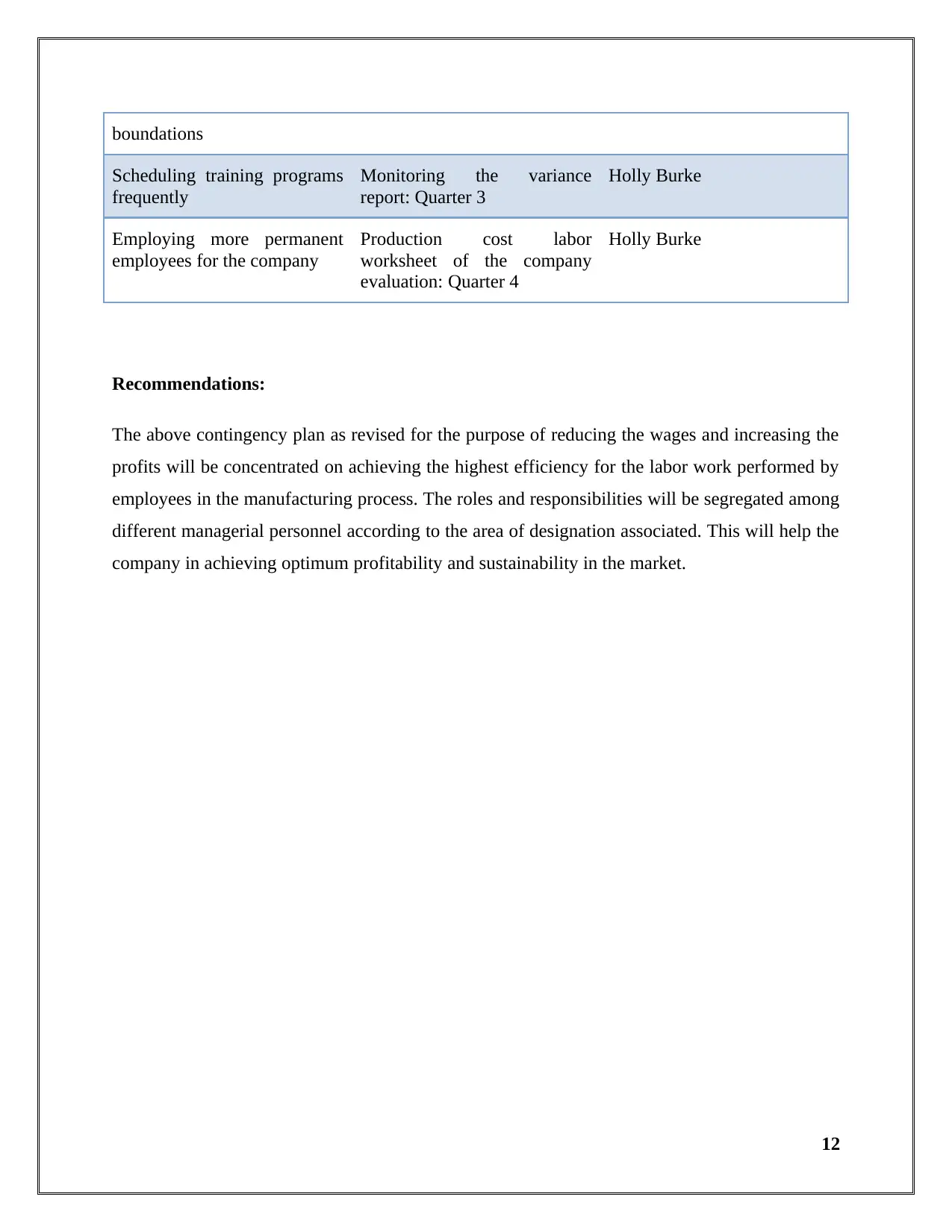

boundations

Scheduling training programs

frequently

Monitoring the variance

report: Quarter 3

Holly Burke

Employing more permanent

employees for the company

Production cost labor

worksheet of the company

evaluation: Quarter 4

Holly Burke

Recommendations:

The above contingency plan as revised for the purpose of reducing the wages and increasing the

profits will be concentrated on achieving the highest efficiency for the labor work performed by

employees in the manufacturing process. The roles and responsibilities will be segregated among

different managerial personnel according to the area of designation associated. This will help the

company in achieving optimum profitability and sustainability in the market.

12

Scheduling training programs

frequently

Monitoring the variance

report: Quarter 3

Holly Burke

Employing more permanent

employees for the company

Production cost labor

worksheet of the company

evaluation: Quarter 4

Holly Burke

Recommendations:

The above contingency plan as revised for the purpose of reducing the wages and increasing the

profits will be concentrated on achieving the highest efficiency for the labor work performed by

employees in the manufacturing process. The roles and responsibilities will be segregated among

different managerial personnel according to the area of designation associated. This will help the

company in achieving optimum profitability and sustainability in the market.

12

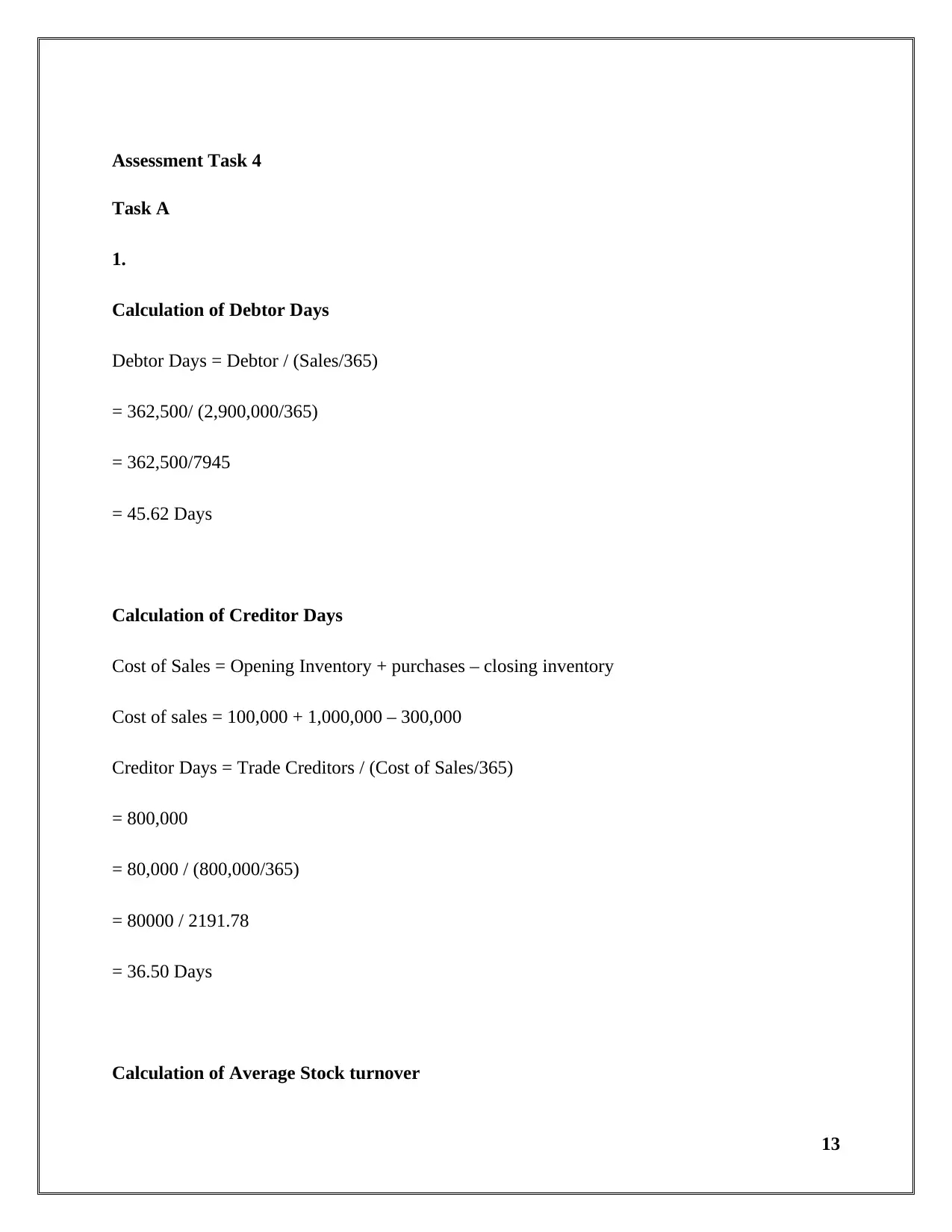

Assessment Task 4

Task A

1.

Calculation of Debtor Days

Debtor Days = Debtor / (Sales/365)

= 362,500/ (2,900,000/365)

= 362,500/7945

= 45.62 Days

Calculation of Creditor Days

Cost of Sales = Opening Inventory + purchases – closing inventory

Cost of sales = 100,000 + 1,000,000 – 300,000

Creditor Days = Trade Creditors / (Cost of Sales/365)

= 800,000

= 80,000 / (800,000/365)

= 80000 / 2191.78

= 36.50 Days

Calculation of Average Stock turnover

13

Task A

1.

Calculation of Debtor Days

Debtor Days = Debtor / (Sales/365)

= 362,500/ (2,900,000/365)

= 362,500/7945

= 45.62 Days

Calculation of Creditor Days

Cost of Sales = Opening Inventory + purchases – closing inventory

Cost of sales = 100,000 + 1,000,000 – 300,000

Creditor Days = Trade Creditors / (Cost of Sales/365)

= 800,000

= 80,000 / (800,000/365)

= 80000 / 2191.78

= 36.50 Days

Calculation of Average Stock turnover

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

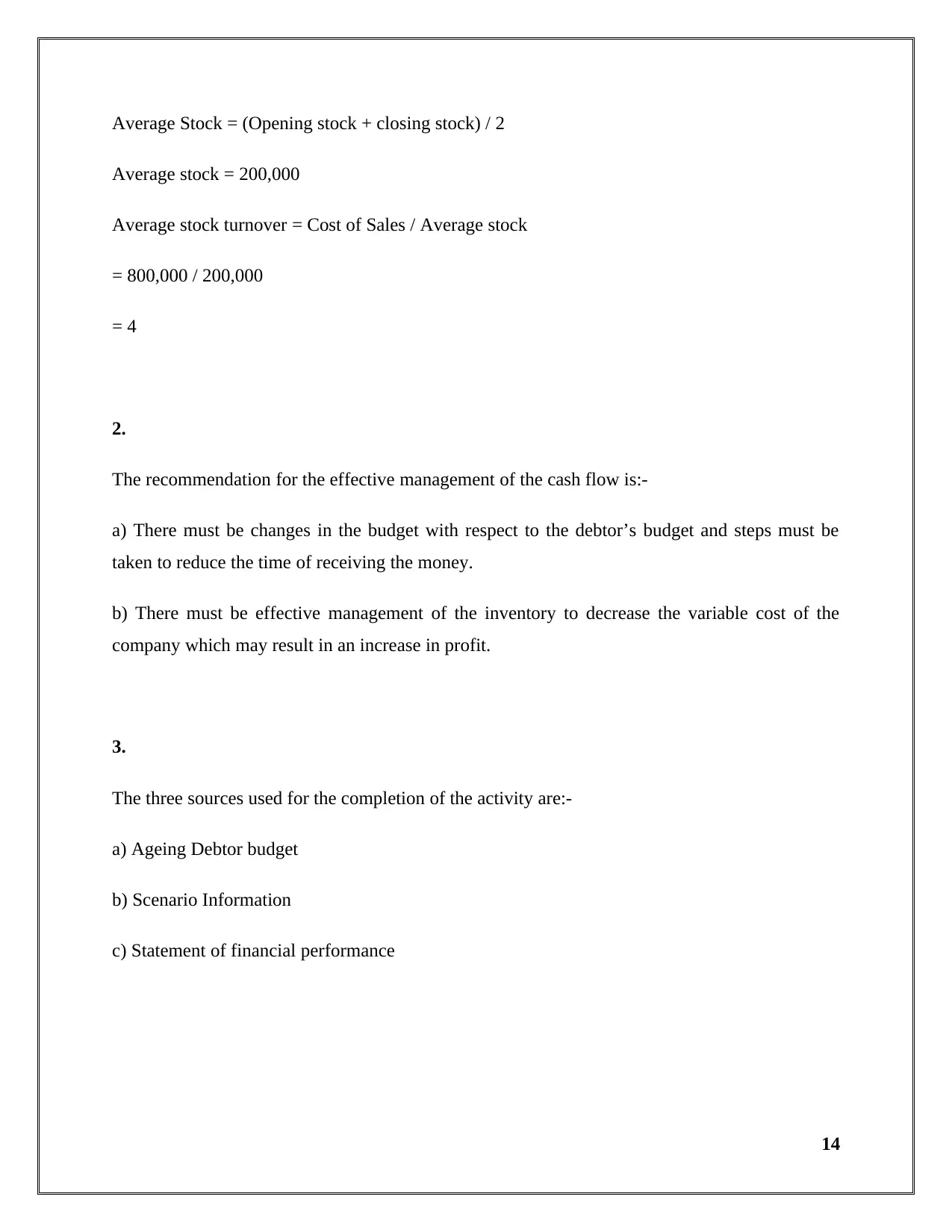

Average Stock = (Opening stock + closing stock) / 2

Average stock = 200,000

Average stock turnover = Cost of Sales / Average stock

= 800,000 / 200,000

= 4

2.

The recommendation for the effective management of the cash flow is:-

a) There must be changes in the budget with respect to the debtor’s budget and steps must be

taken to reduce the time of receiving the money.

b) There must be effective management of the inventory to decrease the variable cost of the

company which may result in an increase in profit.

3.

The three sources used for the completion of the activity are:-

a) Ageing Debtor budget

b) Scenario Information

c) Statement of financial performance

14

Average stock = 200,000

Average stock turnover = Cost of Sales / Average stock

= 800,000 / 200,000

= 4

2.

The recommendation for the effective management of the cash flow is:-

a) There must be changes in the budget with respect to the debtor’s budget and steps must be

taken to reduce the time of receiving the money.

b) There must be effective management of the inventory to decrease the variable cost of the

company which may result in an increase in profit.

3.

The three sources used for the completion of the activity are:-

a) Ageing Debtor budget

b) Scenario Information

c) Statement of financial performance

14

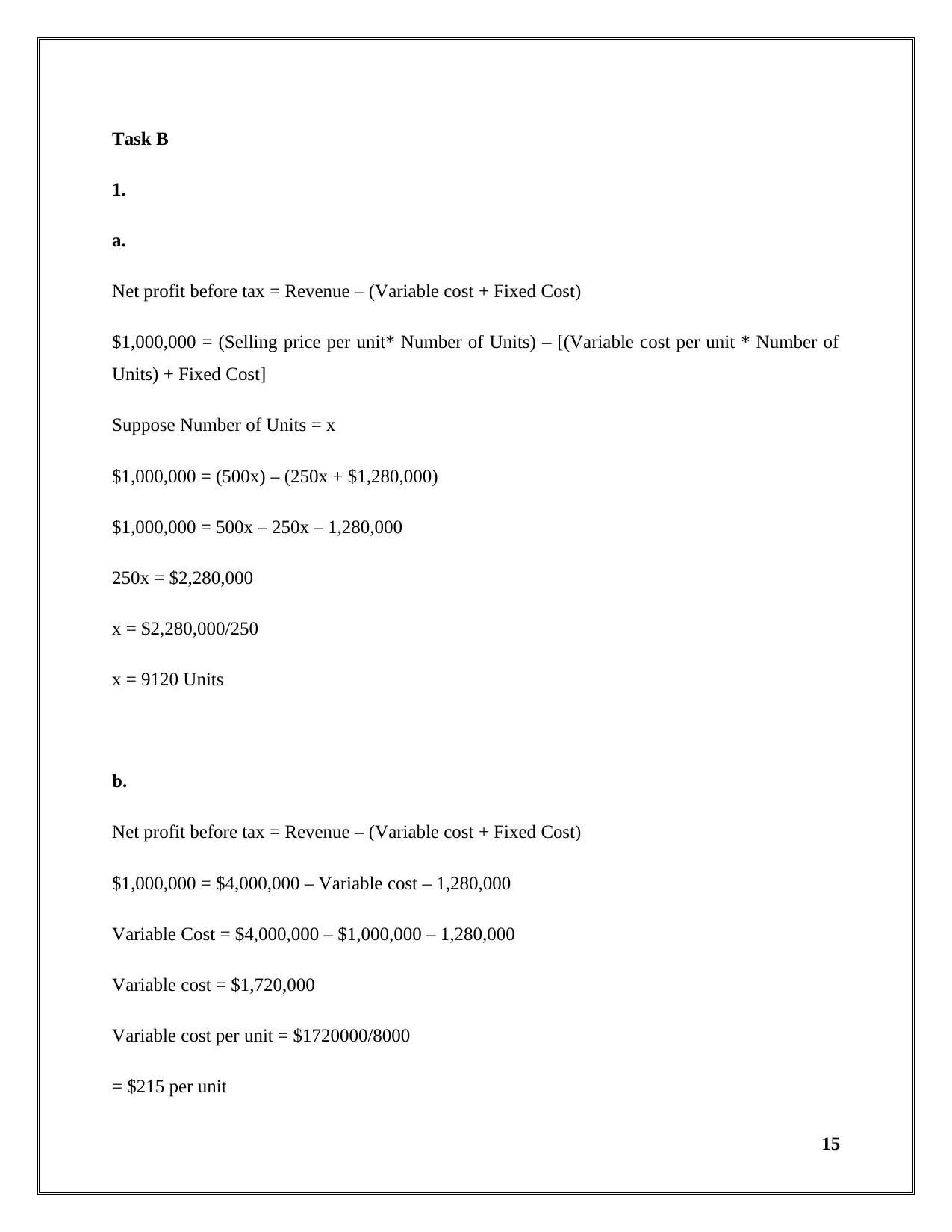

Task B

1.

a.

Net profit before tax = Revenue – (Variable cost + Fixed Cost)

$1,000,000 = (Selling price per unit* Number of Units) – [(Variable cost per unit * Number of

Units) + Fixed Cost]

Suppose Number of Units = x

$1,000,000 = (500x) – (250x + $1,280,000)

$1,000,000 = 500x – 250x – 1,280,000

250x = $2,280,000

x = $2,280,000/250

x = 9120 Units

b.

Net profit before tax = Revenue – (Variable cost + Fixed Cost)

$1,000,000 = $4,000,000 – Variable cost – 1,280,000

Variable Cost = $4,000,000 – $1,000,000 – 1,280,000

Variable cost = $1,720,000

Variable cost per unit = $1720000/8000

= $215 per unit

15

1.

a.

Net profit before tax = Revenue – (Variable cost + Fixed Cost)

$1,000,000 = (Selling price per unit* Number of Units) – [(Variable cost per unit * Number of

Units) + Fixed Cost]

Suppose Number of Units = x

$1,000,000 = (500x) – (250x + $1,280,000)

$1,000,000 = 500x – 250x – 1,280,000

250x = $2,280,000

x = $2,280,000/250

x = 9120 Units

b.

Net profit before tax = Revenue – (Variable cost + Fixed Cost)

$1,000,000 = $4,000,000 – Variable cost – 1,280,000

Variable Cost = $4,000,000 – $1,000,000 – 1,280,000

Variable cost = $1,720,000

Variable cost per unit = $1720000/8000

= $215 per unit

15

2.

It is important for the organisation to manage the variable cost that is being incurred so that there

can be an increase in the profit margin of the company. It is important that to decrease the

variable cost the operational efficiency must be increased so that there can be full utilisation of

the resources that are available to them. The utilisation of the resources will help in minimising

the overhead cost thus reducing the overall variable cost of the company. The decrease in

variable cost will help the big red bicycle to achieve the objective of the company that is to earn

a net profit before tax of $1,000,000.

3.

The sources of information that would be required for the same are:-

a) Profit and Loss account

b) Cash flow statement

c) Business activity statement

16

It is important for the organisation to manage the variable cost that is being incurred so that there

can be an increase in the profit margin of the company. It is important that to decrease the

variable cost the operational efficiency must be increased so that there can be full utilisation of

the resources that are available to them. The utilisation of the resources will help in minimising

the overhead cost thus reducing the overall variable cost of the company. The decrease in

variable cost will help the big red bicycle to achieve the objective of the company that is to earn

a net profit before tax of $1,000,000.

3.

The sources of information that would be required for the same are:-

a) Profit and Loss account

b) Cash flow statement

c) Business activity statement

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

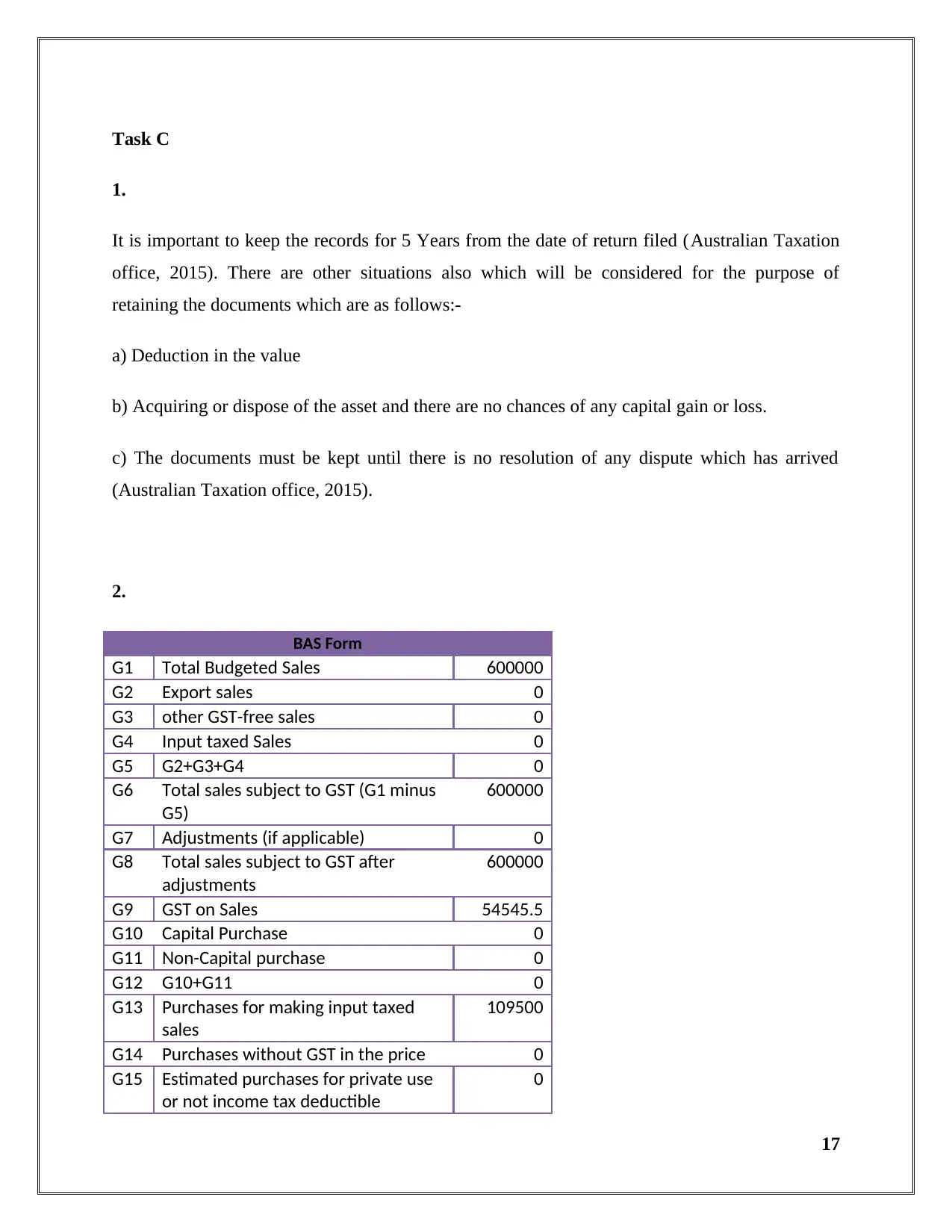

Task C

1.

It is important to keep the records for 5 Years from the date of return filed (Australian Taxation

office, 2015). There are other situations also which will be considered for the purpose of

retaining the documents which are as follows:-

a) Deduction in the value

b) Acquiring or dispose of the asset and there are no chances of any capital gain or loss.

c) The documents must be kept until there is no resolution of any dispute which has arrived

(Australian Taxation office, 2015).

2.

BAS Form

G1 Total Budgeted Sales 600000

G2 Export sales 0

G3 other GST-free sales 0

G4 Input taxed Sales 0

G5 G2+G3+G4 0

G6 Total sales subject to GST (G1 minus

G5)

600000

G7 Adjustments (if applicable) 0

G8 Total sales subject to GST after

adjustments

600000

G9 GST on Sales 54545.5

G10 Capital Purchase 0

G11 Non-Capital purchase 0

G12 G10+G11 0

G13 Purchases for making input taxed

sales

109500

G14 Purchases without GST in the price 0

G15 Estimated purchases for private use

or not income tax deductible

0

17

1.

It is important to keep the records for 5 Years from the date of return filed (Australian Taxation

office, 2015). There are other situations also which will be considered for the purpose of

retaining the documents which are as follows:-

a) Deduction in the value

b) Acquiring or dispose of the asset and there are no chances of any capital gain or loss.

c) The documents must be kept until there is no resolution of any dispute which has arrived

(Australian Taxation office, 2015).

2.

BAS Form

G1 Total Budgeted Sales 600000

G2 Export sales 0

G3 other GST-free sales 0

G4 Input taxed Sales 0

G5 G2+G3+G4 0

G6 Total sales subject to GST (G1 minus

G5)

600000

G7 Adjustments (if applicable) 0

G8 Total sales subject to GST after

adjustments

600000

G9 GST on Sales 54545.5

G10 Capital Purchase 0

G11 Non-Capital purchase 0

G12 G10+G11 0

G13 Purchases for making input taxed

sales

109500

G14 Purchases without GST in the price 0

G15 Estimated purchases for private use

or not income tax deductible

0

17

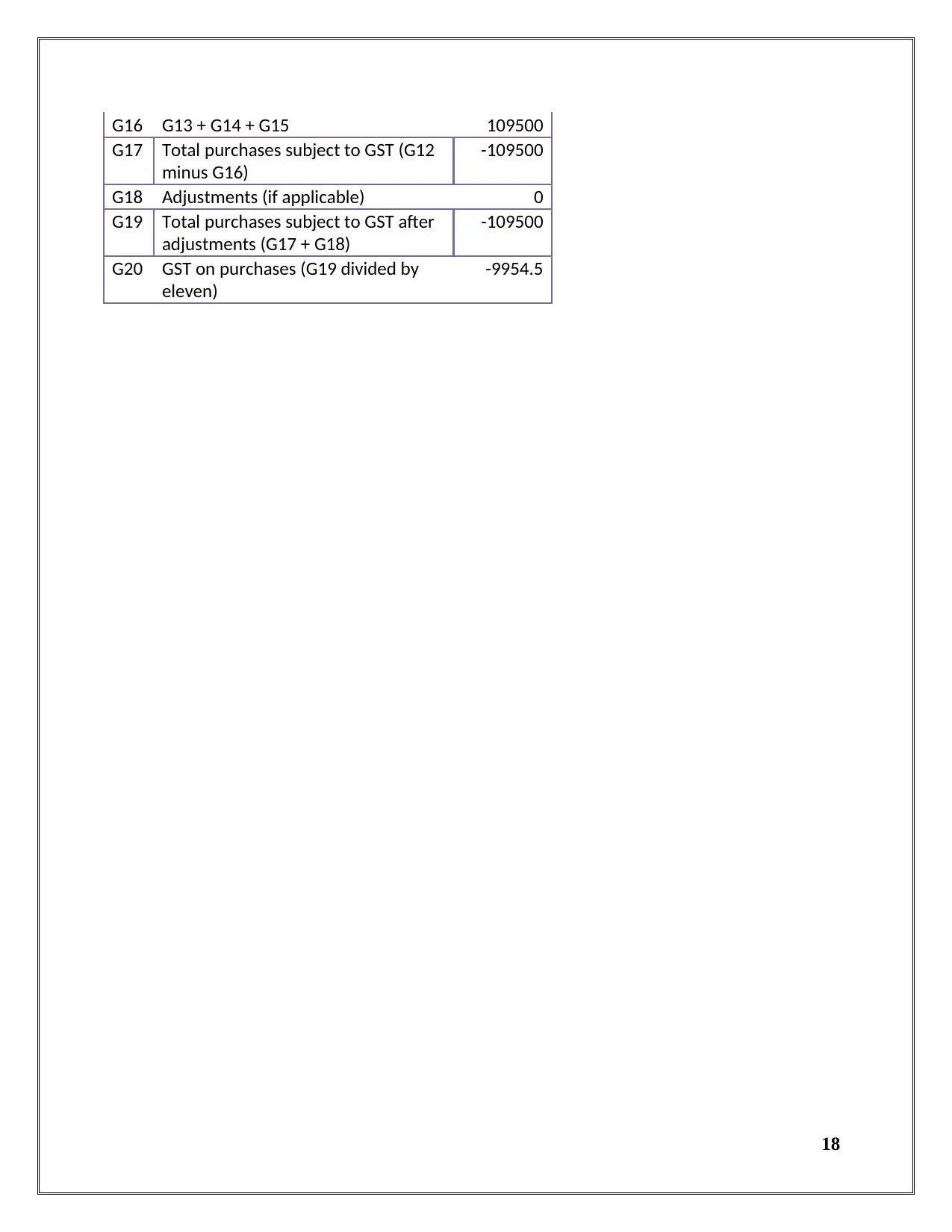

G16 G13 + G14 + G15 109500

G17 Total purchases subject to GST (G12

minus G16)

-109500

G18 Adjustments (if applicable) 0

G19 Total purchases subject to GST after

adjustments (G17 + G18)

-109500

G20 GST on purchases (G19 divided by

eleven)

-9954.5

18

G17 Total purchases subject to GST (G12

minus G16)

-109500

G18 Adjustments (if applicable) 0

G19 Total purchases subject to GST after

adjustments (G17 + G18)

-109500

G20 GST on purchases (G19 divided by

eleven)

-9954.5

18

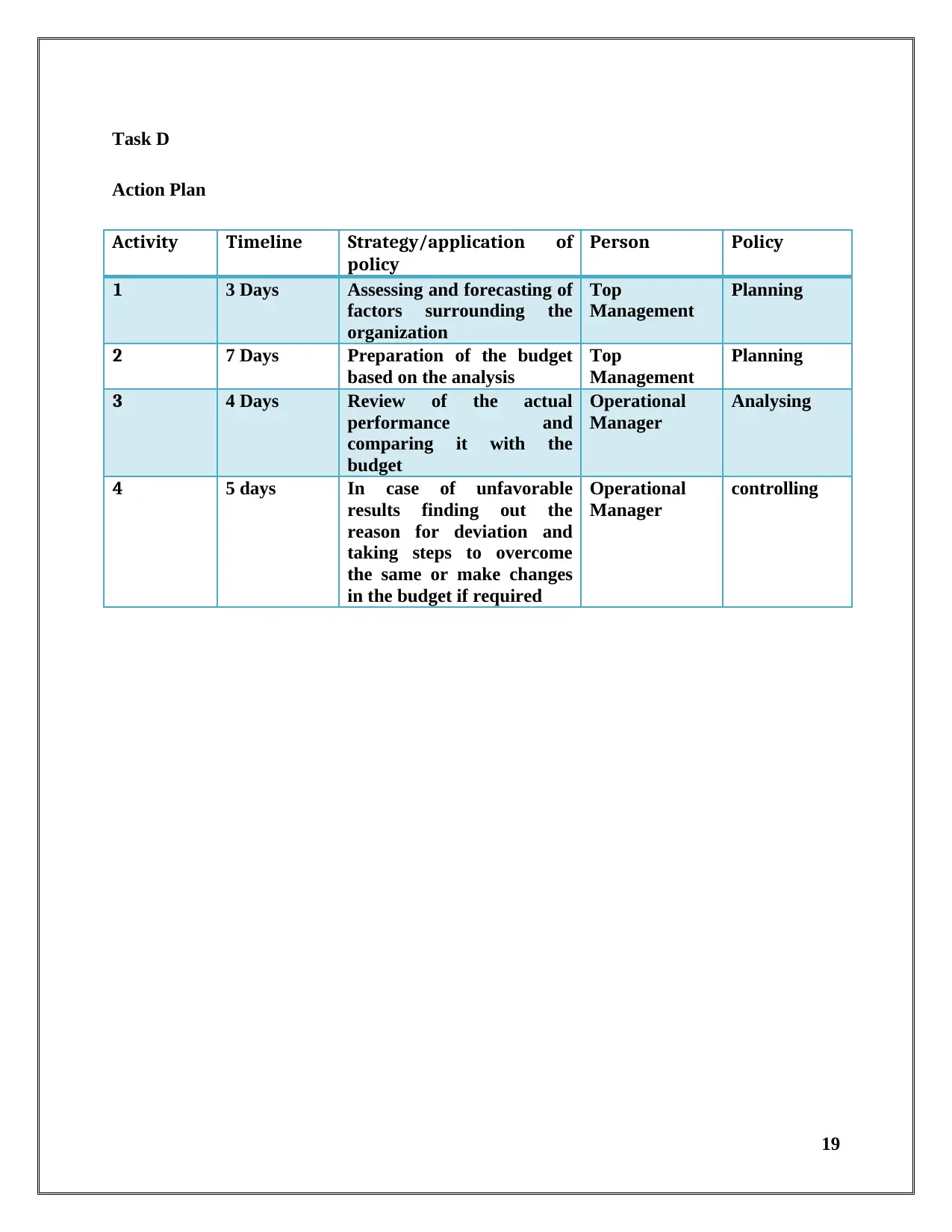

Task D

Action Plan

Activity Timeline Strategy/application of

policy

Person Policy

1 3 Days Assessing and forecasting of

factors surrounding the

organization

Top

Management

Planning

2 7 Days Preparation of the budget

based on the analysis

Top

Management

Planning

3 4 Days Review of the actual

performance and

comparing it with the

budget

Operational

Manager

Analysing

4 5 days In case of unfavorable

results finding out the

reason for deviation and

taking steps to overcome

the same or make changes

in the budget if required

Operational

Manager

controlling

19

Action Plan

Activity Timeline Strategy/application of

policy

Person Policy

1 3 Days Assessing and forecasting of

factors surrounding the

organization

Top

Management

Planning

2 7 Days Preparation of the budget

based on the analysis

Top

Management

Planning

3 4 Days Review of the actual

performance and

comparing it with the

budget

Operational

Manager

Analysing

4 5 days In case of unfavorable

results finding out the

reason for deviation and

taking steps to overcome

the same or make changes

in the budget if required

Operational

Manager

controlling

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task E

1.

According to MissCPA, (2012) accounting principle and concept are as follows:-

a) Business Entity

b) Going Concern

c) Monetary Unit

d) Matching Concept

e) Accounting Period

f) Consistency

g) Materiality

h) Objectivity

i) Accrual

j) Historical Cost

k) Conservatism

2.)

Cash flow can be defined as the inflow and outflow of the money flowing in both the directions.

The cash flow statement is based on the actual transactions that are both inflow and outflow. It is

important to prepare the cash flow statement for better management of the resources that are

available (Murray, 2017).

20

1.

According to MissCPA, (2012) accounting principle and concept are as follows:-

a) Business Entity

b) Going Concern

c) Monetary Unit

d) Matching Concept

e) Accounting Period

f) Consistency

g) Materiality

h) Objectivity

i) Accrual

j) Historical Cost

k) Conservatism

2.)

Cash flow can be defined as the inflow and outflow of the money flowing in both the directions.

The cash flow statement is based on the actual transactions that are both inflow and outflow. It is

important to prepare the cash flow statement for better management of the resources that are

available (Murray, 2017).

20

3.

The financial statement comprises of the balance sheet, income and expenditure statement,

owner’s equity statement, cash flow statement, and notes to accounts. The ledger accounts

consist of the debit and credit balances which are then matched based on the transaction that is

being conducted during the particular year.

4.

The profit and loss account can be defined as the summary of the revenue that is being earned

during the particular year through operations, expenses that are incurred during the year. The