Financial Analysis of Smart Computers: Report for CX554001, Block 1

VerifiedAdded on 2023/04/22

|15

|3271

|231

Report

AI Summary

This report presents a comprehensive financial analysis of Smart Computers, a sole trader, based on financial statements from 2017 to 2019. The analysis includes an introduction to financial analysis, ratio analysis (profitability, liquidity, and efficiency), a budget report, variance analysis, and CVP analysis. The report assesses the company's performance using key financial ratios, comparing them to industry averages where applicable. It calculates and interprets variances in the budget report, identifying favorable and unfavorable variances and their potential causes. Furthermore, the report analyzes the nature of expenses, including fixed and variable costs, and determines the break-even point in units. The conclusion summarizes the financial position of the company and provides recommendations to investors. The appendix provides supporting calculations and data.

Running head: REPORT 1

INTRODUCTION TO ACCOUNTING

STUDENT DETAILS:

2/25/2019

INTRODUCTION TO ACCOUNTING

STUDENT DETAILS:

2/25/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 2

Contents

Requirement 1:............................................................................................................................................3

Introduction.............................................................................................................................................3

Ratio analysis..........................................................................................................................................3

Profitability ratios................................................................................................................................3

Liquidity ratios....................................................................................................................................4

Efficiency ratio....................................................................................................................................4

Conclusion...............................................................................................................................................5

Requirement 2:............................................................................................................................................6

Budget Report..........................................................................................................................................6

Requirement 3:............................................................................................................................................6

Calculation of variances and nature of variances.....................................................................................6

Reasons of variance-................................................................................................................................8

Requirement 4:............................................................................................................................................8

Calculation of nature of expenses-...........................................................................................................8

Calculation of total fixed expenses-.........................................................................................................9

Calculation of total Variable expenses-.................................................................................................10

Calculation of variable cost per unit-.....................................................................................................10

Calculation of breakeven point in unit...................................................................................................10

Calculation of Units-.............................................................................................................................11

References.................................................................................................................................................12

Appendix...................................................................................................................................................14

Requirement 1:..........................................................................................................................................14

Contents

Requirement 1:............................................................................................................................................3

Introduction.............................................................................................................................................3

Ratio analysis..........................................................................................................................................3

Profitability ratios................................................................................................................................3

Liquidity ratios....................................................................................................................................4

Efficiency ratio....................................................................................................................................4

Conclusion...............................................................................................................................................5

Requirement 2:............................................................................................................................................6

Budget Report..........................................................................................................................................6

Requirement 3:............................................................................................................................................6

Calculation of variances and nature of variances.....................................................................................6

Reasons of variance-................................................................................................................................8

Requirement 4:............................................................................................................................................8

Calculation of nature of expenses-...........................................................................................................8

Calculation of total fixed expenses-.........................................................................................................9

Calculation of total Variable expenses-.................................................................................................10

Calculation of variable cost per unit-.....................................................................................................10

Calculation of breakeven point in unit...................................................................................................10

Calculation of Units-.............................................................................................................................11

References.................................................................................................................................................12

Appendix...................................................................................................................................................14

Requirement 1:..........................................................................................................................................14

REPORT 3

Requirement 1:

Introduction

The financial Analysis is considered as a significant tool. The financial analysis is very

helpful in deciding the company’s performance on the basis of evaluation of an income statement

of company, statement of financial position, evaluation with the help of ratio analysis and trend

analysis. The main purpose of the financial analysis is to decide whether the company is stable or

not, whether the company is solvent, liquid and profitable to affirm the financial investments.

The company can easily make the decisions related to investment. With the help of financial

analysis, the company can decide its strength and weakness. In this report, ratio analysis,

profitability of business, financial stability of business and asset analysis of business is discussed

and evaluated.

Ratio analysis

Profitability ratios

The profitability ratios of an entity are the ratios that decide how profitable an entity is

and how much share’s amount is available for the stakeholders after the expenditure’s payment

(Williams & Dobelman, 2017). The EPS of the entity may only be decided by an entity after the

calculation of the scenario of the profits.

Net profit ratio is a famous profitability ratio. The profitability ratio refers to the ratio that

decides the corporation’s capability to make the revenues out of sale generated in the year. This

ratio establishes the relation between net sales and net profit after the tax. It is calculated by

dividing net profit after tax by the net sales (Caudron, et.a l, 2018). The net profit is the major

standard for the investors, who have made invested in the businesses, to evaluate the economic

condition of the business. The net profit ratio is very is very useful in assessing whole

profitability of the company. The highest ratio states the proper management of the business’s

affairs. To see the improvement of profitability of company, the net profit ratio of smart

computers is compared with industry’s average net profit ratio. The net profit of the smart

computers is -3% in 2017, 11% in 2018 and 25.54% in the year 2019. It means company is

performing well. On the other hand, industry’s average net profit ratio is 21.68% in year 2019. It

means that the position of company is profitable in the comparison of industry.

Further, the gross profit ratio refers to the profitability ratio, which states the relation

between net sales and gross profit (Hançerlioğulları, Şen & Aktunç, 2016). This ratio is useful in

examining the company’s operational performance. The gross profit ratio is calculated by divide

gross profit by net sales. The main elements of the GP ratio is net sales and gross profit. The

gross profit is the net sales excluding the cost of goods sold. This ratio is very significant for the

companies. The gross profit must be proper to cover the expenditures. The highest gross profit

ratio is considered as the best gross profit ratio. The gross profit ratio of the company may be

assess by the comparison of ratio with the ratio of other companies in industry. The gross profit

Requirement 1:

Introduction

The financial Analysis is considered as a significant tool. The financial analysis is very

helpful in deciding the company’s performance on the basis of evaluation of an income statement

of company, statement of financial position, evaluation with the help of ratio analysis and trend

analysis. The main purpose of the financial analysis is to decide whether the company is stable or

not, whether the company is solvent, liquid and profitable to affirm the financial investments.

The company can easily make the decisions related to investment. With the help of financial

analysis, the company can decide its strength and weakness. In this report, ratio analysis,

profitability of business, financial stability of business and asset analysis of business is discussed

and evaluated.

Ratio analysis

Profitability ratios

The profitability ratios of an entity are the ratios that decide how profitable an entity is

and how much share’s amount is available for the stakeholders after the expenditure’s payment

(Williams & Dobelman, 2017). The EPS of the entity may only be decided by an entity after the

calculation of the scenario of the profits.

Net profit ratio is a famous profitability ratio. The profitability ratio refers to the ratio that

decides the corporation’s capability to make the revenues out of sale generated in the year. This

ratio establishes the relation between net sales and net profit after the tax. It is calculated by

dividing net profit after tax by the net sales (Caudron, et.a l, 2018). The net profit is the major

standard for the investors, who have made invested in the businesses, to evaluate the economic

condition of the business. The net profit ratio is very is very useful in assessing whole

profitability of the company. The highest ratio states the proper management of the business’s

affairs. To see the improvement of profitability of company, the net profit ratio of smart

computers is compared with industry’s average net profit ratio. The net profit of the smart

computers is -3% in 2017, 11% in 2018 and 25.54% in the year 2019. It means company is

performing well. On the other hand, industry’s average net profit ratio is 21.68% in year 2019. It

means that the position of company is profitable in the comparison of industry.

Further, the gross profit ratio refers to the profitability ratio, which states the relation

between net sales and gross profit (Hançerlioğulları, Şen & Aktunç, 2016). This ratio is useful in

examining the company’s operational performance. The gross profit ratio is calculated by divide

gross profit by net sales. The main elements of the GP ratio is net sales and gross profit. The

gross profit is the net sales excluding the cost of goods sold. This ratio is very significant for the

companies. The gross profit must be proper to cover the expenditures. The highest gross profit

ratio is considered as the best gross profit ratio. The gross profit ratio of the company may be

assess by the comparison of ratio with the ratio of other companies in industry. The gross profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 4

ratio of the smart computers is 60% in 2017, 62% in 2018 and 67.75% in year 2019. The

company is doing well. On the other hand, the gross profit ratio of the other companies of

industry is 64%. The gross profit ratio of smart computers is high. It means that the company

have sufficient profit to run company (Alexander, 2011).

Liquidity ratios

To assess the liquidity position of an entity, the current ratio and the quick ratio of an

entity is determined to find out the entity’s ability to provide the current liabilities through the

assistance of the current asset (Brigham & Houston, 2012).

The current ratio is the working capital ratio. The current ratio evaluates the ability of the

business to fulfil the short-term pending obligations in a year. The current ratio covers the weight

of current liabilities versus current assets (Hofstead-Duffy, et. al, 2012). The current ratio of the

company defines the economic health of the corporation and how this may increase the liquidity

of the current assets to set debts. The current ratio of the company should be preferably in the

ratio of 2:1. But, the current ratio of the smart computer is 2.81 in 2017, 1.51 in 2018 and 1.25 in

year 2019. On the other hand, the industry’s average current ratio is 1.90 in 2019. The company

should increase the current ratio for the viability of company. Otherwise, it can lead the

liquidation of company.

The liquidity ratio is known as quick ratio of the company (Rodrigues & Rodrigues,

2018). It is also known as acid-test ratio. The liquidity ratio refers to the ratio that evaluate the

capacity of the corporation to utilize the quick asset or cash to quench or withdraw the current

liabilities instantly. The normal liquid ratio is 1: 1 (Datta & Chakraborty, 2018). The quick ratio

of the smart computer is 2.06 in 2017, 1.08 in 2018 and 0.93 in 2019. On the other hand, liquid

ratio of industry is 1.15 in 2019. The company should increase the quick ratio to one or more

than one to do well (Yanadori & Kato, 2017).

Efficiency ratio

Asset management efficiency is assessed after examining the efficiency and productivity

of an entity to handle the assets (Vogel, 2014). Efficiency of assets management state in respect

of the position of asset in reference of numerous financial information. This assessment assists

the investor to recognize the operation and efficiency of an entity. The efficiency ratios are

chosen for evaluating because this ratio evaluate the ability of the corporation to make utilisation

of asset and source (Brammer, Brooks & Pavelin, 2016).

The inventory turnover ratio (times per year) refers to an activity ratio, which measure

the productivity of the inventory management of the company (Erasmus, et. al, 2016). The

inventory turnover ratio shows that how many times the company normally turns the inventories

in the sale per annum. The inventory turnover ratio may be calculated by dividing the COGS by

the average inventories of the company. For various companies, the ideal inventory turnover

ratio of the smart computers is 60% in 2017, 62% in 2018 and 67.75% in year 2019. The

company is doing well. On the other hand, the gross profit ratio of the other companies of

industry is 64%. The gross profit ratio of smart computers is high. It means that the company

have sufficient profit to run company (Alexander, 2011).

Liquidity ratios

To assess the liquidity position of an entity, the current ratio and the quick ratio of an

entity is determined to find out the entity’s ability to provide the current liabilities through the

assistance of the current asset (Brigham & Houston, 2012).

The current ratio is the working capital ratio. The current ratio evaluates the ability of the

business to fulfil the short-term pending obligations in a year. The current ratio covers the weight

of current liabilities versus current assets (Hofstead-Duffy, et. al, 2012). The current ratio of the

company defines the economic health of the corporation and how this may increase the liquidity

of the current assets to set debts. The current ratio of the company should be preferably in the

ratio of 2:1. But, the current ratio of the smart computer is 2.81 in 2017, 1.51 in 2018 and 1.25 in

year 2019. On the other hand, the industry’s average current ratio is 1.90 in 2019. The company

should increase the current ratio for the viability of company. Otherwise, it can lead the

liquidation of company.

The liquidity ratio is known as quick ratio of the company (Rodrigues & Rodrigues,

2018). It is also known as acid-test ratio. The liquidity ratio refers to the ratio that evaluate the

capacity of the corporation to utilize the quick asset or cash to quench or withdraw the current

liabilities instantly. The normal liquid ratio is 1: 1 (Datta & Chakraborty, 2018). The quick ratio

of the smart computer is 2.06 in 2017, 1.08 in 2018 and 0.93 in 2019. On the other hand, liquid

ratio of industry is 1.15 in 2019. The company should increase the quick ratio to one or more

than one to do well (Yanadori & Kato, 2017).

Efficiency ratio

Asset management efficiency is assessed after examining the efficiency and productivity

of an entity to handle the assets (Vogel, 2014). Efficiency of assets management state in respect

of the position of asset in reference of numerous financial information. This assessment assists

the investor to recognize the operation and efficiency of an entity. The efficiency ratios are

chosen for evaluating because this ratio evaluate the ability of the corporation to make utilisation

of asset and source (Brammer, Brooks & Pavelin, 2016).

The inventory turnover ratio (times per year) refers to an activity ratio, which measure

the productivity of the inventory management of the company (Erasmus, et. al, 2016). The

inventory turnover ratio shows that how many times the company normally turns the inventories

in the sale per annum. The inventory turnover ratio may be calculated by dividing the COGS by

the average inventories of the company. For various companies, the ideal inventory turnover

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 5

ratio is four to six. All businesses are dissimilar, obviously, however generally the ratio between

four and six normally means that the rate at which restock articles is balanced properly with the

turnover. The inventory turnover ratio of smart computers is 8 in 2017, 5 in 2018 and 4 in 2019.

On the other hand, the inventory turnover average industry ratio is 8 in 2019. The inventory

turnover ratio of the smart computers is ideal ratio in comparison of industry (Bartram, Brown &

Fehle, 2019).

Further, the account receivables turnover (times per year) is the number of times per year,

which the companies collect the average account receivable (Ferrer & Ferrer, 2016). The account

receivables turnover is useful in the evaluation of the capability of an entity to properly issue

credits to the consumers and take fund in the proper manner. When the account receivables

turnover (times per year) ratio is unreasonably less, the purchaser may view this as chances to

implement the more dynamic credit and collection practice, thus decreasing the working capital

investment required to operate the company (Bernstein, et. al, 2016). The account receivables

turnover (times per year) of smart computer is 3.57 in 2017, 1.92 in 2018 and 1.50 in 2019. On

the other hand, the account receivables turnover (times per year) of other companies of industry

is 9 in year 2019. The company should improved the credit policy for high account receivables

turnover in (Xia, et. al, 2016).

Conclusion

As per the above analysis, it can be concluded that financial analyses is significant tool to

analyze the financial position of the company in proper manner. However, the financial

statement analysis does not render answer to each question of user. In effect, it normally

generates additional queries. The ratio analysis renders an idea to investors in regarding the

financial position of corporation. Through the above calculations of ratios it can be said that the

net profit ratio and gross profit ratio is high. The smart computers also has ideal current ratio and

ideal inventory turnover ratio. The investor is suggested to make the investment in smart

computers.

ratio is four to six. All businesses are dissimilar, obviously, however generally the ratio between

four and six normally means that the rate at which restock articles is balanced properly with the

turnover. The inventory turnover ratio of smart computers is 8 in 2017, 5 in 2018 and 4 in 2019.

On the other hand, the inventory turnover average industry ratio is 8 in 2019. The inventory

turnover ratio of the smart computers is ideal ratio in comparison of industry (Bartram, Brown &

Fehle, 2019).

Further, the account receivables turnover (times per year) is the number of times per year,

which the companies collect the average account receivable (Ferrer & Ferrer, 2016). The account

receivables turnover is useful in the evaluation of the capability of an entity to properly issue

credits to the consumers and take fund in the proper manner. When the account receivables

turnover (times per year) ratio is unreasonably less, the purchaser may view this as chances to

implement the more dynamic credit and collection practice, thus decreasing the working capital

investment required to operate the company (Bernstein, et. al, 2016). The account receivables

turnover (times per year) of smart computer is 3.57 in 2017, 1.92 in 2018 and 1.50 in 2019. On

the other hand, the account receivables turnover (times per year) of other companies of industry

is 9 in year 2019. The company should improved the credit policy for high account receivables

turnover in (Xia, et. al, 2016).

Conclusion

As per the above analysis, it can be concluded that financial analyses is significant tool to

analyze the financial position of the company in proper manner. However, the financial

statement analysis does not render answer to each question of user. In effect, it normally

generates additional queries. The ratio analysis renders an idea to investors in regarding the

financial position of corporation. Through the above calculations of ratios it can be said that the

net profit ratio and gross profit ratio is high. The smart computers also has ideal current ratio and

ideal inventory turnover ratio. The investor is suggested to make the investment in smart

computers.

REPORT 6

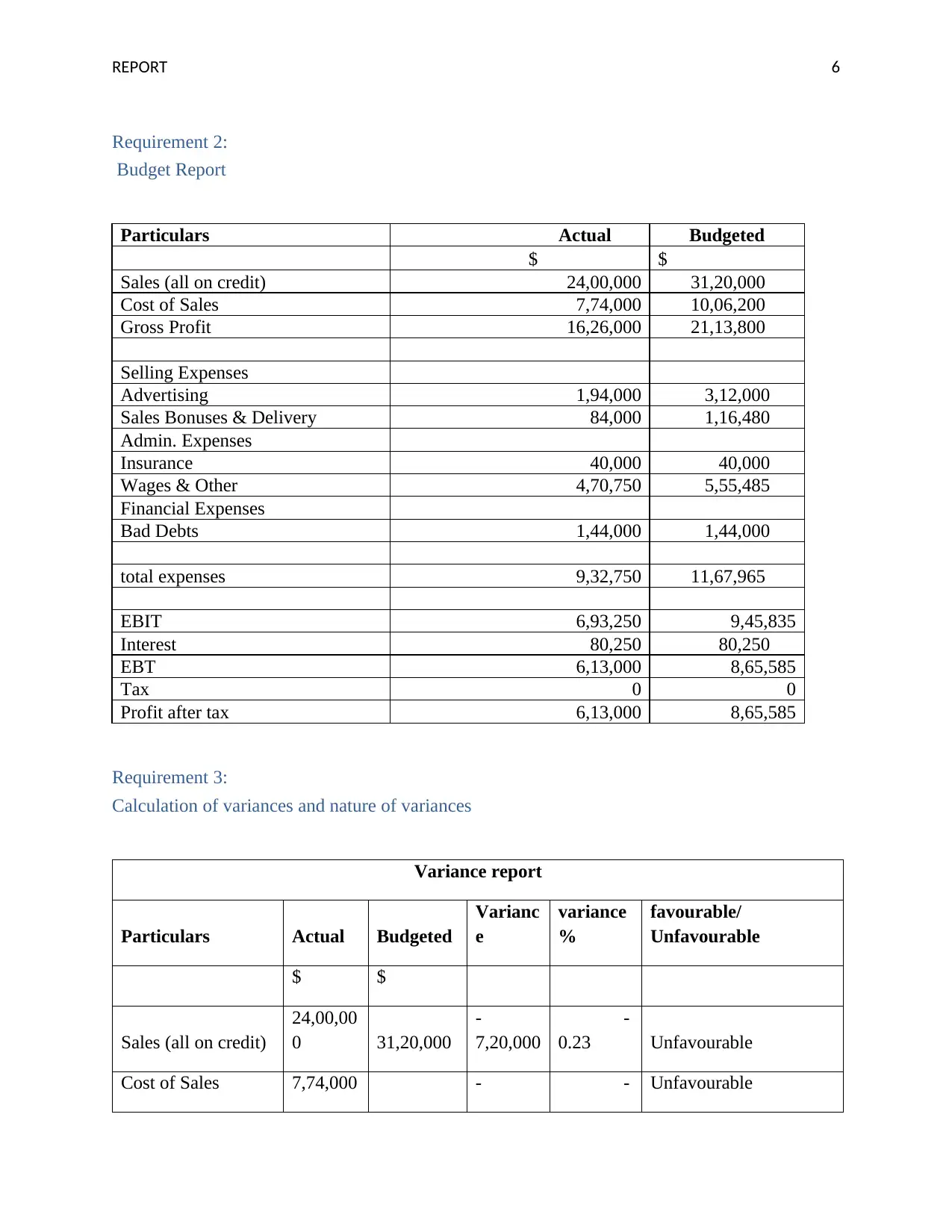

Requirement 2:

Budget Report

Particulars Actual Budgeted

$ $

Sales (all on credit) 24,00,000 31,20,000

Cost of Sales 7,74,000 10,06,200

Gross Profit 16,26,000 21,13,800

Selling Expenses

Advertising 1,94,000 3,12,000

Sales Bonuses & Delivery 84,000 1,16,480

Admin. Expenses

Insurance 40,000 40,000

Wages & Other 4,70,750 5,55,485

Financial Expenses

Bad Debts 1,44,000 1,44,000

total expenses 9,32,750 11,67,965

EBIT 6,93,250 9,45,835

Interest 80,250 80,250

EBT 6,13,000 8,65,585

Tax 0 0

Profit after tax 6,13,000 8,65,585

Requirement 3:

Calculation of variances and nature of variances

Variance report

Particulars Actual Budgeted

Varianc

e

variance

%

favourable/

Unfavourable

$ $

Sales (all on credit)

24,00,00

0 31,20,000

-

7,20,000

-

0.23 Unfavourable

Cost of Sales 7,74,000 - - Unfavourable

Requirement 2:

Budget Report

Particulars Actual Budgeted

$ $

Sales (all on credit) 24,00,000 31,20,000

Cost of Sales 7,74,000 10,06,200

Gross Profit 16,26,000 21,13,800

Selling Expenses

Advertising 1,94,000 3,12,000

Sales Bonuses & Delivery 84,000 1,16,480

Admin. Expenses

Insurance 40,000 40,000

Wages & Other 4,70,750 5,55,485

Financial Expenses

Bad Debts 1,44,000 1,44,000

total expenses 9,32,750 11,67,965

EBIT 6,93,250 9,45,835

Interest 80,250 80,250

EBT 6,13,000 8,65,585

Tax 0 0

Profit after tax 6,13,000 8,65,585

Requirement 3:

Calculation of variances and nature of variances

Variance report

Particulars Actual Budgeted

Varianc

e

variance

%

favourable/

Unfavourable

$ $

Sales (all on credit)

24,00,00

0 31,20,000

-

7,20,000

-

0.23 Unfavourable

Cost of Sales 7,74,000 - - Unfavourable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

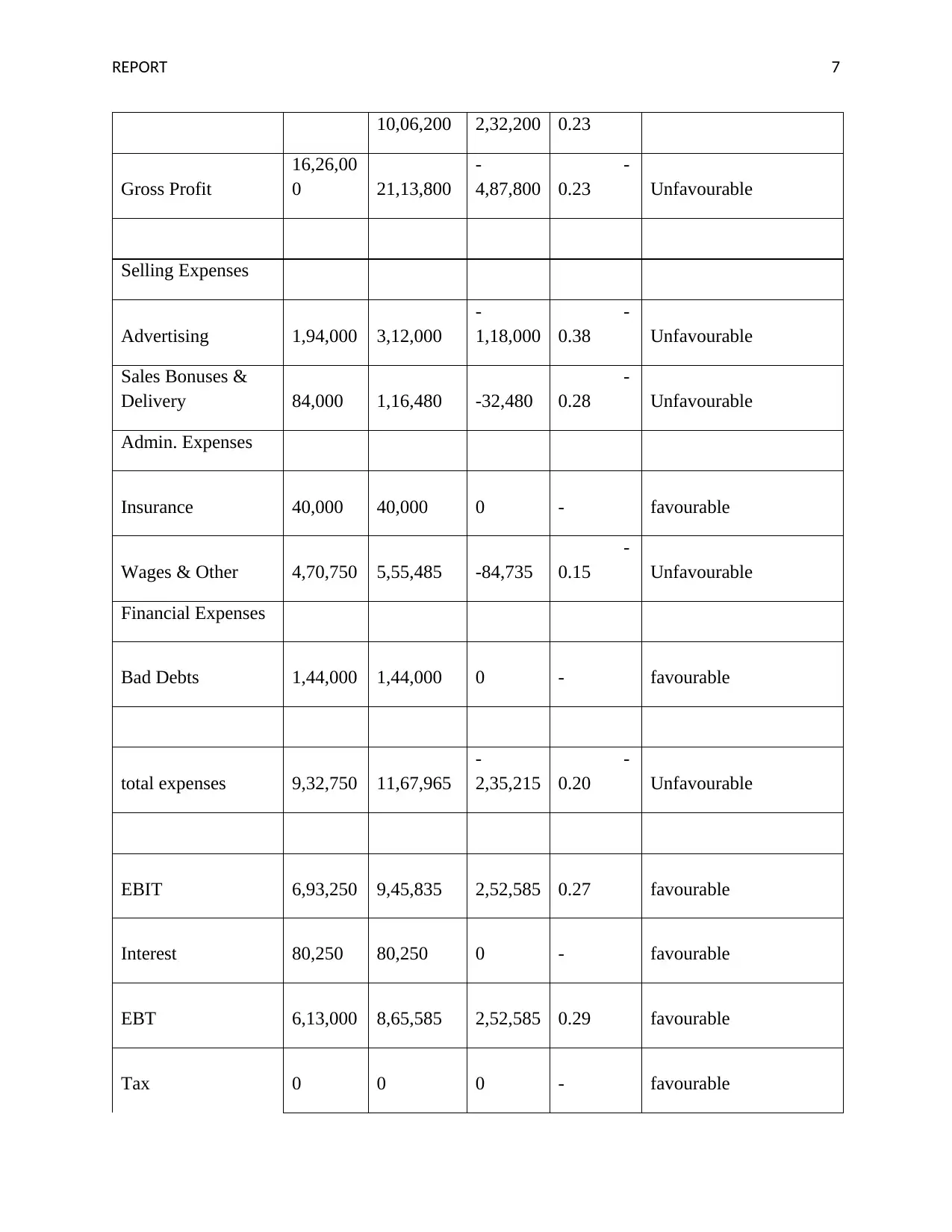

REPORT 7

10,06,200 2,32,200 0.23

Gross Profit

16,26,00

0 21,13,800

-

4,87,800

-

0.23 Unfavourable

Selling Expenses

Advertising 1,94,000 3,12,000

-

1,18,000

-

0.38 Unfavourable

Sales Bonuses &

Delivery 84,000 1,16,480 -32,480

-

0.28 Unfavourable

Admin. Expenses

Insurance 40,000 40,000 0 - favourable

Wages & Other 4,70,750 5,55,485 -84,735

-

0.15 Unfavourable

Financial Expenses

Bad Debts 1,44,000 1,44,000 0 - favourable

total expenses 9,32,750 11,67,965

-

2,35,215

-

0.20 Unfavourable

EBIT 6,93,250 9,45,835 2,52,585 0.27 favourable

Interest 80,250 80,250 0 - favourable

EBT 6,13,000 8,65,585 2,52,585 0.29 favourable

Tax 0 0 0 - favourable

10,06,200 2,32,200 0.23

Gross Profit

16,26,00

0 21,13,800

-

4,87,800

-

0.23 Unfavourable

Selling Expenses

Advertising 1,94,000 3,12,000

-

1,18,000

-

0.38 Unfavourable

Sales Bonuses &

Delivery 84,000 1,16,480 -32,480

-

0.28 Unfavourable

Admin. Expenses

Insurance 40,000 40,000 0 - favourable

Wages & Other 4,70,750 5,55,485 -84,735

-

0.15 Unfavourable

Financial Expenses

Bad Debts 1,44,000 1,44,000 0 - favourable

total expenses 9,32,750 11,67,965

-

2,35,215

-

0.20 Unfavourable

EBIT 6,93,250 9,45,835 2,52,585 0.27 favourable

Interest 80,250 80,250 0 - favourable

EBT 6,13,000 8,65,585 2,52,585 0.29 favourable

Tax 0 0 0 - favourable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 8

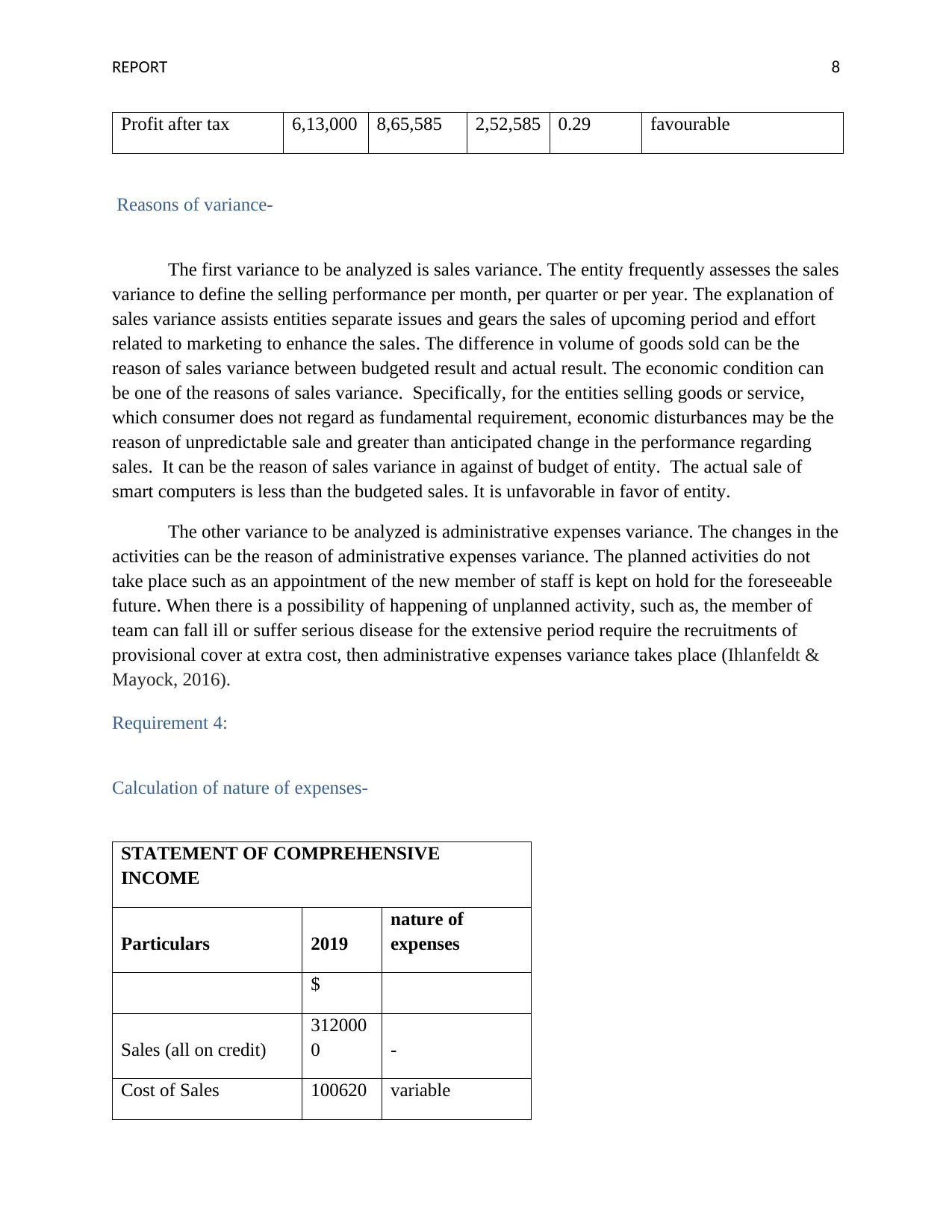

Profit after tax 6,13,000 8,65,585 2,52,585 0.29 favourable

Reasons of variance-

The first variance to be analyzed is sales variance. The entity frequently assesses the sales

variance to define the selling performance per month, per quarter or per year. The explanation of

sales variance assists entities separate issues and gears the sales of upcoming period and effort

related to marketing to enhance the sales. The difference in volume of goods sold can be the

reason of sales variance between budgeted result and actual result. The economic condition can

be one of the reasons of sales variance. Specifically, for the entities selling goods or service,

which consumer does not regard as fundamental requirement, economic disturbances may be the

reason of unpredictable sale and greater than anticipated change in the performance regarding

sales. It can be the reason of sales variance in against of budget of entity. The actual sale of

smart computers is less than the budgeted sales. It is unfavorable in favor of entity.

The other variance to be analyzed is administrative expenses variance. The changes in the

activities can be the reason of administrative expenses variance. The planned activities do not

take place such as an appointment of the new member of staff is kept on hold for the foreseeable

future. When there is a possibility of happening of unplanned activity, such as, the member of

team can fall ill or suffer serious disease for the extensive period require the recruitments of

provisional cover at extra cost, then administrative expenses variance takes place (Ihlanfeldt &

Mayock, 2016).

Requirement 4:

Calculation of nature of expenses-

STATEMENT OF COMPREHENSIVE

INCOME

Particulars 2019

nature of

expenses

$

Sales (all on credit)

312000

0 -

Cost of Sales 100620 variable

Profit after tax 6,13,000 8,65,585 2,52,585 0.29 favourable

Reasons of variance-

The first variance to be analyzed is sales variance. The entity frequently assesses the sales

variance to define the selling performance per month, per quarter or per year. The explanation of

sales variance assists entities separate issues and gears the sales of upcoming period and effort

related to marketing to enhance the sales. The difference in volume of goods sold can be the

reason of sales variance between budgeted result and actual result. The economic condition can

be one of the reasons of sales variance. Specifically, for the entities selling goods or service,

which consumer does not regard as fundamental requirement, economic disturbances may be the

reason of unpredictable sale and greater than anticipated change in the performance regarding

sales. It can be the reason of sales variance in against of budget of entity. The actual sale of

smart computers is less than the budgeted sales. It is unfavorable in favor of entity.

The other variance to be analyzed is administrative expenses variance. The changes in the

activities can be the reason of administrative expenses variance. The planned activities do not

take place such as an appointment of the new member of staff is kept on hold for the foreseeable

future. When there is a possibility of happening of unplanned activity, such as, the member of

team can fall ill or suffer serious disease for the extensive period require the recruitments of

provisional cover at extra cost, then administrative expenses variance takes place (Ihlanfeldt &

Mayock, 2016).

Requirement 4:

Calculation of nature of expenses-

STATEMENT OF COMPREHENSIVE

INCOME

Particulars 2019

nature of

expenses

$

Sales (all on credit)

312000

0 -

Cost of Sales 100620 variable

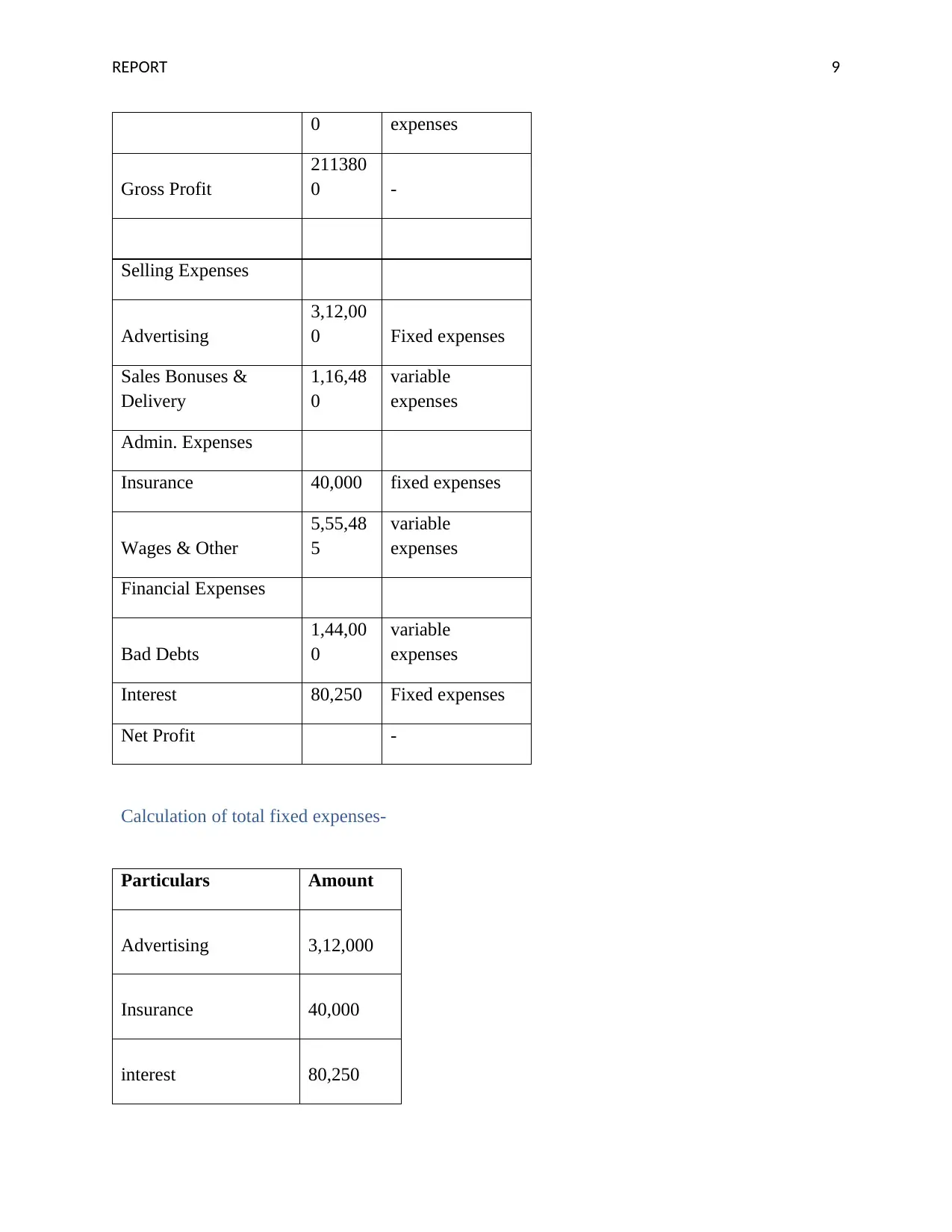

REPORT 9

0 expenses

Gross Profit

211380

0 -

Selling Expenses

Advertising

3,12,00

0 Fixed expenses

Sales Bonuses &

Delivery

1,16,48

0

variable

expenses

Admin. Expenses

Insurance 40,000 fixed expenses

Wages & Other

5,55,48

5

variable

expenses

Financial Expenses

Bad Debts

1,44,00

0

variable

expenses

Interest 80,250 Fixed expenses

Net Profit -

Calculation of total fixed expenses-

Particulars Amount

Advertising 3,12,000

Insurance 40,000

interest 80,250

0 expenses

Gross Profit

211380

0 -

Selling Expenses

Advertising

3,12,00

0 Fixed expenses

Sales Bonuses &

Delivery

1,16,48

0

variable

expenses

Admin. Expenses

Insurance 40,000 fixed expenses

Wages & Other

5,55,48

5

variable

expenses

Financial Expenses

Bad Debts

1,44,00

0

variable

expenses

Interest 80,250 Fixed expenses

Net Profit -

Calculation of total fixed expenses-

Particulars Amount

Advertising 3,12,000

Insurance 40,000

interest 80,250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 10

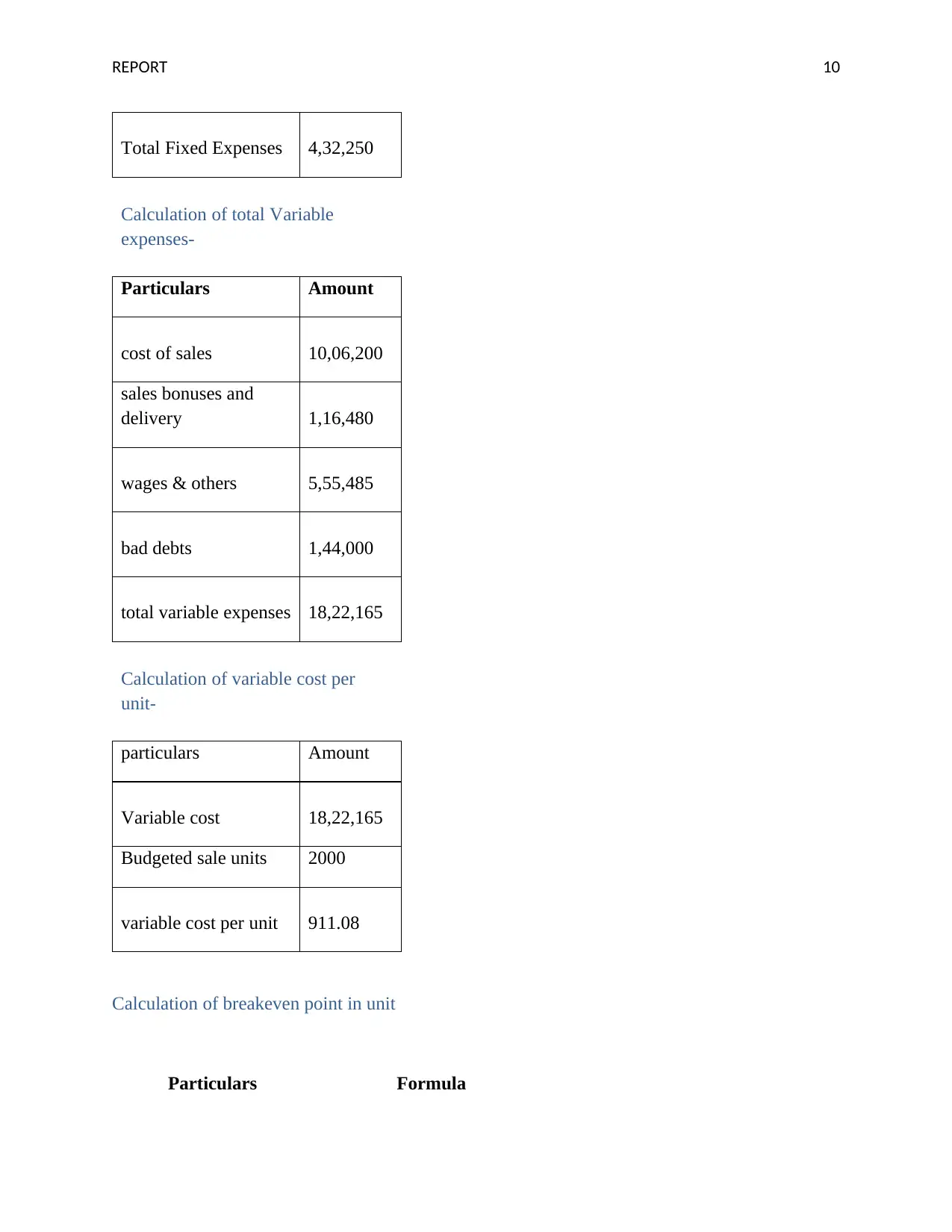

Total Fixed Expenses 4,32,250

Calculation of total Variable

expenses-

Particulars Amount

cost of sales 10,06,200

sales bonuses and

delivery 1,16,480

wages & others 5,55,485

bad debts 1,44,000

total variable expenses 18,22,165

Calculation of variable cost per

unit-

particulars Amount

Variable cost 18,22,165

Budgeted sale units 2000

variable cost per unit 911.08

Calculation of breakeven point in unit

Particulars Formula

Total Fixed Expenses 4,32,250

Calculation of total Variable

expenses-

Particulars Amount

cost of sales 10,06,200

sales bonuses and

delivery 1,16,480

wages & others 5,55,485

bad debts 1,44,000

total variable expenses 18,22,165

Calculation of variable cost per

unit-

particulars Amount

Variable cost 18,22,165

Budgeted sale units 2000

variable cost per unit 911.08

Calculation of breakeven point in unit

Particulars Formula

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 11

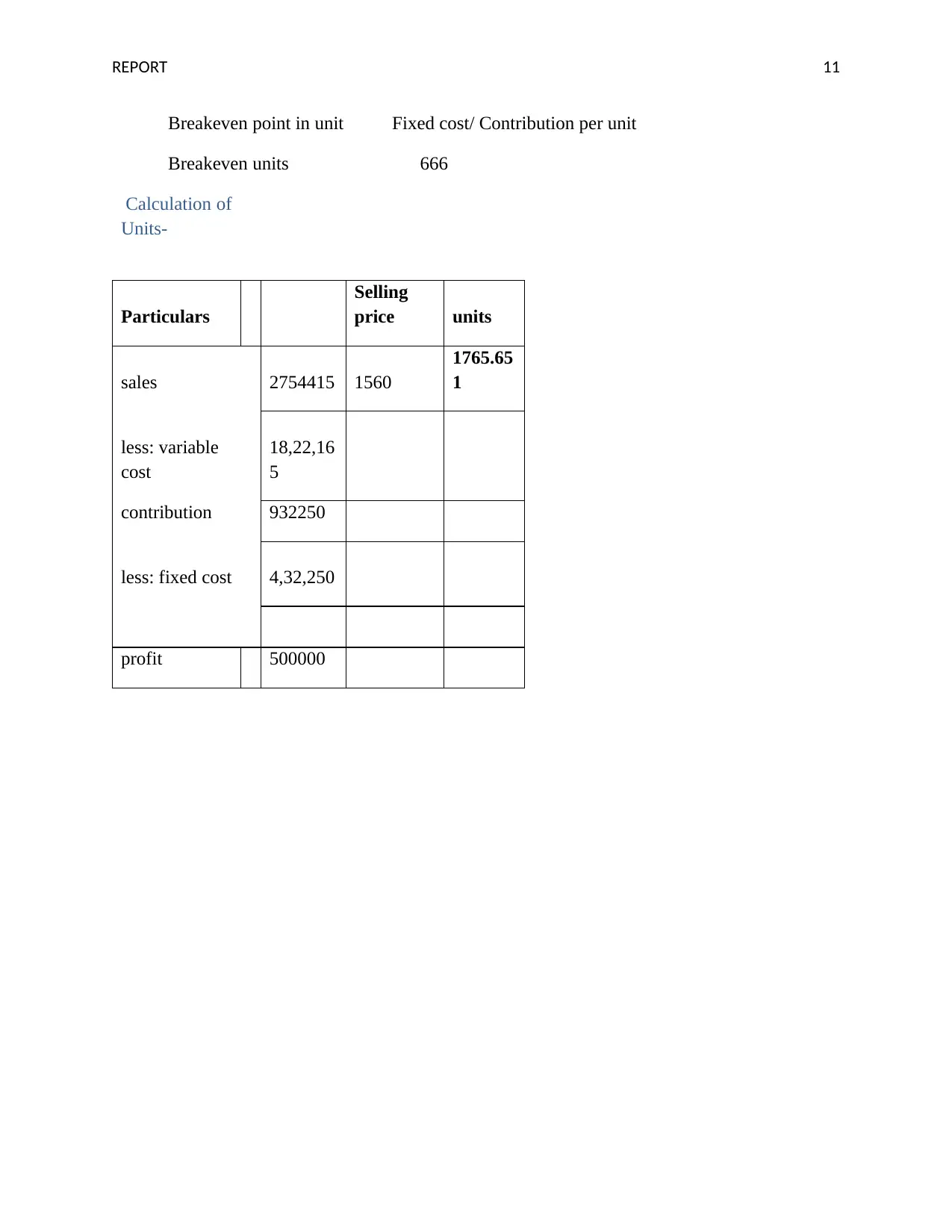

Breakeven point in unit Fixed cost/ Contribution per unit

Breakeven units 666

Calculation of

Units-

Particulars

Selling

price units

sales 2754415 1560

1765.65

1

less: variable

cost

18,22,16

5

contribution 932250

less: fixed cost 4,32,250

profit 500000

Breakeven point in unit Fixed cost/ Contribution per unit

Breakeven units 666

Calculation of

Units-

Particulars

Selling

price units

sales 2754415 1560

1765.65

1

less: variable

cost

18,22,16

5

contribution 932250

less: fixed cost 4,32,250

profit 500000

REPORT 12

References

Alexander, C. (2011). Market models: A guide to financial data analysis. USA: John Wiley &

Sons.

Bartram, S. M., Brown, G. W., & Fehle, F. R. (2019). International evidence on financial

derivatives usage. Financial management, 38(1), 185-206.

Bernstein, S., Lerner, J., Sorensen, M., & Strömberg, P. (2016). Private equity and industry

performance. Management Science, 63(4), 1198-1213.

Brammer, S., Brooks, C., & Pavelin, S. (2016). Corporate social performance and stock returns:

UK evidence from disaggregate measures. Financial management, 35(3), 97-116.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of financial management. UK: Cengage

Learning.

Caudron, C., White, R. S., Green, R. G., Woods, J., Ágústsdóttir, T., Donaldson, C.,&

Brandsdóttir, B. (2018). Seismic Amplitude Ratio Analysis of the 2014–2015 Bár

arbunga‐Holuhraun Dike Propagation and Eruption. Journal of Geophysical Research:

Solid Earth, 123(1), 264-276.

Datta, S., & Chakraborty, A. (2018). Industry Concentration and Stock Returns: Indian

Evidence. JIM QUEST, 14(1), 93.

Erasmus, S. W., Muller, M., van der Rijst, M., & Hoffman, L. C. (2016). Stable isotope ratio

analysis: A potential analytical tool for the authentication of South African lamb

meat. Food chemistry, 192, 997-1005.

Ferrer, R. C., & Ferrer, G. J. (2016). Earnings management indicators and their impact on

inventory turnover under food, beverage and tobacco sector: a thorough study using

simultaneous equations model. Academy of Accounting and Financial Studies

Journal, 20(2), 93.

Hançerlioğulları, G., Şen, A., & Aktunç, E. A. (2016). Demand uncertainty and inventory

turnover performance: An empirical analysis of the US retail industry. International

Journal of Physical Distribution & Logistics Management, 46(6/7), 681-708.

Hofstead-Duffy, A. M., Chen, D. J., Sun, S. G., & Tong, Y. J. (2012). Origin of the current peak

of negative scan in the cyclic voltammetry of methanol electro-oxidation on Pt-based

electrocatalysts: a revisit to the current ratio criterion. Journal of Materials

Chemistry, 22(11), 5205-5208.

Ihlanfeldt, K., & Mayock, T. (2016). The variance in foreclosure spillovers across neighborhood

types. Public Finance Review, 44(1), 80-108.

References

Alexander, C. (2011). Market models: A guide to financial data analysis. USA: John Wiley &

Sons.

Bartram, S. M., Brown, G. W., & Fehle, F. R. (2019). International evidence on financial

derivatives usage. Financial management, 38(1), 185-206.

Bernstein, S., Lerner, J., Sorensen, M., & Strömberg, P. (2016). Private equity and industry

performance. Management Science, 63(4), 1198-1213.

Brammer, S., Brooks, C., & Pavelin, S. (2016). Corporate social performance and stock returns:

UK evidence from disaggregate measures. Financial management, 35(3), 97-116.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of financial management. UK: Cengage

Learning.

Caudron, C., White, R. S., Green, R. G., Woods, J., Ágústsdóttir, T., Donaldson, C.,&

Brandsdóttir, B. (2018). Seismic Amplitude Ratio Analysis of the 2014–2015 Bár

arbunga‐Holuhraun Dike Propagation and Eruption. Journal of Geophysical Research:

Solid Earth, 123(1), 264-276.

Datta, S., & Chakraborty, A. (2018). Industry Concentration and Stock Returns: Indian

Evidence. JIM QUEST, 14(1), 93.

Erasmus, S. W., Muller, M., van der Rijst, M., & Hoffman, L. C. (2016). Stable isotope ratio

analysis: A potential analytical tool for the authentication of South African lamb

meat. Food chemistry, 192, 997-1005.

Ferrer, R. C., & Ferrer, G. J. (2016). Earnings management indicators and their impact on

inventory turnover under food, beverage and tobacco sector: a thorough study using

simultaneous equations model. Academy of Accounting and Financial Studies

Journal, 20(2), 93.

Hançerlioğulları, G., Şen, A., & Aktunç, E. A. (2016). Demand uncertainty and inventory

turnover performance: An empirical analysis of the US retail industry. International

Journal of Physical Distribution & Logistics Management, 46(6/7), 681-708.

Hofstead-Duffy, A. M., Chen, D. J., Sun, S. G., & Tong, Y. J. (2012). Origin of the current peak

of negative scan in the cyclic voltammetry of methanol electro-oxidation on Pt-based

electrocatalysts: a revisit to the current ratio criterion. Journal of Materials

Chemistry, 22(11), 5205-5208.

Ihlanfeldt, K., & Mayock, T. (2016). The variance in foreclosure spillovers across neighborhood

types. Public Finance Review, 44(1), 80-108.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.