American College: SITXFIN003 Project - Budget Management

VerifiedAdded on 2023/06/08

|21

|5429

|443

Project

AI Summary

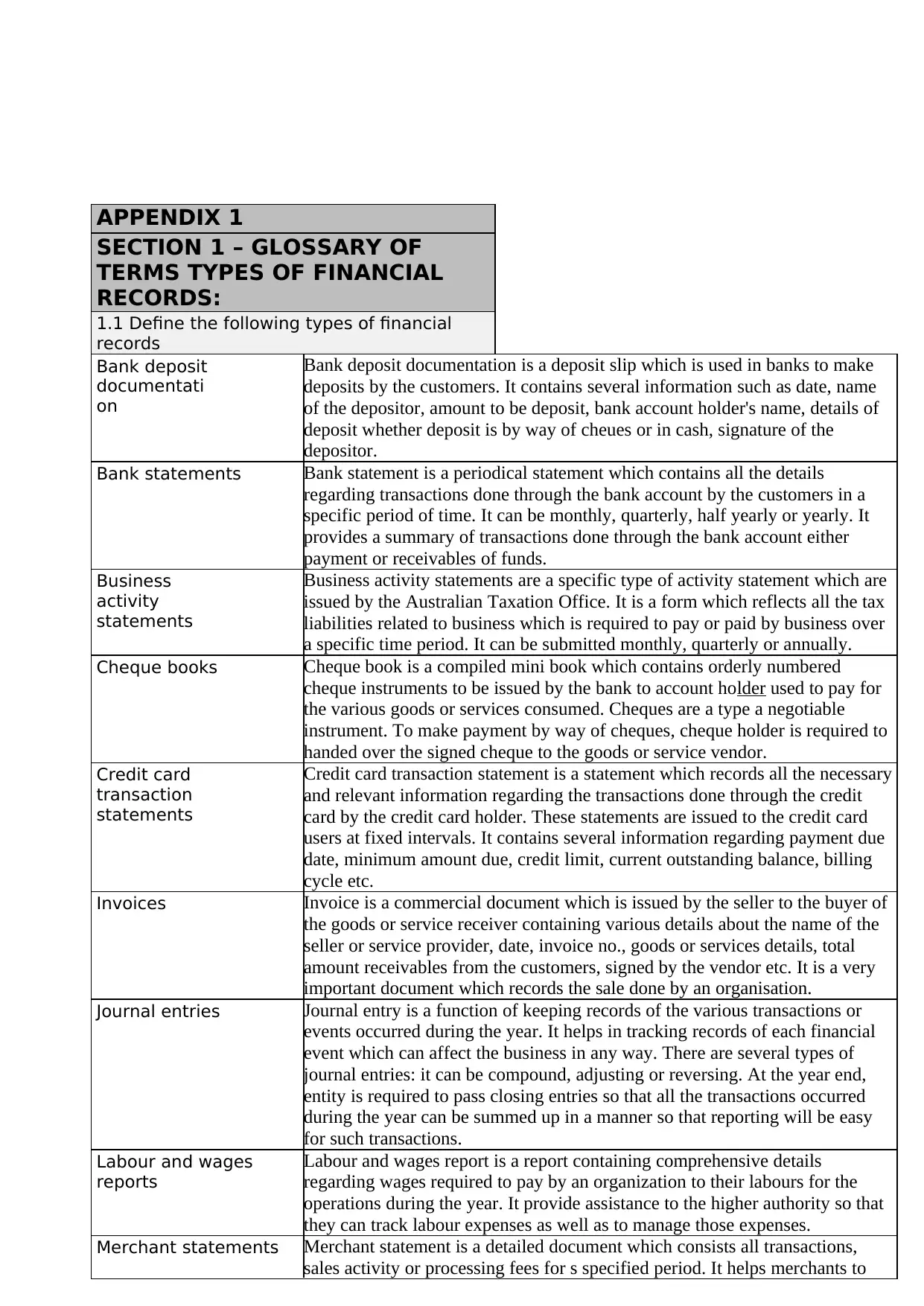

This project document, designed for the SITXFIN003 unit, focuses on the critical skills required to manage finances within a budget. The project includes a comprehensive glossary of terms, covering various types of financial records such as bank statements, invoices, and transaction reports. It also provides detailed explanations and examples in the form of FAQs regarding different types of budgets, including cash budgets, departmental budgets, and sales budgets. Furthermore, the project addresses factors for consideration in the preparation of financial and statistical reports, such as cash flow, cost-benefit analysis, and variance analysis. The student is required to demonstrate understanding of budget resource allocation, financial activity monitoring, and the identification of opportunities for improved budget performance. The project aims to equip students with the knowledge and practical skills necessary for effective budget management in the tourism, travel, hospitality, and event sectors.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.