UWTSD Financial Management: Budget Report & Forecasting for Hotels

VerifiedAdded on 2023/01/09

|9

|1937

|37

Report

AI Summary

This report presents a detailed financial analysis for a hotel, encompassing a month-by-month cash budget forecast for the St Brides Group from January to December 2020. The report includes predicted revenue, cash sales, credit sales distribution, and various expenses such as hybrid motor vehicles...

Budget Report & Budget

forecasting

forecasting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

TASK 1............................................................................................................................................1

Month by month cash budget forecast for January 2020 to December 2020 (St Brides Group) 1

TASK 2............................................................................................................................................4

(a) Defining and evaluating the process of zero-base budgeting.................................................4

(b) Assessing the advantages zero-base budgeting has over traditional based............................5

(c) How the organisation might introduce such a technique in practical terms...........................6

REFERENCES................................................................................................................................7

TASK 1............................................................................................................................................1

Month by month cash budget forecast for January 2020 to December 2020 (St Brides Group) 1

TASK 2............................................................................................................................................4

(a) Defining and evaluating the process of zero-base budgeting.................................................4

(b) Assessing the advantages zero-base budgeting has over traditional based............................5

(c) How the organisation might introduce such a technique in practical terms...........................6

REFERENCES................................................................................................................................7

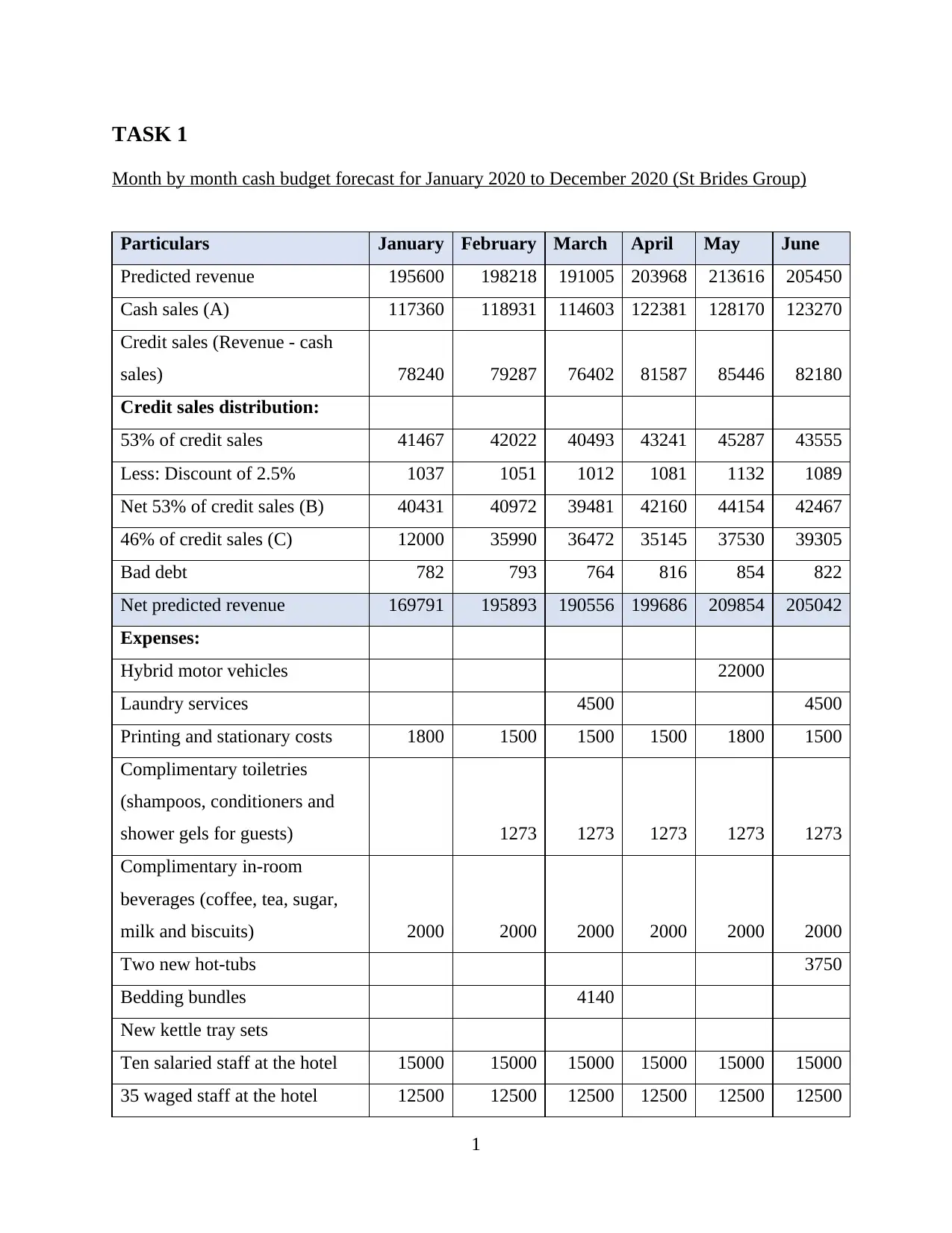

TASK 1

Month by month cash budget forecast for January 2020 to December 2020 (St Brides Group)

Particulars January February March April May June

Predicted revenue 195600 198218 191005 203968 213616 205450

Cash sales (A) 117360 118931 114603 122381 128170 123270

Credit sales (Revenue - cash

sales) 78240 79287 76402 81587 85446 82180

Credit sales distribution:

53% of credit sales 41467 42022 40493 43241 45287 43555

Less: Discount of 2.5% 1037 1051 1012 1081 1132 1089

Net 53% of credit sales (B) 40431 40972 39481 42160 44154 42467

46% of credit sales (C) 12000 35990 36472 35145 37530 39305

Bad debt 782 793 764 816 854 822

Net predicted revenue 169791 195893 190556 199686 209854 205042

Expenses:

Hybrid motor vehicles 22000

Laundry services 4500 4500

Printing and stationary costs 1800 1500 1500 1500 1800 1500

Complimentary toiletries

(shampoos, conditioners and

shower gels for guests) 1273 1273 1273 1273 1273

Complimentary in-room

beverages (coffee, tea, sugar,

milk and biscuits) 2000 2000 2000 2000 2000 2000

Two new hot-tubs 3750

Bedding bundles 4140

New kettle tray sets

Ten salaried staff at the hotel 15000 15000 15000 15000 15000 15000

35 waged staff at the hotel 12500 12500 12500 12500 12500 12500

1

Month by month cash budget forecast for January 2020 to December 2020 (St Brides Group)

Particulars January February March April May June

Predicted revenue 195600 198218 191005 203968 213616 205450

Cash sales (A) 117360 118931 114603 122381 128170 123270

Credit sales (Revenue - cash

sales) 78240 79287 76402 81587 85446 82180

Credit sales distribution:

53% of credit sales 41467 42022 40493 43241 45287 43555

Less: Discount of 2.5% 1037 1051 1012 1081 1132 1089

Net 53% of credit sales (B) 40431 40972 39481 42160 44154 42467

46% of credit sales (C) 12000 35990 36472 35145 37530 39305

Bad debt 782 793 764 816 854 822

Net predicted revenue 169791 195893 190556 199686 209854 205042

Expenses:

Hybrid motor vehicles 22000

Laundry services 4500 4500

Printing and stationary costs 1800 1500 1500 1500 1800 1500

Complimentary toiletries

(shampoos, conditioners and

shower gels for guests) 1273 1273 1273 1273 1273

Complimentary in-room

beverages (coffee, tea, sugar,

milk and biscuits) 2000 2000 2000 2000 2000 2000

Two new hot-tubs 3750

Bedding bundles 4140

New kettle tray sets

Ten salaried staff at the hotel 15000 15000 15000 15000 15000 15000

35 waged staff at the hotel 12500 12500 12500 12500 12500 12500

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

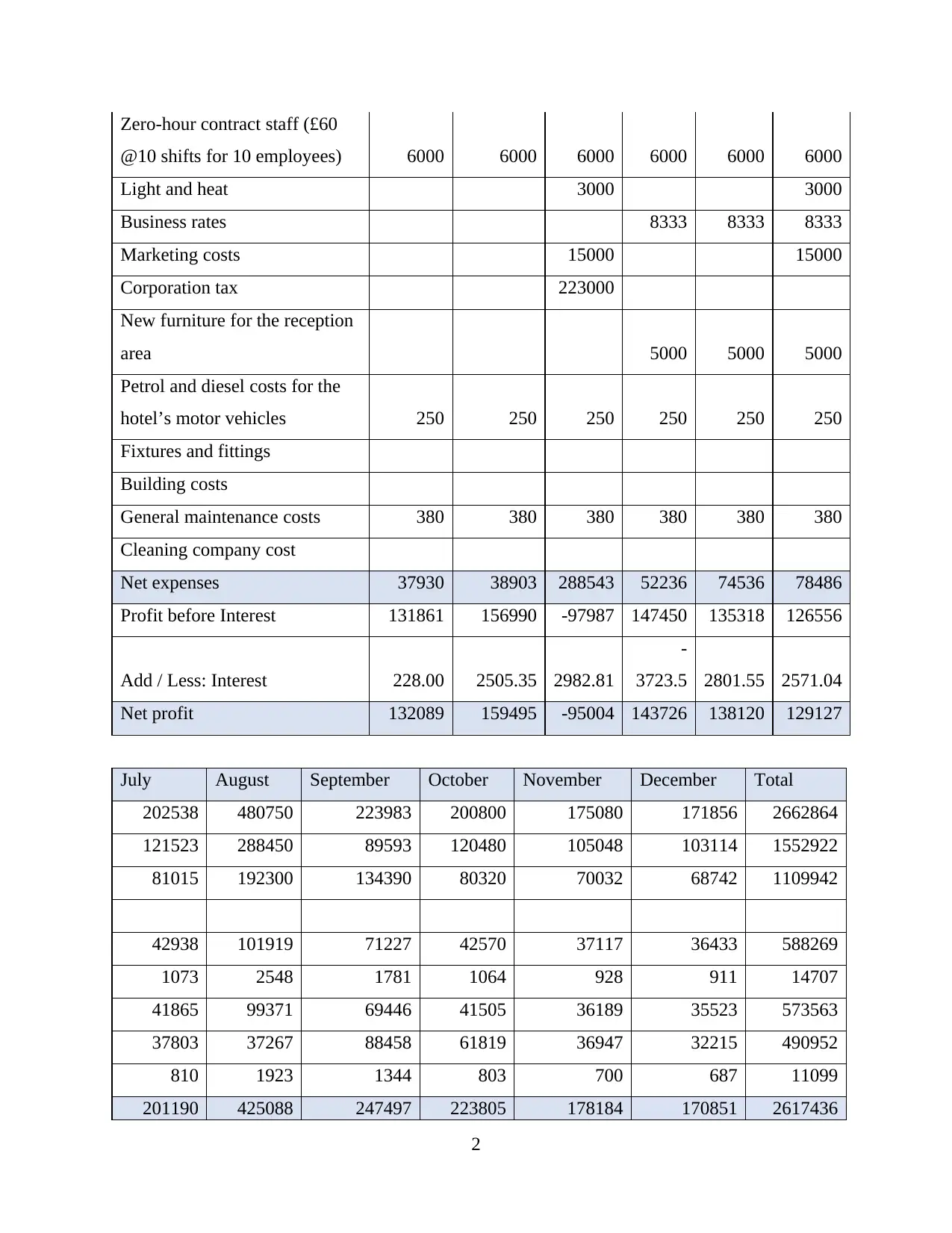

Zero-hour contract staff (£60

@10 shifts for 10 employees) 6000 6000 6000 6000 6000 6000

Light and heat 3000 3000

Business rates 8333 8333 8333

Marketing costs 15000 15000

Corporation tax 223000

New furniture for the reception

area 5000 5000 5000

Petrol and diesel costs for the

hotel’s motor vehicles 250 250 250 250 250 250

Fixtures and fittings

Building costs

General maintenance costs 380 380 380 380 380 380

Cleaning company cost

Net expenses 37930 38903 288543 52236 74536 78486

Profit before Interest 131861 156990 -97987 147450 135318 126556

Add / Less: Interest 228.00 2505.35 2982.81

-

3723.5 2801.55 2571.04

Net profit 132089 159495 -95004 143726 138120 129127

July August September October November December Total

202538 480750 223983 200800 175080 171856 2662864

121523 288450 89593 120480 105048 103114 1552922

81015 192300 134390 80320 70032 68742 1109942

42938 101919 71227 42570 37117 36433 588269

1073 2548 1781 1064 928 911 14707

41865 99371 69446 41505 36189 35523 573563

37803 37267 88458 61819 36947 32215 490952

810 1923 1344 803 700 687 11099

201190 425088 247497 223805 178184 170851 2617436

2

@10 shifts for 10 employees) 6000 6000 6000 6000 6000 6000

Light and heat 3000 3000

Business rates 8333 8333 8333

Marketing costs 15000 15000

Corporation tax 223000

New furniture for the reception

area 5000 5000 5000

Petrol and diesel costs for the

hotel’s motor vehicles 250 250 250 250 250 250

Fixtures and fittings

Building costs

General maintenance costs 380 380 380 380 380 380

Cleaning company cost

Net expenses 37930 38903 288543 52236 74536 78486

Profit before Interest 131861 156990 -97987 147450 135318 126556

Add / Less: Interest 228.00 2505.35 2982.81

-

3723.5 2801.55 2571.04

Net profit 132089 159495 -95004 143726 138120 129127

July August September October November December Total

202538 480750 223983 200800 175080 171856 2662864

121523 288450 89593 120480 105048 103114 1552922

81015 192300 134390 80320 70032 68742 1109942

42938 101919 71227 42570 37117 36433 588269

1073 2548 1781 1064 928 911 14707

41865 99371 69446 41505 36189 35523 573563

37803 37267 88458 61819 36947 32215 490952

810 1923 1344 803 700 687 11099

201190 425088 247497 223805 178184 170851 2617436

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

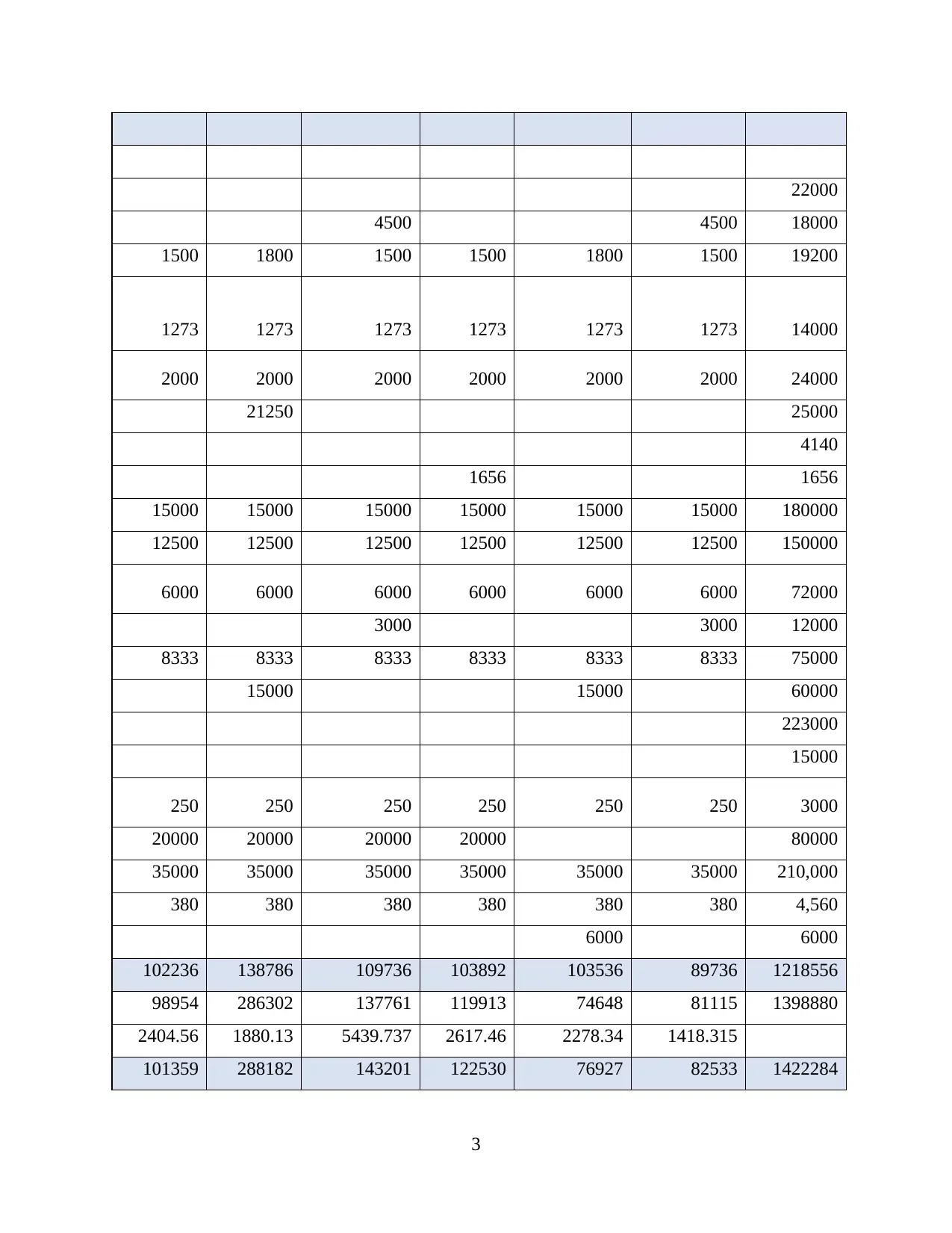

22000

4500 4500 18000

1500 1800 1500 1500 1800 1500 19200

1273 1273 1273 1273 1273 1273 14000

2000 2000 2000 2000 2000 2000 24000

21250 25000

4140

1656 1656

15000 15000 15000 15000 15000 15000 180000

12500 12500 12500 12500 12500 12500 150000

6000 6000 6000 6000 6000 6000 72000

3000 3000 12000

8333 8333 8333 8333 8333 8333 75000

15000 15000 60000

223000

15000

250 250 250 250 250 250 3000

20000 20000 20000 20000 80000

35000 35000 35000 35000 35000 35000 210,000

380 380 380 380 380 380 4,560

6000 6000

102236 138786 109736 103892 103536 89736 1218556

98954 286302 137761 119913 74648 81115 1398880

2404.56 1880.13 5439.737 2617.46 2278.34 1418.315

101359 288182 143201 122530 76927 82533 1422284

3

4500 4500 18000

1500 1800 1500 1500 1800 1500 19200

1273 1273 1273 1273 1273 1273 14000

2000 2000 2000 2000 2000 2000 24000

21250 25000

4140

1656 1656

15000 15000 15000 15000 15000 15000 180000

12500 12500 12500 12500 12500 12500 150000

6000 6000 6000 6000 6000 6000 72000

3000 3000 12000

8333 8333 8333 8333 8333 8333 75000

15000 15000 60000

223000

15000

250 250 250 250 250 250 3000

20000 20000 20000 20000 80000

35000 35000 35000 35000 35000 35000 210,000

380 380 380 380 380 380 4,560

6000 6000

102236 138786 109736 103892 103536 89736 1218556

98954 286302 137761 119913 74648 81115 1398880

2404.56 1880.13 5439.737 2617.46 2278.34 1418.315

101359 288182 143201 122530 76927 82533 1422284

3

**Assumptions

There was no information given about the occupancy of St Brides Group hotel’s room

due to which it has been assumed that there is average occupancy of more than 80% in

every month. In the month of September occupancy is 100% due to Sports venue.

It has been also assumed that the suppliers which are paid two months after receipt of

goods are Hotel’s usual supplier of Branded 46 bedding bundles to be purchased in

January and 46 new kettle tray sets purchased in August.

As the average occupancy of hotel is 80%, the complimentary in-room beverages are

costed to £2,000. In addition to this, due to average occupancy of 80% in every month,

the zero-hour contract staff is also employed every month.

The opening cash balance at 1st January 2020 is £12,000. This cash balance is considered

as 46% of credit sales for January month and Profit before Interest for month of

December which is used to calculate Interest amount of January.

TASK 2

(a) Defining and evaluating the process of zero-base budgeting

Zero base budgeting is an approach of developing a new budget from scratch in every

financial period. As the name of this budgeting technique suggests, a zero base budget starts with

a zero which makes it different from traditional budgets that use to make budgets based on

previous budgets (Zero-Based Budgeting, 2015). In this budget, it is important to justify all the

expenses despite of the fact they occur in every financial period. The primary goal of such

budget is to make sure that all unnecessary costs are cut wherever possible and expenses must

not be incurred only because they are incurred in every budgeting cycle.

Zero based budgeting is not only an approach but also a process which helps in developing

a budget from scratch. The steps which are involved in such a budget / process are analysed

below:

Identifying decision units – The first step in this process of zero base budgeting is to

identify all the viable areas for which decisions are required to be made. A budget is a document

which is developed by predicting expenses and revenue streams at the beginning of a new

financial period. In order to develop an effective budget, the first step is to identify areas that

require to make decisions. For example: An accountant has identified purchase of new vehicle

4

There was no information given about the occupancy of St Brides Group hotel’s room

due to which it has been assumed that there is average occupancy of more than 80% in

every month. In the month of September occupancy is 100% due to Sports venue.

It has been also assumed that the suppliers which are paid two months after receipt of

goods are Hotel’s usual supplier of Branded 46 bedding bundles to be purchased in

January and 46 new kettle tray sets purchased in August.

As the average occupancy of hotel is 80%, the complimentary in-room beverages are

costed to £2,000. In addition to this, due to average occupancy of 80% in every month,

the zero-hour contract staff is also employed every month.

The opening cash balance at 1st January 2020 is £12,000. This cash balance is considered

as 46% of credit sales for January month and Profit before Interest for month of

December which is used to calculate Interest amount of January.

TASK 2

(a) Defining and evaluating the process of zero-base budgeting

Zero base budgeting is an approach of developing a new budget from scratch in every

financial period. As the name of this budgeting technique suggests, a zero base budget starts with

a zero which makes it different from traditional budgets that use to make budgets based on

previous budgets (Zero-Based Budgeting, 2015). In this budget, it is important to justify all the

expenses despite of the fact they occur in every financial period. The primary goal of such

budget is to make sure that all unnecessary costs are cut wherever possible and expenses must

not be incurred only because they are incurred in every budgeting cycle.

Zero based budgeting is not only an approach but also a process which helps in developing

a budget from scratch. The steps which are involved in such a budget / process are analysed

below:

Identifying decision units – The first step in this process of zero base budgeting is to

identify all the viable areas for which decisions are required to be made. A budget is a document

which is developed by predicting expenses and revenue streams at the beginning of a new

financial period. In order to develop an effective budget, the first step is to identify areas that

require to make decisions. For example: An accountant has identified purchase of new vehicle

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision unit, petty and miscellaneous decision unit, acquisition of new tools decision unit and

more

Creating decision packages – After all the decision units and areas are identified, it is

important to divide all the decisions units into few decision packages according to the nature and

aim of each decision package. Every decision package is developed to make sure that every

decision unit is considered and if held viable, these units will be allotted few funds and

resources. For example, the purchase of new vehicle and tools decision unit are united in a

decision package of purchasing new assets for organisation.

Prioritising decision packages – After developing different decision packages, it is now

important at this stage, to prioritise every decision package. The most effective technique of

prioritising decision packages is to provide ranking to each package and then according to the

available resources, select few top ranked decision packages. For example: Accountant has

ranked purchase of raw material as 1, petty and miscellaneous expenses package as rank 2 and

purchase of new assets as rank 2.

Allocating available funds – In this stage of all the prioritised decision packages are

allotted a suitable monetary fund and in last if some funds are left over then they are allotted to

next prioritised decision package. For example, there are limited monetary resources, due to

which organisation has allotted them to rank 1 and 2 decision packages only (Zero-based

budgeting process, 2017).

Monitoring and control – At this last stage, performance of each decision package is

monitored and controlled in order to identify any deviations. The output from each decision

package is measured to ascertain the overall performance of the organisation.

All the above stages are the steps of developing a zero based budget that can help an

organisation in developing a budget from scratch.

(b) Assessing the advantages zero-base budgeting has over traditional based

A zero based budget is a budgetary document which is prepared using modern approaches

due to which it is different from traditional budgets and systems. There are various advantages of

Zero based budget over traditional budgets which are analysed below:

A traditional budget works on cost accounting principle which makes it an accountancy

oriented budget, but on the other hand ZBB is based on decision making due to which an

organisation can take effective decision regarding allocating funds to appropriate units.

5

more

Creating decision packages – After all the decision units and areas are identified, it is

important to divide all the decisions units into few decision packages according to the nature and

aim of each decision package. Every decision package is developed to make sure that every

decision unit is considered and if held viable, these units will be allotted few funds and

resources. For example, the purchase of new vehicle and tools decision unit are united in a

decision package of purchasing new assets for organisation.

Prioritising decision packages – After developing different decision packages, it is now

important at this stage, to prioritise every decision package. The most effective technique of

prioritising decision packages is to provide ranking to each package and then according to the

available resources, select few top ranked decision packages. For example: Accountant has

ranked purchase of raw material as 1, petty and miscellaneous expenses package as rank 2 and

purchase of new assets as rank 2.

Allocating available funds – In this stage of all the prioritised decision packages are

allotted a suitable monetary fund and in last if some funds are left over then they are allotted to

next prioritised decision package. For example, there are limited monetary resources, due to

which organisation has allotted them to rank 1 and 2 decision packages only (Zero-based

budgeting process, 2017).

Monitoring and control – At this last stage, performance of each decision package is

monitored and controlled in order to identify any deviations. The output from each decision

package is measured to ascertain the overall performance of the organisation.

All the above stages are the steps of developing a zero based budget that can help an

organisation in developing a budget from scratch.

(b) Assessing the advantages zero-base budgeting has over traditional based

A zero based budget is a budgetary document which is prepared using modern approaches

due to which it is different from traditional budgets and systems. There are various advantages of

Zero based budget over traditional budgets which are analysed below:

A traditional budget works on cost accounting principle which makes it an accountancy

oriented budget, but on the other hand ZBB is based on decision making due to which an

organisation can take effective decision regarding allocating funds to appropriate units.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to the traditional budgeting, every departmental unit is provided with a

suitable budget that is allotted to these units every year. Such budget encourages

departments to spent even if the spending is not necessary. When a fund is allotted to

each department they spend it as if they don’t, they will lose their funds. This deviation in

this approach is bridged under zero based budgeting as a ZBB do not allocate same funds

every year as these budgets are developed from scratch every year and are not related

with last year (Traditional Budgeting Vs. Zero Base Budgeting, 2020).

Another advantage of ZBB over traditional budgeting is accuracy. In the method of ZBB,

budgets are developed from a zero level every year due to which if there are any arbitrary

changes are included from last year, they are eliminated in current year’s budget which

reduces overall expenditure of the organisation.

(c) How the organisation might introduce such a technique in practical terms

There are various benefits of zero based budgeting but developing such a budget is a

complex task due to which organisations avoid to adopt approach of zero based budgeting. There

are various ways by which an organisation can introduce ZBB in practical terms:

An organisation can hire a professional so that the complex task of developing a ZBB can be

done.

Another way of introducing ZBB is to identify each and every decision unit in the

organisation which requires funds. Under this way, all decisions units will be identified and

organisation will know that to a what extend they require monetary resources.

An organisation can introduce ZBB by making clear objectives for their operations and

future revenues so that the budget will consider those aims and according will prioritize each

decision unit or a decision package.

Developing a budget is a task for accountants but developing a zero based budget requires

strategic decisions due to which managers of an organisation can first set out their business

strategies which will provide a base to develop zero based budget (Ways to use Zero-based

budgeting, 2020).

6

suitable budget that is allotted to these units every year. Such budget encourages

departments to spent even if the spending is not necessary. When a fund is allotted to

each department they spend it as if they don’t, they will lose their funds. This deviation in

this approach is bridged under zero based budgeting as a ZBB do not allocate same funds

every year as these budgets are developed from scratch every year and are not related

with last year (Traditional Budgeting Vs. Zero Base Budgeting, 2020).

Another advantage of ZBB over traditional budgeting is accuracy. In the method of ZBB,

budgets are developed from a zero level every year due to which if there are any arbitrary

changes are included from last year, they are eliminated in current year’s budget which

reduces overall expenditure of the organisation.

(c) How the organisation might introduce such a technique in practical terms

There are various benefits of zero based budgeting but developing such a budget is a

complex task due to which organisations avoid to adopt approach of zero based budgeting. There

are various ways by which an organisation can introduce ZBB in practical terms:

An organisation can hire a professional so that the complex task of developing a ZBB can be

done.

Another way of introducing ZBB is to identify each and every decision unit in the

organisation which requires funds. Under this way, all decisions units will be identified and

organisation will know that to a what extend they require monetary resources.

An organisation can introduce ZBB by making clear objectives for their operations and

future revenues so that the budget will consider those aims and according will prioritize each

decision unit or a decision package.

Developing a budget is a task for accountants but developing a zero based budget requires

strategic decisions due to which managers of an organisation can first set out their business

strategies which will provide a base to develop zero based budget (Ways to use Zero-based

budgeting, 2020).

6

REFERENCES

Online

Zero-Based Budgeting. 2015. [Online]. Available through:

<https://www2.deloitte.com/content/dam/Deloitte/us/Documents/process-and-

operations/us-cons-zero-based-budgeting.pdf >

Zero-based budgeting process. 2017. [Online]. Available through:

<https://www.patriotsoftware.com/blog/accounting/what-is-zero-based-budgeting-

example-process/>

Traditional Budgeting Vs. Zero Base Budgeting. 2020. [Online]. Available through:

<https://cleartax.in/s/zero-based-budgeting>

Ways to use Zero-based budgeting. 2020. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/zero-based-

budgeting/>

7

Online

Zero-Based Budgeting. 2015. [Online]. Available through:

<https://www2.deloitte.com/content/dam/Deloitte/us/Documents/process-and-

operations/us-cons-zero-based-budgeting.pdf >

Zero-based budgeting process. 2017. [Online]. Available through:

<https://www.patriotsoftware.com/blog/accounting/what-is-zero-based-budgeting-

example-process/>

Traditional Budgeting Vs. Zero Base Budgeting. 2020. [Online]. Available through:

<https://cleartax.in/s/zero-based-budgeting>

Ways to use Zero-based budgeting. 2020. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/zero-based-

budgeting/>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.