Comprehensive Budget Report and Financial Analysis for Gaia Ltd.

VerifiedAdded on 2023/06/05

|13

|2331

|331

Report

AI Summary

This report provides a comprehensive financial analysis of Gaia Ltd.'s budget. Part A focuses on the cash budget, examining cash inflows, outflows, and the resulting cash position. It includes an evaluation of financing sources like equity shares, debentures, and term loans. Part B delves into ratio calculations, comparing the company's performance over two years using liquidity, profitability, and working capital ratios, along with a discussion of the key performance indicators. Part C presents a flexible sales budget, exploring the impact of different sales volumes on profitability and identifying potential issues such as the effects of economies of scale on variable costs. The analysis highlights the importance of effective financial management and strategic decision-making for the company's success.

Budget report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART A.......................................................................................................................................................................................................3

Cash Budget.............................................................................................................................................................................................3

Examining the Cash Budget....................................................................................................................................................................4

Evaluation of Sources of Finance............................................................................................................................................................4

PART B.......................................................................................................................................................................................................5

Ratio Calculation.....................................................................................................................................................................................5

Comparing Performance of Both the Years.............................................................................................................................................9

Part C.........................................................................................................................................................................................................10

Flexible Sales Budget............................................................................................................................................................................10

Identification & Discussion of Issues....................................................................................................................................................11

REFERENCES............................................................................................................................................................................................1

PART A.......................................................................................................................................................................................................3

Cash Budget.............................................................................................................................................................................................3

Examining the Cash Budget....................................................................................................................................................................4

Evaluation of Sources of Finance............................................................................................................................................................4

PART B.......................................................................................................................................................................................................5

Ratio Calculation.....................................................................................................................................................................................5

Comparing Performance of Both the Years.............................................................................................................................................9

Part C.........................................................................................................................................................................................................10

Flexible Sales Budget............................................................................................................................................................................10

Identification & Discussion of Issues....................................................................................................................................................11

REFERENCES............................................................................................................................................................................................1

PART A

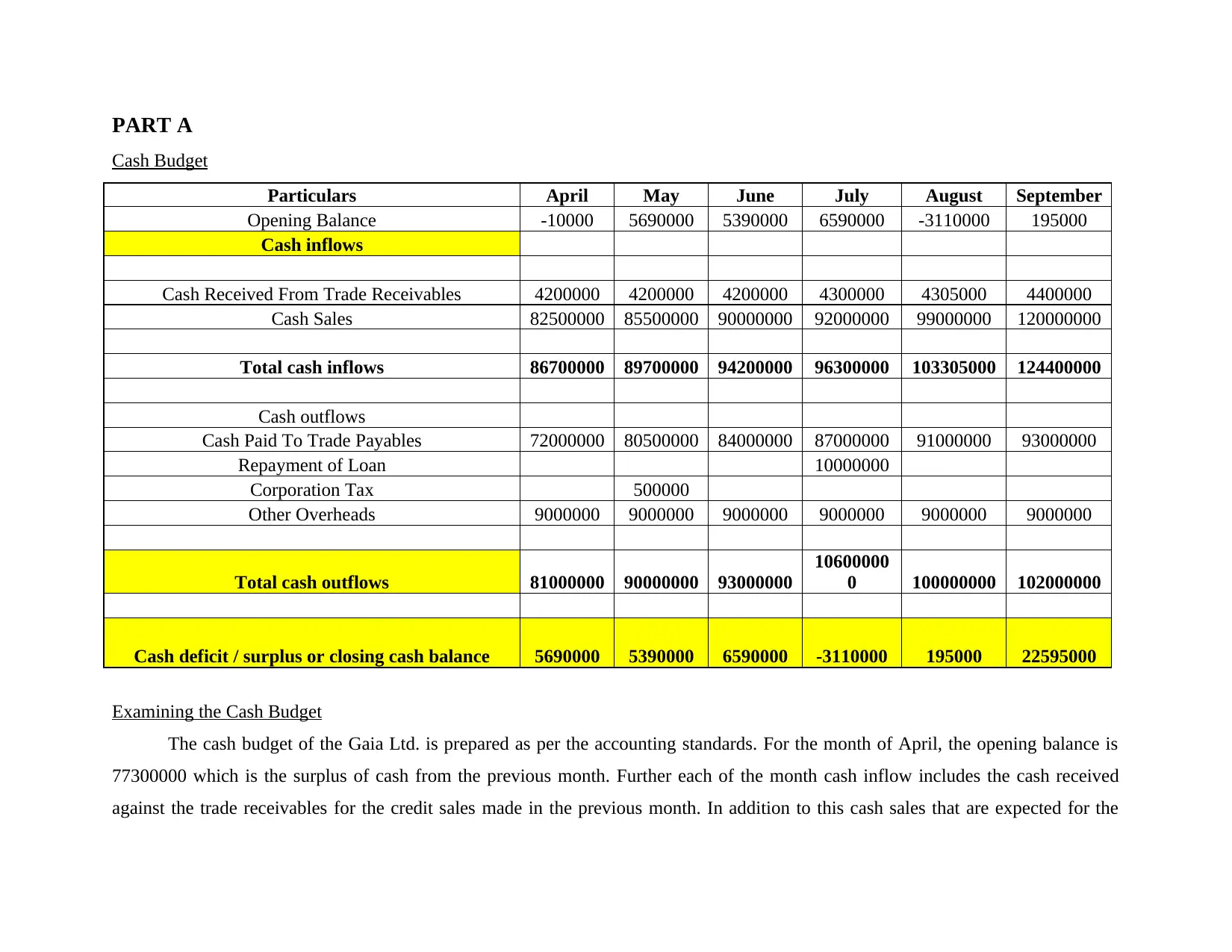

Cash Budget

Particulars April May June July August September

Opening Balance -10000 5690000 5390000 6590000 -3110000 195000

Cash inflows

Cash Received From Trade Receivables 4200000 4200000 4200000 4300000 4305000 4400000

Cash Sales 82500000 85500000 90000000 92000000 99000000 120000000

Total cash inflows 86700000 89700000 94200000 96300000 103305000 124400000

Cash outflows

Cash Paid To Trade Payables 72000000 80500000 84000000 87000000 91000000 93000000

Repayment of Loan 10000000

Corporation Tax 500000

Other Overheads 9000000 9000000 9000000 9000000 9000000 9000000

Total cash outflows 81000000 90000000 93000000

10600000

0 100000000 102000000

Cash deficit / surplus or closing cash balance 5690000 5390000 6590000 -3110000 195000 22595000

Examining the Cash Budget

The cash budget of the Gaia Ltd. is prepared as per the accounting standards. For the month of April, the opening balance is

77300000 which is the surplus of cash from the previous month. Further each of the month cash inflow includes the cash received

against the trade receivables for the credit sales made in the previous month. In addition to this cash sales that are expected for the

Cash Budget

Particulars April May June July August September

Opening Balance -10000 5690000 5390000 6590000 -3110000 195000

Cash inflows

Cash Received From Trade Receivables 4200000 4200000 4200000 4300000 4305000 4400000

Cash Sales 82500000 85500000 90000000 92000000 99000000 120000000

Total cash inflows 86700000 89700000 94200000 96300000 103305000 124400000

Cash outflows

Cash Paid To Trade Payables 72000000 80500000 84000000 87000000 91000000 93000000

Repayment of Loan 10000000

Corporation Tax 500000

Other Overheads 9000000 9000000 9000000 9000000 9000000 9000000

Total cash outflows 81000000 90000000 93000000

10600000

0 100000000 102000000

Cash deficit / surplus or closing cash balance 5690000 5390000 6590000 -3110000 195000 22595000

Examining the Cash Budget

The cash budget of the Gaia Ltd. is prepared as per the accounting standards. For the month of April, the opening balance is

77300000 which is the surplus of cash from the previous month. Further each of the month cash inflow includes the cash received

against the trade receivables for the credit sales made in the previous month. In addition to this cash sales that are expected for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

month are also included to the cash inflows (Kurniawati, 2022). Further for the month of April, the firm expects to have a bank

overdraft of 10,000 pounds. The cash outflowing activities for the Gaia Ltd are expected to be making of payments to the creditors of

the firm from whom it purchases materials on credit. Such payments are made after a month, so any of the particular month contains

payments for the credit purchases that are done in the month previous to it. The month of July includes a repayment of loan of

10,000,000 pounds. Further, there is a payment of 500000 pounds against the head corporation tax, other overheads accounts to be

9,000,000 pounds every month. The firm is having enough positive cash flow for each of the months, it should make effective use of

such funds to earn more income.

Evaluation of Sources of Finance

Issue of Shares – Issuing of equity shares is known to be the main source for a firm to arrange the amount of funds that are

required by itself. Such shares are issued to the general public. Equity shareholders do not get any kind of preferential rights in

terms of repayment and receiving of dividend. The company have to give the equity shareholder their share from the

company’s residual income. There are various advantages that Gaia Ltd. can enjoy by using this source to raise funds. To

begin with the company will get funds that are of permanent in nature and hence it will not have any kind of liability in terms

of repayment. Furthermore, it will not create any obligation of the business enterprise in terms of paying the dividends. Lastly

the credit worthiness of the company will enhance. The limitations include cost of equity is the highest as compared with all

the sources of funds that are available to a company (Wadesango and et.al., 2019). The dividends that are paid to equity

shareholder are not tax deductible, and also the floatation expenses are high.

Debentures – The literal meaning of debentures is to take loan or borrow. Issuing of debentures by the company is like issuing

of unsecured loans. The company will have to pay the debentures holders fixed interest payments and repay the principal

amount in the event of repayment. The advantage is that this source is more effective than the issue of shares option. The

company will retain its ownership rights among its existing owner. Interest payments are tax deductible so it will be

overdraft of 10,000 pounds. The cash outflowing activities for the Gaia Ltd are expected to be making of payments to the creditors of

the firm from whom it purchases materials on credit. Such payments are made after a month, so any of the particular month contains

payments for the credit purchases that are done in the month previous to it. The month of July includes a repayment of loan of

10,000,000 pounds. Further, there is a payment of 500000 pounds against the head corporation tax, other overheads accounts to be

9,000,000 pounds every month. The firm is having enough positive cash flow for each of the months, it should make effective use of

such funds to earn more income.

Evaluation of Sources of Finance

Issue of Shares – Issuing of equity shares is known to be the main source for a firm to arrange the amount of funds that are

required by itself. Such shares are issued to the general public. Equity shareholders do not get any kind of preferential rights in

terms of repayment and receiving of dividend. The company have to give the equity shareholder their share from the

company’s residual income. There are various advantages that Gaia Ltd. can enjoy by using this source to raise funds. To

begin with the company will get funds that are of permanent in nature and hence it will not have any kind of liability in terms

of repayment. Furthermore, it will not create any obligation of the business enterprise in terms of paying the dividends. Lastly

the credit worthiness of the company will enhance. The limitations include cost of equity is the highest as compared with all

the sources of funds that are available to a company (Wadesango and et.al., 2019). The dividends that are paid to equity

shareholder are not tax deductible, and also the floatation expenses are high.

Debentures – The literal meaning of debentures is to take loan or borrow. Issuing of debentures by the company is like issuing

of unsecured loans. The company will have to pay the debentures holders fixed interest payments and repay the principal

amount in the event of repayment. The advantage is that this source is more effective than the issue of shares option. The

company will retain its ownership rights among its existing owner. Interest payments are tax deductible so it will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

advantageous for Gaia Ltd. The limitations are that the interest & principal payments become a burden for the company in the

years of low or no profits. There is huge amount of cash outflow during the repayments are made to the debentures’ holders.

Term Loans

PART B

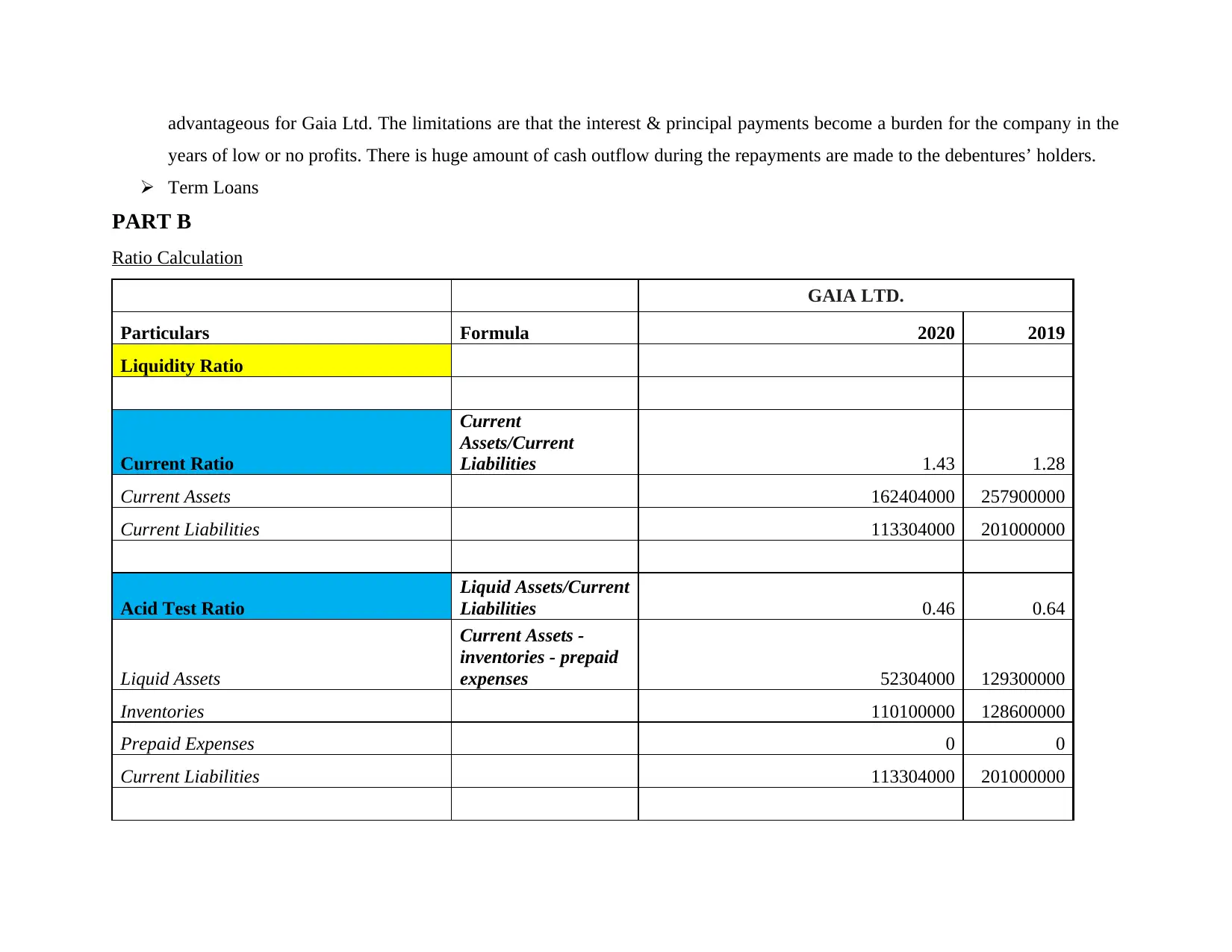

Ratio Calculation

GAIA LTD.

Particulars Formula 2020 2019

Liquidity Ratio

Current Ratio

Current

Assets/Current

Liabilities 1.43 1.28

Current Assets 162404000 257900000

Current Liabilities 113304000 201000000

Acid Test Ratio

Liquid Assets/Current

Liabilities 0.46 0.64

Liquid Assets

Current Assets -

inventories - prepaid

expenses 52304000 129300000

Inventories 110100000 128600000

Prepaid Expenses 0 0

Current Liabilities 113304000 201000000

years of low or no profits. There is huge amount of cash outflow during the repayments are made to the debentures’ holders.

Term Loans

PART B

Ratio Calculation

GAIA LTD.

Particulars Formula 2020 2019

Liquidity Ratio

Current Ratio

Current

Assets/Current

Liabilities 1.43 1.28

Current Assets 162404000 257900000

Current Liabilities 113304000 201000000

Acid Test Ratio

Liquid Assets/Current

Liabilities 0.46 0.64

Liquid Assets

Current Assets -

inventories - prepaid

expenses 52304000 129300000

Inventories 110100000 128600000

Prepaid Expenses 0 0

Current Liabilities 113304000 201000000

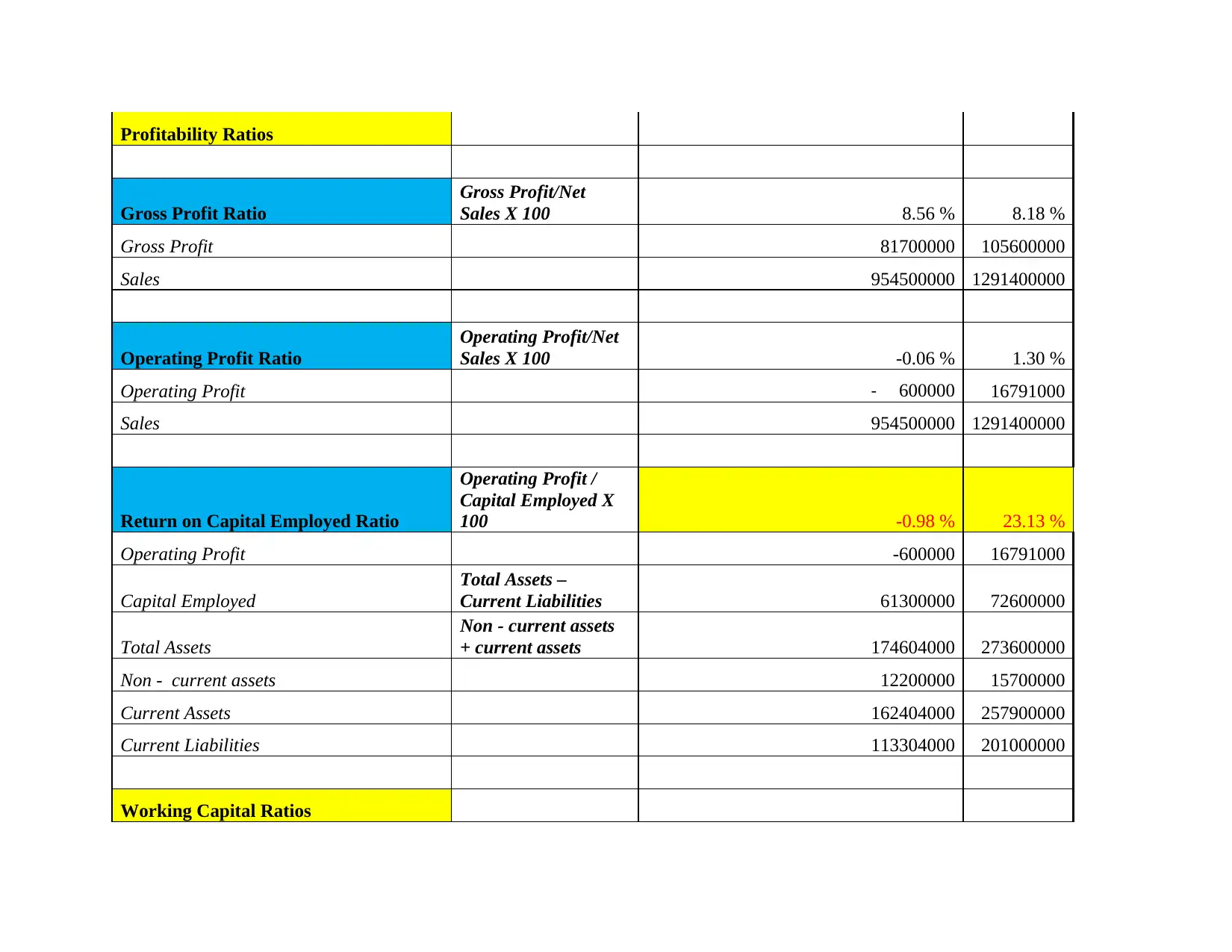

Profitability Ratios

Gross Profit Ratio

Gross Profit/Net

Sales X 100 8.56 % 8.18 %

Gross Profit 81700000 105600000

Sales 954500000 1291400000

Operating Profit Ratio

Operating Profit/Net

Sales X 100 -0.06 % 1.30 %

Operating Profit - 600000 16791000

Sales 954500000 1291400000

Return on Capital Employed Ratio

Operating Profit /

Capital Employed X

100 -0.98 % 23.13 %

Operating Profit -600000 16791000

Capital Employed

Total Assets –

Current Liabilities 61300000 72600000

Total Assets

Non - current assets

+ current assets 174604000 273600000

Non - current assets 12200000 15700000

Current Assets 162404000 257900000

Current Liabilities 113304000 201000000

Working Capital Ratios

Gross Profit Ratio

Gross Profit/Net

Sales X 100 8.56 % 8.18 %

Gross Profit 81700000 105600000

Sales 954500000 1291400000

Operating Profit Ratio

Operating Profit/Net

Sales X 100 -0.06 % 1.30 %

Operating Profit - 600000 16791000

Sales 954500000 1291400000

Return on Capital Employed Ratio

Operating Profit /

Capital Employed X

100 -0.98 % 23.13 %

Operating Profit -600000 16791000

Capital Employed

Total Assets –

Current Liabilities 61300000 72600000

Total Assets

Non - current assets

+ current assets 174604000 273600000

Non - current assets 12200000 15700000

Current Assets 162404000 257900000

Current Liabilities 113304000 201000000

Working Capital Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

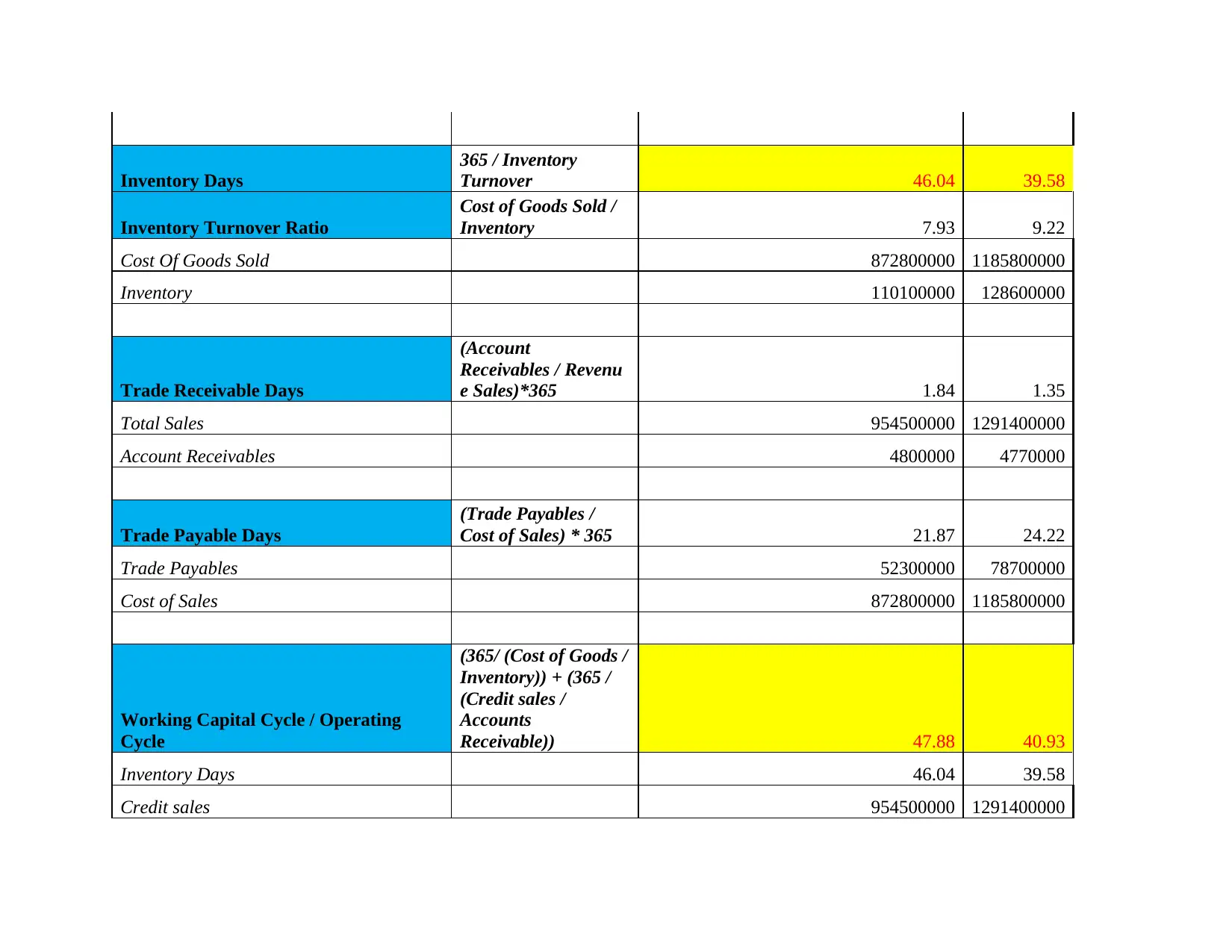

Inventory Days

365 / Inventory

Turnover 46.04 39.58

Inventory Turnover Ratio

Cost of Goods Sold /

Inventory 7.93 9.22

Cost Of Goods Sold 872800000 1185800000

Inventory 110100000 128600000

Trade Receivable Days

(Account

Receivables / Revenu

e Sales)*365 1.84 1.35

Total Sales 954500000 1291400000

Account Receivables 4800000 4770000

Trade Payable Days

(Trade Payables /

Cost of Sales) * 365 21.87 24.22

Trade Payables 52300000 78700000

Cost of Sales 872800000 1185800000

Working Capital Cycle / Operating

Cycle

(365/ (Cost of Goods /

Inventory)) + (365 /

(Credit sales /

Accounts

Receivable)) 47.88 40.93

Inventory Days 46.04 39.58

Credit sales 954500000 1291400000

365 / Inventory

Turnover 46.04 39.58

Inventory Turnover Ratio

Cost of Goods Sold /

Inventory 7.93 9.22

Cost Of Goods Sold 872800000 1185800000

Inventory 110100000 128600000

Trade Receivable Days

(Account

Receivables / Revenu

e Sales)*365 1.84 1.35

Total Sales 954500000 1291400000

Account Receivables 4800000 4770000

Trade Payable Days

(Trade Payables /

Cost of Sales) * 365 21.87 24.22

Trade Payables 52300000 78700000

Cost of Sales 872800000 1185800000

Working Capital Cycle / Operating

Cycle

(365/ (Cost of Goods /

Inventory)) + (365 /

(Credit sales /

Accounts

Receivable)) 47.88 40.93

Inventory Days 46.04 39.58

Credit sales 954500000 1291400000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts Receivables 4800000 4770000

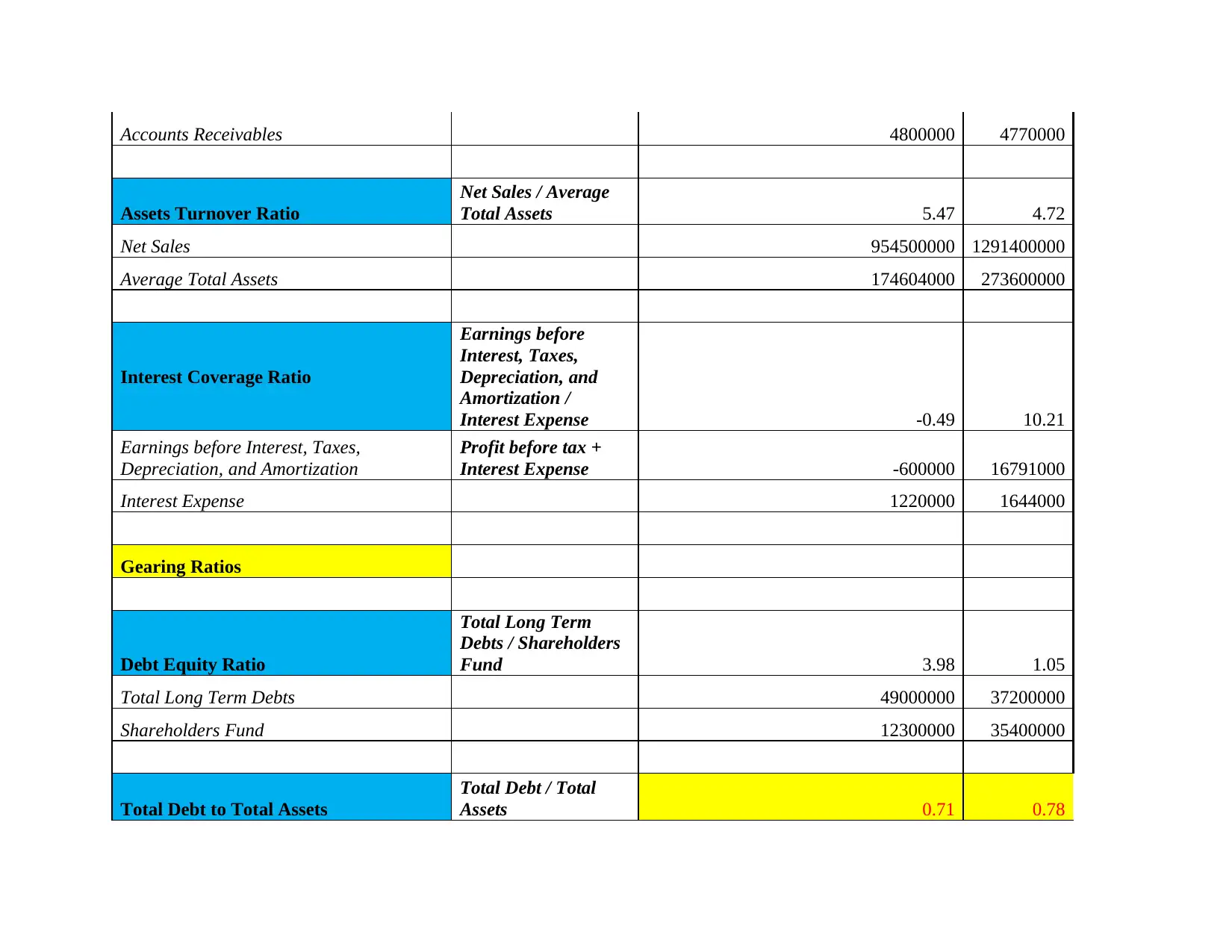

Assets Turnover Ratio

Net Sales / Average

Total Assets 5.47 4.72

Net Sales 954500000 1291400000

Average Total Assets 174604000 273600000

Interest Coverage Ratio

Earnings before

Interest, Taxes,

Depreciation, and

Amortization /

Interest Expense -0.49 10.21

Earnings before Interest, Taxes,

Depreciation, and Amortization

Profit before tax +

Interest Expense -600000 16791000

Interest Expense 1220000 1644000

Gearing Ratios

Debt Equity Ratio

Total Long Term

Debts / Shareholders

Fund 3.98 1.05

Total Long Term Debts 49000000 37200000

Shareholders Fund 12300000 35400000

Total Debt to Total Assets

Total Debt / Total

Assets 0.71 0.78

Assets Turnover Ratio

Net Sales / Average

Total Assets 5.47 4.72

Net Sales 954500000 1291400000

Average Total Assets 174604000 273600000

Interest Coverage Ratio

Earnings before

Interest, Taxes,

Depreciation, and

Amortization /

Interest Expense -0.49 10.21

Earnings before Interest, Taxes,

Depreciation, and Amortization

Profit before tax +

Interest Expense -600000 16791000

Interest Expense 1220000 1644000

Gearing Ratios

Debt Equity Ratio

Total Long Term

Debts / Shareholders

Fund 3.98 1.05

Total Long Term Debts 49000000 37200000

Shareholders Fund 12300000 35400000

Total Debt to Total Assets

Total Debt / Total

Assets 0.71 0.78

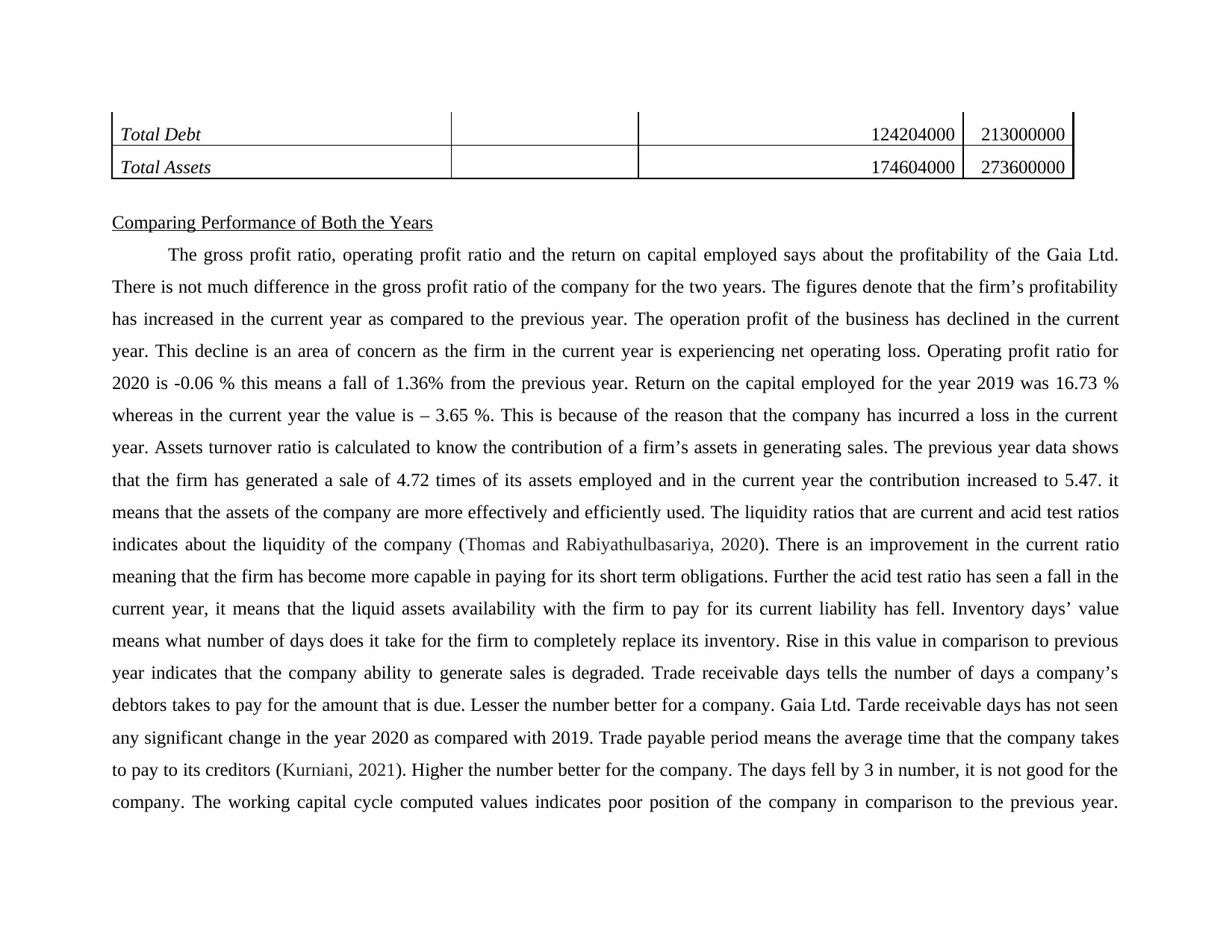

Total Debt 124204000 213000000

Total Assets 174604000 273600000

Comparing Performance of Both the Years

The gross profit ratio, operating profit ratio and the return on capital employed says about the profitability of the Gaia Ltd.

There is not much difference in the gross profit ratio of the company for the two years. The figures denote that the firm’s profitability

has increased in the current year as compared to the previous year. The operation profit of the business has declined in the current

year. This decline is an area of concern as the firm in the current year is experiencing net operating loss. Operating profit ratio for

2020 is -0.06 % this means a fall of 1.36% from the previous year. Return on the capital employed for the year 2019 was 16.73 %

whereas in the current year the value is – 3.65 %. This is because of the reason that the company has incurred a loss in the current

year. Assets turnover ratio is calculated to know the contribution of a firm’s assets in generating sales. The previous year data shows

that the firm has generated a sale of 4.72 times of its assets employed and in the current year the contribution increased to 5.47. it

means that the assets of the company are more effectively and efficiently used. The liquidity ratios that are current and acid test ratios

indicates about the liquidity of the company (Thomas and Rabiyathulbasariya, 2020). There is an improvement in the current ratio

meaning that the firm has become more capable in paying for its short term obligations. Further the acid test ratio has seen a fall in the

current year, it means that the liquid assets availability with the firm to pay for its current liability has fell. Inventory days’ value

means what number of days does it take for the firm to completely replace its inventory. Rise in this value in comparison to previous

year indicates that the company ability to generate sales is degraded. Trade receivable days tells the number of days a company’s

debtors takes to pay for the amount that is due. Lesser the number better for a company. Gaia Ltd. Tarde receivable days has not seen

any significant change in the year 2020 as compared with 2019. Trade payable period means the average time that the company takes

to pay to its creditors (Kurniani, 2021). Higher the number better for the company. The days fell by 3 in number, it is not good for the

company. The working capital cycle computed values indicates poor position of the company in comparison to the previous year.

Total Assets 174604000 273600000

Comparing Performance of Both the Years

The gross profit ratio, operating profit ratio and the return on capital employed says about the profitability of the Gaia Ltd.

There is not much difference in the gross profit ratio of the company for the two years. The figures denote that the firm’s profitability

has increased in the current year as compared to the previous year. The operation profit of the business has declined in the current

year. This decline is an area of concern as the firm in the current year is experiencing net operating loss. Operating profit ratio for

2020 is -0.06 % this means a fall of 1.36% from the previous year. Return on the capital employed for the year 2019 was 16.73 %

whereas in the current year the value is – 3.65 %. This is because of the reason that the company has incurred a loss in the current

year. Assets turnover ratio is calculated to know the contribution of a firm’s assets in generating sales. The previous year data shows

that the firm has generated a sale of 4.72 times of its assets employed and in the current year the contribution increased to 5.47. it

means that the assets of the company are more effectively and efficiently used. The liquidity ratios that are current and acid test ratios

indicates about the liquidity of the company (Thomas and Rabiyathulbasariya, 2020). There is an improvement in the current ratio

meaning that the firm has become more capable in paying for its short term obligations. Further the acid test ratio has seen a fall in the

current year, it means that the liquid assets availability with the firm to pay for its current liability has fell. Inventory days’ value

means what number of days does it take for the firm to completely replace its inventory. Rise in this value in comparison to previous

year indicates that the company ability to generate sales is degraded. Trade receivable days tells the number of days a company’s

debtors takes to pay for the amount that is due. Lesser the number better for a company. Gaia Ltd. Tarde receivable days has not seen

any significant change in the year 2020 as compared with 2019. Trade payable period means the average time that the company takes

to pay to its creditors (Kurniani, 2021). Higher the number better for the company. The days fell by 3 in number, it is not good for the

company. The working capital cycle computed values indicates poor position of the company in comparison to the previous year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Gearing ratios of the company shows increasing dependency of the company over the external sources of funds. Interest

coverage ratio indicates the incapability of the company to meet its interest obligations. It is not recommended for the company to

expand further.

To sum up the ratio analysis of the company Gaia Ltd. it can be said that the company has seen and improvement in its current

ratio which is good but still its current ratio is not an ideal ratio. So the company should focus on further improving its current ratio.

Speaking about the other liquidity ratio that is the liquidity ratio, in the previous year it was also not ideal and company should have

tried to improve it but the present year computed value shows that it has further diminished which is again not a good indicator of the

liquidity of the company. Hence, it should concentrate on improving it to remain attractive to the existing and potential investors.

Gross profit ratio shows minute improvement, overall the gross margin of the company is not good. It should increase its sales through

marketing and also control its production or direct expenses. Operating expenses of the company needs to be controlled on priority

basis for making improvements in its operating margin which is negative currently. Inventory days increased meaning poor sales

activities of the company. The Gaia Ltd. should focus on enhancing its sales. Increase in trade receivable days shows the inability of

the company to recover its money faster from its debtors which is again not a good sign. The company should make its credit terms

clear and offer incentives on early payments.

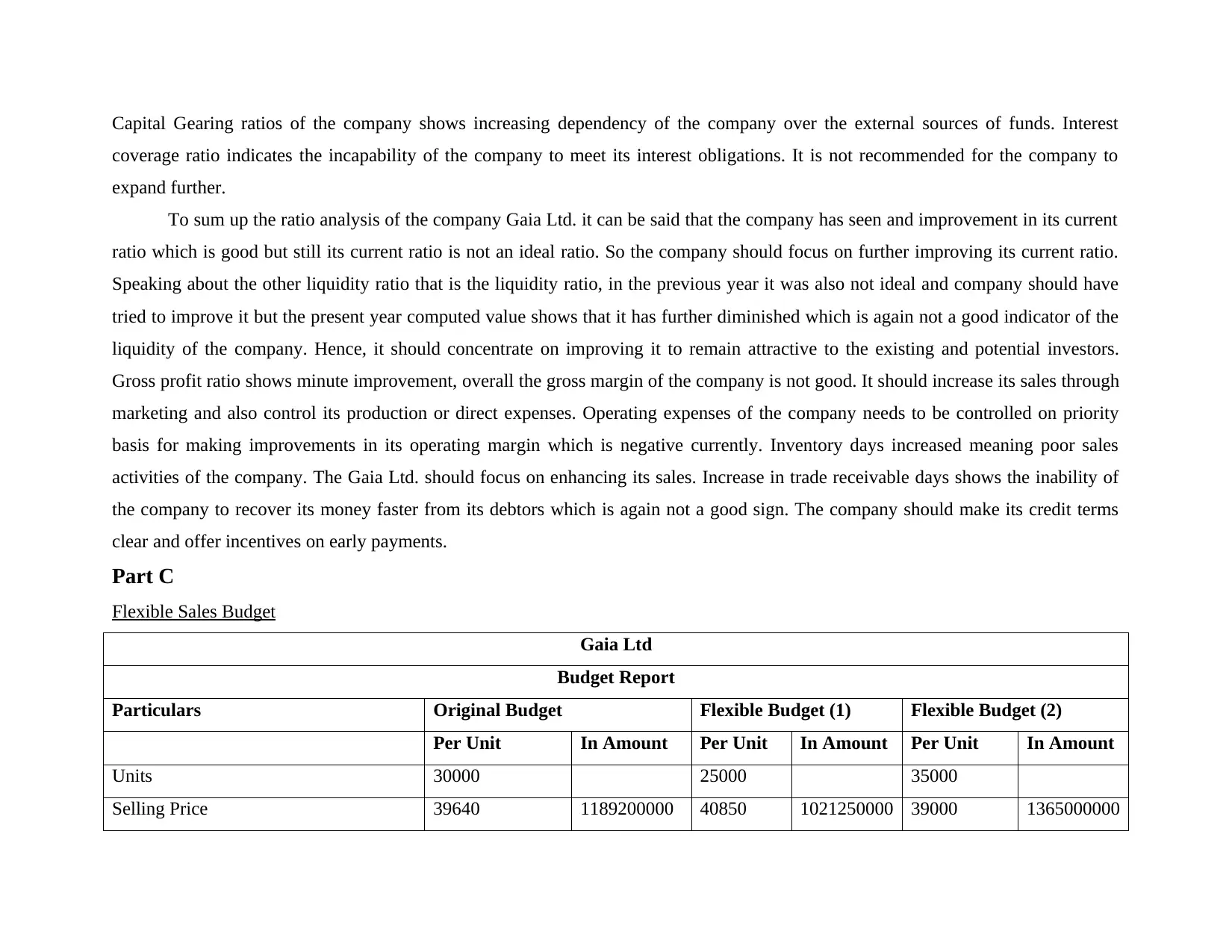

Part C

Flexible Sales Budget

Gaia Ltd

Budget Report

Particulars Original Budget Flexible Budget (1) Flexible Budget (2)

Per Unit In Amount Per Unit In Amount Per Unit In Amount

Units 30000 25000 35000

Selling Price 39640 1189200000 40850 1021250000 39000 1365000000

coverage ratio indicates the incapability of the company to meet its interest obligations. It is not recommended for the company to

expand further.

To sum up the ratio analysis of the company Gaia Ltd. it can be said that the company has seen and improvement in its current

ratio which is good but still its current ratio is not an ideal ratio. So the company should focus on further improving its current ratio.

Speaking about the other liquidity ratio that is the liquidity ratio, in the previous year it was also not ideal and company should have

tried to improve it but the present year computed value shows that it has further diminished which is again not a good indicator of the

liquidity of the company. Hence, it should concentrate on improving it to remain attractive to the existing and potential investors.

Gross profit ratio shows minute improvement, overall the gross margin of the company is not good. It should increase its sales through

marketing and also control its production or direct expenses. Operating expenses of the company needs to be controlled on priority

basis for making improvements in its operating margin which is negative currently. Inventory days increased meaning poor sales

activities of the company. The Gaia Ltd. should focus on enhancing its sales. Increase in trade receivable days shows the inability of

the company to recover its money faster from its debtors which is again not a good sign. The company should make its credit terms

clear and offer incentives on early payments.

Part C

Flexible Sales Budget

Gaia Ltd

Budget Report

Particulars Original Budget Flexible Budget (1) Flexible Budget (2)

Per Unit In Amount Per Unit In Amount Per Unit In Amount

Units 30000 25000 35000

Selling Price 39640 1189200000 40850 1021250000 39000 1365000000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

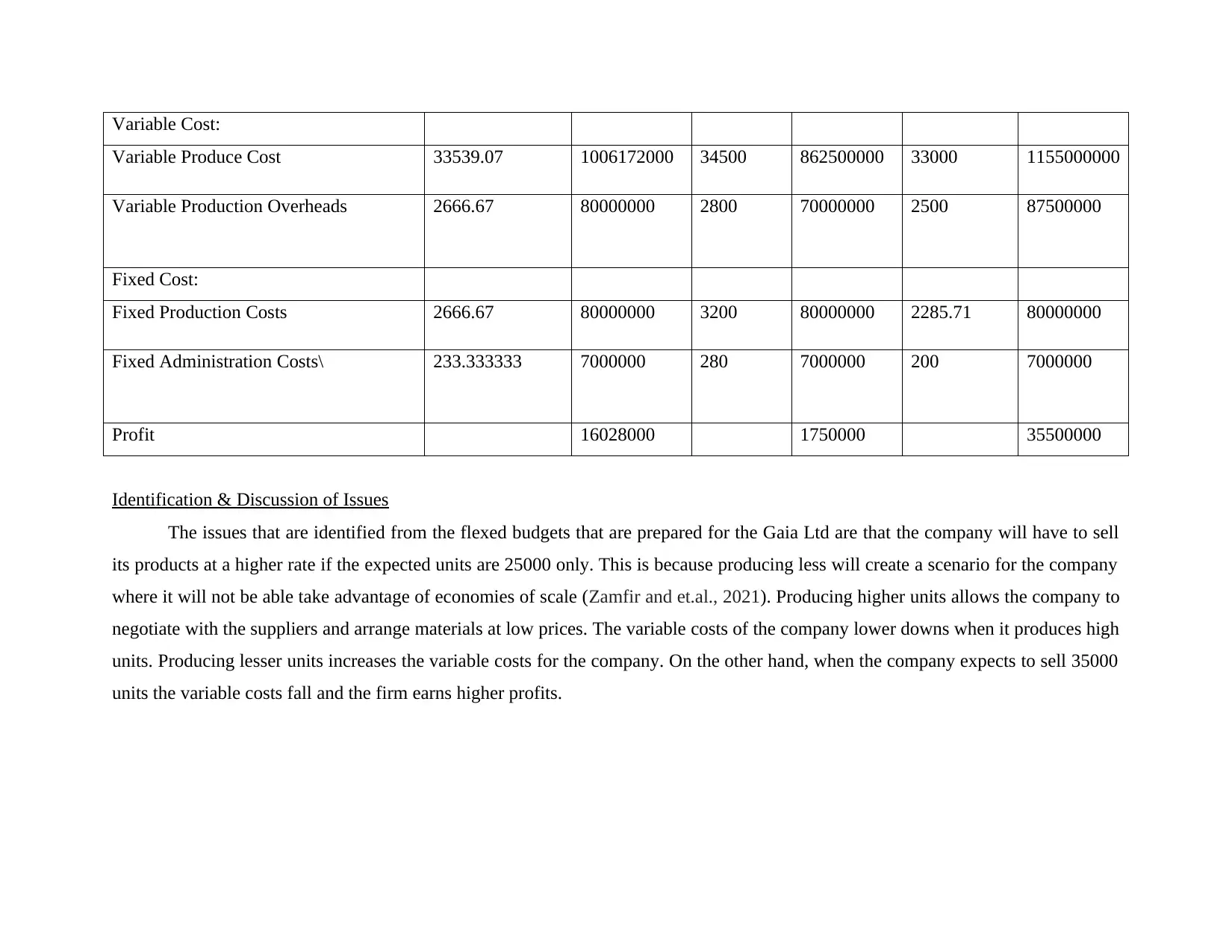

Variable Cost:

Variable Produce Cost 33539.07 1006172000 34500 862500000 33000 1155000000

Variable Production Overheads 2666.67 80000000 2800 70000000 2500 87500000

Fixed Cost:

Fixed Production Costs 2666.67 80000000 3200 80000000 2285.71 80000000

Fixed Administration Costs\ 233.333333 7000000 280 7000000 200 7000000

Profit 16028000 1750000 35500000

Identification & Discussion of Issues

The issues that are identified from the flexed budgets that are prepared for the Gaia Ltd are that the company will have to sell

its products at a higher rate if the expected units are 25000 only. This is because producing less will create a scenario for the company

where it will not be able take advantage of economies of scale (Zamfir and et.al., 2021). Producing higher units allows the company to

negotiate with the suppliers and arrange materials at low prices. The variable costs of the company lower downs when it produces high

units. Producing lesser units increases the variable costs for the company. On the other hand, when the company expects to sell 35000

units the variable costs fall and the firm earns higher profits.

Variable Produce Cost 33539.07 1006172000 34500 862500000 33000 1155000000

Variable Production Overheads 2666.67 80000000 2800 70000000 2500 87500000

Fixed Cost:

Fixed Production Costs 2666.67 80000000 3200 80000000 2285.71 80000000

Fixed Administration Costs\ 233.333333 7000000 280 7000000 200 7000000

Profit 16028000 1750000 35500000

Identification & Discussion of Issues

The issues that are identified from the flexed budgets that are prepared for the Gaia Ltd are that the company will have to sell

its products at a higher rate if the expected units are 25000 only. This is because producing less will create a scenario for the company

where it will not be able take advantage of economies of scale (Zamfir and et.al., 2021). Producing higher units allows the company to

negotiate with the suppliers and arrange materials at low prices. The variable costs of the company lower downs when it produces high

units. Producing lesser units increases the variable costs for the company. On the other hand, when the company expects to sell 35000

units the variable costs fall and the firm earns higher profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.