R.L. Maynard & Management Accounting Techniques

VerifiedAdded on 2020/01/16

|25

|6101

|168

Report

AI Summary

This assignment analyzes the use of management accounting techniques by R.L. Maynard, a small business venture. It explores how financial planning, cost analysis, budgeting control, and performance measurement contribute to the company's success. The report also compares R.L. Maynard's approach with its competitors, highlighting the differences and their impact on organizational performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

P.2 Different methods for management accounting reporting...................................................4

P3 Income statement of marginal and absorption costing..........................................................8

TASK 3..........................................................................................................................................12

P4 Different types of planning tools used for budgetary control with their advantages and

limitations..................................................................................................................................12

TASK 4 .........................................................................................................................................16

P5) Significance of management accounting systems in financial development of

R.L.Maynard.............................................................................................................................16

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

P.2 Different methods for management accounting reporting...................................................4

P3 Income statement of marginal and absorption costing..........................................................8

TASK 3..........................................................................................................................................12

P4 Different types of planning tools used for budgetary control with their advantages and

limitations..................................................................................................................................12

TASK 4 .........................................................................................................................................16

P5) Significance of management accounting systems in financial development of

R.L.Maynard.............................................................................................................................16

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

ILLUSTRATION INDEX

Illustration 1: Financial Planning Process........................................................................................5

Illustration 2: Income statement using marginal costing method....................................................9

Illustration 3: Income statement using absorption costing............................................................10

Illustration 4: NPV.........................................................................................................................13

Illustration 5: IRR .........................................................................................................................14

Illustration 1: Financial Planning Process........................................................................................5

Illustration 2: Income statement using marginal costing method....................................................9

Illustration 3: Income statement using absorption costing............................................................10

Illustration 4: NPV.........................................................................................................................13

Illustration 5: IRR .........................................................................................................................14

INTRODUCTION

Management Accounting is the process of analysing the financial position of the

organisation through the financial data available, to provide corrective short term decisions

within the organisation. It is the process of preparing various reports and accounts that provide

accurate financial information that helps the managers to make decisions regarding funding in

the new product or service or any other short term projects require ensuring the smooth running

of the enterprise (Abdel-Kader, 2011). Thus, management accounting deals with the

management of funds and optimum utilization of these funds to achieve the efficient and best

results. This report explains the various types of management accounting with their benefits and

limitations. It also explains the different methods of the management reporting with their

differences, through an income statement showing the absorption and marginal costing. This

report also signifies the merits and demerits of various budgetary control techniques. An analysis

and comparison of income statement as per absorption costing techniques and marginal costing

techniques is mentioned in this report and its detailed analysis is made to get quantity and price

variance in order to investigate the reason for such variances (Albu, and Albu, 2012).

TASK 1

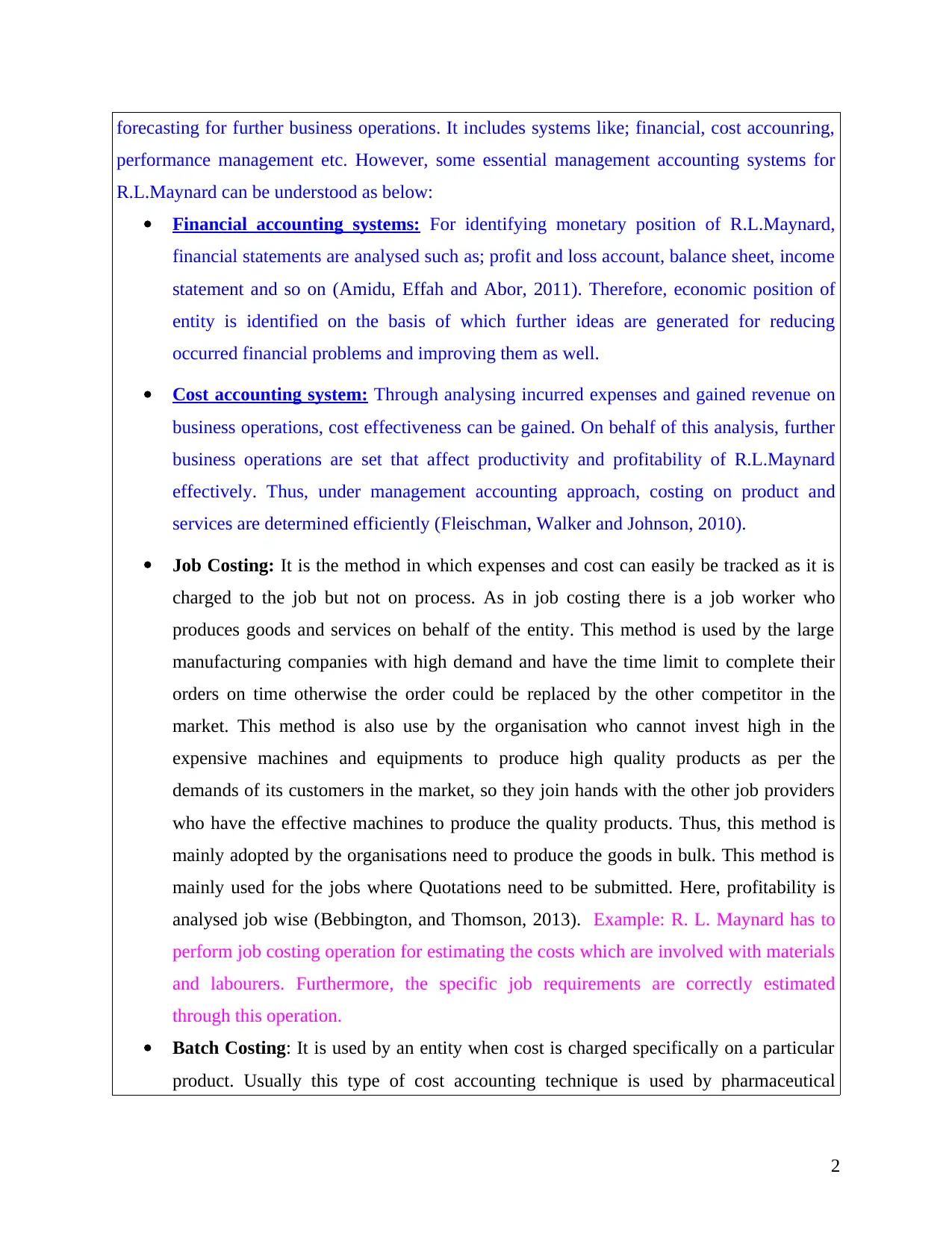

P1 Management accounting and its different types

General manager

R. L. Maynard

Management accounting: It signifies the way of the efficiently utilize the funds available

of the cited company. This process utilizes various techniques like budgetary control, variance

analysis and financial statement analysis in order to address all the requirements of

organisation. It provides the detail scenario of the organisation starting from analysing market

elements which may affect the process of organisation and ends with implementation of plans

and strategies with review of such plans (Amidu, Effah, and Abor, 2011). Thus, this process

helps the organisation to find out the variances and loop holes from the standards maintained

and actual results achieved so that the effective and timely actions could be taken to eliminate

them quickly before it affects the ultimate goals of the organisation. Various types of

management accounting systems are as follows:

There are different systems of management accounting regarding decision-making and

1

Management Accounting is the process of analysing the financial position of the

organisation through the financial data available, to provide corrective short term decisions

within the organisation. It is the process of preparing various reports and accounts that provide

accurate financial information that helps the managers to make decisions regarding funding in

the new product or service or any other short term projects require ensuring the smooth running

of the enterprise (Abdel-Kader, 2011). Thus, management accounting deals with the

management of funds and optimum utilization of these funds to achieve the efficient and best

results. This report explains the various types of management accounting with their benefits and

limitations. It also explains the different methods of the management reporting with their

differences, through an income statement showing the absorption and marginal costing. This

report also signifies the merits and demerits of various budgetary control techniques. An analysis

and comparison of income statement as per absorption costing techniques and marginal costing

techniques is mentioned in this report and its detailed analysis is made to get quantity and price

variance in order to investigate the reason for such variances (Albu, and Albu, 2012).

TASK 1

P1 Management accounting and its different types

General manager

R. L. Maynard

Management accounting: It signifies the way of the efficiently utilize the funds available

of the cited company. This process utilizes various techniques like budgetary control, variance

analysis and financial statement analysis in order to address all the requirements of

organisation. It provides the detail scenario of the organisation starting from analysing market

elements which may affect the process of organisation and ends with implementation of plans

and strategies with review of such plans (Amidu, Effah, and Abor, 2011). Thus, this process

helps the organisation to find out the variances and loop holes from the standards maintained

and actual results achieved so that the effective and timely actions could be taken to eliminate

them quickly before it affects the ultimate goals of the organisation. Various types of

management accounting systems are as follows:

There are different systems of management accounting regarding decision-making and

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

forecasting for further business operations. It includes systems like; financial, cost accounring,

performance management etc. However, some essential management accounting systems for

R.L.Maynard can be understood as below:

Financial accounting systems: For identifying monetary position of R.L.Maynard,

financial statements are analysed such as; profit and loss account, balance sheet, income

statement and so on (Amidu, Effah and Abor, 2011). Therefore, economic position of

entity is identified on the basis of which further ideas are generated for reducing

occurred financial problems and improving them as well.

Cost accounting system: Through analysing incurred expenses and gained revenue on

business operations, cost effectiveness can be gained. On behalf of this analysis, further

business operations are set that affect productivity and profitability of R.L.Maynard

effectively. Thus, under management accounting approach, costing on product and

services are determined efficiently (Fleischman, Walker and Johnson, 2010).

Job Costing: It is the method in which expenses and cost can easily be tracked as it is

charged to the job but not on process. As in job costing there is a job worker who

produces goods and services on behalf of the entity. This method is used by the large

manufacturing companies with high demand and have the time limit to complete their

orders on time otherwise the order could be replaced by the other competitor in the

market. This method is also use by the organisation who cannot invest high in the

expensive machines and equipments to produce high quality products as per the

demands of its customers in the market, so they join hands with the other job providers

who have the effective machines to produce the quality products. Thus, this method is

mainly adopted by the organisations need to produce the goods in bulk. This method is

mainly used for the jobs where Quotations need to be submitted. Here, profitability is

analysed job wise (Bebbington, and Thomson, 2013). Example: R. L. Maynard has to

perform job costing operation for estimating the costs which are involved with materials

and labourers. Furthermore, the specific job requirements are correctly estimated

through this operation.

Batch Costing: It is used by an entity when cost is charged specifically on a particular

product. Usually this type of cost accounting technique is used by pharmaceutical

2

performance management etc. However, some essential management accounting systems for

R.L.Maynard can be understood as below:

Financial accounting systems: For identifying monetary position of R.L.Maynard,

financial statements are analysed such as; profit and loss account, balance sheet, income

statement and so on (Amidu, Effah and Abor, 2011). Therefore, economic position of

entity is identified on the basis of which further ideas are generated for reducing

occurred financial problems and improving them as well.

Cost accounting system: Through analysing incurred expenses and gained revenue on

business operations, cost effectiveness can be gained. On behalf of this analysis, further

business operations are set that affect productivity and profitability of R.L.Maynard

effectively. Thus, under management accounting approach, costing on product and

services are determined efficiently (Fleischman, Walker and Johnson, 2010).

Job Costing: It is the method in which expenses and cost can easily be tracked as it is

charged to the job but not on process. As in job costing there is a job worker who

produces goods and services on behalf of the entity. This method is used by the large

manufacturing companies with high demand and have the time limit to complete their

orders on time otherwise the order could be replaced by the other competitor in the

market. This method is also use by the organisation who cannot invest high in the

expensive machines and equipments to produce high quality products as per the

demands of its customers in the market, so they join hands with the other job providers

who have the effective machines to produce the quality products. Thus, this method is

mainly adopted by the organisations need to produce the goods in bulk. This method is

mainly used for the jobs where Quotations need to be submitted. Here, profitability is

analysed job wise (Bebbington, and Thomson, 2013). Example: R. L. Maynard has to

perform job costing operation for estimating the costs which are involved with materials

and labourers. Furthermore, the specific job requirements are correctly estimated

through this operation.

Batch Costing: It is used by an entity when cost is charged specifically on a particular

product. Usually this type of cost accounting technique is used by pharmaceutical

2

industry. Such batches contains identical units but their prices are different. If each

batch and its cost is easily ascertainable only in that case batch costing technique can be

used by a firm. In this method every batch has the fixed price thus these batches could

easily be traced through the batch number. To calculate the cost the products produced

are averaged and thus thus in this method cost per product is generally low as it deals

with the large scale production like medicines. This method consists of mainly two type

of cost i.e. preparation cost and carrying cost. Set up cost is the cost involved in the

setting up of machines and the equipments require for the production and carrying cost

includes manufacturing cost, storage cost, depreciation etc (Brandau, and 2013).

Price optimization system: Through this management accounting system, price

optimization for production and distribution of goods and services. However, it is able

for cost effectiveness and proper management of entire business operations affect

further implementation. In this regard, appropriate cost is set on the basis of incurred

cost on expenditures regarding business operations (Douglas and CFM, 2012).

Therefore, price optimization system is essential for effective decision making and

forecasting on management of further business operations of R.L.Maynard.

Contract costing: In this type of cost accounting or management accounting

techniques cost is tracked on the basis of specific order. It simply means that cost related

with a contract is charged exclusively on that particular contract. The contract means the

legal agreement between the two parties to carry out the specific work within the time

limit. Contract costing signifies the method to calculate the cost of the long term

contract like construction of the bridges and dams which took about two or three years

to complete but the cost is pre decided in the agreement having an escalation clause that

signifies the hike in the contract price at fixed percentage due to hike in the material,

labour and other raw materials necessary for the contract to be completed. The payment

in this contract is made to the contractee on the basis of the work certified by the

engineer of the contractee (Callahan, Stetz, and Brooks, 2011).

Inventory management system: This management accounting system is able to

manage inventories of R.L.Maynard that affect its productivity and profitability. In

addition to this, inventory management system is essential to be identified for adequacy

of resources and fund systematically (Ihantolaand Kihn, 2011). Therefore, inventory

3

batch and its cost is easily ascertainable only in that case batch costing technique can be

used by a firm. In this method every batch has the fixed price thus these batches could

easily be traced through the batch number. To calculate the cost the products produced

are averaged and thus thus in this method cost per product is generally low as it deals

with the large scale production like medicines. This method consists of mainly two type

of cost i.e. preparation cost and carrying cost. Set up cost is the cost involved in the

setting up of machines and the equipments require for the production and carrying cost

includes manufacturing cost, storage cost, depreciation etc (Brandau, and 2013).

Price optimization system: Through this management accounting system, price

optimization for production and distribution of goods and services. However, it is able

for cost effectiveness and proper management of entire business operations affect

further implementation. In this regard, appropriate cost is set on the basis of incurred

cost on expenditures regarding business operations (Douglas and CFM, 2012).

Therefore, price optimization system is essential for effective decision making and

forecasting on management of further business operations of R.L.Maynard.

Contract costing: In this type of cost accounting or management accounting

techniques cost is tracked on the basis of specific order. It simply means that cost related

with a contract is charged exclusively on that particular contract. The contract means the

legal agreement between the two parties to carry out the specific work within the time

limit. Contract costing signifies the method to calculate the cost of the long term

contract like construction of the bridges and dams which took about two or three years

to complete but the cost is pre decided in the agreement having an escalation clause that

signifies the hike in the contract price at fixed percentage due to hike in the material,

labour and other raw materials necessary for the contract to be completed. The payment

in this contract is made to the contractee on the basis of the work certified by the

engineer of the contractee (Callahan, Stetz, and Brooks, 2011).

Inventory management system: This management accounting system is able to

manage inventories of R.L.Maynard that affect its productivity and profitability. In

addition to this, inventory management system is essential to be identified for adequacy

of resources and fund systematically (Ihantolaand Kihn, 2011). Therefore, inventory

3

management is vital approach of accounting system affect balancing production and

distribution of goods efficiently.

Performance management system: As management accounting is multidisciplinary

approach also remains able to manage its employees' performance (Harris and Durden,

2012). In this regard, their performances are identified and further decisions are made to

improve them through conducting training and development programs efficiently.

P.2 Different methods for management accounting reporting

Management accounting reporting signifies the way to present the process, productivity

and profitability of the R.L. Maynard which is the small business venture that has the business to

hold the management activities of the large corporation in Gerrards Cross in UK. Management

accounting differs from the financial accounting as financial accounting is based on the double

entry system and have some specific standards to be followed whereas management accounting

do not have any prescribed standards to be followed. These report could be maintained by the

organisations as per their necessity and preferences (Fleischman, Walker, and Johnson, 2010).

These reports are not legally prescribed by the income tax department to be presented in the

annual returns. Thus, these reports are maintained by the corporates for their own analysis and

evaluation to know exact position of the company in the market to take the long term and short

term decisions regarding the finance or other related services delivered by the company

R.L.Maynard. For example, Budgeting techniques are available in management accounting for

the forecasting of future projects but on the other side there is no any such forecasting technique

which is available in financial accounting (Gates, Nicolas, and Walker,2012).

Various methods of management accounting reporting is mentioned below :

Financial Planning: Financial planning is the continuous process that direct the

organisation to make the effective decisions regarding money, that how and where the funds

present could be effectively utilize to meet the ultimate goals of the organisation. Financial plan

of the R.L.Maynard could effectively be used to have clear view of the objectives to be achieved

as following:

4

distribution of goods efficiently.

Performance management system: As management accounting is multidisciplinary

approach also remains able to manage its employees' performance (Harris and Durden,

2012). In this regard, their performances are identified and further decisions are made to

improve them through conducting training and development programs efficiently.

P.2 Different methods for management accounting reporting

Management accounting reporting signifies the way to present the process, productivity

and profitability of the R.L. Maynard which is the small business venture that has the business to

hold the management activities of the large corporation in Gerrards Cross in UK. Management

accounting differs from the financial accounting as financial accounting is based on the double

entry system and have some specific standards to be followed whereas management accounting

do not have any prescribed standards to be followed. These report could be maintained by the

organisations as per their necessity and preferences (Fleischman, Walker, and Johnson, 2010).

These reports are not legally prescribed by the income tax department to be presented in the

annual returns. Thus, these reports are maintained by the corporates for their own analysis and

evaluation to know exact position of the company in the market to take the long term and short

term decisions regarding the finance or other related services delivered by the company

R.L.Maynard. For example, Budgeting techniques are available in management accounting for

the forecasting of future projects but on the other side there is no any such forecasting technique

which is available in financial accounting (Gates, Nicolas, and Walker,2012).

Various methods of management accounting reporting is mentioned below :

Financial Planning: Financial planning is the continuous process that direct the

organisation to make the effective decisions regarding money, that how and where the funds

present could be effectively utilize to meet the ultimate goals of the organisation. Financial plan

of the R.L.Maynard could effectively be used to have clear view of the objectives to be achieved

as following:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

First stage of the financial planning is to gather the client information and then the goals

are set as per the specific goals and objectives for the organisation as per the current scenario of

the market. Second stage to analyse the present financial situation of the organisation through the

other management accounting reports till the date such as budgetary control statement, inventory

and manufacturing report, job cost report etc. This helps the organisation to underline the basic

fund requirement and the company's position to utilize its internal resources (Harris, and Durden,

2012). After the financial analysis, the management need to develop the effective plan about how

the available funds will be utilize effectively. If the corporate requires the external funds it need

to also plan its sources in this stage. This plan also give the clear view of how the plan is

implemented and what is the outcome of the implementation. Thus, financial planning is also

helps in reporting management accounting system.

Budget Report :

5

Illustration 1: Financial Planning Process

Source: (Financial Planning Process, 2017)

are set as per the specific goals and objectives for the organisation as per the current scenario of

the market. Second stage to analyse the present financial situation of the organisation through the

other management accounting reports till the date such as budgetary control statement, inventory

and manufacturing report, job cost report etc. This helps the organisation to underline the basic

fund requirement and the company's position to utilize its internal resources (Harris, and Durden,

2012). After the financial analysis, the management need to develop the effective plan about how

the available funds will be utilize effectively. If the corporate requires the external funds it need

to also plan its sources in this stage. This plan also give the clear view of how the plan is

implemented and what is the outcome of the implementation. Thus, financial planning is also

helps in reporting management accounting system.

Budget Report :

5

Illustration 1: Financial Planning Process

Source: (Financial Planning Process, 2017)

Budget reports helps the small business organisations like R.L.Maynard to analyse their

department's performance taking into account the standards prescribed and the actual results

achieved. This method help the organisation to calculate the variances and take effective steps to

eliminate these variances and achieve the desired standards. Here, the estimated budget is based

on the actual expenses of prior years thus any changes in the cost in the current year leads to the

variances (Hyndman, and Connolly, 2011) . This report can also be used by the managers to

provide incentives as per the targets achieved so it is the effective method to motivate the

employees as this report gives the clear picture of what need to be achieve. This is the effective

method to plan the effective allocation and utilization of the available resources in the

organisation. Thus, this method facilitate the continuous control on the operations performed in

the organisation. These budgets are the warning signs for the organisation that appropriate

actions are required. But, since the budgets are based on the future prospects and it is not

possible to predict the future accurately thus errors and inaccuracies are possible (Ihantola, and

Kihn, 2011).

Inventory And Manufacturing:

Companies with physical inventory maintains this report to analyse the right position of

the inventory waste, hourly labour costs and per unit overhead cost. Manufacturing companies

could sustain in the market for the long run only when they keep their product's cost competitive

low as compare to the other competitors . Thus, they need to achieve an competitive advantage

over the cost of the product which could be only possible through effective utilization of the

resources available and thus effective planning is required on the same. The managers through

this report can even improve the working of their departments and can also motivate the same on

its improvements through the monitory and non monitory incentives ( Mat, Smith, and

Djajadikerta, 2010).

Financial Statements Analysis :

Financials or financial statements is analysed in order to understand the current financial

position of business enterprise(Fleischman, Walker and Johnson, 2010). The facts which are

extracted through such analysis can be shown in the financial reporting of R.L.Maynard.

Cost Accounting :

It is a method through which reporting can be done as it includes various techniques of

budgetary control and variance analysis through which better presentations can be made and

6

department's performance taking into account the standards prescribed and the actual results

achieved. This method help the organisation to calculate the variances and take effective steps to

eliminate these variances and achieve the desired standards. Here, the estimated budget is based

on the actual expenses of prior years thus any changes in the cost in the current year leads to the

variances (Hyndman, and Connolly, 2011) . This report can also be used by the managers to

provide incentives as per the targets achieved so it is the effective method to motivate the

employees as this report gives the clear picture of what need to be achieve. This is the effective

method to plan the effective allocation and utilization of the available resources in the

organisation. Thus, this method facilitate the continuous control on the operations performed in

the organisation. These budgets are the warning signs for the organisation that appropriate

actions are required. But, since the budgets are based on the future prospects and it is not

possible to predict the future accurately thus errors and inaccuracies are possible (Ihantola, and

Kihn, 2011).

Inventory And Manufacturing:

Companies with physical inventory maintains this report to analyse the right position of

the inventory waste, hourly labour costs and per unit overhead cost. Manufacturing companies

could sustain in the market for the long run only when they keep their product's cost competitive

low as compare to the other competitors . Thus, they need to achieve an competitive advantage

over the cost of the product which could be only possible through effective utilization of the

resources available and thus effective planning is required on the same. The managers through

this report can even improve the working of their departments and can also motivate the same on

its improvements through the monitory and non monitory incentives ( Mat, Smith, and

Djajadikerta, 2010).

Financial Statements Analysis :

Financials or financial statements is analysed in order to understand the current financial

position of business enterprise(Fleischman, Walker and Johnson, 2010). The facts which are

extracted through such analysis can be shown in the financial reporting of R.L.Maynard.

Cost Accounting :

It is a method through which reporting can be done as it includes various techniques of

budgetary control and variance analysis through which better presentations can be made and

6

comparison between estimation, expectation and real output can be made. Cost can be controlled

as well as it can be reduced up to a certain level at which cited entity can attain the aim of

profitability.

Cost Reports

Cost reports can be prepared by the management accountant in four steps(Hyndman and

Connolly,2011). These steps are mentioned below which needs to be followed by cited

entity to prepare production cost report :

Computation of physical units

Computation of equivalent units in respect of production

Cost per unit

Preparation of cost reconciliation statements.

By following the above mentioned steps management can prepare cost report in respect

of its products. Financial or cost reporting assist an entity to find the core areas in which the

corporate requires to improvise itself. Further they can strengthen such areas so that they can

attain a major share in targeted market. There are some cost drivers which needs to be manage so

that company can get a cracking profit margin. There are some performance indicators or key

performance indicators which are nothing but the objectives of entity which acts as a

measurement of performance as if entity has achieved those objectives then its means it is

performing good in the market and vice-versa(Ihantola and Kihn,2011). These key performance

indicators (KPI) are mainly customer satisfaction, profitability, cost and customer retention.

These can be classified as performance measurements as if management can achieve the targets

which are set the by them .

Performance reports:

When business organisations develop reports on the performance of their enterprise or

employees or any other subject then such reports are considered as performance reports. Often

such kind of publications are produced by respective authoritative government. The objectives

which are developed by businesses for getting a directional flow have to be accomplished. The

attributes that contribute to this accomplishment depict the performance.

Segmental/Departmental Reports:

There are different functioning departments, divisions or subsidiaries associated with a

business. These are considered as departments or segments. The allocation of resources, income,

7

as well as it can be reduced up to a certain level at which cited entity can attain the aim of

profitability.

Cost Reports

Cost reports can be prepared by the management accountant in four steps(Hyndman and

Connolly,2011). These steps are mentioned below which needs to be followed by cited

entity to prepare production cost report :

Computation of physical units

Computation of equivalent units in respect of production

Cost per unit

Preparation of cost reconciliation statements.

By following the above mentioned steps management can prepare cost report in respect

of its products. Financial or cost reporting assist an entity to find the core areas in which the

corporate requires to improvise itself. Further they can strengthen such areas so that they can

attain a major share in targeted market. There are some cost drivers which needs to be manage so

that company can get a cracking profit margin. There are some performance indicators or key

performance indicators which are nothing but the objectives of entity which acts as a

measurement of performance as if entity has achieved those objectives then its means it is

performing good in the market and vice-versa(Ihantola and Kihn,2011). These key performance

indicators (KPI) are mainly customer satisfaction, profitability, cost and customer retention.

These can be classified as performance measurements as if management can achieve the targets

which are set the by them .

Performance reports:

When business organisations develop reports on the performance of their enterprise or

employees or any other subject then such reports are considered as performance reports. Often

such kind of publications are produced by respective authoritative government. The objectives

which are developed by businesses for getting a directional flow have to be accomplished. The

attributes that contribute to this accomplishment depict the performance.

Segmental/Departmental Reports:

There are different functioning departments, divisions or subsidiaries associated with a

business. These are considered as departments or segments. The allocation of resources, income,

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

expenditures, assets and liabilities, etc. are some of the elements of these segmental or

departmental reports.

Product/Service profitability Reports:

Profitability is an attribute which depicts the amount of benefits which can be procured

by a particular product or service. The nature of product or service that is provided by the

company and its impact over the target audience is estimated in these kinds of profitability

reports. It is important to understand the profit levels which will be reached by the company after

launching or introducing a product in the strategic markets.

Inventory management Reports:

Inventory management reports are completely based on the analysed and managed

information about the inventory that is the goods which are acquired by company currently. The

current status of the inventory, analysis and integrity reports are an integral inventory

management reports.

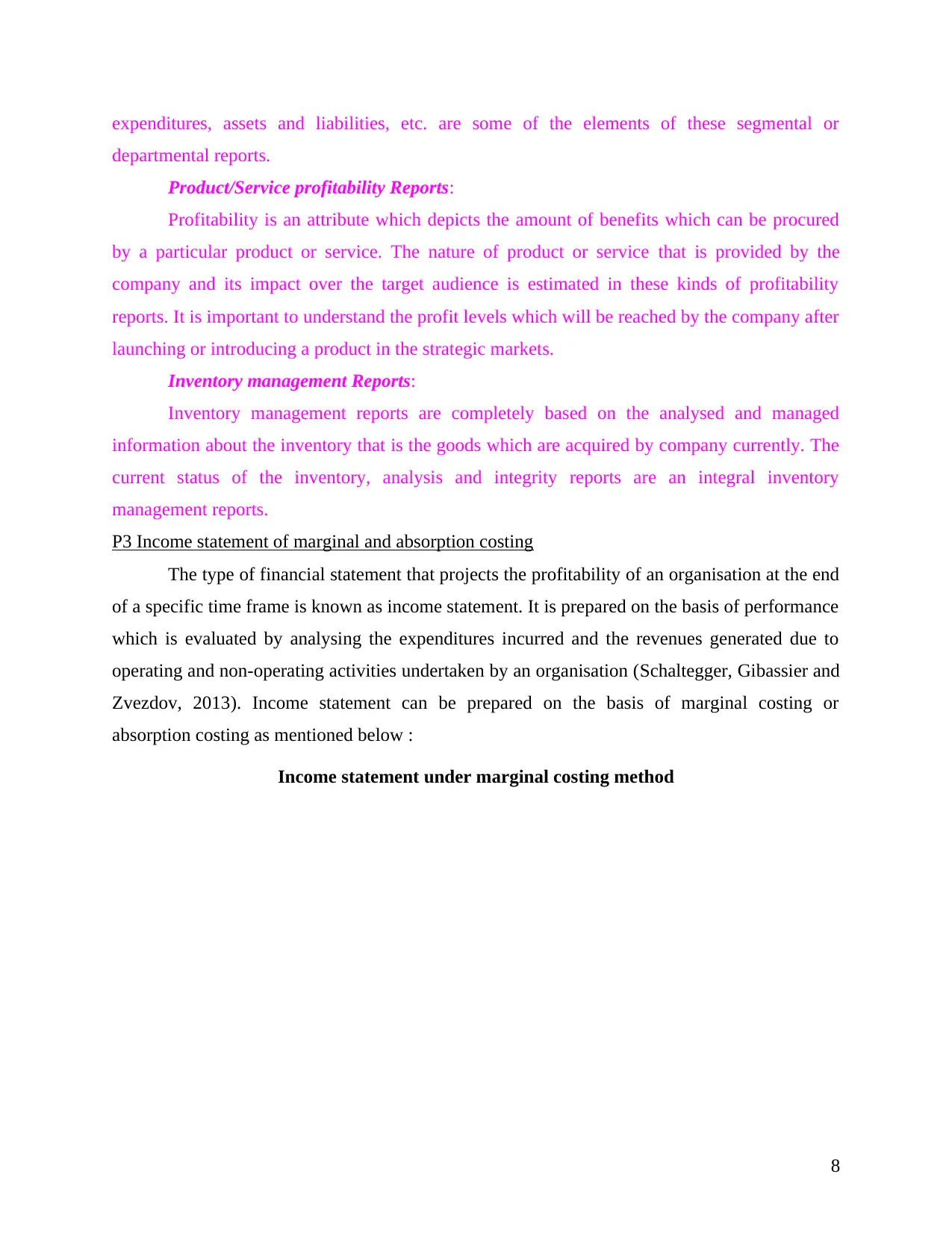

P3 Income statement of marginal and absorption costing

The type of financial statement that projects the profitability of an organisation at the end

of a specific time frame is known as income statement. It is prepared on the basis of performance

which is evaluated by analysing the expenditures incurred and the revenues generated due to

operating and non-operating activities undertaken by an organisation (Schaltegger, Gibassier and

Zvezdov, 2013). Income statement can be prepared on the basis of marginal costing or

absorption costing as mentioned below :

Income statement under marginal costing method

8

departmental reports.

Product/Service profitability Reports:

Profitability is an attribute which depicts the amount of benefits which can be procured

by a particular product or service. The nature of product or service that is provided by the

company and its impact over the target audience is estimated in these kinds of profitability

reports. It is important to understand the profit levels which will be reached by the company after

launching or introducing a product in the strategic markets.

Inventory management Reports:

Inventory management reports are completely based on the analysed and managed

information about the inventory that is the goods which are acquired by company currently. The

current status of the inventory, analysis and integrity reports are an integral inventory

management reports.

P3 Income statement of marginal and absorption costing

The type of financial statement that projects the profitability of an organisation at the end

of a specific time frame is known as income statement. It is prepared on the basis of performance

which is evaluated by analysing the expenditures incurred and the revenues generated due to

operating and non-operating activities undertaken by an organisation (Schaltegger, Gibassier and

Zvezdov, 2013). Income statement can be prepared on the basis of marginal costing or

absorption costing as mentioned below :

Income statement under marginal costing method

8

Income statement on the basis of absorption costing method

9

Illustration 2: Income statement using marginal costing method

9

Illustration 2: Income statement using marginal costing method

It can be analysed from the above income statements that company is generating better

net profits at the end of the month. The amount of net profit calculated under marginal and

absorption varies i.e. net profit earned on the basis of marginal costing method amounts to

£12600 which is higher as compared to net profit under absorption which amount to £9300. This

difference arises mainly due to different costs that are taken into account under both these

methods (van der Steen, 2011). Moreover, in the context of expenditures, it can be interpreted

that expenses under absorption are more i.e. £5100 because it considers both fixed costs and

variable costs. Whereas, expenses as per marginal amounts to £1800 which is quite less because

only variable expenditures are considered in this method.

10

Illustration 3: Income statement using absorption costing

net profits at the end of the month. The amount of net profit calculated under marginal and

absorption varies i.e. net profit earned on the basis of marginal costing method amounts to

£12600 which is higher as compared to net profit under absorption which amount to £9300. This

difference arises mainly due to different costs that are taken into account under both these

methods (van der Steen, 2011). Moreover, in the context of expenditures, it can be interpreted

that expenses under absorption are more i.e. £5100 because it considers both fixed costs and

variable costs. Whereas, expenses as per marginal amounts to £1800 which is quite less because

only variable expenditures are considered in this method.

10

Illustration 3: Income statement using absorption costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Generally, most of the companies prefer absorption costing method over marginal costing

method as it taken into account both fixed as well as variable expenditures of an organisation.

Therefore, absorption costing method helps to prepare income statement that shows clear and

appropriate financial performance with regard to profitability of an organisation at the period

end.

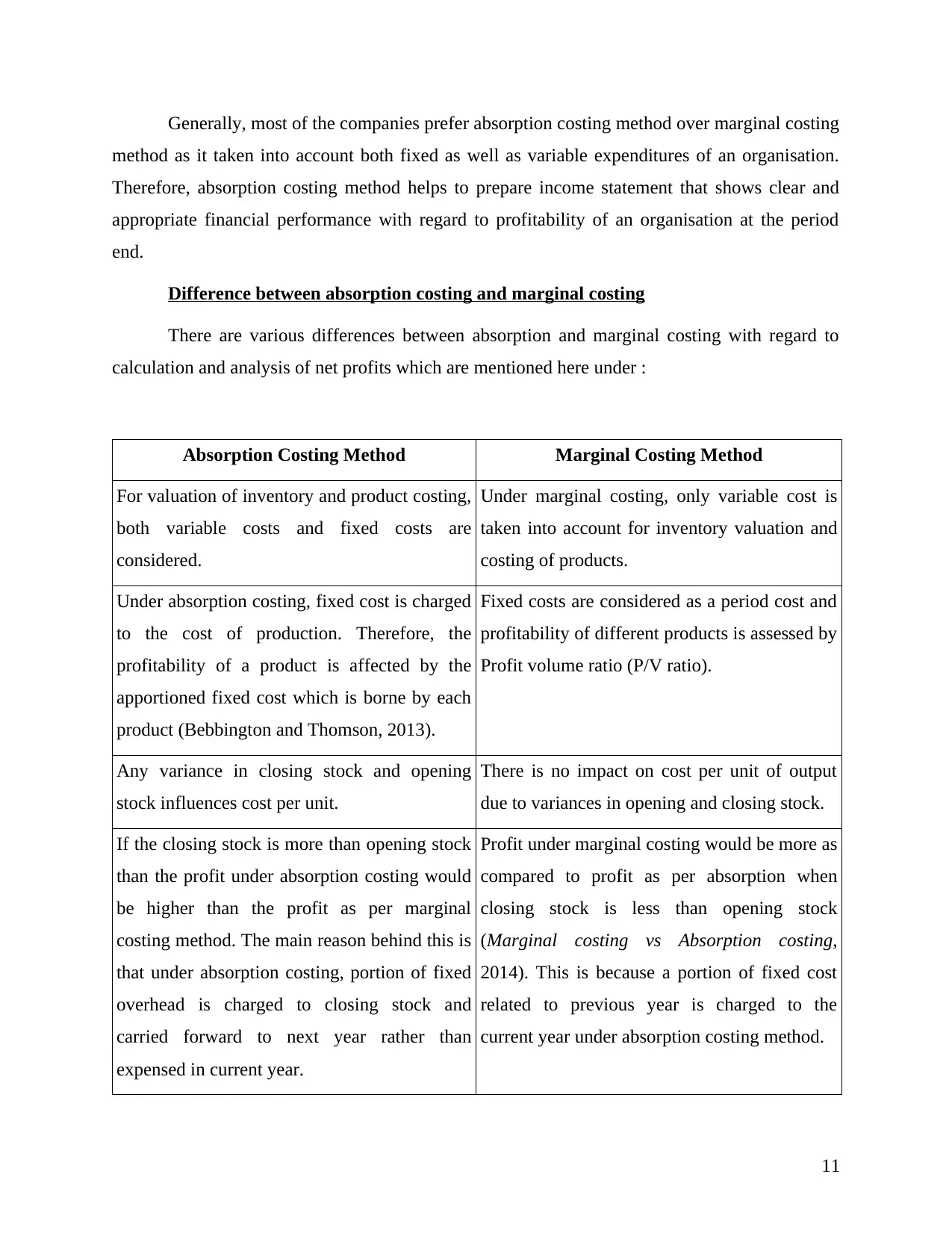

Difference between absorption costing and marginal costing

There are various differences between absorption and marginal costing with regard to

calculation and analysis of net profits which are mentioned here under :

Absorption Costing Method Marginal Costing Method

For valuation of inventory and product costing,

both variable costs and fixed costs are

considered.

Under marginal costing, only variable cost is

taken into account for inventory valuation and

costing of products.

Under absorption costing, fixed cost is charged

to the cost of production. Therefore, the

profitability of a product is affected by the

apportioned fixed cost which is borne by each

product (Bebbington and Thomson, 2013).

Fixed costs are considered as a period cost and

profitability of different products is assessed by

Profit volume ratio (P/V ratio).

Any variance in closing stock and opening

stock influences cost per unit.

There is no impact on cost per unit of output

due to variances in opening and closing stock.

If the closing stock is more than opening stock

than the profit under absorption costing would

be higher than the profit as per marginal

costing method. The main reason behind this is

that under absorption costing, portion of fixed

overhead is charged to closing stock and

carried forward to next year rather than

expensed in current year.

Profit under marginal costing would be more as

compared to profit as per absorption when

closing stock is less than opening stock

(Marginal costing vs Absorption costing,

2014). This is because a portion of fixed cost

related to previous year is charged to the

current year under absorption costing method.

11

method as it taken into account both fixed as well as variable expenditures of an organisation.

Therefore, absorption costing method helps to prepare income statement that shows clear and

appropriate financial performance with regard to profitability of an organisation at the period

end.

Difference between absorption costing and marginal costing

There are various differences between absorption and marginal costing with regard to

calculation and analysis of net profits which are mentioned here under :

Absorption Costing Method Marginal Costing Method

For valuation of inventory and product costing,

both variable costs and fixed costs are

considered.

Under marginal costing, only variable cost is

taken into account for inventory valuation and

costing of products.

Under absorption costing, fixed cost is charged

to the cost of production. Therefore, the

profitability of a product is affected by the

apportioned fixed cost which is borne by each

product (Bebbington and Thomson, 2013).

Fixed costs are considered as a period cost and

profitability of different products is assessed by

Profit volume ratio (P/V ratio).

Any variance in closing stock and opening

stock influences cost per unit.

There is no impact on cost per unit of output

due to variances in opening and closing stock.

If the closing stock is more than opening stock

than the profit under absorption costing would

be higher than the profit as per marginal

costing method. The main reason behind this is

that under absorption costing, portion of fixed

overhead is charged to closing stock and

carried forward to next year rather than

expensed in current year.

Profit under marginal costing would be more as

compared to profit as per absorption when

closing stock is less than opening stock

(Marginal costing vs Absorption costing,

2014). This is because a portion of fixed cost

related to previous year is charged to the

current year under absorption costing method.

11

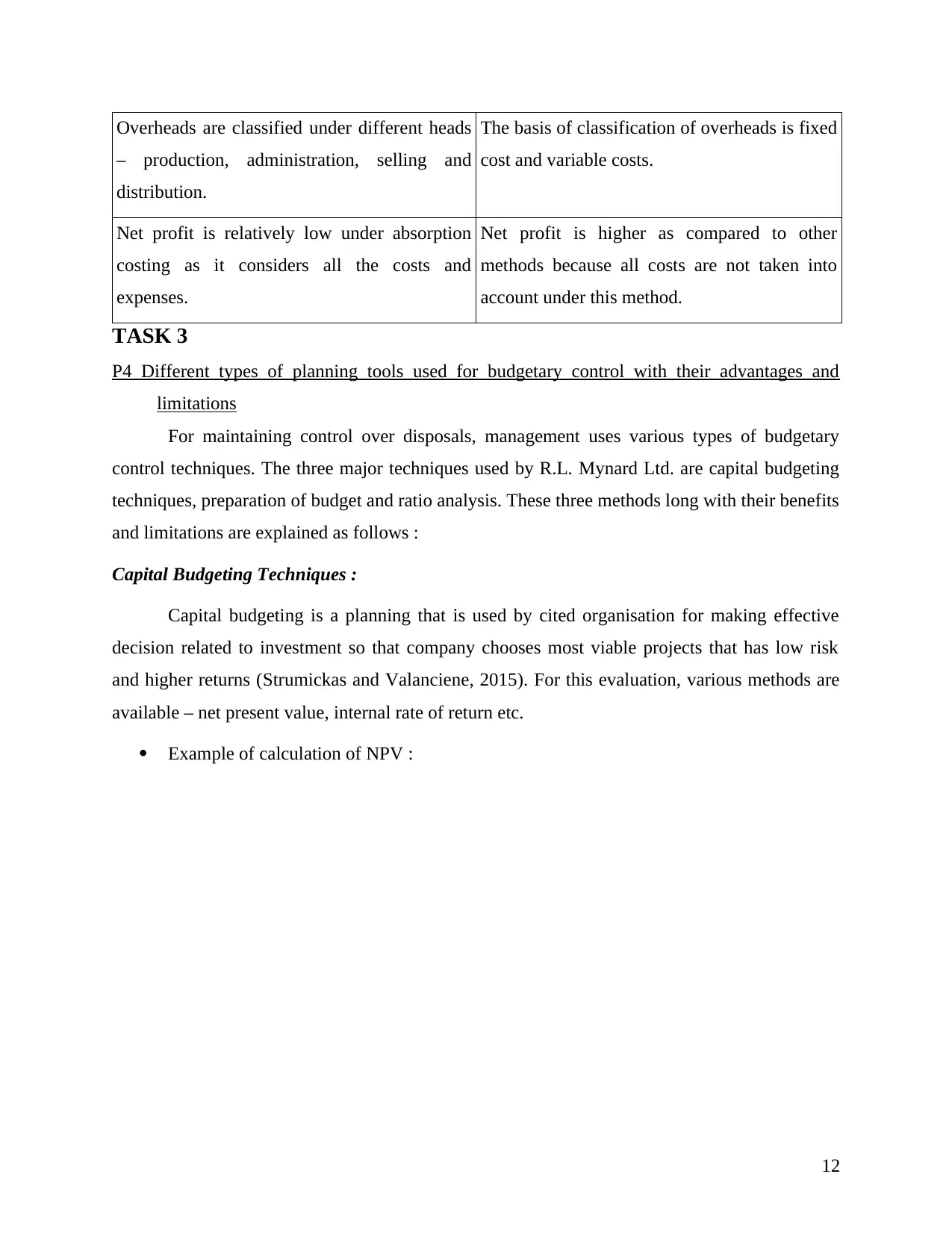

Overheads are classified under different heads

– production, administration, selling and

distribution.

The basis of classification of overheads is fixed

cost and variable costs.

Net profit is relatively low under absorption

costing as it considers all the costs and

expenses.

Net profit is higher as compared to other

methods because all costs are not taken into

account under this method.

TASK 3

P4 Different types of planning tools used for budgetary control with their advantages and

limitations

For maintaining control over disposals, management uses various types of budgetary

control techniques. The three major techniques used by R.L. Mynard Ltd. are capital budgeting

techniques, preparation of budget and ratio analysis. These three methods long with their benefits

and limitations are explained as follows :

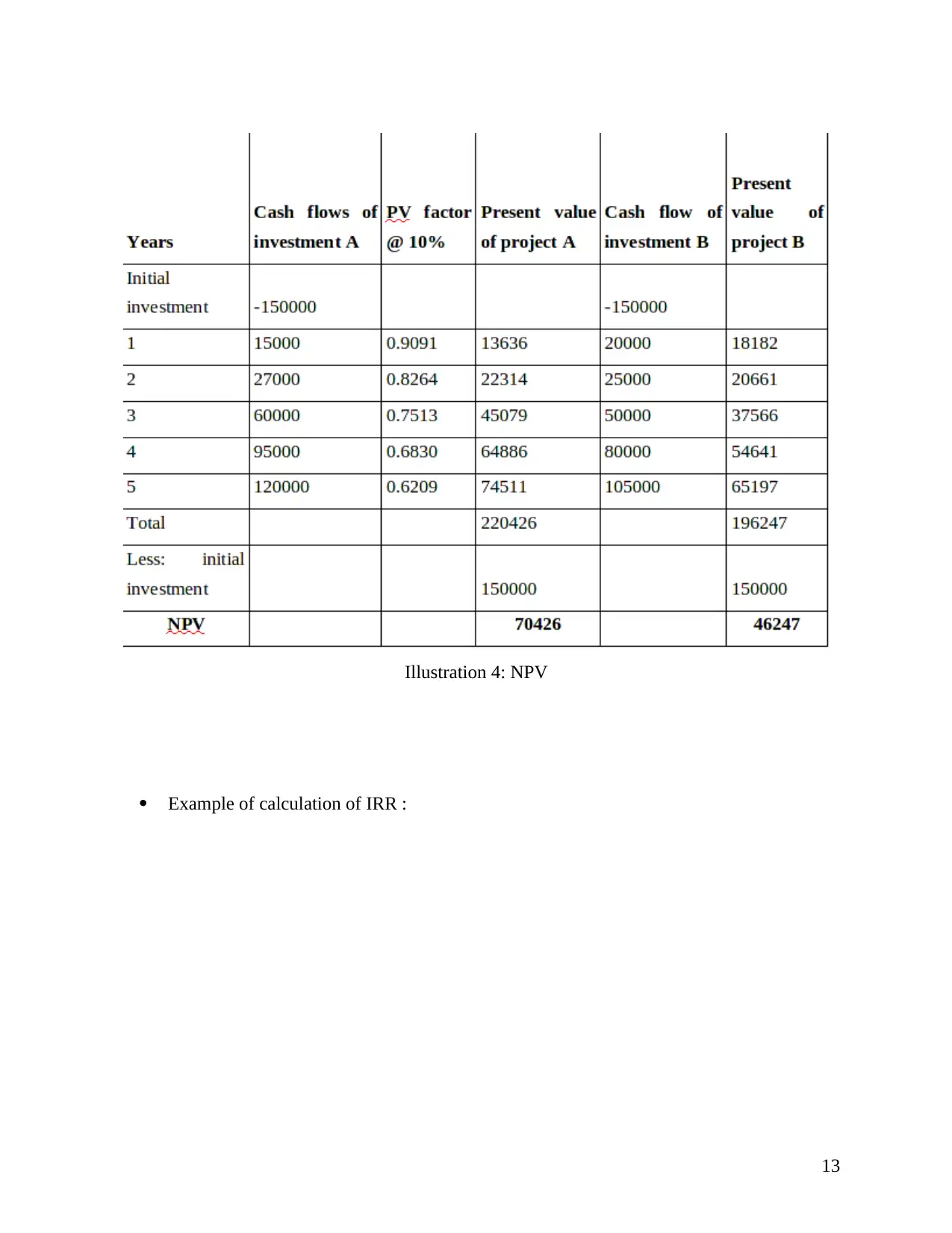

Capital Budgeting Techniques :

Capital budgeting is a planning that is used by cited organisation for making effective

decision related to investment so that company chooses most viable projects that has low risk

and higher returns (Strumickas and Valanciene, 2015). For this evaluation, various methods are

available – net present value, internal rate of return etc.

Example of calculation of NPV :

12

– production, administration, selling and

distribution.

The basis of classification of overheads is fixed

cost and variable costs.

Net profit is relatively low under absorption

costing as it considers all the costs and

expenses.

Net profit is higher as compared to other

methods because all costs are not taken into

account under this method.

TASK 3

P4 Different types of planning tools used for budgetary control with their advantages and

limitations

For maintaining control over disposals, management uses various types of budgetary

control techniques. The three major techniques used by R.L. Mynard Ltd. are capital budgeting

techniques, preparation of budget and ratio analysis. These three methods long with their benefits

and limitations are explained as follows :

Capital Budgeting Techniques :

Capital budgeting is a planning that is used by cited organisation for making effective

decision related to investment so that company chooses most viable projects that has low risk

and higher returns (Strumickas and Valanciene, 2015). For this evaluation, various methods are

available – net present value, internal rate of return etc.

Example of calculation of NPV :

12

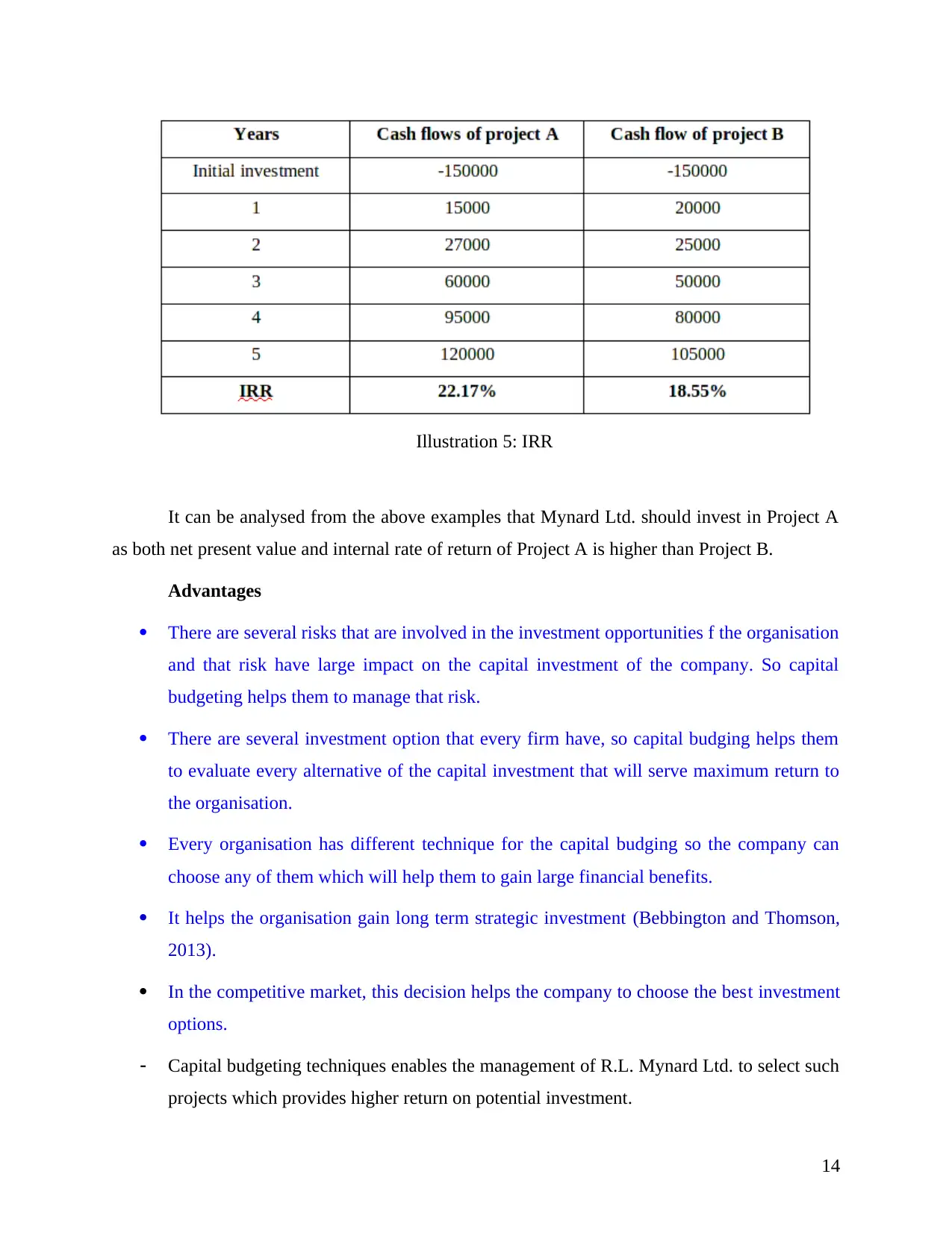

Example of calculation of IRR :

13

Illustration 4: NPV

13

Illustration 4: NPV

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

It can be analysed from the above examples that Mynard Ltd. should invest in Project A

as both net present value and internal rate of return of Project A is higher than Project B.

Advantages

There are several risks that are involved in the investment opportunities f the organisation

and that risk have large impact on the capital investment of the company. So capital

budgeting helps them to manage that risk.

There are several investment option that every firm have, so capital budging helps them

to evaluate every alternative of the capital investment that will serve maximum return to

the organisation.

Every organisation has different technique for the capital budging so the company can

choose any of them which will help them to gain large financial benefits.

It helps the organisation gain long term strategic investment (Bebbington and Thomson,

2013).

In the competitive market, this decision helps the company to choose the best investment

options.

Capital budgeting techniques enables the management of R.L. Mynard Ltd. to select such

projects which provides higher return on potential investment.

14

Illustration 5: IRR

as both net present value and internal rate of return of Project A is higher than Project B.

Advantages

There are several risks that are involved in the investment opportunities f the organisation

and that risk have large impact on the capital investment of the company. So capital

budgeting helps them to manage that risk.

There are several investment option that every firm have, so capital budging helps them

to evaluate every alternative of the capital investment that will serve maximum return to

the organisation.

Every organisation has different technique for the capital budging so the company can

choose any of them which will help them to gain large financial benefits.

It helps the organisation gain long term strategic investment (Bebbington and Thomson,

2013).

In the competitive market, this decision helps the company to choose the best investment

options.

Capital budgeting techniques enables the management of R.L. Mynard Ltd. to select such

projects which provides higher return on potential investment.

14

Illustration 5: IRR

It helps in effective decision-making as the concept of cost of capital as well as time

value of money are both considered in this method (Taipaleenmäki and Ikäheimo, 2013).

This technique helps in ascertaining profitability and viability of different projects and

helps to select better one from two mutually exclusive projects.

It is simple to understand as calculations are not complex and lengthy.

It provides better control over the financial instruments so that they can show the exact

position of company in target market(Schäffer, 2013). Further this can be helpful for

stakeholder during decision making as well as it also assist managerial personnels in

taking decisions regarding organisational structure and operations.

This can also helpful in determination of goal and purpose of entity. Further it also shows

them a way to achieve those targets.

Strategies which are made by management in a way to run the business and operating,

financing and investing activities of a firm smoothly and efficiently can easily executed

by them.

Budgetary control techniques assist an entity to set targets which are easily

attainable(Sisaye and Birnberg, 2010). Attainability of targets can be assured by

quantifying them and these planning tools quantify the targets hence they can be achieved

by an entity.

Personal development of workers is there as they works in way to gain profitability in

this way they enhances there capability which allow them to develop their skills and

competencies (Otley, 2016).

Finance and funding with their management gets easy through planning tools.

R.L.Maynard can perfectly exploit its financial resources so that they can generate

healthier results.

Disadvantages

As this technique is based on the future prediction and investment, sometimes it is very

difficult for the organisation to make decision related to the uncertainty.

Capital budgeting will always remain the introspective with that rest and discounting

factor will remain subject so the manager perception is very difficult to analyse (van ,

2011).

15

value of money are both considered in this method (Taipaleenmäki and Ikäheimo, 2013).

This technique helps in ascertaining profitability and viability of different projects and

helps to select better one from two mutually exclusive projects.

It is simple to understand as calculations are not complex and lengthy.

It provides better control over the financial instruments so that they can show the exact

position of company in target market(Schäffer, 2013). Further this can be helpful for

stakeholder during decision making as well as it also assist managerial personnels in

taking decisions regarding organisational structure and operations.

This can also helpful in determination of goal and purpose of entity. Further it also shows

them a way to achieve those targets.

Strategies which are made by management in a way to run the business and operating,

financing and investing activities of a firm smoothly and efficiently can easily executed

by them.

Budgetary control techniques assist an entity to set targets which are easily

attainable(Sisaye and Birnberg, 2010). Attainability of targets can be assured by

quantifying them and these planning tools quantify the targets hence they can be achieved

by an entity.

Personal development of workers is there as they works in way to gain profitability in

this way they enhances there capability which allow them to develop their skills and

competencies (Otley, 2016).

Finance and funding with their management gets easy through planning tools.

R.L.Maynard can perfectly exploit its financial resources so that they can generate

healthier results.

Disadvantages

As this technique is based on the future prediction and investment, sometimes it is very

difficult for the organisation to make decision related to the uncertainty.

Capital budgeting will always remain the introspective with that rest and discounting

factor will remain subject so the manager perception is very difficult to analyse (van ,

2011).

15

If the organisation have taken the wrong capital budgeting decision so that will affect

them in the long term so it is necessary for the company to understand their investment

project.

For application of this technique, skilled employees are needed who have understanding

of financial terms.

It might be time consuming at times as calculations in certain methods like payback

period and average rate of return are huge and complex.

Proper execution of strategies becomes tough when situation changes. As future is

dynamic and unpredictable as circumstances are keeps on changing everyday. Hence

strategies should be flexible so that if situation changes then mangers and supervisors of

various departments can easily mould the strategies which suits best on the condition. But

the strategies which are made through the planning tools of budgetary control cannot be

moulded as per the situation as they are fixed or rigid in nature. As a result better results

cannot be extracted out of processes in case of change in scenario.

There may be a chance when supervisors of different departments shows the estimated

expenditures on high level which clearly shows that they want to avoid the situation of

over expenditure (Stergiou, Ashraf and Uddin, 2013). In that case, organisation will not

be able to clearly understand their financial position and their rate of over expenditure.

Cash budgeting: This budgetary control system is effective for cash management and proper

costing on business operations of R.L.Maynard. However, decisions are made regarding cost

incurred on production and supplement of its products and services. Its advantages and

drawbacks can be understood as:

Advantages:

Cash management is possible appropriately for management of further business

operations.

Different ideas are generated for reducing expenses and increasing sales revenue of

R.L.Maynard.

Preparing this budget is able for effective price determination and enhancing profitability

of the enterprise.

16

them in the long term so it is necessary for the company to understand their investment

project.

For application of this technique, skilled employees are needed who have understanding

of financial terms.

It might be time consuming at times as calculations in certain methods like payback

period and average rate of return are huge and complex.

Proper execution of strategies becomes tough when situation changes. As future is

dynamic and unpredictable as circumstances are keeps on changing everyday. Hence

strategies should be flexible so that if situation changes then mangers and supervisors of

various departments can easily mould the strategies which suits best on the condition. But

the strategies which are made through the planning tools of budgetary control cannot be

moulded as per the situation as they are fixed or rigid in nature. As a result better results

cannot be extracted out of processes in case of change in scenario.

There may be a chance when supervisors of different departments shows the estimated

expenditures on high level which clearly shows that they want to avoid the situation of

over expenditure (Stergiou, Ashraf and Uddin, 2013). In that case, organisation will not

be able to clearly understand their financial position and their rate of over expenditure.

Cash budgeting: This budgetary control system is effective for cash management and proper

costing on business operations of R.L.Maynard. However, decisions are made regarding cost

incurred on production and supplement of its products and services. Its advantages and

drawbacks can be understood as:

Advantages:

Cash management is possible appropriately for management of further business

operations.

Different ideas are generated for reducing expenses and increasing sales revenue of

R.L.Maynard.

Preparing this budget is able for effective price determination and enhancing profitability

of the enterprise.

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Drawbacks:

Estimation on cash regarding business operations remain unable for proper management

and further operations for R.L.Maynard.

Due to changes in market price, it is difficult to set cost for incurred on each business

operations.

Fixed budget:

Under this budgetary control system, all set strategies are not change with according to changes

in market price. However, planning for incurred cost5 on business operations remain same for

R.L.Maynard. In this regard, critical evaluation on fixed budget can be understood as:

Advantages:

Activities are implemented as determined for project and task accomplishments.

Work segmentation among workers is also done on the basis of prepared strategies for

team building and achieving the goals.

Drawbacks

No flexibility in business operation remains unable for project management and

managing business operations.

It remains unfavourable for effectiveness of R.L.Maynard and further business

operations.

TASK 4

P5) Significance of management accounting systems in financial development of R.L.Maynard

Different organisations use the different methods of the management accounting to

understand the clear vision of the organisation's financial position. Today in the dynamic

environment it is very essential to integrate the social and environmental factors in the financial

planning process to achieve the desire goals as R.L.Maynard have appointed the management

accountant to develop and implement the effective financial planning process to grab the

demands of the clients in the market and analyse the financial position of the organisation

17

Estimation on cash regarding business operations remain unable for proper management

and further operations for R.L.Maynard.

Due to changes in market price, it is difficult to set cost for incurred on each business

operations.

Fixed budget:

Under this budgetary control system, all set strategies are not change with according to changes

in market price. However, planning for incurred cost5 on business operations remain same for

R.L.Maynard. In this regard, critical evaluation on fixed budget can be understood as:

Advantages:

Activities are implemented as determined for project and task accomplishments.

Work segmentation among workers is also done on the basis of prepared strategies for

team building and achieving the goals.

Drawbacks

No flexibility in business operation remains unable for project management and

managing business operations.

It remains unfavourable for effectiveness of R.L.Maynard and further business

operations.

TASK 4

P5) Significance of management accounting systems in financial development of R.L.Maynard

Different organisations use the different methods of the management accounting to

understand the clear vision of the organisation's financial position. Today in the dynamic

environment it is very essential to integrate the social and environmental factors in the financial

planning process to achieve the desire goals as R.L.Maynard have appointed the management

accountant to develop and implement the effective financial planning process to grab the

demands of the clients in the market and analyse the financial position of the organisation

17

through various management accounting techniques IRR and NPV to decide the profitability and

feasibility of the decision need to be taken because every new project requires the high

expenditure on the research, development of the product and its marketing thus the pre analysis

of the feasibility of the project through the management accounting technique is very essential.

This helps to utilize the available limited resources since R.L.Maynard is the small business

venture thus it can't take any risk to develop a new plan and then back off after the poor results.

This poor results could also lead to company's bankruptcy (Schäffer, 2013). R.L.Maynard is

dealing with the large organisations to provide them the management operations so since they are

delivering their services to the they need to be very keen about financial planning process to

attain their goal to achieve their ultimate results. The other competitor of the R.L.Maynard is

using the Budgetary techniques to achieve their results. Here the management prepares the

budget as per the results of the previous year and thus this method help the organisation to

calculate the variances and take effective steps to eliminate these variances and achieve the

desired standards. Here, the estimated budget is based on the actual expenses of prior years

thus any changes in the cost in the current year leads to the variances. This is the effective

method to plan the effective allocation and utilization of the available resources in the

organisation. Thus, this method facilitate the continuous control on the operations performed in

the organisation. These budgets are the warning signs for the organisation that appropriate

actions are required. But, since the budgets are based on the future prospects and it is not

possible to predict the future accurately thus errors and inaccuracies are possible (Schaltegger,

Gibassier, and Zvezdov, 2013).

Management accounting systems play crucial role in reducing financial issue of

R.L.Maynard can be understood as below:

Financial accounting system: In this process system, management accountant analyses

economic position of entity using financial statements and notes. Therefore, ideas are

generated for redcuing expenditures and increasing sales revenue ((Stergiou, Ashraf and

Uddin, 2013). It influences profitability of R.L.Maynard and further business operations.

Thus, financial accounting system plays crucial role in decreasing issues and increasing

monetary position of the enterprise efficiently.

Cost accounting system: Under this process, different ideas are generated for cost

effectiveness and increasing sales revenue of R.L.Maynard. Therefore, financial

18

feasibility of the decision need to be taken because every new project requires the high

expenditure on the research, development of the product and its marketing thus the pre analysis

of the feasibility of the project through the management accounting technique is very essential.

This helps to utilize the available limited resources since R.L.Maynard is the small business

venture thus it can't take any risk to develop a new plan and then back off after the poor results.

This poor results could also lead to company's bankruptcy (Schäffer, 2013). R.L.Maynard is

dealing with the large organisations to provide them the management operations so since they are

delivering their services to the they need to be very keen about financial planning process to

attain their goal to achieve their ultimate results. The other competitor of the R.L.Maynard is

using the Budgetary techniques to achieve their results. Here the management prepares the

budget as per the results of the previous year and thus this method help the organisation to

calculate the variances and take effective steps to eliminate these variances and achieve the

desired standards. Here, the estimated budget is based on the actual expenses of prior years

thus any changes in the cost in the current year leads to the variances. This is the effective

method to plan the effective allocation and utilization of the available resources in the

organisation. Thus, this method facilitate the continuous control on the operations performed in

the organisation. These budgets are the warning signs for the organisation that appropriate

actions are required. But, since the budgets are based on the future prospects and it is not

possible to predict the future accurately thus errors and inaccuracies are possible (Schaltegger,

Gibassier, and Zvezdov, 2013).

Management accounting systems play crucial role in reducing financial issue of

R.L.Maynard can be understood as below:

Financial accounting system: In this process system, management accountant analyses

economic position of entity using financial statements and notes. Therefore, ideas are

generated for redcuing expenditures and increasing sales revenue ((Stergiou, Ashraf and

Uddin, 2013). It influences profitability of R.L.Maynard and further business operations.

Thus, financial accounting system plays crucial role in decreasing issues and increasing

monetary position of the enterprise efficiently.

Cost accounting system: Under this process, different ideas are generated for cost

effectiveness and increasing sales revenue of R.L.Maynard. Therefore, financial

18

development of enterprise is possible by using this system and implementing strategies

regarding business activities in the future time (Otley, 2016).

Thus, R.L.Maynard is using more efficient management accounting system to have the clear

vision of the market opportunities to achieve the desired goals more effectively. This is the

Product or service quality:

Growth levels

Output per employee performance Liquidity level or return on investment: Reason R.L.Maynard is growing rapidly in the

market and various big corporate firms are joining it, as it quickly sense the market

demand and swiftly act on it.

Budgeting

In order to make successful results in the organisation, financial system assists to arrange

fund and money for enhance operations in different areas. It assists to make plan and operations

according to the system of company. In this process, plan has been created which assists to spend

more money and attain growth within the enterprise.

Targeting

Targeting is the area in which business promote their productivity and performance to

ascertain profitability at workplace. As results, they are taking specific area in which promotion

is needed for accomplish objectives and goals.

Benchmarking

In this way, every organisation attain positive results through evaluate their performances

with other enterprise. It gives particular results which device to make comparison for ascertain

positive performances. Dimensions are very typical to make positive results and performances.

In this aspect, the organisation can take their system and compare it with another businesses. KPI

is the best element which assists to indicate key performance to measure their performances of

different activities. National key performances indicators measure simply set targets and goals as

per the view of company structure so that it would be beneficial to assess national performances

data.

Product or service quality: Management accounting systems help in maintaining and

improving the product or service quality. When company will be able to utilise resources

19

regarding business activities in the future time (Otley, 2016).

Thus, R.L.Maynard is using more efficient management accounting system to have the clear

vision of the market opportunities to achieve the desired goals more effectively. This is the

Product or service quality:

Growth levels

Output per employee performance Liquidity level or return on investment: Reason R.L.Maynard is growing rapidly in the

market and various big corporate firms are joining it, as it quickly sense the market

demand and swiftly act on it.

Budgeting

In order to make successful results in the organisation, financial system assists to arrange

fund and money for enhance operations in different areas. It assists to make plan and operations

according to the system of company. In this process, plan has been created which assists to spend

more money and attain growth within the enterprise.

Targeting

Targeting is the area in which business promote their productivity and performance to

ascertain profitability at workplace. As results, they are taking specific area in which promotion

is needed for accomplish objectives and goals.

Benchmarking

In this way, every organisation attain positive results through evaluate their performances

with other enterprise. It gives particular results which device to make comparison for ascertain

positive performances. Dimensions are very typical to make positive results and performances.

In this aspect, the organisation can take their system and compare it with another businesses. KPI

is the best element which assists to indicate key performance to measure their performances of

different activities. National key performances indicators measure simply set targets and goals as

per the view of company structure so that it would be beneficial to assess national performances

data.

Product or service quality: Management accounting systems help in maintaining and

improving the product or service quality. When company will be able to utilise resources

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

effectively then cost of production is decreased and more emphasis is given to quality. This

automatically helps in improving customer satisfaction levels.

Growth levels: R. L. Maynard can reach higher growth levels when there is scope of

improvement and effective change management is implemented. It is important to understand

and analyse the opportunities which can be used for enhancing growth and development.

Output per employee performance : Performance is not just limited to the organisation

but also impacting employees. The human resource is the most important component that

contributes to productivity and profitability. When certain strategic systems are implemented by

the company then output per employee can be estimated and respective performance can be

evaluated.

Liquidity level or return on investment: Liquidity is the degree which estimates the

extent upto which an asset can be sold or bought immediately from the market or in the market

without affecting the actual price. Organisation's capabilities of utilising the assets is determined

in liquidity. On the other hand, return on investment is a kind of performance measure which

helps in understanding the efficiency of the organisation after making an investment. The

benefits are estimated in terms of ratios or percentages.

CONCLUSION

The above report signifies that R.L.Maynard is the small business venture that have used

the Financial planning technique to achieve the desire goals in the market and sustain long in the

same. This report also contains the various management accounting techniques which the

different organisation use to analyse their financial position and take the long term and short

term decisions as basic functions. For example Manufacturing companies uses the inventory and

manufacturing report and the cost report to strengthen their position and pharmaceutical

companies use Batch Costing method. This report also specify the various budgetary control

techniques and their advantages and disadvantages. This report also includes comparison of the

R.L.Mayanrd with its competitor to explain the difference between the two management

accounting methods and their effects on both the organisation.

20

automatically helps in improving customer satisfaction levels.

Growth levels: R. L. Maynard can reach higher growth levels when there is scope of

improvement and effective change management is implemented. It is important to understand

and analyse the opportunities which can be used for enhancing growth and development.

Output per employee performance : Performance is not just limited to the organisation

but also impacting employees. The human resource is the most important component that

contributes to productivity and profitability. When certain strategic systems are implemented by

the company then output per employee can be estimated and respective performance can be

evaluated.

Liquidity level or return on investment: Liquidity is the degree which estimates the

extent upto which an asset can be sold or bought immediately from the market or in the market

without affecting the actual price. Organisation's capabilities of utilising the assets is determined

in liquidity. On the other hand, return on investment is a kind of performance measure which