Comprehensive Budgetary Forecast Report: Cardiff Central Hotel

VerifiedAdded on 2023/01/07

|12

|2788

|51

Report

AI Summary

This report presents a detailed analysis of budgetary forecasts for the Cardiff Central Hotel, encompassing both cash and profit budgets. The cash budget meticulously outlines the anticipated inflow and outflow of cash over a specified period, revealing the hotel's liquidity and financial health. The report highlights the steady rise in net room sales, influenced by the hotel's position within the tourism sector, and identifies fixed and variable expenses. Furthermore, the profit budget forecast projects the hotel's profitability by comparing revenue streams against expenses. The analysis indicates a positive financial outlook, with increasing sales and well-managed expenses. The report provides valuable insights into the hotel's financial management, supporting informed decision-making for future strategic planning and investment opportunities.

BUDGETARY FORECASTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Cash Budget.................................................................................................................................3

TASK 2............................................................................................................................................7

Profit Budget Forecast.................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Cash Budget.................................................................................................................................3

TASK 2............................................................................................................................................7

Profit Budget Forecast.................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Budgetary forecasts are a key in the overall management of the financial capacities in an organisation and the overall utilisation of the

finances that are available (DeFranco and Schmidgall, 2020). The budgetary forecasts help in overall maintenance of the inflow as

well as outflow of the cash and the overall expenses that are taking place in an organisation. In this report, a cash budget will be

prepared for the Cardiff Central hotel which will detail all the potential sources of income and expense and all also the net balance that

is available in the organisation (DeFranco and Schmidgall, 2017). Further the report will also identify the profit budget forecasts for

the company so that value of estimated profits can be ascertained for the organisation.

MAIN BODY

TASK 1

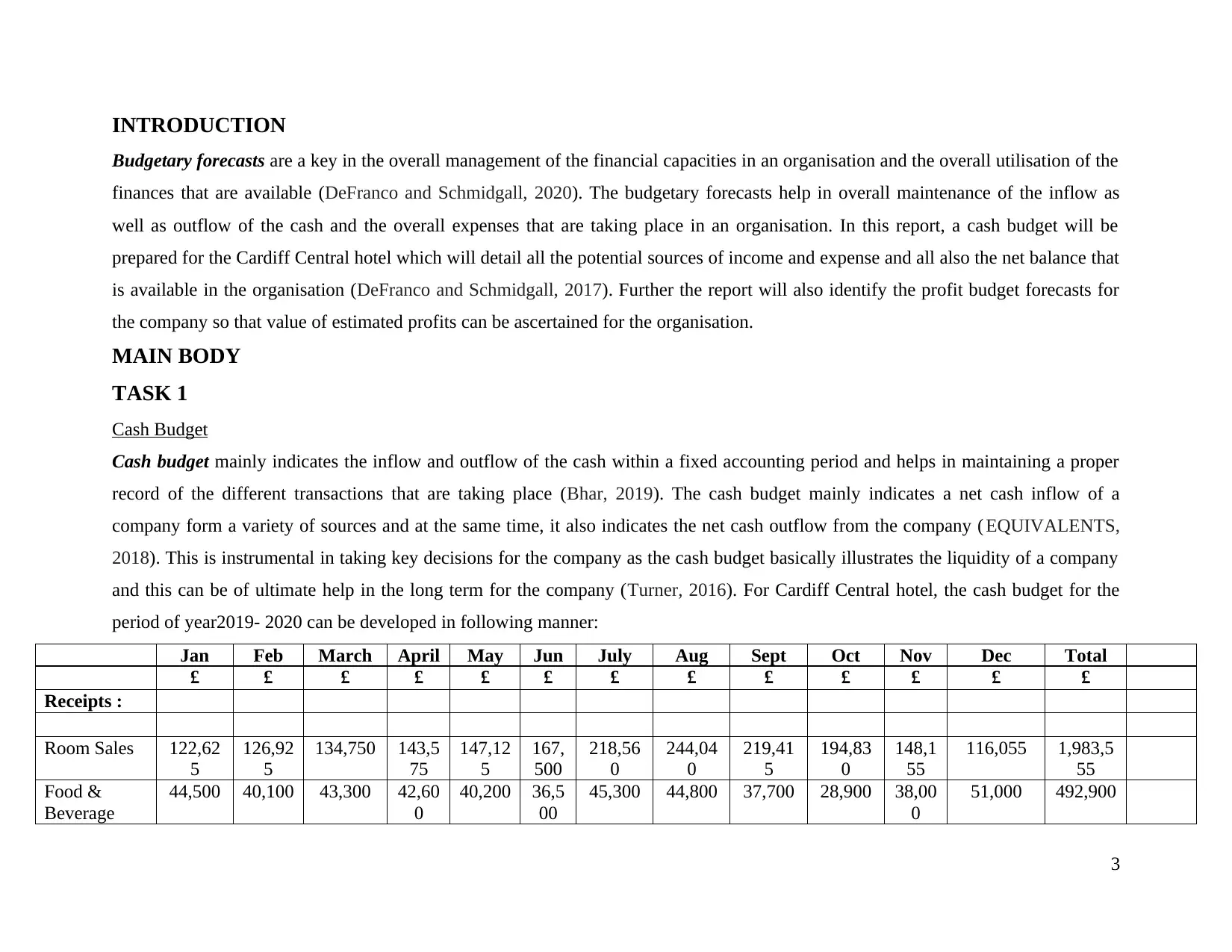

Cash Budget

Cash budget mainly indicates the inflow and outflow of the cash within a fixed accounting period and helps in maintaining a proper

record of the different transactions that are taking place (Bhar, 2019). The cash budget mainly indicates a net cash inflow of a

company form a variety of sources and at the same time, it also indicates the net cash outflow from the company ( EQUIVALENTS,

2018). This is instrumental in taking key decisions for the company as the cash budget basically illustrates the liquidity of a company

and this can be of ultimate help in the long term for the company (Turner, 2016). For Cardiff Central hotel, the cash budget for the

period of year2019- 2020 can be developed in following manner:

Jan Feb March April May Jun July Aug Sept Oct Nov Dec Total

£ £ £ £ £ £ £ £ £ £ £ £ £

Receipts :

Room Sales 122,62

5

126,92

5

134,750 143,5

75

147,12

5

167,

500

218,56

0

244,04

0

219,41

5

194,83

0

148,1

55

116,055 1,983,5

55

Food &

Beverage

44,500 40,100 43,300 42,60

0

40,200 36,5

00

45,300 44,800 37,700 28,900 38,00

0

51,000 492,900

3

Budgetary forecasts are a key in the overall management of the financial capacities in an organisation and the overall utilisation of the

finances that are available (DeFranco and Schmidgall, 2020). The budgetary forecasts help in overall maintenance of the inflow as

well as outflow of the cash and the overall expenses that are taking place in an organisation. In this report, a cash budget will be

prepared for the Cardiff Central hotel which will detail all the potential sources of income and expense and all also the net balance that

is available in the organisation (DeFranco and Schmidgall, 2017). Further the report will also identify the profit budget forecasts for

the company so that value of estimated profits can be ascertained for the organisation.

MAIN BODY

TASK 1

Cash Budget

Cash budget mainly indicates the inflow and outflow of the cash within a fixed accounting period and helps in maintaining a proper

record of the different transactions that are taking place (Bhar, 2019). The cash budget mainly indicates a net cash inflow of a

company form a variety of sources and at the same time, it also indicates the net cash outflow from the company ( EQUIVALENTS,

2018). This is instrumental in taking key decisions for the company as the cash budget basically illustrates the liquidity of a company

and this can be of ultimate help in the long term for the company (Turner, 2016). For Cardiff Central hotel, the cash budget for the

period of year2019- 2020 can be developed in following manner:

Jan Feb March April May Jun July Aug Sept Oct Nov Dec Total

£ £ £ £ £ £ £ £ £ £ £ £ £

Receipts :

Room Sales 122,62

5

126,92

5

134,750 143,5

75

147,12

5

167,

500

218,56

0

244,04

0

219,41

5

194,83

0

148,1

55

116,055 1,983,5

55

Food &

Beverage

44,500 40,100 43,300 42,60

0

40,200 36,5

00

45,300 44,800 37,700 28,900 38,00

0

51,000 492,900

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rent 950 950 950 950 950 950 950 950 950 950 950 950 11,400

Commission 25 55 20 15 10 40 25 35 30 45 50 35 385

Total

Receipts

168,10

0

168,03

0

179,020 187,1

40

188,28

5

204,

990

264,83

5

289,82

5

258,09

5

224,72

5

187,1

55

168,040 2,488,2

40

Payments :

Laundry 6,250 6,250 6,250 6,250 6,25

0

6,250 6,250 6,250 6,250 6,250 6,250 68,750

Rates 21,66

8

5,417 5,41

7

5,417 5,417 5,417 5,417 5,417 5,417 65,004

Printing and

stationary

2,000 2,000 2,000 2,000 2,900 2,00

0

2,000 2,000 2,000 2,000 2,900 2,000 25,800

Wages 11,667 11,667 11,667 11,66

7

11,667 11,6

67

11,667 11,667 11,667 11,667 11,66

7

11,667 140,000

Toiletries 46,000 46,000

Salaries 110,

000

110,000 220,000

Marketing

cost

60,0

00

60,000

Lighting and

heating

27,500 27,5

00

27,500 27,500 110,000

Payment

towards

suppliers

0 2,000 12,300 2,000 16,400 2,00

0

2,750 2,000 2,000 3,500 2,000 2,000 48,950

Petrol &

diesel

1,000 1,000 1,000 1,000 1,000 1,00

0

1,000 1,000 1,000 1,000 1,000 1,000 12,000

Restaurant

Improvements

8,800 22,0

00

13,200 44,000

Van 28,000 28,000

4

Commission 25 55 20 15 10 40 25 35 30 45 50 35 385

Total

Receipts

168,10

0

168,03

0

179,020 187,1

40

188,28

5

204,

990

264,83

5

289,82

5

258,09

5

224,72

5

187,1

55

168,040 2,488,2

40

Payments :

Laundry 6,250 6,250 6,250 6,250 6,25

0

6,250 6,250 6,250 6,250 6,250 6,250 68,750

Rates 21,66

8

5,417 5,41

7

5,417 5,417 5,417 5,417 5,417 5,417 65,004

Printing and

stationary

2,000 2,000 2,000 2,000 2,900 2,00

0

2,000 2,000 2,000 2,000 2,900 2,000 25,800

Wages 11,667 11,667 11,667 11,66

7

11,667 11,6

67

11,667 11,667 11,667 11,667 11,66

7

11,667 140,000

Toiletries 46,000 46,000

Salaries 110,

000

110,000 220,000

Marketing

cost

60,0

00

60,000

Lighting and

heating

27,500 27,5

00

27,500 27,500 110,000

Payment

towards

suppliers

0 2,000 12,300 2,000 16,400 2,00

0

2,750 2,000 2,000 3,500 2,000 2,000 48,950

Petrol &

diesel

1,000 1,000 1,000 1,000 1,000 1,00

0

1,000 1,000 1,000 1,000 1,000 1,000 12,000

Restaurant

Improvements

8,800 22,0

00

13,200 44,000

Van 28,000 28,000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

General

Maintenance

charges

5,000 5,000 5,000 5,000 5,000 5,00

0

5,000 5,000 5,000 5,000 5,000 5,000 60,000

Total

payments

19,667 73,917 102,517 49,58

4

48,634 252,

834

34,084 46,534 60,834 34,834 34,23

4

170,834 928,504

Balance b / f 265,00

0

413,43

3

507,547 584,0

50

721,60

6

861,

257

813,41

3

1,044,1

65

1,287,4

56

1,484,7

17

1,674

,609

1,827,530 1,824,7

36

Net cash

flow in

month

148,43

3

94,113 76,503 137,5

56

139,65

1

(47,8

44)

230,75

1

243,29

1

197,26

1

189,89

1

152,9

21

(2,794) 1,559,7

36

Balance c / f 413,43

3

507,54

7

584,050 721,6

06

861,25

7

813,

413

1,044,1

65

1,287,4

56

1,484,7

17

1,674,6

09

1,827

,530

1,824,736 3,384,4

73

CALCULATION

Nov Dec Jan Febr

uary

Marc

h

Apri

l

May June July August Sept Oct Nov Dec

Room sales 123000 10800

0

130,500 125,0

00

140,00

0

145,

500

148,00

0

178,00

0

240,40

0

246,00

0

205,1

00

189,300 126,000 110,70

0

Food &

beverage

36000 47000 44,500 40,10

0

43,300 42,6

00

40,200 36,500 45,300 44,800 37,70

0

28,900 38,000 51,000

Rent 950 950 950 950 950 950 950 950 950 950 950 950 950 950

Commission 120 15 25 55 20 15 10 40 25 35 30 45 50 35

Room Sales

Business 37800 4567 43750 4900 50925 51800 62300 84140 8610 71785 66255 44100

5

Maintenance

charges

5,000 5,000 5,000 5,000 5,000 5,00

0

5,000 5,000 5,000 5,000 5,000 5,000 60,000

Total

payments

19,667 73,917 102,517 49,58

4

48,634 252,

834

34,084 46,534 60,834 34,834 34,23

4

170,834 928,504

Balance b / f 265,00

0

413,43

3

507,547 584,0

50

721,60

6

861,

257

813,41

3

1,044,1

65

1,287,4

56

1,484,7

17

1,674

,609

1,827,530 1,824,7

36

Net cash

flow in

month

148,43

3

94,113 76,503 137,5

56

139,65

1

(47,8

44)

230,75

1

243,29

1

197,26

1

189,89

1

152,9

21

(2,794) 1,559,7

36

Balance c / f 413,43

3

507,54

7

584,050 721,6

06

861,25

7

813,

413

1,044,1

65

1,287,4

56

1,484,7

17

1,674,6

09

1,827

,530

1,824,736 3,384,4

73

CALCULATION

Nov Dec Jan Febr

uary

Marc

h

Apri

l

May June July August Sept Oct Nov Dec

Room sales 123000 10800

0

130,500 125,0

00

140,00

0

145,

500

148,00

0

178,00

0

240,40

0

246,00

0

205,1

00

189,300 126,000 110,70

0

Food &

beverage

36000 47000 44,500 40,10

0

43,300 42,6

00

40,200 36,500 45,300 44,800 37,70

0

28,900 38,000 51,000

Rent 950 950 950 950 950 950 950 950 950 950 950 950 950 950

Commission 120 15 25 55 20 15 10 40 25 35 30 45 50 35

Room Sales

Business 37800 4567 43750 4900 50925 51800 62300 84140 8610 71785 66255 44100

5

concerns

35%

5 0 0

Individuals 84825 8125

0

91000 9457

5

96200 115700 156260 159900 1333

15

123045 81900 71955

Collection

from sales

122625 1269

25

13475

0

1435

75

147125 167500 218560 244040 2194

15

194830 148155 11605

5

Payment to

Suppliers

Jan Feb Mar Apri

l

May June July Aug Sept Oct Nov Dec

In room

beverages

2000 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Kettle trays 1500

Bedding

bundles

700 750

Complimenta

ry items

9600 14400

Total 0 2000 12300 2000 16400 2000 2750 2000 2000 3500 2000 2000

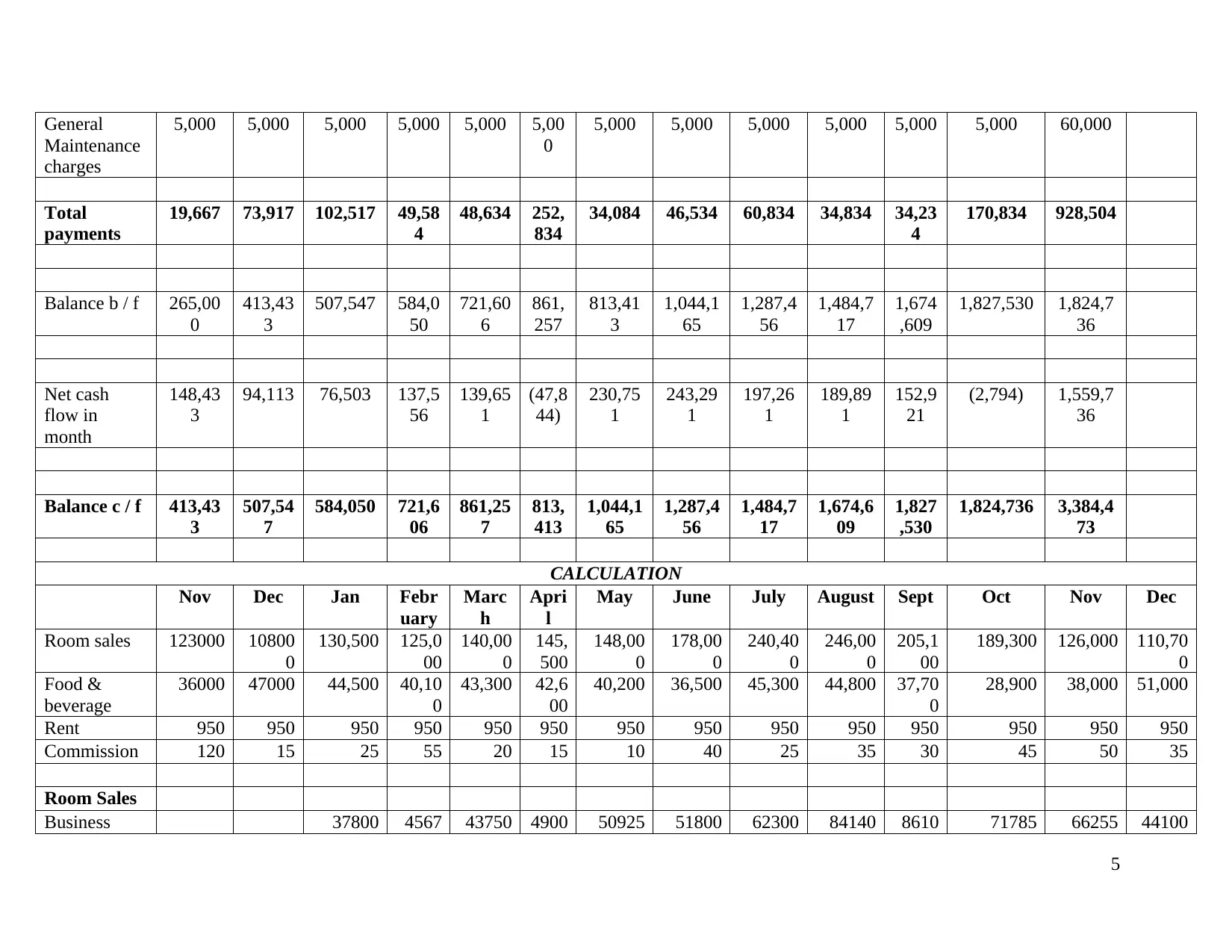

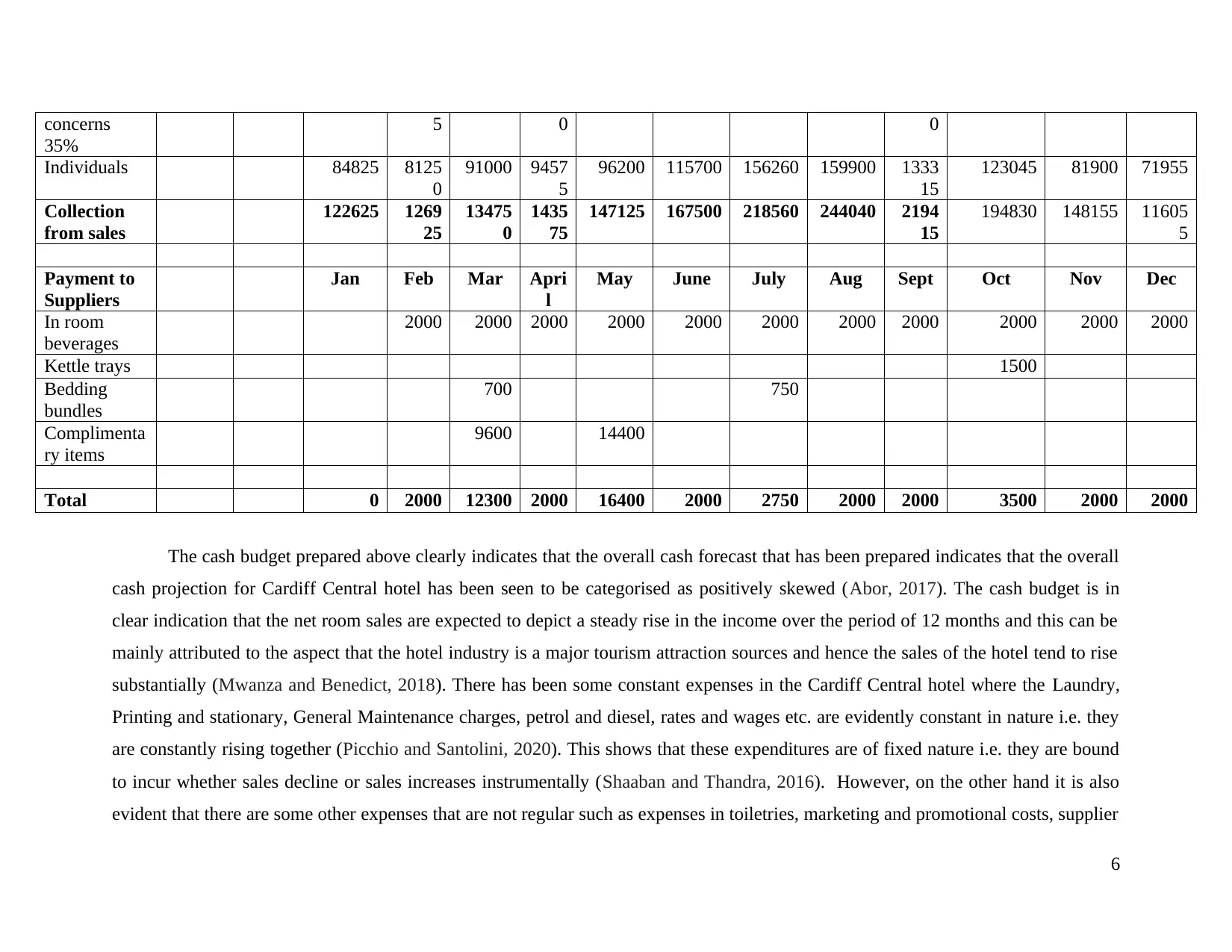

The cash budget prepared above clearly indicates that the overall cash forecast that has been prepared indicates that the overall

cash projection for Cardiff Central hotel has been seen to be categorised as positively skewed (Abor, 2017). The cash budget is in

clear indication that the net room sales are expected to depict a steady rise in the income over the period of 12 months and this can be

mainly attributed to the aspect that the hotel industry is a major tourism attraction sources and hence the sales of the hotel tend to rise

substantially (Mwanza and Benedict, 2018). There has been some constant expenses in the Cardiff Central hotel where the Laundry,

Printing and stationary, General Maintenance charges, petrol and diesel, rates and wages etc. are evidently constant in nature i.e. they

are constantly rising together (Picchio and Santolini, 2020). This shows that these expenditures are of fixed nature i.e. they are bound

to incur whether sales decline or sales increases instrumentally (Shaaban and Thandra, 2016). However, on the other hand it is also

evident that there are some other expenses that are not regular such as expenses in toiletries, marketing and promotional costs, supplier

6

35%

5 0 0

Individuals 84825 8125

0

91000 9457

5

96200 115700 156260 159900 1333

15

123045 81900 71955

Collection

from sales

122625 1269

25

13475

0

1435

75

147125 167500 218560 244040 2194

15

194830 148155 11605

5

Payment to

Suppliers

Jan Feb Mar Apri

l

May June July Aug Sept Oct Nov Dec

In room

beverages

2000 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Kettle trays 1500

Bedding

bundles

700 750

Complimenta

ry items

9600 14400

Total 0 2000 12300 2000 16400 2000 2750 2000 2000 3500 2000 2000

The cash budget prepared above clearly indicates that the overall cash forecast that has been prepared indicates that the overall

cash projection for Cardiff Central hotel has been seen to be categorised as positively skewed (Abor, 2017). The cash budget is in

clear indication that the net room sales are expected to depict a steady rise in the income over the period of 12 months and this can be

mainly attributed to the aspect that the hotel industry is a major tourism attraction sources and hence the sales of the hotel tend to rise

substantially (Mwanza and Benedict, 2018). There has been some constant expenses in the Cardiff Central hotel where the Laundry,

Printing and stationary, General Maintenance charges, petrol and diesel, rates and wages etc. are evidently constant in nature i.e. they

are constantly rising together (Picchio and Santolini, 2020). This shows that these expenditures are of fixed nature i.e. they are bound

to incur whether sales decline or sales increases instrumentally (Shaaban and Thandra, 2016). However, on the other hand it is also

evident that there are some other expenses that are not regular such as expenses in toiletries, marketing and promotional costs, supplier

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

payments, investment in restaurant improvements, investment in fixed assets such as van etc. these are of occasional nature and the

hotel tends to incur them only when they are in a good profitable situation collectively (Zietlow, 2020).

Apart from this, the prepared cash budget also indicates that the cash net flow for Cardiff Central Hotel seems to be constantly

raising till the month of November where it reaches the amount of £ 1,827,530 and then it shows a slight decline in the month of

December when it reaches the amount of £ 1,824,736. This indicates that the company might be having a slow down due to festive

season where people prefer going to home rather than the hotels and the staff is also comparatively shorter (Penkovskya, 2019).

Collectively, it can be evidently ascertained that the cash budget and its preparations is instrumental in the overall ascertainment of the

net profitability of the company and it also resolves or rather facilitates the decision making of the hotel management (Sokolov, 2019).

For instance, in this case the hotel management of Cardiff Central hotel was able to identify that they had spare investment

possibilities and these could be done satisfactorily in the form of buying a van which is essential for their quicker services ( Yılmaz,

2018). Similarly, it can help in future decision making for the Cardiff Central hotel as well.

TASK 2

Profit Budget Forecast

The preparation of profit budget forecast is mainly done in order to ascertain that whether the organisation will be in a profitable

situation or not i.e. the potential sources of profit as well as loss generation that are possible in the company are ascertained in the

form of the profit budget forecast (West and Ries, 2018). It is prepared systematically where all the potential sources of revenue are

taken into consideration and these are then compared to the all possible expenses in the given time period (Neilsen, 2020). This then

helps in indicating that if the revenue is more than income then the difference between the two is positive showing profit and if the

revenue is less than potential expenses then the difference is negative indicating the losses (Peters, Gudergan and Booth, 2019). In this

manner, any company can evaluate that what are the chances of profit generation and by what estimated amount. This can further help

the company in maintaining its overall expenditures and trying to eliminate or reduce them if the expected revenue is not to the par

7

hotel tends to incur them only when they are in a good profitable situation collectively (Zietlow, 2020).

Apart from this, the prepared cash budget also indicates that the cash net flow for Cardiff Central Hotel seems to be constantly

raising till the month of November where it reaches the amount of £ 1,827,530 and then it shows a slight decline in the month of

December when it reaches the amount of £ 1,824,736. This indicates that the company might be having a slow down due to festive

season where people prefer going to home rather than the hotels and the staff is also comparatively shorter (Penkovskya, 2019).

Collectively, it can be evidently ascertained that the cash budget and its preparations is instrumental in the overall ascertainment of the

net profitability of the company and it also resolves or rather facilitates the decision making of the hotel management (Sokolov, 2019).

For instance, in this case the hotel management of Cardiff Central hotel was able to identify that they had spare investment

possibilities and these could be done satisfactorily in the form of buying a van which is essential for their quicker services ( Yılmaz,

2018). Similarly, it can help in future decision making for the Cardiff Central hotel as well.

TASK 2

Profit Budget Forecast

The preparation of profit budget forecast is mainly done in order to ascertain that whether the organisation will be in a profitable

situation or not i.e. the potential sources of profit as well as loss generation that are possible in the company are ascertained in the

form of the profit budget forecast (West and Ries, 2018). It is prepared systematically where all the potential sources of revenue are

taken into consideration and these are then compared to the all possible expenses in the given time period (Neilsen, 2020). This then

helps in indicating that if the revenue is more than income then the difference between the two is positive showing profit and if the

revenue is less than potential expenses then the difference is negative indicating the losses (Peters, Gudergan and Booth, 2019). In this

manner, any company can evaluate that what are the chances of profit generation and by what estimated amount. This can further help

the company in maintaining its overall expenditures and trying to eliminate or reduce them if the expected revenue is not to the par

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Choi, 2016). This therefore acts as of instrumental importance in the overall decision making and financial maintenance of the

organisation.

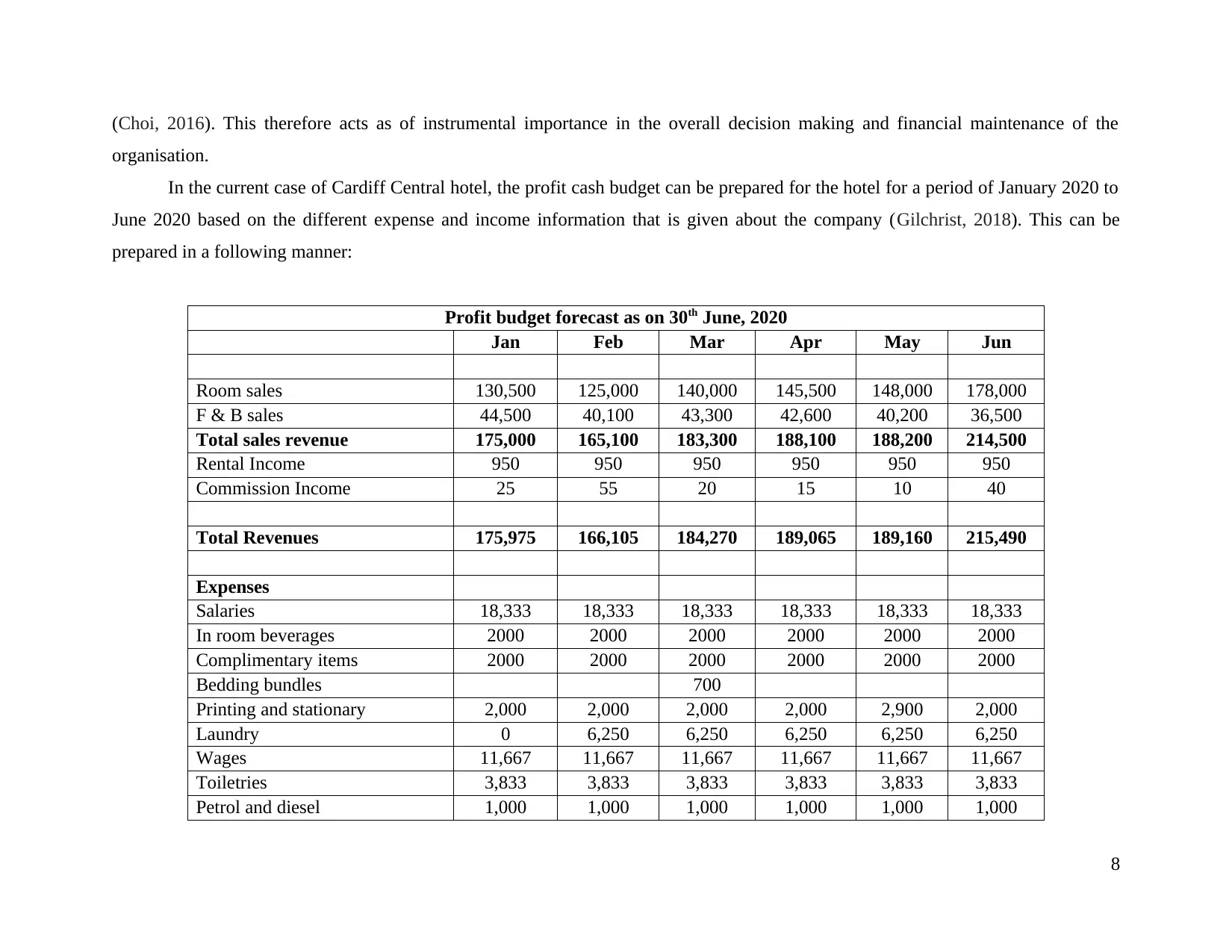

In the current case of Cardiff Central hotel, the profit cash budget can be prepared for the hotel for a period of January 2020 to

June 2020 based on the different expense and income information that is given about the company (Gilchrist, 2018). This can be

prepared in a following manner:

Profit budget forecast as on 30th June, 2020

Jan Feb Mar Apr May Jun

Room sales 130,500 125,000 140,000 145,500 148,000 178,000

F & B sales 44,500 40,100 43,300 42,600 40,200 36,500

Total sales revenue 175,000 165,100 183,300 188,100 188,200 214,500

Rental Income 950 950 950 950 950 950

Commission Income 25 55 20 15 10 40

Total Revenues 175,975 166,105 184,270 189,065 189,160 215,490

Expenses

Salaries 18,333 18,333 18,333 18,333 18,333 18,333

In room beverages 2000 2000 2000 2000 2000 2000

Complimentary items 2000 2000 2000 2000 2000 2000

Bedding bundles 700

Printing and stationary 2,000 2,000 2,000 2,000 2,900 2,000

Laundry 0 6,250 6,250 6,250 6,250 6,250

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Toiletries 3,833 3,833 3,833 3,833 3,833 3,833

Petrol and diesel 1,000 1,000 1,000 1,000 1,000 1,000

8

organisation.

In the current case of Cardiff Central hotel, the profit cash budget can be prepared for the hotel for a period of January 2020 to

June 2020 based on the different expense and income information that is given about the company (Gilchrist, 2018). This can be

prepared in a following manner:

Profit budget forecast as on 30th June, 2020

Jan Feb Mar Apr May Jun

Room sales 130,500 125,000 140,000 145,500 148,000 178,000

F & B sales 44,500 40,100 43,300 42,600 40,200 36,500

Total sales revenue 175,000 165,100 183,300 188,100 188,200 214,500

Rental Income 950 950 950 950 950 950

Commission Income 25 55 20 15 10 40

Total Revenues 175,975 166,105 184,270 189,065 189,160 215,490

Expenses

Salaries 18,333 18,333 18,333 18,333 18,333 18,333

In room beverages 2000 2000 2000 2000 2000 2000

Complimentary items 2000 2000 2000 2000 2000 2000

Bedding bundles 700

Printing and stationary 2,000 2,000 2,000 2,000 2,900 2,000

Laundry 0 6,250 6,250 6,250 6,250 6,250

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Toiletries 3,833 3,833 3,833 3,833 3,833 3,833

Petrol and diesel 1,000 1,000 1,000 1,000 1,000 1,000

8

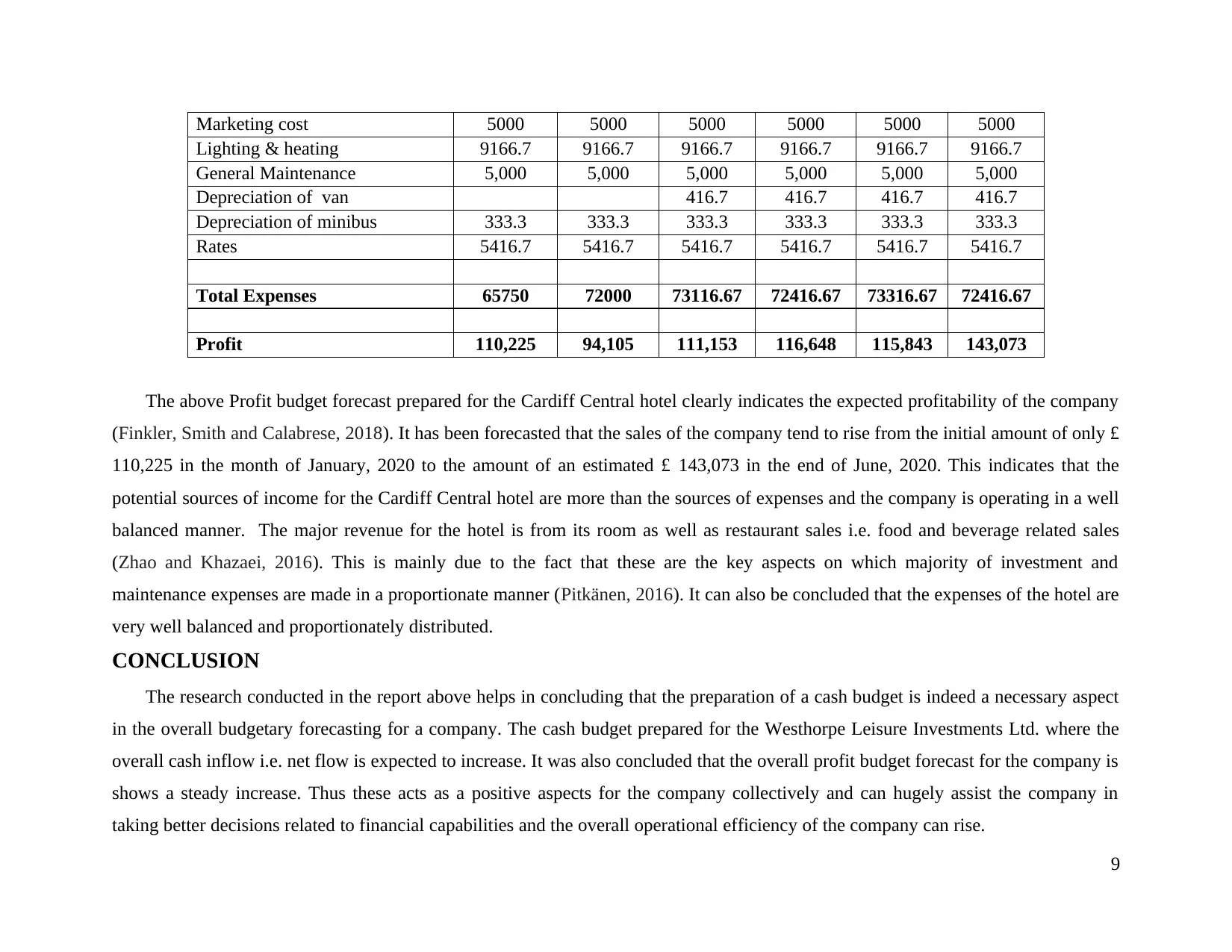

Marketing cost 5000 5000 5000 5000 5000 5000

Lighting & heating 9166.7 9166.7 9166.7 9166.7 9166.7 9166.7

General Maintenance 5,000 5,000 5,000 5,000 5,000 5,000

Depreciation of van 416.7 416.7 416.7 416.7

Depreciation of minibus 333.3 333.3 333.3 333.3 333.3 333.3

Rates 5416.7 5416.7 5416.7 5416.7 5416.7 5416.7

Total Expenses 65750 72000 73116.67 72416.67 73316.67 72416.67

Profit 110,225 94,105 111,153 116,648 115,843 143,073

The above Profit budget forecast prepared for the Cardiff Central hotel clearly indicates the expected profitability of the company

(Finkler, Smith and Calabrese, 2018). It has been forecasted that the sales of the company tend to rise from the initial amount of only £

110,225 in the month of January, 2020 to the amount of an estimated £ 143,073 in the end of June, 2020. This indicates that the

potential sources of income for the Cardiff Central hotel are more than the sources of expenses and the company is operating in a well

balanced manner. The major revenue for the hotel is from its room as well as restaurant sales i.e. food and beverage related sales

(Zhao and Khazaei, 2016). This is mainly due to the fact that these are the key aspects on which majority of investment and

maintenance expenses are made in a proportionate manner (Pitkänen, 2016). It can also be concluded that the expenses of the hotel are

very well balanced and proportionately distributed.

CONCLUSION

The research conducted in the report above helps in concluding that the preparation of a cash budget is indeed a necessary aspect

in the overall budgetary forecasting for a company. The cash budget prepared for the Westhorpe Leisure Investments Ltd. where the

overall cash inflow i.e. net flow is expected to increase. It was also concluded that the overall profit budget forecast for the company is

shows a steady increase. Thus these acts as a positive aspects for the company collectively and can hugely assist the company in

taking better decisions related to financial capabilities and the overall operational efficiency of the company can rise.

9

Lighting & heating 9166.7 9166.7 9166.7 9166.7 9166.7 9166.7

General Maintenance 5,000 5,000 5,000 5,000 5,000 5,000

Depreciation of van 416.7 416.7 416.7 416.7

Depreciation of minibus 333.3 333.3 333.3 333.3 333.3 333.3

Rates 5416.7 5416.7 5416.7 5416.7 5416.7 5416.7

Total Expenses 65750 72000 73116.67 72416.67 73316.67 72416.67

Profit 110,225 94,105 111,153 116,648 115,843 143,073

The above Profit budget forecast prepared for the Cardiff Central hotel clearly indicates the expected profitability of the company

(Finkler, Smith and Calabrese, 2018). It has been forecasted that the sales of the company tend to rise from the initial amount of only £

110,225 in the month of January, 2020 to the amount of an estimated £ 143,073 in the end of June, 2020. This indicates that the

potential sources of income for the Cardiff Central hotel are more than the sources of expenses and the company is operating in a well

balanced manner. The major revenue for the hotel is from its room as well as restaurant sales i.e. food and beverage related sales

(Zhao and Khazaei, 2016). This is mainly due to the fact that these are the key aspects on which majority of investment and

maintenance expenses are made in a proportionate manner (Pitkänen, 2016). It can also be concluded that the expenses of the hotel are

very well balanced and proportionately distributed.

CONCLUSION

The research conducted in the report above helps in concluding that the preparation of a cash budget is indeed a necessary aspect

in the overall budgetary forecasting for a company. The cash budget prepared for the Westhorpe Leisure Investments Ltd. where the

overall cash inflow i.e. net flow is expected to increase. It was also concluded that the overall profit budget forecast for the company is

shows a steady increase. Thus these acts as a positive aspects for the company collectively and can hugely assist the company in

taking better decisions related to financial capabilities and the overall operational efficiency of the company can rise.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abor, J.Y., 2017. Financial Planning and Forecasting. In Entrepreneurial Finance for MSMEs (pp. 199-224). Palgrave Macmillan,

Cham.

Bhar, A.K., 2019. Design & implementation of a personal Cash flow program using Microsoft Excel®. Global Journal of Business,

Economics and Management: Current Issues, 9(1), pp.29-40.

Choi, T.M., 2016. Multi-period risk minimization purchasing models for fashion products with interest rate, budget, and profit target

considerations. Annals of Operations Research, 237(1-2), pp.77-98.

DeFranco, A.L. and Schmidgall, R.S., 2017. Cash Budgets, Controls, and Management in Clubs. The Journal of Hospitality Financial

Management, 25(2), pp.112-122.

DeFranco, A.L. and Schmidgall, R.S., 2020. Are We Keeping Our Cash in Our Hotels?. Journal of Hospitality Financial

Management, 28(1), p.7.

EQUIVALENTS, C., 2018. CASH & CASH EQUIVALENTS. BALANCE SHEET.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2018. Financial management for public, health, and not-for-profit organizations. CQ

Press.

Gilchrist, R.R., 2018. Managing for profit: The added value concept. Routledge.

Mwanza, P.S. and Benedict, H.O., 2018. Journal of Entrepreneurship & Organization Management.

Neilsen, A., 2020. Budget blitz. Ragtrader, (May 2020), p.33.

Penkovskya, E.V., 2019. ECONOMICS OF SOCIAL AND LEGAL CULTURE OF SOCIETY IN THE XXI CENTURY. In Роль

интеллектуального капитала в экономической, социальной и правовой культуре общества XXI века (pp. 24-26).

Peters, M.D., Gudergan, S. and Booth, P., 2019. Interactive profit-planning systems and market turbulence: A dynamic capabilities

perspective. Long Range Planning, 52(3), pp.386-405.

10

Books and Journals

Abor, J.Y., 2017. Financial Planning and Forecasting. In Entrepreneurial Finance for MSMEs (pp. 199-224). Palgrave Macmillan,

Cham.

Bhar, A.K., 2019. Design & implementation of a personal Cash flow program using Microsoft Excel®. Global Journal of Business,

Economics and Management: Current Issues, 9(1), pp.29-40.

Choi, T.M., 2016. Multi-period risk minimization purchasing models for fashion products with interest rate, budget, and profit target

considerations. Annals of Operations Research, 237(1-2), pp.77-98.

DeFranco, A.L. and Schmidgall, R.S., 2017. Cash Budgets, Controls, and Management in Clubs. The Journal of Hospitality Financial

Management, 25(2), pp.112-122.

DeFranco, A.L. and Schmidgall, R.S., 2020. Are We Keeping Our Cash in Our Hotels?. Journal of Hospitality Financial

Management, 28(1), p.7.

EQUIVALENTS, C., 2018. CASH & CASH EQUIVALENTS. BALANCE SHEET.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2018. Financial management for public, health, and not-for-profit organizations. CQ

Press.

Gilchrist, R.R., 2018. Managing for profit: The added value concept. Routledge.

Mwanza, P.S. and Benedict, H.O., 2018. Journal of Entrepreneurship & Organization Management.

Neilsen, A., 2020. Budget blitz. Ragtrader, (May 2020), p.33.

Penkovskya, E.V., 2019. ECONOMICS OF SOCIAL AND LEGAL CULTURE OF SOCIETY IN THE XXI CENTURY. In Роль

интеллектуального капитала в экономической, социальной и правовой культуре общества XXI века (pp. 24-26).

Peters, M.D., Gudergan, S. and Booth, P., 2019. Interactive profit-planning systems and market turbulence: A dynamic capabilities

perspective. Long Range Planning, 52(3), pp.386-405.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Picchio, M. and Santolini, R., 2020. Fiscal rules and budget forecast errors of Italian municipalities. European Journal of Political

Economy, p.101921.

Pitkänen, A., 2016. Cash Flow Forecasting: Proposal for New Long-Term Cash Flow Forecast in the Case Company.

Shaaban, A.F. and Thandra, V., 2016. System and Method for Budgeting and Cash Flow Forecasting. U.S. Patent Application

14/788,779.

Sokolov, I., 2019. Federal Budget for 2020–2022: Main Parameters. Monitoring of Russia's Economic Outlook. Moscow, (16), pp.5-8.

Turner, J.A., 2016. Net Operating Working Capital, Capital Budgeting, And Cash Budgets: A Teaching Example. American Journal

of Business Education (AJBE), 9(1), pp.31-38.

West, A. and Ries, R., 2018. Top challenges facing not-for-profit CFOs today: Revisiting the toughest challenges. The CPA

Journal, 88(4), pp.15-17.

Yılmaz, F., 2018. Budgeting as a Tool for Sustainable Development. In Handbook of Research on Supply Chain Management for

Sustainable Development (pp. 42-60). IGI Global.

Zhao, Y. and Khazaei, H., 2016, July. An incentive compatible profit allocation mechanism for renewable energy aggregation. In 2016

IEEE Power and Energy Society General Meeting (PESGM) (pp. 1-5). IEEE.

Zietlow, J., 2020. 10 Treasury, Cash, and Liquidity Management in Nonprofit Organizations. Financing Nonprofit Organizations.

11

Economy, p.101921.

Pitkänen, A., 2016. Cash Flow Forecasting: Proposal for New Long-Term Cash Flow Forecast in the Case Company.

Shaaban, A.F. and Thandra, V., 2016. System and Method for Budgeting and Cash Flow Forecasting. U.S. Patent Application

14/788,779.

Sokolov, I., 2019. Federal Budget for 2020–2022: Main Parameters. Monitoring of Russia's Economic Outlook. Moscow, (16), pp.5-8.

Turner, J.A., 2016. Net Operating Working Capital, Capital Budgeting, And Cash Budgets: A Teaching Example. American Journal

of Business Education (AJBE), 9(1), pp.31-38.

West, A. and Ries, R., 2018. Top challenges facing not-for-profit CFOs today: Revisiting the toughest challenges. The CPA

Journal, 88(4), pp.15-17.

Yılmaz, F., 2018. Budgeting as a Tool for Sustainable Development. In Handbook of Research on Supply Chain Management for

Sustainable Development (pp. 42-60). IGI Global.

Zhao, Y. and Khazaei, H., 2016, July. An incentive compatible profit allocation mechanism for renewable energy aggregation. In 2016

IEEE Power and Energy Society General Meeting (PESGM) (pp. 1-5). IEEE.

Zietlow, J., 2020. 10 Treasury, Cash, and Liquidity Management in Nonprofit Organizations. Financing Nonprofit Organizations.

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.