Budgeting and Financial Performance Analysis Assignment

VerifiedAdded on 2022/11/19

|8

|1147

|69

Homework Assignment

AI Summary

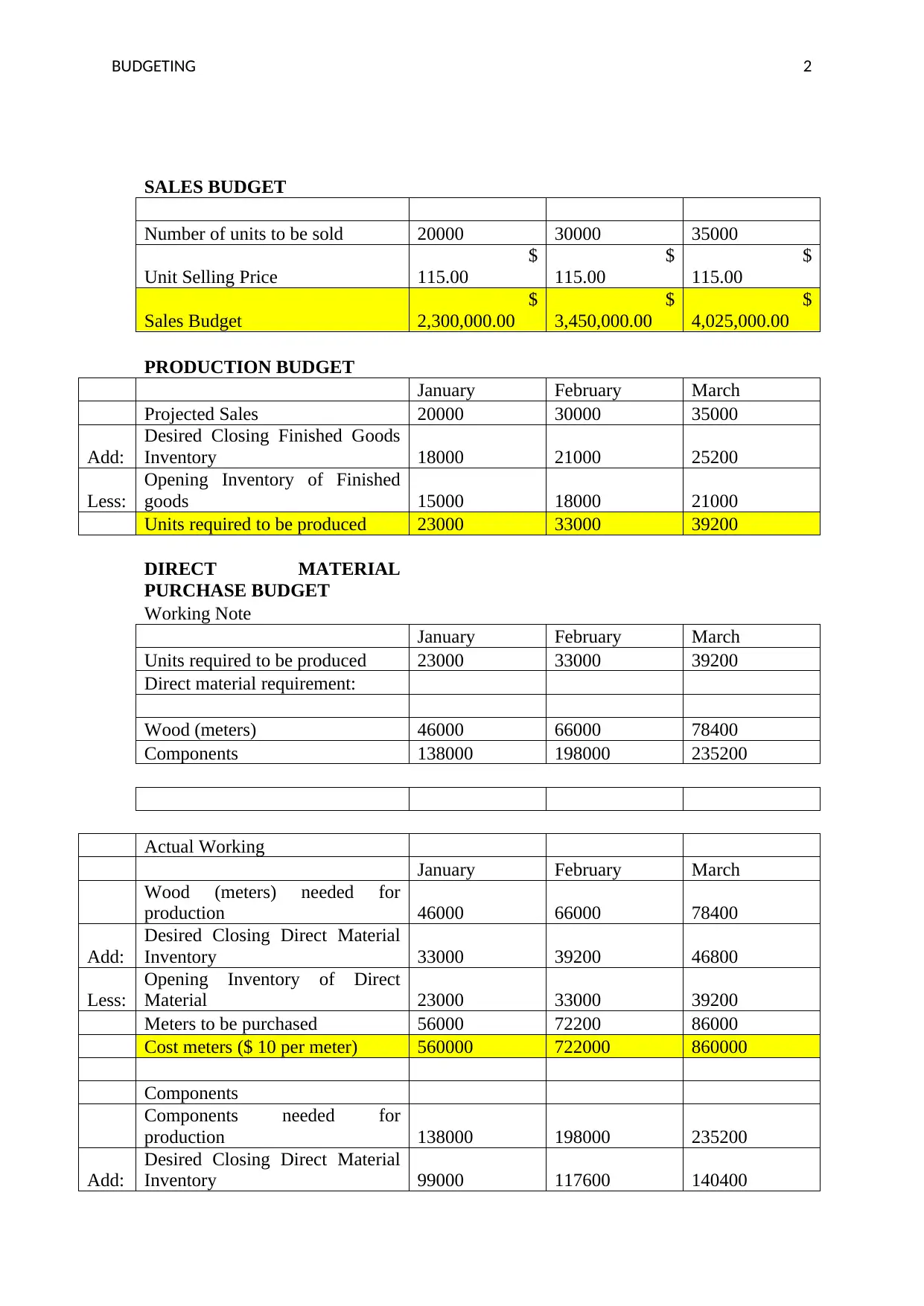

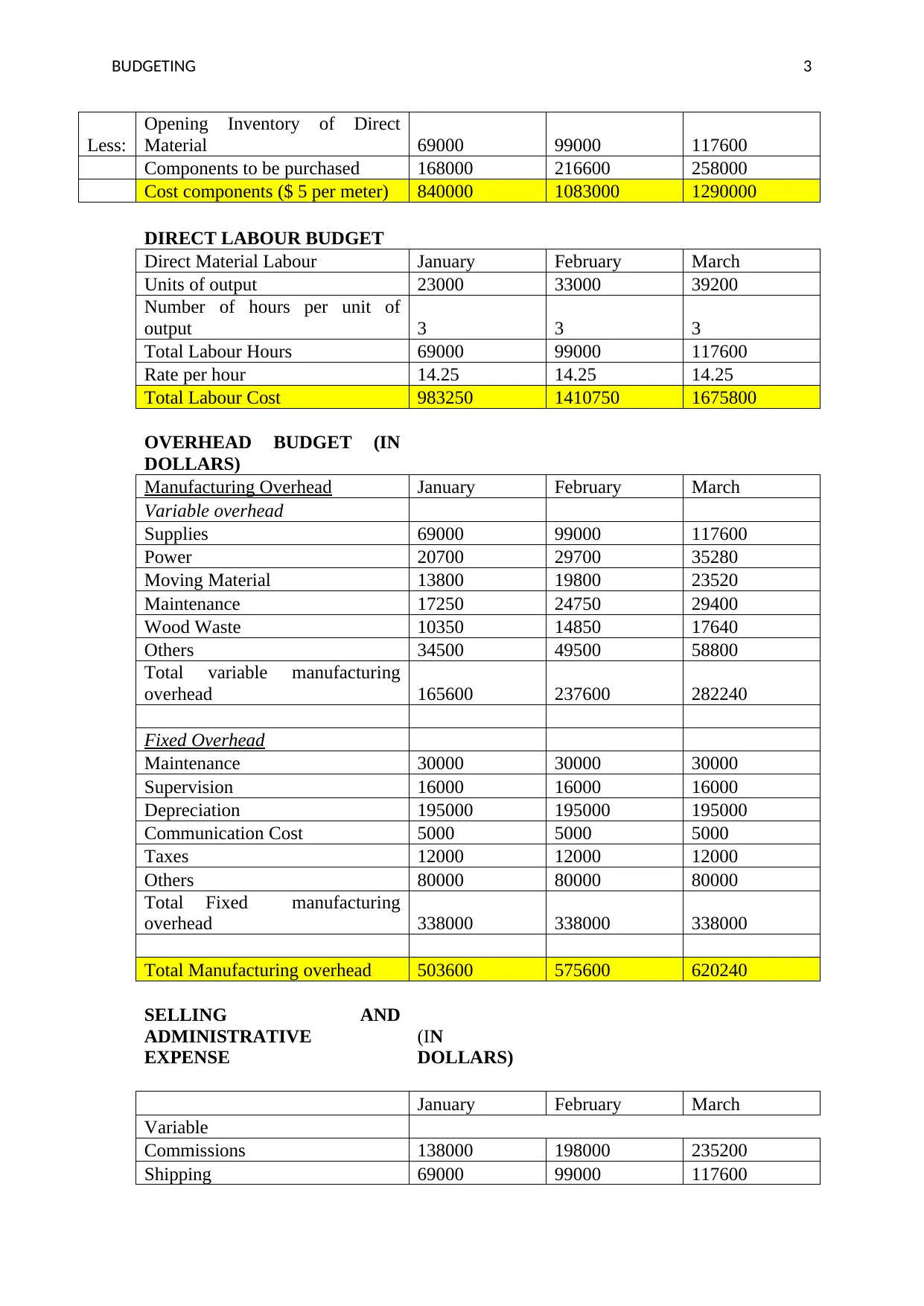

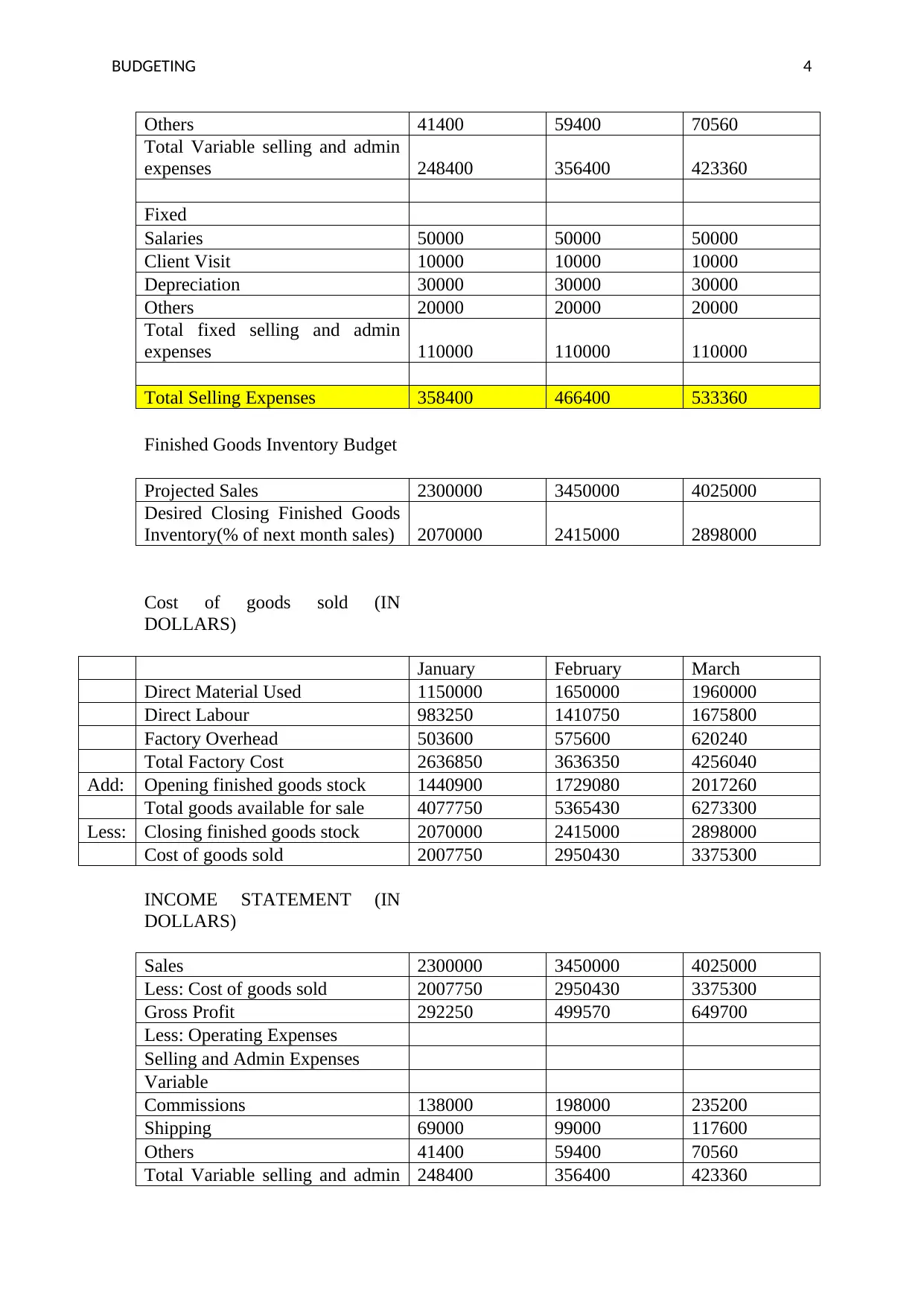

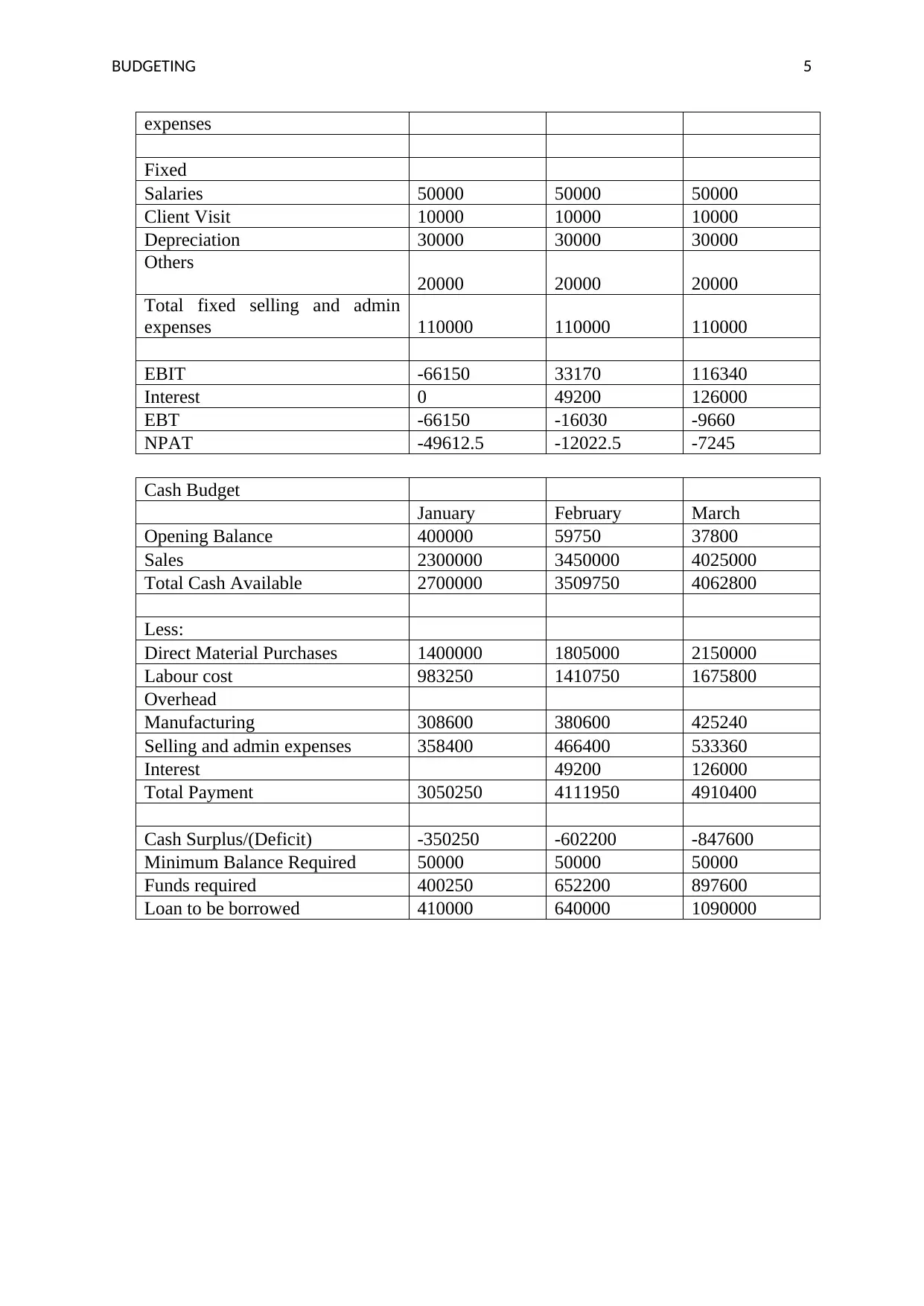

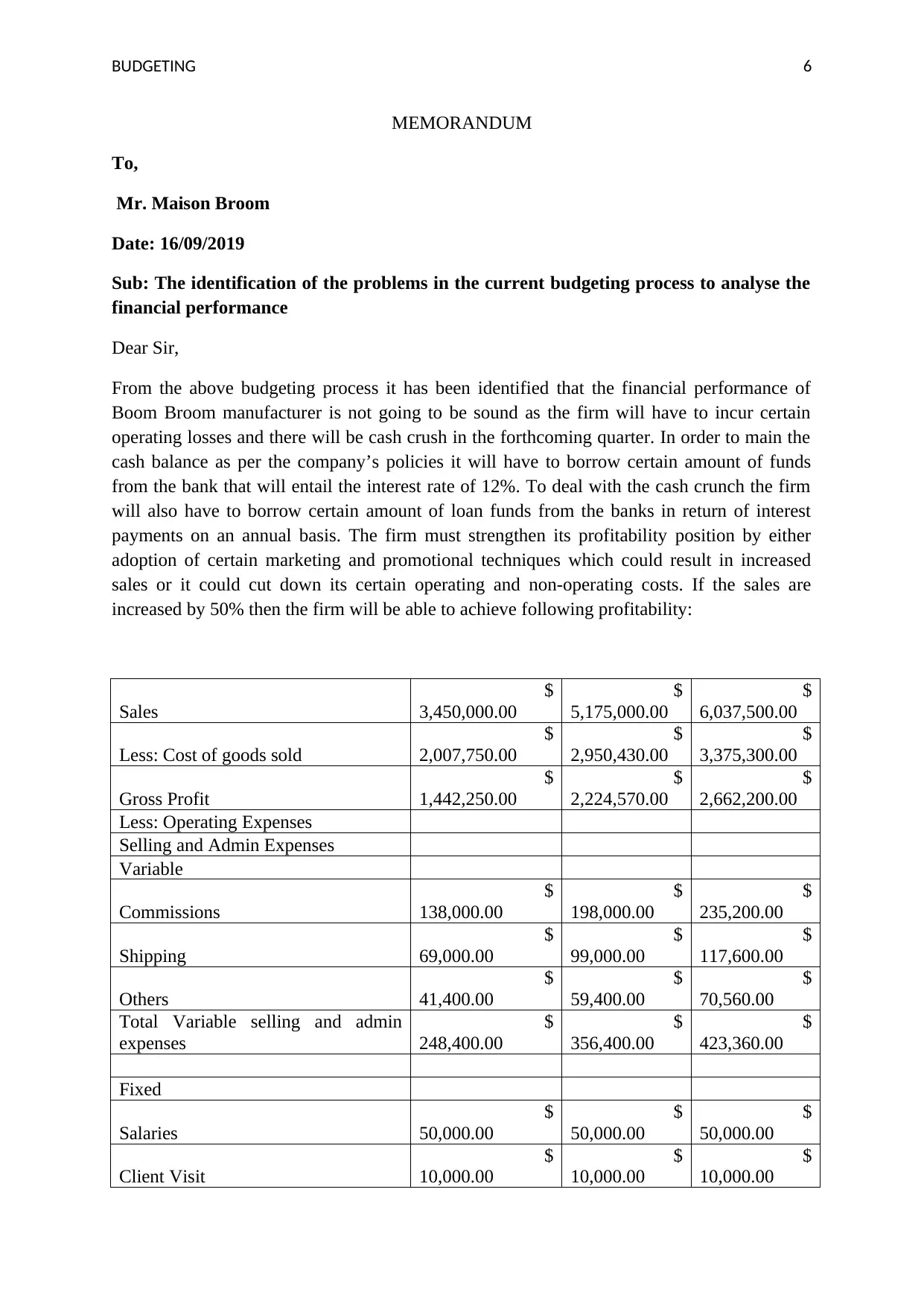

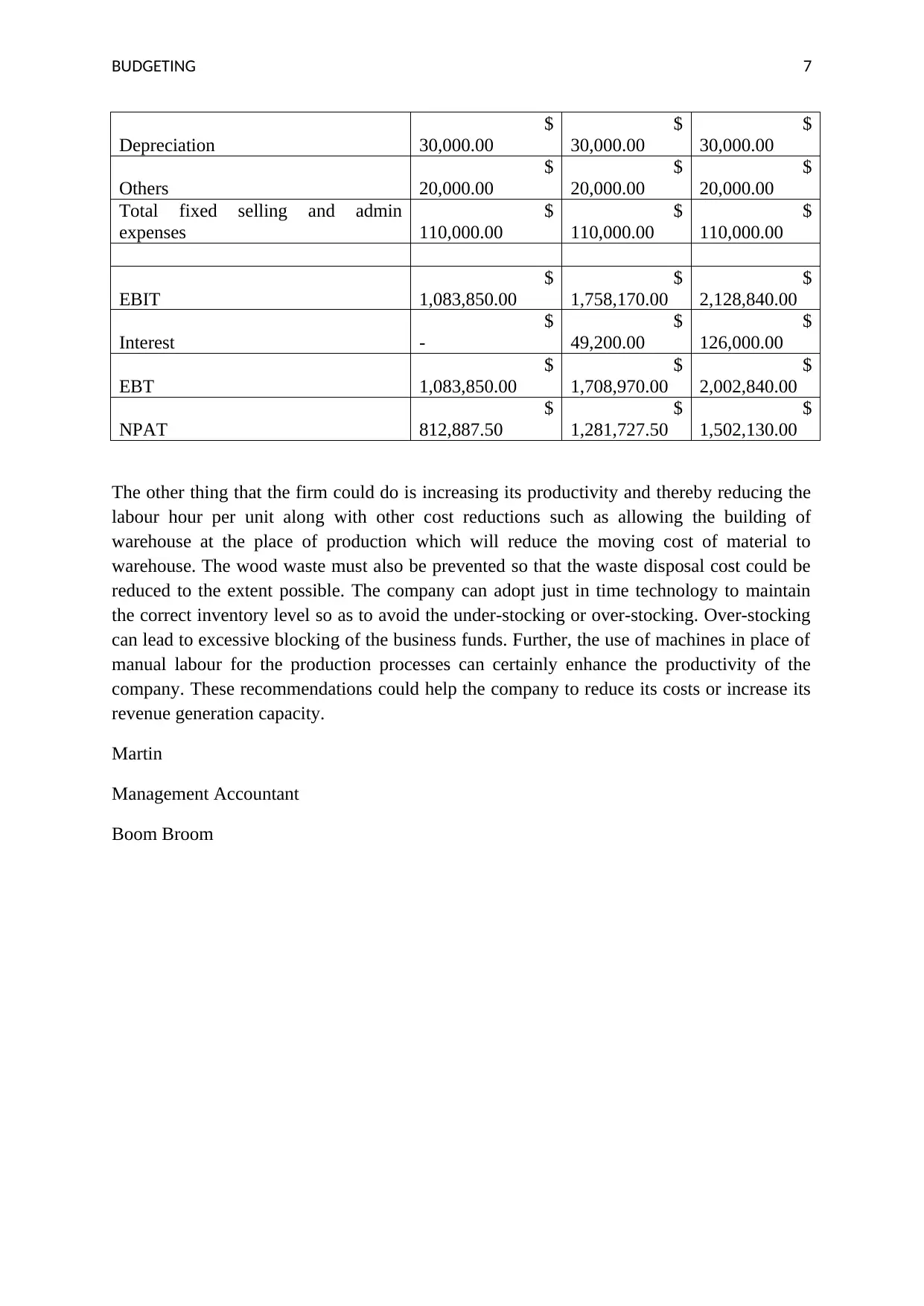

This assignment solution provides a comprehensive analysis of a company's financial performance through a master budget, including sales, production, direct materials, direct labor, overhead, selling and administrative expenses, and cash flow projections for three months. The solution presents detailed calculations for each budget component, culminating in an income statement and a cash budget. The assignment further includes a memorandum identifying potential financial problems, such as potential operating losses and cash flow issues, and offers recommendations to improve the company's financial health. These recommendations include strategies to increase sales, reduce costs, and enhance productivity. The analysis highlights the importance of effective budgeting in identifying and mitigating financial risks, as well as making informed decisions to drive profitability and long-term financial stability. The solution emphasizes the critical role of financial planning and cost management in achieving business success.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.