Budgeting for Organic Farm Products

VerifiedAdded on 2023/01/18

|18

|2317

|72

AI Summary

This document discusses the budgeting process for organic farm products, including the vision, purpose, and goals of the business. It also covers the estimation of direct material and labor costs, variable and fixed overheads, and the preparation of a master budget for one month of operation. The document provides insights into the knowledge and skills gained through the assignment and includes references for further reading.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Budgeting

Name of the student-

[DATE]

Hewlett-Packard

[Company address]

Name of the student-

[DATE]

Hewlett-Packard

[Company address]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

1. Create product or service your choice, and discuss the vision, purpose, and goal of your

activity...........................................................................................................................2

2. Estimate standard direct material and direct labour costs for your product or service.........3

3. Estimate standard variable overheads and fixed overheads for producing the product or

service............................................................................................................................6

4. Prepare master budget for your 1 month of operation (including sales, costs of sales, profit

and loss budgets).............................................................................................................9

5. Reflection on knowledge and skills.............................................................................12

References....................................................................................................................13

1. Create product or service your choice, and discuss the vision, purpose, and goal of your

activity...........................................................................................................................2

2. Estimate standard direct material and direct labour costs for your product or service.........3

3. Estimate standard variable overheads and fixed overheads for producing the product or

service............................................................................................................................6

4. Prepare master budget for your 1 month of operation (including sales, costs of sales, profit

and loss budgets).............................................................................................................9

5. Reflection on knowledge and skills.............................................................................12

References....................................................................................................................13

1. Create product or service your choice, and discuss the vision, purpose, and goal of

your activity.

PRODUCT OR SERVICE: The product chosen for offering into the market is organic farm

products. The primary product shall be far produced fruits, mainly the citrus ones. The setting

proposed for the production shall be mainly traditional with the use of labour intensive

technique (Garibaldi, et. al 2017). The land chosen shall be feasibly tested initially to check

the suitability for the proposed production. The production month shall be based upon the

months suitable for each fruit type, in order to promote production function happening on a

continuous basis.

REASON: the reason for the selected products is the ongoing demand in the market for the

healthy produce rather than chemically grown items. The opportunity to strike market share is

high in this category of product (Reganold, & Wachter, 2016).

VISION: the vision of business is promotion of a system of agricultural supply that is safe

and sustainable. Promoting the health of the consumers along with environment protection

(Niggli, Willer, & Baker, 2016).

PURPOSE: the purpose of business is provision of good quality, and full of nutrition fruits

for making it available for consumption to several regions of Australia. The main purpose is

attainment of sustainability (Barker, 2016).

GOAL: the goal is to strike a balance with consumers to incentivise them to make purchase

decision that can improvise their health. Along with consumer health, the environment and

community care is also to be sought of. The target is expansion of use of practice of organic

farming and reduction of chemically grown food products. The sustainability of the

Australian agricultural system is aimed to be fostered (Crowder, & Reganold, 2015).

your activity.

PRODUCT OR SERVICE: The product chosen for offering into the market is organic farm

products. The primary product shall be far produced fruits, mainly the citrus ones. The setting

proposed for the production shall be mainly traditional with the use of labour intensive

technique (Garibaldi, et. al 2017). The land chosen shall be feasibly tested initially to check

the suitability for the proposed production. The production month shall be based upon the

months suitable for each fruit type, in order to promote production function happening on a

continuous basis.

REASON: the reason for the selected products is the ongoing demand in the market for the

healthy produce rather than chemically grown items. The opportunity to strike market share is

high in this category of product (Reganold, & Wachter, 2016).

VISION: the vision of business is promotion of a system of agricultural supply that is safe

and sustainable. Promoting the health of the consumers along with environment protection

(Niggli, Willer, & Baker, 2016).

PURPOSE: the purpose of business is provision of good quality, and full of nutrition fruits

for making it available for consumption to several regions of Australia. The main purpose is

attainment of sustainability (Barker, 2016).

GOAL: the goal is to strike a balance with consumers to incentivise them to make purchase

decision that can improvise their health. Along with consumer health, the environment and

community care is also to be sought of. The target is expansion of use of practice of organic

farming and reduction of chemically grown food products. The sustainability of the

Australian agricultural system is aimed to be fostered (Crowder, & Reganold, 2015).

The futuristic goal is to bring an entire reform in the manner production is done and

materialised. Knowledge about the environmental and health benefits of the system of

organic farming is required to be spread in the local masses.

LINKAGE OF DECISION: the decision to produce the organic fruits has been taken with

the view to exploit the growing demand in market for healthy produce. The company’s

vision, purpose and goal are linked with exploiting this opportunity. The company’s foremost

aim is creating a sustainable environment for the company’s production process. This

sustainability can be achieved by promoting organic production as well as the promotion of

the organic sales.

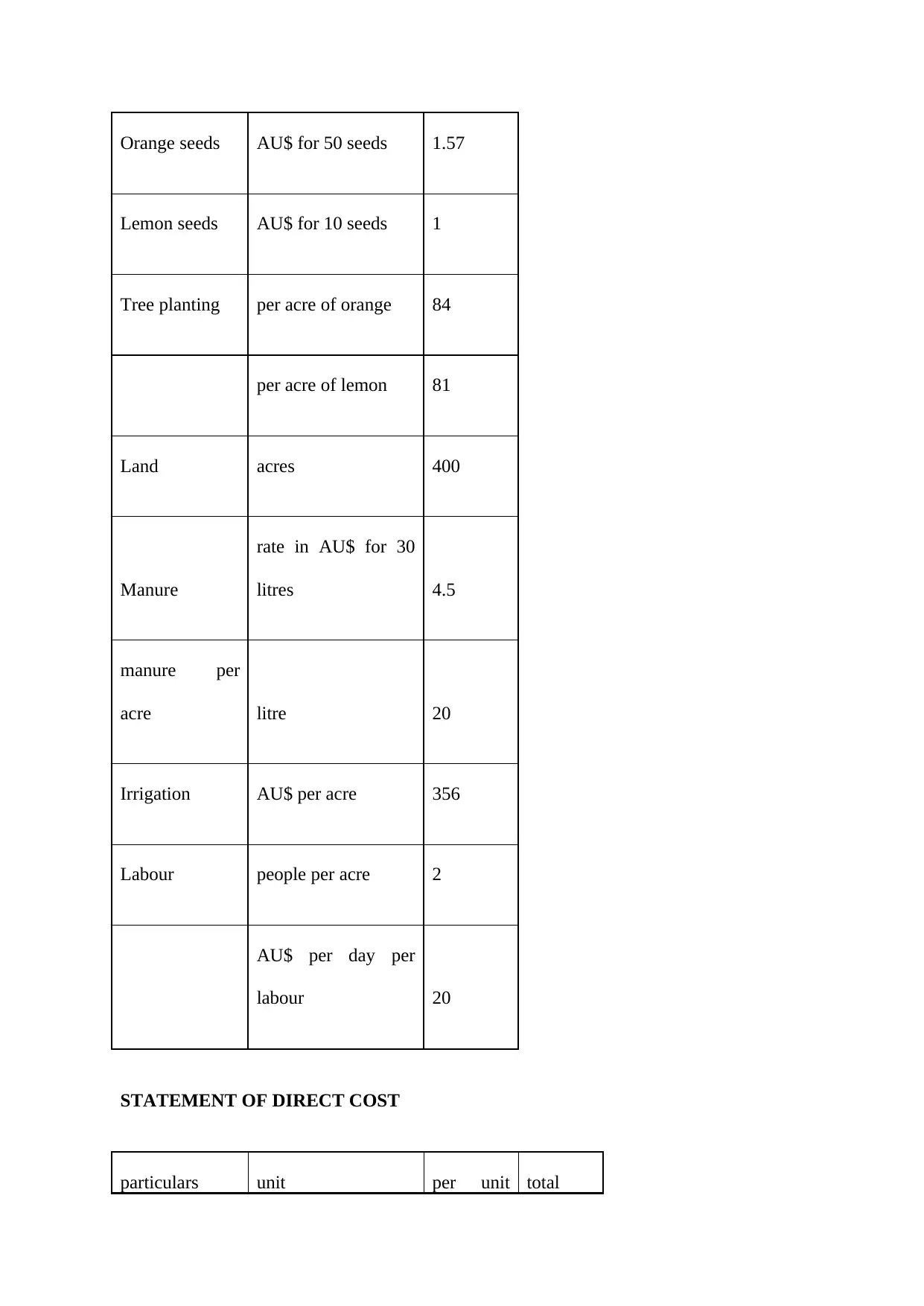

2. Estimate standard direct material and direct labour costs for your product or service.

The direct material costs required for the production of agricultural farm business shall relate

to seeds, and irrigation, with manure. The direct labour shall comprise of the labor costs. The

current production list comprises of oranges, and lemon. The process of cost estimation is

done as follows:

NOTE: the calculation of labor and material cost is done on an annual basis. Assumption

taken is that, both lemon and oranges shall be grown simultaneously on 200 acre land. The

production shall take 12 months for realise in sale. Hence, the master budget prepared shall

be for the month after the production is done (Gao, & Wong, 2017).

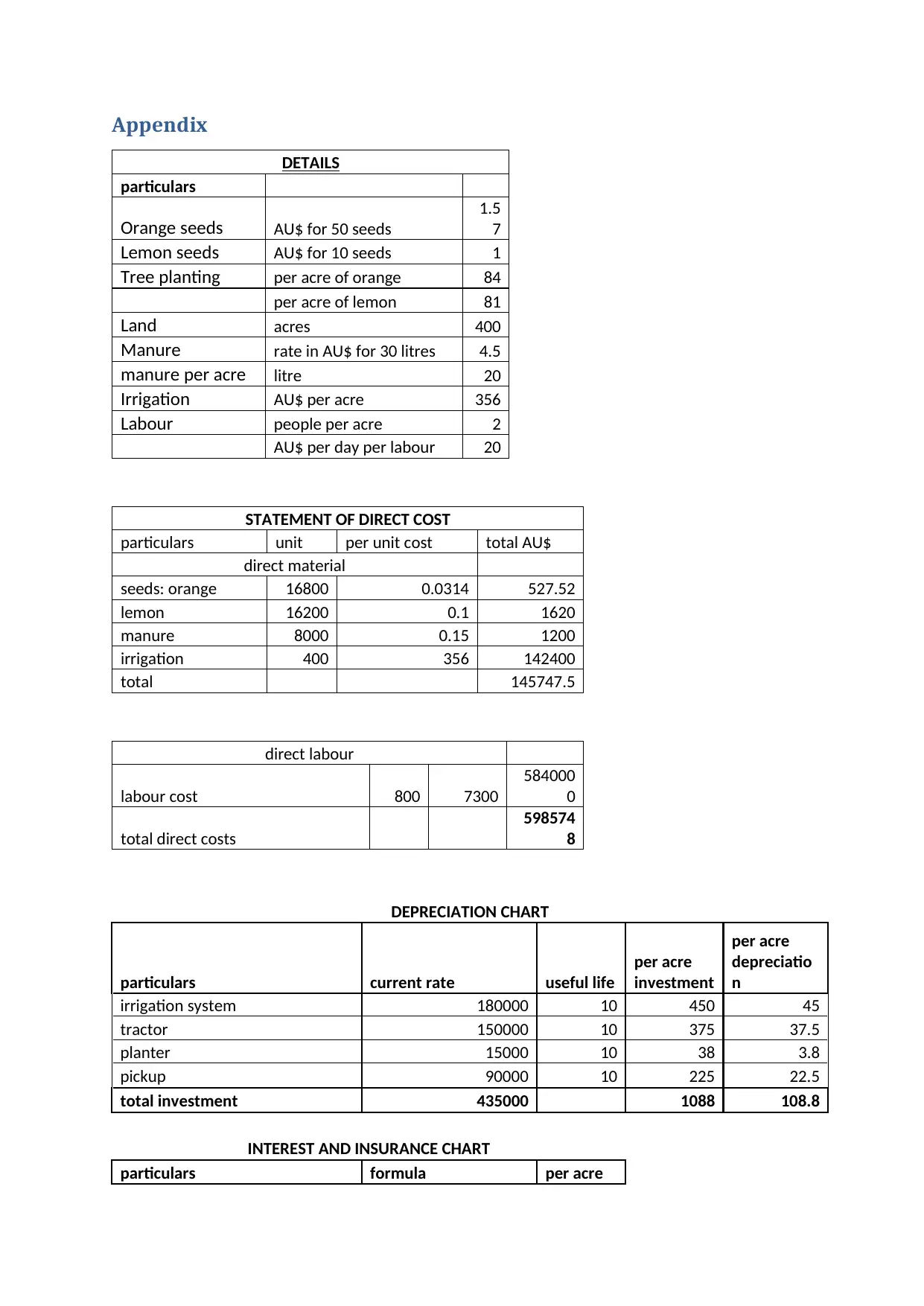

DETAILS

particulars

materialised. Knowledge about the environmental and health benefits of the system of

organic farming is required to be spread in the local masses.

LINKAGE OF DECISION: the decision to produce the organic fruits has been taken with

the view to exploit the growing demand in market for healthy produce. The company’s

vision, purpose and goal are linked with exploiting this opportunity. The company’s foremost

aim is creating a sustainable environment for the company’s production process. This

sustainability can be achieved by promoting organic production as well as the promotion of

the organic sales.

2. Estimate standard direct material and direct labour costs for your product or service.

The direct material costs required for the production of agricultural farm business shall relate

to seeds, and irrigation, with manure. The direct labour shall comprise of the labor costs. The

current production list comprises of oranges, and lemon. The process of cost estimation is

done as follows:

NOTE: the calculation of labor and material cost is done on an annual basis. Assumption

taken is that, both lemon and oranges shall be grown simultaneously on 200 acre land. The

production shall take 12 months for realise in sale. Hence, the master budget prepared shall

be for the month after the production is done (Gao, & Wong, 2017).

DETAILS

particulars

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Orange seeds AU$ for 50 seeds 1.57

Lemon seeds AU$ for 10 seeds 1

Tree planting per acre of orange 84

per acre of lemon 81

Land acres 400

Manure

rate in AU$ for 30

litres 4.5

manure per

acre litre 20

Irrigation AU$ per acre 356

Labour people per acre 2

AU$ per day per

labour 20

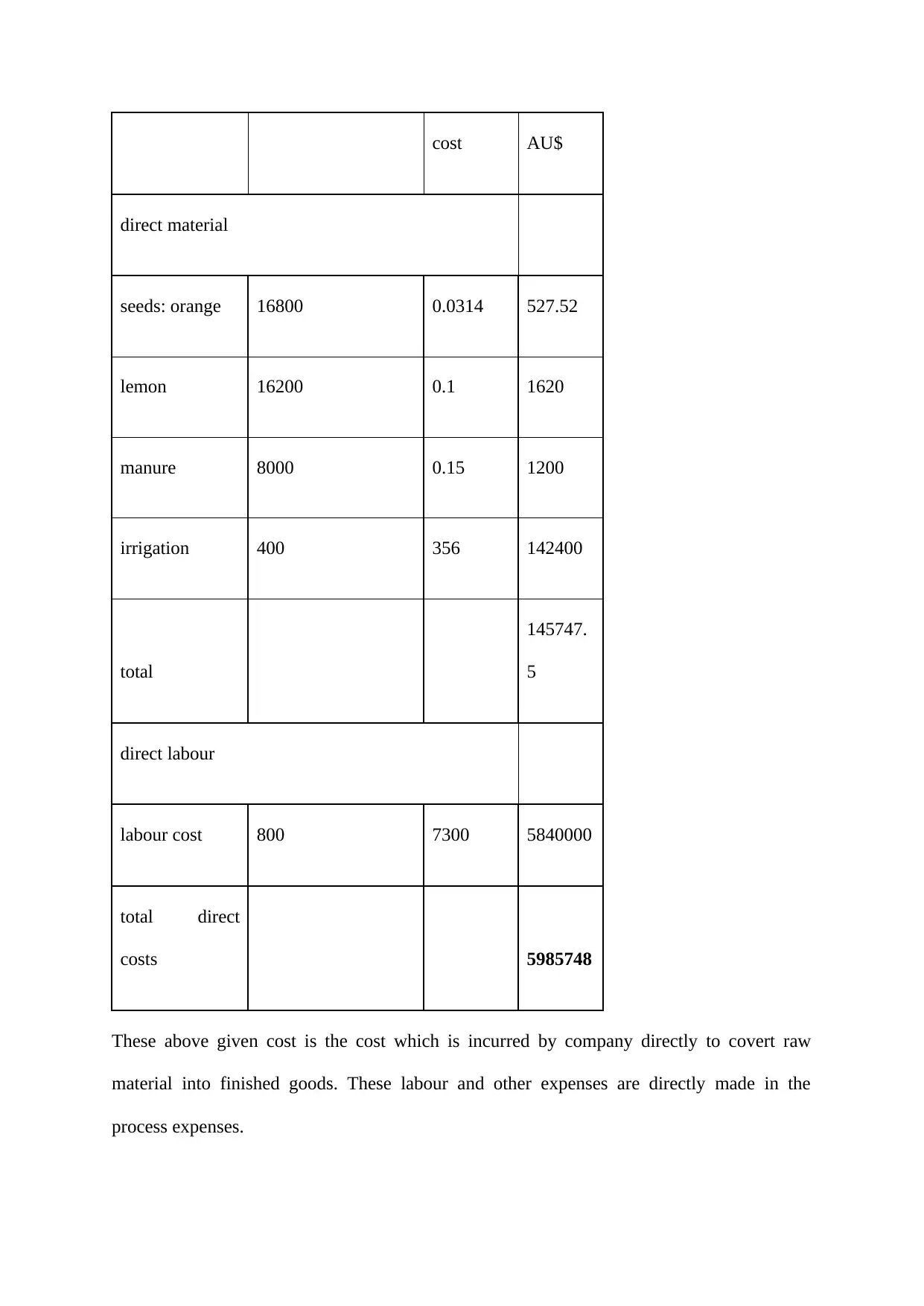

STATEMENT OF DIRECT COST

particulars unit per unit total

Lemon seeds AU$ for 10 seeds 1

Tree planting per acre of orange 84

per acre of lemon 81

Land acres 400

Manure

rate in AU$ for 30

litres 4.5

manure per

acre litre 20

Irrigation AU$ per acre 356

Labour people per acre 2

AU$ per day per

labour 20

STATEMENT OF DIRECT COST

particulars unit per unit total

cost AU$

direct material

seeds: orange 16800 0.0314 527.52

lemon 16200 0.1 1620

manure 8000 0.15 1200

irrigation 400 356 142400

total

145747.

5

direct labour

labour cost 800 7300 5840000

total direct

costs 5985748

These above given cost is the cost which is incurred by company directly to covert raw

material into finished goods. These labour and other expenses are directly made in the

process expenses.

direct material

seeds: orange 16800 0.0314 527.52

lemon 16200 0.1 1620

manure 8000 0.15 1200

irrigation 400 356 142400

total

145747.

5

direct labour

labour cost 800 7300 5840000

total direct

costs 5985748

These above given cost is the cost which is incurred by company directly to covert raw

material into finished goods. These labour and other expenses are directly made in the

process expenses.

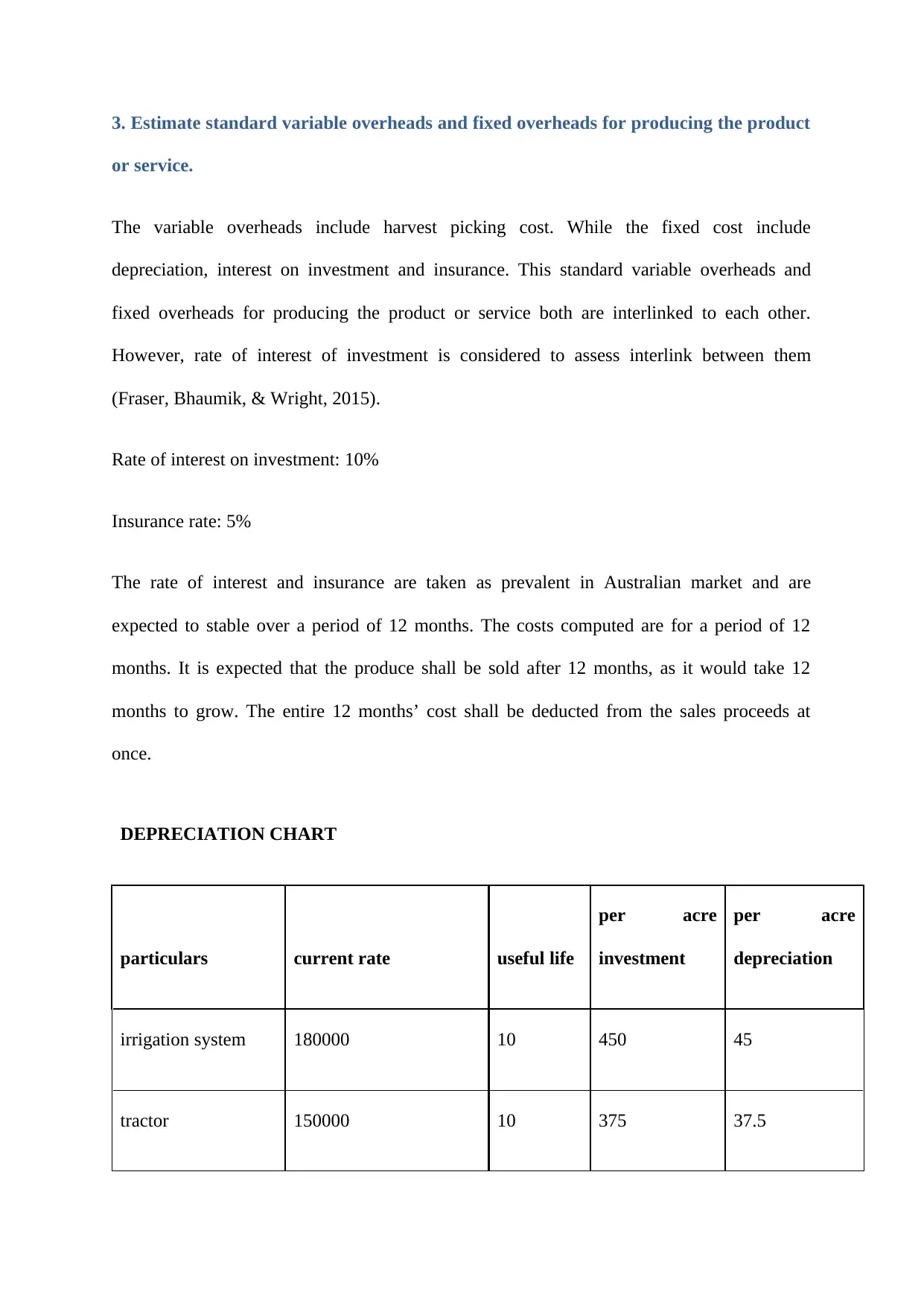

3. Estimate standard variable overheads and fixed overheads for producing the product

or service.

The variable overheads include harvest picking cost. While the fixed cost include

depreciation, interest on investment and insurance. This standard variable overheads and

fixed overheads for producing the product or service both are interlinked to each other.

However, rate of interest of investment is considered to assess interlink between them

(Fraser, Bhaumik, & Wright, 2015).

Rate of interest on investment: 10%

Insurance rate: 5%

The rate of interest and insurance are taken as prevalent in Australian market and are

expected to stable over a period of 12 months. The costs computed are for a period of 12

months. It is expected that the produce shall be sold after 12 months, as it would take 12

months to grow. The entire 12 months’ cost shall be deducted from the sales proceeds at

once.

DEPRECIATION CHART

particulars current rate useful life

per acre

investment

per acre

depreciation

irrigation system 180000 10 450 45

tractor 150000 10 375 37.5

or service.

The variable overheads include harvest picking cost. While the fixed cost include

depreciation, interest on investment and insurance. This standard variable overheads and

fixed overheads for producing the product or service both are interlinked to each other.

However, rate of interest of investment is considered to assess interlink between them

(Fraser, Bhaumik, & Wright, 2015).

Rate of interest on investment: 10%

Insurance rate: 5%

The rate of interest and insurance are taken as prevalent in Australian market and are

expected to stable over a period of 12 months. The costs computed are for a period of 12

months. It is expected that the produce shall be sold after 12 months, as it would take 12

months to grow. The entire 12 months’ cost shall be deducted from the sales proceeds at

once.

DEPRECIATION CHART

particulars current rate useful life

per acre

investment

per acre

depreciation

irrigation system 180000 10 450 45

tractor 150000 10 375 37.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

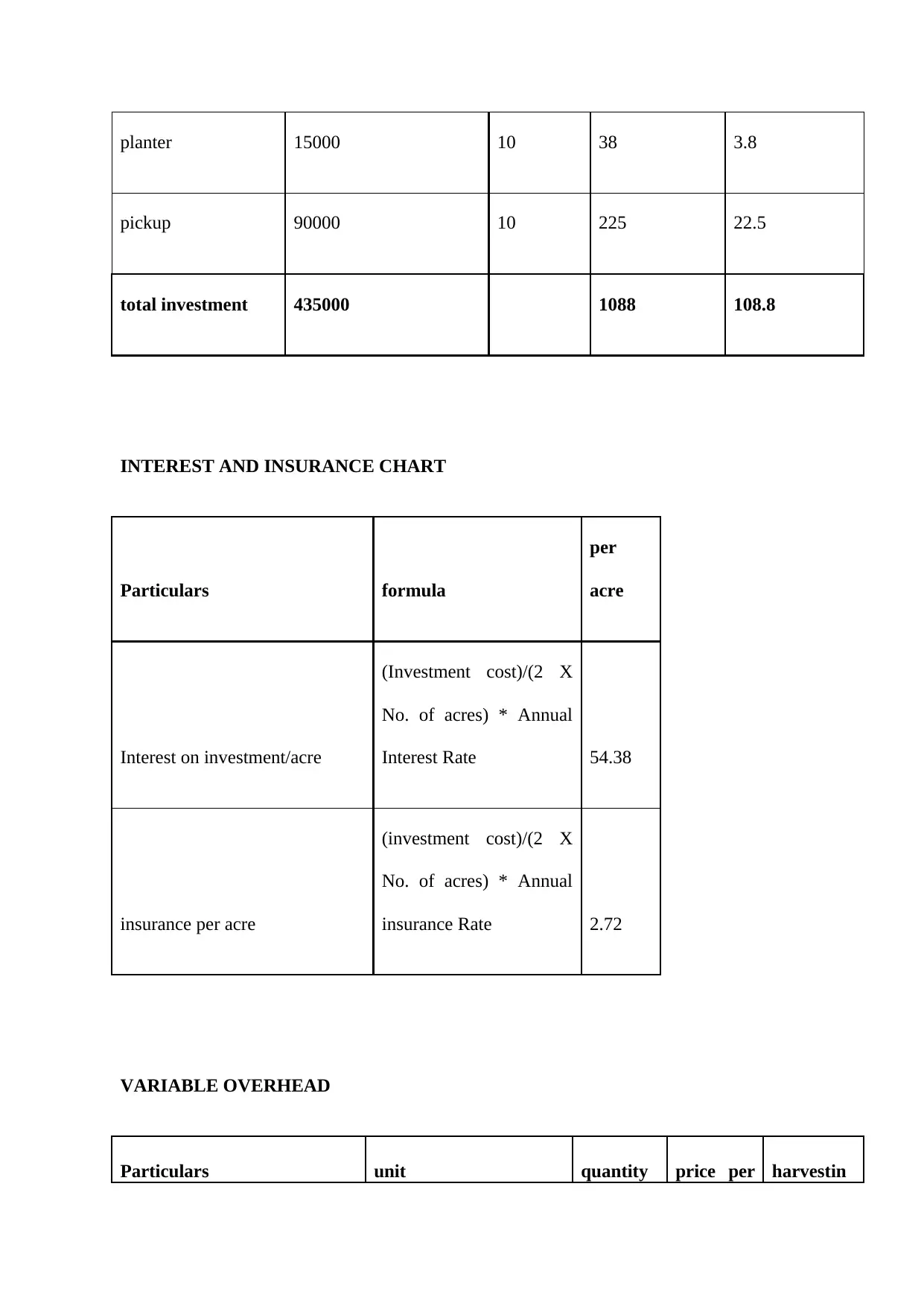

planter 15000 10 38 3.8

pickup 90000 10 225 22.5

total investment 435000 1088 108.8

INTEREST AND INSURANCE CHART

Particulars formula

per

acre

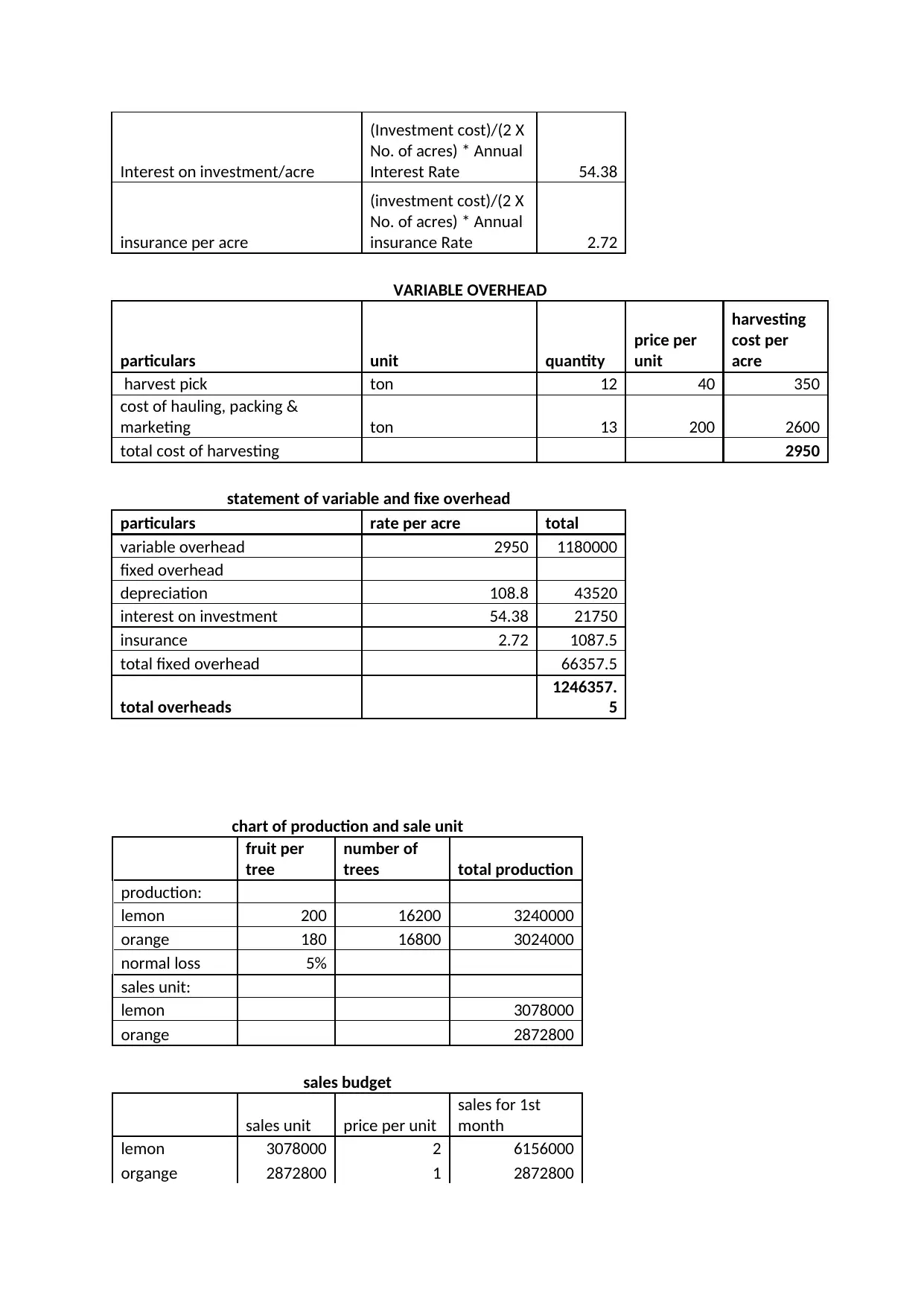

Interest on investment/acre

(Investment cost)/(2 X

No. of acres) * Annual

Interest Rate 54.38

insurance per acre

(investment cost)/(2 X

No. of acres) * Annual

insurance Rate 2.72

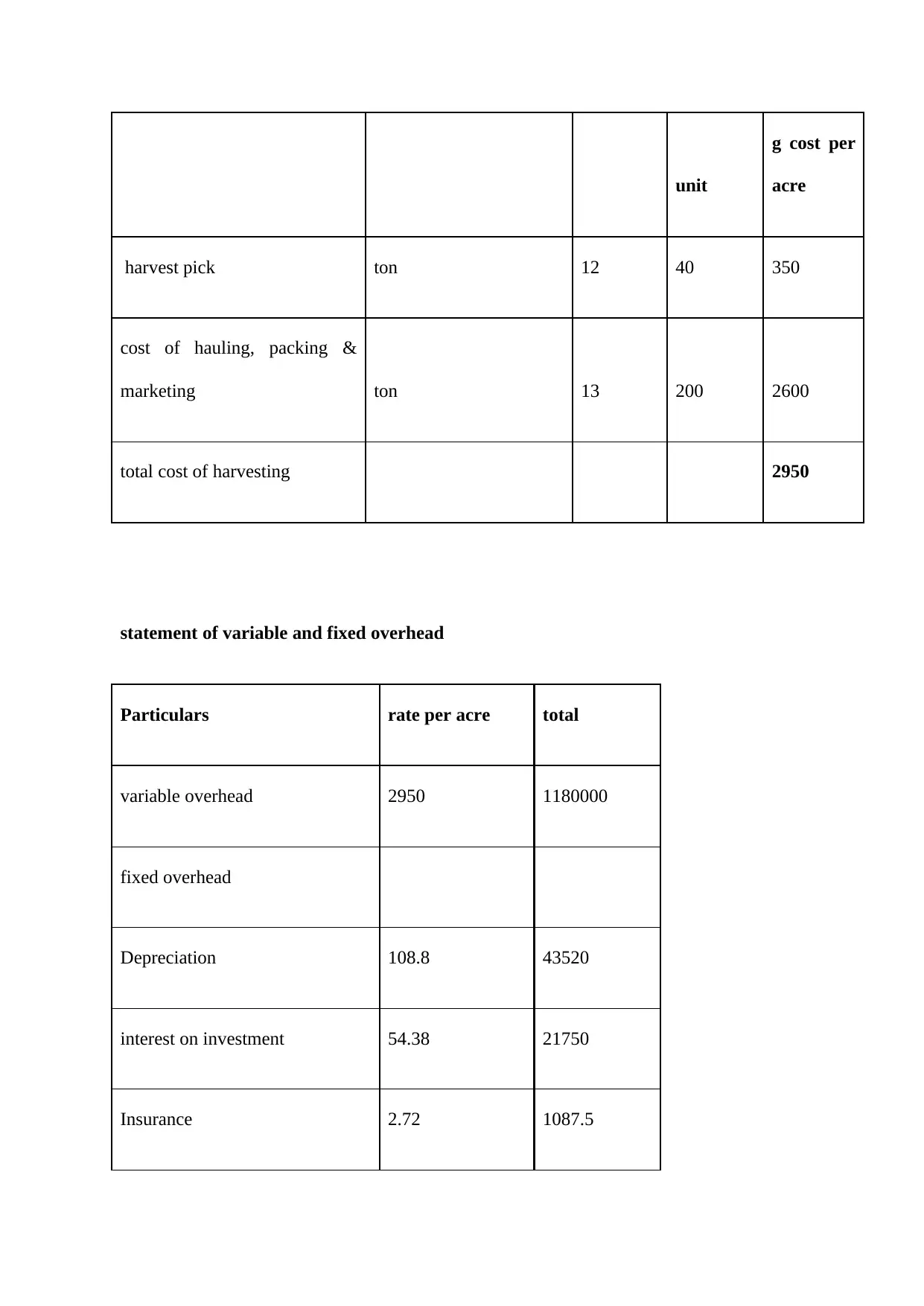

VARIABLE OVERHEAD

Particulars unit quantity price per harvestin

pickup 90000 10 225 22.5

total investment 435000 1088 108.8

INTEREST AND INSURANCE CHART

Particulars formula

per

acre

Interest on investment/acre

(Investment cost)/(2 X

No. of acres) * Annual

Interest Rate 54.38

insurance per acre

(investment cost)/(2 X

No. of acres) * Annual

insurance Rate 2.72

VARIABLE OVERHEAD

Particulars unit quantity price per harvestin

unit

g cost per

acre

harvest pick ton 12 40 350

cost of hauling, packing &

marketing ton 13 200 2600

total cost of harvesting 2950

statement of variable and fixed overhead

Particulars rate per acre total

variable overhead 2950 1180000

fixed overhead

Depreciation 108.8 43520

interest on investment 54.38 21750

Insurance 2.72 1087.5

g cost per

acre

harvest pick ton 12 40 350

cost of hauling, packing &

marketing ton 13 200 2600

total cost of harvesting 2950

statement of variable and fixed overhead

Particulars rate per acre total

variable overhead 2950 1180000

fixed overhead

Depreciation 108.8 43520

interest on investment 54.38 21750

Insurance 2.72 1087.5

total fixed overhead 66357.5

total overheads 1246357.5

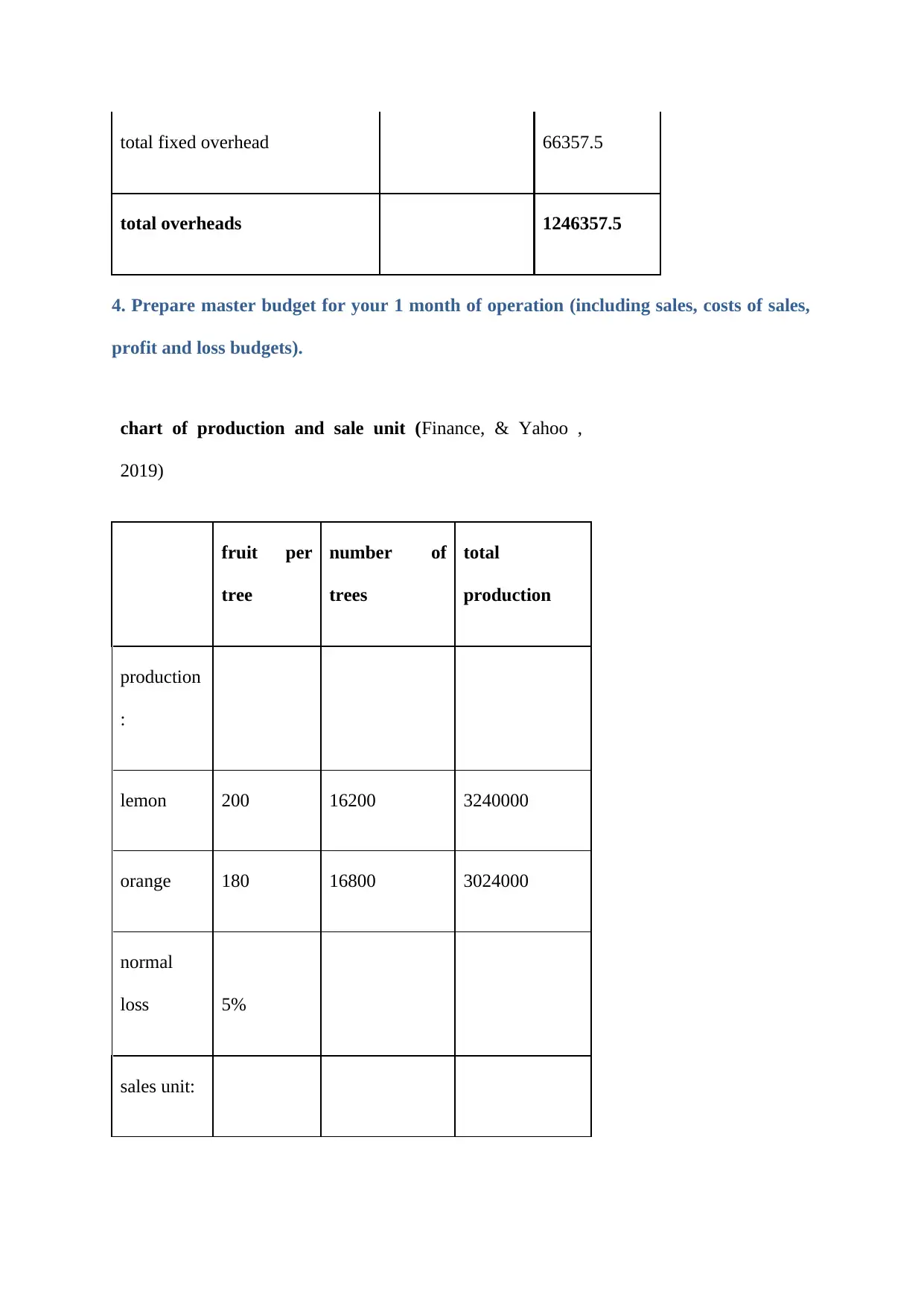

4. Prepare master budget for your 1 month of operation (including sales, costs of sales,

profit and loss budgets).

chart of production and sale unit (Finance, & Yahoo ,

2019)

fruit per

tree

number of

trees

total

production

production

:

lemon 200 16200 3240000

orange 180 16800 3024000

normal

loss 5%

sales unit:

total overheads 1246357.5

4. Prepare master budget for your 1 month of operation (including sales, costs of sales,

profit and loss budgets).

chart of production and sale unit (Finance, & Yahoo ,

2019)

fruit per

tree

number of

trees

total

production

production

:

lemon 200 16200 3240000

orange 180 16800 3024000

normal

loss 5%

sales unit:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

lemon 3078000

orange 2872800

sales budget

sales unit price per unit sales for 1st month

lemon 3078000 2 6156000

orange 2872800 1 2872800

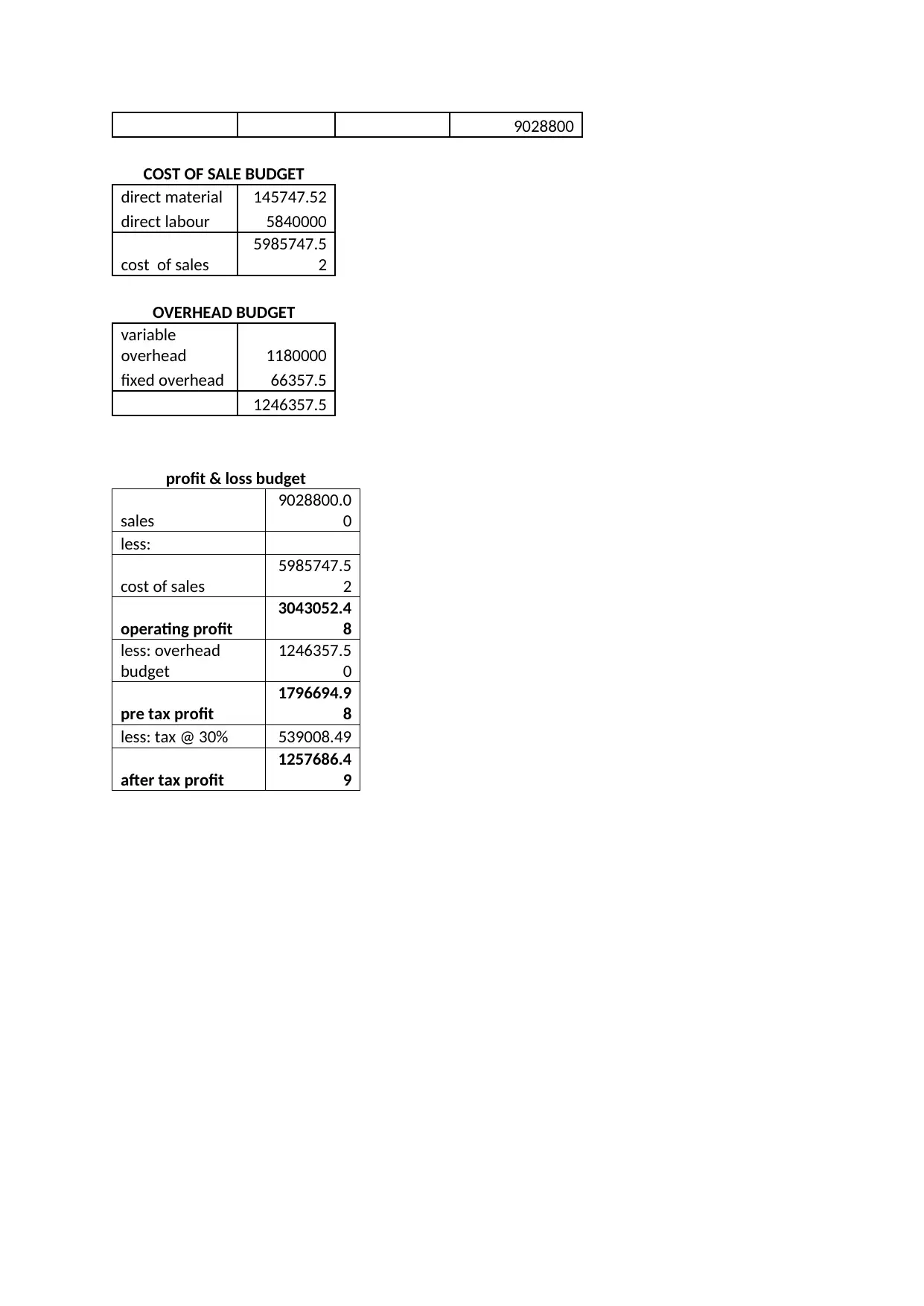

9028800

COST OF SALE

BUDGET

direct

material 145747.52

direct labour 5840000

orange 2872800

sales budget

sales unit price per unit sales for 1st month

lemon 3078000 2 6156000

orange 2872800 1 2872800

9028800

COST OF SALE

BUDGET

direct

material 145747.52

direct labour 5840000

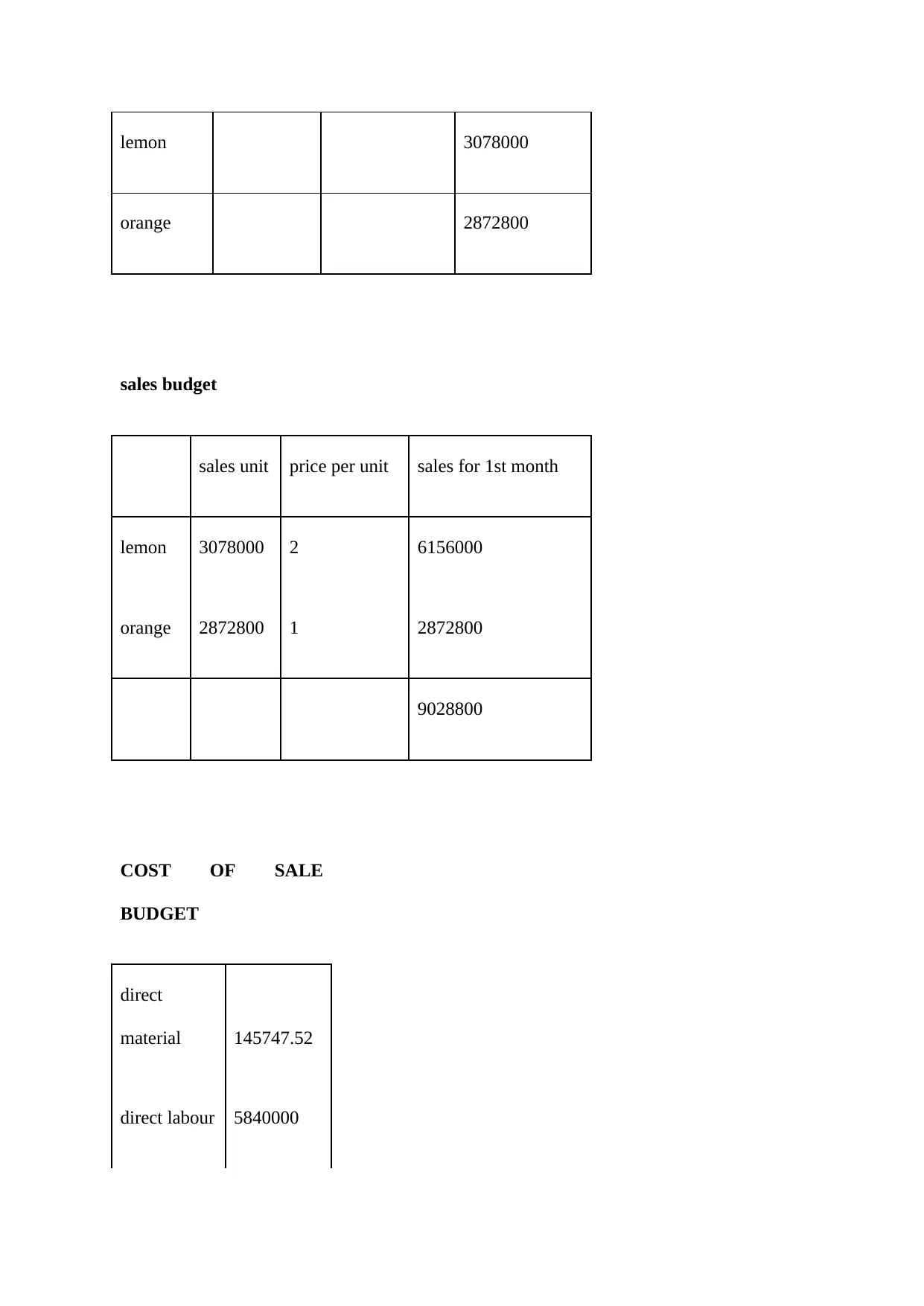

cost of sales 5985747.52

OVERHEAD BUDGET

variable

overhead 1180000

fixed overhead 66357.5

1246357.

5

profit & loss budget

sales

9028800.0

0

less:

cost of sales

5985747.5

2

operating profit 3043052.4

OVERHEAD BUDGET

variable

overhead 1180000

fixed overhead 66357.5

1246357.

5

profit & loss budget

sales

9028800.0

0

less:

cost of sales

5985747.5

2

operating profit 3043052.4

8

less: overhead

budget

1246357.5

0

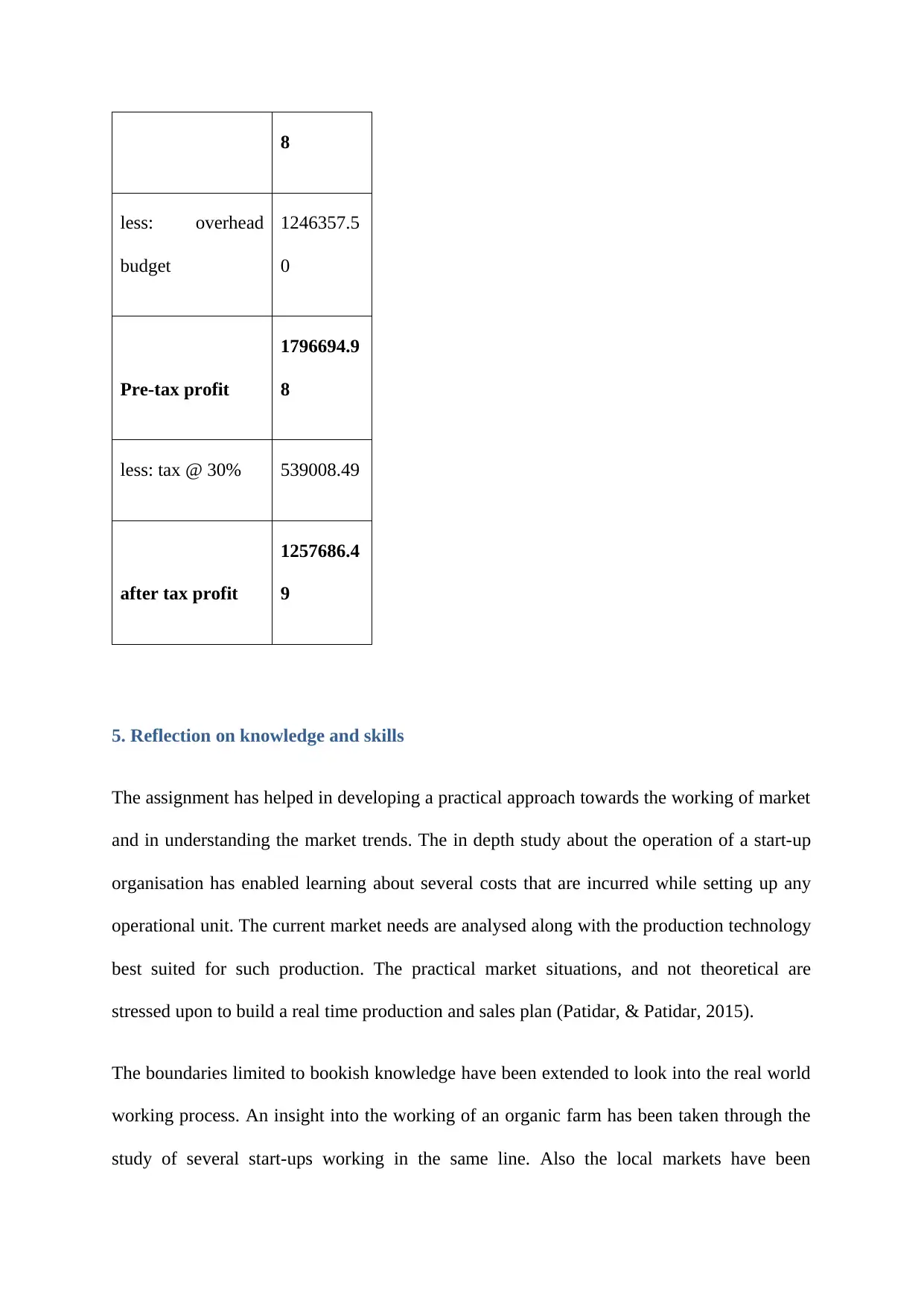

Pre-tax profit

1796694.9

8

less: tax @ 30% 539008.49

after tax profit

1257686.4

9

5. Reflection on knowledge and skills

The assignment has helped in developing a practical approach towards the working of market

and in understanding the market trends. The in depth study about the operation of a start-up

organisation has enabled learning about several costs that are incurred while setting up any

operational unit. The current market needs are analysed along with the production technology

best suited for such production. The practical market situations, and not theoretical are

stressed upon to build a real time production and sales plan (Patidar, & Patidar, 2015).

The boundaries limited to bookish knowledge have been extended to look into the real world

working process. An insight into the working of an organic farm has been taken through the

study of several start-ups working in the same line. Also the local markets have been

less: overhead

budget

1246357.5

0

Pre-tax profit

1796694.9

8

less: tax @ 30% 539008.49

after tax profit

1257686.4

9

5. Reflection on knowledge and skills

The assignment has helped in developing a practical approach towards the working of market

and in understanding the market trends. The in depth study about the operation of a start-up

organisation has enabled learning about several costs that are incurred while setting up any

operational unit. The current market needs are analysed along with the production technology

best suited for such production. The practical market situations, and not theoretical are

stressed upon to build a real time production and sales plan (Patidar, & Patidar, 2015).

The boundaries limited to bookish knowledge have been extended to look into the real world

working process. An insight into the working of an organic farm has been taken through the

study of several start-ups working in the same line. Also the local markets have been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

explored to understand the price at which the organic produce is best sold and accepted

willingly. The procedure towards production has also been studied (Jouzi, et. al 2017).

Therefore, after assessing all the details and case study, it could be inferred that company

prepare its budget with a view to control and assess the costing of the newly introduced

product and control the possible expenses.

willingly. The procedure towards production has also been studied (Jouzi, et. al 2017).

Therefore, after assessing all the details and case study, it could be inferred that company

prepare its budget with a view to control and assess the costing of the newly introduced

product and control the possible expenses.

References

Barker, A. V. (2016). Science and technology of organic farming. Australia: CRC Press.

Crowder, D. W., & Reganold, J. P. (2015). Financial competitiveness of organic agriculture on a

global scale. Proceedings of the National Academy of Sciences, 112(24), 7611-7616.

Garibaldi, L. A., Gemmill-Herren, B., D’Annolfo, R., Graeub, B. E., Cunningham, S. A., & Breeze,

T. D. (2017). Farming approaches for greater biodiversity, livelihoods, and food

security. Trends in ecology & evolution, 32(1), 68-80.

Jouzi, Z., Azadi, H., Taheri, F., Zarafshani, K., Gebrehiwot, K., Van Passel, S., & Lebailly, P.

(2017). Organic farming and small-scale farmers: Main opportunities and

challenges. Ecological Economics, 132(1), 144-154.

Niggli, U., Willer, H., & Baker, B. (2016). A global vision and strategy for organic farming research.

Patidar, S., & Patidar, H. (2015). A study of perception of farmers towards organic

farming. International Journal of Application or Innovation in Engineering &

Management, 4(3), 269-277.

Reganold, J. P., & Wachter, J. M. (2016). Organic agriculture in the twenty-first century. Nature

plants, 2(2), 15221.

Fraser, S., Bhaumik, S. k., & Wright, M. (2015). What do we know about entrepreneurial finance

and its relationship with growth. International Small Business Journal,, 33(1), 70-88.

Gao, , B., & Wong, T. Y. (2017). Long-Term Capital Budgeting and Incentive Mechanism. USA:

Pearson.

finance, Y., & Yahoo , F. (2019). Financial data. Retrieved from https://in.finance.yahoo.com/

Barker, A. V. (2016). Science and technology of organic farming. Australia: CRC Press.

Crowder, D. W., & Reganold, J. P. (2015). Financial competitiveness of organic agriculture on a

global scale. Proceedings of the National Academy of Sciences, 112(24), 7611-7616.

Garibaldi, L. A., Gemmill-Herren, B., D’Annolfo, R., Graeub, B. E., Cunningham, S. A., & Breeze,

T. D. (2017). Farming approaches for greater biodiversity, livelihoods, and food

security. Trends in ecology & evolution, 32(1), 68-80.

Jouzi, Z., Azadi, H., Taheri, F., Zarafshani, K., Gebrehiwot, K., Van Passel, S., & Lebailly, P.

(2017). Organic farming and small-scale farmers: Main opportunities and

challenges. Ecological Economics, 132(1), 144-154.

Niggli, U., Willer, H., & Baker, B. (2016). A global vision and strategy for organic farming research.

Patidar, S., & Patidar, H. (2015). A study of perception of farmers towards organic

farming. International Journal of Application or Innovation in Engineering &

Management, 4(3), 269-277.

Reganold, J. P., & Wachter, J. M. (2016). Organic agriculture in the twenty-first century. Nature

plants, 2(2), 15221.

Fraser, S., Bhaumik, S. k., & Wright, M. (2015). What do we know about entrepreneurial finance

and its relationship with growth. International Small Business Journal,, 33(1), 70-88.

Gao, , B., & Wong, T. Y. (2017). Long-Term Capital Budgeting and Incentive Mechanism. USA:

Pearson.

finance, Y., & Yahoo , F. (2019). Financial data. Retrieved from https://in.finance.yahoo.com/

Appendix

DETAILS

particulars

Orange seeds AU$ for 50 seeds

1.5

7

Lemon seeds AU$ for 10 seeds 1

Tree planting per acre of orange 84

per acre of lemon 81

Land acres 400

Manure rate in AU$ for 30 litres 4.5

manure per acre litre 20

Irrigation AU$ per acre 356

Labour people per acre 2

AU$ per day per labour 20

STATEMENT OF DIRECT COST

particulars unit per unit cost total AU$

direct material

seeds: orange 16800 0.0314 527.52

lemon 16200 0.1 1620

manure 8000 0.15 1200

irrigation 400 356 142400

total 145747.5

direct labour

labour cost 800 7300

584000

0

total direct costs

598574

8

DEPRECIATION CHART

particulars current rate useful life

per acre

investment

per acre

depreciatio

n

irrigation system 180000 10 450 45

tractor 150000 10 375 37.5

planter 15000 10 38 3.8

pickup 90000 10 225 22.5

total investment 435000 1088 108.8

INTEREST AND INSURANCE CHART

particulars formula per acre

DETAILS

particulars

Orange seeds AU$ for 50 seeds

1.5

7

Lemon seeds AU$ for 10 seeds 1

Tree planting per acre of orange 84

per acre of lemon 81

Land acres 400

Manure rate in AU$ for 30 litres 4.5

manure per acre litre 20

Irrigation AU$ per acre 356

Labour people per acre 2

AU$ per day per labour 20

STATEMENT OF DIRECT COST

particulars unit per unit cost total AU$

direct material

seeds: orange 16800 0.0314 527.52

lemon 16200 0.1 1620

manure 8000 0.15 1200

irrigation 400 356 142400

total 145747.5

direct labour

labour cost 800 7300

584000

0

total direct costs

598574

8

DEPRECIATION CHART

particulars current rate useful life

per acre

investment

per acre

depreciatio

n

irrigation system 180000 10 450 45

tractor 150000 10 375 37.5

planter 15000 10 38 3.8

pickup 90000 10 225 22.5

total investment 435000 1088 108.8

INTEREST AND INSURANCE CHART

particulars formula per acre

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Interest on investment/acre

(Investment cost)/(2 X

No. of acres) * Annual

Interest Rate 54.38

insurance per acre

(investment cost)/(2 X

No. of acres) * Annual

insurance Rate 2.72

VARIABLE OVERHEAD

particulars unit quantity

price per

unit

harvesting

cost per

acre

harvest pick ton 12 40 350

cost of hauling, packing &

marketing ton 13 200 2600

total cost of harvesting 2950

statement of variable and fixe overhead

particulars rate per acre total

variable overhead 2950 1180000

fixed overhead

depreciation 108.8 43520

interest on investment 54.38 21750

insurance 2.72 1087.5

total fixed overhead 66357.5

total overheads

1246357.

5

chart of production and sale unit

fruit per

tree

number of

trees total production

production:

lemon 200 16200 3240000

orange 180 16800 3024000

normal loss 5%

sales unit:

lemon 3078000

orange 2872800

sales budget

sales unit price per unit

sales for 1st

month

lemon 3078000 2 6156000

organge 2872800 1 2872800

(Investment cost)/(2 X

No. of acres) * Annual

Interest Rate 54.38

insurance per acre

(investment cost)/(2 X

No. of acres) * Annual

insurance Rate 2.72

VARIABLE OVERHEAD

particulars unit quantity

price per

unit

harvesting

cost per

acre

harvest pick ton 12 40 350

cost of hauling, packing &

marketing ton 13 200 2600

total cost of harvesting 2950

statement of variable and fixe overhead

particulars rate per acre total

variable overhead 2950 1180000

fixed overhead

depreciation 108.8 43520

interest on investment 54.38 21750

insurance 2.72 1087.5

total fixed overhead 66357.5

total overheads

1246357.

5

chart of production and sale unit

fruit per

tree

number of

trees total production

production:

lemon 200 16200 3240000

orange 180 16800 3024000

normal loss 5%

sales unit:

lemon 3078000

orange 2872800

sales budget

sales unit price per unit

sales for 1st

month

lemon 3078000 2 6156000

organge 2872800 1 2872800

9028800

COST OF SALE BUDGET

direct material 145747.52

direct labour 5840000

cost of sales

5985747.5

2

OVERHEAD BUDGET

variable

overhead 1180000

fixed overhead 66357.5

1246357.5

profit & loss budget

sales

9028800.0

0

less:

cost of sales

5985747.5

2

operating profit

3043052.4

8

less: overhead

budget

1246357.5

0

pre tax profit

1796694.9

8

less: tax @ 30% 539008.49

after tax profit

1257686.4

9

COST OF SALE BUDGET

direct material 145747.52

direct labour 5840000

cost of sales

5985747.5

2

OVERHEAD BUDGET

variable

overhead 1180000

fixed overhead 66357.5

1246357.5

profit & loss budget

sales

9028800.0

0

less:

cost of sales

5985747.5

2

operating profit

3043052.4

8

less: overhead

budget

1246357.5

0

pre tax profit

1796694.9

8

less: tax @ 30% 539008.49

after tax profit

1257686.4

9

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.