International Finance: BHP Billiton, Bruin Aircraft, Beacon Lighting, UniSuper

VerifiedAdded on 2023/04/21

|11

|2050

|351

AI Summary

This assignment explores various topics in international finance, including the flow of funds in BHP Billiton, medium-term loans of Citigroup, factors affecting the demand for pounds in Australia, production cost analysis in Beacon Lighting, and investment opportunities in Poland for UniSuper.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUS 330 INTERNATIONAL FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Table of Contents

Introduction......................................................................................................................................3

Chapter 3: BHP Billiton.................................................................................................................3

A. Flow of BHP’s fund................................................................................................................3

B. Medium-Term Loans of Citigroup..........................................................................................3

Chapter 5: Bruin Aircraft Pty Ltd....................................................................................................5

Chapter 6: Beacon Lighting.............................................................................................................7

A. Scenario description regarding high production cost..............................................................7

B. Incurring high production cost................................................................................................7

C. Stability of Australian dollar outflow......................................................................................7

D. Relationship with Alibaba.......................................................................................................8

Chapter 7: UniSuper........................................................................................................................9

A. Investing in Poland..................................................................................................................9

B. Covering arbitrage of interest..................................................................................................9

C. Risk in covering arbitrage.....................................................................................................10

D. Choosing between Australian treasury bills and covered interest arbitrage.........................10

Conclusion.....................................................................................................................................10

Reference List:...............................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Chapter 3: BHP Billiton.................................................................................................................3

A. Flow of BHP’s fund................................................................................................................3

B. Medium-Term Loans of Citigroup..........................................................................................3

Chapter 5: Bruin Aircraft Pty Ltd....................................................................................................5

Chapter 6: Beacon Lighting.............................................................................................................7

A. Scenario description regarding high production cost..............................................................7

B. Incurring high production cost................................................................................................7

C. Stability of Australian dollar outflow......................................................................................7

D. Relationship with Alibaba.......................................................................................................8

Chapter 7: UniSuper........................................................................................................................9

A. Investing in Poland..................................................................................................................9

B. Covering arbitrage of interest..................................................................................................9

C. Risk in covering arbitrage.....................................................................................................10

D. Choosing between Australian treasury bills and covered interest arbitrage.........................10

Conclusion.....................................................................................................................................10

Reference List:...............................................................................................................................11

3

Introduction

Exchange rates freely float that corresponds to frequent fluctuations and this depends on various

factors, which will be detailed in this current assignment. This task is based on the international

financial market. BHP Billiton is a multinational company of Australia that has eight subsidiary

companies. Detail several factors impact exchange rates along with scenario for increasing

production rate would also in this current section.

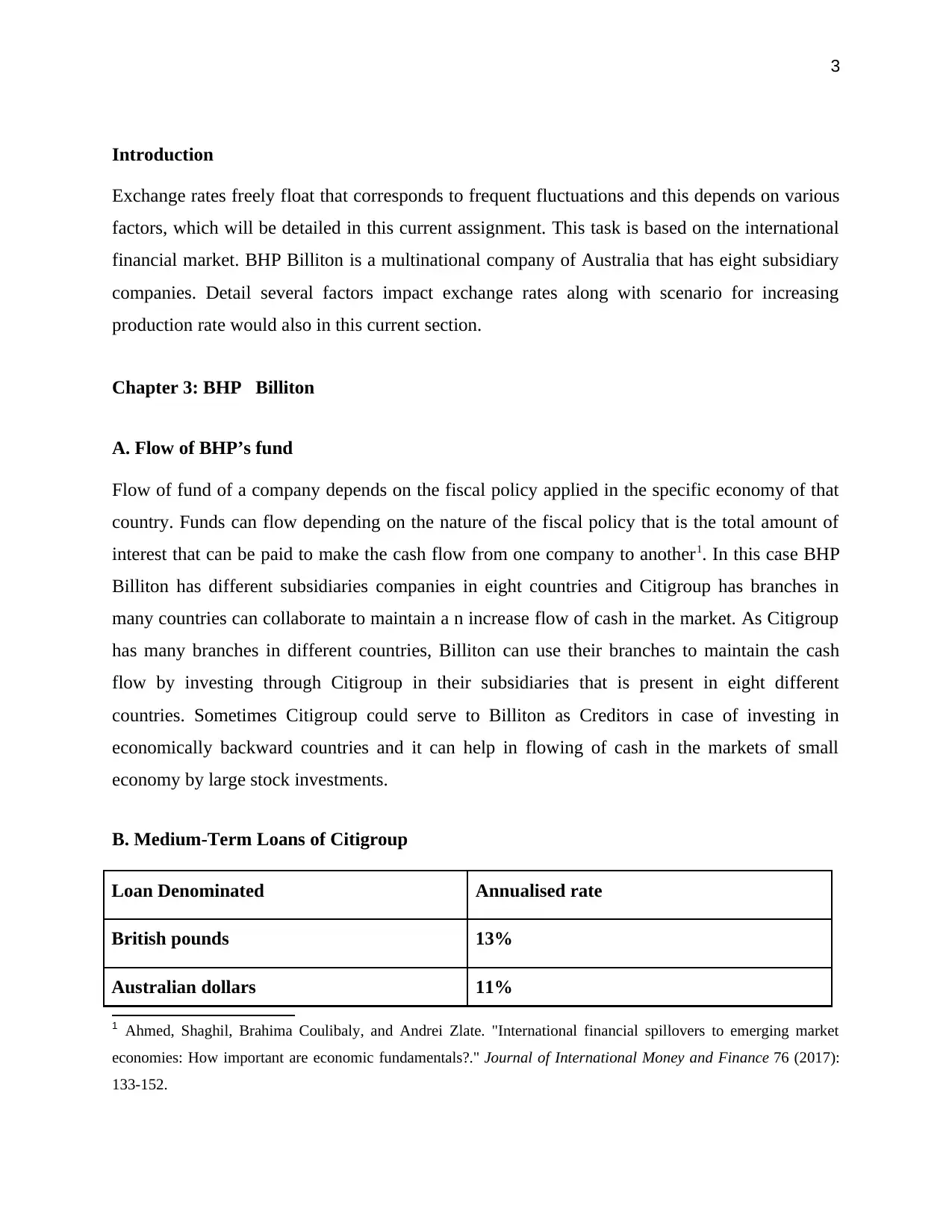

Chapter 3: BHP Billiton

A. Flow of BHP’s fund

Flow of fund of a company depends on the fiscal policy applied in the specific economy of that

country. Funds can flow depending on the nature of the fiscal policy that is the total amount of

interest that can be paid to make the cash flow from one company to another1. In this case BHP

Billiton has different subsidiaries companies in eight countries and Citigroup has branches in

many countries can collaborate to maintain a n increase flow of cash in the market. As Citigroup

has many branches in different countries, Billiton can use their branches to maintain the cash

flow by investing through Citigroup in their subsidiaries that is present in eight different

countries. Sometimes Citigroup could serve to Billiton as Creditors in case of investing in

economically backward countries and it can help in flowing of cash in the markets of small

economy by large stock investments.

B. Medium-Term Loans of Citigroup

Loan Denominated Annualised rate

British pounds 13%

Australian dollars 11%

1 Ahmed, Shaghil, Brahima Coulibaly, and Andrei Zlate. "International financial spillovers to emerging market

economies: How important are economic fundamentals?." Journal of International Money and Finance 76 (2017):

133-152.

Introduction

Exchange rates freely float that corresponds to frequent fluctuations and this depends on various

factors, which will be detailed in this current assignment. This task is based on the international

financial market. BHP Billiton is a multinational company of Australia that has eight subsidiary

companies. Detail several factors impact exchange rates along with scenario for increasing

production rate would also in this current section.

Chapter 3: BHP Billiton

A. Flow of BHP’s fund

Flow of fund of a company depends on the fiscal policy applied in the specific economy of that

country. Funds can flow depending on the nature of the fiscal policy that is the total amount of

interest that can be paid to make the cash flow from one company to another1. In this case BHP

Billiton has different subsidiaries companies in eight countries and Citigroup has branches in

many countries can collaborate to maintain a n increase flow of cash in the market. As Citigroup

has many branches in different countries, Billiton can use their branches to maintain the cash

flow by investing through Citigroup in their subsidiaries that is present in eight different

countries. Sometimes Citigroup could serve to Billiton as Creditors in case of investing in

economically backward countries and it can help in flowing of cash in the markets of small

economy by large stock investments.

B. Medium-Term Loans of Citigroup

Loan Denominated Annualised rate

British pounds 13%

Australian dollars 11%

1 Ahmed, Shaghil, Brahima Coulibaly, and Andrei Zlate. "International financial spillovers to emerging market

economies: How important are economic fundamentals?." Journal of International Money and Finance 76 (2017):

133-152.

4

Canadian dollars 10%

Japanese yen 8%

Table 1: Medium-term loan interest percentage

(Source: Given by the researcher)

British subsidiaries could use Japanese yen as the interest rate is less compared to remaining

currencies that are British Pounds, Australian Dollars and Canadian Dollars. Medium term loan

refers to the loan given by main companies to their subsidiary branches. In this case, Citigroup is

the medium of passing the loan from Billiton to their subsidiary companies. Japanese yen is

giving only 8% interest on the loan, which means there will be more chances of investment in

those countries where the subsidiaries will give increase returns to the loan.

Canadian dollars 10%

Japanese yen 8%

Table 1: Medium-term loan interest percentage

(Source: Given by the researcher)

British subsidiaries could use Japanese yen as the interest rate is less compared to remaining

currencies that are British Pounds, Australian Dollars and Canadian Dollars. Medium term loan

refers to the loan given by main companies to their subsidiary branches. In this case, Citigroup is

the medium of passing the loan from Billiton to their subsidiary companies. Japanese yen is

giving only 8% interest on the loan, which means there will be more chances of investment in

those countries where the subsidiaries will give increase returns to the loan.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

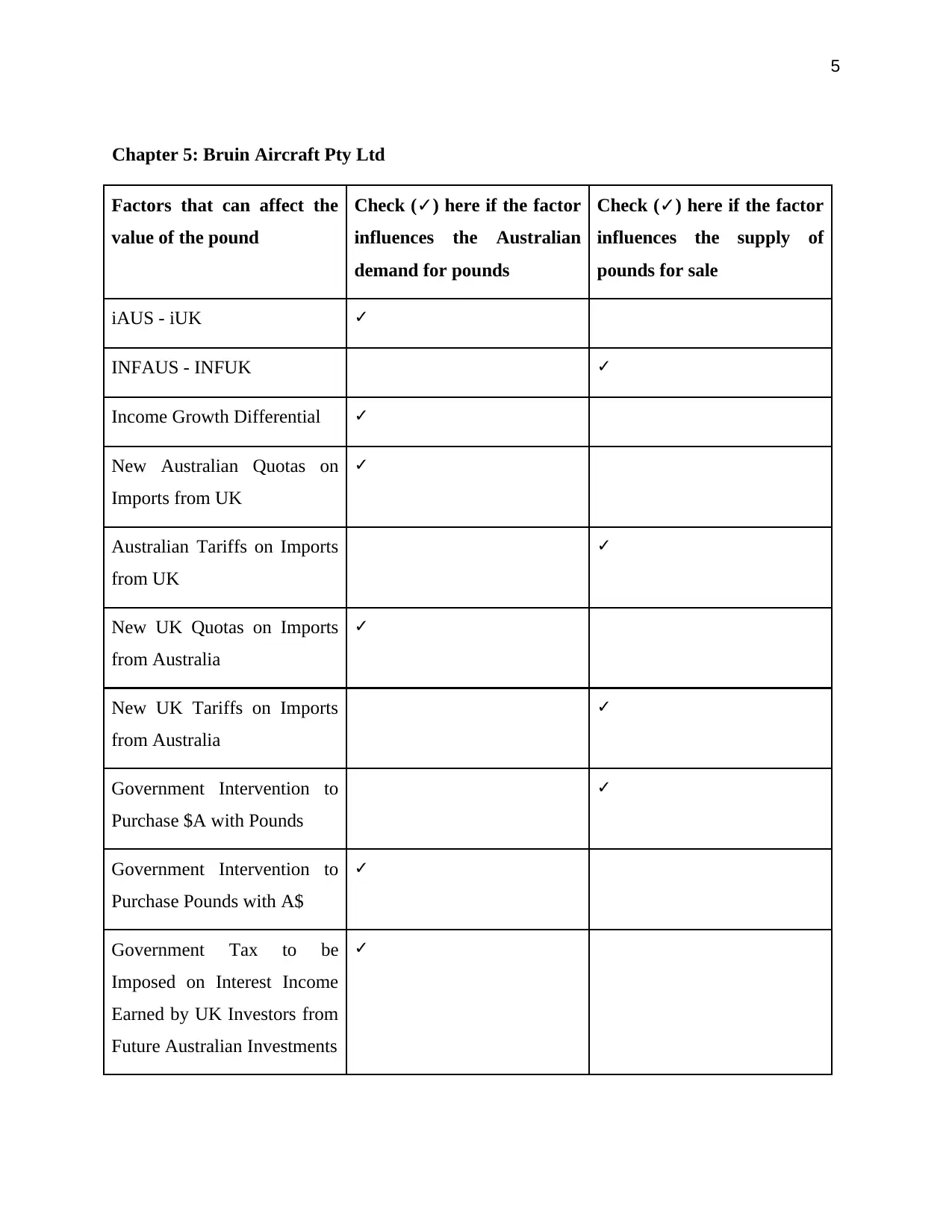

Chapter 5: Bruin Aircraft Pty Ltd

Factors that can affect the

value of the pound

Check (✓) here if the factor

influences the Australian

demand for pounds

Check (✓) here if the factor

influences the supply of

pounds for sale

iAUS - iUK ✓

INFAUS - INFUK ✓

Income Growth Differential ✓

New Australian Quotas on

Imports from UK

✓

Australian Tariffs on Imports

from UK

✓

New UK Quotas on Imports

from Australia

✓

New UK Tariffs on Imports

from Australia

✓

Government Intervention to

Purchase $A with Pounds

✓

Government Intervention to

Purchase Pounds with A$

✓

Government Tax to be

Imposed on Interest Income

Earned by UK Investors from

Future Australian Investments

✓

Chapter 5: Bruin Aircraft Pty Ltd

Factors that can affect the

value of the pound

Check (✓) here if the factor

influences the Australian

demand for pounds

Check (✓) here if the factor

influences the supply of

pounds for sale

iAUS - iUK ✓

INFAUS - INFUK ✓

Income Growth Differential ✓

New Australian Quotas on

Imports from UK

✓

Australian Tariffs on Imports

from UK

✓

New UK Quotas on Imports

from Australia

✓

New UK Tariffs on Imports

from Australia

✓

Government Intervention to

Purchase $A with Pounds

✓

Government Intervention to

Purchase Pounds with A$

✓

Government Tax to be

Imposed on Interest Income

Earned by UK Investors from

Future Australian Investments

✓

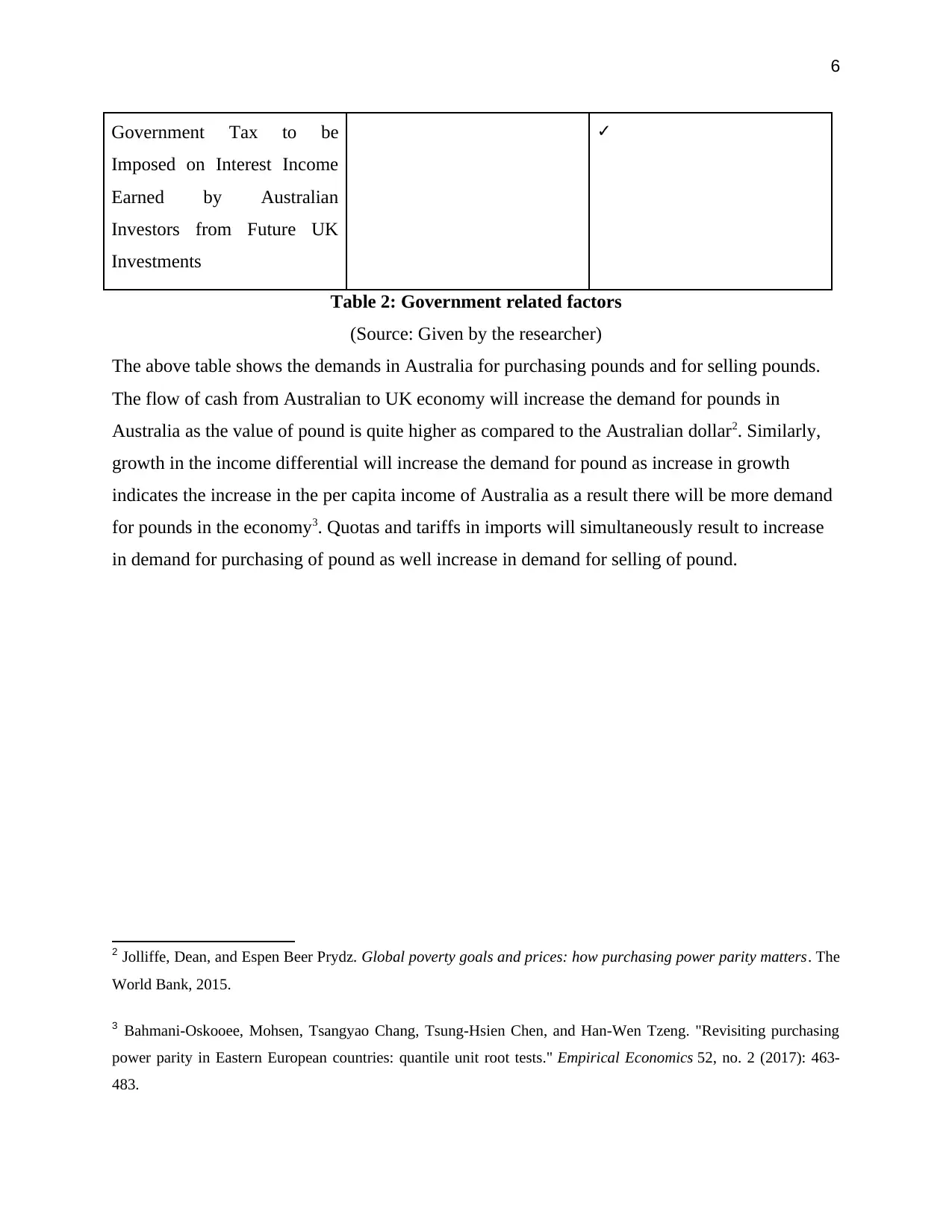

6

Government Tax to be

Imposed on Interest Income

Earned by Australian

Investors from Future UK

Investments

✓

Table 2: Government related factors

(Source: Given by the researcher)

The above table shows the demands in Australia for purchasing pounds and for selling pounds.

The flow of cash from Australian to UK economy will increase the demand for pounds in

Australia as the value of pound is quite higher as compared to the Australian dollar2. Similarly,

growth in the income differential will increase the demand for pound as increase in growth

indicates the increase in the per capita income of Australia as a result there will be more demand

for pounds in the economy3. Quotas and tariffs in imports will simultaneously result to increase

in demand for purchasing of pound as well increase in demand for selling of pound.

2 Jolliffe, Dean, and Espen Beer Prydz. Global poverty goals and prices: how purchasing power parity matters. The

World Bank, 2015.

3 Bahmani-Oskooee, Mohsen, Tsangyao Chang, Tsung-Hsien Chen, and Han-Wen Tzeng. "Revisiting purchasing

power parity in Eastern European countries: quantile unit root tests." Empirical Economics 52, no. 2 (2017): 463-

483.

Government Tax to be

Imposed on Interest Income

Earned by Australian

Investors from Future UK

Investments

✓

Table 2: Government related factors

(Source: Given by the researcher)

The above table shows the demands in Australia for purchasing pounds and for selling pounds.

The flow of cash from Australian to UK economy will increase the demand for pounds in

Australia as the value of pound is quite higher as compared to the Australian dollar2. Similarly,

growth in the income differential will increase the demand for pound as increase in growth

indicates the increase in the per capita income of Australia as a result there will be more demand

for pounds in the economy3. Quotas and tariffs in imports will simultaneously result to increase

in demand for purchasing of pound as well increase in demand for selling of pound.

2 Jolliffe, Dean, and Espen Beer Prydz. Global poverty goals and prices: how purchasing power parity matters. The

World Bank, 2015.

3 Bahmani-Oskooee, Mohsen, Tsangyao Chang, Tsung-Hsien Chen, and Han-Wen Tzeng. "Revisiting purchasing

power parity in Eastern European countries: quantile unit root tests." Empirical Economics 52, no. 2 (2017): 463-

483.

7

Chapter 6: Beacon Lighting

A. Scenario description regarding high production cost

Beacon lighting can decrease the production cost a little bit by purchasing raw materials of lamps

from Alibaba. The raw materials can be produced in the manufacturing department of Beacon

Lighting and as a result, the cost of production can be minimised as the importing costs of raw

materials for manufacturing lamps can be much less than already manufactured lamps4. This can

lead to increase in profit more than 20%.

B. Incurring high production cost

Beacon lighting imports part of lamps from Alibaba China, which causes them a specific amount

of cost in Australian Dollar. This Australian dollar when translated to Chinese Yuan the price

gets automatically high for Alibaba, but the rising inflation in China can cause to the change of

Yuan value compared to Australian dollar. In that situation once, Beacon imports manufactured

lights from China then they will suffer from high production cost. Beacon will be profited if they

manufacture the lights in Australia, as the cost-incurred value will be same as the revenue

incurred value.

C. Stability of Australian dollar outflow

Beacon can experience stable Australian dollar outflow payments to Alibaba, as the current

situation of China is that the value of Chinese Yuan is increasing due to inflation in their country

but similarly the value of Australian dollar is also increasing due to the inflation in Australian

economy. The cost of production paid to Alibaba will be Stable as the difference is quite high

between Australian dollar and Chinese Yuan5. So, as a result Beacon will experience stable

Australian dollar outflow.

4 Ocampo, José Antonio. "International Asymmetries and the Design of the International Financial System 1."

In Critical Issues in International Financial Reform, pp. 45-74. Routledge, 2018.

5 Bech, Morten L., and Aytek Malkhozov. "How have central banks implemented negative policy rates?." BIS

Quarterly Review March (2016).

Chapter 6: Beacon Lighting

A. Scenario description regarding high production cost

Beacon lighting can decrease the production cost a little bit by purchasing raw materials of lamps

from Alibaba. The raw materials can be produced in the manufacturing department of Beacon

Lighting and as a result, the cost of production can be minimised as the importing costs of raw

materials for manufacturing lamps can be much less than already manufactured lamps4. This can

lead to increase in profit more than 20%.

B. Incurring high production cost

Beacon lighting imports part of lamps from Alibaba China, which causes them a specific amount

of cost in Australian Dollar. This Australian dollar when translated to Chinese Yuan the price

gets automatically high for Alibaba, but the rising inflation in China can cause to the change of

Yuan value compared to Australian dollar. In that situation once, Beacon imports manufactured

lights from China then they will suffer from high production cost. Beacon will be profited if they

manufacture the lights in Australia, as the cost-incurred value will be same as the revenue

incurred value.

C. Stability of Australian dollar outflow

Beacon can experience stable Australian dollar outflow payments to Alibaba, as the current

situation of China is that the value of Chinese Yuan is increasing due to inflation in their country

but similarly the value of Australian dollar is also increasing due to the inflation in Australian

economy. The cost of production paid to Alibaba will be Stable as the difference is quite high

between Australian dollar and Chinese Yuan5. So, as a result Beacon will experience stable

Australian dollar outflow.

4 Ocampo, José Antonio. "International Asymmetries and the Design of the International Financial System 1."

In Critical Issues in International Financial Reform, pp. 45-74. Routledge, 2018.

5 Bech, Morten L., and Aytek Malkhozov. "How have central banks implemented negative policy rates?." BIS

Quarterly Review March (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

D. Relationship with Alibaba

The relationship of Beacon with Alibaba can change the amount risks as all the manufacturing

work is done by Alibaba. Beacon is involved in buying the manufactured lamps and then

importing those lamps and selling them in Australia. Manufacturing process needs a huge criteria

and different skilled workers with innovative methods, but importing from Alibaba is quite

affordable and risks in manufacturing are not involved with Beacon.

D. Relationship with Alibaba

The relationship of Beacon with Alibaba can change the amount risks as all the manufacturing

work is done by Alibaba. Beacon is involved in buying the manufactured lamps and then

importing those lamps and selling them in Australia. Manufacturing process needs a huge criteria

and different skilled workers with innovative methods, but importing from Alibaba is quite

affordable and risks in manufacturing are not involved with Beacon.

9

Chapter 7: UniSuper

A. Investing in Poland

Investing in Poland is a critical idea as the value of Poland Zloty is A$0.40 which is quite low

compared to other countries but the amount of investment return in Poland is 14% that is much

higher than the current return percentage in Australia that is 9%. After viewing this two

perspectives investment in Poland will be profitable medium as the increase investment return

can help in earning of lump sum amount of profit6.

B. Covering arbitrage of interest

Covering the interest arbitrage can be done by investing in minimum subdivided parts. In other

words, the investment should be done in more than four companies or investment areas like

government bonds, shares and others as this can help in earning interest return from different

subdivided parts, which will result in earning profit7. If loss is incurred then also it cannot affect

the investment as much it could if invested in a single investment area.

Parameters Investment Interest Interest return

Australian Treasury Bills 10000000 14% 14000

Poland covered interest arbitrage 4000000 9% 3600

Australian Treasury Bills 10000000 14% 14000

Poland covered interest arbitrage 3900000 9% 3510

Table 3: Covering arbitrage of interest

(Source: Given by the researcher)

6 Rime, Dagfinn, Andreas Schrimpf, and Olav Syrstad. "Segmented money markets and covered interest parity

arbitrage." (2017).

7 Engel, Charles, Nelson C. Mark, and Kenneth D. West. "Factor model forecasts of exchange rates." Econometric

Reviews 34, no. 1-2 (2015): 32-55.

Chapter 7: UniSuper

A. Investing in Poland

Investing in Poland is a critical idea as the value of Poland Zloty is A$0.40 which is quite low

compared to other countries but the amount of investment return in Poland is 14% that is much

higher than the current return percentage in Australia that is 9%. After viewing this two

perspectives investment in Poland will be profitable medium as the increase investment return

can help in earning of lump sum amount of profit6.

B. Covering arbitrage of interest

Covering the interest arbitrage can be done by investing in minimum subdivided parts. In other

words, the investment should be done in more than four companies or investment areas like

government bonds, shares and others as this can help in earning interest return from different

subdivided parts, which will result in earning profit7. If loss is incurred then also it cannot affect

the investment as much it could if invested in a single investment area.

Parameters Investment Interest Interest return

Australian Treasury Bills 10000000 14% 14000

Poland covered interest arbitrage 4000000 9% 3600

Australian Treasury Bills 10000000 14% 14000

Poland covered interest arbitrage 3900000 9% 3510

Table 3: Covering arbitrage of interest

(Source: Given by the researcher)

6 Rime, Dagfinn, Andreas Schrimpf, and Olav Syrstad. "Segmented money markets and covered interest parity

arbitrage." (2017).

7 Engel, Charles, Nelson C. Mark, and Kenneth D. West. "Factor model forecasts of exchange rates." Econometric

Reviews 34, no. 1-2 (2015): 32-55.

10

C. Risk in covering arbitrage

The risk that is involved in covering the arbitrage is the deflation in Poland economy. The

decrease in the value of their currency that is Poland Zloty is the main risk factor in covering the

arbitrage.

D. Choosing between Australian treasury bills and covered interest arbitrage

Australian treasury bills will be more profitable as the currency value of Poland is much higher

compared to Australian dollar and the deflation in their economy can cause to incurring loss

from investment. Australian treasury bills is profitable than covered interest arbitrage.

Conclusion

It can be concluded that the value of Australian currency depends on the inflationary measures

taken in the economy. It could be said that flow of funds are analysed by the central bank of the

respective nation. The risks factors involved in investment in Poland can be managed by

investing in small and limited units in multiple subdivided parts of their investment area. This, it

could also be said that investing in foreign countries instead of manufacturing in own country

can be a profitable measures for companies in Australia.

C. Risk in covering arbitrage

The risk that is involved in covering the arbitrage is the deflation in Poland economy. The

decrease in the value of their currency that is Poland Zloty is the main risk factor in covering the

arbitrage.

D. Choosing between Australian treasury bills and covered interest arbitrage

Australian treasury bills will be more profitable as the currency value of Poland is much higher

compared to Australian dollar and the deflation in their economy can cause to incurring loss

from investment. Australian treasury bills is profitable than covered interest arbitrage.

Conclusion

It can be concluded that the value of Australian currency depends on the inflationary measures

taken in the economy. It could be said that flow of funds are analysed by the central bank of the

respective nation. The risks factors involved in investment in Poland can be managed by

investing in small and limited units in multiple subdivided parts of their investment area. This, it

could also be said that investing in foreign countries instead of manufacturing in own country

can be a profitable measures for companies in Australia.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

Reference List

Ahmed, Shaghil, Brahima Coulibaly, and Andrei Zlate. "International financial spillovers to

emerging market economies: How important are economic fundamentals?." Journal of

International Money and Finance 76 (2017): 133-152.

Bahmani-Oskooee, Mohsen, Tsangyao Chang, Tsung-Hsien Chen, and Han-Wen Tzeng.

"Revisiting purchasing power parity in Eastern European countries: quantile unit root

tests." Empirical Economics 52, no. 2 (2017): 463-483.

Bech, Morten L., and Aytek Malkhozov. "How have central banks implemented negative policy

rates?." BIS Quarterly Review March (2016).

Engel, Charles, Nelson C. Mark, and Kenneth D. West. "Factor model forecasts of exchange

rates." Econometric Reviews 34, no. 1-2 (2015): 32-55.

Jolliffe, Dean, and Espen Beer Prydz. Global poverty goals and prices: how purchasing power

parity matters. The World Bank, 2015.

Ocampo, José Antonio. "International Asymmetries and the Design of the International Financial

System 1." In Critical Issues in International Financial Reform, pp. 45-74. Routledge, 2018.

Rime, Dagfinn, Andreas Schrimpf, and Olav Syrstad. "Segmented money markets and covered

interest parity arbitrage." (2017).

Reference List

Ahmed, Shaghil, Brahima Coulibaly, and Andrei Zlate. "International financial spillovers to

emerging market economies: How important are economic fundamentals?." Journal of

International Money and Finance 76 (2017): 133-152.

Bahmani-Oskooee, Mohsen, Tsangyao Chang, Tsung-Hsien Chen, and Han-Wen Tzeng.

"Revisiting purchasing power parity in Eastern European countries: quantile unit root

tests." Empirical Economics 52, no. 2 (2017): 463-483.

Bech, Morten L., and Aytek Malkhozov. "How have central banks implemented negative policy

rates?." BIS Quarterly Review March (2016).

Engel, Charles, Nelson C. Mark, and Kenneth D. West. "Factor model forecasts of exchange

rates." Econometric Reviews 34, no. 1-2 (2015): 32-55.

Jolliffe, Dean, and Espen Beer Prydz. Global poverty goals and prices: how purchasing power

parity matters. The World Bank, 2015.

Ocampo, José Antonio. "International Asymmetries and the Design of the International Financial

System 1." In Critical Issues in International Financial Reform, pp. 45-74. Routledge, 2018.

Rime, Dagfinn, Andreas Schrimpf, and Olav Syrstad. "Segmented money markets and covered

interest parity arbitrage." (2017).

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.