BUS2002 Management Accounting: ABC System Implementation Case Study

VerifiedAdded on 2023/06/15

|10

|2585

|429

Case Study

AI Summary

This case study delves into activity-based costing (ABC) and its practical application within the context of 'AM,' focusing on product-line profitability. It elaborates on the development, challenges, and application of ABC, contrasting it with simple/traditional costing systems to prepare product-line profitability reports. The study further explores the new insights that the ABC system provides to AM managers, emphasizing its role in motivating sustainability and better decision-making within the organization. It examines how ABC helps in identifying costs, measuring activity drivers, identifying profitable customers, deciding when to outsource, and setting profit margins, ultimately contributing to the firm's growth and success. The case study concludes that ABC costing is a valuable tool for informed decision-making and sustainable practices.

CASE STUDY

ASSESSMENT 3

ASSESSMENT 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

QUESTION 1...................................................................................................................................3

Elaborate development, challenges and application of activity-based costing............................3

QUESTION 2...................................................................................................................................4

Simple/traditional costing system to prepare a product-line profitability report for AM............4

QUESTION 3...................................................................................................................................5

ABC system to prepare a product-line profitability report for AM.............................................5

QUESTION 4...................................................................................................................................6

New insights does the ABC system in requirement provide to AM managers...........................6

QUESTION 5...................................................................................................................................7

ABC system motivates sustainability and better decision making in the organisation...............7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

QUESTION 1...................................................................................................................................3

Elaborate development, challenges and application of activity-based costing............................3

QUESTION 2...................................................................................................................................4

Simple/traditional costing system to prepare a product-line profitability report for AM............4

QUESTION 3...................................................................................................................................5

ABC system to prepare a product-line profitability report for AM.............................................5

QUESTION 4...................................................................................................................................6

New insights does the ABC system in requirement provide to AM managers...........................6

QUESTION 5...................................................................................................................................7

ABC system motivates sustainability and better decision making in the organisation...............7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

ABC costing is one of the major forms of costing that will enable the company to make the

analysis of the cost and the expenses that would be required to incur by the company with regard

to the production of the item and the product. This is an important concept with respect to

company that would assist in decision making by the company. This report will discuss the

concept of activity-based costing, its development, challenges along with its linking to decision

making. This report also makes a practical exposure through making use of traditional costing

system in order to prepare product line profitability report for A M. At the same time, it has

covered information pertaining to new insight related to ABC system that are required to provide

to AM manager.

MAIN BODY

QUESTION 1

Elaborate development, challenges and application of activity-based costing

Activity based costing

This is one of the major costing system that is related with the activities and operation

which will be added in the overall product. This is costing is related with the activities and

elements which will be added in the overall cost in making the product. It is termed as method of

assigning overhead and indirect cost like the salaries, wages and other expenses towards the

product and services (Quesado and Silva, 2021). As per this costing method all the indirect

expenses will be added to the main product and cost so that the actual price and concerned

expenses in relation with the product will be determined.

Development

As per the development of product and service the ABC costing play an important role

towards the determination of the actual costing of the product and services. This means if the

cost will be identified by the production regarding the production of the product, then it will be

assisted towards the management in determining the profit margin and profitability. This will

lead to play an important role towards the company and the management in terms of making a

smooth operational flow of production activities (Almeida and Cunha, 2017). This concept i.e.,

activity-based costing would lead to determine the management the actual cost that will enable

the managers and the company to determine the pricing decision so that along with the covering

ABC costing is one of the major forms of costing that will enable the company to make the

analysis of the cost and the expenses that would be required to incur by the company with regard

to the production of the item and the product. This is an important concept with respect to

company that would assist in decision making by the company. This report will discuss the

concept of activity-based costing, its development, challenges along with its linking to decision

making. This report also makes a practical exposure through making use of traditional costing

system in order to prepare product line profitability report for A M. At the same time, it has

covered information pertaining to new insight related to ABC system that are required to provide

to AM manager.

MAIN BODY

QUESTION 1

Elaborate development, challenges and application of activity-based costing

Activity based costing

This is one of the major costing system that is related with the activities and operation

which will be added in the overall product. This is costing is related with the activities and

elements which will be added in the overall cost in making the product. It is termed as method of

assigning overhead and indirect cost like the salaries, wages and other expenses towards the

product and services (Quesado and Silva, 2021). As per this costing method all the indirect

expenses will be added to the main product and cost so that the actual price and concerned

expenses in relation with the product will be determined.

Development

As per the development of product and service the ABC costing play an important role

towards the determination of the actual costing of the product and services. This means if the

cost will be identified by the production regarding the production of the product, then it will be

assisted towards the management in determining the profit margin and profitability. This will

lead to play an important role towards the company and the management in terms of making a

smooth operational flow of production activities (Almeida and Cunha, 2017). This concept i.e.,

activity-based costing would lead to determine the management the actual cost that will enable

the managers and the company to determine the pricing decision so that along with the covering

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of cost and expenses in the making of the product would be cover but at the same time it will

also enable the company to make earning of the sufficient earning. With the development of

activity-based costing the company would be able to make an analysis of value of the product

along with assisting it towards the decision that would be made by the company (Al Hanini,

2018). ABC costing is considered as better and developed more while making it compared with

the absorption costing. This will also lead to assist the company in terms of taking of most

adequate and right decision that would further lead to play an important role in profitability and

accomplishment of its objective of raising of revenue.

Challenges

The main challenges that the company would face in relation with the ABC costing is

related with the time i.e. it requires a lot of time in collecting and preparing the data that will be

material to the company and the concerned product. In the same way with the aspect of making a

determination of the aspect and element that will add cost to the product would also lead to be

time consuming with respect to company. Another challenge is related with the cost i.e. apart

from making an identification of cost in relation with the product manufacturing the company

may also need to incur a lot of cost in accumulating and making an analysis of the information.

This means the ABC costing would lead to impact the cost structure of the company which may

act as challenge (Araujo and et.al., 2020). In the same way the source data identification that will

lead to add value and cost to the company and its production of the product is also very difficult

to get identified. This means the company need to face challenge in terms of making an

identification of the overhead and other related expenses that are associated with the production

of the products.

QUESTION 2

Simple/traditional costing system to prepare a product-line profitability report for AM

Product line profitability report for AM

Particular

Pottery and

cake

Dairy

product

Meat

product Total

Revenue 55000 60000 62000 177000

COGS 35000 45000 45000 125000

30% of COGS 11000 15100 10500 36600

also enable the company to make earning of the sufficient earning. With the development of

activity-based costing the company would be able to make an analysis of value of the product

along with assisting it towards the decision that would be made by the company (Al Hanini,

2018). ABC costing is considered as better and developed more while making it compared with

the absorption costing. This will also lead to assist the company in terms of taking of most

adequate and right decision that would further lead to play an important role in profitability and

accomplishment of its objective of raising of revenue.

Challenges

The main challenges that the company would face in relation with the ABC costing is

related with the time i.e. it requires a lot of time in collecting and preparing the data that will be

material to the company and the concerned product. In the same way with the aspect of making a

determination of the aspect and element that will add cost to the product would also lead to be

time consuming with respect to company. Another challenge is related with the cost i.e. apart

from making an identification of cost in relation with the product manufacturing the company

may also need to incur a lot of cost in accumulating and making an analysis of the information.

This means the ABC costing would lead to impact the cost structure of the company which may

act as challenge (Araujo and et.al., 2020). In the same way the source data identification that will

lead to add value and cost to the company and its production of the product is also very difficult

to get identified. This means the company need to face challenge in terms of making an

identification of the overhead and other related expenses that are associated with the production

of the products.

QUESTION 2

Simple/traditional costing system to prepare a product-line profitability report for AM

Product line profitability report for AM

Particular

Pottery and

cake

Dairy

product

Meat

product Total

Revenue 55000 60000 62000 177000

COGS 35000 45000 45000 125000

30% of COGS 11000 15100 10500 36600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

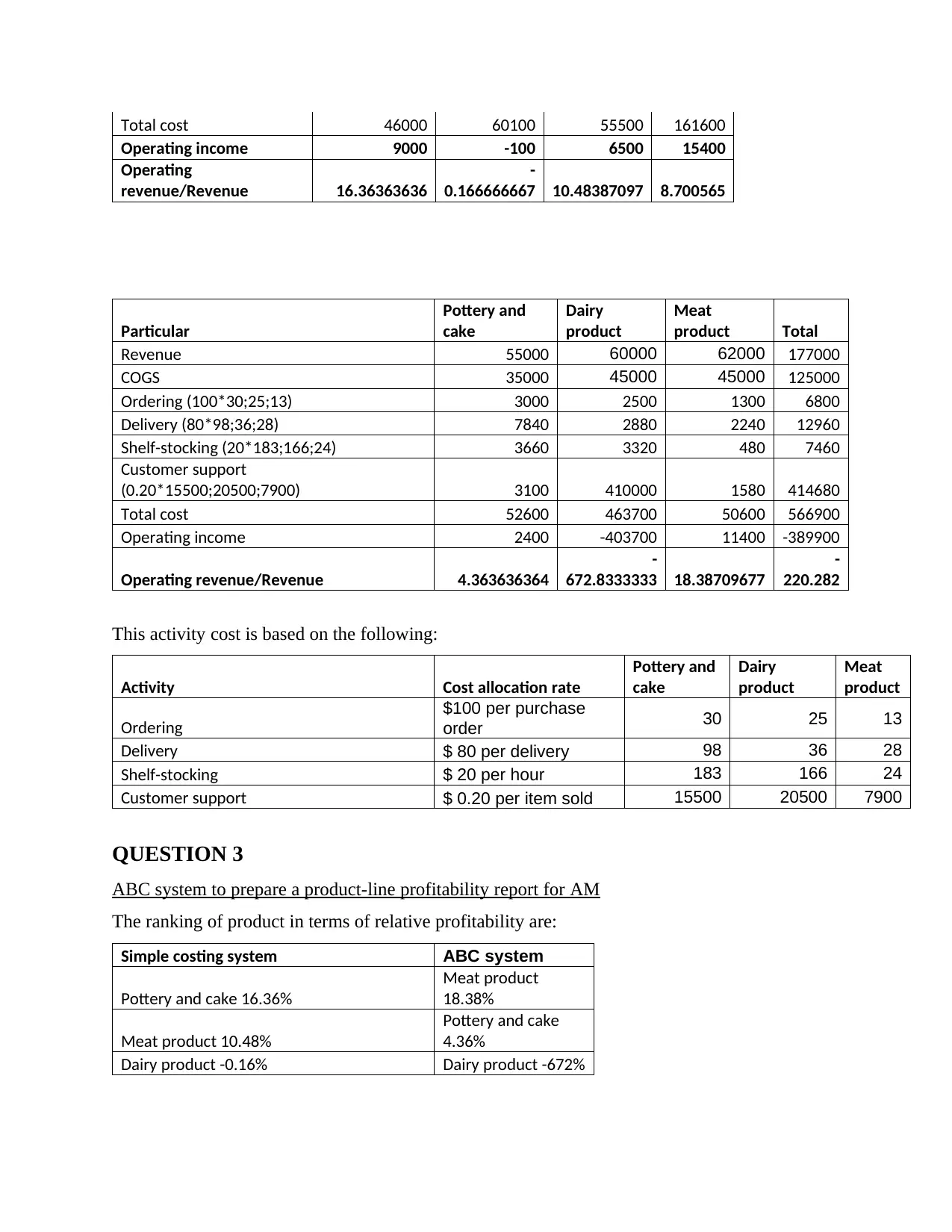

Total cost 46000 60100 55500 161600

Operating income 9000 -100 6500 15400

Operating

revenue/Revenue 16.36363636

-

0.166666667 10.48387097 8.700565

Particular

Pottery and

cake

Dairy

product

Meat

product Total

Revenue 55000 60000 62000 177000

COGS 35000 45000 45000 125000

Ordering (100*30;25;13) 3000 2500 1300 6800

Delivery (80*98;36;28) 7840 2880 2240 12960

Shelf-stocking (20*183;166;24) 3660 3320 480 7460

Customer support

(0.20*15500;20500;7900) 3100 410000 1580 414680

Total cost 52600 463700 50600 566900

Operating income 2400 -403700 11400 -389900

Operating revenue/Revenue 4.363636364

-

672.8333333 18.38709677

-

220.282

This activity cost is based on the following:

Activity Cost allocation rate

Pottery and

cake

Dairy

product

Meat

product

Ordering

$100 per purchase

order 30 25 13

Delivery $ 80 per delivery 98 36 28

Shelf-stocking $ 20 per hour 183 166 24

Customer support $ 0.20 per item sold 15500 20500 7900

QUESTION 3

ABC system to prepare a product-line profitability report for AM

The ranking of product in terms of relative profitability are:

Simple costing system ABC system

Pottery and cake 16.36%

Meat product

18.38%

Meat product 10.48%

Pottery and cake

4.36%

Dairy product -0.16% Dairy product -672%

Operating income 9000 -100 6500 15400

Operating

revenue/Revenue 16.36363636

-

0.166666667 10.48387097 8.700565

Particular

Pottery and

cake

Dairy

product

Meat

product Total

Revenue 55000 60000 62000 177000

COGS 35000 45000 45000 125000

Ordering (100*30;25;13) 3000 2500 1300 6800

Delivery (80*98;36;28) 7840 2880 2240 12960

Shelf-stocking (20*183;166;24) 3660 3320 480 7460

Customer support

(0.20*15500;20500;7900) 3100 410000 1580 414680

Total cost 52600 463700 50600 566900

Operating income 2400 -403700 11400 -389900

Operating revenue/Revenue 4.363636364

-

672.8333333 18.38709677

-

220.282

This activity cost is based on the following:

Activity Cost allocation rate

Pottery and

cake

Dairy

product

Meat

product

Ordering

$100 per purchase

order 30 25 13

Delivery $ 80 per delivery 98 36 28

Shelf-stocking $ 20 per hour 183 166 24

Customer support $ 0.20 per item sold 15500 20500 7900

QUESTION 3

ABC system to prepare a product-line profitability report for AM

The ranking of product in terms of relative profitability are:

Simple costing system ABC system

Pottery and cake 16.36%

Meat product

18.38%

Meat product 10.48%

Pottery and cake

4.36%

Dairy product -0.16% Dairy product -672%

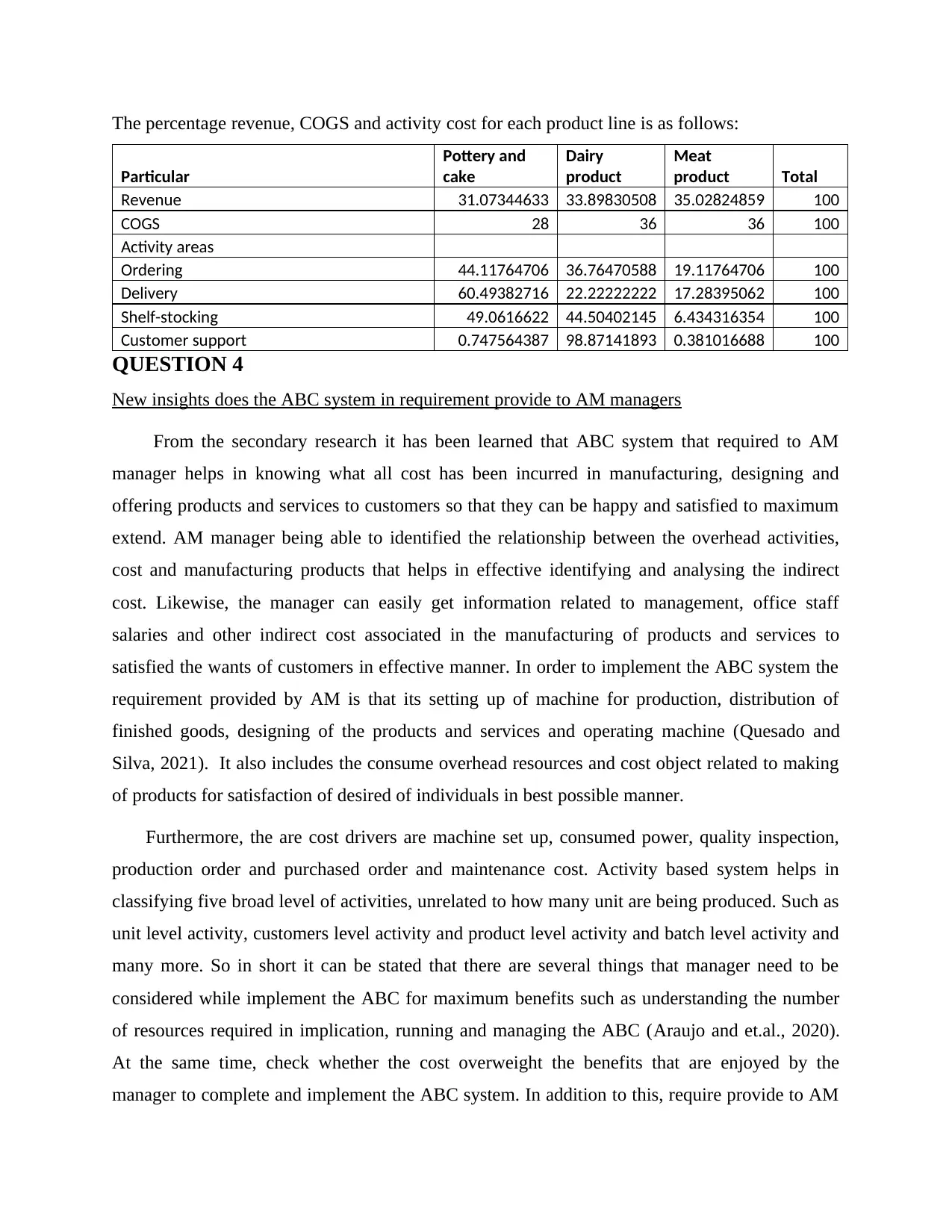

The percentage revenue, COGS and activity cost for each product line is as follows:

Particular

Pottery and

cake

Dairy

product

Meat

product Total

Revenue 31.07344633 33.89830508 35.02824859 100

COGS 28 36 36 100

Activity areas

Ordering 44.11764706 36.76470588 19.11764706 100

Delivery 60.49382716 22.22222222 17.28395062 100

Shelf-stocking 49.0616622 44.50402145 6.434316354 100

Customer support 0.747564387 98.87141893 0.381016688 100

QUESTION 4

New insights does the ABC system in requirement provide to AM managers

From the secondary research it has been learned that ABC system that required to AM

manager helps in knowing what all cost has been incurred in manufacturing, designing and

offering products and services to customers so that they can be happy and satisfied to maximum

extend. AM manager being able to identified the relationship between the overhead activities,

cost and manufacturing products that helps in effective identifying and analysing the indirect

cost. Likewise, the manager can easily get information related to management, office staff

salaries and other indirect cost associated in the manufacturing of products and services to

satisfied the wants of customers in effective manner. In order to implement the ABC system the

requirement provided by AM is that its setting up of machine for production, distribution of

finished goods, designing of the products and services and operating machine (Quesado and

Silva, 2021). It also includes the consume overhead resources and cost object related to making

of products for satisfaction of desired of individuals in best possible manner.

Furthermore, the are cost drivers are machine set up, consumed power, quality inspection,

production order and purchased order and maintenance cost. Activity based system helps in

classifying five broad level of activities, unrelated to how many unit are being produced. Such as

unit level activity, customers level activity and product level activity and batch level activity and

many more. So in short it can be stated that there are several things that manager need to be

considered while implement the ABC for maximum benefits such as understanding the number

of resources required in implication, running and managing the ABC (Araujo and et.al., 2020).

At the same time, check whether the cost overweight the benefits that are enjoyed by the

manager to complete and implement the ABC system. In addition to this, require provide to AM

Particular

Pottery and

cake

Dairy

product

Meat

product Total

Revenue 31.07344633 33.89830508 35.02824859 100

COGS 28 36 36 100

Activity areas

Ordering 44.11764706 36.76470588 19.11764706 100

Delivery 60.49382716 22.22222222 17.28395062 100

Shelf-stocking 49.0616622 44.50402145 6.434316354 100

Customer support 0.747564387 98.87141893 0.381016688 100

QUESTION 4

New insights does the ABC system in requirement provide to AM managers

From the secondary research it has been learned that ABC system that required to AM

manager helps in knowing what all cost has been incurred in manufacturing, designing and

offering products and services to customers so that they can be happy and satisfied to maximum

extend. AM manager being able to identified the relationship between the overhead activities,

cost and manufacturing products that helps in effective identifying and analysing the indirect

cost. Likewise, the manager can easily get information related to management, office staff

salaries and other indirect cost associated in the manufacturing of products and services to

satisfied the wants of customers in effective manner. In order to implement the ABC system the

requirement provided by AM is that its setting up of machine for production, distribution of

finished goods, designing of the products and services and operating machine (Quesado and

Silva, 2021). It also includes the consume overhead resources and cost object related to making

of products for satisfaction of desired of individuals in best possible manner.

Furthermore, the are cost drivers are machine set up, consumed power, quality inspection,

production order and purchased order and maintenance cost. Activity based system helps in

classifying five broad level of activities, unrelated to how many unit are being produced. Such as

unit level activity, customers level activity and product level activity and batch level activity and

many more. So in short it can be stated that there are several things that manager need to be

considered while implement the ABC for maximum benefits such as understanding the number

of resources required in implication, running and managing the ABC (Araujo and et.al., 2020).

At the same time, check whether the cost overweight the benefits that are enjoyed by the

manager to complete and implement the ABC system. In addition to this, require provide to AM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

related to whether this helps in effective identification of activities and associated cost or not. At

last it can be stated that whether the ABC contribute in understanding that it helps in increasing

overall profitability of the firm or not.

QUESTION 5

ABC system motivates sustainability and better decision making in the organisation

Activity-based costing is the method of assigning overhead and indirect cost to products

and services for example the utilities and salaries. It focuses on activities to determine the cost of

products and services that company needs to be incurred to fulfil the wants of customers in

effective manner. It provides more accurate method of products or services costing, taking

decision related to price of product so that organisation can earn high profit margin and market

share in external environment. The reason why ABC system motivates sustainability and better

decision making in the firm because it helps in identification of cost that are incurred in

manufacturing of products and services (Zamrud, Abu, Kamil and Safeiee, 2019). Such as

distribution cost, warehousing, raw material and research and advertisement cost that are being

incurred by firm to offer products to customers. Along with it, the ABC system helps in

measuring the activity drivers that helps in allocating actual cost to each and every item for

measuring the actual price or cost that has been paid to make the product. Furthermore, it helps

in taking decision related to identification of profitable customers through identifying the

overhead component or cost incurred in the products such as unusual high customers service

level, marketing, product return handling and many more. So, that less number of issue needs to

be face by customers while experiencing in the company. This analysis helps company in

effectively segregating of unprofitable customers thus organisation can easily planned strategies

to attract the target customers that can be easily part of the firm.

Activity based costing also helps in deciding when to outsource, that is comprehensive

view of each and every cost that is incurred in manufacturing of products. Thus, company can

easily take decision related to the cost that can be outsources so that it can be reduce to

maximum extend. It also helps manager in taking decision elated to setting actual profit margin

of the product and the manner in which the resources should be utilised so that firm can easily

achieve higher growth and success. All this helps in promoting the sustainability of the

organisation through ensuring that the products are being offered to customers at minimum price

last it can be stated that whether the ABC contribute in understanding that it helps in increasing

overall profitability of the firm or not.

QUESTION 5

ABC system motivates sustainability and better decision making in the organisation

Activity-based costing is the method of assigning overhead and indirect cost to products

and services for example the utilities and salaries. It focuses on activities to determine the cost of

products and services that company needs to be incurred to fulfil the wants of customers in

effective manner. It provides more accurate method of products or services costing, taking

decision related to price of product so that organisation can earn high profit margin and market

share in external environment. The reason why ABC system motivates sustainability and better

decision making in the firm because it helps in identification of cost that are incurred in

manufacturing of products and services (Zamrud, Abu, Kamil and Safeiee, 2019). Such as

distribution cost, warehousing, raw material and research and advertisement cost that are being

incurred by firm to offer products to customers. Along with it, the ABC system helps in

measuring the activity drivers that helps in allocating actual cost to each and every item for

measuring the actual price or cost that has been paid to make the product. Furthermore, it helps

in taking decision related to identification of profitable customers through identifying the

overhead component or cost incurred in the products such as unusual high customers service

level, marketing, product return handling and many more. So, that less number of issue needs to

be face by customers while experiencing in the company. This analysis helps company in

effectively segregating of unprofitable customers thus organisation can easily planned strategies

to attract the target customers that can be easily part of the firm.

Activity based costing also helps in deciding when to outsource, that is comprehensive

view of each and every cost that is incurred in manufacturing of products. Thus, company can

easily take decision related to the cost that can be outsources so that it can be reduce to

maximum extend. It also helps manager in taking decision elated to setting actual profit margin

of the product and the manner in which the resources should be utilised so that firm can easily

achieve higher growth and success. All this helps in promoting the sustainability of the

organisation through ensuring that the products are being offered to customers at minimum price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

possible. In addition to this, different products require different indirect expenses so it helps in its

recognition and allocation of resources for fruitful outcome (Altawati and et.al., 2018.). The

manager can take decision related to cutting back of overhead costs so that maximum value can

be offered to customers at minimum price. Through the activity based costing, companies are

able to effectively set budget for the company that is associated cost that has to be incurred by

company in future circumstances. Finally, it can be summarised that ABC is best system to

contributing in sustainability and decision making for growth and expansion of firm.

CONCLUSION

From the above report it can be concluded that ABC costing is of the major form of costing

that will assist the company in making decision related with the production of products and

services. In the same way this report also summarized various challenges that may lead to impact

the concept of ABC costing. Activity based costing is best method used by many of the manager

to set right price of the product for attracting maximum number of customer within the firm. In

addition of this it is also summarize that how with the implication of ABC costing the company

would be assisted in taking of right decision with respect to its production. At last it can be stated

that ABC system motivates sustainability and better decision making in the organisation through

effectively understanding the actual cost that has been incurred in order to design a particular

products and services for benefits of the organisation.

recognition and allocation of resources for fruitful outcome (Altawati and et.al., 2018.). The

manager can take decision related to cutting back of overhead costs so that maximum value can

be offered to customers at minimum price. Through the activity based costing, companies are

able to effectively set budget for the company that is associated cost that has to be incurred by

company in future circumstances. Finally, it can be summarised that ABC is best system to

contributing in sustainability and decision making for growth and expansion of firm.

CONCLUSION

From the above report it can be concluded that ABC costing is of the major form of costing

that will assist the company in making decision related with the production of products and

services. In the same way this report also summarized various challenges that may lead to impact

the concept of ABC costing. Activity based costing is best method used by many of the manager

to set right price of the product for attracting maximum number of customer within the firm. In

addition of this it is also summarize that how with the implication of ABC costing the company

would be assisted in taking of right decision with respect to its production. At last it can be stated

that ABC system motivates sustainability and better decision making in the organisation through

effectively understanding the actual cost that has been incurred in order to design a particular

products and services for benefits of the organisation.

REFERENCES

Books and journals

Al Hanini, E. A., 2018. The impact of adopting Activity Based Costing (ABC) on decreasing

cost and maximizing profitability in industrial companies listed in Amman Stock

Exchange. Academy of Accounting and Financial Studies Journal, 22(5). pp.1-8.

Almeida, A. and Cunha, J., 2017. The implementation of an Activity-Based Costing (ABC)

system in a manufacturing company. Procedia manufacturing. 13. pp.932-939.

Altawati, N.O.M.T and et.al., 2018. A review of traditional cost system versus activity based

costing approaches. Advanced science letters, 24(6). pp.4688-4694.

Araujo, and et.al., 2020. Use of the activity-based costing methodology (ABC) in the cost

analysis of successional agroforestry systems. Agroforestry Systems. 94(1). pp.71-80.

Araujo, J.B.C.N and et.al., 2020. Use of the activity-based costing methodology (ABC) in the

cost analysis of successional agroforestry systems. Agroforestry Systems, 94(1).

pp.71-80.

Quesado, P. and Silva, R., 2021. Activity-Based Costing (ABC) and Its Implication for Open

Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1).

p.41.

Quesado, P. and Silva, R., 2021. Activity-Based Costing (ABC) and Its Implication for Open

Innovation. Journal of Open Innovation: Technology, Market, and Complexity. 7(1).

p.41.

Zamrud, N.F., Abu, M.Y., Kamil, N.N.N.M. and Safeiee, F.L.M., 2019, August. A comparative

study of product costing by using activity-based costing (ABC) and time-driven

activity-based costing (TDABC) method. In Proceedings of the International

Manufacturing Engineering Conference & The Asia Pacific Conference on

Manufacturing Systems (pp. 171-178). Springer, Singapore.

9

Books and journals

Al Hanini, E. A., 2018. The impact of adopting Activity Based Costing (ABC) on decreasing

cost and maximizing profitability in industrial companies listed in Amman Stock

Exchange. Academy of Accounting and Financial Studies Journal, 22(5). pp.1-8.

Almeida, A. and Cunha, J., 2017. The implementation of an Activity-Based Costing (ABC)

system in a manufacturing company. Procedia manufacturing. 13. pp.932-939.

Altawati, N.O.M.T and et.al., 2018. A review of traditional cost system versus activity based

costing approaches. Advanced science letters, 24(6). pp.4688-4694.

Araujo, and et.al., 2020. Use of the activity-based costing methodology (ABC) in the cost

analysis of successional agroforestry systems. Agroforestry Systems. 94(1). pp.71-80.

Araujo, J.B.C.N and et.al., 2020. Use of the activity-based costing methodology (ABC) in the

cost analysis of successional agroforestry systems. Agroforestry Systems, 94(1).

pp.71-80.

Quesado, P. and Silva, R., 2021. Activity-Based Costing (ABC) and Its Implication for Open

Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1).

p.41.

Quesado, P. and Silva, R., 2021. Activity-Based Costing (ABC) and Its Implication for Open

Innovation. Journal of Open Innovation: Technology, Market, and Complexity. 7(1).

p.41.

Zamrud, N.F., Abu, M.Y., Kamil, N.N.N.M. and Safeiee, F.L.M., 2019, August. A comparative

study of product costing by using activity-based costing (ABC) and time-driven

activity-based costing (TDABC) method. In Proceedings of the International

Manufacturing Engineering Conference & The Asia Pacific Conference on

Manufacturing Systems (pp. 171-178). Springer, Singapore.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.