Significance of Journal Entries and Trial Balance in Business Accounting

VerifiedAdded on 2023/04/21

|17

|3246

|336

AI Summary

This report discusses the significance of journal entries and trial balance in business accounting. It explains the purpose of creating a trial balance and how it helps in detecting errors. It also highlights the importance of journal entries in correcting errors and preparing financial statements. The report includes examples of journal entries and a sample income statement and balance sheet.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS ACCOUNTING

Business accounting

Name of the student

Name of the university

Author note

Business accounting

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Step 2 – Journal entries for adjustment entries..........................................................................3

Step 3 – Worksheet completion.................................................................................................4

Step 4 – Income statement prepared from adjusted worksheet..................................................5

Step 5 – Journal entries for closing entries................................................................................6

Step 6 – Changes in equity.........................................................................................................6

Step 7..........................................................................................................................................8

1. Trial balance and purpose of its creation........................................................................8

2. Adjusting journal entries and purpose of recording it.....................................................9

3. Purpose of preparing the adjusted trial balance............................................................10

4. Difference between closing journal entries and adjusting journal entries....................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

Table of Contents

Introduction................................................................................................................................2

Step 2 – Journal entries for adjustment entries..........................................................................3

Step 3 – Worksheet completion.................................................................................................4

Step 4 – Income statement prepared from adjusted worksheet..................................................5

Step 5 – Journal entries for closing entries................................................................................6

Step 6 – Changes in equity.........................................................................................................6

Step 7..........................................................................................................................................8

1. Trial balance and purpose of its creation........................................................................8

2. Adjusting journal entries and purpose of recording it.....................................................9

3. Purpose of preparing the adjusted trial balance............................................................10

4. Difference between closing journal entries and adjusting journal entries....................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

2BUSINESS ACCOUNTING

Introduction

Aim of the report is to concentrate on the significance of journal entries and

preparation of trial balance for preparing the income statement as well as the balance sheet.

This report will present journal entries with regard to the given adjusting entries and from the

adjusted trial balance it will prepare the profit and loss statement and balance sheet for the

concerned period. Trial balance is the preparation of account that represents balances from

the entire general ledger with regard to the transactions taken place during the concerned

period. Under the trial balance, total debit amount must be equal to total credit amount.

Adjusting journal entries on the other hand, are used as the tool for correction of errors and

these shall be completed before preparing the final financial statements for the year (Edwards

2013).

Step 2 – Journal entries for adjustment entries

In the books of Paul services journal entries for the period ended 30th June 2016

Date Particulars

Acc

No. Debit Credit

30th June

2016

Interest Expense 201

$

12,800.00

Interest Payable 201

$

12,800.00

(Interest accrued on mortgage)

Supplies Expense 201

$

960.00

Supplies 115

$

960.00

(using supplies for the period)

Insurance Expense 201

$

2,048.00

Prepaid Insurance 120

$

2,048.00

(To record prepaid amortisation)

Depreciation Expense - Furniture ((32000-2000)/5) 201 $

Introduction

Aim of the report is to concentrate on the significance of journal entries and

preparation of trial balance for preparing the income statement as well as the balance sheet.

This report will present journal entries with regard to the given adjusting entries and from the

adjusted trial balance it will prepare the profit and loss statement and balance sheet for the

concerned period. Trial balance is the preparation of account that represents balances from

the entire general ledger with regard to the transactions taken place during the concerned

period. Under the trial balance, total debit amount must be equal to total credit amount.

Adjusting journal entries on the other hand, are used as the tool for correction of errors and

these shall be completed before preparing the final financial statements for the year (Edwards

2013).

Step 2 – Journal entries for adjustment entries

In the books of Paul services journal entries for the period ended 30th June 2016

Date Particulars

Acc

No. Debit Credit

30th June

2016

Interest Expense 201

$

12,800.00

Interest Payable 201

$

12,800.00

(Interest accrued on mortgage)

Supplies Expense 201

$

960.00

Supplies 115

$

960.00

(using supplies for the period)

Insurance Expense 201

$

2,048.00

Prepaid Insurance 120

$

2,048.00

(To record prepaid amortisation)

Depreciation Expense - Furniture ((32000-2000)/5) 201 $

3BUSINESS ACCOUNTING

6,000.00

Accmulated Depreciation. - Furniture 137

$

6,000.00

(depreciation expense transferred to accumulated

depreciation)

Depreciation Expense - Office Equipment ((64000-4000)/5) 201

$

12,000.00

Acc. Depreciation - Office Equipment 141

$

12,000.00

(depreciation expense transferred to accumulated

depreciation)

Depreciation Expense - Store Equipment ((96000-6000)/10) 201

$

9,000.00

Acc. Depreciation - Store Equipment 146

$

9,000.00

(depreciation expense transferred to accumulated

depreciation)

Depreciation Expense - Automobile ((128000-8000)/10) 201

$

12,000.00

Acc. Depreciation - Automobile 171

$

12,000.00

(depreciation expense transferred to accumulated

depreciation)

Unearned revenue 201

$

8,000.00

Revenue 201

$

8,000.00

(Unearned revenue earned)

6,000.00

Accmulated Depreciation. - Furniture 137

$

6,000.00

(depreciation expense transferred to accumulated

depreciation)

Depreciation Expense - Office Equipment ((64000-4000)/5) 201

$

12,000.00

Acc. Depreciation - Office Equipment 141

$

12,000.00

(depreciation expense transferred to accumulated

depreciation)

Depreciation Expense - Store Equipment ((96000-6000)/10) 201

$

9,000.00

Acc. Depreciation - Store Equipment 146

$

9,000.00

(depreciation expense transferred to accumulated

depreciation)

Depreciation Expense - Automobile ((128000-8000)/10) 201

$

12,000.00

Acc. Depreciation - Automobile 171

$

12,000.00

(depreciation expense transferred to accumulated

depreciation)

Unearned revenue 201

$

8,000.00

Revenue 201

$

8,000.00

(Unearned revenue earned)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS ACCOUNTING

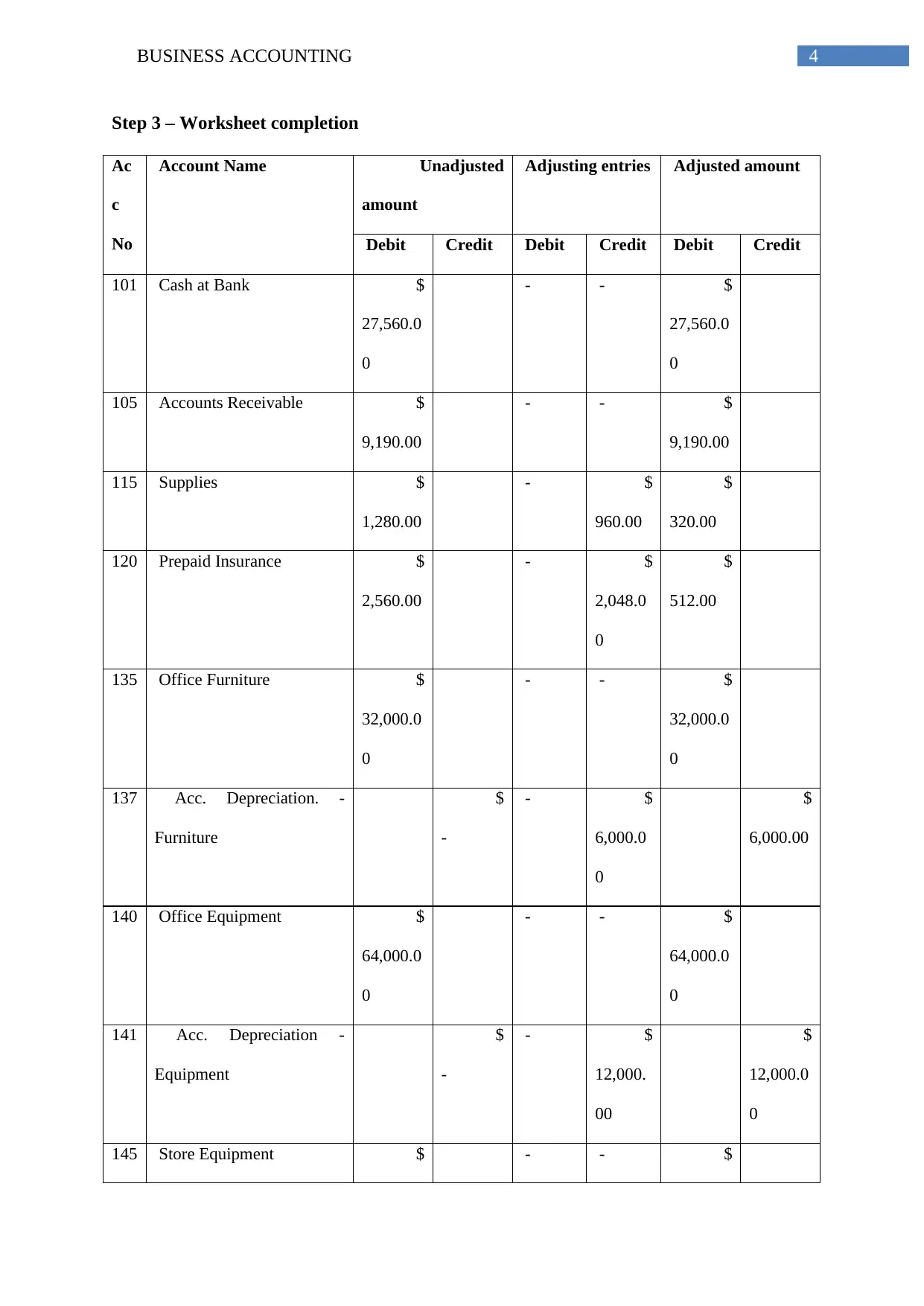

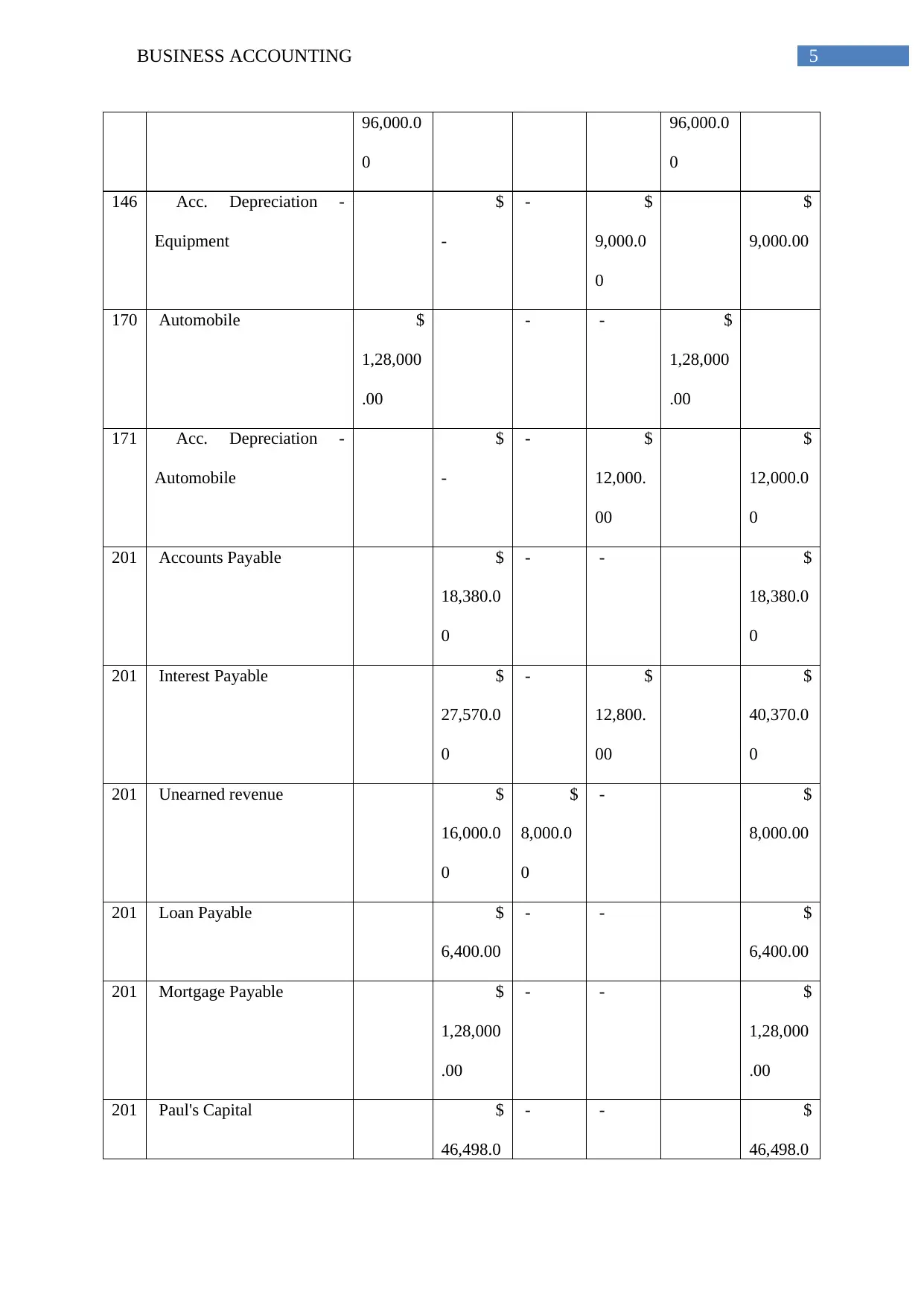

Step 3 – Worksheet completion

Ac

c

No

Account Name Unadjusted

amount

Adjusting entries Adjusted amount

Debit Credit Debit Credit Debit Credit

101 Cash at Bank $

27,560.0

0

- - $

27,560.0

0

105 Accounts Receivable $

9,190.00

- - $

9,190.00

115 Supplies $

1,280.00

- $

960.00

$

320.00

120 Prepaid Insurance $

2,560.00

- $

2,048.0

0

$

512.00

135 Office Furniture $

32,000.0

0

- - $

32,000.0

0

137 Acc. Depreciation. -

Furniture

$

-

- $

6,000.0

0

$

6,000.00

140 Office Equipment $

64,000.0

0

- - $

64,000.0

0

141 Acc. Depreciation -

Equipment

$

-

- $

12,000.

00

$

12,000.0

0

145 Store Equipment $ - - $

Step 3 – Worksheet completion

Ac

c

No

Account Name Unadjusted

amount

Adjusting entries Adjusted amount

Debit Credit Debit Credit Debit Credit

101 Cash at Bank $

27,560.0

0

- - $

27,560.0

0

105 Accounts Receivable $

9,190.00

- - $

9,190.00

115 Supplies $

1,280.00

- $

960.00

$

320.00

120 Prepaid Insurance $

2,560.00

- $

2,048.0

0

$

512.00

135 Office Furniture $

32,000.0

0

- - $

32,000.0

0

137 Acc. Depreciation. -

Furniture

$

-

- $

6,000.0

0

$

6,000.00

140 Office Equipment $

64,000.0

0

- - $

64,000.0

0

141 Acc. Depreciation -

Equipment

$

-

- $

12,000.

00

$

12,000.0

0

145 Store Equipment $ - - $

5BUSINESS ACCOUNTING

96,000.0

0

96,000.0

0

146 Acc. Depreciation -

Equipment

$

-

- $

9,000.0

0

$

9,000.00

170 Automobile $

1,28,000

.00

- - $

1,28,000

.00

171 Acc. Depreciation -

Automobile

$

-

- $

12,000.

00

$

12,000.0

0

201 Accounts Payable $

18,380.0

0

- - $

18,380.0

0

201 Interest Payable $

27,570.0

0

- $

12,800.

00

$

40,370.0

0

201 Unearned revenue $

16,000.0

0

$

8,000.0

0

- $

8,000.00

201 Loan Payable $

6,400.00

- - $

6,400.00

201 Mortgage Payable $

1,28,000

.00

- - $

1,28,000

.00

201 Paul's Capital $

46,498.0

- - $

46,498.0

96,000.0

0

96,000.0

0

146 Acc. Depreciation -

Equipment

$

-

- $

9,000.0

0

$

9,000.00

170 Automobile $

1,28,000

.00

- - $

1,28,000

.00

171 Acc. Depreciation -

Automobile

$

-

- $

12,000.

00

$

12,000.0

0

201 Accounts Payable $

18,380.0

0

- - $

18,380.0

0

201 Interest Payable $

27,570.0

0

- $

12,800.

00

$

40,370.0

0

201 Unearned revenue $

16,000.0

0

$

8,000.0

0

- $

8,000.00

201 Loan Payable $

6,400.00

- - $

6,400.00

201 Mortgage Payable $

1,28,000

.00

- - $

1,28,000

.00

201 Paul's Capital $

46,498.0

- - $

46,498.0

6BUSINESS ACCOUNTING

0 0

201 Paul's Drawings $

128.00

- - $

128.00

201 Revenue $

1,28,000

.00

- $

8,000.0

0

$

1,36,000

.00

201 Advertising Expense $

600.00

- - $

600.00

201 Automobile Expense $

5,775.00

- - $

5,775.00

201 Depreciation Expense -

Furniture

$

-

$

6,000.0

0

- $

6,000.00

201 Depreciation Expense -

Equipment

$

-

$

12,000.

00

- $

12,000.0

0

201 Depreciation Expense -

Store Equipment

$

-

$

9,000.0

0

- $

9,000.00

201 Depreciation Expense -

Automobile

$

-

$

12,000.

00

- $

12,000.0

0

201 Insurance Expense $

500.00

$

2,048.0

0

- $

2,548.00

201 Maintenance Expense $

2,100.00

- - $

2,100.00

0 0

201 Paul's Drawings $

128.00

- - $

128.00

201 Revenue $

1,28,000

.00

- $

8,000.0

0

$

1,36,000

.00

201 Advertising Expense $

600.00

- - $

600.00

201 Automobile Expense $

5,775.00

- - $

5,775.00

201 Depreciation Expense -

Furniture

$

-

$

6,000.0

0

- $

6,000.00

201 Depreciation Expense -

Equipment

$

-

$

12,000.

00

- $

12,000.0

0

201 Depreciation Expense -

Store Equipment

$

-

$

9,000.0

0

- $

9,000.00

201 Depreciation Expense -

Automobile

$

-

$

12,000.

00

- $

12,000.0

0

201 Insurance Expense $

500.00

$

2,048.0

0

- $

2,548.00

201 Maintenance Expense $

2,100.00

- - $

2,100.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS ACCOUNTING

201 Miscellaneous Expense $

1,155.00

- - $

1,155.00

201 Rent Expense $

-

- - $

-

201 Supplies Expense $

-

$

960.00

- $

960.00

201 Utilities Expense $

-

- - $

-

201 Interest Expense $

-

$

12,800.

00

- $

12,800.0

0

Total $

3,70,848

.00

$

3,70,848

.00

$

62,808.

00

$

62,808.

00

$

4,22,648

.00

$

4,22,648

.00

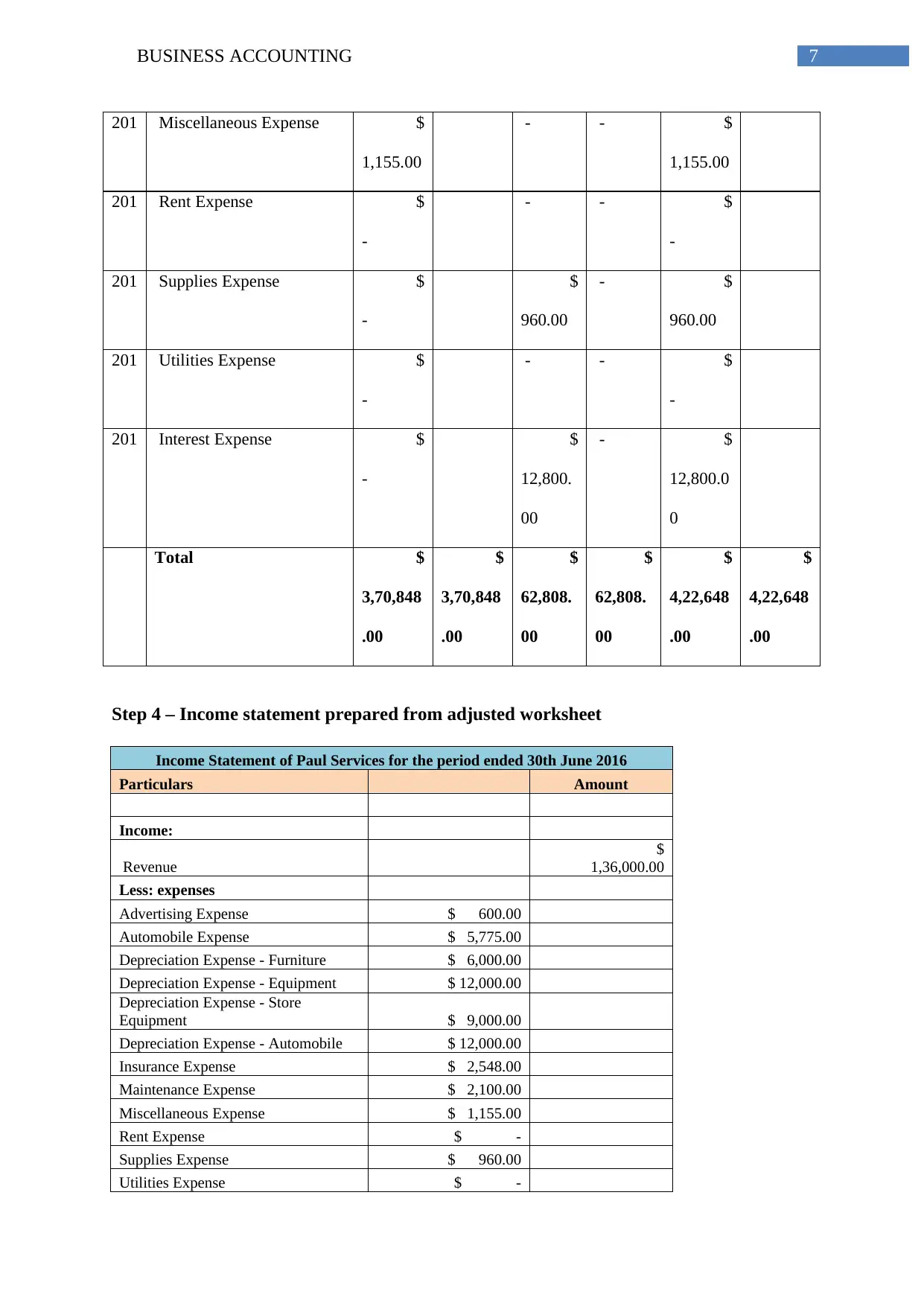

Step 4 – Income statement prepared from adjusted worksheet

Income Statement of Paul Services for the period ended 30th June 2016

Particulars Amount

Income:

Revenue

$

1,36,000.00

Less: expenses

Advertising Expense $ 600.00

Automobile Expense $ 5,775.00

Depreciation Expense - Furniture $ 6,000.00

Depreciation Expense - Equipment $ 12,000.00

Depreciation Expense - Store

Equipment $ 9,000.00

Depreciation Expense - Automobile $ 12,000.00

Insurance Expense $ 2,548.00

Maintenance Expense $ 2,100.00

Miscellaneous Expense $ 1,155.00

Rent Expense $ -

Supplies Expense $ 960.00

Utilities Expense $ -

201 Miscellaneous Expense $

1,155.00

- - $

1,155.00

201 Rent Expense $

-

- - $

-

201 Supplies Expense $

-

$

960.00

- $

960.00

201 Utilities Expense $

-

- - $

-

201 Interest Expense $

-

$

12,800.

00

- $

12,800.0

0

Total $

3,70,848

.00

$

3,70,848

.00

$

62,808.

00

$

62,808.

00

$

4,22,648

.00

$

4,22,648

.00

Step 4 – Income statement prepared from adjusted worksheet

Income Statement of Paul Services for the period ended 30th June 2016

Particulars Amount

Income:

Revenue

$

1,36,000.00

Less: expenses

Advertising Expense $ 600.00

Automobile Expense $ 5,775.00

Depreciation Expense - Furniture $ 6,000.00

Depreciation Expense - Equipment $ 12,000.00

Depreciation Expense - Store

Equipment $ 9,000.00

Depreciation Expense - Automobile $ 12,000.00

Insurance Expense $ 2,548.00

Maintenance Expense $ 2,100.00

Miscellaneous Expense $ 1,155.00

Rent Expense $ -

Supplies Expense $ 960.00

Utilities Expense $ -

8BUSINESS ACCOUNTING

Interest Expense $ 12,800.00

Total expenses

$

64,938.00

Net Profit

$

71,062.00

Step 5 – Journal entries for closing entries

Date Particulars Account No.

Amount

(Dr.)

Amount

(Cr.)

30-Jun-16 Revenue 201

$

1,36,000.00

Advertising Expense 201

$

600.00

Automobile Expense 201

$

5,775.00

Depreciation Expense - Furniture 201

$

14,000.00

Depreciation Expense - Equipment 201

$

28,000.00

Depreciation Expense - Store

Equipment 201

$

22,000.00

Depreciation Expense - Automobile 201

$

29,000.00

Insurance Expense 201

$

8,036.00

Maintenance Expense 201

$

13,650.00

Miscellaneous Expense 201

$

1,155.00

Rent Expense 201

$

-

Supplies Expense 201

$

2,220.00

Utilities Expense 201

$

-

Interest Expense 201

$

29,600.00

Retained earnings

$

71,062.00

[Recording the closing entries]

Step 6 – Changes in equity

Statement of Changes in Equity of Paul services For the year ended 30th June, 2016

Particulars Capital Retained Earnings Total

Opening balance $ 46,498.00 - $ 46,498.00

Drawings $ (128.00)

Profit for the year $ 71,062.00

Closing Balance $ 46,370.00 $ 71,062.00 $ 46,498.00

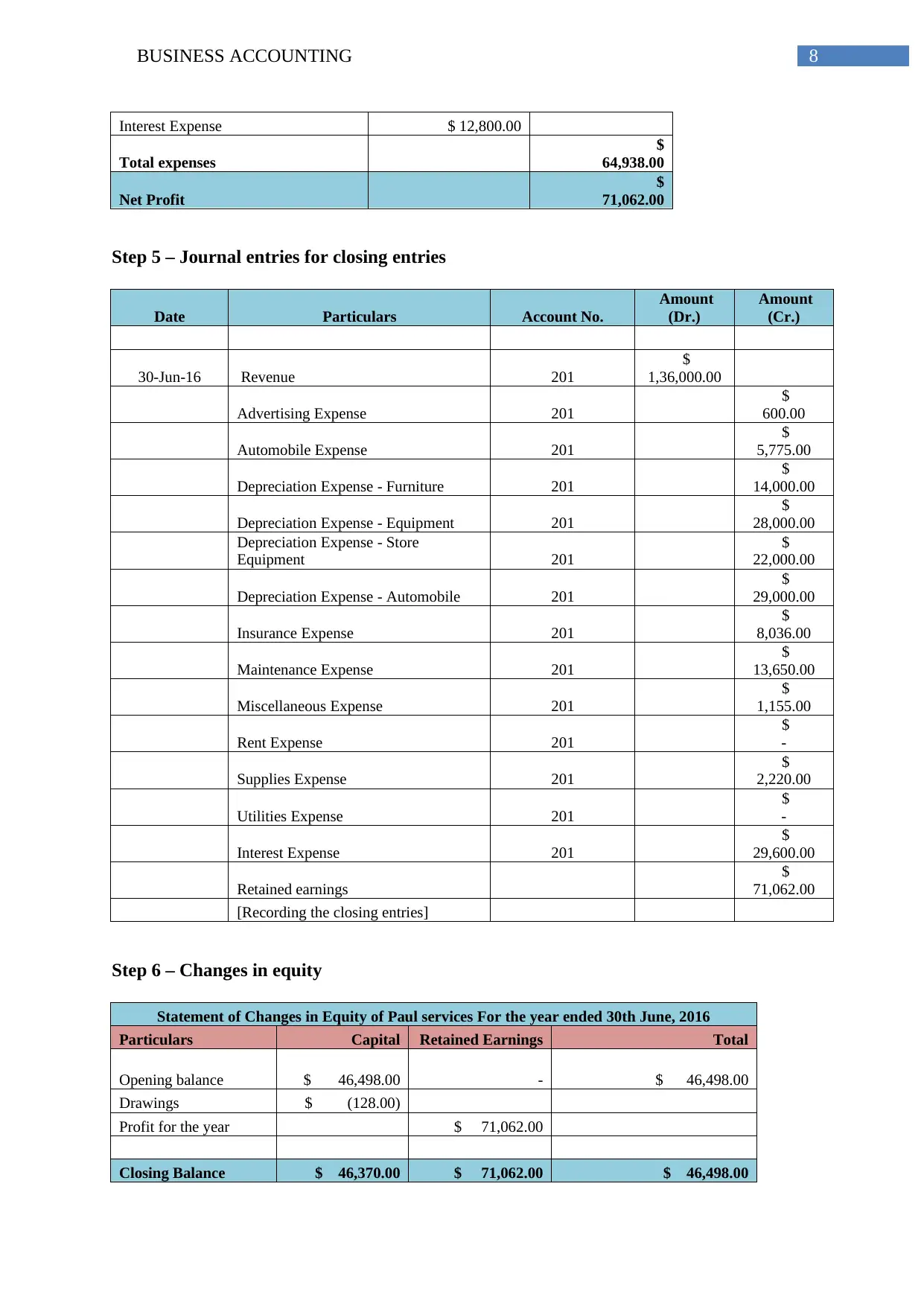

Interest Expense $ 12,800.00

Total expenses

$

64,938.00

Net Profit

$

71,062.00

Step 5 – Journal entries for closing entries

Date Particulars Account No.

Amount

(Dr.)

Amount

(Cr.)

30-Jun-16 Revenue 201

$

1,36,000.00

Advertising Expense 201

$

600.00

Automobile Expense 201

$

5,775.00

Depreciation Expense - Furniture 201

$

14,000.00

Depreciation Expense - Equipment 201

$

28,000.00

Depreciation Expense - Store

Equipment 201

$

22,000.00

Depreciation Expense - Automobile 201

$

29,000.00

Insurance Expense 201

$

8,036.00

Maintenance Expense 201

$

13,650.00

Miscellaneous Expense 201

$

1,155.00

Rent Expense 201

$

-

Supplies Expense 201

$

2,220.00

Utilities Expense 201

$

-

Interest Expense 201

$

29,600.00

Retained earnings

$

71,062.00

[Recording the closing entries]

Step 6 – Changes in equity

Statement of Changes in Equity of Paul services For the year ended 30th June, 2016

Particulars Capital Retained Earnings Total

Opening balance $ 46,498.00 - $ 46,498.00

Drawings $ (128.00)

Profit for the year $ 71,062.00

Closing Balance $ 46,370.00 $ 71,062.00 $ 46,498.00

9BUSINESS ACCOUNTING

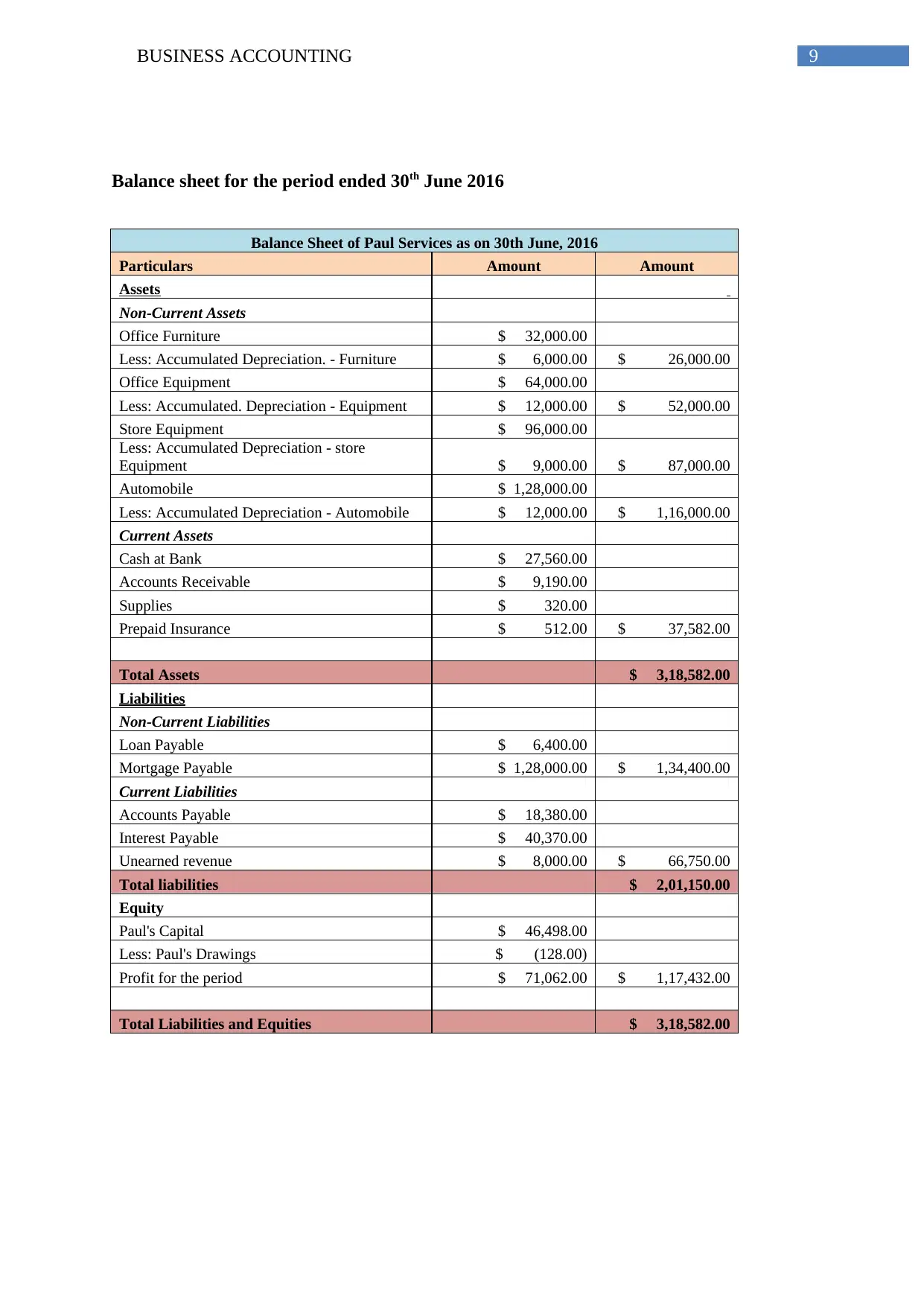

Balance sheet for the period ended 30th June 2016

Balance Sheet of Paul Services as on 30th June, 2016

Particulars Amount Amount

Assets

Non-Current Assets

Office Furniture $ 32,000.00

Less: Accumulated Depreciation. - Furniture $ 6,000.00 $ 26,000.00

Office Equipment $ 64,000.00

Less: Accumulated. Depreciation - Equipment $ 12,000.00 $ 52,000.00

Store Equipment $ 96,000.00

Less: Accumulated Depreciation - store

Equipment $ 9,000.00 $ 87,000.00

Automobile $ 1,28,000.00

Less: Accumulated Depreciation - Automobile $ 12,000.00 $ 1,16,000.00

Current Assets

Cash at Bank $ 27,560.00

Accounts Receivable $ 9,190.00

Supplies $ 320.00

Prepaid Insurance $ 512.00 $ 37,582.00

Total Assets $ 3,18,582.00

Liabilities

Non-Current Liabilities

Loan Payable $ 6,400.00

Mortgage Payable $ 1,28,000.00 $ 1,34,400.00

Current Liabilities

Accounts Payable $ 18,380.00

Interest Payable $ 40,370.00

Unearned revenue $ 8,000.00 $ 66,750.00

Total liabilities $ 2,01,150.00

Equity

Paul's Capital $ 46,498.00

Less: Paul's Drawings $ (128.00)

Profit for the period $ 71,062.00 $ 1,17,432.00

Total Liabilities and Equities $ 3,18,582.00

Balance sheet for the period ended 30th June 2016

Balance Sheet of Paul Services as on 30th June, 2016

Particulars Amount Amount

Assets

Non-Current Assets

Office Furniture $ 32,000.00

Less: Accumulated Depreciation. - Furniture $ 6,000.00 $ 26,000.00

Office Equipment $ 64,000.00

Less: Accumulated. Depreciation - Equipment $ 12,000.00 $ 52,000.00

Store Equipment $ 96,000.00

Less: Accumulated Depreciation - store

Equipment $ 9,000.00 $ 87,000.00

Automobile $ 1,28,000.00

Less: Accumulated Depreciation - Automobile $ 12,000.00 $ 1,16,000.00

Current Assets

Cash at Bank $ 27,560.00

Accounts Receivable $ 9,190.00

Supplies $ 320.00

Prepaid Insurance $ 512.00 $ 37,582.00

Total Assets $ 3,18,582.00

Liabilities

Non-Current Liabilities

Loan Payable $ 6,400.00

Mortgage Payable $ 1,28,000.00 $ 1,34,400.00

Current Liabilities

Accounts Payable $ 18,380.00

Interest Payable $ 40,370.00

Unearned revenue $ 8,000.00 $ 66,750.00

Total liabilities $ 2,01,150.00

Equity

Paul's Capital $ 46,498.00

Less: Paul's Drawings $ (128.00)

Profit for the period $ 71,062.00 $ 1,17,432.00

Total Liabilities and Equities $ 3,18,582.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS ACCOUNTING

Step 7

1. Trial balance and purpose of its creation

Trial balance is considered as the heart of business and is the summary for the

business activities. It indicates the financial health of business and helps the investors to take

decisions regarding investment in the company. Various entries for various accounts are

prepared through ledger. Trial balance is presenting all ledger balances in single worksheet as

on particular date (Fields 2016). Credit balances are reported in the credit column and the

debit balances are reported in the debit column. Sum of the debit column shall be matched

with the sum of credit balance. Trial balance can are prepared for checking the accuracy of

ledger accounts and ensuring that all transaction taken place during the concerned period has

been recorded in appropriate manner. As per the manual procedure of preparing the trial

balance the accountant generally prepares the trial balance for analysing the errors exists in

the accounts, if any (Henderson et al. 2015). Main purposes of creating the trial balance are

revealing –

Details adjustments for all transactions

all balances after making the required adjustments

Account balances of all the ledger account s before making the adjustments.

Trial balance assists in detecting the errors involved in the calculation, if any that will

have impact on the final accounts of the business. Various reasons for error in the general

ledger are material errors, misclassification of items or recording the entry in wrong amount

(Wahlen, Baginski and Bradshaw 2014). Trial balance is created for –

assuring that arithmetical accuracies are there with regard to the accounts books taken

place with the adjustments and recording the entries as per double entry bookkeeping

Step 7

1. Trial balance and purpose of its creation

Trial balance is considered as the heart of business and is the summary for the

business activities. It indicates the financial health of business and helps the investors to take

decisions regarding investment in the company. Various entries for various accounts are

prepared through ledger. Trial balance is presenting all ledger balances in single worksheet as

on particular date (Fields 2016). Credit balances are reported in the credit column and the

debit balances are reported in the debit column. Sum of the debit column shall be matched

with the sum of credit balance. Trial balance can are prepared for checking the accuracy of

ledger accounts and ensuring that all transaction taken place during the concerned period has

been recorded in appropriate manner. As per the manual procedure of preparing the trial

balance the accountant generally prepares the trial balance for analysing the errors exists in

the accounts, if any (Henderson et al. 2015). Main purposes of creating the trial balance are

revealing –

Details adjustments for all transactions

all balances after making the required adjustments

Account balances of all the ledger account s before making the adjustments.

Trial balance assists in detecting the errors involved in the calculation, if any that will

have impact on the final accounts of the business. Various reasons for error in the general

ledger are material errors, misclassification of items or recording the entry in wrong amount

(Wahlen, Baginski and Bradshaw 2014). Trial balance is created for –

assuring that arithmetical accuracies are there with regard to the accounts books taken

place with the adjustments and recording the entries as per double entry bookkeeping

11BUSINESS ACCOUNTING

It is represented as the summary sheet for listing all balances related to ledger

accounts. Therefore, it offers bird eye view for accounting transactions of the business

As the pre-requisite for preparing the financial statements as tallied trial balance helps

in preparing the financial statements (Warren and Jones 2018)

It can also be provided to the bank while applied for any loan or borrowings to

provide details regarding its credibility and capacity to take loan.

2. Adjusting journal entries and purpose of recording it

Adjusting entries are the accounting journal entries those are used to convert the

accounting records of the firm on the basis of accrual basis of the accounting. Adjusting

journal entries are generally made prior to the issuance of annual statements of the company

(Apostolou et al. 2013). Adjusting journal entries are prepared for assigning –

Prepayments of expenditures to the period when actually the expenses are incurred

Unearned revenue received from prepayment to period under which the income

earned

Accrues expenses to be paid in future when the expenses will actually be incurred

Accrued revenue those are already earned but will be received in future period (Weil,

Schipper and Francis 2013)

Further, adjusting entries are used to correcting errors and are required to be

completed before issuing the entity’s financial report. It includes the following events –

When the company has not recorded any entries for some of the expenses and

revenues but the expenses and revenues have been taken place during the concern

period and shall have been included in the profit and loss statement and balance sheet

for the same period.

It is represented as the summary sheet for listing all balances related to ledger

accounts. Therefore, it offers bird eye view for accounting transactions of the business

As the pre-requisite for preparing the financial statements as tallied trial balance helps

in preparing the financial statements (Warren and Jones 2018)

It can also be provided to the bank while applied for any loan or borrowings to

provide details regarding its credibility and capacity to take loan.

2. Adjusting journal entries and purpose of recording it

Adjusting entries are the accounting journal entries those are used to convert the

accounting records of the firm on the basis of accrual basis of the accounting. Adjusting

journal entries are generally made prior to the issuance of annual statements of the company

(Apostolou et al. 2013). Adjusting journal entries are prepared for assigning –

Prepayments of expenditures to the period when actually the expenses are incurred

Unearned revenue received from prepayment to period under which the income

earned

Accrues expenses to be paid in future when the expenses will actually be incurred

Accrued revenue those are already earned but will be received in future period (Weil,

Schipper and Francis 2013)

Further, adjusting entries are used to correcting errors and are required to be

completed before issuing the entity’s financial report. It includes the following events –

When the company has not recorded any entries for some of the expenses and

revenues but the expenses and revenues have been taken place during the concern

period and shall have been included in the profit and loss statement and balance sheet

for the same period.

12BUSINESS ACCOUNTING

Entry is made by the entity under one accounting period but it shall have been

required to e recorded in the period during which the revenues is actually earned or

expenses actually incurred or the expenses or revenues is to be separated for 2 or

more accounting period (Weygandt, Kimmel and Kieso 2015).

While in accordance with the entity’s policy item like fixed asset is reported as capital

account but that shall have been reported as expenses under the income statement.

3. Purpose of preparing the adjusted trial balance

Adjusted trial balance involves list down of all account balances and titles included in

the general ledger after preparing the adjusting entries for particular accounting period those

have been posted to accounts. It is considered as the internal rather than as the financial

statement. Main purpose of preparing the adjusted trial balance is becoming certain that the

total value of the debit balances in general ledger is equal to the total value of the credit

balances in general ledger (Hoyle, Schaefer and Doupnik 2015). Reason behind preparation

of adjusted trial balance is assuring that the adjusting entries have been posted correctly. This

is considered as the last step before preparation of the financial reports intended for the

external as well as internal users. If the balances reported under financial statements are not

correct, the statements will not be accurate. For the purpose of preparing the adjusted trial

balance different columns such as adjustment columns, profit and loss column and balance

sheet column is added (Gitman, Juchau and Flanagan 2015). Before preparing the financial

statement it shall be assured that the debit amount equal to the credit amount. This is

conformed through preparation of trial balance including all the expenses, revenues, assets,

liabilities and equities.

While the accrual method is followed by the entity, revenues are reported in the books

while they are earned rather than recording it when it is received. In same way, expenses are

reported in the period when it is incurred rather than when the payment has been made.

Entry is made by the entity under one accounting period but it shall have been

required to e recorded in the period during which the revenues is actually earned or

expenses actually incurred or the expenses or revenues is to be separated for 2 or

more accounting period (Weygandt, Kimmel and Kieso 2015).

While in accordance with the entity’s policy item like fixed asset is reported as capital

account but that shall have been reported as expenses under the income statement.

3. Purpose of preparing the adjusted trial balance

Adjusted trial balance involves list down of all account balances and titles included in

the general ledger after preparing the adjusting entries for particular accounting period those

have been posted to accounts. It is considered as the internal rather than as the financial

statement. Main purpose of preparing the adjusted trial balance is becoming certain that the

total value of the debit balances in general ledger is equal to the total value of the credit

balances in general ledger (Hoyle, Schaefer and Doupnik 2015). Reason behind preparation

of adjusted trial balance is assuring that the adjusting entries have been posted correctly. This

is considered as the last step before preparation of the financial reports intended for the

external as well as internal users. If the balances reported under financial statements are not

correct, the statements will not be accurate. For the purpose of preparing the adjusted trial

balance different columns such as adjustment columns, profit and loss column and balance

sheet column is added (Gitman, Juchau and Flanagan 2015). Before preparing the financial

statement it shall be assured that the debit amount equal to the credit amount. This is

conformed through preparation of trial balance including all the expenses, revenues, assets,

liabilities and equities.

While the accrual method is followed by the entity, revenues are reported in the books

while they are earned rather than recording it when it is received. In same way, expenses are

reported in the period when it is incurred rather than when the payment has been made.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUSINESS ACCOUNTING

Hence, prior to accounting period end, adjusting entries prepared to update all the accounts

(Year 2017).

4. Difference in closing journal entries and adjusting journal entries

Closing entries are considered as the journal entries passed at closing of the financial

period for shifting the temporary account to the permanent accounts. On the other hand,

adjusting journal entries are associated with the accounts for prepaid expenses, accrued

revenues, unearned revenues and accrued expenses (Needles, Powers and Crosson 2013).

Closing entries are prepared on last day of financial period but are reported in

accounts after the preparation of financial statements. Generally, the closing entries involve

profit and loss account. The closing entries set balances of expenses accounts and revenue

accounts to zero. It means the expenses account and revenue account will start with zero

balance in the new accounting period which in turn will enable the entity to to report the

amount of revenues as well as expenses easily in the account (Lee 2014). However, the net

amount of revenues and expenses at the closing of the accounting period are reported as

owner’s equity or retained earnings.

On the contrary, adjusting entries are passed at the closing of the accounting period

however are made prior to the preparation of financial statements. It is passed for making the

financial statements of the entity updated on accrual approach of accounting. For example,

the electricity is used by the entity each day however the bill is received after one month.

Similarly, the wage expenses are incurred by the entity each day however payroll including

the wages of the employees for last day of month is not entered in accounting records till the

closing of the accounting period. In addition to those, adjusting entries includes the amount

paid by the entity before they become the expenses (Edmonds et al. 2013). For instance,

insurance premium paid by the entity for the period of 3 months have been paid before

Hence, prior to accounting period end, adjusting entries prepared to update all the accounts

(Year 2017).

4. Difference in closing journal entries and adjusting journal entries

Closing entries are considered as the journal entries passed at closing of the financial

period for shifting the temporary account to the permanent accounts. On the other hand,

adjusting journal entries are associated with the accounts for prepaid expenses, accrued

revenues, unearned revenues and accrued expenses (Needles, Powers and Crosson 2013).

Closing entries are prepared on last day of financial period but are reported in

accounts after the preparation of financial statements. Generally, the closing entries involve

profit and loss account. The closing entries set balances of expenses accounts and revenue

accounts to zero. It means the expenses account and revenue account will start with zero

balance in the new accounting period which in turn will enable the entity to to report the

amount of revenues as well as expenses easily in the account (Lee 2014). However, the net

amount of revenues and expenses at the closing of the accounting period are reported as

owner’s equity or retained earnings.

On the contrary, adjusting entries are passed at the closing of the accounting period

however are made prior to the preparation of financial statements. It is passed for making the

financial statements of the entity updated on accrual approach of accounting. For example,

the electricity is used by the entity each day however the bill is received after one month.

Similarly, the wage expenses are incurred by the entity each day however payroll including

the wages of the employees for last day of month is not entered in accounting records till the

closing of the accounting period. In addition to those, adjusting entries includes the amount

paid by the entity before they become the expenses (Edmonds et al. 2013). For instance,

insurance premium paid by the entity for the period of 3 months have been paid before

14BUSINESS ACCOUNTING

commencement of those 3 months. The expenses may be deferred by the entity through

reporting it prior to start of 3 months period.

Conclusion

From the above conversation it is concluded that trial balance is an important part in

accounting. Using the trial balance, the entity can prepare income statement, trading account

and balance sheet as the account balances are available at the single place. Further, the

adjusted trial balances are used for assuring that the adjusting entries have been posted

correctly. It is the last step before preparation of the financial reports intended for the external

as well as internal users. Main purpose behind preparation of adjusted trial balance is

becoming certain that the total value of the debit balances in general ledger is equal to the

total value of the credit balances in general ledger. Adjusting entries as well as closing entries

both are prepared on last day of financial period however closing entries are reported in

accounts after the preparing annual statements and adjusting entries are passed prior to the

preparation of financial statements.

commencement of those 3 months. The expenses may be deferred by the entity through

reporting it prior to start of 3 months period.

Conclusion

From the above conversation it is concluded that trial balance is an important part in

accounting. Using the trial balance, the entity can prepare income statement, trading account

and balance sheet as the account balances are available at the single place. Further, the

adjusted trial balances are used for assuring that the adjusting entries have been posted

correctly. It is the last step before preparation of the financial reports intended for the external

as well as internal users. Main purpose behind preparation of adjusted trial balance is

becoming certain that the total value of the debit balances in general ledger is equal to the

total value of the credit balances in general ledger. Adjusting entries as well as closing entries

both are prepared on last day of financial period however closing entries are reported in

accounts after the preparing annual statements and adjusting entries are passed prior to the

preparation of financial statements.

15BUSINESS ACCOUNTING

Reference

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Watson, S.F., 2013. Accounting education

literature review (2010–2012). Journal of Accounting Education, 31(2), pp.107-161.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Edwards, J.R., 2013. A history of financial accounting (RLE Accounting) (Vol. 29).

Routledge.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers.

Amacom.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Cengage Learning.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Reference

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Watson, S.F., 2013. Accounting education

literature review (2010–2012). Journal of Accounting Education, 31(2), pp.107-161.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Edwards, J.R., 2013. A history of financial accounting (RLE Accounting) (Vol. 29).

Routledge.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers.

Amacom.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Cengage Learning.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16BUSINESS ACCOUNTING

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Year, B.C.S., 2017. Advanced accounting. Journal Entries in the books of Company, 12,

pp.12-750.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Year, B.C.S., 2017. Advanced accounting. Journal Entries in the books of Company, 12,

pp.12-750.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.