Analysis of Ferrari's IPO: Business Accounting and Finance Report

VerifiedAdded on 2022/09/11

|13

|3307

|14

Report

AI Summary

This report provides a comprehensive analysis of Ferrari's 2015 Initial Public Offering (IPO). It begins by exploring the benefits and drawbacks of going public, the motivations behind Ferrari's decision to list on the NYSE, and the details of the shares sold. The report delves into key aspects of the IPO, including the Greenshoe option, underwriting processes, book-building, and pricing strategies. It examines underwriters' roles, compensation, and price-stabilization techniques. Furthermore, it discusses lock-up agreements, compares the IPO's short-term and long-term performance, and analyzes the evolution of Ferrari's capital structure. The analysis incorporates relevant financial data and market dynamics to offer a detailed understanding of the IPO's success and implications.

Business Accounting and Finance

‘Ferrari: The 2015 Initial Public Offering’

Student Name:

Date:

‘Ferrari: The 2015 Initial Public Offering’

Student Name:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting and Finance

Table of Contents

Introduction.................................................................................................................................3

i...................................................................................................................................................3

a) Drawbacks and benefits related to going public......................................................................3

b) Motivation to go public for Ferrari........................................................................................3

c) Reason for going public by Ferrari using the (NYSE).............................................................4

d) Details of shares sold in Ferrari’s IPO: whether secondary or primary......................................4

ii. Meaning of Greenshoe option and whether such option was inclusive in Ferrari’s IPO.................4

iii. Underwriting.......................................................................................................................5

a) Key tasks to be performed by Underwriter.............................................................................5

b) Primary considerations for Underwriter’s selection................................................................5

c) Reasons for Syndication.......................................................................................................5

d) Underwriters’ Compensation................................................................................................5

e) Price-stabilization................................................................................................................6

iv. Book-building.....................................................................................................................6

v. Discussion about Ferrari’s pricing of IPO.................................................................................7

vi. Lock-up agreements of IPO..................................................................................................8

vii. Comparison of IPO performance...........................................................................................8

i. In short-term.......................................................................................................................8

ii. In Long-term.......................................................................................................................8

vii. Evolution of capital structure of Ferrari.................................................................................9

Conclusion................................................................................................................................10

References..................................................................................................................................12

1

Table of Contents

Introduction.................................................................................................................................3

i...................................................................................................................................................3

a) Drawbacks and benefits related to going public......................................................................3

b) Motivation to go public for Ferrari........................................................................................3

c) Reason for going public by Ferrari using the (NYSE).............................................................4

d) Details of shares sold in Ferrari’s IPO: whether secondary or primary......................................4

ii. Meaning of Greenshoe option and whether such option was inclusive in Ferrari’s IPO.................4

iii. Underwriting.......................................................................................................................5

a) Key tasks to be performed by Underwriter.............................................................................5

b) Primary considerations for Underwriter’s selection................................................................5

c) Reasons for Syndication.......................................................................................................5

d) Underwriters’ Compensation................................................................................................5

e) Price-stabilization................................................................................................................6

iv. Book-building.....................................................................................................................6

v. Discussion about Ferrari’s pricing of IPO.................................................................................7

vi. Lock-up agreements of IPO..................................................................................................8

vii. Comparison of IPO performance...........................................................................................8

i. In short-term.......................................................................................................................8

ii. In Long-term.......................................................................................................................8

vii. Evolution of capital structure of Ferrari.................................................................................9

Conclusion................................................................................................................................10

References..................................................................................................................................12

1

Business Accounting and Finance

Introduction

This report divulges the key information of the related to the initial public offer and further public offer

related to the public issue. In this report, motivational to the public limited company by the Ferrari and

other associated factors related to the underwriter has been taken into consideration. In addition to this,

key aspects related to the retaining, attracting and rewarding the talented management and technical

people in the organization by providing perks of direct ownership through shareholding has been

divulged. Furthermore, IPO is underperforming in the long run only when the share prices reflected

after the first trading day tend to be lower than the trading day price. Certain theories have proven this

concept based on evidence from certain countries have been divulged. In the end, the capital structure

of the company reveals that it has high financial leverage and due to the increased profitability, it has

less impact on the profit charges. This shows the financial structure and possible changes in the capital

of the company has been taken into consideration.

i.

a) Drawbacks and benefits related to going public

Benefits

Capital can be raised quickly as the quantum of investors reached is large.

The chances of generating publicity are huge as by going public, even the lesser popular

organizations come frequently in conversation because of their IPO.

Indirectly, the brand of the company initially grows because of being listed on well-known

stock exchanges (The Motley Fool, 2016).

Drawbacks

The process of going public is an expensive process concerning both the monetary cost and

time taken.

By being a public company, additional disclosure requirements get attached to the

organization, which again is costlier to follow (The Motley Fool, 2016).

b) Motivation to go public for Ferrari

Several opportunities available ahead of Ferrari after going public which motivated the organization is:

2

Introduction

This report divulges the key information of the related to the initial public offer and further public offer

related to the public issue. In this report, motivational to the public limited company by the Ferrari and

other associated factors related to the underwriter has been taken into consideration. In addition to this,

key aspects related to the retaining, attracting and rewarding the talented management and technical

people in the organization by providing perks of direct ownership through shareholding has been

divulged. Furthermore, IPO is underperforming in the long run only when the share prices reflected

after the first trading day tend to be lower than the trading day price. Certain theories have proven this

concept based on evidence from certain countries have been divulged. In the end, the capital structure

of the company reveals that it has high financial leverage and due to the increased profitability, it has

less impact on the profit charges. This shows the financial structure and possible changes in the capital

of the company has been taken into consideration.

i.

a) Drawbacks and benefits related to going public

Benefits

Capital can be raised quickly as the quantum of investors reached is large.

The chances of generating publicity are huge as by going public, even the lesser popular

organizations come frequently in conversation because of their IPO.

Indirectly, the brand of the company initially grows because of being listed on well-known

stock exchanges (The Motley Fool, 2016).

Drawbacks

The process of going public is an expensive process concerning both the monetary cost and

time taken.

By being a public company, additional disclosure requirements get attached to the

organization, which again is costlier to follow (The Motley Fool, 2016).

b) Motivation to go public for Ferrari

Several opportunities available ahead of Ferrari after going public which motivated the organization is:

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Accounting and Finance

Extension and promotion of brand name in the global luxurious and premier lifestyle

corporations.

Accessibility to debt and equity capital for Ferrari on favorable covenants.

Retaining, attracting and rewarding the talented management and technical people in the

organization by providing them perks of direct ownership through shareholding.

c) Reason for going public by Ferrari using the (NYSE)

Ferrari since the initial success had been a vendor of handmade cars and later on other variants to

various Americans. The company’s clients comprise of wealthiest families based in America and even

included, princes, and kings. The company through the NYSE wanted to aim upon these clients and

other important American investors, as America always was a very crucial market for Ferrari. Hence,

NYSE was chosen.

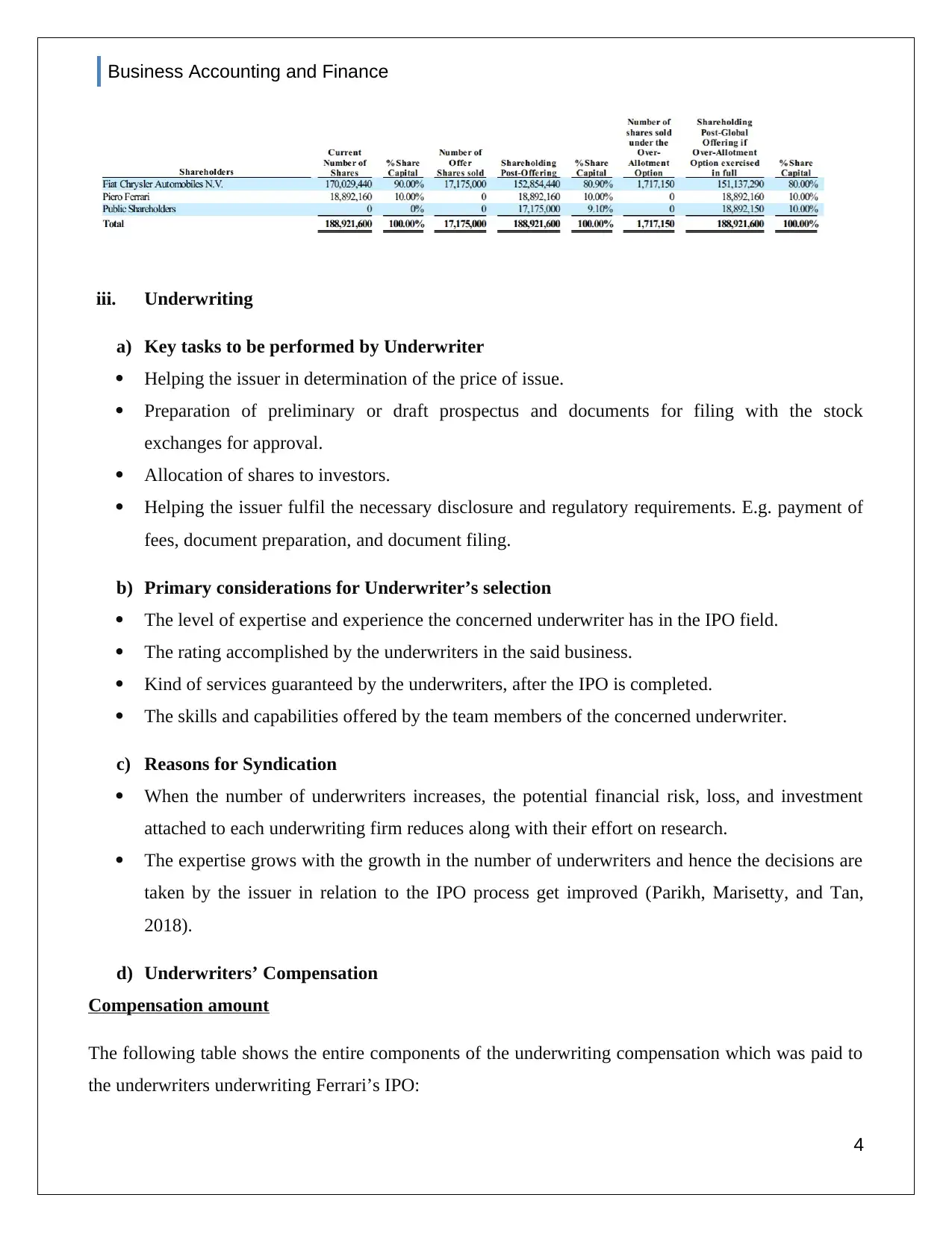

d) Details of shares sold in Ferrari’s IPO: whether secondary or primary

The IPO was undertaken by FCA as a means to separate Ferrari to operate it as a distinct entity.

Resultant, through the IPO, 17.175 million secondary shares of the organization Ferrari were initially

sold, which ranged to around the company’s 9% share capital. These are secondary shares only as prior

to this IPO, these shares are held by the current selling shareholder of them, i.e. “Fiat Chrysler

Automobiles” N.V. (FCA). These are not primary shares for Ferrari as no proceeds out of them shall

belong to Ferrari.

ii. Meaning of Greenshoe option and whether such option was inclusive in Ferrari’s IPO

Through this option the underwriters of the issue can sell additional shares (not more than 15% of

issue) during an issue using the IPO option. A special agreement is required to be contracted between

the underwriters and the issuer for the same. However, generally, the option has to be exercised by the

underwriters within 30 days after which offer have been made. This practice is usually followed to

legally stabilize the initial pricing of the offer (Ribeiro, 2008).

Did Ferrari provided its underwriters with Greenshoe option?

However, Ferrari has also provided its underwriters the greenshoe option. The underwriters are allowed

to sell 1,717,150 shares additionally within 30 days from prospectus’s offering if their exists over-

allotments.

3

Extension and promotion of brand name in the global luxurious and premier lifestyle

corporations.

Accessibility to debt and equity capital for Ferrari on favorable covenants.

Retaining, attracting and rewarding the talented management and technical people in the

organization by providing them perks of direct ownership through shareholding.

c) Reason for going public by Ferrari using the (NYSE)

Ferrari since the initial success had been a vendor of handmade cars and later on other variants to

various Americans. The company’s clients comprise of wealthiest families based in America and even

included, princes, and kings. The company through the NYSE wanted to aim upon these clients and

other important American investors, as America always was a very crucial market for Ferrari. Hence,

NYSE was chosen.

d) Details of shares sold in Ferrari’s IPO: whether secondary or primary

The IPO was undertaken by FCA as a means to separate Ferrari to operate it as a distinct entity.

Resultant, through the IPO, 17.175 million secondary shares of the organization Ferrari were initially

sold, which ranged to around the company’s 9% share capital. These are secondary shares only as prior

to this IPO, these shares are held by the current selling shareholder of them, i.e. “Fiat Chrysler

Automobiles” N.V. (FCA). These are not primary shares for Ferrari as no proceeds out of them shall

belong to Ferrari.

ii. Meaning of Greenshoe option and whether such option was inclusive in Ferrari’s IPO

Through this option the underwriters of the issue can sell additional shares (not more than 15% of

issue) during an issue using the IPO option. A special agreement is required to be contracted between

the underwriters and the issuer for the same. However, generally, the option has to be exercised by the

underwriters within 30 days after which offer have been made. This practice is usually followed to

legally stabilize the initial pricing of the offer (Ribeiro, 2008).

Did Ferrari provided its underwriters with Greenshoe option?

However, Ferrari has also provided its underwriters the greenshoe option. The underwriters are allowed

to sell 1,717,150 shares additionally within 30 days from prospectus’s offering if their exists over-

allotments.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting and Finance

iii. Underwriting

a) Key tasks to be performed by Underwriter

Helping the issuer in determination of the price of issue.

Preparation of preliminary or draft prospectus and documents for filing with the stock

exchanges for approval.

Allocation of shares to investors.

Helping the issuer fulfil the necessary disclosure and regulatory requirements. E.g. payment of

fees, document preparation, and document filing.

b) Primary considerations for Underwriter’s selection

The level of expertise and experience the concerned underwriter has in the IPO field.

The rating accomplished by the underwriters in the said business.

Kind of services guaranteed by the underwriters, after the IPO is completed.

The skills and capabilities offered by the team members of the concerned underwriter.

c) Reasons for Syndication

When the number of underwriters increases, the potential financial risk, loss, and investment

attached to each underwriting firm reduces along with their effort on research.

The expertise grows with the growth in the number of underwriters and hence the decisions are

taken by the issuer in relation to the IPO process get improved (Parikh, Marisetty, and Tan,

2018).

d) Underwriters’ Compensation

Compensation amount

The following table shows the entire components of the underwriting compensation which was paid to

the underwriters underwriting Ferrari’s IPO:

4

iii. Underwriting

a) Key tasks to be performed by Underwriter

Helping the issuer in determination of the price of issue.

Preparation of preliminary or draft prospectus and documents for filing with the stock

exchanges for approval.

Allocation of shares to investors.

Helping the issuer fulfil the necessary disclosure and regulatory requirements. E.g. payment of

fees, document preparation, and document filing.

b) Primary considerations for Underwriter’s selection

The level of expertise and experience the concerned underwriter has in the IPO field.

The rating accomplished by the underwriters in the said business.

Kind of services guaranteed by the underwriters, after the IPO is completed.

The skills and capabilities offered by the team members of the concerned underwriter.

c) Reasons for Syndication

When the number of underwriters increases, the potential financial risk, loss, and investment

attached to each underwriting firm reduces along with their effort on research.

The expertise grows with the growth in the number of underwriters and hence the decisions are

taken by the issuer in relation to the IPO process get improved (Parikh, Marisetty, and Tan,

2018).

d) Underwriters’ Compensation

Compensation amount

The following table shows the entire components of the underwriting compensation which was paid to

the underwriters underwriting Ferrari’s IPO:

4

Business Accounting and Finance

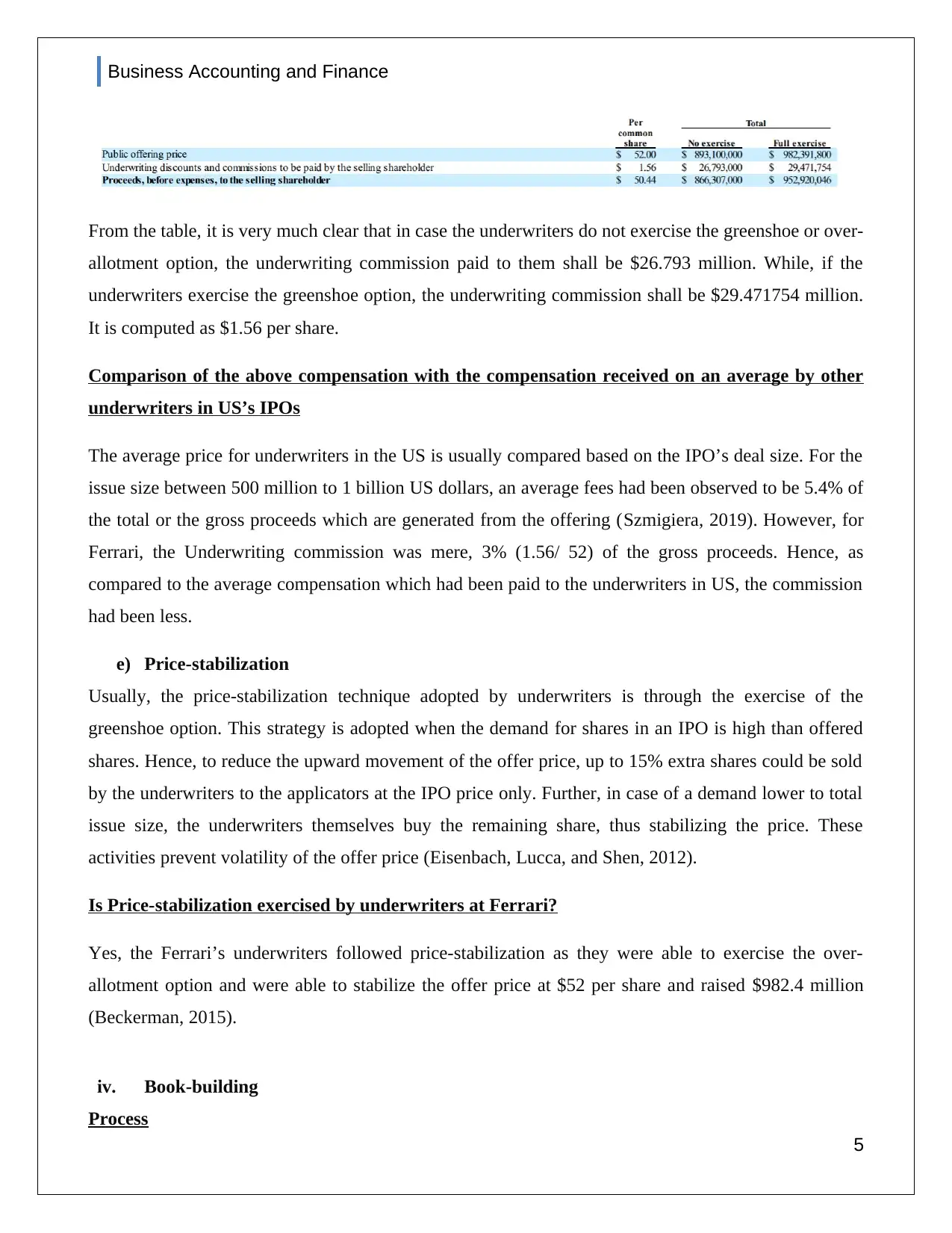

From the table, it is very much clear that in case the underwriters do not exercise the greenshoe or over-

allotment option, the underwriting commission paid to them shall be $26.793 million. While, if the

underwriters exercise the greenshoe option, the underwriting commission shall be $29.471754 million.

It is computed as $1.56 per share.

Comparison of the above compensation with the compensation received on an average by other

underwriters in US’s IPOs

The average price for underwriters in the US is usually compared based on the IPO’s deal size. For the

issue size between 500 million to 1 billion US dollars, an average fees had been observed to be 5.4% of

the total or the gross proceeds which are generated from the offering (Szmigiera, 2019). However, for

Ferrari, the Underwriting commission was mere, 3% (1.56/ 52) of the gross proceeds. Hence, as

compared to the average compensation which had been paid to the underwriters in US, the commission

had been less.

e) Price-stabilization

Usually, the price-stabilization technique adopted by underwriters is through the exercise of the

greenshoe option. This strategy is adopted when the demand for shares in an IPO is high than offered

shares. Hence, to reduce the upward movement of the offer price, up to 15% extra shares could be sold

by the underwriters to the applicators at the IPO price only. Further, in case of a demand lower to total

issue size, the underwriters themselves buy the remaining share, thus stabilizing the price. These

activities prevent volatility of the offer price (Eisenbach, Lucca, and Shen, 2012).

Is Price-stabilization exercised by underwriters at Ferrari?

Yes, the Ferrari’s underwriters followed price-stabilization as they were able to exercise the over-

allotment option and were able to stabilize the offer price at $52 per share and raised $982.4 million

(Beckerman, 2015).

iv. Book-building

Process

5

From the table, it is very much clear that in case the underwriters do not exercise the greenshoe or over-

allotment option, the underwriting commission paid to them shall be $26.793 million. While, if the

underwriters exercise the greenshoe option, the underwriting commission shall be $29.471754 million.

It is computed as $1.56 per share.

Comparison of the above compensation with the compensation received on an average by other

underwriters in US’s IPOs

The average price for underwriters in the US is usually compared based on the IPO’s deal size. For the

issue size between 500 million to 1 billion US dollars, an average fees had been observed to be 5.4% of

the total or the gross proceeds which are generated from the offering (Szmigiera, 2019). However, for

Ferrari, the Underwriting commission was mere, 3% (1.56/ 52) of the gross proceeds. Hence, as

compared to the average compensation which had been paid to the underwriters in US, the commission

had been less.

e) Price-stabilization

Usually, the price-stabilization technique adopted by underwriters is through the exercise of the

greenshoe option. This strategy is adopted when the demand for shares in an IPO is high than offered

shares. Hence, to reduce the upward movement of the offer price, up to 15% extra shares could be sold

by the underwriters to the applicators at the IPO price only. Further, in case of a demand lower to total

issue size, the underwriters themselves buy the remaining share, thus stabilizing the price. These

activities prevent volatility of the offer price (Eisenbach, Lucca, and Shen, 2012).

Is Price-stabilization exercised by underwriters at Ferrari?

Yes, the Ferrari’s underwriters followed price-stabilization as they were able to exercise the over-

allotment option and were able to stabilize the offer price at $52 per share and raised $982.4 million

(Beckerman, 2015).

iv. Book-building

Process

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Accounting and Finance

During an IPO book-build process an efficient price is discovered for the IPO offerings. A range is

decided during the process, based upon which the final price on which offer shall be made is

determined. In this method, bids at various prices are obtained from different investors, during the

period when IPO is exposed. These bids are equivalent or exceeding the base price of the offer. The

final price determination is however done after the date of closing of the bid.

Ferrari’s Book-build price range

For Ferrari, the book-build price range decided had been between USD 48 to USD 52 (Hirsch,2015).

Reasons for choosing USD52, i.e. top-end as offer price

Eventually, the offer price had been decided at USD52. The top-end of the range had been used

because of the expectation with the investors to be willing to pay high for the shares of a big brand

name like Ferrari. Additionally based on the statistics collected from meetings conducted in a road-

show with certain investors, the company analyzed a strong demand for its offered shares in the market.

Plus, the company has a syndicated underwriting, which further reduced the risk attached to losses due

to under-allotment due to high pricing (Driebusch, and Sylvers, 2015).

v. Discussion about Ferrari’s pricing of IPO

The pricing of IPO for Ferrari had been a result of the bookbuild process. The basic range set for the

bookbuild had been between USD 48 to USD 52. While at the bid end, Ferrari announced the IPO offer

price to be on the high end, i.e. at USD 52, along with the option to underwriters for stabilizing the

same using the greenshoe option. This high price plus the over-allotment option both had been

exercised based on the expectation of the high demand of the company’s stocks in the share market

(Hirsch,2015).

The pricing seems accurate concerning the brand name as well as the demand for the company’s

shares. The effective research placed by the syndicated underwriters has helped the company to

determine this offer price.

Would I Invest at the said price?

At this price or even a higher, Ferrari’s share is a must to do investment. The reason is the expectation

of high growth in share prices because of a good brand and high profitability. Additionally, the

6

During an IPO book-build process an efficient price is discovered for the IPO offerings. A range is

decided during the process, based upon which the final price on which offer shall be made is

determined. In this method, bids at various prices are obtained from different investors, during the

period when IPO is exposed. These bids are equivalent or exceeding the base price of the offer. The

final price determination is however done after the date of closing of the bid.

Ferrari’s Book-build price range

For Ferrari, the book-build price range decided had been between USD 48 to USD 52 (Hirsch,2015).

Reasons for choosing USD52, i.e. top-end as offer price

Eventually, the offer price had been decided at USD52. The top-end of the range had been used

because of the expectation with the investors to be willing to pay high for the shares of a big brand

name like Ferrari. Additionally based on the statistics collected from meetings conducted in a road-

show with certain investors, the company analyzed a strong demand for its offered shares in the market.

Plus, the company has a syndicated underwriting, which further reduced the risk attached to losses due

to under-allotment due to high pricing (Driebusch, and Sylvers, 2015).

v. Discussion about Ferrari’s pricing of IPO

The pricing of IPO for Ferrari had been a result of the bookbuild process. The basic range set for the

bookbuild had been between USD 48 to USD 52. While at the bid end, Ferrari announced the IPO offer

price to be on the high end, i.e. at USD 52, along with the option to underwriters for stabilizing the

same using the greenshoe option. This high price plus the over-allotment option both had been

exercised based on the expectation of the high demand of the company’s stocks in the share market

(Hirsch,2015).

The pricing seems accurate concerning the brand name as well as the demand for the company’s

shares. The effective research placed by the syndicated underwriters has helped the company to

determine this offer price.

Would I Invest at the said price?

At this price or even a higher, Ferrari’s share is a must to do investment. The reason is the expectation

of high growth in share prices because of a good brand and high profitability. Additionally, the

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting and Finance

company’s aim behind the IPO is not for leveraging debt, but for the creation of a separate brand than

FCA. Hence, the eventual risk is very low.

vi. Lock-up agreements of IPO

Lock-up agreements signify the legal contract entered by the underwriters with the insiders of the

issuer in the IPO process. This contract legally binds the underwriters from vending or disposing the

shares held by them.

Ferrari’s agreement of Lock-up

The Ferrari’s lock-up agreement called the underwriters to restrain from any pledge, offer, sale, selling

contract, purchase, selling option, or purchase option, or in any transfer and/or swap or exercise the

registration rights in respect to the common shares held by them for a tenure being 90 days from the

prospectus date, without obtaining the prior permission of Merrill Lynch, FennerandSmith

Incorporated, Pierce, and f UBS Securities LLC.

vii. Comparison of IPO performance

i. In short-term

As per signalling theory, issuers usually under-priced IPOs in the shorter-run for signalling their quality

and value to the investors in the market. In this method, a smaller portion of the equity is only offered

in IPO at a lower price, but later on the remaining equity at an increased price in secondary market. A

positive relationship though exists in this short term under-pricing and the overall improvement in the

market performance in the long-run (Perera, and Kulendran, 2016).

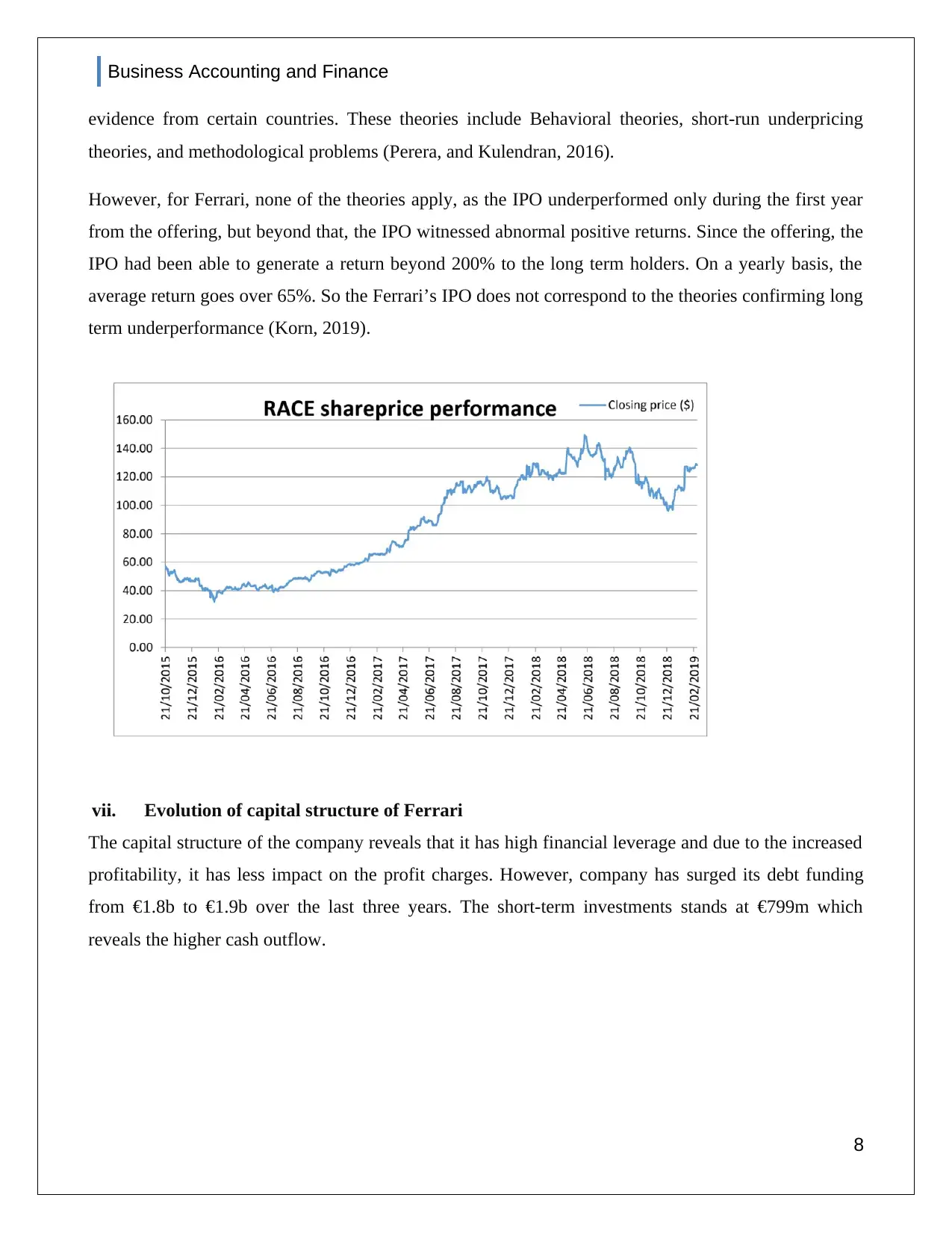

Ferrari’s performance seems to confirm this theory, as the offer price was USD52, which ended

USD55, signalling a growth of 5.77%. The growth shows obvious under-pricing on trade day. Further,

the company only offered approximately 9% of equity through IPO, with the rest 81% targeted for the

later period.

ii. In Long-term

An IPO is underperforming in the long run only when the share prices reflected after the first trading

day tend to be lower than the trading day price. Certain theories have proven this concept based on

7

company’s aim behind the IPO is not for leveraging debt, but for the creation of a separate brand than

FCA. Hence, the eventual risk is very low.

vi. Lock-up agreements of IPO

Lock-up agreements signify the legal contract entered by the underwriters with the insiders of the

issuer in the IPO process. This contract legally binds the underwriters from vending or disposing the

shares held by them.

Ferrari’s agreement of Lock-up

The Ferrari’s lock-up agreement called the underwriters to restrain from any pledge, offer, sale, selling

contract, purchase, selling option, or purchase option, or in any transfer and/or swap or exercise the

registration rights in respect to the common shares held by them for a tenure being 90 days from the

prospectus date, without obtaining the prior permission of Merrill Lynch, FennerandSmith

Incorporated, Pierce, and f UBS Securities LLC.

vii. Comparison of IPO performance

i. In short-term

As per signalling theory, issuers usually under-priced IPOs in the shorter-run for signalling their quality

and value to the investors in the market. In this method, a smaller portion of the equity is only offered

in IPO at a lower price, but later on the remaining equity at an increased price in secondary market. A

positive relationship though exists in this short term under-pricing and the overall improvement in the

market performance in the long-run (Perera, and Kulendran, 2016).

Ferrari’s performance seems to confirm this theory, as the offer price was USD52, which ended

USD55, signalling a growth of 5.77%. The growth shows obvious under-pricing on trade day. Further,

the company only offered approximately 9% of equity through IPO, with the rest 81% targeted for the

later period.

ii. In Long-term

An IPO is underperforming in the long run only when the share prices reflected after the first trading

day tend to be lower than the trading day price. Certain theories have proven this concept based on

7

Business Accounting and Finance

evidence from certain countries. These theories include Behavioral theories, short-run underpricing

theories, and methodological problems (Perera, and Kulendran, 2016).

However, for Ferrari, none of the theories apply, as the IPO underperformed only during the first year

from the offering, but beyond that, the IPO witnessed abnormal positive returns. Since the offering, the

IPO had been able to generate a return beyond 200% to the long term holders. On a yearly basis, the

average return goes over 65%. So the Ferrari’s IPO does not correspond to the theories confirming long

term underperformance (Korn, 2019).

vii. Evolution of capital structure of Ferrari

The capital structure of the company reveals that it has high financial leverage and due to the increased

profitability, it has less impact on the profit charges. However, company has surged its debt funding

from €1.8b to €1.9b over the last three years. The short-term investments stands at €799m which

reveals the higher cash outflow.

8

evidence from certain countries. These theories include Behavioral theories, short-run underpricing

theories, and methodological problems (Perera, and Kulendran, 2016).

However, for Ferrari, none of the theories apply, as the IPO underperformed only during the first year

from the offering, but beyond that, the IPO witnessed abnormal positive returns. Since the offering, the

IPO had been able to generate a return beyond 200% to the long term holders. On a yearly basis, the

average return goes over 65%. So the Ferrari’s IPO does not correspond to the theories confirming long

term underperformance (Korn, 2019).

vii. Evolution of capital structure of Ferrari

The capital structure of the company reveals that it has high financial leverage and due to the increased

profitability, it has less impact on the profit charges. However, company has surged its debt funding

from €1.8b to €1.9b over the last three years. The short-term investments stands at €799m which

reveals the higher cash outflow.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Accounting and Finance

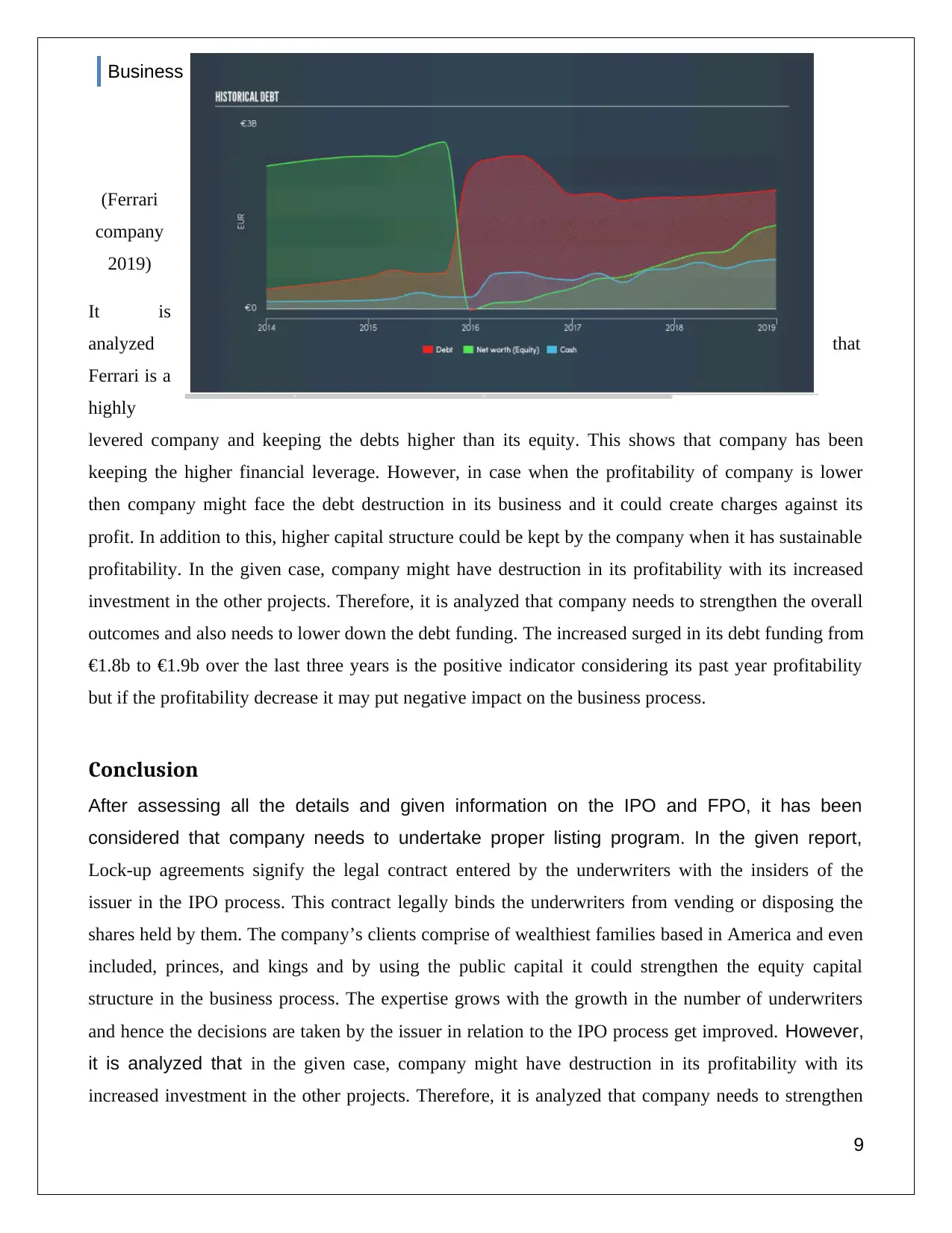

(Ferrari

company

2019)

It is

analyzed that

Ferrari is a

highly

levered company and keeping the debts higher than its equity. This shows that company has been

keeping the higher financial leverage. However, in case when the profitability of company is lower

then company might face the debt destruction in its business and it could create charges against its

profit. In addition to this, higher capital structure could be kept by the company when it has sustainable

profitability. In the given case, company might have destruction in its profitability with its increased

investment in the other projects. Therefore, it is analyzed that company needs to strengthen the overall

outcomes and also needs to lower down the debt funding. The increased surged in its debt funding from

€1.8b to €1.9b over the last three years is the positive indicator considering its past year profitability

but if the profitability decrease it may put negative impact on the business process.

Conclusion

After assessing all the details and given information on the IPO and FPO, it has been

considered that company needs to undertake proper listing program. In the given report,

Lock-up agreements signify the legal contract entered by the underwriters with the insiders of the

issuer in the IPO process. This contract legally binds the underwriters from vending or disposing the

shares held by them. The company’s clients comprise of wealthiest families based in America and even

included, princes, and kings and by using the public capital it could strengthen the equity capital

structure in the business process. The expertise grows with the growth in the number of underwriters

and hence the decisions are taken by the issuer in relation to the IPO process get improved. However,

it is analyzed that in the given case, company might have destruction in its profitability with its

increased investment in the other projects. Therefore, it is analyzed that company needs to strengthen

9

(Ferrari

company

2019)

It is

analyzed that

Ferrari is a

highly

levered company and keeping the debts higher than its equity. This shows that company has been

keeping the higher financial leverage. However, in case when the profitability of company is lower

then company might face the debt destruction in its business and it could create charges against its

profit. In addition to this, higher capital structure could be kept by the company when it has sustainable

profitability. In the given case, company might have destruction in its profitability with its increased

investment in the other projects. Therefore, it is analyzed that company needs to strengthen the overall

outcomes and also needs to lower down the debt funding. The increased surged in its debt funding from

€1.8b to €1.9b over the last three years is the positive indicator considering its past year profitability

but if the profitability decrease it may put negative impact on the business process.

Conclusion

After assessing all the details and given information on the IPO and FPO, it has been

considered that company needs to undertake proper listing program. In the given report,

Lock-up agreements signify the legal contract entered by the underwriters with the insiders of the

issuer in the IPO process. This contract legally binds the underwriters from vending or disposing the

shares held by them. The company’s clients comprise of wealthiest families based in America and even

included, princes, and kings and by using the public capital it could strengthen the equity capital

structure in the business process. The expertise grows with the growth in the number of underwriters

and hence the decisions are taken by the issuer in relation to the IPO process get improved. However,

it is analyzed that in the given case, company might have destruction in its profitability with its

increased investment in the other projects. Therefore, it is analyzed that company needs to strengthen

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Accounting and Finance

the overall outcomes and also needs to lower down the debt funding. The company through the NYSE

wanted to aim upon these clients and other important American investors, as America always was a

very crucial market for Ferrari. By being a public company, additional disclosure requirements get

attached to the organization, which again is costlier to follow and strengthen the brand image and

credibility of the company. The effective research placed by the syndicated underwriters has helped the

company to determine this offer price.

10

the overall outcomes and also needs to lower down the debt funding. The company through the NYSE

wanted to aim upon these clients and other important American investors, as America always was a

very crucial market for Ferrari. By being a public company, additional disclosure requirements get

attached to the organization, which again is costlier to follow and strengthen the brand image and

credibility of the company. The effective research placed by the syndicated underwriters has helped the

company to determine this offer price.

10

Business Accounting and Finance

References

Ferrari company (2019). Allocation Discretion, Information Sharing and Underwriter Syndication.

Available at https://simplywall.st/stocks/us/automobiles/nyse-race/ferrari/news/is-ferrari-n-v-nyserace-

a-financially-sound-company/ Accessed on 12th, December, 2019

Perera, W., and Kulendran, N. (2016). Why does underperformance of IPOs in the long-run become

debatable? A theoretical review. Retrieved December 12, 2019, from

http://www.maco.jfn.ac.lk/ijabf/wp-content/uploads/2017/11/Vol2_Issue1_1.pdf.

Ribeiro, A. G. (2008, August). Greenshoe Options: An IPOs Best Friend Available at

https://www.investopedia.com/articles/optioninvestor/08/greenshoe-option-ipo.asp. Accessed on 12th,

December, 2019

Eisenbach, T. M., Lucca, D. O., and Shen, K. (2012, October 31). In a Relationship: Evidence of

Underwriters' Efforts to Stabilize the Share Price in the Facebook IPO. Retrieved December 12, 2019,

Available at https://libertystreeteconomics.newyorkfed.org/2012/10/in-a-relationship-underwriters-

efforts-to-stabilize-the-share-price-in-the-facebook-ipo.html. Accessed on 12th, December, 2019

Driebusch, C., and Sylvers, E. (2015, October 20). Ferrari IPO Prices at Top of Range. Retrieved from

https://www.wsj.com/articles/ferrari-ipo-prices-at-high-end-of-range-1445375676.

Hirsch, L. (2015, October 21). Ferrari faithful rev IPO price to top of range. Retrieved from

https://www.reuters.com/article/us-ferrari-ipo-idUSKCN0SE23S20151021.

Beckerman, J. (2015, October 22). Ferrari overallotment sold, IPO totaled $982.4M. Available at

https://www.marketwatch.com/story/ferrari-overallotment-sold-ipo-totaled-9824m-2015-10-22.

Accessed on 12th, December, 2019

The Motley Fool. (2016, May 18). Advantages and Disadvantages of Going Public Using an IPO.

Available at https://www.fool.com/knowledge-center/advantages-disadvantages-of-going-public-using-

an.aspx. Accessed on 12th, December, 2019

Parikh, N., Marisetty, V., and Tan, M. (2018, July 23). Allocation Discretion, Information Sharing and

Underwriter Syndication. Available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3217770.

Accessed on 12th, December, 2019

11

References

Ferrari company (2019). Allocation Discretion, Information Sharing and Underwriter Syndication.

Available at https://simplywall.st/stocks/us/automobiles/nyse-race/ferrari/news/is-ferrari-n-v-nyserace-

a-financially-sound-company/ Accessed on 12th, December, 2019

Perera, W., and Kulendran, N. (2016). Why does underperformance of IPOs in the long-run become

debatable? A theoretical review. Retrieved December 12, 2019, from

http://www.maco.jfn.ac.lk/ijabf/wp-content/uploads/2017/11/Vol2_Issue1_1.pdf.

Ribeiro, A. G. (2008, August). Greenshoe Options: An IPOs Best Friend Available at

https://www.investopedia.com/articles/optioninvestor/08/greenshoe-option-ipo.asp. Accessed on 12th,

December, 2019

Eisenbach, T. M., Lucca, D. O., and Shen, K. (2012, October 31). In a Relationship: Evidence of

Underwriters' Efforts to Stabilize the Share Price in the Facebook IPO. Retrieved December 12, 2019,

Available at https://libertystreeteconomics.newyorkfed.org/2012/10/in-a-relationship-underwriters-

efforts-to-stabilize-the-share-price-in-the-facebook-ipo.html. Accessed on 12th, December, 2019

Driebusch, C., and Sylvers, E. (2015, October 20). Ferrari IPO Prices at Top of Range. Retrieved from

https://www.wsj.com/articles/ferrari-ipo-prices-at-high-end-of-range-1445375676.

Hirsch, L. (2015, October 21). Ferrari faithful rev IPO price to top of range. Retrieved from

https://www.reuters.com/article/us-ferrari-ipo-idUSKCN0SE23S20151021.

Beckerman, J. (2015, October 22). Ferrari overallotment sold, IPO totaled $982.4M. Available at

https://www.marketwatch.com/story/ferrari-overallotment-sold-ipo-totaled-9824m-2015-10-22.

Accessed on 12th, December, 2019

The Motley Fool. (2016, May 18). Advantages and Disadvantages of Going Public Using an IPO.

Available at https://www.fool.com/knowledge-center/advantages-disadvantages-of-going-public-using-

an.aspx. Accessed on 12th, December, 2019

Parikh, N., Marisetty, V., and Tan, M. (2018, July 23). Allocation Discretion, Information Sharing and

Underwriter Syndication. Available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3217770.

Accessed on 12th, December, 2019

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13