Importance of Revaluation of Assets and Fundamental Characteristics of Financial Information

VerifiedAdded on 2023/04/04

|14

|2437

|442

AI Summary

This essay discusses the importance of revaluation of assets and the fundamental characteristics of financial information. It explores the relevance and faithful representation of financial information in the context of Telstra and BRISCOE Group Limited. The essay highlights the impact of these characteristics on investment decision-making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS ACCOUNTING

Business Accounting

Name of the Student

Name of the University

Author’s Note

Business Accounting

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS ACCOUNTING

Summary

It can be seen from the first part of the essay that the management of Telstra is required to

undertake the revaluation of the property in order to ensure the faithful representation of the

financial information. After that, this essay discusses about the two main fundamental

characteristic of financial information that are relevance and faithful representation. It can be

seen from the third part of the essay that the management of BRISCOE Group Limited has

ensured the presentation of fundamental characteristic of financial information in the reporting of

inventories and property, plant and equipment which helps the investors in gaining the

information so that they can make effective investment decision about the firm.

Summary

It can be seen from the first part of the essay that the management of Telstra is required to

undertake the revaluation of the property in order to ensure the faithful representation of the

financial information. After that, this essay discusses about the two main fundamental

characteristic of financial information that are relevance and faithful representation. It can be

seen from the third part of the essay that the management of BRISCOE Group Limited has

ensured the presentation of fundamental characteristic of financial information in the reporting of

inventories and property, plant and equipment which helps the investors in gaining the

information so that they can make effective investment decision about the firm.

2BUSINESS ACCOUNTING

Table of Contents

Part 1................................................................................................................................................3

Part 2................................................................................................................................................4

Part 3................................................................................................................................................6

Part 4..............................................................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Part 1................................................................................................................................................3

Part 2................................................................................................................................................4

Part 3................................................................................................................................................6

Part 4..............................................................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3BUSINESS ACCOUNTING

Part 1

Revaluation of assets is considered as a crucial aspect for the managements of the

companies because it helps in showing the fair value of the assets. For this reason, asset

revaluation is considered as the adjusted made to the recorded value of an asset in order to

accurately reflect the current market value of that particular asset (Choi et al. 2013). The vast

practice of asset revaluation can be seen in the financial system of Australia where the

availability of AASB 116 Property, Plant and Equipment can be seen for providing the

necessary guidelines on property revaluation. According to AASB 116, Paragraph 31, after the

recognition of an asset, a company is needed to carry an item of property, plant and equipment at

a revalued amount whose fair values can be measured on reliable basis (aasb.gov.au 2019). It

also states that the item needs to be carried at fair value at the revaluation date. The frequency of

revaluation is largely dependent upon the fair value changes of the item that is being evaluated

by the company (aasb.gov.au 2019).

Now, it needs to be mentioned that the revaluation of a property at fair value has certain

positive connection with the qualitative characteristic of faithful representation. Faithful

presentation is considered as a crucial qualitative characteristic which ensures that financial

statements accurately reflect the business condition (Sytnik 2014). This characteristic states that

the financial information must be presented in the true and faithful manner in order to be useful

to the users of the financial statements. For example, in case a firm shows in its statement of

financial position that it has an accounts receivable of $100,000 as of the end of the year, then

the amount should indeed have been presented in the statement of financial position of that

Part 1

Revaluation of assets is considered as a crucial aspect for the managements of the

companies because it helps in showing the fair value of the assets. For this reason, asset

revaluation is considered as the adjusted made to the recorded value of an asset in order to

accurately reflect the current market value of that particular asset (Choi et al. 2013). The vast

practice of asset revaluation can be seen in the financial system of Australia where the

availability of AASB 116 Property, Plant and Equipment can be seen for providing the

necessary guidelines on property revaluation. According to AASB 116, Paragraph 31, after the

recognition of an asset, a company is needed to carry an item of property, plant and equipment at

a revalued amount whose fair values can be measured on reliable basis (aasb.gov.au 2019). It

also states that the item needs to be carried at fair value at the revaluation date. The frequency of

revaluation is largely dependent upon the fair value changes of the item that is being evaluated

by the company (aasb.gov.au 2019).

Now, it needs to be mentioned that the revaluation of a property at fair value has certain

positive connection with the qualitative characteristic of faithful representation. Faithful

presentation is considered as a crucial qualitative characteristic which ensures that financial

statements accurately reflect the business condition (Sytnik 2014). This characteristic states that

the financial information must be presented in the true and faithful manner in order to be useful

to the users of the financial statements. For example, in case a firm shows in its statement of

financial position that it has an accounts receivable of $100,000 as of the end of the year, then

the amount should indeed have been presented in the statement of financial position of that

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS ACCOUNTING

company. It implies that the assets are needed to be presented at their fair value so that it reflects

the true financial reality of the company (Sytnik 2014).

According to the provided scenario of Telstra, the price of the property was $52 million

when it was bought in 2010, but the market value of the same in June 2018 has become more

than $200 million. It indicates towards the fact that there is a significant change in the market

value of that property in the current scenario. In this case, if the property is shown at the

historical cost price, it will be mere delivery of the information about the legal form of the asset

because there will not be any information on the substance of this asset. This will create a

material difference in the price of that property. However, the revaluation of the property as

suggested by the accountant will ensure that the property is reported in the financial statement at

its fair value after deducting any subsequent accumulated depreciation and subsequent

accumulated impairment losses due to the decrease or increase in the fair value of the asset

(Hodder, Hopkins and Schipper 2014). For this reason, the management of Telstra is

recommended to accept the suggestion of the accountant to revalue the property.

Part 2

According to the Australian financial regulatory framework, there are two fundamental

qualitative characteristic of accounting information in Australian business practices; they are

Relevance and Faithful Representation. These are discussed below:

Relevance – Relevant financial information has the capability to create a difference in the users’

decision-making process. For this, financial information needs to be both the predictive value

and confirmatory value. Financial information has the predictive value in case the users can use

them for predicting the firm’s future outcome (aasb.gov.au 2019). On the other hand, financial

company. It implies that the assets are needed to be presented at their fair value so that it reflects

the true financial reality of the company (Sytnik 2014).

According to the provided scenario of Telstra, the price of the property was $52 million

when it was bought in 2010, but the market value of the same in June 2018 has become more

than $200 million. It indicates towards the fact that there is a significant change in the market

value of that property in the current scenario. In this case, if the property is shown at the

historical cost price, it will be mere delivery of the information about the legal form of the asset

because there will not be any information on the substance of this asset. This will create a

material difference in the price of that property. However, the revaluation of the property as

suggested by the accountant will ensure that the property is reported in the financial statement at

its fair value after deducting any subsequent accumulated depreciation and subsequent

accumulated impairment losses due to the decrease or increase in the fair value of the asset

(Hodder, Hopkins and Schipper 2014). For this reason, the management of Telstra is

recommended to accept the suggestion of the accountant to revalue the property.

Part 2

According to the Australian financial regulatory framework, there are two fundamental

qualitative characteristic of accounting information in Australian business practices; they are

Relevance and Faithful Representation. These are discussed below:

Relevance – Relevant financial information has the capability to create a difference in the users’

decision-making process. For this, financial information needs to be both the predictive value

and confirmatory value. Financial information has the predictive value in case the users can use

them for predicting the firm’s future outcome (aasb.gov.au 2019). On the other hand, financial

5BUSINESS ACCOUNTING

information has confirmatory value in case the users can gain feedback from it about the

previous evaluation. These two values have interconnection because information with predictive

value also possesses the confirmatory value. Two crucial aspects under this fundamental

qualitative characteristic are materiality and measurement uncertainty. Information can be

considered as material in case its omission can influence the decision-making process of the

primary users of general purpose financial reports that have been prepared based on the financial

information about the company (Henderson et al. 2015). Thus, materiality can be considered as a

firm-specific feature of relevance on the basis of magnitude or nature, or both, of the financial

substance of the firm. At the same time, measurement uncertainty affects the relevance of

financial information. The occurrence of measurement uncertainly can be seen when an asset or

liability related measure cannot be directly observed. For this reason, an estimate has the

capability of providing relevant information (Francis, Pinnuck and Watanabe 2013).

Faithful Representation – Economic phenomena in words and numbers can be seen in the

financial statements and in order to be useful to the users of the financial statement, financial

information must be faithfully represented along with maintaining its relevance. Faithful

representation helps in providing information about an economic phenomena’s substance instead

of its mere delivery of legal form related information (aasb.gov.au 2019). The presence of three

characteristic needs to be there in order to be faithfully represented; they are complete, neutral

and free from error. Complete means the inclusion of all information required for the users for

understanding the depiction of the phenomena including all required explanation as well as

description. Neutral means the absence of bias in the selection or presentation of the financial

statements. Free from errors means the absence of errors or omissions in the description of the

economic phenomena in the financial statements (Palea 2013).

information has confirmatory value in case the users can gain feedback from it about the

previous evaluation. These two values have interconnection because information with predictive

value also possesses the confirmatory value. Two crucial aspects under this fundamental

qualitative characteristic are materiality and measurement uncertainty. Information can be

considered as material in case its omission can influence the decision-making process of the

primary users of general purpose financial reports that have been prepared based on the financial

information about the company (Henderson et al. 2015). Thus, materiality can be considered as a

firm-specific feature of relevance on the basis of magnitude or nature, or both, of the financial

substance of the firm. At the same time, measurement uncertainty affects the relevance of

financial information. The occurrence of measurement uncertainly can be seen when an asset or

liability related measure cannot be directly observed. For this reason, an estimate has the

capability of providing relevant information (Francis, Pinnuck and Watanabe 2013).

Faithful Representation – Economic phenomena in words and numbers can be seen in the

financial statements and in order to be useful to the users of the financial statement, financial

information must be faithfully represented along with maintaining its relevance. Faithful

representation helps in providing information about an economic phenomena’s substance instead

of its mere delivery of legal form related information (aasb.gov.au 2019). The presence of three

characteristic needs to be there in order to be faithfully represented; they are complete, neutral

and free from error. Complete means the inclusion of all information required for the users for

understanding the depiction of the phenomena including all required explanation as well as

description. Neutral means the absence of bias in the selection or presentation of the financial

statements. Free from errors means the absence of errors or omissions in the description of the

economic phenomena in the financial statements (Palea 2013).

6BUSINESS ACCOUNTING

Part 3

According to the conceptual framework of AASB, there are three steps for ascertaining

whether fundamental characteristics are presented in the financial statements. They are:

1. Identification of the economic phenomena that has the capability to become useful to the

users of the financial information;

2. Identification of the type of information related to the selected economic phenomena that

would be most relevant in case it is available and can be faithfully represented; and,

3. Determination of the fact that whether that information is available and can be faithfully

presented (aasb.gov.au 2019).

The following discussion shows the example of fundamental characteristics presented in the

annual report of BRISCOE Group Limited.

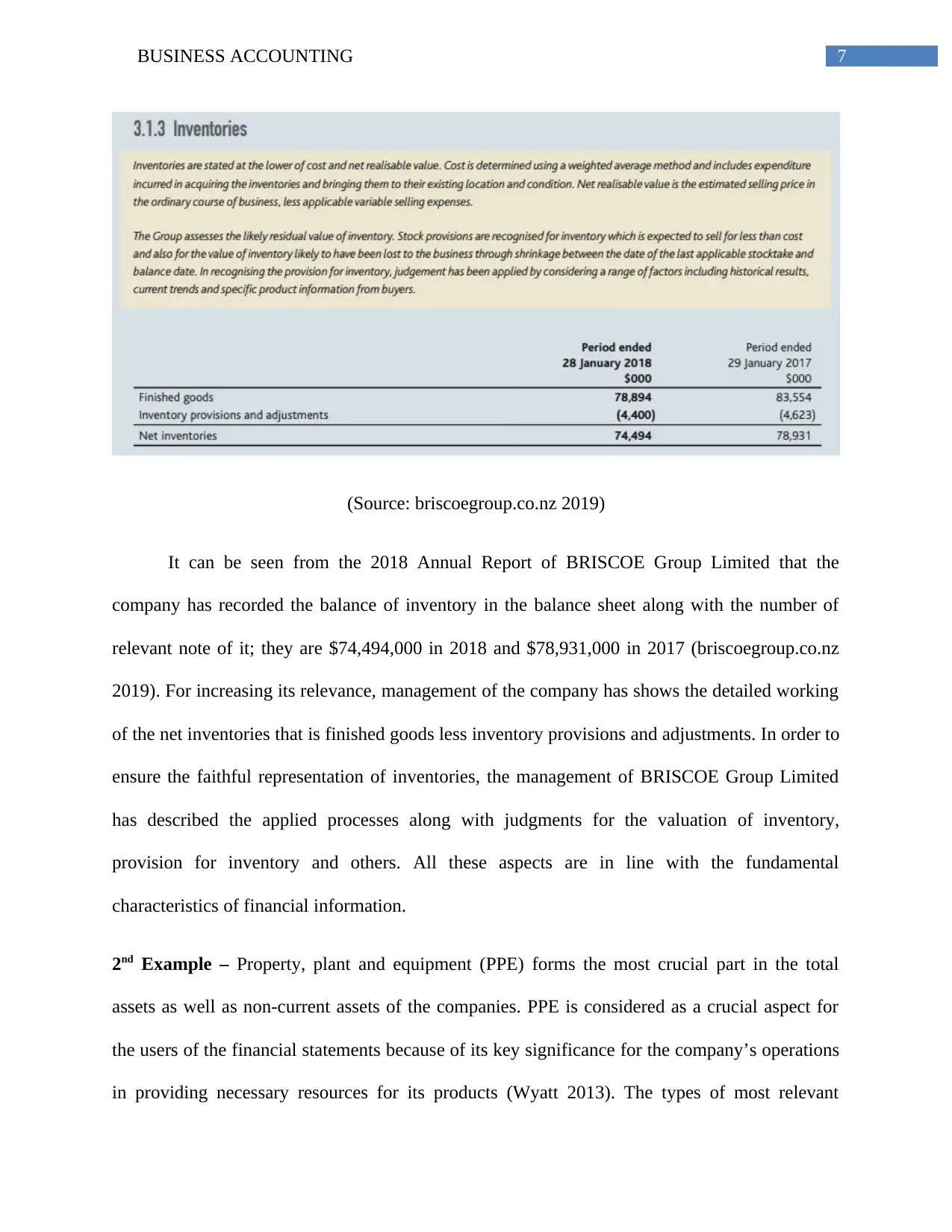

1st Example – Inventories form a crucial part in the current assets of the companies and thus, the

users of the financial statements consider inventories as crucial economic phenomena for

ascertaining the liquidity position as well as efficiency of the working capital management of the

companies (Nisha 2015). Inventory is crucial for BRISCOE Group Limited since they operate in

the retail industry. The most relevant type of information about inventory is their balance in the

balance sheet along with adopted accounting policies by BRISCOE Group Limited for the

valuation of inventory.

Part 3

According to the conceptual framework of AASB, there are three steps for ascertaining

whether fundamental characteristics are presented in the financial statements. They are:

1. Identification of the economic phenomena that has the capability to become useful to the

users of the financial information;

2. Identification of the type of information related to the selected economic phenomena that

would be most relevant in case it is available and can be faithfully represented; and,

3. Determination of the fact that whether that information is available and can be faithfully

presented (aasb.gov.au 2019).

The following discussion shows the example of fundamental characteristics presented in the

annual report of BRISCOE Group Limited.

1st Example – Inventories form a crucial part in the current assets of the companies and thus, the

users of the financial statements consider inventories as crucial economic phenomena for

ascertaining the liquidity position as well as efficiency of the working capital management of the

companies (Nisha 2015). Inventory is crucial for BRISCOE Group Limited since they operate in

the retail industry. The most relevant type of information about inventory is their balance in the

balance sheet along with adopted accounting policies by BRISCOE Group Limited for the

valuation of inventory.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS ACCOUNTING

(Source: briscoegroup.co.nz 2019)

It can be seen from the 2018 Annual Report of BRISCOE Group Limited that the

company has recorded the balance of inventory in the balance sheet along with the number of

relevant note of it; they are $74,494,000 in 2018 and $78,931,000 in 2017 (briscoegroup.co.nz

2019). For increasing its relevance, management of the company has shows the detailed working

of the net inventories that is finished goods less inventory provisions and adjustments. In order to

ensure the faithful representation of inventories, the management of BRISCOE Group Limited

has described the applied processes along with judgments for the valuation of inventory,

provision for inventory and others. All these aspects are in line with the fundamental

characteristics of financial information.

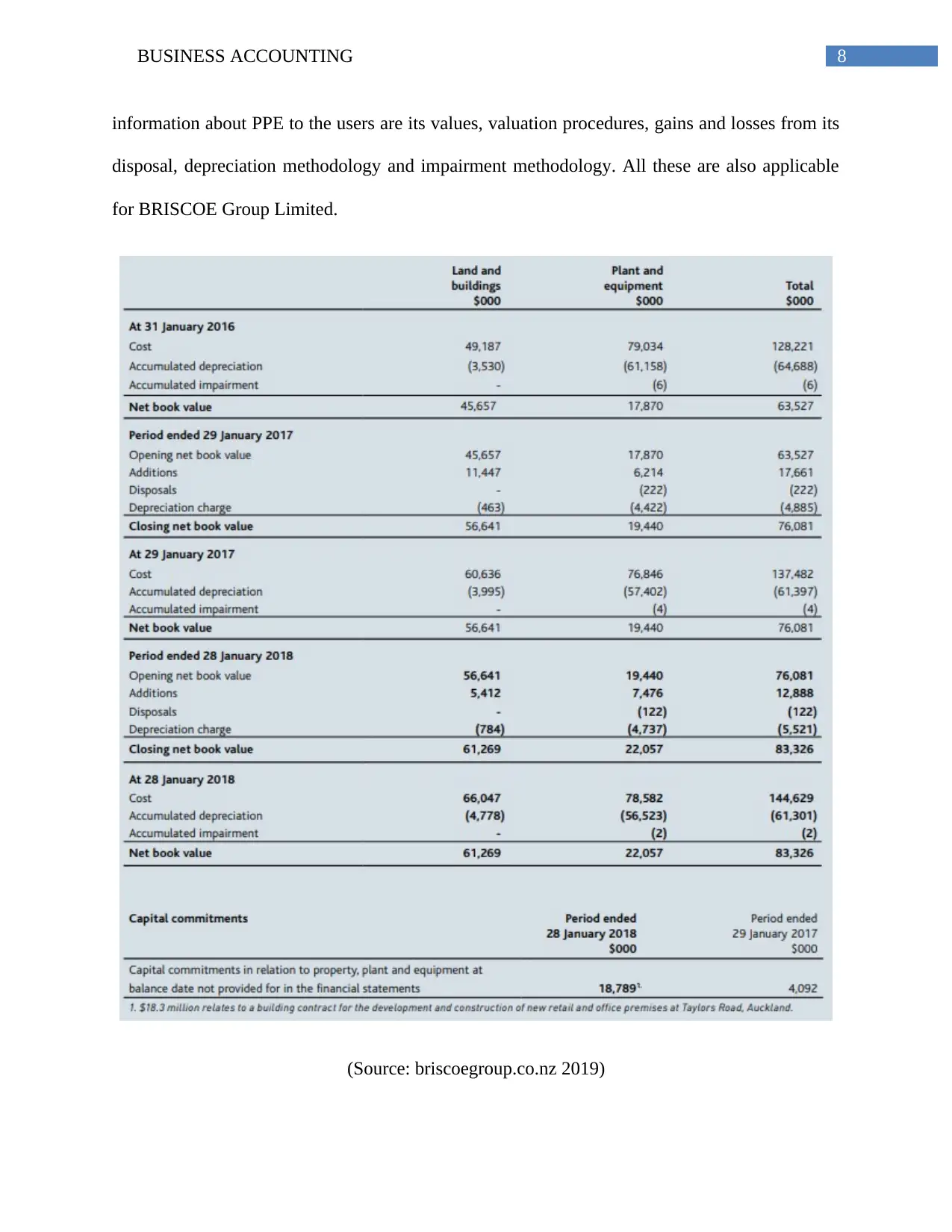

2nd Example – Property, plant and equipment (PPE) forms the most crucial part in the total

assets as well as non-current assets of the companies. PPE is considered as a crucial aspect for

the users of the financial statements because of its key significance for the company’s operations

in providing necessary resources for its products (Wyatt 2013). The types of most relevant

(Source: briscoegroup.co.nz 2019)

It can be seen from the 2018 Annual Report of BRISCOE Group Limited that the

company has recorded the balance of inventory in the balance sheet along with the number of

relevant note of it; they are $74,494,000 in 2018 and $78,931,000 in 2017 (briscoegroup.co.nz

2019). For increasing its relevance, management of the company has shows the detailed working

of the net inventories that is finished goods less inventory provisions and adjustments. In order to

ensure the faithful representation of inventories, the management of BRISCOE Group Limited

has described the applied processes along with judgments for the valuation of inventory,

provision for inventory and others. All these aspects are in line with the fundamental

characteristics of financial information.

2nd Example – Property, plant and equipment (PPE) forms the most crucial part in the total

assets as well as non-current assets of the companies. PPE is considered as a crucial aspect for

the users of the financial statements because of its key significance for the company’s operations

in providing necessary resources for its products (Wyatt 2013). The types of most relevant

8BUSINESS ACCOUNTING

information about PPE to the users are its values, valuation procedures, gains and losses from its

disposal, depreciation methodology and impairment methodology. All these are also applicable

for BRISCOE Group Limited.

(Source: briscoegroup.co.nz 2019)

information about PPE to the users are its values, valuation procedures, gains and losses from its

disposal, depreciation methodology and impairment methodology. All these are also applicable

for BRISCOE Group Limited.

(Source: briscoegroup.co.nz 2019)

9BUSINESS ACCOUNTING

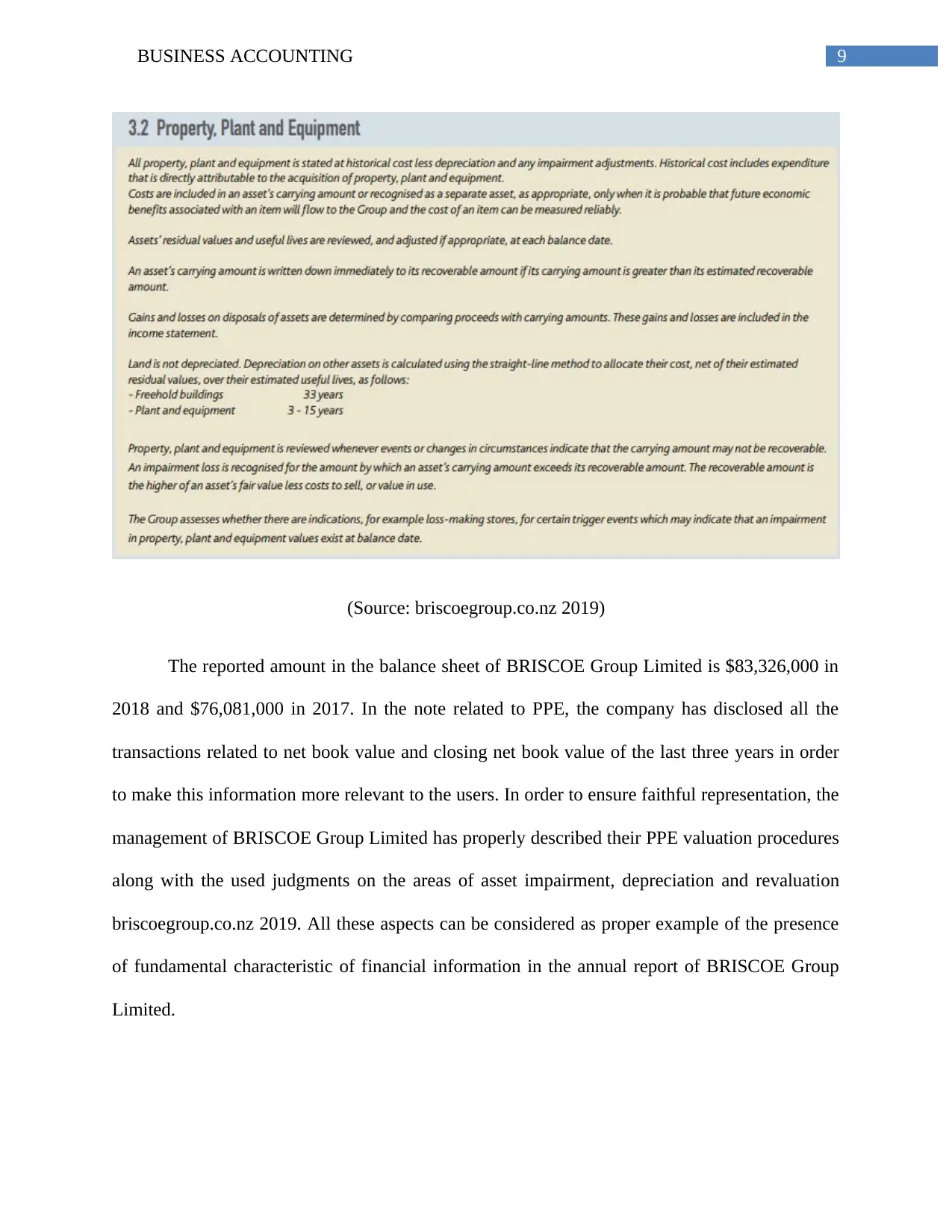

(Source: briscoegroup.co.nz 2019)

The reported amount in the balance sheet of BRISCOE Group Limited is $83,326,000 in

2018 and $76,081,000 in 2017. In the note related to PPE, the company has disclosed all the

transactions related to net book value and closing net book value of the last three years in order

to make this information more relevant to the users. In order to ensure faithful representation, the

management of BRISCOE Group Limited has properly described their PPE valuation procedures

along with the used judgments on the areas of asset impairment, depreciation and revaluation

briscoegroup.co.nz 2019. All these aspects can be considered as proper example of the presence

of fundamental characteristic of financial information in the annual report of BRISCOE Group

Limited.

(Source: briscoegroup.co.nz 2019)

The reported amount in the balance sheet of BRISCOE Group Limited is $83,326,000 in

2018 and $76,081,000 in 2017. In the note related to PPE, the company has disclosed all the

transactions related to net book value and closing net book value of the last three years in order

to make this information more relevant to the users. In order to ensure faithful representation, the

management of BRISCOE Group Limited has properly described their PPE valuation procedures

along with the used judgments on the areas of asset impairment, depreciation and revaluation

briscoegroup.co.nz 2019. All these aspects can be considered as proper example of the presence

of fundamental characteristic of financial information in the annual report of BRISCOE Group

Limited.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS ACCOUNTING

Part 4

The above discussion indicates towards the crucial fact that the information provided in

the financial statements must be relevant to the needs of the users of financial information and

they must be represented in faithful manner. There are certain groups of stakeholders of the

companies who are the statutory recipients of the fundamental qualitative characteristic of

financial information (Barth 2013). One of them is the investors who represent the security

markets. The presence of these fundamental characteristics of financial information is paramount

for the investors in gaining the required information about the economic phenomena of the

companies so that they can make effective investment decisions. In the presence of relevance and

faithful representation of financial information, investors can gain the exact information they

need to make the investment decisions (Nobes 2014).

It can be seen from the above discussion that there is the presence of all fundamental

characteristics of financial information in the annual report of BRISCOE Group Limited

regarding two crucial economic phenomena which are inventories and PPE. In the presence of

both relevance as well as faithful representation of financial information on these economic

phenomena, the investors can gain crucial information on the overall asset position of the

company along with the liquidity strength of the company (Barth 2013). This information assists

the investors in ascertaining BRISCOE Group Limited’s efficiency position and the overall

financial position in the financial year of 2018. These disclosures related to the inventory and

PPE will lead to the increase in faith of the investors of the company. At the same time,

BRISCOE Group Limited will be able in establishing goodwill in the securities markets for the

effective disclosure of financial information containing the fundamental characteristics of

financial information (Garanina and Kormiltseva 2014).

Part 4

The above discussion indicates towards the crucial fact that the information provided in

the financial statements must be relevant to the needs of the users of financial information and

they must be represented in faithful manner. There are certain groups of stakeholders of the

companies who are the statutory recipients of the fundamental qualitative characteristic of

financial information (Barth 2013). One of them is the investors who represent the security

markets. The presence of these fundamental characteristics of financial information is paramount

for the investors in gaining the required information about the economic phenomena of the

companies so that they can make effective investment decisions. In the presence of relevance and

faithful representation of financial information, investors can gain the exact information they

need to make the investment decisions (Nobes 2014).

It can be seen from the above discussion that there is the presence of all fundamental

characteristics of financial information in the annual report of BRISCOE Group Limited

regarding two crucial economic phenomena which are inventories and PPE. In the presence of

both relevance as well as faithful representation of financial information on these economic

phenomena, the investors can gain crucial information on the overall asset position of the

company along with the liquidity strength of the company (Barth 2013). This information assists

the investors in ascertaining BRISCOE Group Limited’s efficiency position and the overall

financial position in the financial year of 2018. These disclosures related to the inventory and

PPE will lead to the increase in faith of the investors of the company. At the same time,

BRISCOE Group Limited will be able in establishing goodwill in the securities markets for the

effective disclosure of financial information containing the fundamental characteristics of

financial information (Garanina and Kormiltseva 2014).

11BUSINESS ACCOUNTING

Conclusion

The above discussion sheds light on the importance as well as usefulness of the

revaluation of assets by considering the provided scenario of Telstra. It can be seen that the

company should revalue the property since the revaluation process will help in reporting the fair

value of the property which is in line with fundamental characteristic of faithful representation.

The above discussion also shows that the two fundamental characteristic of financial information

are relevance and faithful representation which increases the usefulness of the financial

information to the users of the financial statements for the purpose of making appropriate

investment decisions about the companies. It can be observed from the above discussion that

BRISCOE Group Limited has presented the fundamental characteristics of financial information

through the reporting of inventories and PPE. The above discussion states that the management

of BRISCOE Group Limited has disclosed the important information on inventories and PPE in

their annual report such as their values, measurement mechanism, impairment methodology,

depreciation methodology and others. In the presence of the disclosure of this information with

the presentation of fundamental characteristic of financial information, the investors from the

securities market can gain the required information on the financial performance, efficiency,

liquidity and financial position of BRISCOE Group Limited to make appropriate investment

decision.

Conclusion

The above discussion sheds light on the importance as well as usefulness of the

revaluation of assets by considering the provided scenario of Telstra. It can be seen that the

company should revalue the property since the revaluation process will help in reporting the fair

value of the property which is in line with fundamental characteristic of faithful representation.

The above discussion also shows that the two fundamental characteristic of financial information

are relevance and faithful representation which increases the usefulness of the financial

information to the users of the financial statements for the purpose of making appropriate

investment decisions about the companies. It can be observed from the above discussion that

BRISCOE Group Limited has presented the fundamental characteristics of financial information

through the reporting of inventories and PPE. The above discussion states that the management

of BRISCOE Group Limited has disclosed the important information on inventories and PPE in

their annual report such as their values, measurement mechanism, impairment methodology,

depreciation methodology and others. In the presence of the disclosure of this information with

the presentation of fundamental characteristic of financial information, the investors from the

securities market can gain the required information on the financial performance, efficiency,

liquidity and financial position of BRISCOE Group Limited to make appropriate investment

decision.

12BUSINESS ACCOUNTING

References

Aasb.gov.au. 2019. Conceptual Framework for Financial Reporting. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed 24 May

2019].

Aasb.gov.au. 2019. Property, Plant and Equipment. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 24 May 2019].

Barth, M.E., 2013. Global comparability in financial reporting: What, why, how, and

when?. China Journal of Accounting Studies, 1(1), pp.2-12.

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Briscoegroup.co.nz. 2019. ANNUAL REPORT for the period ended 28 January 2018. [online]

Available at: https://briscoegroup.co.nz/wp-content/uploads/BGP-2018-Annual-Report.pdf

[Accessed 24 May 2019].

Choi, T.H., Pae, J., Park, S. and Song, Y., 2013. Asset revaluations: motives and choice of items

to revalue. Asia-Pacific Journal of Accounting & Economics, 20(2), pp.144-171.

Francis, J.R., Pinnuck, M.L. and Watanabe, O., 2013. Auditor style and financial statement

comparability. The Accounting Review, 89(2), pp.605-633.

References

Aasb.gov.au. 2019. Conceptual Framework for Financial Reporting. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed 24 May

2019].

Aasb.gov.au. 2019. Property, Plant and Equipment. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 24 May 2019].

Barth, M.E., 2013. Global comparability in financial reporting: What, why, how, and

when?. China Journal of Accounting Studies, 1(1), pp.2-12.

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Briscoegroup.co.nz. 2019. ANNUAL REPORT for the period ended 28 January 2018. [online]

Available at: https://briscoegroup.co.nz/wp-content/uploads/BGP-2018-Annual-Report.pdf

[Accessed 24 May 2019].

Choi, T.H., Pae, J., Park, S. and Song, Y., 2013. Asset revaluations: motives and choice of items

to revalue. Asia-Pacific Journal of Accounting & Economics, 20(2), pp.144-171.

Francis, J.R., Pinnuck, M.L. and Watanabe, O., 2013. Auditor style and financial statement

comparability. The Accounting Review, 89(2), pp.605-633.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUSINESS ACCOUNTING

Garanina, T.A. and Kormiltseva, P.S., 2014. The effect of International Financial Reporting

Standards (IFRS) adoption on the value relevance of financial reporting: a case of Russia.

In Accounting in Central and Eastern Europe (pp. 27-60). Emerald Group Publishing Limited.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hodder, L., Hopkins, P. and Schipper, K., 2014. Fair value measurement in financial

reporting. Foundations and Trends® in Accounting, 8(3-4), pp.143-270.

Nisha, N., 2015. Inventory valuation practices: A developing country perspective. International

Journal of Information Research and Review, 2(7), pp.867-874.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Palea, V., 2013. IAS/IFRS and financial reporting quality: Lessons from the European

experience. China Journal of Accounting Research, 6(4), pp.247-263.

Sytnik, O.E., 2014. Comparative analysis of the guidelines for the preparation of financial

statements in accordance with IFRS and formed the Russian accounting rules. Сборник научных

трудов Sworld, 27(2), p.27.

Wyatt, P., 2013. Property valuation. John Wiley & Sons.

Garanina, T.A. and Kormiltseva, P.S., 2014. The effect of International Financial Reporting

Standards (IFRS) adoption on the value relevance of financial reporting: a case of Russia.

In Accounting in Central and Eastern Europe (pp. 27-60). Emerald Group Publishing Limited.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hodder, L., Hopkins, P. and Schipper, K., 2014. Fair value measurement in financial

reporting. Foundations and Trends® in Accounting, 8(3-4), pp.143-270.

Nisha, N., 2015. Inventory valuation practices: A developing country perspective. International

Journal of Information Research and Review, 2(7), pp.867-874.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Palea, V., 2013. IAS/IFRS and financial reporting quality: Lessons from the European

experience. China Journal of Accounting Research, 6(4), pp.247-263.

Sytnik, O.E., 2014. Comparative analysis of the guidelines for the preparation of financial

statements in accordance with IFRS and formed the Russian accounting rules. Сборник научных

трудов Sworld, 27(2), p.27.

Wyatt, P., 2013. Property valuation. John Wiley & Sons.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.