Accounting Principles: Trial Balance, Adjustments, and Financials

VerifiedAdded on 2023/06/04

|13

|2239

|413

Report

AI Summary

This report provides a detailed analysis of business accounting concepts, starting with an unadjusted trial balance for Paul Services as of June 30, 2016. It includes adjustment journal entries based on given adjustments, leading to the preparation of an adjusted trial balance. The report then constructs an income statement, closes journal entries, and presents the balance sheet and statement of changes in equity. Furthermore, it discusses the necessity of financial statements, explaining the purpose and importance of trial balances, adjustment entries, adjusted trial balances, and closing entries in ensuring accurate financial reporting and adherence to accounting principles such as matching and accrual concepts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Introduction.................................................................................................................................................3

Analysis and Calculation.............................................................................................................................4

Discussion....................................................................................................................................................9

Trial Balance............................................................................................................................................9

Adjustment Journal Entries.....................................................................................................................9

Adjusted Trial balance...........................................................................................................................10

Closing Journal Entries...........................................................................................................................10

References.................................................................................................................................................11

2 | P a g e

Contents

Introduction.................................................................................................................................................3

Analysis and Calculation.............................................................................................................................4

Discussion....................................................................................................................................................9

Trial Balance............................................................................................................................................9

Adjustment Journal Entries.....................................................................................................................9

Adjusted Trial balance...........................................................................................................................10

Closing Journal Entries...........................................................................................................................10

References.................................................................................................................................................11

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

A report has been prepared on the business accounting concepts. The unadjusted Trial Balance

of the company has been given along with the sheet showing the various adjustments. The

journal entries have been passed based on the adjustment given and the adjusted trial balance

has been prepared (Dumay & Baard, 2017). Post this the income statement has been prepared

and the closing entries have been passed in the journal books. Finally the balance sheet and the

statement of changes in equity was also being plotted. Post the analysis section, the theoretical

question on the need of financial statements and why the same is being prepared has been

done.

3 | P a g e

Introduction

A report has been prepared on the business accounting concepts. The unadjusted Trial Balance

of the company has been given along with the sheet showing the various adjustments. The

journal entries have been passed based on the adjustment given and the adjusted trial balance

has been prepared (Dumay & Baard, 2017). Post this the income statement has been prepared

and the closing entries have been passed in the journal books. Finally the balance sheet and the

statement of changes in equity was also being plotted. Post the analysis section, the theoretical

question on the need of financial statements and why the same is being prepared has been

done.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

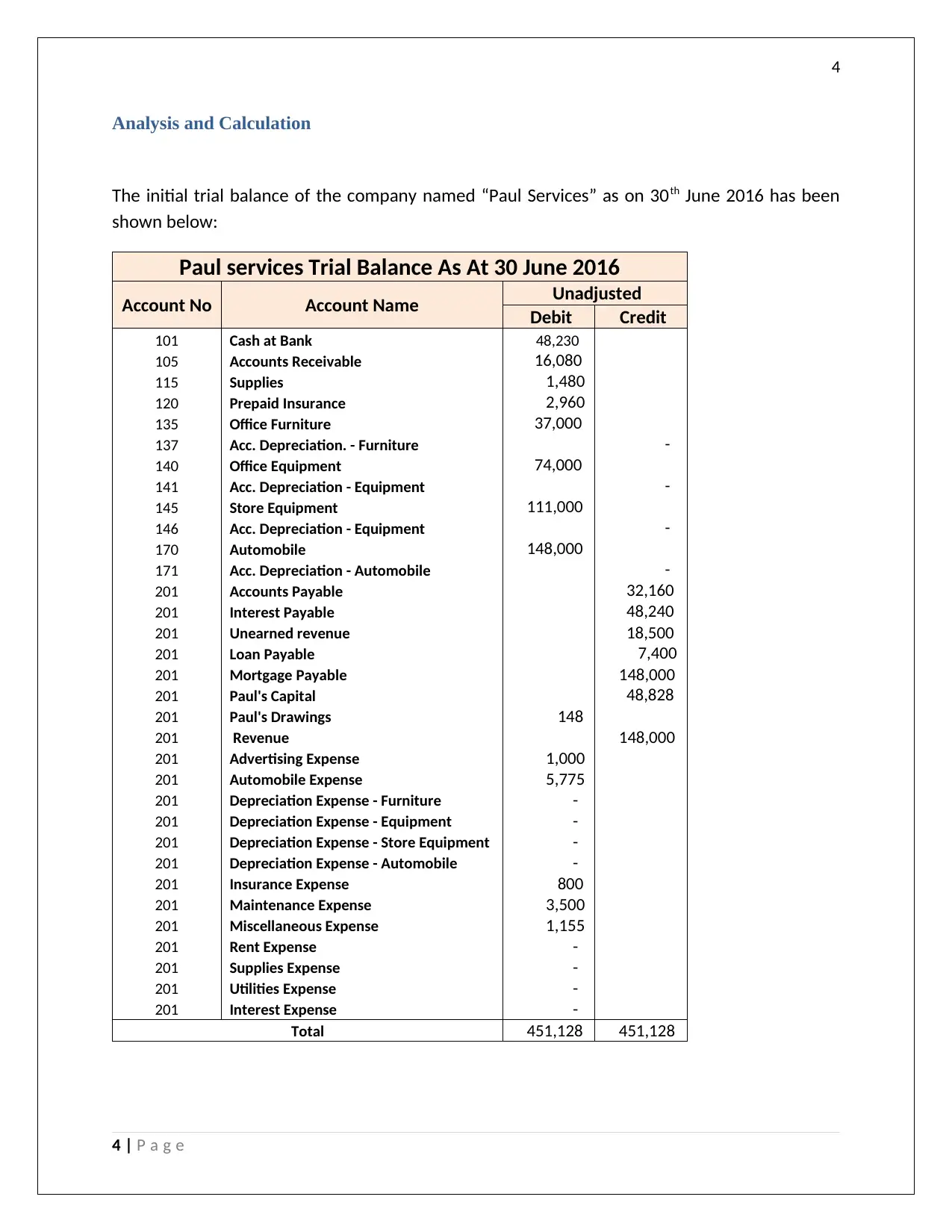

Analysis and Calculation

The initial trial balance of the company named “Paul Services” as on 30th June 2016 has been

shown below:

Paul services Trial Balance As At 30 June 2016

Account No Account Name Unadjusted

Debit Credit

101 Cash at Bank 48,230

105 Accounts Receivable 16,080

115 Supplies 1,480

120 Prepaid Insurance 2,960

135 Office Furniture 37,000

137 Acc. Depreciation. - Furniture -

140 Office Equipment 74,000

141 Acc. Depreciation - Equipment -

145 Store Equipment 111,000

146 Acc. Depreciation - Equipment -

170 Automobile 148,000

171 Acc. Depreciation - Automobile -

201 Accounts Payable 32,160

201 Interest Payable 48,240

201 Unearned revenue 18,500

201 Loan Payable 7,400

201 Mortgage Payable 148,000

201 Paul's Capital 48,828

201 Paul's Drawings 148

201 Revenue 148,000

201 Advertising Expense 1,000

201 Automobile Expense 5,775

201 Depreciation Expense - Furniture -

201 Depreciation Expense - Equipment -

201 Depreciation Expense - Store Equipment -

201 Depreciation Expense - Automobile -

201 Insurance Expense 800

201 Maintenance Expense 3,500

201 Miscellaneous Expense 1,155

201 Rent Expense -

201 Supplies Expense -

201 Utilities Expense -

201 Interest Expense -

Total 451,128 451,128

4 | P a g e

Analysis and Calculation

The initial trial balance of the company named “Paul Services” as on 30th June 2016 has been

shown below:

Paul services Trial Balance As At 30 June 2016

Account No Account Name Unadjusted

Debit Credit

101 Cash at Bank 48,230

105 Accounts Receivable 16,080

115 Supplies 1,480

120 Prepaid Insurance 2,960

135 Office Furniture 37,000

137 Acc. Depreciation. - Furniture -

140 Office Equipment 74,000

141 Acc. Depreciation - Equipment -

145 Store Equipment 111,000

146 Acc. Depreciation - Equipment -

170 Automobile 148,000

171 Acc. Depreciation - Automobile -

201 Accounts Payable 32,160

201 Interest Payable 48,240

201 Unearned revenue 18,500

201 Loan Payable 7,400

201 Mortgage Payable 148,000

201 Paul's Capital 48,828

201 Paul's Drawings 148

201 Revenue 148,000

201 Advertising Expense 1,000

201 Automobile Expense 5,775

201 Depreciation Expense - Furniture -

201 Depreciation Expense - Equipment -

201 Depreciation Expense - Store Equipment -

201 Depreciation Expense - Automobile -

201 Insurance Expense 800

201 Maintenance Expense 3,500

201 Miscellaneous Expense 1,155

201 Rent Expense -

201 Supplies Expense -

201 Utilities Expense -

201 Interest Expense -

Total 451,128 451,128

4 | P a g e

5

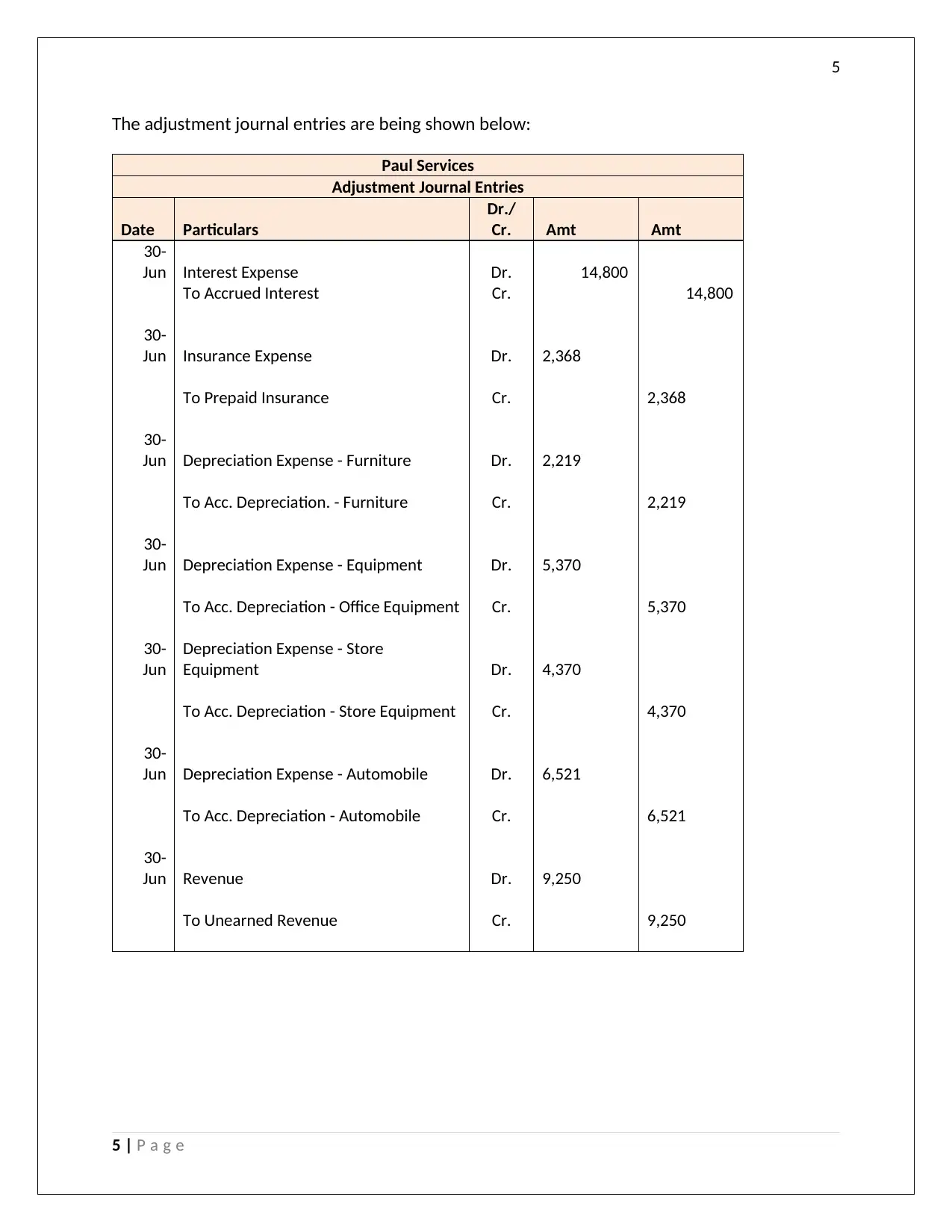

The adjustment journal entries are being shown below:

Paul Services

Adjustment Journal Entries

Date Particulars

Dr./

Cr. Amt Amt

30-

Jun Interest Expense Dr. 14,800

To Accrued Interest Cr. 14,800

30-

Jun Insurance Expense Dr. 2,368

To Prepaid Insurance Cr. 2,368

30-

Jun Depreciation Expense - Furniture Dr. 2,219

To Acc. Depreciation. - Furniture Cr. 2,219

30-

Jun Depreciation Expense - Equipment Dr. 5,370

To Acc. Depreciation - Office Equipment Cr. 5,370

30-

Jun

Depreciation Expense - Store

Equipment Dr. 4,370

To Acc. Depreciation - Store Equipment Cr. 4,370

30-

Jun Depreciation Expense - Automobile Dr. 6,521

To Acc. Depreciation - Automobile Cr. 6,521

30-

Jun Revenue Dr. 9,250

To Unearned Revenue Cr. 9,250

5 | P a g e

The adjustment journal entries are being shown below:

Paul Services

Adjustment Journal Entries

Date Particulars

Dr./

Cr. Amt Amt

30-

Jun Interest Expense Dr. 14,800

To Accrued Interest Cr. 14,800

30-

Jun Insurance Expense Dr. 2,368

To Prepaid Insurance Cr. 2,368

30-

Jun Depreciation Expense - Furniture Dr. 2,219

To Acc. Depreciation. - Furniture Cr. 2,219

30-

Jun Depreciation Expense - Equipment Dr. 5,370

To Acc. Depreciation - Office Equipment Cr. 5,370

30-

Jun

Depreciation Expense - Store

Equipment Dr. 4,370

To Acc. Depreciation - Store Equipment Cr. 4,370

30-

Jun Depreciation Expense - Automobile Dr. 6,521

To Acc. Depreciation - Automobile Cr. 6,521

30-

Jun Revenue Dr. 9,250

To Unearned Revenue Cr. 9,250

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

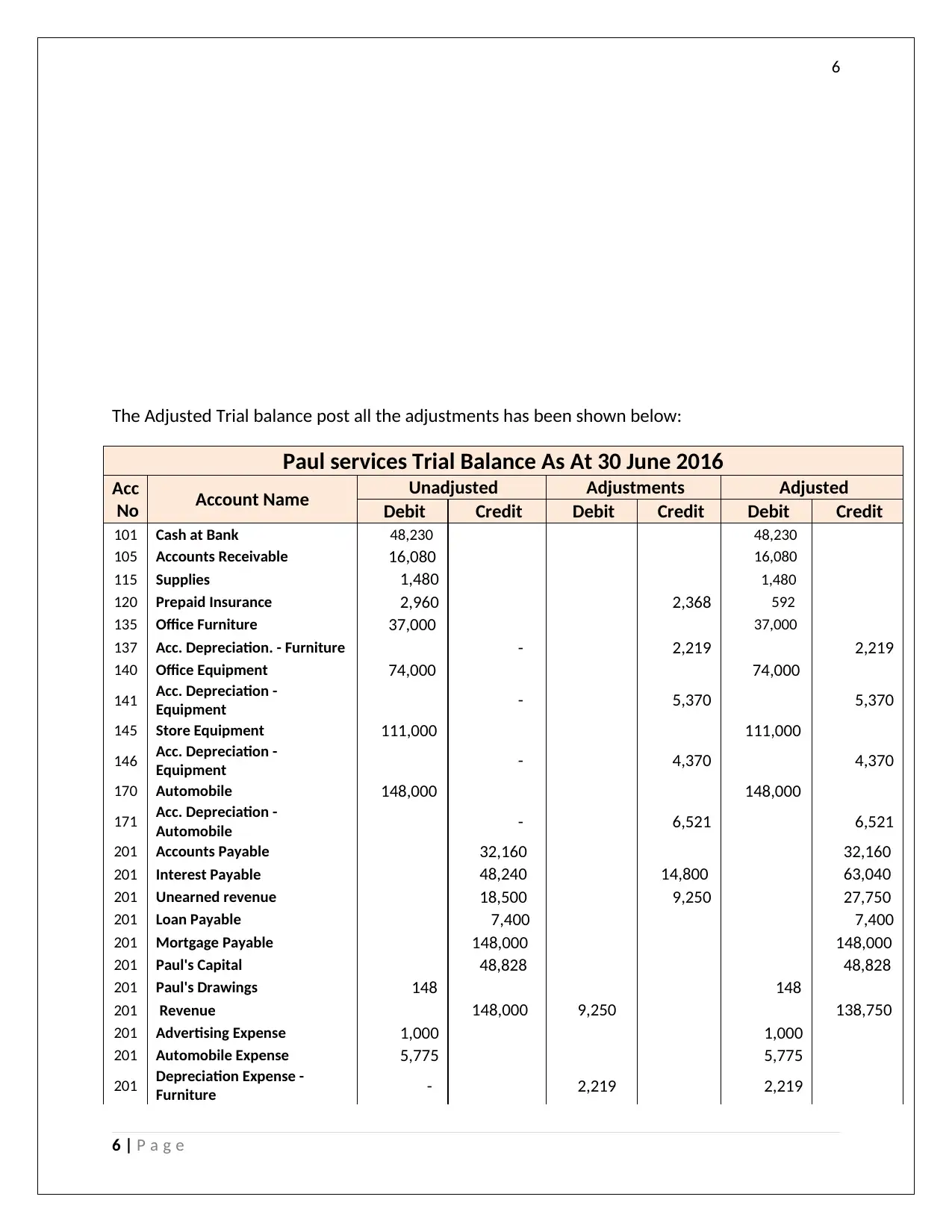

The Adjusted Trial balance post all the adjustments has been shown below:

Paul services Trial Balance As At 30 June 2016

Acc

No Account Name Unadjusted Adjustments Adjusted

Debit Credit Debit Credit Debit Credit

101 Cash at Bank 48,230 48,230

105 Accounts Receivable 16,080 16,080

115 Supplies 1,480 1,480

120 Prepaid Insurance 2,960 2,368 592

135 Office Furniture 37,000 37,000

137 Acc. Depreciation. - Furniture - 2,219 2,219

140 Office Equipment 74,000 74,000

141 Acc. Depreciation -

Equipment - 5,370 5,370

145 Store Equipment 111,000 111,000

146 Acc. Depreciation -

Equipment - 4,370 4,370

170 Automobile 148,000 148,000

171 Acc. Depreciation -

Automobile - 6,521 6,521

201 Accounts Payable 32,160 32,160

201 Interest Payable 48,240 14,800 63,040

201 Unearned revenue 18,500 9,250 27,750

201 Loan Payable 7,400 7,400

201 Mortgage Payable 148,000 148,000

201 Paul's Capital 48,828 48,828

201 Paul's Drawings 148 148

201 Revenue 148,000 9,250 138,750

201 Advertising Expense 1,000 1,000

201 Automobile Expense 5,775 5,775

201 Depreciation Expense -

Furniture - 2,219 2,219

6 | P a g e

The Adjusted Trial balance post all the adjustments has been shown below:

Paul services Trial Balance As At 30 June 2016

Acc

No Account Name Unadjusted Adjustments Adjusted

Debit Credit Debit Credit Debit Credit

101 Cash at Bank 48,230 48,230

105 Accounts Receivable 16,080 16,080

115 Supplies 1,480 1,480

120 Prepaid Insurance 2,960 2,368 592

135 Office Furniture 37,000 37,000

137 Acc. Depreciation. - Furniture - 2,219 2,219

140 Office Equipment 74,000 74,000

141 Acc. Depreciation -

Equipment - 5,370 5,370

145 Store Equipment 111,000 111,000

146 Acc. Depreciation -

Equipment - 4,370 4,370

170 Automobile 148,000 148,000

171 Acc. Depreciation -

Automobile - 6,521 6,521

201 Accounts Payable 32,160 32,160

201 Interest Payable 48,240 14,800 63,040

201 Unearned revenue 18,500 9,250 27,750

201 Loan Payable 7,400 7,400

201 Mortgage Payable 148,000 148,000

201 Paul's Capital 48,828 48,828

201 Paul's Drawings 148 148

201 Revenue 148,000 9,250 138,750

201 Advertising Expense 1,000 1,000

201 Automobile Expense 5,775 5,775

201 Depreciation Expense -

Furniture - 2,219 2,219

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

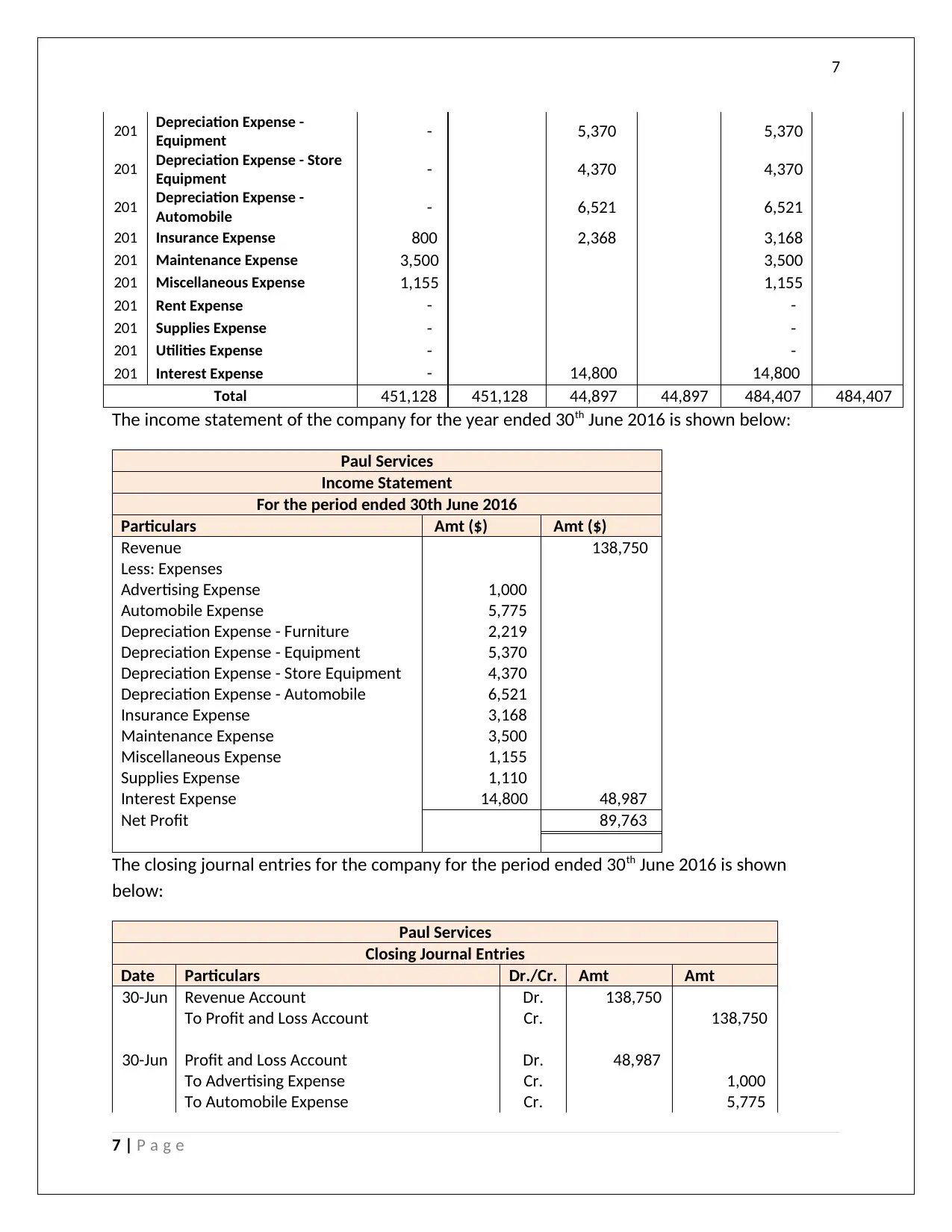

201 Depreciation Expense -

Equipment - 5,370 5,370

201 Depreciation Expense - Store

Equipment - 4,370 4,370

201 Depreciation Expense -

Automobile - 6,521 6,521

201 Insurance Expense 800 2,368 3,168

201 Maintenance Expense 3,500 3,500

201 Miscellaneous Expense 1,155 1,155

201 Rent Expense - -

201 Supplies Expense - -

201 Utilities Expense - -

201 Interest Expense - 14,800 14,800

Total 451,128 451,128 44,897 44,897 484,407 484,407

The income statement of the company for the year ended 30th June 2016 is shown below:

Paul Services

Income Statement

For the period ended 30th June 2016

Particulars Amt ($) Amt ($)

Revenue 138,750

Less: Expenses

Advertising Expense 1,000

Automobile Expense 5,775

Depreciation Expense - Furniture 2,219

Depreciation Expense - Equipment 5,370

Depreciation Expense - Store Equipment 4,370

Depreciation Expense - Automobile 6,521

Insurance Expense 3,168

Maintenance Expense 3,500

Miscellaneous Expense 1,155

Supplies Expense 1,110

Interest Expense 14,800 48,987

Net Profit 89,763

The closing journal entries for the company for the period ended 30th June 2016 is shown

below:

Paul Services

Closing Journal Entries

Date Particulars Dr./Cr. Amt Amt

30-Jun Revenue Account Dr. 138,750

To Profit and Loss Account Cr. 138,750

30-Jun Profit and Loss Account Dr. 48,987

To Advertising Expense Cr. 1,000

To Automobile Expense Cr. 5,775

7 | P a g e

201 Depreciation Expense -

Equipment - 5,370 5,370

201 Depreciation Expense - Store

Equipment - 4,370 4,370

201 Depreciation Expense -

Automobile - 6,521 6,521

201 Insurance Expense 800 2,368 3,168

201 Maintenance Expense 3,500 3,500

201 Miscellaneous Expense 1,155 1,155

201 Rent Expense - -

201 Supplies Expense - -

201 Utilities Expense - -

201 Interest Expense - 14,800 14,800

Total 451,128 451,128 44,897 44,897 484,407 484,407

The income statement of the company for the year ended 30th June 2016 is shown below:

Paul Services

Income Statement

For the period ended 30th June 2016

Particulars Amt ($) Amt ($)

Revenue 138,750

Less: Expenses

Advertising Expense 1,000

Automobile Expense 5,775

Depreciation Expense - Furniture 2,219

Depreciation Expense - Equipment 5,370

Depreciation Expense - Store Equipment 4,370

Depreciation Expense - Automobile 6,521

Insurance Expense 3,168

Maintenance Expense 3,500

Miscellaneous Expense 1,155

Supplies Expense 1,110

Interest Expense 14,800 48,987

Net Profit 89,763

The closing journal entries for the company for the period ended 30th June 2016 is shown

below:

Paul Services

Closing Journal Entries

Date Particulars Dr./Cr. Amt Amt

30-Jun Revenue Account Dr. 138,750

To Profit and Loss Account Cr. 138,750

30-Jun Profit and Loss Account Dr. 48,987

To Advertising Expense Cr. 1,000

To Automobile Expense Cr. 5,775

7 | P a g e

8

To Depreciation Expense - Furniture Cr. 2,219

To Depreciation Expense - Equipment Cr. 5,370

To Depreciation Expense - Store Equipment Cr. 4,370

To Depreciation Expense - Automobile Cr. 6,521

To Insurance Expense Cr. 3,168

To Maintenance Expense Cr. 3,500

To Miscellaneous Expense Cr. 1,155

To Supplies Expense Cr. 1,110

To Interest Expense Cr. 14,800

30-Jun Profit and Loss Account Dr. 89,763

To Retained Earnings Cr. 89,763

The balance sheet and the statement of changes in equity of the company post all the

adjustments and the profit and loss account is as follows:

Paul Services

Balance Sheet

as on 30th June 2016

Particulars Amt ($) Amt ($)

Assets -

Non-Current Assets

Office Furniture 37,000

Acc. Depreciation. - Furniture (2,219)

Office Equipment 74,000

Acc. Depreciation - Equipment (5,370)

Store Equipment 111,000

Acc. Depreciation - Equipment (4,370)

Automobile 148,000

Acc. Depreciation - Automobile (6,521) 351,521

Current Assets

Cash at Bank 48,230

Accounts Receivable 16,080

Supplies 370

Prepaid Insurance 592 65,272

Total Assets 416,793

Equity & Liabilities

Non-Current Liabilities

Loan Payable 7,400

Mortgage Payable 148,000 155,400

Current Liabilities

Accounts Payable 32,160

8 | P a g e

To Depreciation Expense - Furniture Cr. 2,219

To Depreciation Expense - Equipment Cr. 5,370

To Depreciation Expense - Store Equipment Cr. 4,370

To Depreciation Expense - Automobile Cr. 6,521

To Insurance Expense Cr. 3,168

To Maintenance Expense Cr. 3,500

To Miscellaneous Expense Cr. 1,155

To Supplies Expense Cr. 1,110

To Interest Expense Cr. 14,800

30-Jun Profit and Loss Account Dr. 89,763

To Retained Earnings Cr. 89,763

The balance sheet and the statement of changes in equity of the company post all the

adjustments and the profit and loss account is as follows:

Paul Services

Balance Sheet

as on 30th June 2016

Particulars Amt ($) Amt ($)

Assets -

Non-Current Assets

Office Furniture 37,000

Acc. Depreciation. - Furniture (2,219)

Office Equipment 74,000

Acc. Depreciation - Equipment (5,370)

Store Equipment 111,000

Acc. Depreciation - Equipment (4,370)

Automobile 148,000

Acc. Depreciation - Automobile (6,521) 351,521

Current Assets

Cash at Bank 48,230

Accounts Receivable 16,080

Supplies 370

Prepaid Insurance 592 65,272

Total Assets 416,793

Equity & Liabilities

Non-Current Liabilities

Loan Payable 7,400

Mortgage Payable 148,000 155,400

Current Liabilities

Accounts Payable 32,160

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

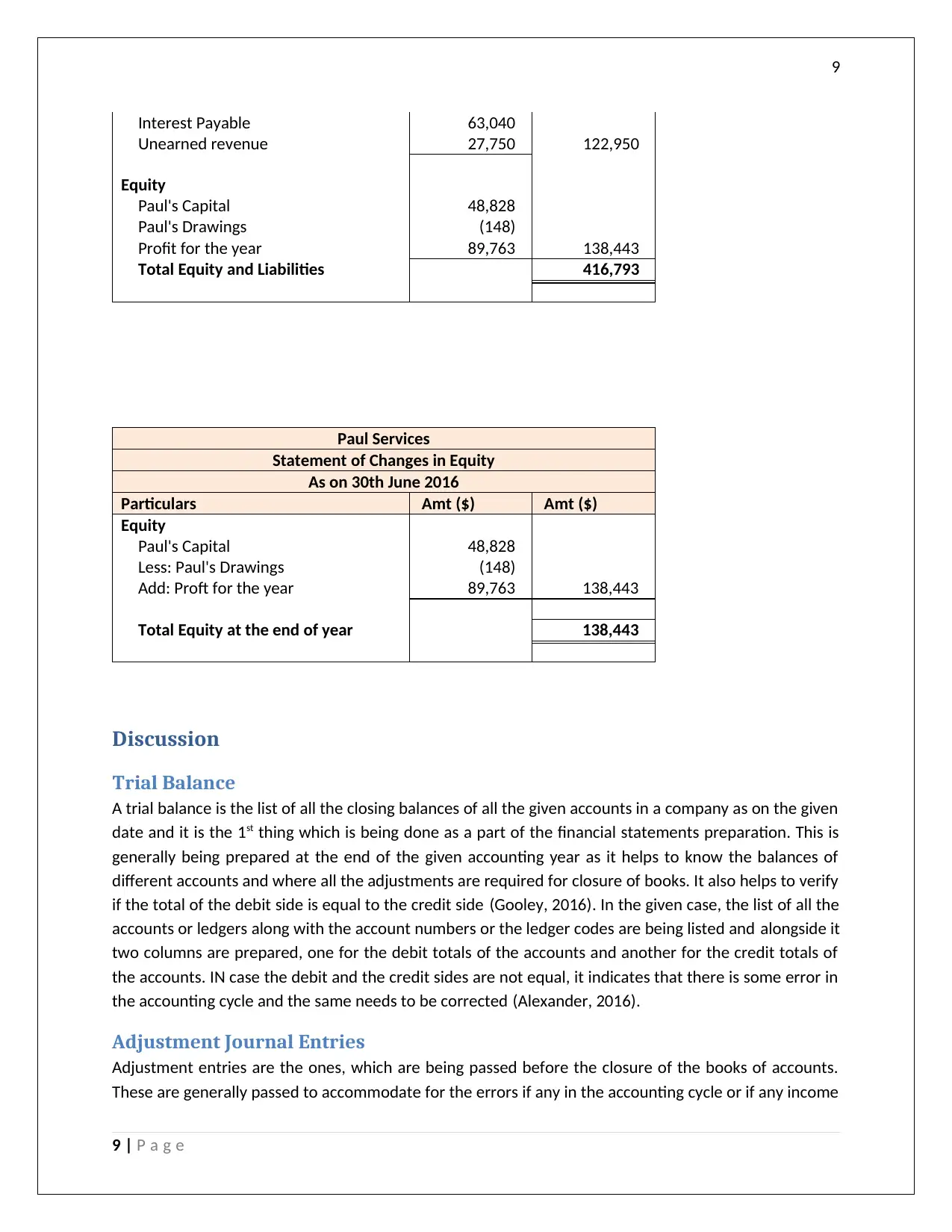

Interest Payable 63,040

Unearned revenue 27,750 122,950

Equity

Paul's Capital 48,828

Paul's Drawings (148)

Profit for the year 89,763 138,443

Total Equity and Liabilities 416,793

Paul Services

Statement of Changes in Equity

As on 30th June 2016

Particulars Amt ($) Amt ($)

Equity

Paul's Capital 48,828

Less: Paul's Drawings (148)

Add: Proft for the year 89,763 138,443

Total Equity at the end of year 138,443

Discussion

Trial Balance

A trial balance is the list of all the closing balances of all the given accounts in a company as on the given

date and it is the 1st thing which is being done as a part of the financial statements preparation. This is

generally being prepared at the end of the given accounting year as it helps to know the balances of

different accounts and where all the adjustments are required for closure of books. It also helps to verify

if the total of the debit side is equal to the credit side (Gooley, 2016). In the given case, the list of all the

accounts or ledgers along with the account numbers or the ledger codes are being listed and alongside it

two columns are prepared, one for the debit totals of the accounts and another for the credit totals of

the accounts. IN case the debit and the credit sides are not equal, it indicates that there is some error in

the accounting cycle and the same needs to be corrected (Alexander, 2016).

Adjustment Journal Entries

Adjustment entries are the ones, which are being passed before the closure of the books of accounts.

These are generally passed to accommodate for the errors if any in the accounting cycle or if any income

9 | P a g e

Interest Payable 63,040

Unearned revenue 27,750 122,950

Equity

Paul's Capital 48,828

Paul's Drawings (148)

Profit for the year 89,763 138,443

Total Equity and Liabilities 416,793

Paul Services

Statement of Changes in Equity

As on 30th June 2016

Particulars Amt ($) Amt ($)

Equity

Paul's Capital 48,828

Less: Paul's Drawings (148)

Add: Proft for the year 89,763 138,443

Total Equity at the end of year 138,443

Discussion

Trial Balance

A trial balance is the list of all the closing balances of all the given accounts in a company as on the given

date and it is the 1st thing which is being done as a part of the financial statements preparation. This is

generally being prepared at the end of the given accounting year as it helps to know the balances of

different accounts and where all the adjustments are required for closure of books. It also helps to verify

if the total of the debit side is equal to the credit side (Gooley, 2016). In the given case, the list of all the

accounts or ledgers along with the account numbers or the ledger codes are being listed and alongside it

two columns are prepared, one for the debit totals of the accounts and another for the credit totals of

the accounts. IN case the debit and the credit sides are not equal, it indicates that there is some error in

the accounting cycle and the same needs to be corrected (Alexander, 2016).

Adjustment Journal Entries

Adjustment entries are the ones, which are being passed before the closure of the books of accounts.

These are generally passed to accommodate for the errors if any in the accounting cycle or if any income

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

or expenses pertaining to the particular period has not been recognized in the books. There are many

such transactions, which start in the given accounting period but may end in the later period. For

properly accounting the same, an adjusting journal entry is required in the books such the financial

reporting is being correctly at the year-end (Heminway, 2017). The other purpose of recording the

adjustment entries is to convert the real time entries in to the accrual system. Suppose in the given case,

the depreciation entries on all the assets (furniture, office equipment, store equipment, etc.) was not

being passed initially and hence the same was included as a part of the adjustment entries.

Furthermore, there was prepaid insurance, which was being paid for future periods initially during the

year. The same had to be adjusted towards the year-end to account for the expenses for the current

period. Most of the adjusting journal entries relate to the concept of prepaid, accrual, outstanding,

unearned expenses and incomes respectively (Bromwich & Scapens, 2016). It is done to ensure the

matching and accrual principles of accounting.

Adjusted Trial balance

Adjusted trial balance is the pre-requisite for preparation of the financial statements. It is the

consolidated list of all the account titles or ledgers along with the respective debit and credit balances. It

is prepared after taking into account the effect of the adjustment journal entries in the books (Fay &

Negangard, 2017). The adjusted trial balance is for the use of preparation of the final financial

statement, is an internal document, and is not to be reported in the annual report of the company. One

more use of preparation of the adjusted trial balance is it helps in the preparation of the all the financial

statements income the income statement or the profit and loss account, the balance sheet of the

company and the statement of changes in the equity (Linden & Freeman, 2017).

Closing Journal Entries

Closing journal entries are much different from the adjustment journal entries. The closing journal

entries are being prepared at the end of the period to set or to transfer the balances of all the

temporary accounts to the permanent accounts and make them zero. This process is commonly referred

to as the closing of the books of accounts (Trieu, 2017). Temporary accounts are the accounts, which

form part of the income statement of the company, which usually shows the results of the accounting

activity over the year. Some examples of temporary accounts is revenue, other incomes, expenses, Cost

of goods sold, taxes, interest, depreciation, etc. On the other hand, permanent accounts are the balance

sheet accounts, which last more than an accounting period, and hence the same needs to be carried

forward. Few examples of the permanent account includes asset account, land, building, furniture,

equipment, cash, debtors, inventory, liabilities like current and non-current liabilities account, creditors,

payables, bank loan, equity reserves, etc. (Choy, 2018).

10 | P a g e

or expenses pertaining to the particular period has not been recognized in the books. There are many

such transactions, which start in the given accounting period but may end in the later period. For

properly accounting the same, an adjusting journal entry is required in the books such the financial

reporting is being correctly at the year-end (Heminway, 2017). The other purpose of recording the

adjustment entries is to convert the real time entries in to the accrual system. Suppose in the given case,

the depreciation entries on all the assets (furniture, office equipment, store equipment, etc.) was not

being passed initially and hence the same was included as a part of the adjustment entries.

Furthermore, there was prepaid insurance, which was being paid for future periods initially during the

year. The same had to be adjusted towards the year-end to account for the expenses for the current

period. Most of the adjusting journal entries relate to the concept of prepaid, accrual, outstanding,

unearned expenses and incomes respectively (Bromwich & Scapens, 2016). It is done to ensure the

matching and accrual principles of accounting.

Adjusted Trial balance

Adjusted trial balance is the pre-requisite for preparation of the financial statements. It is the

consolidated list of all the account titles or ledgers along with the respective debit and credit balances. It

is prepared after taking into account the effect of the adjustment journal entries in the books (Fay &

Negangard, 2017). The adjusted trial balance is for the use of preparation of the final financial

statement, is an internal document, and is not to be reported in the annual report of the company. One

more use of preparation of the adjusted trial balance is it helps in the preparation of the all the financial

statements income the income statement or the profit and loss account, the balance sheet of the

company and the statement of changes in the equity (Linden & Freeman, 2017).

Closing Journal Entries

Closing journal entries are much different from the adjustment journal entries. The closing journal

entries are being prepared at the end of the period to set or to transfer the balances of all the

temporary accounts to the permanent accounts and make them zero. This process is commonly referred

to as the closing of the books of accounts (Trieu, 2017). Temporary accounts are the accounts, which

form part of the income statement of the company, which usually shows the results of the accounting

activity over the year. Some examples of temporary accounts is revenue, other incomes, expenses, Cost

of goods sold, taxes, interest, depreciation, etc. On the other hand, permanent accounts are the balance

sheet accounts, which last more than an accounting period, and hence the same needs to be carried

forward. Few examples of the permanent account includes asset account, land, building, furniture,

equipment, cash, debtors, inventory, liabilities like current and non-current liabilities account, creditors,

payables, bank loan, equity reserves, etc. (Choy, 2018).

10 | P a g e

11

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, Volume 31, pp. 1-9.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Dumay, J. & Baard, V., 2017. An introduction to interventionist research in accounting.. The Routledge

Companion to Qualitative Accounting Research Methods, p. 265.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Gooley, J., 2016. Principles of Australian Contract Law. Australia: Lexis Nexis.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, Volume 93, pp. 111-124.

11 | P a g e

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, Volume 31, pp. 1-9.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Dumay, J. & Baard, V., 2017. An introduction to interventionist research in accounting.. The Routledge

Companion to Qualitative Accounting Research Methods, p. 265.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Gooley, J., 2016. Principles of Australian Contract Law. Australia: Lexis Nexis.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, Volume 93, pp. 111-124.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.