Comprehensive Report on Management Accounting in Business Operations

VerifiedAdded on 2020/10/05

|19

|6061

|158

Report

AI Summary

This report provides a comprehensive overview of management accounting, covering its fundamentals, types, and applications in a business environment. It delves into the importance of management accounting for managerial decisions, differentiating it from financial accounting and exploring various systems like cost accounting, inventory management, job costing, and price optimization. The report also examines different methods of management accounting reporting, including cost reports, budget reports, and performance reports, highlighting their roles in financial analysis and decision-making. Furthermore, it discusses the implications of suitable costing methods, such as marginal costing and absorption costing, for preparing income statements. The report includes an analysis of planning tools used for budgetary control, a SWOT analysis of a company, and a discussion on benchmarks, key performance indicators, and variance analysis, providing valuable insights into financial and non-financial aspects of business operations.

Business accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

P1 Management accounting, its requirement and its types.........................................................1

P2 Methods for management accounting reporting...................................................................3

P3 Implication of suitable costing method for preparing income statement...............................5

P4 Merits and demerits of planning tools used for budgetary control........................................8

SWOT analysis of Tech UK Ltd....................................................................................................13

P5 Benchmarks, key performance indicators (financial and non financial) and variance

analysis......................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

P1 Management accounting, its requirement and its types.........................................................1

P2 Methods for management accounting reporting...................................................................3

P3 Implication of suitable costing method for preparing income statement...............................5

P4 Merits and demerits of planning tools used for budgetary control........................................8

SWOT analysis of Tech UK Ltd....................................................................................................13

P5 Benchmarks, key performance indicators (financial and non financial) and variance

analysis......................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

The main objective of this report is to give some light on fundamentals of management

accounting which is applied to the business environment and in addition to this, organizations

which are operating in that environment. Management accounting is applied to financial data for

assisting in monitoring, planning, decisions and managing of finance along with the company.

This report will also give a brief understanding of management accounting systems with its

proper explanation and its significance and combination with organisation is briefed. The role,

origin and principles of management accounting are very essential. Though management

accounting and financial accounting sound similar but there are major differences which are

explained below. The different types of management accounting system are cost accounting

system, inventory management systems, job costing system and price optimising system.

Planning tools which are used in management accounting system are briefed and ways in which

company must use management accounting to respond the financial problems.

P1 Management accounting, its requirement and its types.

Management accounting is playing vital role for managerial decisions. It helps in

providing and preparing financial and statistical information to all business managers who take

managerial decisions i.e. short term or day to day decisions (Lee and et.al., 2011). It is the

process of identifying, measuring, analysing, interpreting and delivering financial information in

the context of organisation's goals which can be also referred as cost accounting. Financial

accounting and management accounting sounds similar but actually they are not, there main

difference is that information related to management accounting objective is for assisting

managers in the company while taking decisions and on the contrary side target for financial

accounting refers to information which is offers to external parties of company. While preparing

management accounts and reports which offer particular, timely and accurate financial and

statistical information which is required by managers for establishing day to day and short term

decisions. The reports which are prepared to accomplish requirements of management is also

considered in it.

All the confidential information of management accounting is used for internal purpose

only which is unique from financial accounting systems i.e. publicly reported (Davies and

Crawford, 2011). These informations are calculated on the basis of management's informational

need instead of generally accepted accounting practices. The basic principle of management

1

The main objective of this report is to give some light on fundamentals of management

accounting which is applied to the business environment and in addition to this, organizations

which are operating in that environment. Management accounting is applied to financial data for

assisting in monitoring, planning, decisions and managing of finance along with the company.

This report will also give a brief understanding of management accounting systems with its

proper explanation and its significance and combination with organisation is briefed. The role,

origin and principles of management accounting are very essential. Though management

accounting and financial accounting sound similar but there are major differences which are

explained below. The different types of management accounting system are cost accounting

system, inventory management systems, job costing system and price optimising system.

Planning tools which are used in management accounting system are briefed and ways in which

company must use management accounting to respond the financial problems.

P1 Management accounting, its requirement and its types.

Management accounting is playing vital role for managerial decisions. It helps in

providing and preparing financial and statistical information to all business managers who take

managerial decisions i.e. short term or day to day decisions (Lee and et.al., 2011). It is the

process of identifying, measuring, analysing, interpreting and delivering financial information in

the context of organisation's goals which can be also referred as cost accounting. Financial

accounting and management accounting sounds similar but actually they are not, there main

difference is that information related to management accounting objective is for assisting

managers in the company while taking decisions and on the contrary side target for financial

accounting refers to information which is offers to external parties of company. While preparing

management accounts and reports which offer particular, timely and accurate financial and

statistical information which is required by managers for establishing day to day and short term

decisions. The reports which are prepared to accomplish requirements of management is also

considered in it.

All the confidential information of management accounting is used for internal purpose

only which is unique from financial accounting systems i.e. publicly reported (Davies and

Crawford, 2011). These informations are calculated on the basis of management's informational

need instead of generally accepted accounting practices. The basic principle of management

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting can be implementation of developing decision making companies and it also consists

of influence, relevance, value and trust. Influence in perspective of communication which gives

insight. Information should be relevant, value which has been impacted should be analysed

properly and trust is build by stewardship. Accounting can be referred as process of identifying,

measuring and communicating or elaborating the economic data for allowing informed decisions

and users of data who take the judgement as per American Accounting Association. The

application of managerial accounting always varies from other as every system is customised for

giving various managerial information which is required by management for decision making.

There are many types of management accounting systems such as cost accounting

system, price optimisation, job costing system and inventory management. Each and every

method has their own objectives, function and elements. The basic elements of accounting

system provides standardized context as the main objective for the data is to be analysed,

communicated and identified properly. Explanation of these types is as follows:

Cost accounting system: Costing system is the basic framework which has been applied

by corporation for identifying approximate cost of its products for valuation of inventory. Cost

control and profitability analysis. In this type allocation of cost is according to traditional costing

system or activity based costing. The approximation for actual products cost is important for

effective and efficient functions (Wu, 2012). The main objective of this system is to capture the

production cost of corporations along with weighing input costs of each and every production

step and in addition to it some fixed cost such as capital equipment depreciation. It will

individually record and measure costs and then actual comparison of outcome from input to the

actual results or output which assists the company's management for measuring financial

performance. Usually the business mangers depends on accounting data in general and

specifically on cost as any of the company's task should be elaborated with its cost. It is the key

concept of management accounting because it provides specific analytical tools such as marginal

costing, budgetary control, operating cost, standard costing and inventory control which has been

applied from the management perspective in replacing their reproducibility efficiently.

Inventory management: This method refers to controlling and keeping track on

ordering, application and storage of the component which the organisation is applying for the

production of goods which has been sold by them. While managing the inventory system it

combines the usage of desktop software, barcode scanners, barcode printers and mobile devices

2

of influence, relevance, value and trust. Influence in perspective of communication which gives

insight. Information should be relevant, value which has been impacted should be analysed

properly and trust is build by stewardship. Accounting can be referred as process of identifying,

measuring and communicating or elaborating the economic data for allowing informed decisions

and users of data who take the judgement as per American Accounting Association. The

application of managerial accounting always varies from other as every system is customised for

giving various managerial information which is required by management for decision making.

There are many types of management accounting systems such as cost accounting

system, price optimisation, job costing system and inventory management. Each and every

method has their own objectives, function and elements. The basic elements of accounting

system provides standardized context as the main objective for the data is to be analysed,

communicated and identified properly. Explanation of these types is as follows:

Cost accounting system: Costing system is the basic framework which has been applied

by corporation for identifying approximate cost of its products for valuation of inventory. Cost

control and profitability analysis. In this type allocation of cost is according to traditional costing

system or activity based costing. The approximation for actual products cost is important for

effective and efficient functions (Wu, 2012). The main objective of this system is to capture the

production cost of corporations along with weighing input costs of each and every production

step and in addition to it some fixed cost such as capital equipment depreciation. It will

individually record and measure costs and then actual comparison of outcome from input to the

actual results or output which assists the company's management for measuring financial

performance. Usually the business mangers depends on accounting data in general and

specifically on cost as any of the company's task should be elaborated with its cost. It is the key

concept of management accounting because it provides specific analytical tools such as marginal

costing, budgetary control, operating cost, standard costing and inventory control which has been

applied from the management perspective in replacing their reproducibility efficiently.

Inventory management: This method refers to controlling and keeping track on

ordering, application and storage of the component which the organisation is applying for the

production of goods which has been sold by them. While managing the inventory system it

combines the usage of desktop software, barcode scanners, barcode printers and mobile devices

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for the streamline of managing inventory such as goods, stock, supplies and consumables. All

finished goods for sale are also been tracked in this method. The main objective is to understand

the present level of inventory and to control or minimise under stock and overstock situations. If

there is efficient tracking, then managers have capability of drawing sufficient inventory

decisions. Inventories represent key assets and accounts for investment which are tied to the

products which are sold.

The main function of inventory management constitutes creation of purchasing orders,

relocating, adjusting, disposing and receiving the inventory. It creates the sales order, packaging,

shipping and picking of the products even the cycle counts and physical counts of inventory has

been performed. The main benefits which represent inventory management system of

organisation are enhancing accuracy of inventory, company's workflow has been improved and

bottom line of company is also improved in same series.

Job costing system: It allocates the manufacturing costs to specific batch or individual

item of the products. This method is usually applied when goods are been processed from one

another. Usually practice of accumulation of data related to cost of particular service or any job

related to production. This information is required for submitting cost data to a consumer who is

in contract where cost is refunded and it is necessary for determining accuracy and estimating

system of the company which is capable for quoting prices. This method combines three types of

direct information labour, overhead and direct material.

Price optimisation systems: It is basic method for the application of mathematical

analysis of the XYZ co. for determining the reactions of consumers for various prices for

services and goods through different channels. Essentially it is used for identifying prices which

XYZ co. shall accomplish goals like increasing the operating profit. An alternative should be

discovered through highest achievable cost or performance which is effective under various

barriers via increasing the desired aspects and vice versa (Siverbo, 2014).

P2 Methods for management accounting reporting

The focus of management accounting is on information which is received internally

through financial accounting. It is essentially applied for controlling, planning and decision

making. Financial statements such as balance sheet, income statement and cash flow statement

gives dependency to the managerial accountants. There are much other information which has

3

finished goods for sale are also been tracked in this method. The main objective is to understand

the present level of inventory and to control or minimise under stock and overstock situations. If

there is efficient tracking, then managers have capability of drawing sufficient inventory

decisions. Inventories represent key assets and accounts for investment which are tied to the

products which are sold.

The main function of inventory management constitutes creation of purchasing orders,

relocating, adjusting, disposing and receiving the inventory. It creates the sales order, packaging,

shipping and picking of the products even the cycle counts and physical counts of inventory has

been performed. The main benefits which represent inventory management system of

organisation are enhancing accuracy of inventory, company's workflow has been improved and

bottom line of company is also improved in same series.

Job costing system: It allocates the manufacturing costs to specific batch or individual

item of the products. This method is usually applied when goods are been processed from one

another. Usually practice of accumulation of data related to cost of particular service or any job

related to production. This information is required for submitting cost data to a consumer who is

in contract where cost is refunded and it is necessary for determining accuracy and estimating

system of the company which is capable for quoting prices. This method combines three types of

direct information labour, overhead and direct material.

Price optimisation systems: It is basic method for the application of mathematical

analysis of the XYZ co. for determining the reactions of consumers for various prices for

services and goods through different channels. Essentially it is used for identifying prices which

XYZ co. shall accomplish goals like increasing the operating profit. An alternative should be

discovered through highest achievable cost or performance which is effective under various

barriers via increasing the desired aspects and vice versa (Siverbo, 2014).

P2 Methods for management accounting reporting

The focus of management accounting is on information which is received internally

through financial accounting. It is essentially applied for controlling, planning and decision

making. Financial statements such as balance sheet, income statement and cash flow statement

gives dependency to the managerial accountants. There are much other information which has

3

been considered by them for evaluating the financial performance of the organisation. This

information consists of budget cost, reports such as product and performance reports.

Cost reports: Management accounting gives calculation of cost of items which are

manufactured. It has been calculated by considering all raw production overhead, costs, labour

and in addition to this extra cost consideration. The aggregate is divided into the amounts of

goods which are produced. It gives the whole summary of all the information related to the XYZ

co. or business. It gives the capacity of mangers for realizing the cost prices of some specific

items as compared to selling prices. The estimation of profit margin and its monitoring is also

been done through cost managerial accounting report. With the help of cost report, there is clear

picture drawn of expenses which is important for proper utilization of resources along with each

and every department. It gives light on specific expenses which are related to specific projects.

Generally they are matched with revenue estimation so XYZ co. can evaluate the profitability

which also leads for higher earning areas of business so special focus will be given on their own

efforts instead to spoiling time and resources on jobs which give less profit margins. Cost reports

helps the manger for planning and managing income limits.

Budget report: The budget report is the most fundamental report in managerial

accounting. It is very critical for measuring the performance of the organisation and to generate

as small business and segregate in department wise for big companies. As each and every

company draws overall budget for the proper understanding of popular schemes related to the

business. The special element of budget accounting is represented as preparation of budget.

Usually budgets are prepared on the basis of previous year budgets and to adjusts them for the

future forecasts by the circumstances which might arise. The budget of the XYZ co. gives all

sources of revenues and expenses. The XYZ co. put all its efforts to stay on budget or to

accomplish the goal to stay in budgeted amount. The manager always prefer new vendor for raw

material in context of saving money and resources along with this they also keep track of

increasing sales and expenses should be reduced in same series. It guides the managers for giving

employee incentives, reduce or cut costs and to renegotiate with the context of raw materials

from suppliers and vendors(Knežević, Rakočević and Đurić, 2011). Budget report is very

explanatory to any of the business or industry.

Performance report: Performance report is formed for reviewing performance of the

XYZ co.s as a whole or even of every employee at the end. In big XYZ co.s, departmental

4

information consists of budget cost, reports such as product and performance reports.

Cost reports: Management accounting gives calculation of cost of items which are

manufactured. It has been calculated by considering all raw production overhead, costs, labour

and in addition to this extra cost consideration. The aggregate is divided into the amounts of

goods which are produced. It gives the whole summary of all the information related to the XYZ

co. or business. It gives the capacity of mangers for realizing the cost prices of some specific

items as compared to selling prices. The estimation of profit margin and its monitoring is also

been done through cost managerial accounting report. With the help of cost report, there is clear

picture drawn of expenses which is important for proper utilization of resources along with each

and every department. It gives light on specific expenses which are related to specific projects.

Generally they are matched with revenue estimation so XYZ co. can evaluate the profitability

which also leads for higher earning areas of business so special focus will be given on their own

efforts instead to spoiling time and resources on jobs which give less profit margins. Cost reports

helps the manger for planning and managing income limits.

Budget report: The budget report is the most fundamental report in managerial

accounting. It is very critical for measuring the performance of the organisation and to generate

as small business and segregate in department wise for big companies. As each and every

company draws overall budget for the proper understanding of popular schemes related to the

business. The special element of budget accounting is represented as preparation of budget.

Usually budgets are prepared on the basis of previous year budgets and to adjusts them for the

future forecasts by the circumstances which might arise. The budget of the XYZ co. gives all

sources of revenues and expenses. The XYZ co. put all its efforts to stay on budget or to

accomplish the goal to stay in budgeted amount. The manager always prefer new vendor for raw

material in context of saving money and resources along with this they also keep track of

increasing sales and expenses should be reduced in same series. It guides the managers for giving

employee incentives, reduce or cut costs and to renegotiate with the context of raw materials

from suppliers and vendors(Knežević, Rakočević and Đurić, 2011). Budget report is very

explanatory to any of the business or industry.

Performance report: Performance report is formed for reviewing performance of the

XYZ co.s as a whole or even of every employee at the end. In big XYZ co.s, departmental

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance report is also generated. These reports are used by mangers for taking strategic

decision about the future of the company. Many individuals are rewarded on the basis of

commitment towards the company and even there is laid off of under performers or dealt if there

is requirement. The managerial accounting related to performance leads to deep insight into

operations of organisation. If setup has not been giving the expected results then performance

report will help in pointing towards the flaws in setup. The accountants usually apply budgets for

giving the comparison of actual revenues and expenditures from the amount which has been

budgeted. While shaping or creating new budgets the variations are been computed and

evaluated properly and all necessary information in the context of amounts which has been listed

on performance report. Each and every year these reports are formed but some organisations

quantify there financial performance by preparing performance report quarterly or even monthly.

These reports helps in assisting managers for prediction of future demands where production and

cost increases. For every company, performance report plays an important role for tracking a

perfect measure of their strategy towards their objective and mission.

P3 Implication of suitable costing method for preparing income statement

To identify the adequate costing techniques which in turn helps in improving the business

operations can be based on the most suitable and efficient analysis over firm's financials.

However, there are two techniques which will be indicative and accurate to the managerial

professionals of the firm to be application and use of measuring the expenses and revenue of the

firm during the period.

Marginal costing methods:

This technique comprises with the method of measuring the costs incurred in the

operations. It consists with treating the costs of an article as variable. In addition, there will be

consideration of various cots which usually incurred in the production such as direct material,

expenses, labours etc. which is treated and measured in analysing the costs of overall expenses

incurred in business operations. Therefore, such analysed costs and expenses will bring

information relevant with the profitability of the firm. Similarly, in relation with such outcomes

the managers will make effective decisions which in turn makes control over expenses of

business. Here the contribution per unit is constant as per profit per units which differs from the

volume of sales. It comprises with no variations with the under and over absorption of

5

decision about the future of the company. Many individuals are rewarded on the basis of

commitment towards the company and even there is laid off of under performers or dealt if there

is requirement. The managerial accounting related to performance leads to deep insight into

operations of organisation. If setup has not been giving the expected results then performance

report will help in pointing towards the flaws in setup. The accountants usually apply budgets for

giving the comparison of actual revenues and expenditures from the amount which has been

budgeted. While shaping or creating new budgets the variations are been computed and

evaluated properly and all necessary information in the context of amounts which has been listed

on performance report. Each and every year these reports are formed but some organisations

quantify there financial performance by preparing performance report quarterly or even monthly.

These reports helps in assisting managers for prediction of future demands where production and

cost increases. For every company, performance report plays an important role for tracking a

perfect measure of their strategy towards their objective and mission.

P3 Implication of suitable costing method for preparing income statement

To identify the adequate costing techniques which in turn helps in improving the business

operations can be based on the most suitable and efficient analysis over firm's financials.

However, there are two techniques which will be indicative and accurate to the managerial

professionals of the firm to be application and use of measuring the expenses and revenue of the

firm during the period.

Marginal costing methods:

This technique comprises with the method of measuring the costs incurred in the

operations. It consists with treating the costs of an article as variable. In addition, there will be

consideration of various cots which usually incurred in the production such as direct material,

expenses, labours etc. which is treated and measured in analysing the costs of overall expenses

incurred in business operations. Therefore, such analysed costs and expenses will bring

information relevant with the profitability of the firm. Similarly, in relation with such outcomes

the managers will make effective decisions which in turn makes control over expenses of

business. Here the contribution per unit is constant as per profit per units which differs from the

volume of sales. It comprises with no variations with the under and over absorption of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overheads. The fixed costs of the organisation which will have varies due to changes in the

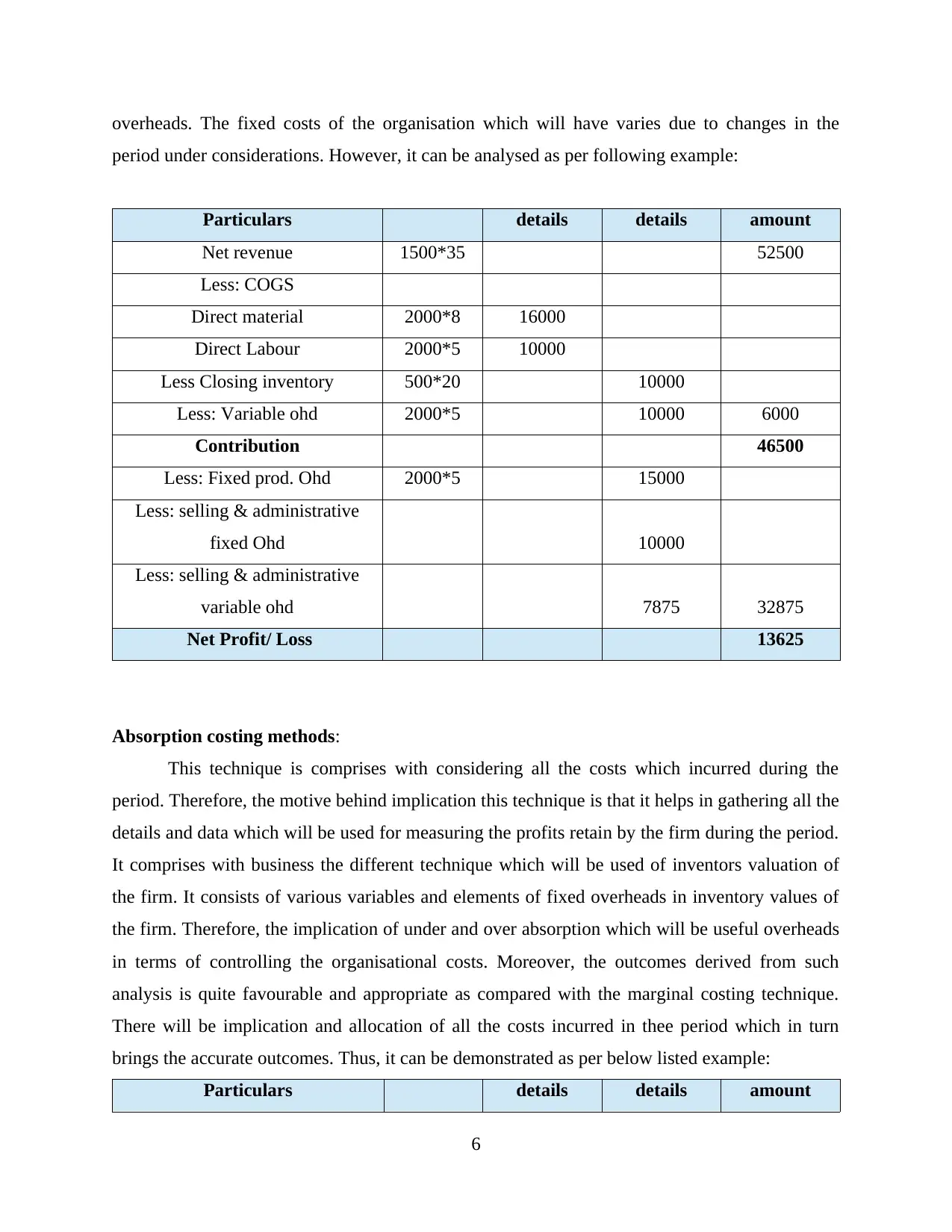

period under considerations. However, it can be analysed as per following example:

Particulars details details amount

Net revenue 1500*35 52500

Less: COGS

Direct material 2000*8 16000

Direct Labour 2000*5 10000

Less Closing inventory 500*20 10000

Less: Variable ohd 2000*5 10000 6000

Contribution 46500

Less: Fixed prod. Ohd 2000*5 15000

Less: selling & administrative

fixed Ohd 10000

Less: selling & administrative

variable ohd 7875 32875

Net Profit/ Loss 13625

Absorption costing methods:

This technique is comprises with considering all the costs which incurred during the

period. Therefore, the motive behind implication this technique is that it helps in gathering all the

details and data which will be used for measuring the profits retain by the firm during the period.

It comprises with business the different technique which will be used of inventors valuation of

the firm. It consists of various variables and elements of fixed overheads in inventory values of

the firm. Therefore, the implication of under and over absorption which will be useful overheads

in terms of controlling the organisational costs. Moreover, the outcomes derived from such

analysis is quite favourable and appropriate as compared with the marginal costing technique.

There will be implication and allocation of all the costs incurred in thee period which in turn

brings the accurate outcomes. Thus, it can be demonstrated as per below listed example:

Particulars details details amount

6

period under considerations. However, it can be analysed as per following example:

Particulars details details amount

Net revenue 1500*35 52500

Less: COGS

Direct material 2000*8 16000

Direct Labour 2000*5 10000

Less Closing inventory 500*20 10000

Less: Variable ohd 2000*5 10000 6000

Contribution 46500

Less: Fixed prod. Ohd 2000*5 15000

Less: selling & administrative

fixed Ohd 10000

Less: selling & administrative

variable ohd 7875 32875

Net Profit/ Loss 13625

Absorption costing methods:

This technique is comprises with considering all the costs which incurred during the

period. Therefore, the motive behind implication this technique is that it helps in gathering all the

details and data which will be used for measuring the profits retain by the firm during the period.

It comprises with business the different technique which will be used of inventors valuation of

the firm. It consists of various variables and elements of fixed overheads in inventory values of

the firm. Therefore, the implication of under and over absorption which will be useful overheads

in terms of controlling the organisational costs. Moreover, the outcomes derived from such

analysis is quite favourable and appropriate as compared with the marginal costing technique.

There will be implication and allocation of all the costs incurred in thee period which in turn

brings the accurate outcomes. Thus, it can be demonstrated as per below listed example:

Particulars details details amount

6

Net revenue 1500*35 52500

Less: COGS

Direct material 2000*8 16000

Direct Labour 2000*5 10000 26000

Fixed Production ohd 15000

cost of production 11000

Closing inventory 500*20 10000 1000

Gross Profit 53500

Less: Variable ohd 2000*5 10000

Less: Fixed production ohd 2000*5 10000

Less: selling & administrative

fixed ohd 10000

Less: selling & administrative

variable ohd 7875 37875

Net profit 15625

Presenting reporting techniques comprised with application of management accounting

methods

The implication of various managements accounting techniques which in context with

analyse the financial condition of the entity as well as enables the managerial professionals to

make the productive efforts. Moreover, there will be improvements in the operational activities

of the business which in turn will have positive impacts over the revenue and operational

efficiency. Moreover, there is need to have adequate implication of various management

accounting techniques which in turn helps in balancing the operational performance of the firm.

To have records of all transactions and operational variations in the business which in turn will

make changes into business operations. Thus, it comprises with various reporting techniques

which will be fruitful for the business operations such as:

Cost- Volume profit: It comprises with the changes in the company's costs and volume

of production during the period. It will be measured through operating income and net income of

the firm. Therefore, in relation with analysing the outcomes there will be consideration of

7

Less: COGS

Direct material 2000*8 16000

Direct Labour 2000*5 10000 26000

Fixed Production ohd 15000

cost of production 11000

Closing inventory 500*20 10000 1000

Gross Profit 53500

Less: Variable ohd 2000*5 10000

Less: Fixed production ohd 2000*5 10000

Less: selling & administrative

fixed ohd 10000

Less: selling & administrative

variable ohd 7875 37875

Net profit 15625

Presenting reporting techniques comprised with application of management accounting

methods

The implication of various managements accounting techniques which in context with

analyse the financial condition of the entity as well as enables the managerial professionals to

make the productive efforts. Moreover, there will be improvements in the operational activities

of the business which in turn will have positive impacts over the revenue and operational

efficiency. Moreover, there is need to have adequate implication of various management

accounting techniques which in turn helps in balancing the operational performance of the firm.

To have records of all transactions and operational variations in the business which in turn will

make changes into business operations. Thus, it comprises with various reporting techniques

which will be fruitful for the business operations such as:

Cost- Volume profit: It comprises with the changes in the company's costs and volume

of production during the period. It will be measured through operating income and net income of

the firm. Therefore, in relation with analysing the outcomes there will be consideration of

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

various elements on which the sale price per unit will remain constant (Bushman and Smith,

2001).

Flexible budgeting: It can be understand as per the nature of this budgeting technique.

Thus, these are flexible and variable budgets which determines the changes into the costs as per

the level of requirements in the activities.

Cost variance: Implication of this technique in analysing the actual costs and the

budgeted costs for the operations which in context with making the appropriate improvements in

the operational activities of the business. Therefore, remaining variance amount will be used in

forwards planning of the organisation. Thus, it ensures the proper utilisation of funds in each

units.

Product costing: To analyse the costs such as direct, indirect, fixed and variable in the

production activities which will be beneficial to the firm as to have the appropriate utilisation of

the resources. Thus, it gives suitable outcomes to the managerial professionals in relation with

adequate and perfect decision making.

Cost of inventories: The carrying costs of the inventory as well as ordering costs will be

measured through various techniques such as economic order quantity, just in time FIFO, LIFO

etc. which in context with improving the operational efficiencies of organisation.

P4 Merits and demerits of planning tools used for budgetary control

Various planning tools used for budgetary control are:

Incremental budgeting

Activity based budgeting

Zero based budgeting

Incremental budgeting: It is an essential part of management accounting which is

specifically on the basis of making small change from previous budget to new budget. All the

amount which has been increased is arrived at numbers which are newly budgeted. Budget of

current fiscal year has become the base of coming year for the allocation of budgetary. There is

an assumption made by management that all the operations at current level of expenses will

continue in the next year and even there will be some additional amount will be added (Ayvaz

and Pehlivanl, 2011). And this assumption has become as approach of incremental budgeting.

Merits and demerits are as follows:

8

2001).

Flexible budgeting: It can be understand as per the nature of this budgeting technique.

Thus, these are flexible and variable budgets which determines the changes into the costs as per

the level of requirements in the activities.

Cost variance: Implication of this technique in analysing the actual costs and the

budgeted costs for the operations which in context with making the appropriate improvements in

the operational activities of the business. Therefore, remaining variance amount will be used in

forwards planning of the organisation. Thus, it ensures the proper utilisation of funds in each

units.

Product costing: To analyse the costs such as direct, indirect, fixed and variable in the

production activities which will be beneficial to the firm as to have the appropriate utilisation of

the resources. Thus, it gives suitable outcomes to the managerial professionals in relation with

adequate and perfect decision making.

Cost of inventories: The carrying costs of the inventory as well as ordering costs will be

measured through various techniques such as economic order quantity, just in time FIFO, LIFO

etc. which in context with improving the operational efficiencies of organisation.

P4 Merits and demerits of planning tools used for budgetary control

Various planning tools used for budgetary control are:

Incremental budgeting

Activity based budgeting

Zero based budgeting

Incremental budgeting: It is an essential part of management accounting which is

specifically on the basis of making small change from previous budget to new budget. All the

amount which has been increased is arrived at numbers which are newly budgeted. Budget of

current fiscal year has become the base of coming year for the allocation of budgetary. There is

an assumption made by management that all the operations at current level of expenses will

continue in the next year and even there will be some additional amount will be added (Ayvaz

and Pehlivanl, 2011). And this assumption has become as approach of incremental budgeting.

Merits and demerits are as follows:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Merits

Incremental budget's implementation is very easy and it does not have any complexity in

calculations as it can be obtained from different departments in the absence of any issue

because there is no need of any detailed analysis.

There is no need of any detailed analysis of requirement of funding as it ensures that

funding should be continued for each and every department (Alleyne and Weekes-

Marshall, 2011).

This approach makes sure that there are not big variations or differences in budget year

after year because of some gradual changes in the requirement of budget. Company

should have stable budget year on year according to this type of budget.

For substituting or eliminating rivalry, this technique is most popular among many XYZ

co.s and it also builds value of equality among each and every departments as everyone

has been given similar increment amount over the previous year.

In the scenario of incremental budgeting, changes and its impact can be easily identified.

It is perfect match for the XYZ co.s where the requirement of funding is generally fixed

or it may have some small variations.

Demerits

There is an assumption that requirement of year is marginally different from previous

year but in actual there are some changes which are structural in context of economy,

XYZ co. or industry which might give more significant changes in budget.

This approach may lead to more expenses by the managers as budget's availability is easy

and it will be using more funds which are not necessary and even not warranted.

From the above assumption about less change from previous year to next year, it will be

creating lack of innovation, creativity and even no incentives for reducing cost to the

managers.

Incremental budgets is usually affecting net income i.e. encourages more spending which

will be added in expenses and but with this budget will be maintained next year.

Budgetary slack will be caused in management with incremental budgeting, where

expenses of the XYZ co. will be more than revenue of the XYZ co. to have some

favourable variances.

9

Incremental budget's implementation is very easy and it does not have any complexity in

calculations as it can be obtained from different departments in the absence of any issue

because there is no need of any detailed analysis.

There is no need of any detailed analysis of requirement of funding as it ensures that

funding should be continued for each and every department (Alleyne and Weekes-

Marshall, 2011).

This approach makes sure that there are not big variations or differences in budget year

after year because of some gradual changes in the requirement of budget. Company

should have stable budget year on year according to this type of budget.

For substituting or eliminating rivalry, this technique is most popular among many XYZ

co.s and it also builds value of equality among each and every departments as everyone

has been given similar increment amount over the previous year.

In the scenario of incremental budgeting, changes and its impact can be easily identified.

It is perfect match for the XYZ co.s where the requirement of funding is generally fixed

or it may have some small variations.

Demerits

There is an assumption that requirement of year is marginally different from previous

year but in actual there are some changes which are structural in context of economy,

XYZ co. or industry which might give more significant changes in budget.

This approach may lead to more expenses by the managers as budget's availability is easy

and it will be using more funds which are not necessary and even not warranted.

From the above assumption about less change from previous year to next year, it will be

creating lack of innovation, creativity and even no incentives for reducing cost to the

managers.

Incremental budgets is usually affecting net income i.e. encourages more spending which

will be added in expenses and but with this budget will be maintained next year.

Budgetary slack will be caused in management with incremental budgeting, where

expenses of the XYZ co. will be more than revenue of the XYZ co. to have some

favourable variances.

9

As in this, reality has been disconnected as actual results are usually different from the

budgeted budget which are on the basis of previous year benchmark not on forecasted or

predicted requirements.

It may lead to wastage of resources, because like individual, every department is different

and needs are different of each and every department, as some funds are not required by

every department so this will lead to wastage of resources.

As budget allocation is more or less similar to every year, then this will lead to run

business in very conservative manner, if any business's wish is to take large risk then

funding is not required (Chenhall, R. H. and Smith, D., 2011).

Activity based budgeting: It is a management accounting tool where budgets are

prepared by using activity based costing after the consideration of overhead costs. It does not

consider the budget of previous or past year for coming at recent year's budget. On the basis of

outcome, resources are allocated to each and every activity. It is an activity oriented budget not a

function oriented budget.

Merits

Each and every cost driver has been evaluated by activity based budgeting and every step

has been considered in the activity and irrelevant activities are substituted by relevant

activities from the part of business

As it eliminates all unnecessary activities which helps the business for reducing cost. The

cost which has been saved while eliminating unnecessary activity gives results in

production of services and good as compared to its competitors. In this way it will create

competitive edge in the market.

It cannot be in form of department if this budgeting technique has been used, it will be

treated as single unit business. The budget has been prepared by top management or

managers by keeping in mind the whole company not any single department.

Activity based budgeting helps in elimination of bottlenecks, as budget is prepared after

deep analysis and research. It removes all useless activities and after these bottlenecks is

rid of and functions of business will be carried so smoothly.

Last but not least, relationship has been improved by activity based budgeting in all

departments or the XYZ co. and customers. As the main objective of this budgeting

technique is to substitute the unnecessary activity and provide the best quality at best

10

budgeted budget which are on the basis of previous year benchmark not on forecasted or

predicted requirements.

It may lead to wastage of resources, because like individual, every department is different

and needs are different of each and every department, as some funds are not required by

every department so this will lead to wastage of resources.

As budget allocation is more or less similar to every year, then this will lead to run

business in very conservative manner, if any business's wish is to take large risk then

funding is not required (Chenhall, R. H. and Smith, D., 2011).

Activity based budgeting: It is a management accounting tool where budgets are

prepared by using activity based costing after the consideration of overhead costs. It does not

consider the budget of previous or past year for coming at recent year's budget. On the basis of

outcome, resources are allocated to each and every activity. It is an activity oriented budget not a

function oriented budget.

Merits

Each and every cost driver has been evaluated by activity based budgeting and every step

has been considered in the activity and irrelevant activities are substituted by relevant

activities from the part of business

As it eliminates all unnecessary activities which helps the business for reducing cost. The

cost which has been saved while eliminating unnecessary activity gives results in

production of services and good as compared to its competitors. In this way it will create

competitive edge in the market.

It cannot be in form of department if this budgeting technique has been used, it will be

treated as single unit business. The budget has been prepared by top management or

managers by keeping in mind the whole company not any single department.

Activity based budgeting helps in elimination of bottlenecks, as budget is prepared after

deep analysis and research. It removes all useless activities and after these bottlenecks is

rid of and functions of business will be carried so smoothly.

Last but not least, relationship has been improved by activity based budgeting in all

departments or the XYZ co. and customers. As the main objective of this budgeting

technique is to substitute the unnecessary activity and provide the best quality at best

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.