Understanding Historical Cost and Fair Value Principles in Business Accounting

VerifiedAdded on 2022/12/28

|13

|1915

|77

AI Summary

This business report discusses the pros and cons of Historical Cost Principle and Fair Value Principle in business accounting. It provides recommendations on which principle to follow and explains how these principles impact financial reporting and asset valuation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

a. Journal entries.....................................................................................................................3

b. Posting entries to ledger.....................................................................................................4

c. Adjusted trial balance.........................................................................................................7

d. Preparing income statement and balance sheet..................................................................8

e. Closing entries and posting them to the ledger..................................................................9

f. Business report..................................................................................................................11

REFERENCES.........................................................................................................................13

a. Journal entries.....................................................................................................................3

b. Posting entries to ledger.....................................................................................................4

c. Adjusted trial balance.........................................................................................................7

d. Preparing income statement and balance sheet..................................................................8

e. Closing entries and posting them to the ledger..................................................................9

f. Business report..................................................................................................................11

REFERENCES.........................................................................................................................13

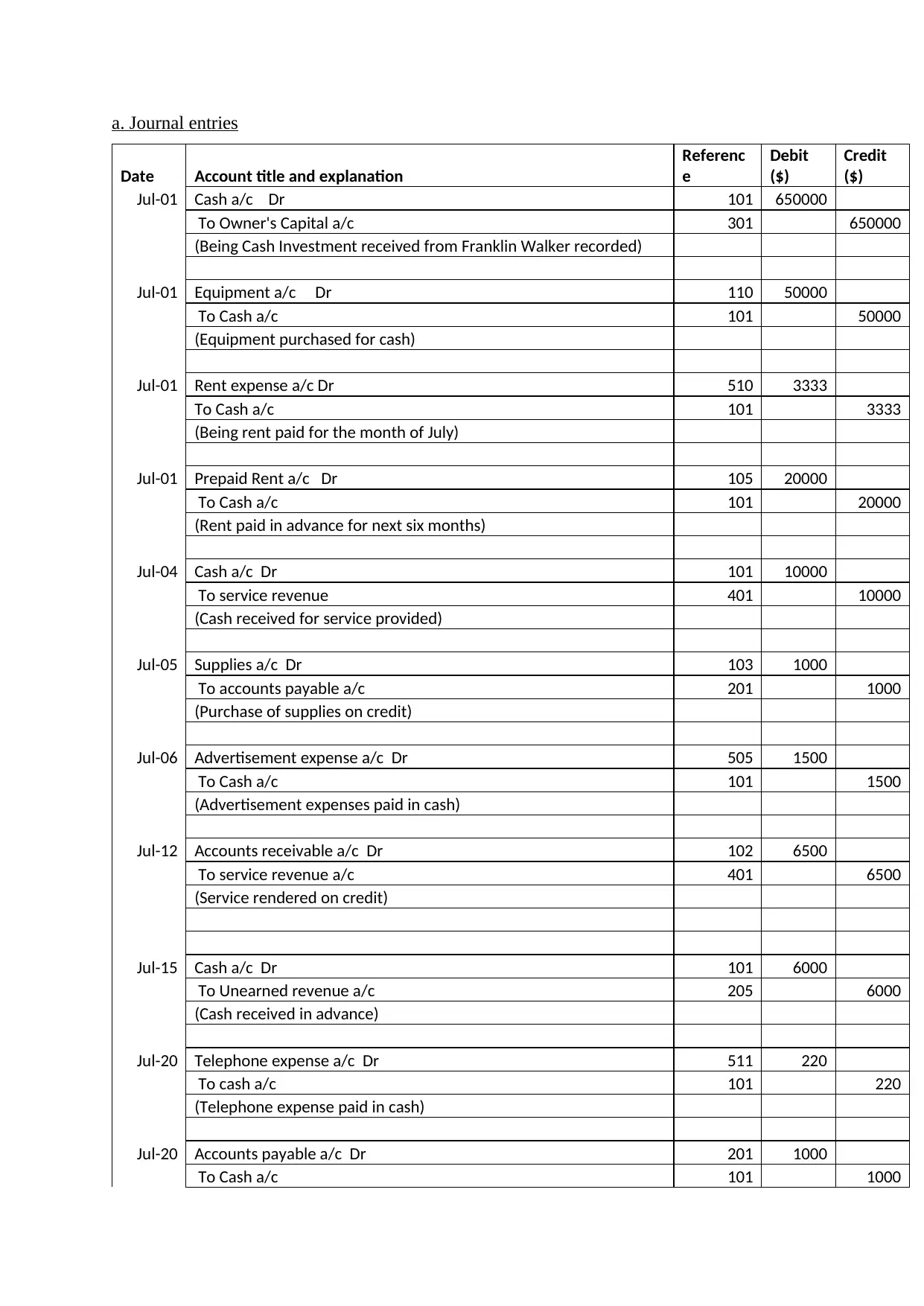

a. Journal entries

Date Account title and explanation

Referenc

e

Debit

($)

Credit

($)

Jul-01 Cash a/c Dr 101 650000

To Owner's Capital a/c 301 650000

(Being Cash Investment received from Franklin Walker recorded)

Jul-01 Equipment a/c Dr 110 50000

To Cash a/c 101 50000

(Equipment purchased for cash)

Jul-01 Rent expense a/c Dr 510 3333

To Cash a/c 101 3333

(Being rent paid for the month of July)

Jul-01 Prepaid Rent a/c Dr 105 20000

To Cash a/c 101 20000

(Rent paid in advance for next six months)

Jul-04 Cash a/c Dr 101 10000

To service revenue 401 10000

(Cash received for service provided)

Jul-05 Supplies a/c Dr 103 1000

To accounts payable a/c 201 1000

(Purchase of supplies on credit)

Jul-06 Advertisement expense a/c Dr 505 1500

To Cash a/c 101 1500

(Advertisement expenses paid in cash)

Jul-12 Accounts receivable a/c Dr 102 6500

To service revenue a/c 401 6500

(Service rendered on credit)

Jul-15 Cash a/c Dr 101 6000

To Unearned revenue a/c 205 6000

(Cash received in advance)

Jul-20 Telephone expense a/c Dr 511 220

To cash a/c 101 220

(Telephone expense paid in cash)

Jul-20 Accounts payable a/c Dr 201 1000

To Cash a/c 101 1000

Date Account title and explanation

Referenc

e

Debit

($)

Credit

($)

Jul-01 Cash a/c Dr 101 650000

To Owner's Capital a/c 301 650000

(Being Cash Investment received from Franklin Walker recorded)

Jul-01 Equipment a/c Dr 110 50000

To Cash a/c 101 50000

(Equipment purchased for cash)

Jul-01 Rent expense a/c Dr 510 3333

To Cash a/c 101 3333

(Being rent paid for the month of July)

Jul-01 Prepaid Rent a/c Dr 105 20000

To Cash a/c 101 20000

(Rent paid in advance for next six months)

Jul-04 Cash a/c Dr 101 10000

To service revenue 401 10000

(Cash received for service provided)

Jul-05 Supplies a/c Dr 103 1000

To accounts payable a/c 201 1000

(Purchase of supplies on credit)

Jul-06 Advertisement expense a/c Dr 505 1500

To Cash a/c 101 1500

(Advertisement expenses paid in cash)

Jul-12 Accounts receivable a/c Dr 102 6500

To service revenue a/c 401 6500

(Service rendered on credit)

Jul-15 Cash a/c Dr 101 6000

To Unearned revenue a/c 205 6000

(Cash received in advance)

Jul-20 Telephone expense a/c Dr 511 220

To cash a/c 101 220

(Telephone expense paid in cash)

Jul-20 Accounts payable a/c Dr 201 1000

To Cash a/c 101 1000

(Made payment for supplies)

Jul-31 Owner's Drawings a/c Dr 302 3000

To Cash a/c 301 3000

(Cash withdraw for personal use)

Jul-31 Salary expense a/c Dr 501 8000

To Cash a/c 101 8000

(Being Salary paid in cash)

Jul-31 Supply expense a/c Dr 503 200

To Cash a/c 101 200

(Being supplies purchased)

Jul-31 Unearned revenue a/c Dr 205 1200

To Service revenue a/c 401 1200

(Services rendered for unearned revenue)

Jul-31 Depreciation expense a/c Dr 507 817

To Accumulated Depreciation a/c 111 817

(Depreciation for 1 month charged0

Total 762770 762770

b. Posting entries to ledger

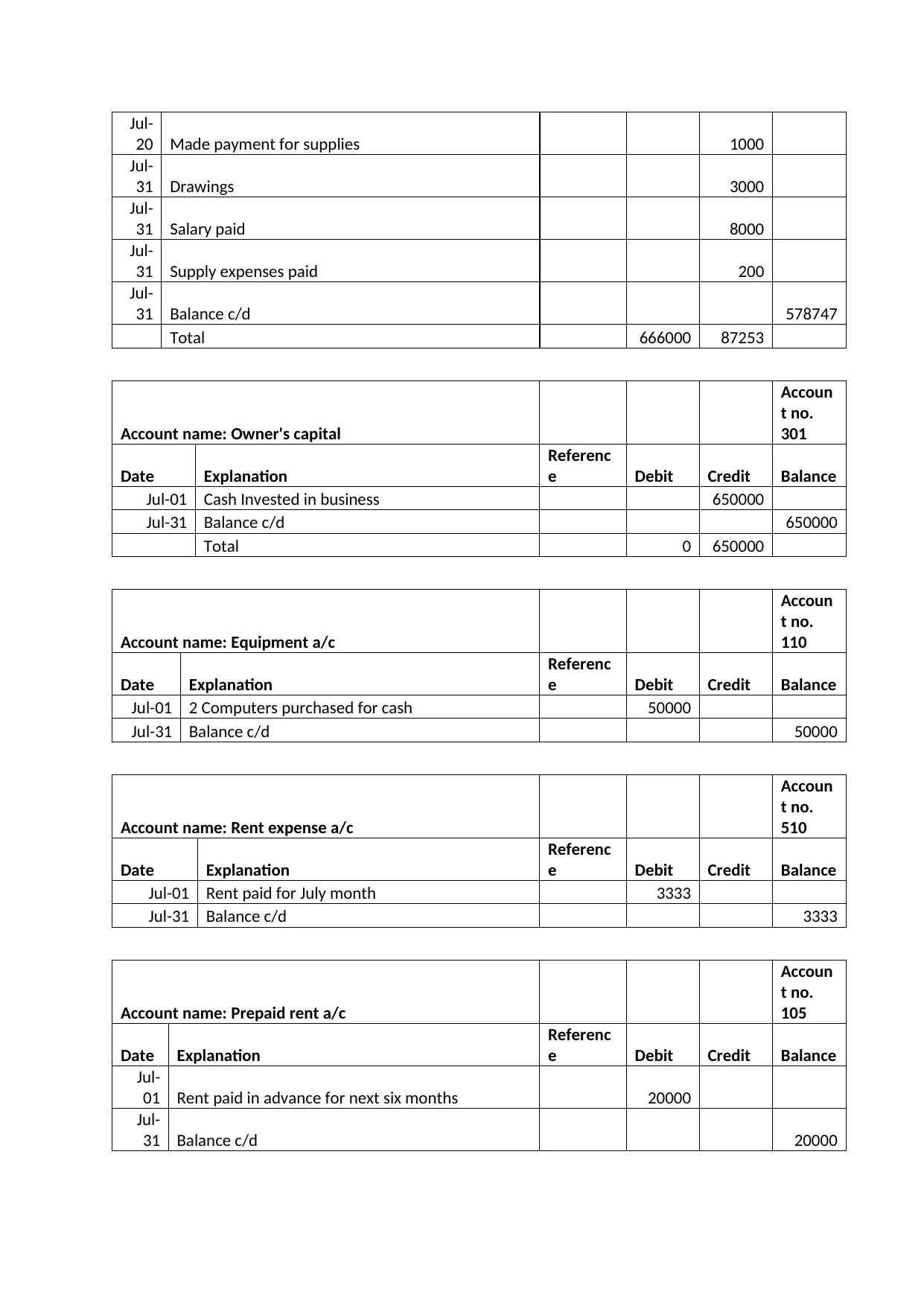

Account name: Cash

Accoun

t no.

101

Dat

e Explanation

Referenc

e Debit Credit Balance

Jul-

01 Cash Investment received from Franklin Walker 650000

Jul-

01 Equipment purchased for cash 50000

Jul-

01 Rent paid for July month 3333

Jul-

01 Prepaid rent 20000

Jul-

04 Cash received for service provided 10000

Jul-

06 Advertisement expenses paid in cash 1500

Jul-

15 Cash received in advance 6000

Jul-

20 Telephone expense paid in cash 220

Jul-31 Owner's Drawings a/c Dr 302 3000

To Cash a/c 301 3000

(Cash withdraw for personal use)

Jul-31 Salary expense a/c Dr 501 8000

To Cash a/c 101 8000

(Being Salary paid in cash)

Jul-31 Supply expense a/c Dr 503 200

To Cash a/c 101 200

(Being supplies purchased)

Jul-31 Unearned revenue a/c Dr 205 1200

To Service revenue a/c 401 1200

(Services rendered for unearned revenue)

Jul-31 Depreciation expense a/c Dr 507 817

To Accumulated Depreciation a/c 111 817

(Depreciation for 1 month charged0

Total 762770 762770

b. Posting entries to ledger

Account name: Cash

Accoun

t no.

101

Dat

e Explanation

Referenc

e Debit Credit Balance

Jul-

01 Cash Investment received from Franklin Walker 650000

Jul-

01 Equipment purchased for cash 50000

Jul-

01 Rent paid for July month 3333

Jul-

01 Prepaid rent 20000

Jul-

04 Cash received for service provided 10000

Jul-

06 Advertisement expenses paid in cash 1500

Jul-

15 Cash received in advance 6000

Jul-

20 Telephone expense paid in cash 220

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Jul-

20 Made payment for supplies 1000

Jul-

31 Drawings 3000

Jul-

31 Salary paid 8000

Jul-

31 Supply expenses paid 200

Jul-

31 Balance c/d 578747

Total 666000 87253

Account name: Owner's capital

Accoun

t no.

301

Date Explanation

Referenc

e Debit Credit Balance

Jul-01 Cash Invested in business 650000

Jul-31 Balance c/d 650000

Total 0 650000

Account name: Equipment a/c

Accoun

t no.

110

Date Explanation

Referenc

e Debit Credit Balance

Jul-01 2 Computers purchased for cash 50000

Jul-31 Balance c/d 50000

Account name: Rent expense a/c

Accoun

t no.

510

Date Explanation

Referenc

e Debit Credit Balance

Jul-01 Rent paid for July month 3333

Jul-31 Balance c/d 3333

Account name: Prepaid rent a/c

Accoun

t no.

105

Date Explanation

Referenc

e Debit Credit Balance

Jul-

01 Rent paid in advance for next six months 20000

Jul-

31 Balance c/d 20000

20 Made payment for supplies 1000

Jul-

31 Drawings 3000

Jul-

31 Salary paid 8000

Jul-

31 Supply expenses paid 200

Jul-

31 Balance c/d 578747

Total 666000 87253

Account name: Owner's capital

Accoun

t no.

301

Date Explanation

Referenc

e Debit Credit Balance

Jul-01 Cash Invested in business 650000

Jul-31 Balance c/d 650000

Total 0 650000

Account name: Equipment a/c

Accoun

t no.

110

Date Explanation

Referenc

e Debit Credit Balance

Jul-01 2 Computers purchased for cash 50000

Jul-31 Balance c/d 50000

Account name: Rent expense a/c

Accoun

t no.

510

Date Explanation

Referenc

e Debit Credit Balance

Jul-01 Rent paid for July month 3333

Jul-31 Balance c/d 3333

Account name: Prepaid rent a/c

Accoun

t no.

105

Date Explanation

Referenc

e Debit Credit Balance

Jul-

01 Rent paid in advance for next six months 20000

Jul-

31 Balance c/d 20000

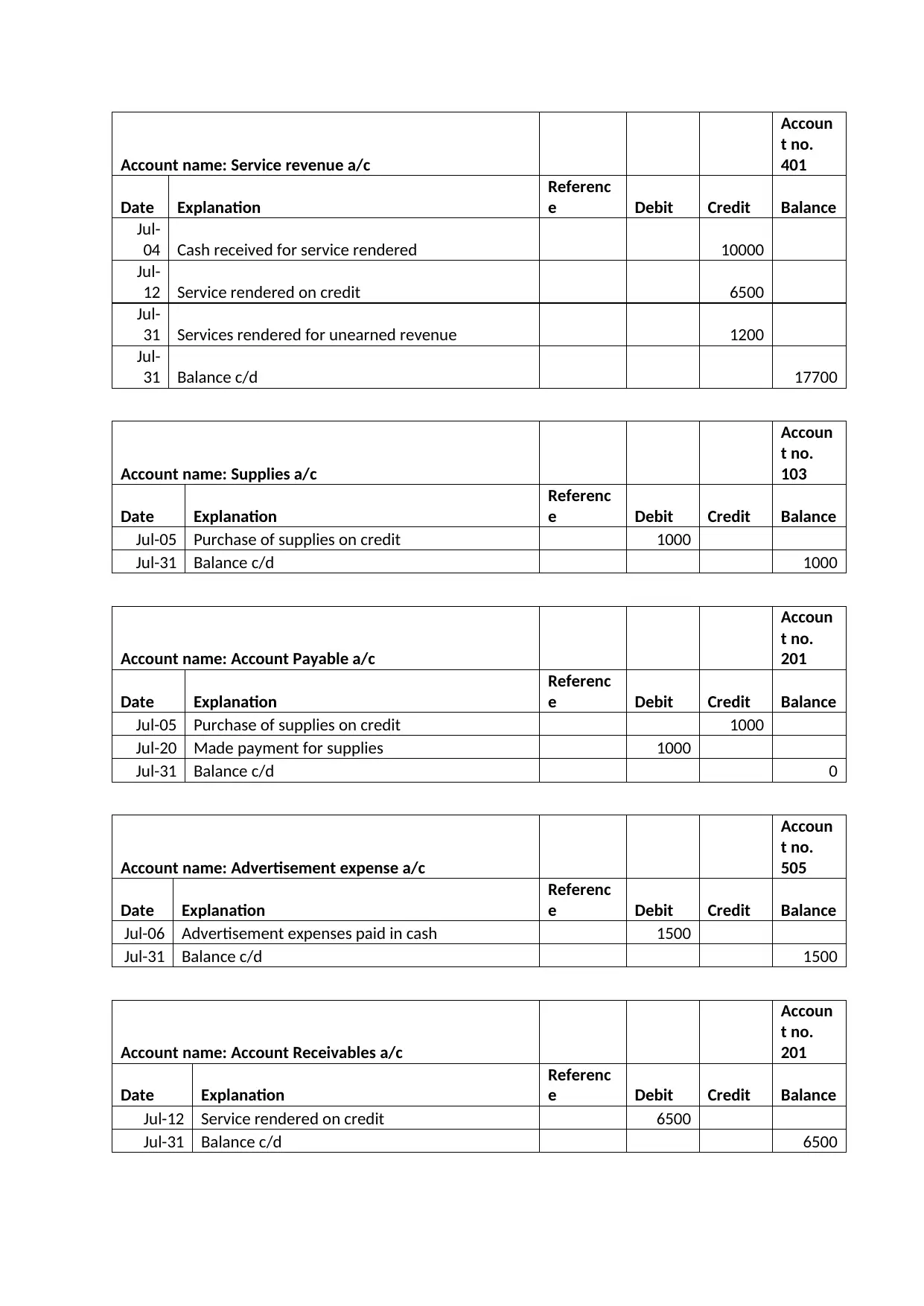

Account name: Service revenue a/c

Accoun

t no.

401

Date Explanation

Referenc

e Debit Credit Balance

Jul-

04 Cash received for service rendered 10000

Jul-

12 Service rendered on credit 6500

Jul-

31 Services rendered for unearned revenue 1200

Jul-

31 Balance c/d 17700

Account name: Supplies a/c

Accoun

t no.

103

Date Explanation

Referenc

e Debit Credit Balance

Jul-05 Purchase of supplies on credit 1000

Jul-31 Balance c/d 1000

Account name: Account Payable a/c

Accoun

t no.

201

Date Explanation

Referenc

e Debit Credit Balance

Jul-05 Purchase of supplies on credit 1000

Jul-20 Made payment for supplies 1000

Jul-31 Balance c/d 0

Account name: Advertisement expense a/c

Accoun

t no.

505

Date Explanation

Referenc

e Debit Credit Balance

Jul-06 Advertisement expenses paid in cash 1500

Jul-31 Balance c/d 1500

Account name: Account Receivables a/c

Accoun

t no.

201

Date Explanation

Referenc

e Debit Credit Balance

Jul-12 Service rendered on credit 6500

Jul-31 Balance c/d 6500

Accoun

t no.

401

Date Explanation

Referenc

e Debit Credit Balance

Jul-

04 Cash received for service rendered 10000

Jul-

12 Service rendered on credit 6500

Jul-

31 Services rendered for unearned revenue 1200

Jul-

31 Balance c/d 17700

Account name: Supplies a/c

Accoun

t no.

103

Date Explanation

Referenc

e Debit Credit Balance

Jul-05 Purchase of supplies on credit 1000

Jul-31 Balance c/d 1000

Account name: Account Payable a/c

Accoun

t no.

201

Date Explanation

Referenc

e Debit Credit Balance

Jul-05 Purchase of supplies on credit 1000

Jul-20 Made payment for supplies 1000

Jul-31 Balance c/d 0

Account name: Advertisement expense a/c

Accoun

t no.

505

Date Explanation

Referenc

e Debit Credit Balance

Jul-06 Advertisement expenses paid in cash 1500

Jul-31 Balance c/d 1500

Account name: Account Receivables a/c

Accoun

t no.

201

Date Explanation

Referenc

e Debit Credit Balance

Jul-12 Service rendered on credit 6500

Jul-31 Balance c/d 6500

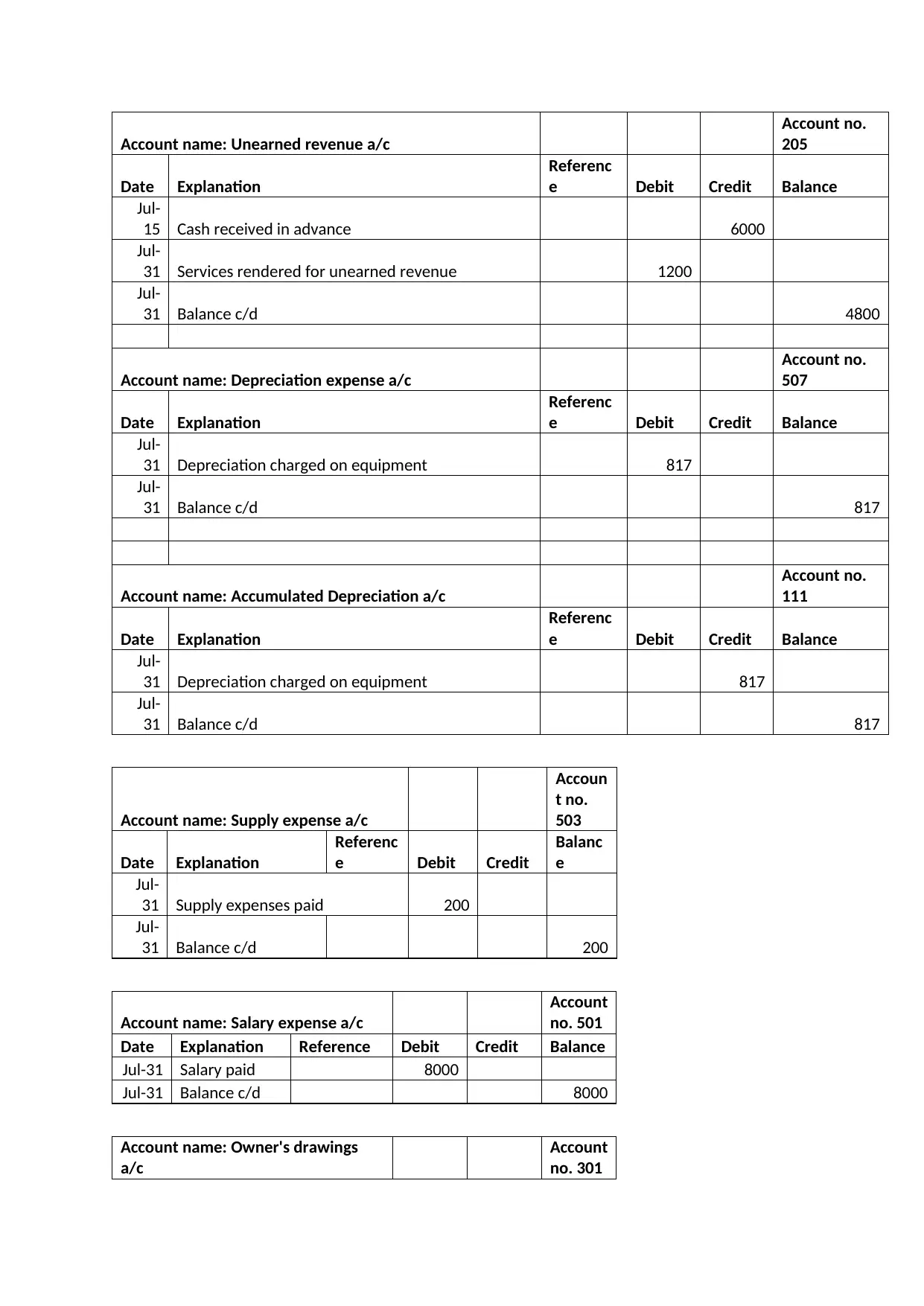

Account name: Unearned revenue a/c

Account no.

205

Date Explanation

Referenc

e Debit Credit Balance

Jul-

15 Cash received in advance 6000

Jul-

31 Services rendered for unearned revenue 1200

Jul-

31 Balance c/d 4800

Account name: Depreciation expense a/c

Account no.

507

Date Explanation

Referenc

e Debit Credit Balance

Jul-

31 Depreciation charged on equipment 817

Jul-

31 Balance c/d 817

Account name: Accumulated Depreciation a/c

Account no.

111

Date Explanation

Referenc

e Debit Credit Balance

Jul-

31 Depreciation charged on equipment 817

Jul-

31 Balance c/d 817

Account name: Supply expense a/c

Accoun

t no.

503

Date Explanation

Referenc

e Debit Credit

Balanc

e

Jul-

31 Supply expenses paid 200

Jul-

31 Balance c/d 200

Account name: Salary expense a/c

Account

no. 501

Date Explanation Reference Debit Credit Balance

Jul-31 Salary paid 8000

Jul-31 Balance c/d 8000

Account name: Owner's drawings

a/c

Account

no. 301

Account no.

205

Date Explanation

Referenc

e Debit Credit Balance

Jul-

15 Cash received in advance 6000

Jul-

31 Services rendered for unearned revenue 1200

Jul-

31 Balance c/d 4800

Account name: Depreciation expense a/c

Account no.

507

Date Explanation

Referenc

e Debit Credit Balance

Jul-

31 Depreciation charged on equipment 817

Jul-

31 Balance c/d 817

Account name: Accumulated Depreciation a/c

Account no.

111

Date Explanation

Referenc

e Debit Credit Balance

Jul-

31 Depreciation charged on equipment 817

Jul-

31 Balance c/d 817

Account name: Supply expense a/c

Accoun

t no.

503

Date Explanation

Referenc

e Debit Credit

Balanc

e

Jul-

31 Supply expenses paid 200

Jul-

31 Balance c/d 200

Account name: Salary expense a/c

Account

no. 501

Date Explanation Reference Debit Credit Balance

Jul-31 Salary paid 8000

Jul-31 Balance c/d 8000

Account name: Owner's drawings

a/c

Account

no. 301

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

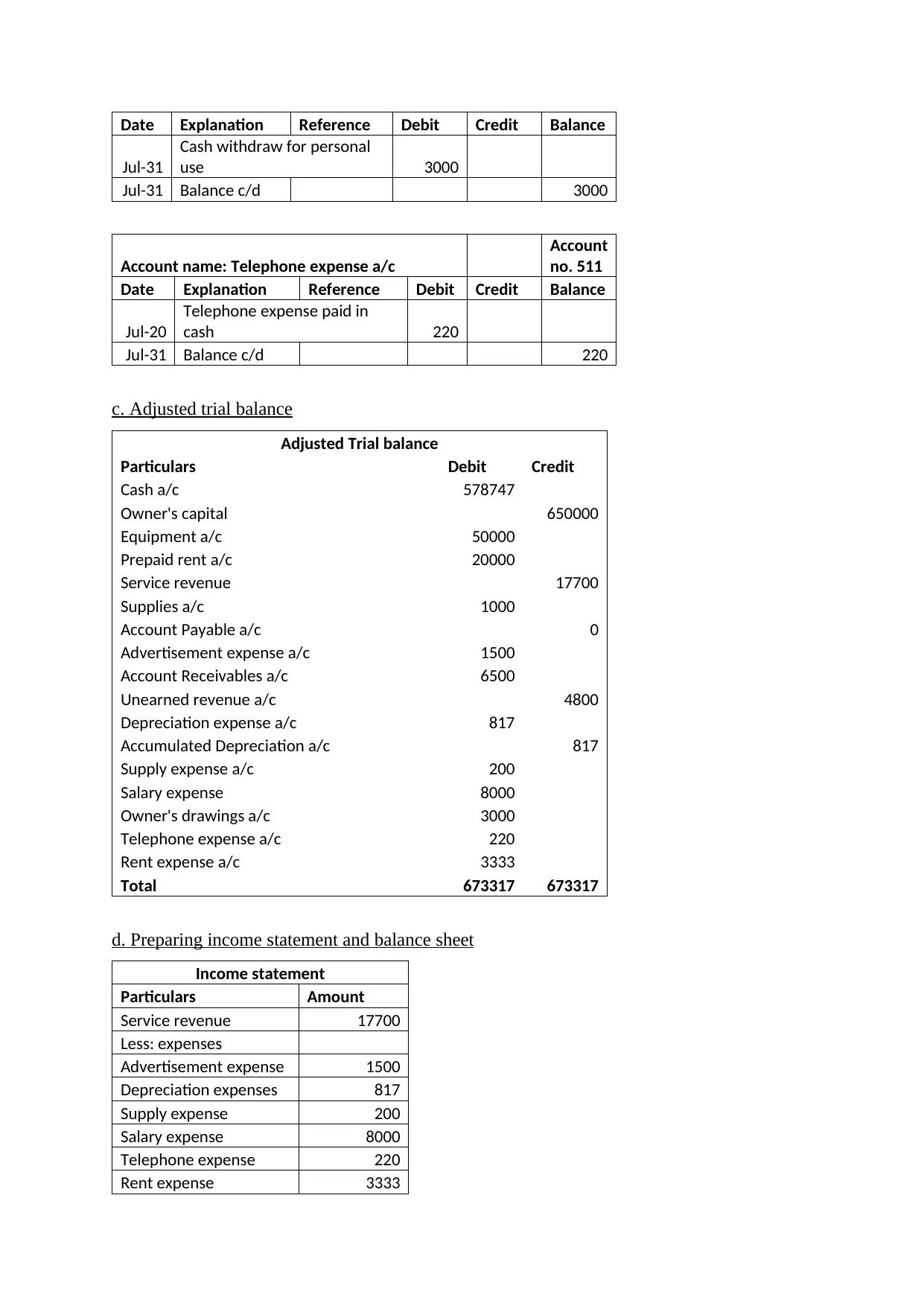

Date Explanation Reference Debit Credit Balance

Jul-31

Cash withdraw for personal

use 3000

Jul-31 Balance c/d 3000

Account name: Telephone expense a/c

Account

no. 511

Date Explanation Reference Debit Credit Balance

Jul-20

Telephone expense paid in

cash 220

Jul-31 Balance c/d 220

c. Adjusted trial balance

Adjusted Trial balance

Particulars Debit Credit

Cash a/c 578747

Owner's capital 650000

Equipment a/c 50000

Prepaid rent a/c 20000

Service revenue 17700

Supplies a/c 1000

Account Payable a/c 0

Advertisement expense a/c 1500

Account Receivables a/c 6500

Unearned revenue a/c 4800

Depreciation expense a/c 817

Accumulated Depreciation a/c 817

Supply expense a/c 200

Salary expense 8000

Owner's drawings a/c 3000

Telephone expense a/c 220

Rent expense a/c 3333

Total 673317 673317

d. Preparing income statement and balance sheet

Income statement

Particulars Amount

Service revenue 17700

Less: expenses

Advertisement expense 1500

Depreciation expenses 817

Supply expense 200

Salary expense 8000

Telephone expense 220

Rent expense 3333

Jul-31

Cash withdraw for personal

use 3000

Jul-31 Balance c/d 3000

Account name: Telephone expense a/c

Account

no. 511

Date Explanation Reference Debit Credit Balance

Jul-20

Telephone expense paid in

cash 220

Jul-31 Balance c/d 220

c. Adjusted trial balance

Adjusted Trial balance

Particulars Debit Credit

Cash a/c 578747

Owner's capital 650000

Equipment a/c 50000

Prepaid rent a/c 20000

Service revenue 17700

Supplies a/c 1000

Account Payable a/c 0

Advertisement expense a/c 1500

Account Receivables a/c 6500

Unearned revenue a/c 4800

Depreciation expense a/c 817

Accumulated Depreciation a/c 817

Supply expense a/c 200

Salary expense 8000

Owner's drawings a/c 3000

Telephone expense a/c 220

Rent expense a/c 3333

Total 673317 673317

d. Preparing income statement and balance sheet

Income statement

Particulars Amount

Service revenue 17700

Less: expenses

Advertisement expense 1500

Depreciation expenses 817

Supply expense 200

Salary expense 8000

Telephone expense 220

Rent expense 3333

Total expenses 14070

Net profit 3630

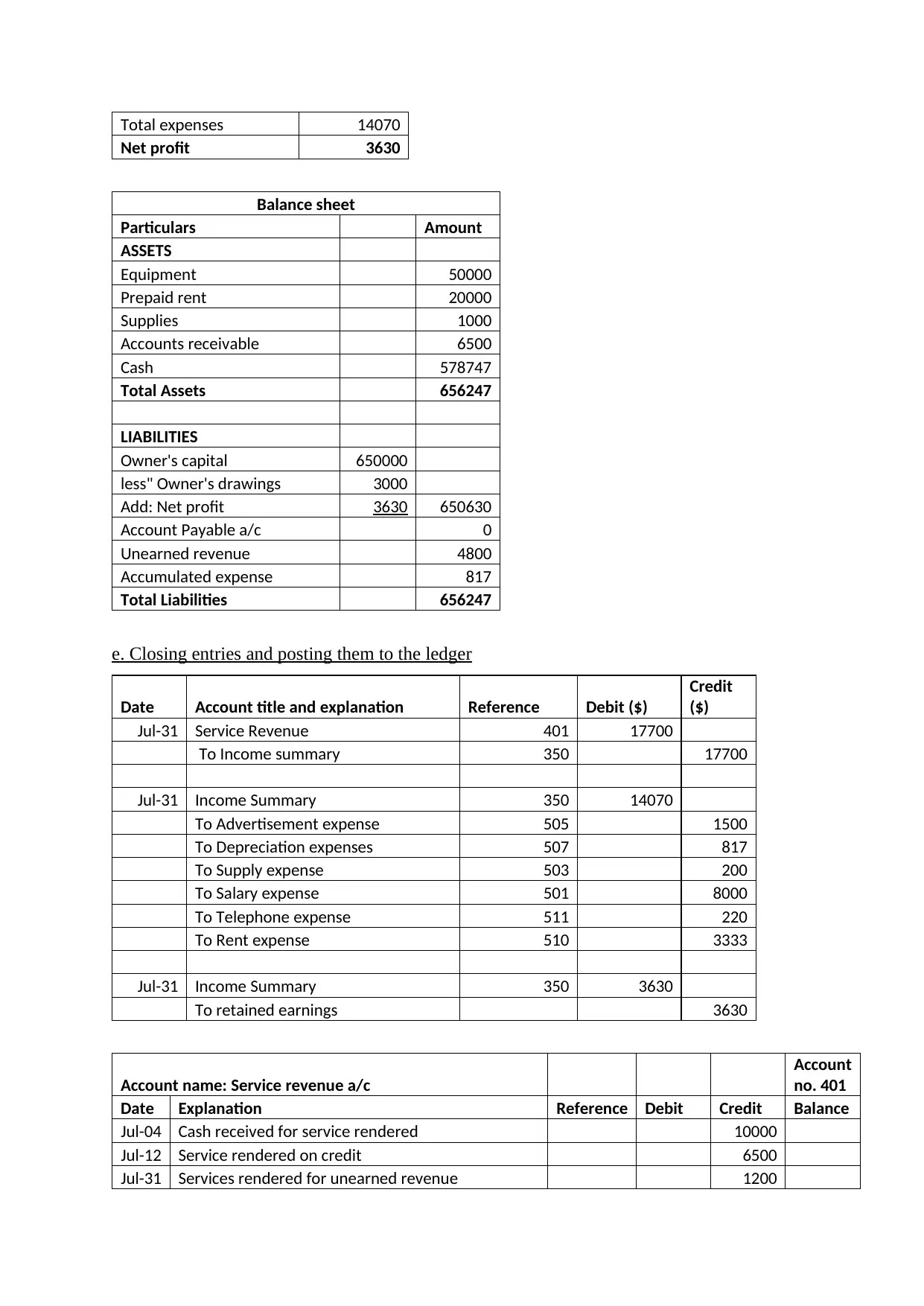

Balance sheet

Particulars Amount

ASSETS

Equipment 50000

Prepaid rent 20000

Supplies 1000

Accounts receivable 6500

Cash 578747

Total Assets 656247

LIABILITIES

Owner's capital 650000

less" Owner's drawings 3000

Add: Net profit 3630 650630

Account Payable a/c 0

Unearned revenue 4800

Accumulated expense 817

Total Liabilities 656247

e. Closing entries and posting them to the ledger

Date Account title and explanation Reference Debit ($)

Credit

($)

Jul-31 Service Revenue 401 17700

To Income summary 350 17700

Jul-31 Income Summary 350 14070

To Advertisement expense 505 1500

To Depreciation expenses 507 817

To Supply expense 503 200

To Salary expense 501 8000

To Telephone expense 511 220

To Rent expense 510 3333

Jul-31 Income Summary 350 3630

To retained earnings 3630

Account name: Service revenue a/c

Account

no. 401

Date Explanation Reference Debit Credit Balance

Jul-04 Cash received for service rendered 10000

Jul-12 Service rendered on credit 6500

Jul-31 Services rendered for unearned revenue 1200

Net profit 3630

Balance sheet

Particulars Amount

ASSETS

Equipment 50000

Prepaid rent 20000

Supplies 1000

Accounts receivable 6500

Cash 578747

Total Assets 656247

LIABILITIES

Owner's capital 650000

less" Owner's drawings 3000

Add: Net profit 3630 650630

Account Payable a/c 0

Unearned revenue 4800

Accumulated expense 817

Total Liabilities 656247

e. Closing entries and posting them to the ledger

Date Account title and explanation Reference Debit ($)

Credit

($)

Jul-31 Service Revenue 401 17700

To Income summary 350 17700

Jul-31 Income Summary 350 14070

To Advertisement expense 505 1500

To Depreciation expenses 507 817

To Supply expense 503 200

To Salary expense 501 8000

To Telephone expense 511 220

To Rent expense 510 3333

Jul-31 Income Summary 350 3630

To retained earnings 3630

Account name: Service revenue a/c

Account

no. 401

Date Explanation Reference Debit Credit Balance

Jul-04 Cash received for service rendered 10000

Jul-12 Service rendered on credit 6500

Jul-31 Services rendered for unearned revenue 1200

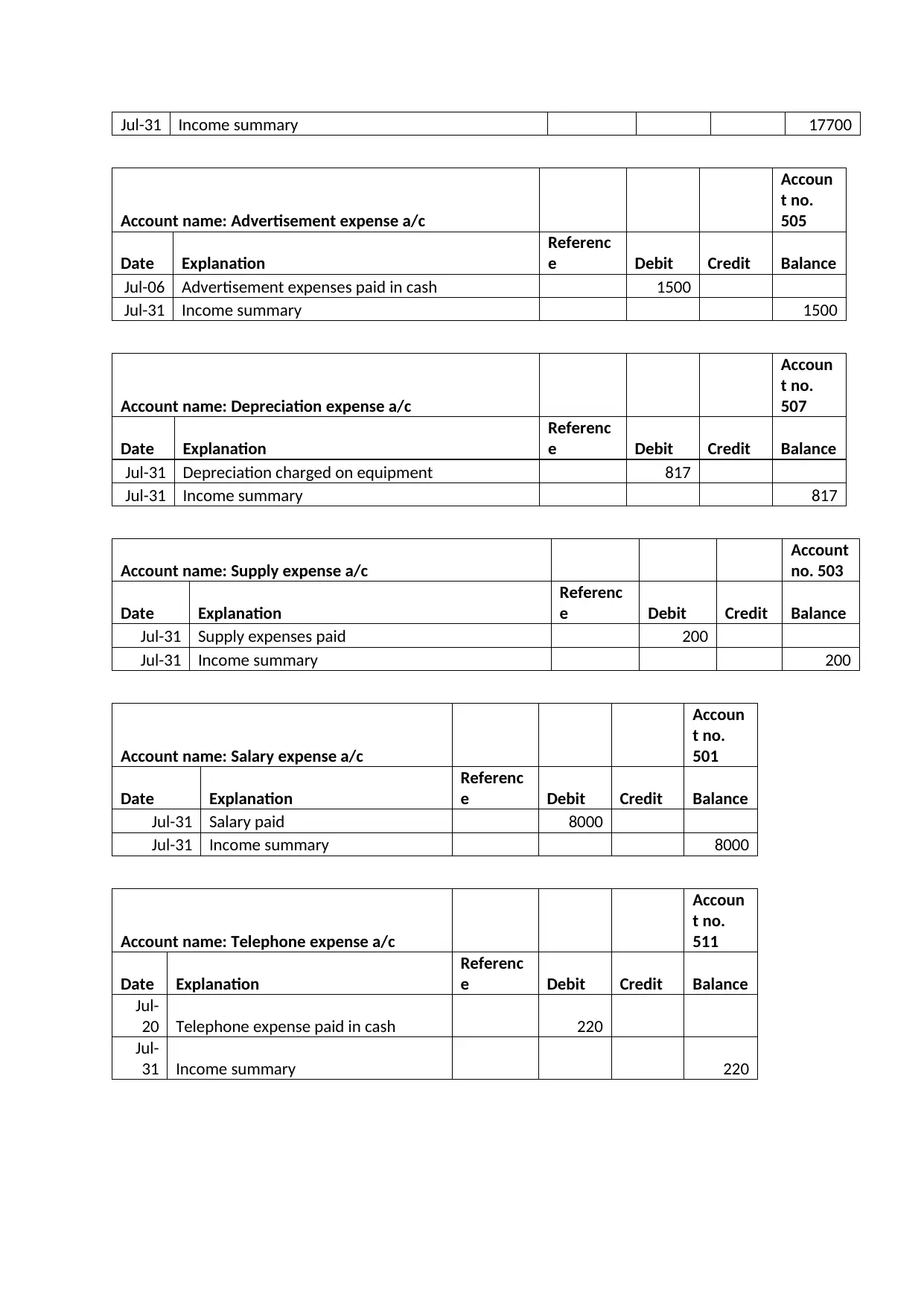

Jul-31 Income summary 17700

Account name: Advertisement expense a/c

Accoun

t no.

505

Date Explanation

Referenc

e Debit Credit Balance

Jul-06 Advertisement expenses paid in cash 1500

Jul-31 Income summary 1500

Account name: Depreciation expense a/c

Accoun

t no.

507

Date Explanation

Referenc

e Debit Credit Balance

Jul-31 Depreciation charged on equipment 817

Jul-31 Income summary 817

Account name: Supply expense a/c

Account

no. 503

Date Explanation

Referenc

e Debit Credit Balance

Jul-31 Supply expenses paid 200

Jul-31 Income summary 200

Account name: Salary expense a/c

Accoun

t no.

501

Date Explanation

Referenc

e Debit Credit Balance

Jul-31 Salary paid 8000

Jul-31 Income summary 8000

Account name: Telephone expense a/c

Accoun

t no.

511

Date Explanation

Referenc

e Debit Credit Balance

Jul-

20 Telephone expense paid in cash 220

Jul-

31 Income summary 220

Account name: Advertisement expense a/c

Accoun

t no.

505

Date Explanation

Referenc

e Debit Credit Balance

Jul-06 Advertisement expenses paid in cash 1500

Jul-31 Income summary 1500

Account name: Depreciation expense a/c

Accoun

t no.

507

Date Explanation

Referenc

e Debit Credit Balance

Jul-31 Depreciation charged on equipment 817

Jul-31 Income summary 817

Account name: Supply expense a/c

Account

no. 503

Date Explanation

Referenc

e Debit Credit Balance

Jul-31 Supply expenses paid 200

Jul-31 Income summary 200

Account name: Salary expense a/c

Accoun

t no.

501

Date Explanation

Referenc

e Debit Credit Balance

Jul-31 Salary paid 8000

Jul-31 Income summary 8000

Account name: Telephone expense a/c

Accoun

t no.

511

Date Explanation

Referenc

e Debit Credit Balance

Jul-

20 Telephone expense paid in cash 220

Jul-

31 Income summary 220

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

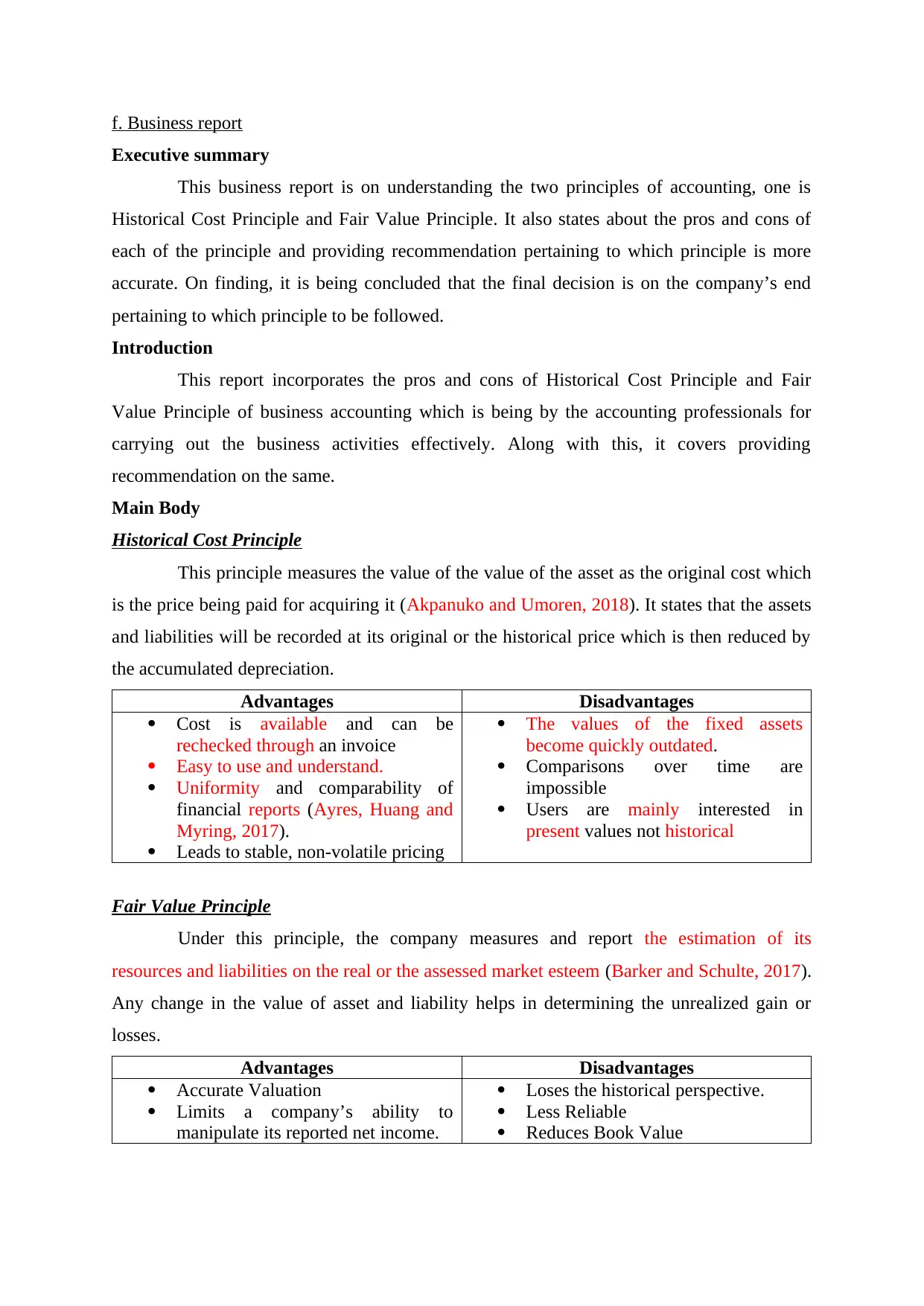

f. Business report

Executive summary

This business report is on understanding the two principles of accounting, one is

Historical Cost Principle and Fair Value Principle. It also states about the pros and cons of

each of the principle and providing recommendation pertaining to which principle is more

accurate. On finding, it is being concluded that the final decision is on the company’s end

pertaining to which principle to be followed.

Introduction

This report incorporates the pros and cons of Historical Cost Principle and Fair

Value Principle of business accounting which is being by the accounting professionals for

carrying out the business activities effectively. Along with this, it covers providing

recommendation on the same.

Main Body

Historical Cost Principle

This principle measures the value of the value of the asset as the original cost which

is the price being paid for acquiring it (Akpanuko and Umoren, 2018). It states that the assets

and liabilities will be recorded at its original or the historical price which is then reduced by

the accumulated depreciation.

Advantages Disadvantages

Cost is available and can be

rechecked through an invoice

Easy to use and understand.

Uniformity and comparability of

financial reports (Ayres, Huang and

Myring, 2017).

Leads to stable, non-volatile pricing

The values of the fixed assets

become quickly outdated.

Comparisons over time are

impossible

Users are mainly interested in

present values not historical

Fair Value Principle

Under this principle, the company measures and report the estimation of its

resources and liabilities on the real or the assessed market esteem (Barker and Schulte, 2017).

Any change in the value of asset and liability helps in determining the unrealized gain or

losses.

Advantages Disadvantages

Accurate Valuation

Limits a company’s ability to

manipulate its reported net income.

Loses the historical perspective.

Less Reliable

Reduces Book Value

Executive summary

This business report is on understanding the two principles of accounting, one is

Historical Cost Principle and Fair Value Principle. It also states about the pros and cons of

each of the principle and providing recommendation pertaining to which principle is more

accurate. On finding, it is being concluded that the final decision is on the company’s end

pertaining to which principle to be followed.

Introduction

This report incorporates the pros and cons of Historical Cost Principle and Fair

Value Principle of business accounting which is being by the accounting professionals for

carrying out the business activities effectively. Along with this, it covers providing

recommendation on the same.

Main Body

Historical Cost Principle

This principle measures the value of the value of the asset as the original cost which

is the price being paid for acquiring it (Akpanuko and Umoren, 2018). It states that the assets

and liabilities will be recorded at its original or the historical price which is then reduced by

the accumulated depreciation.

Advantages Disadvantages

Cost is available and can be

rechecked through an invoice

Easy to use and understand.

Uniformity and comparability of

financial reports (Ayres, Huang and

Myring, 2017).

Leads to stable, non-volatile pricing

The values of the fixed assets

become quickly outdated.

Comparisons over time are

impossible

Users are mainly interested in

present values not historical

Fair Value Principle

Under this principle, the company measures and report the estimation of its

resources and liabilities on the real or the assessed market esteem (Barker and Schulte, 2017).

Any change in the value of asset and liability helps in determining the unrealized gain or

losses.

Advantages Disadvantages

Accurate Valuation

Limits a company’s ability to

manipulate its reported net income.

Loses the historical perspective.

Less Reliable

Reduces Book Value

Recommendation

It is recommended that the company makes use of combination of both the concepts

as it should value its assets considering both fair and historical value and the principle which

can help in presenting better financial outcomes for the company

Conclusion

It can be inferred from the above that both the principles are having few pros and

cons which are against each other. So, the final decision is required to be made by the

company in regard to which principle should be implemented considering its benefits to the

business.

It is recommended that the company makes use of combination of both the concepts

as it should value its assets considering both fair and historical value and the principle which

can help in presenting better financial outcomes for the company

Conclusion

It can be inferred from the above that both the principles are having few pros and

cons which are against each other. So, the final decision is required to be made by the

company in regard to which principle should be implemented considering its benefits to the

business.

REFERENCES

Books and Journals

Akpanuko, E. E. and Umoren, N. J., 2018. The influence of creative accounting on the

credibility of accounting reports. Journal of Financial Reporting and Accounting.

Ayres, D., Huang, X. S. and Myring, M., 2017. Fair value accounting and analyst forecast

accuracy. Advances in Accounting. 37. pp.58-70.

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society. 56.

pp.55-67.

Books and Journals

Akpanuko, E. E. and Umoren, N. J., 2018. The influence of creative accounting on the

credibility of accounting reports. Journal of Financial Reporting and Accounting.

Ayres, D., Huang, X. S. and Myring, M., 2017. Fair value accounting and analyst forecast

accuracy. Advances in Accounting. 37. pp.58-70.

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society. 56.

pp.55-67.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.