Business Accounting: Financial Statement Preparation & Ratio Analysis

VerifiedAdded on 2023/06/18

|20

|3440

|485

Report

AI Summary

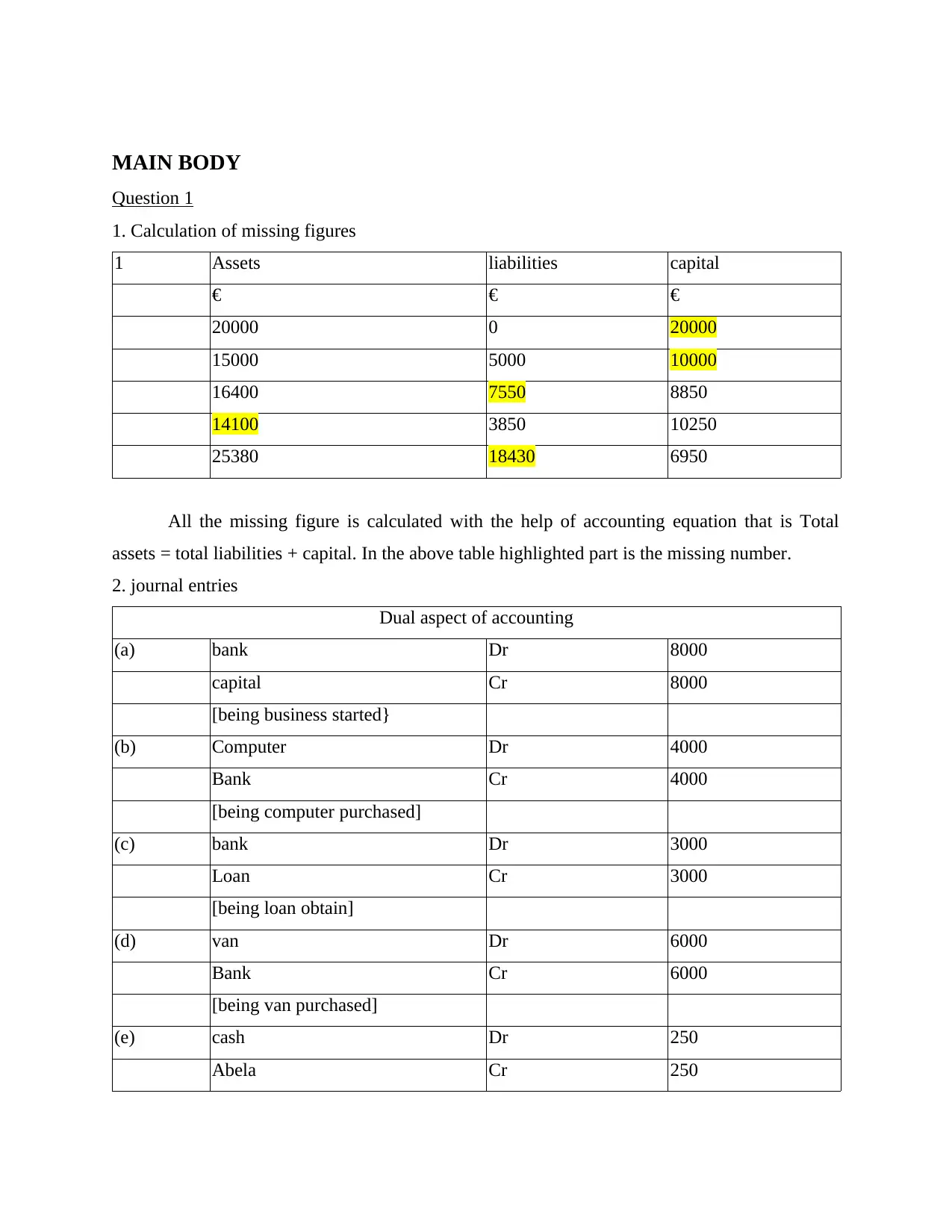

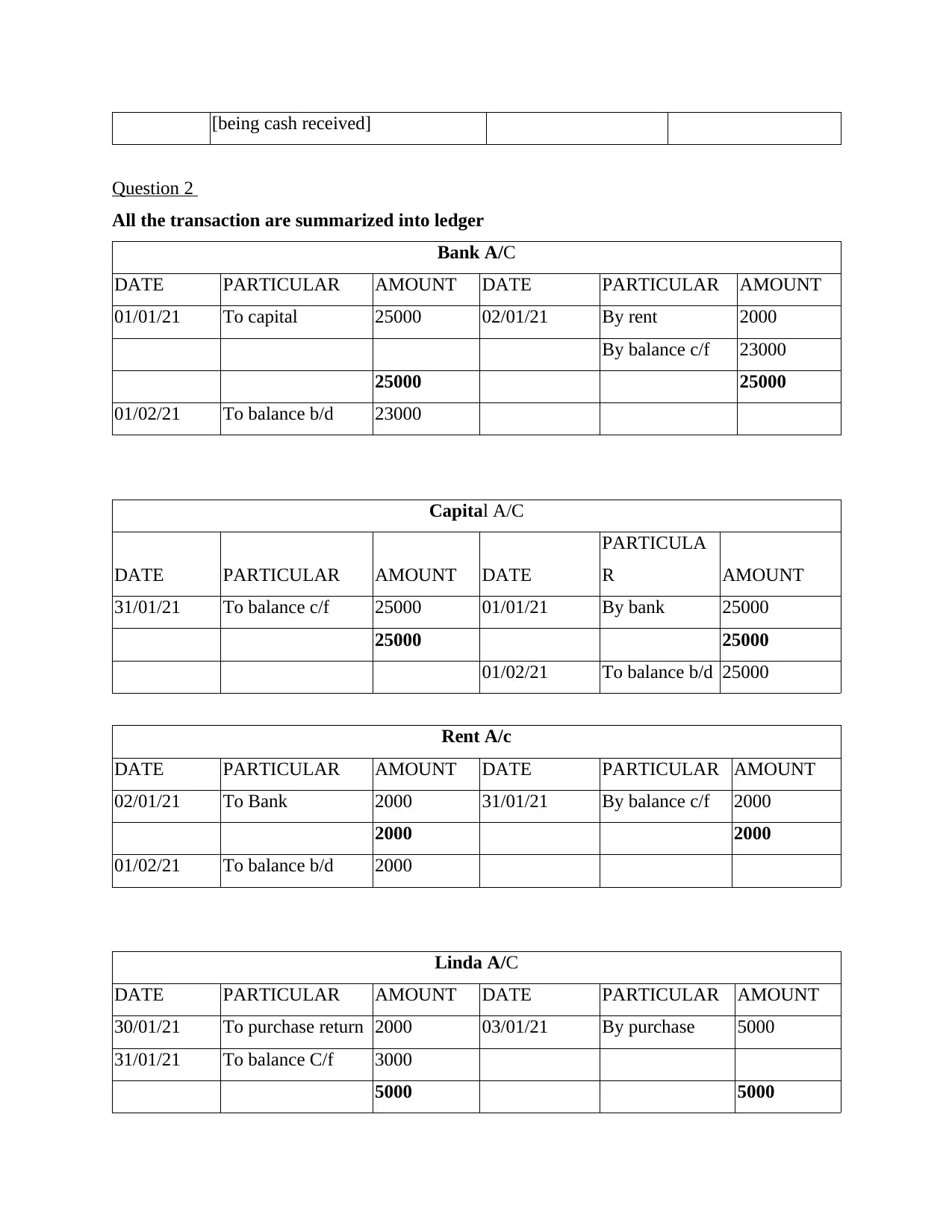

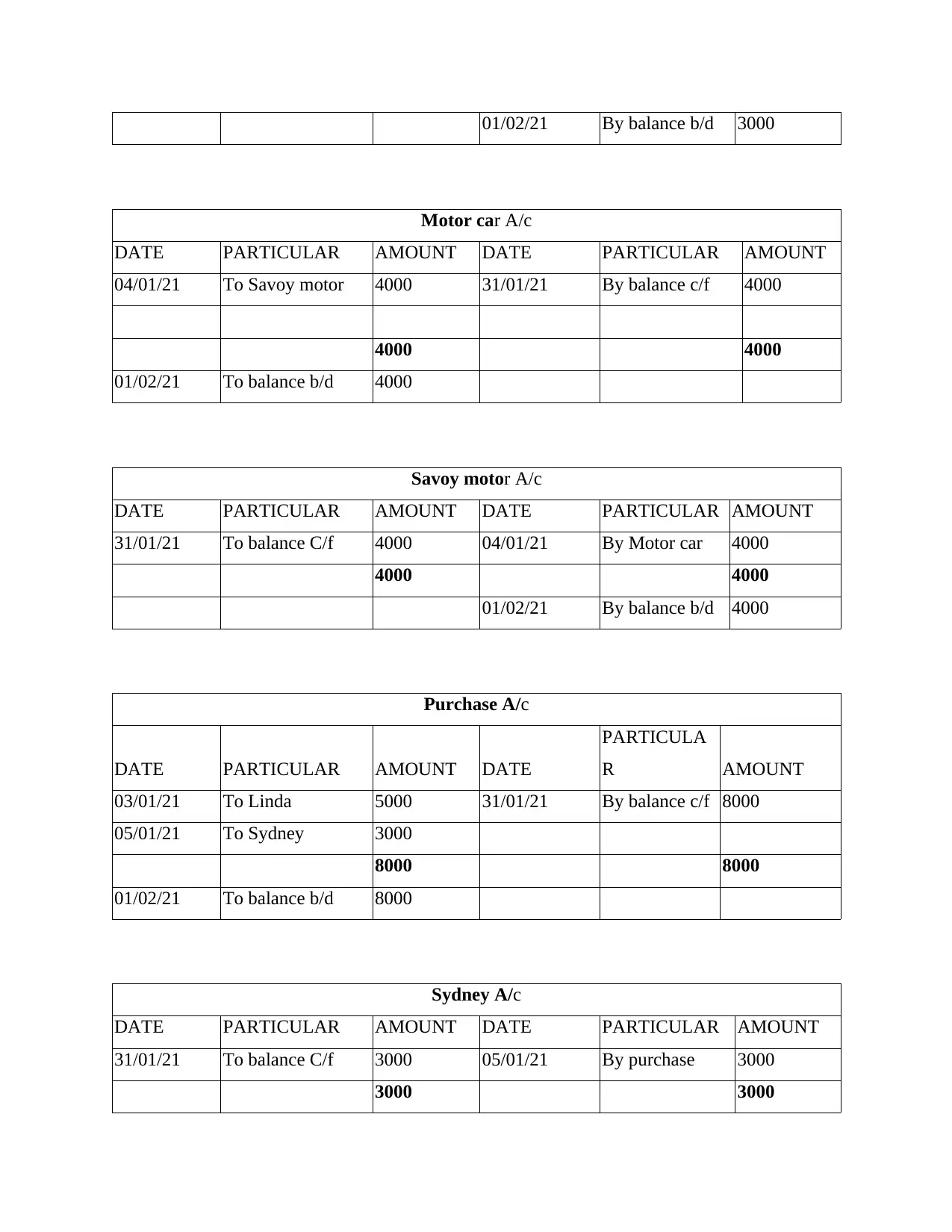

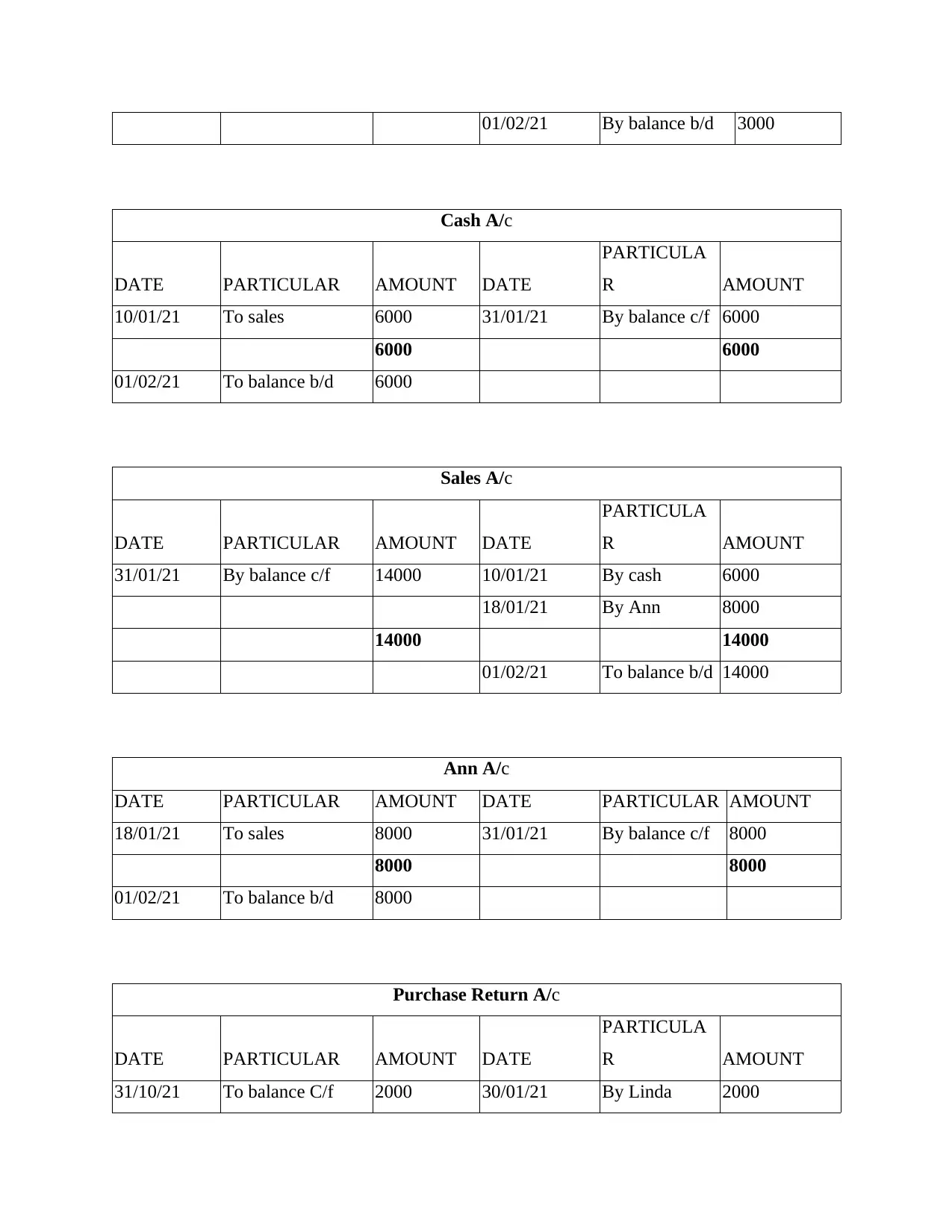

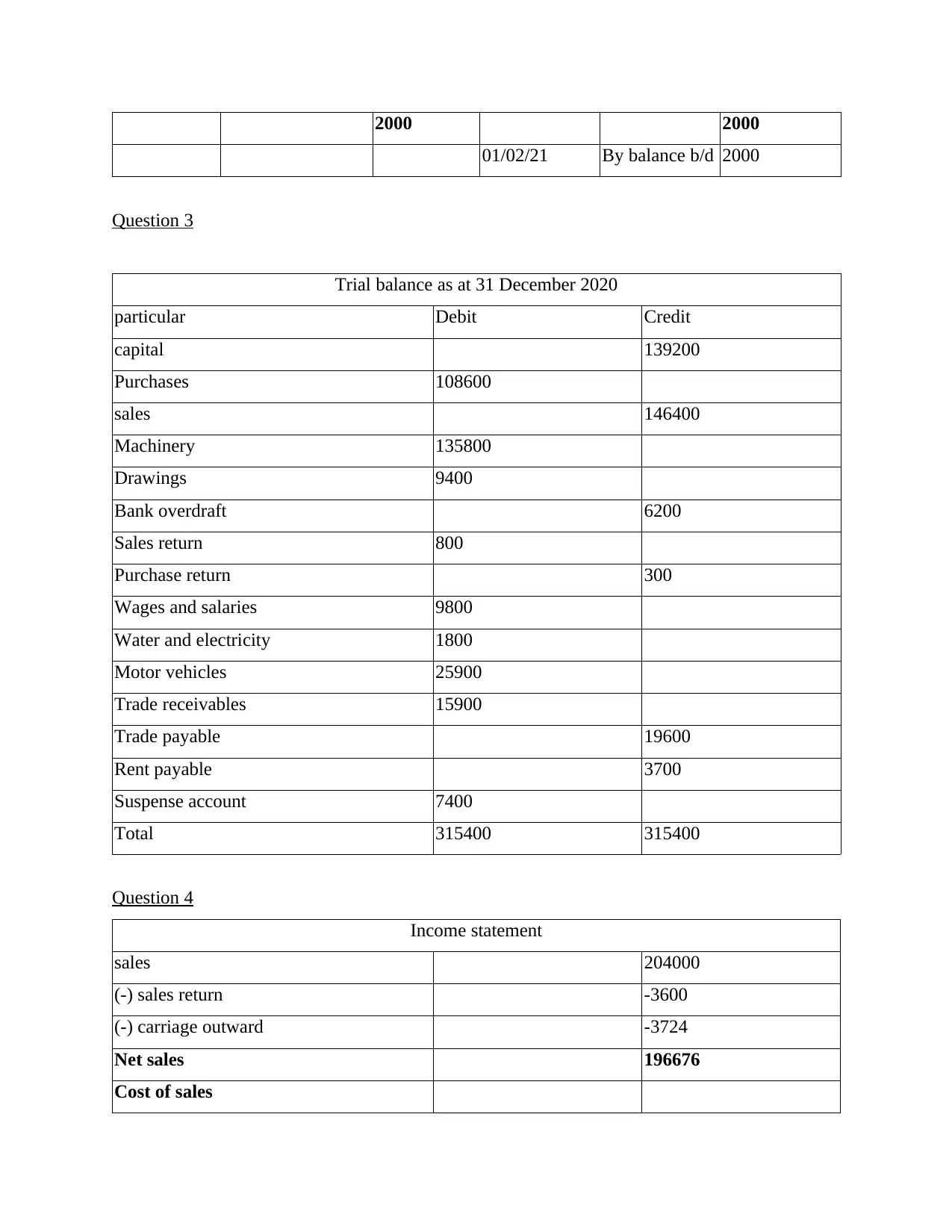

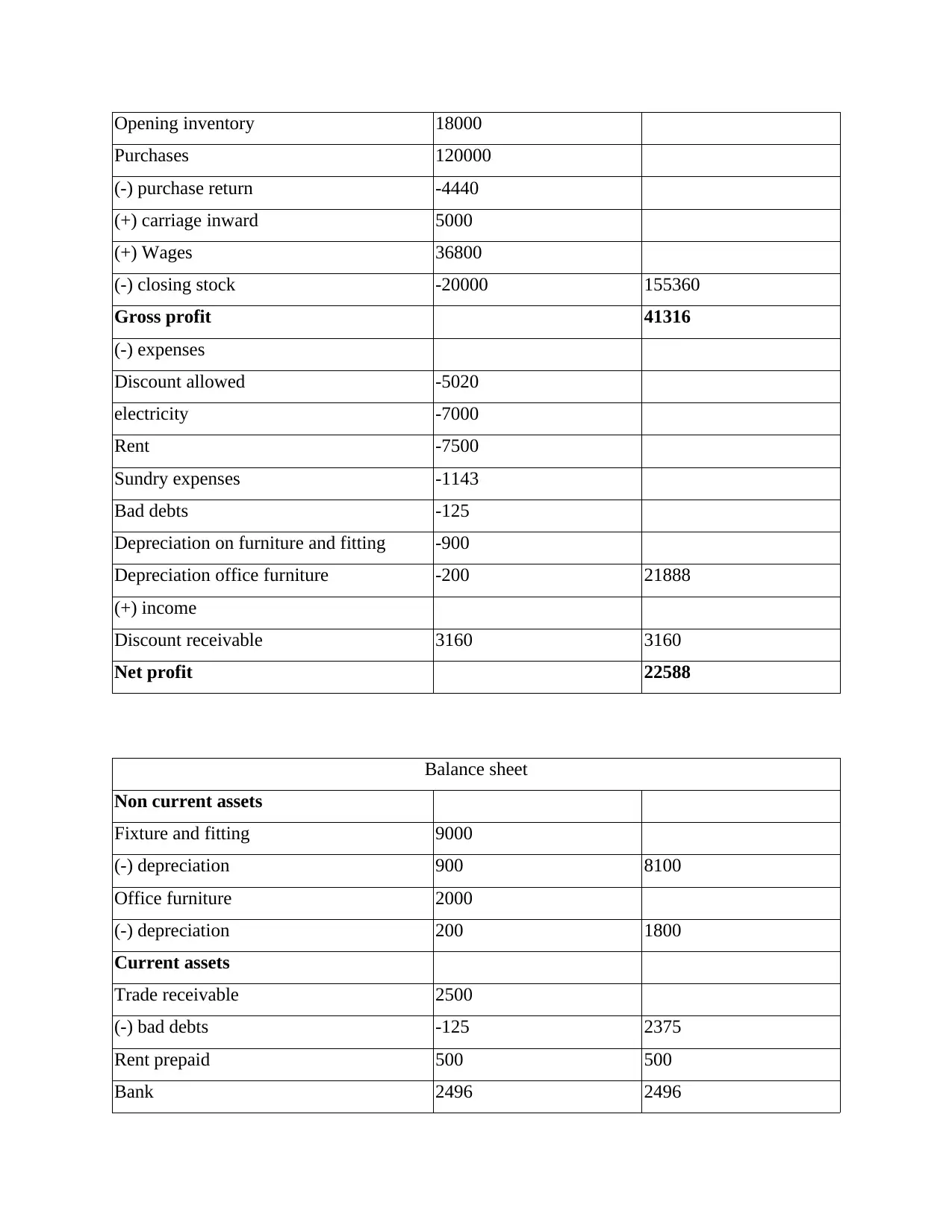

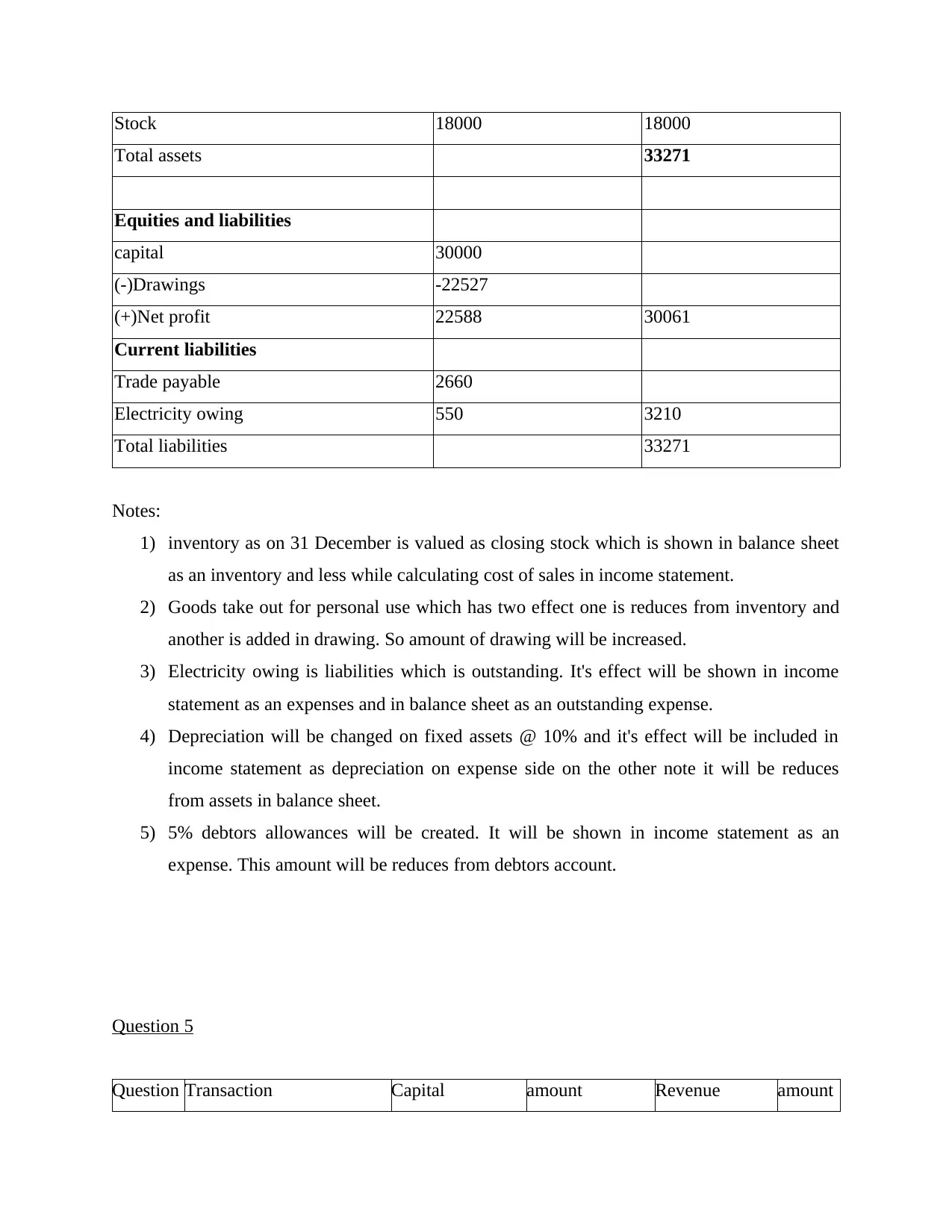

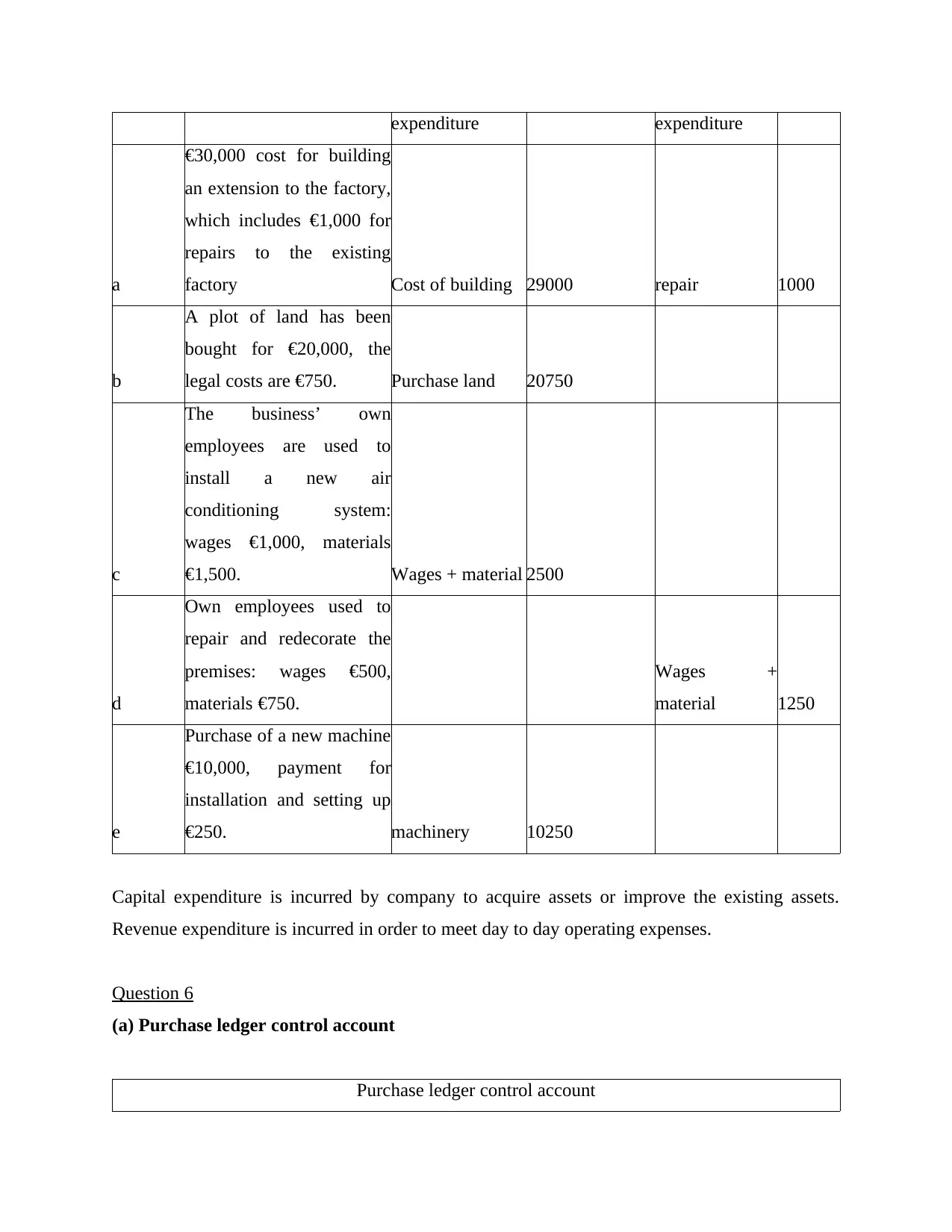

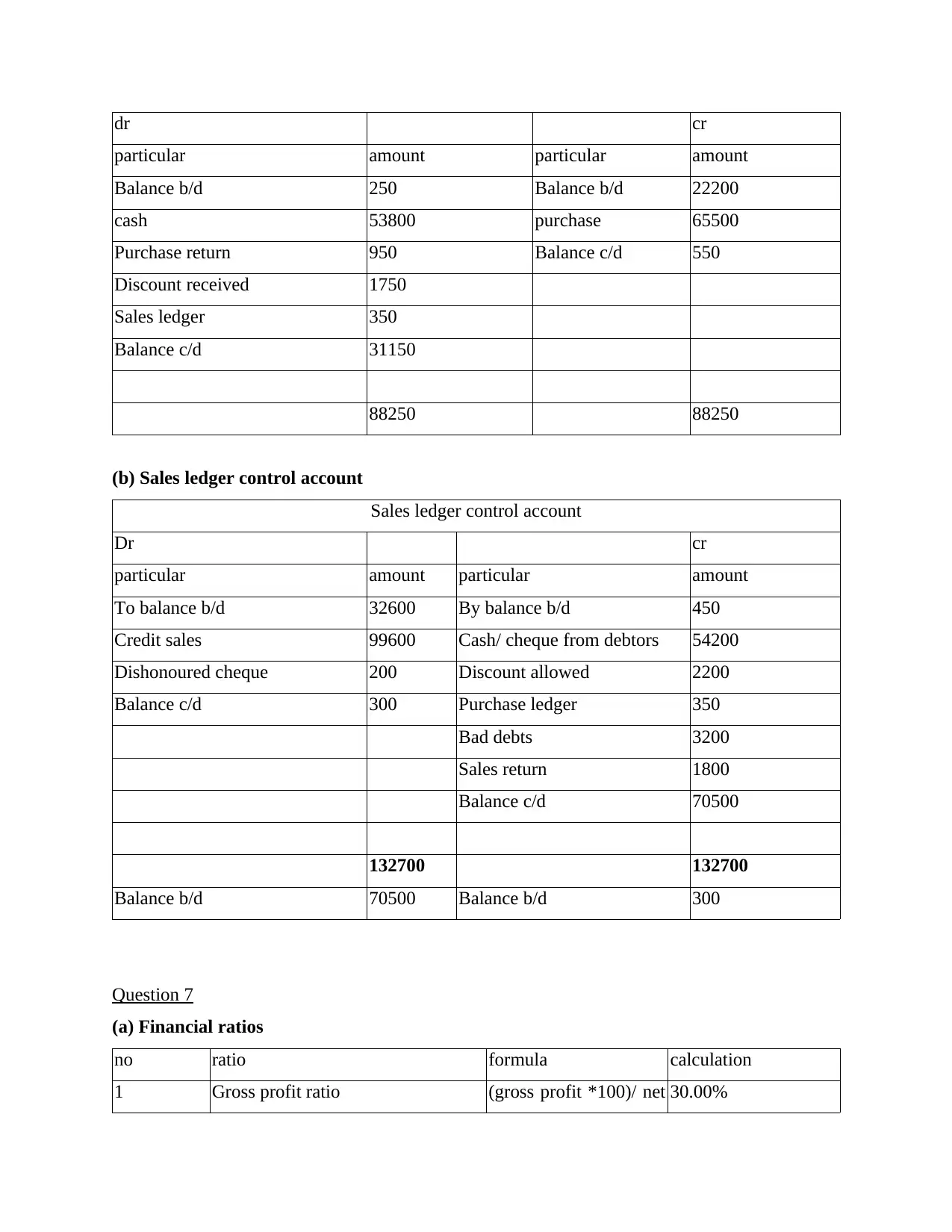

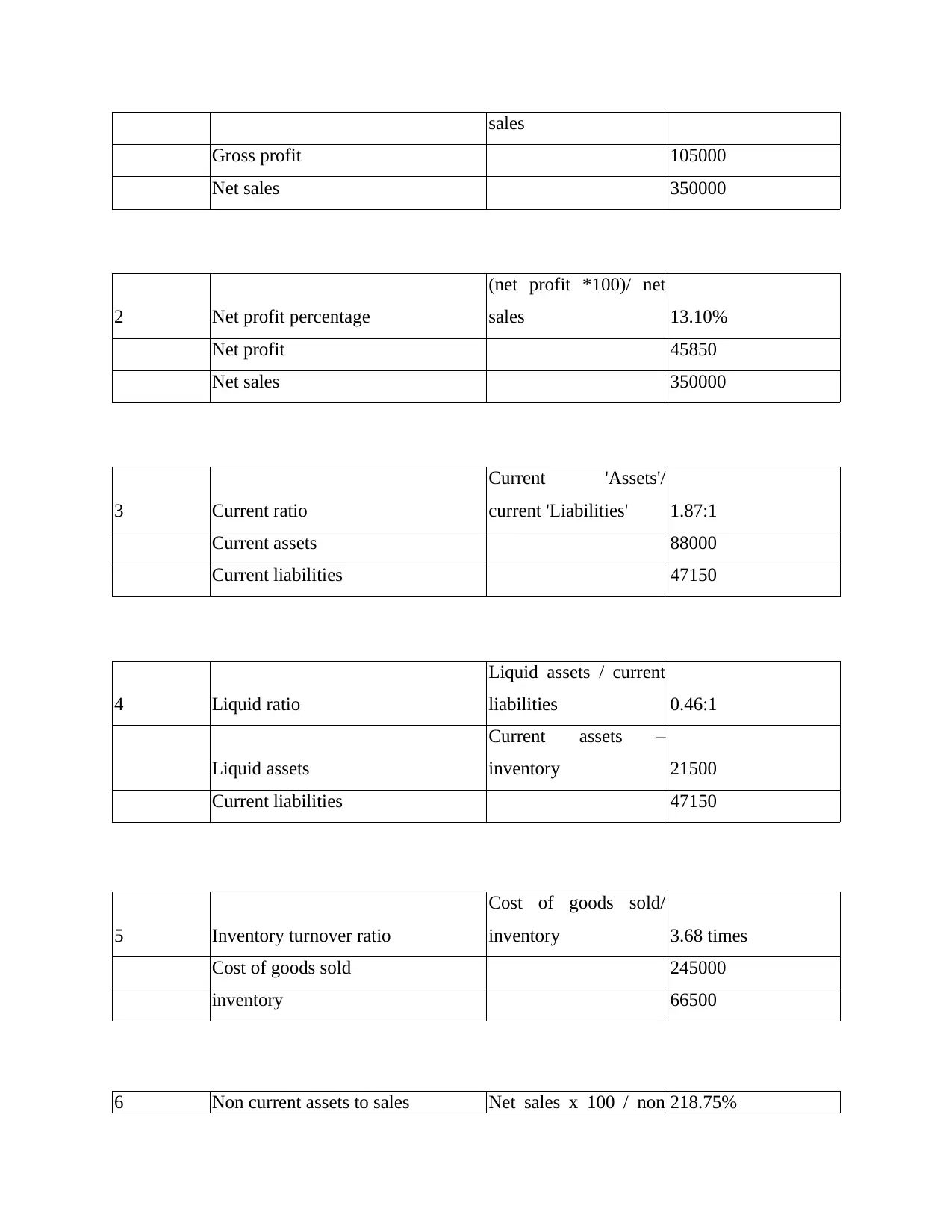

This assignment solution covers various aspects of business accounting, including the calculation of missing figures using the accounting equation, journal entries, ledger postings, and the preparation of a trial balance. It also includes the preparation of an income statement and balance sheet, along with notes on inventory valuation, goods taken for personal use, electricity owing, depreciation, and debtors' allowances. Further, it discusses the difference between capital and revenue expenditure. The solution also covers the preparation of purchase and sales ledger control accounts and calculates various financial ratios to analyze business performance. Finally, it includes payback period and net present value calculations for investment appraisal and discusses the reasons for companies employing accountants, the need for external auditors for limited liability companies, and the benefits of non-accountants studying accounting. Desklib is a platform where students can find a wide array of assignments and study tools to help them excel in their academic pursuits.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.