Business Analysis Assignment Solution - Finance Module, Semester 1

VerifiedAdded on 2020/04/15

|8

|1185

|38

Homework Assignment

AI Summary

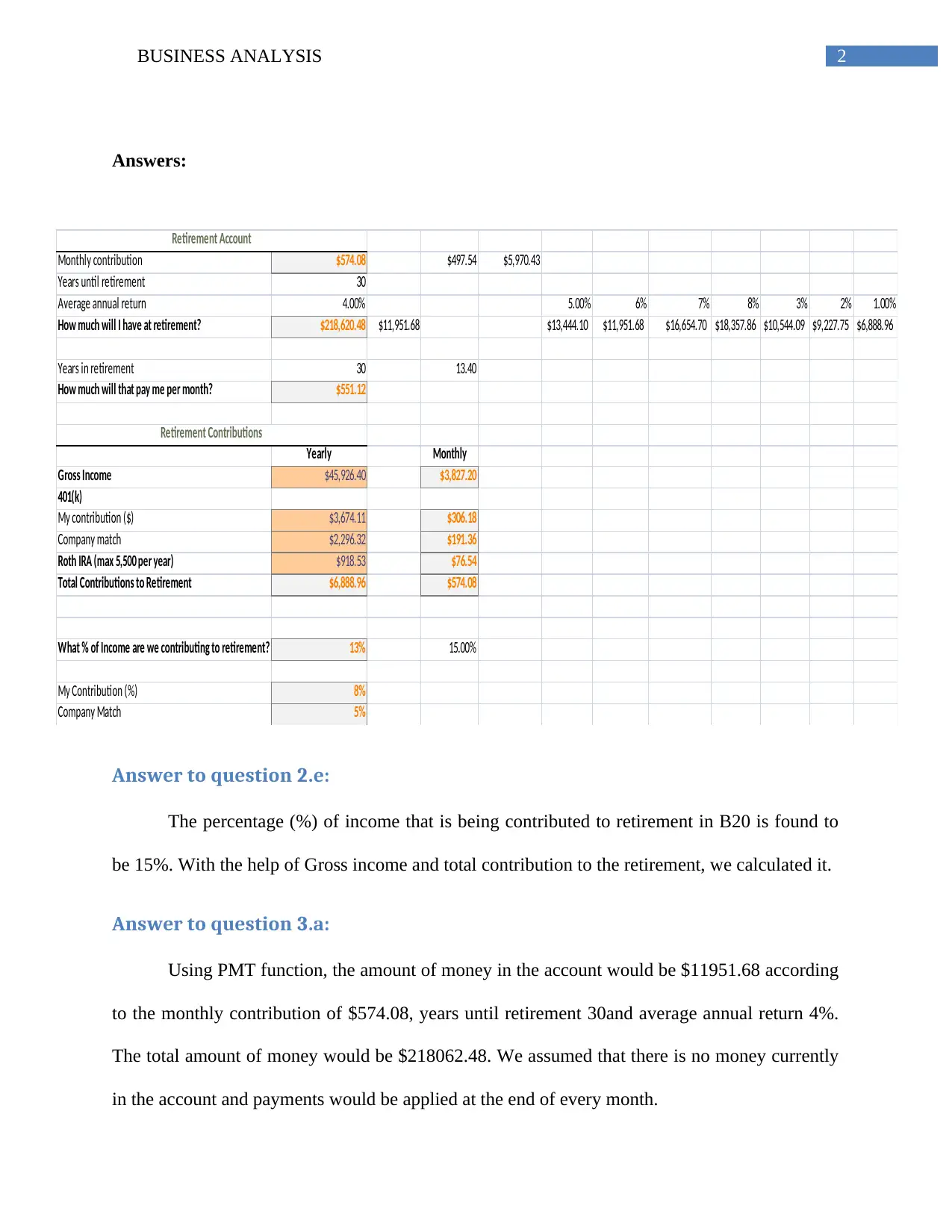

This document presents a comprehensive solution to a business analysis assignment focused on personal finance and retirement planning. The solution includes detailed answers to questions concerning retirement contributions, utilizing the PMT function in Excel to calculate future values and monthly payments. The assignment explores different scenarios by varying annual return rates to demonstrate their impact on retirement savings. Furthermore, it analyzes the impact of different contribution rates and retirement timelines. The solution highlights key concepts such as company match and the importance of understanding Excel functions for financial planning. The assignment also includes an annotated bibliography with relevant academic sources, providing a foundation for the analysis. The student demonstrates an understanding of financial concepts, applying them practically to a retirement plan scenario.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.