MIS775: Investment Portfolio Optimisation with Decision Models

VerifiedAdded on 2022/09/22

Analytics

Investment Portfolio Optimisation

Group No:

Paraphrase This Document

• Objective: Evaluation of different approaches to

optimisation of portfolio subject to constraints using

different models namely:

(a) Linear Programming Model

(b)Integer Linear Programming Model

(c) Non-Linear Programming Model.

• For the purpose of this assignment, group members have

identified 10 assets across 5 different categories.

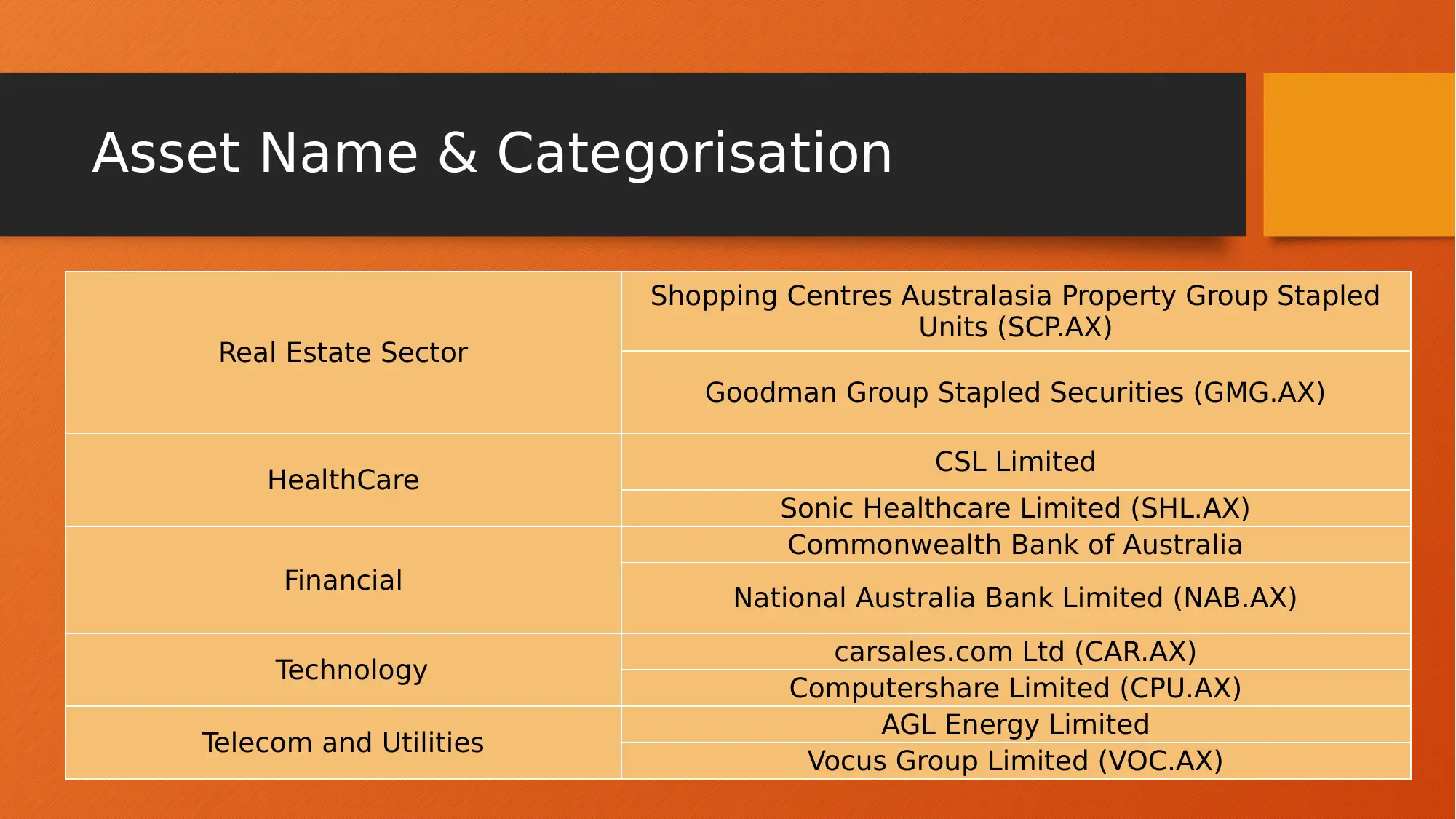

Real Estate Sector

Shopping Centres Australasia Property Group Stapled

Units (SCP.AX)

Goodman Group Stapled Securities (GMG.AX)

HealthCare CSL Limited

Sonic Healthcare Limited (SHL.AX)

Financial

Commonwealth Bank of Australia

National Australia Bank Limited (NAB.AX)

Technology carsales.com Ltd (CAR.AX)

Computershare Limited (CPU.AX)

Telecom and Utilities AGL Energy Limited

Vocus Group Limited (VOC.AX)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

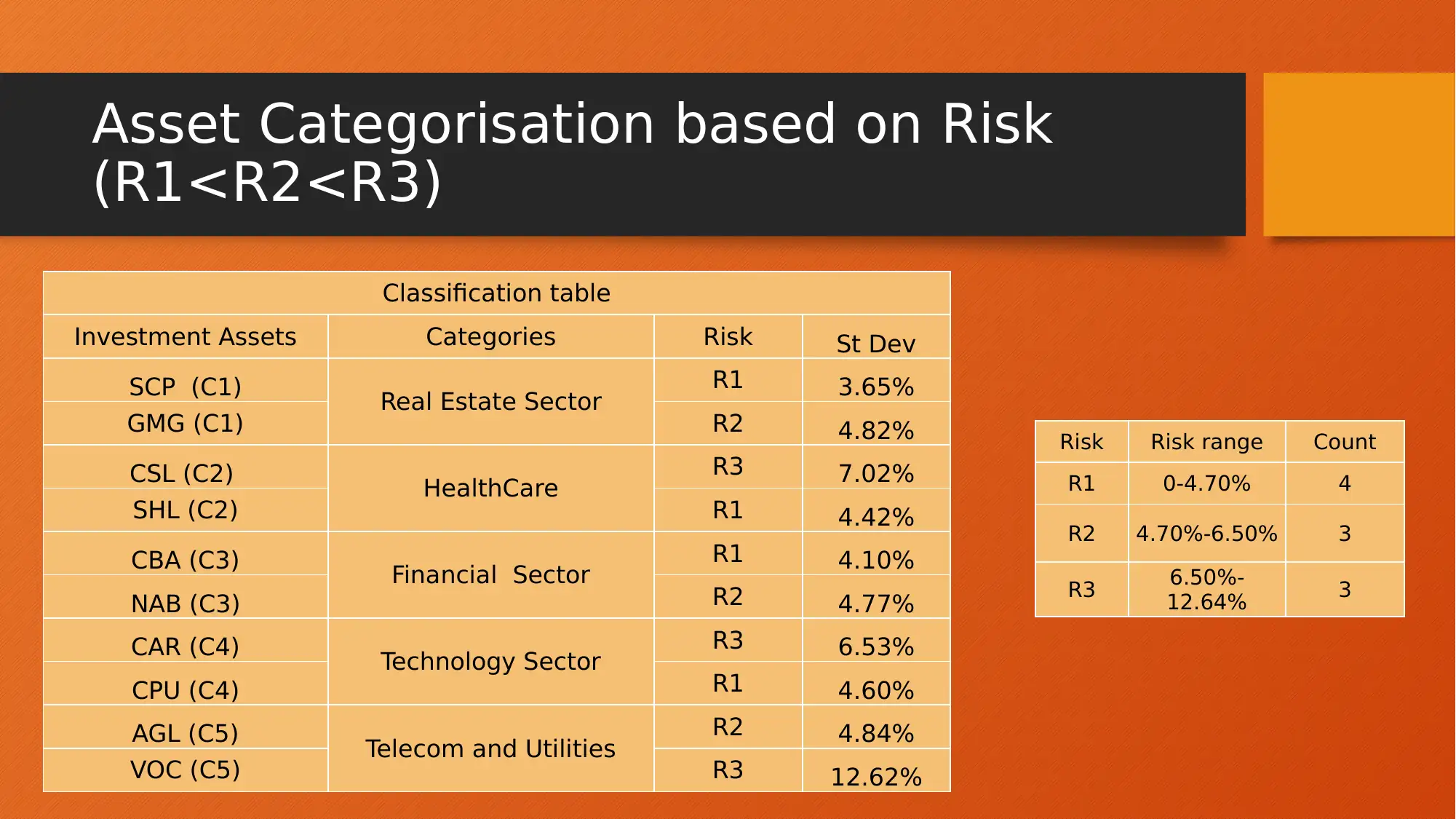

(R1<R2<R3)

Classification table

Investment Assets Categories Risk St Dev

SCP (C1) Real Estate Sector R1 3.65%

GMG (C1) R2 4.82%

CSL (C2) HealthCare R3 7.02%

SHL (C2) R1 4.42%

CBA (C3) Financial Sector R1 4.10%

NAB (C3) R2 4.77%

CAR (C4) Technology Sector R3 6.53%

CPU (C4) R1 4.60%

AGL (C5) Telecom and Utilities R2 4.84%

VOC (C5) R3 12.62%

Risk Risk range Count

R1 0-4.70% 4

R2 4.70%-6.50% 3

R3 6.50%-

12.64% 3

Paraphrase This Document

• The financial stock values for each of these 10 assets were collected over a period of 37

months

• Using this data we calculated the following:

(a) Average and monthly returns for each stock

(b) Average and monthly risk associated with each stock

(c) Average annual return for each stock

• In addition to this, all assets chosen satisfy the following general constraints:

(a) 37 months of data should be collected for each of these assets up to and including

Feb 2020.

(b) The assets should be selected from 5 different categories and there should 2 assets

in each category.

(c)These assets must span a reasonable range of risks and must be classified into 3 risk

groups (R1, R2, R3), with R1 being the least volatile and R4 being the most volatile.

(d) Each risk group must contains at least 3 assets.

Objective & Constraint

Constraints

Total Weight = 100%

Technology <= 20%

Real Estate <= 25%

Health = 10%

Financial <= 30%

Telcom ≤ 30%

R1 <= 20%

R2 <= 15%

R3 >= 10%

Objective: Maximisation of return of portfolio subject to constraint stated

here-in-below

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

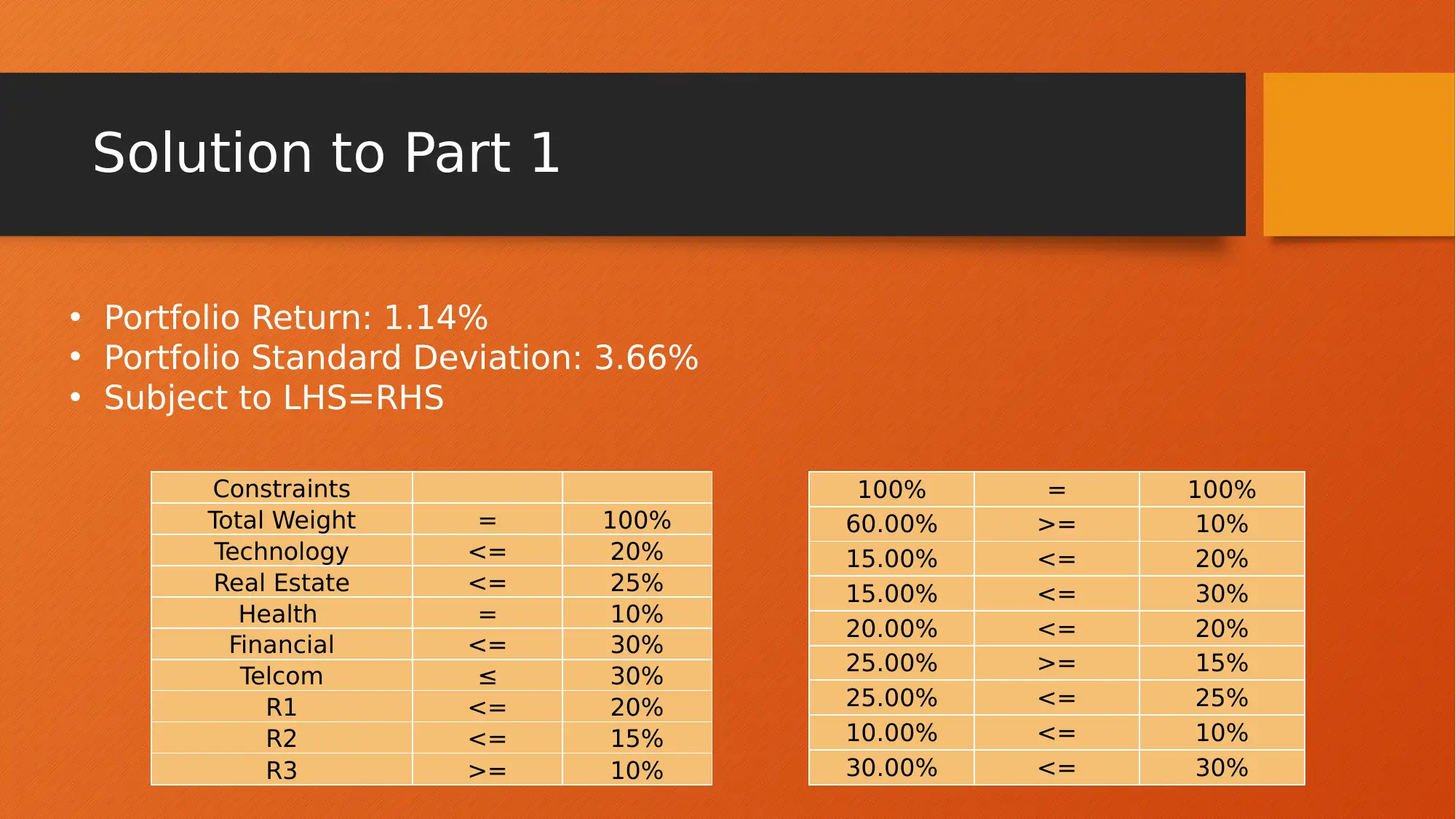

• Portfolio Return: 1.14%

• Portfolio Standard Deviation: 3.66%

• Subject to LHS=RHS

100% = 100%

60.00% >= 10%

15.00% <= 20%

15.00% <= 30%

20.00% <= 20%

25.00% >= 15%

25.00% <= 25%

10.00% <= 10%

30.00% <= 30%

Constraints

Total Weight = 100%

Technology <= 20%

Real Estate <= 25%

Health = 10%

Financial <= 30%

Telcom ≤ 30%

R1 <= 20%

R2 <= 15%

R3 >= 10%

Paraphrase This Document

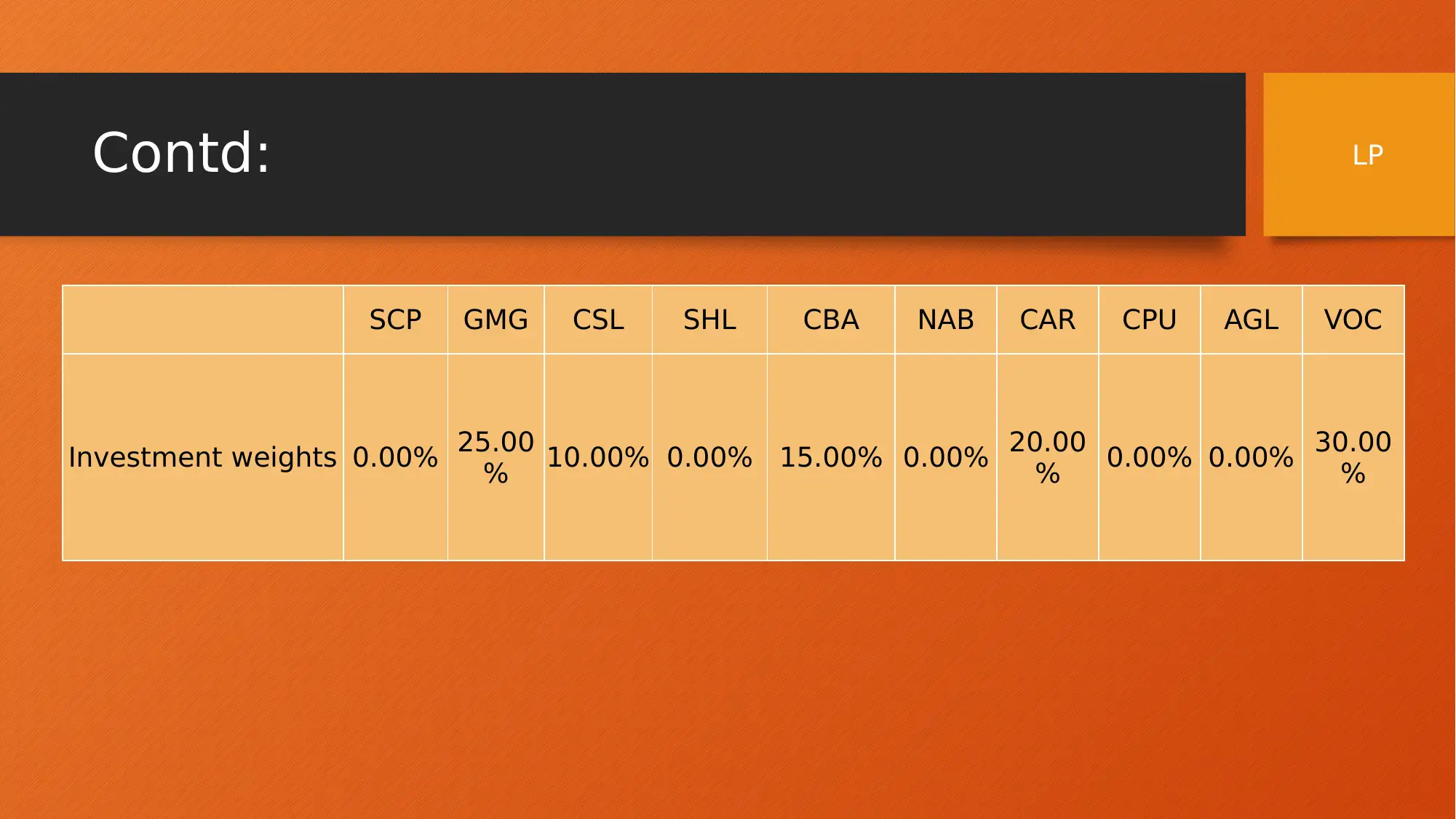

SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Investment weights 0.00% 25.00

% 10.00% 0.00% 15.00% 0.00% 20.00

% 0.00% 0.00% 30.00

%

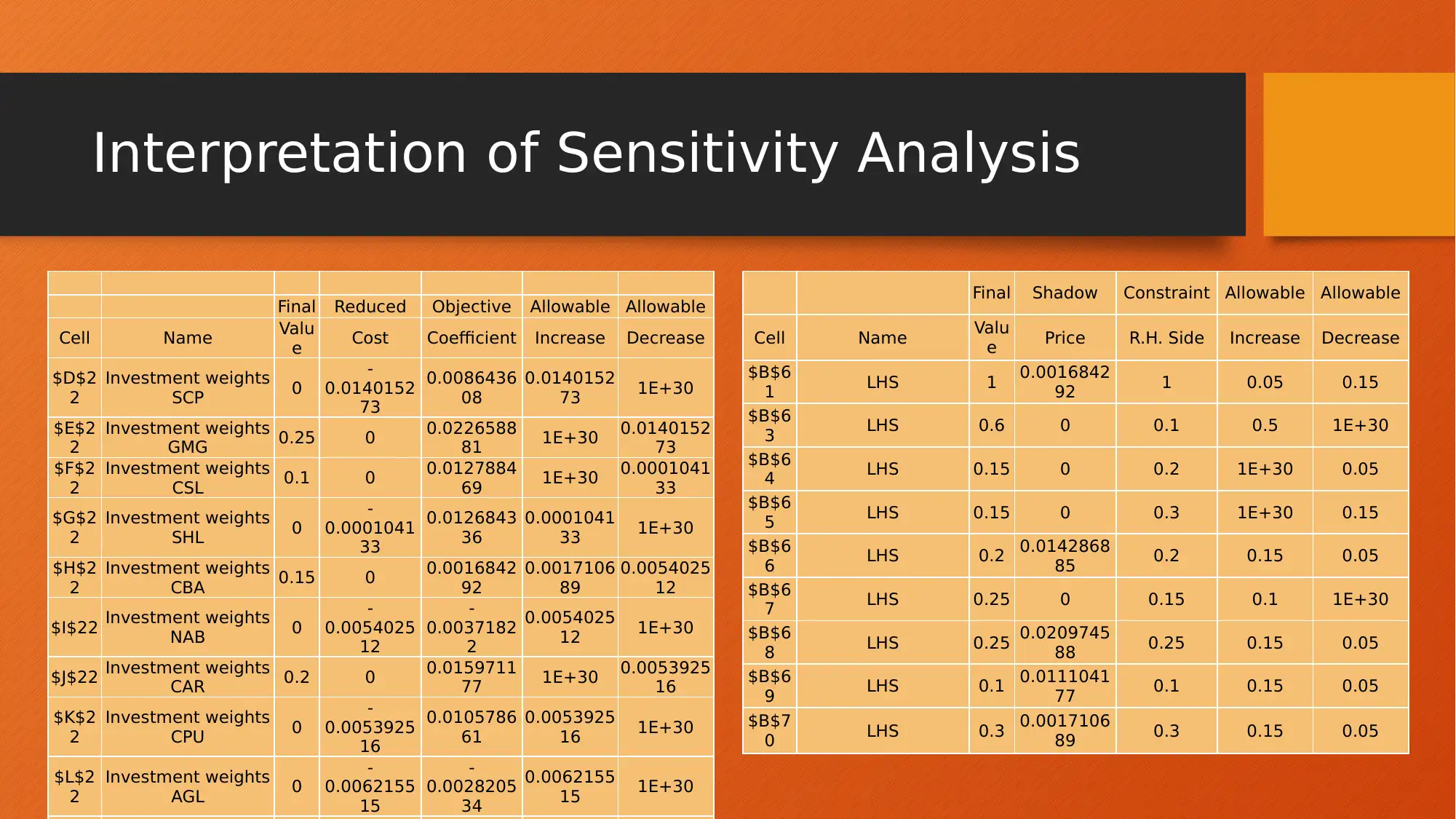

LP

Final Reduced Objective Allowable Allowable

Cell Name Valu

e Cost Coefficient Increase Decrease

$D$2

2

Investment weights

SCP 0

-

0.0140152

73

0.0086436

08

0.0140152

73 1E+30

$E$2

2

Investment weights

GMG 0.25 0 0.0226588

81 1E+30 0.0140152

73

$F$2

2

Investment weights

CSL 0.1 0 0.0127884

69 1E+30 0.0001041

33

$G$2

2

Investment weights

SHL 0

-

0.0001041

33

0.0126843

36

0.0001041

33 1E+30

$H$2

2

Investment weights

CBA 0.15 0 0.0016842

92

0.0017106

89

0.0054025

12

$I$22 Investment weights

NAB 0

-

0.0054025

12

-

0.0037182

2

0.0054025

12 1E+30

$J$22 Investment weights

CAR 0.2 0 0.0159711

77 1E+30 0.0053925

16

$K$2

2

Investment weights

CPU 0

-

0.0053925

16

0.0105786

61

0.0053925

16 1E+30

$L$2

2

Investment weights

AGL 0

-

0.0062155

15

-

0.0028205

34

0.0062155

15 1E+30

Final Shadow Constraint Allowable Allowable

Cell Name Valu

e Price R.H. Side Increase Decrease

$B$6

1 LHS 1 0.0016842

92 1 0.05 0.15

$B$6

3 LHS 0.6 0 0.1 0.5 1E+30

$B$6

4 LHS 0.15 0 0.2 1E+30 0.05

$B$6

5 LHS 0.15 0 0.3 1E+30 0.15

$B$6

6 LHS 0.2 0.0142868

85 0.2 0.15 0.05

$B$6

7 LHS 0.25 0 0.15 0.1 1E+30

$B$6

8 LHS 0.25 0.0209745

88 0.25 0.15 0.05

$B$6

9 LHS 0.1 0.0111041

77 0.1 0.15 0.05

$B$7

0 LHS 0.3 0.0017106

89 0.3 0.15 0.05

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• On perusal of the above tables, it may be inferred that the there is allowable increase

for five assets in the portfolio and allowable decrease of five asset in the portfolio.

• Further, the reduction in each of the asset has been duly shown to achieve the desired

portfolio.

• Probable increase or decrease in constraint which can impact the return of the portfolio

like allowable increase for weights is 0.05 (increase) to 0.15 (decrease)

• Similarly, Investment in R3 cannot be exceeded further.

• For R2 it has been stated that allowable increase of 0.5 is permitted and so on.

Paraphrase This Document

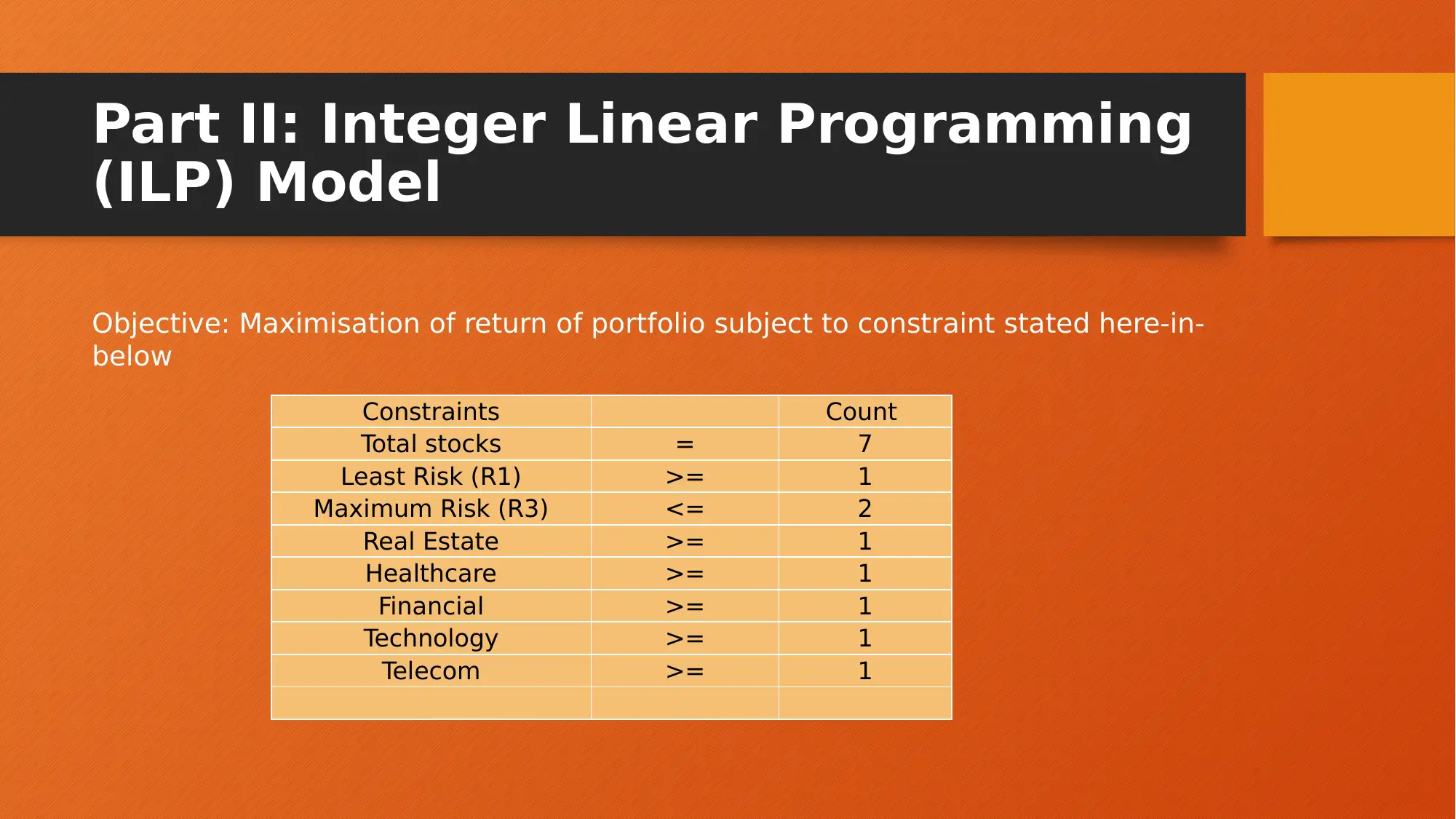

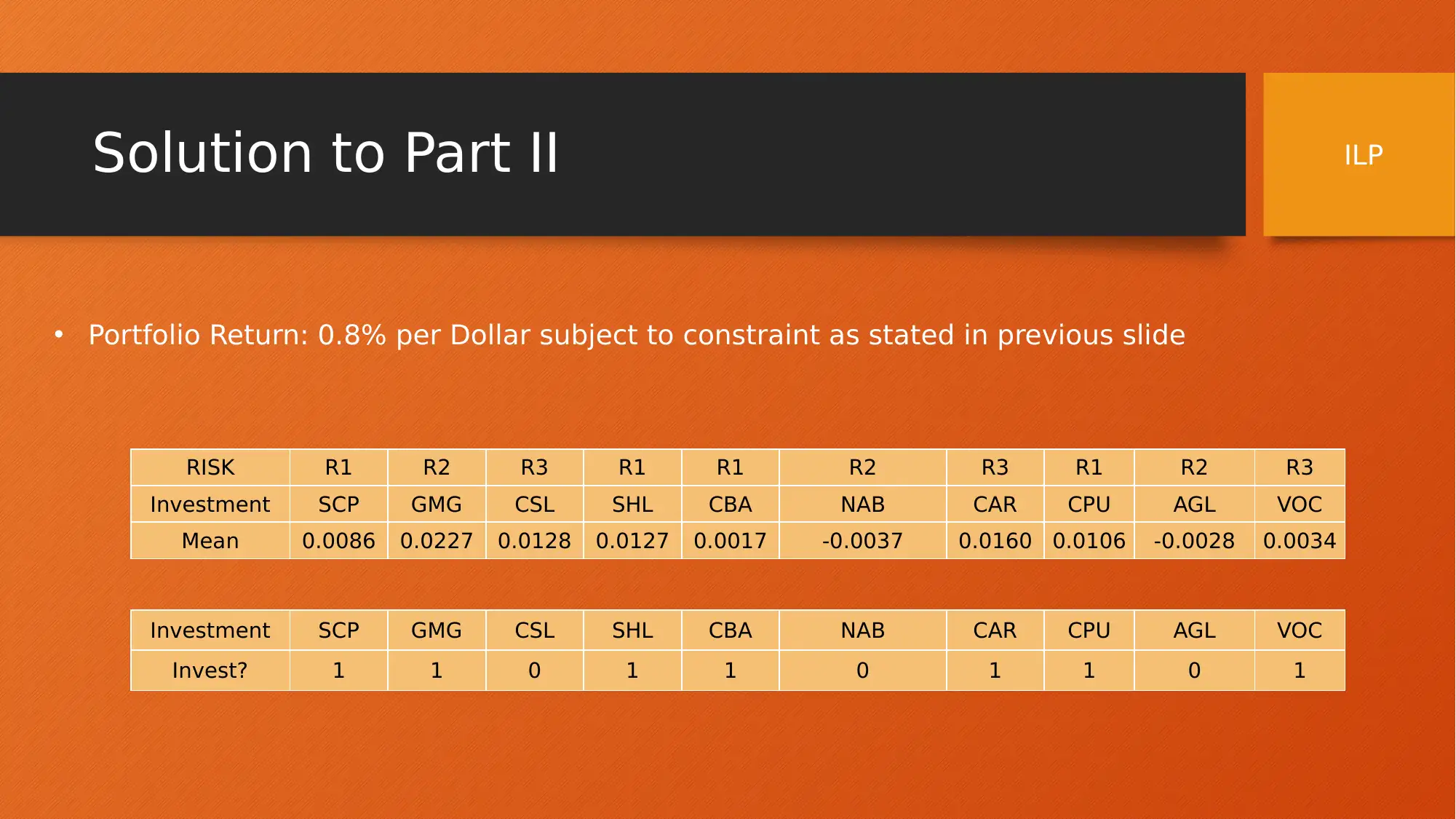

(ILP) Model

Objective: Maximisation of return of portfolio subject to constraint stated here-in-

below

Constraints Count

Total stocks = 7

Least Risk (R1) >= 1

Maximum Risk (R3) <= 2

Real Estate >= 1

Healthcare >= 1

Financial >= 1

Technology >= 1

Telecom >= 1

• Portfolio Return: 0.8% per Dollar subject to constraint as stated in previous slide

RISK R1 R2 R3 R1 R1 R2 R3 R1 R2 R3

Investment SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Mean 0.0086 0.0227 0.0128 0.0127 0.0017 -0.0037 0.0160 0.0106 -0.0028 0.0034

Investment SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Invest? 1 1 0 1 1 0 1 1 0 1

ILP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

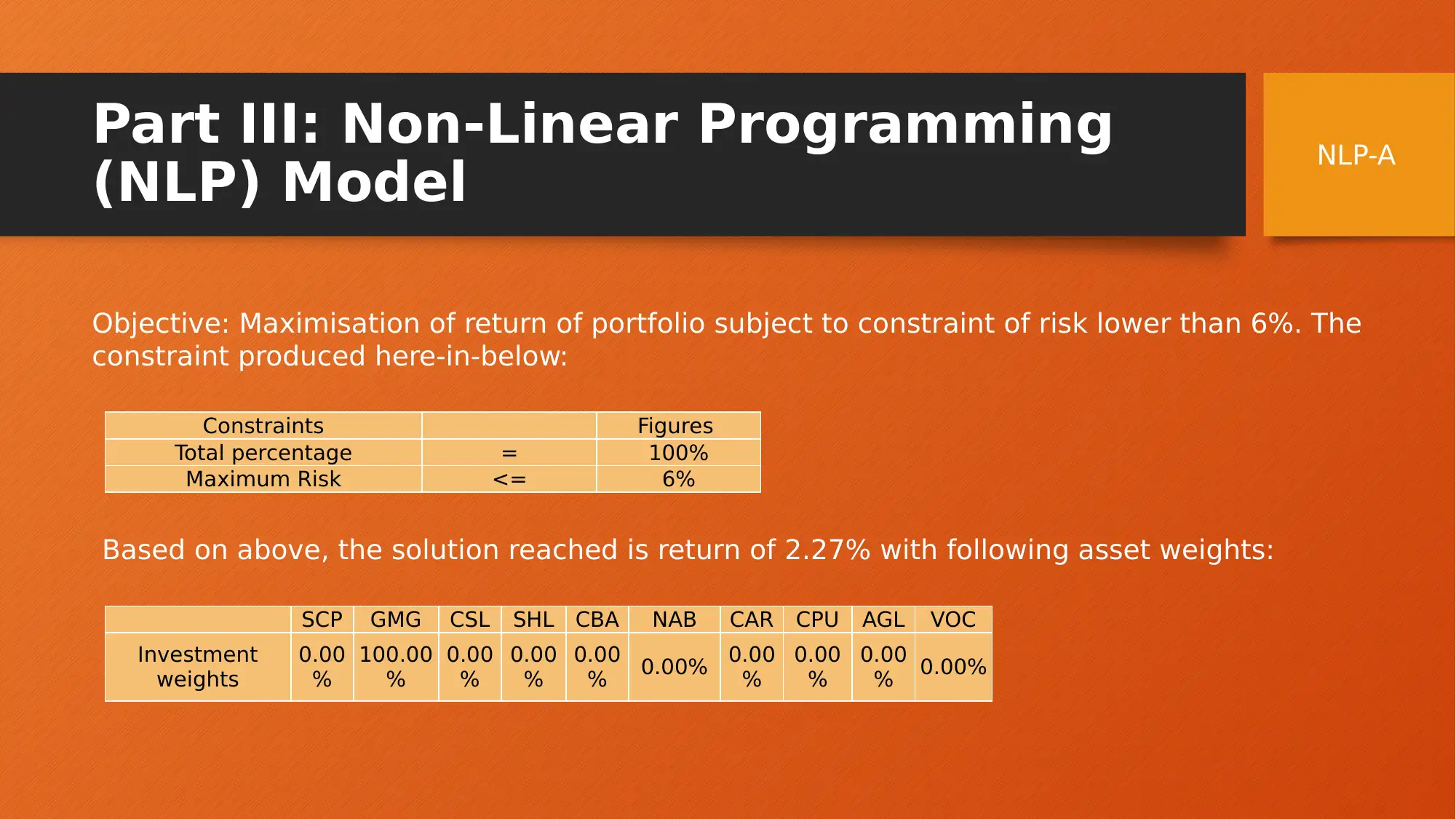

(NLP) Model

Objective: Maximisation of return of portfolio subject to constraint of risk lower than 6%. The

constraint produced here-in-below:

Constraints Figures

Total percentage = 100%

Maximum Risk <= 6%

Based on above, the solution reached is return of 2.27% with following asset weights:

SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Investment

weights

0.00

%

100.00

%

0.00

%

0.00

%

0.00

% 0.00% 0.00

%

0.00

%

0.00

% 0.00%

NLP-A

Paraphrase This Document

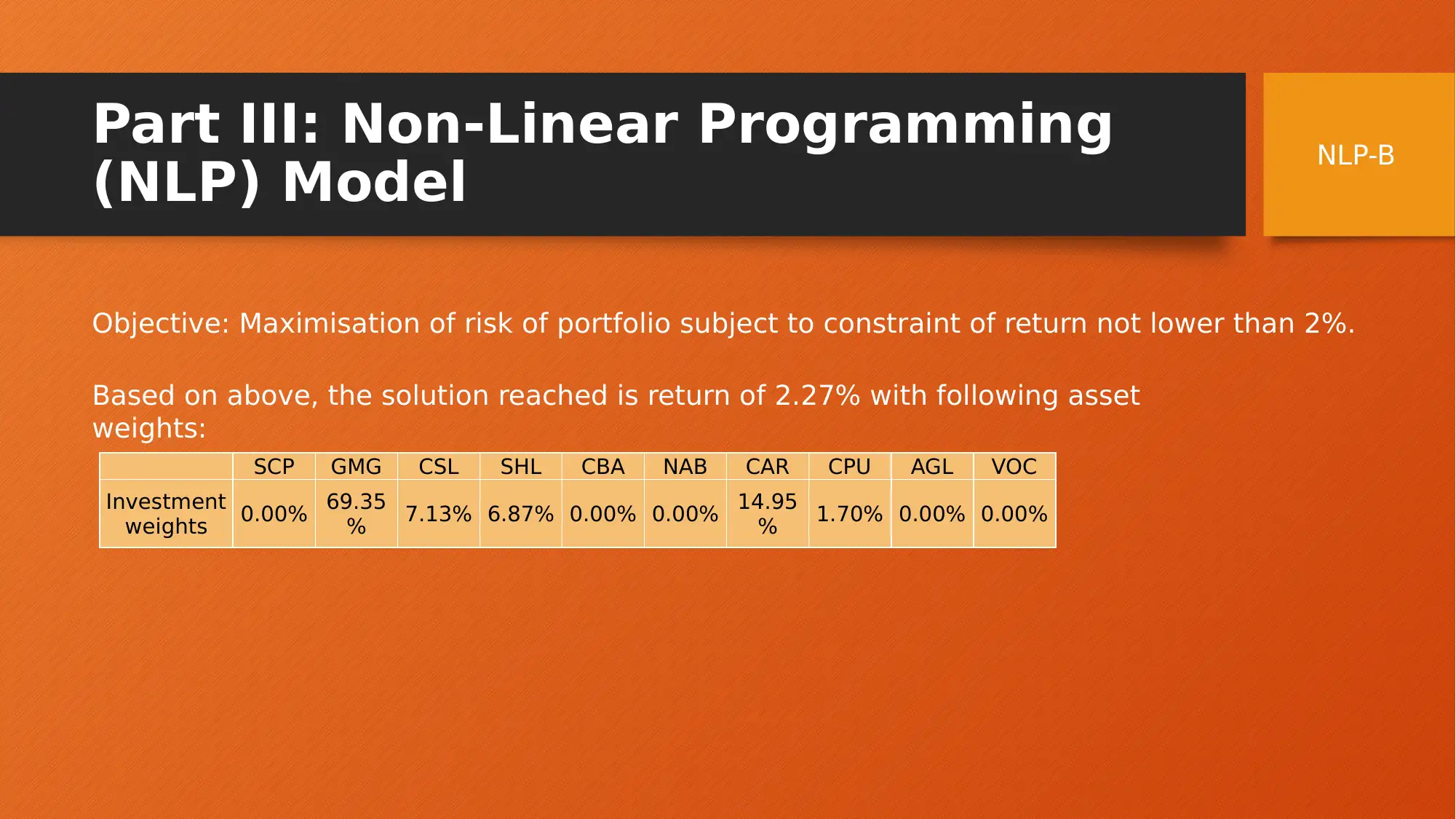

(NLP) Model

Objective: Maximisation of risk of portfolio subject to constraint of return not lower than 2%.

Based on above, the solution reached is return of 2.27% with following asset

weights:

SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Investment

weights 0.00% 69.35

% 7.13% 6.87% 0.00% 0.00% 14.95

% 1.70% 0.00% 0.00%

NLP-B

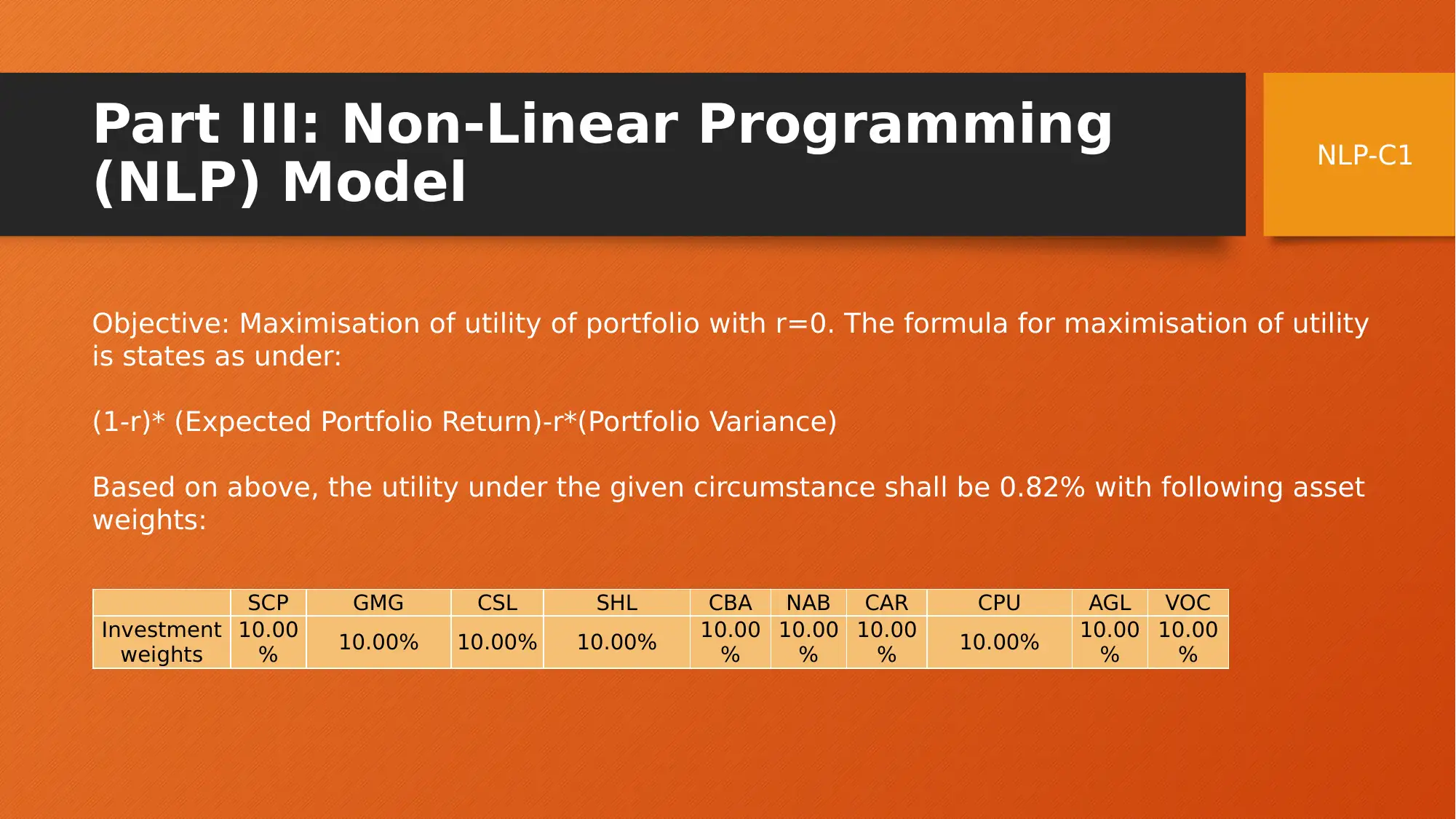

(NLP) Model

Objective: Maximisation of utility of portfolio with r=0. The formula for maximisation of utility

is states as under:

(1-r)* (Expected Portfolio Return)-r*(Portfolio Variance)

Based on above, the utility under the given circumstance shall be 0.82% with following asset

weights:

SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Investment

weights

10.00

% 10.00% 10.00% 10.00% 10.00

%

10.00

%

10.00

% 10.00% 10.00

%

10.00

%

NLP-C1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

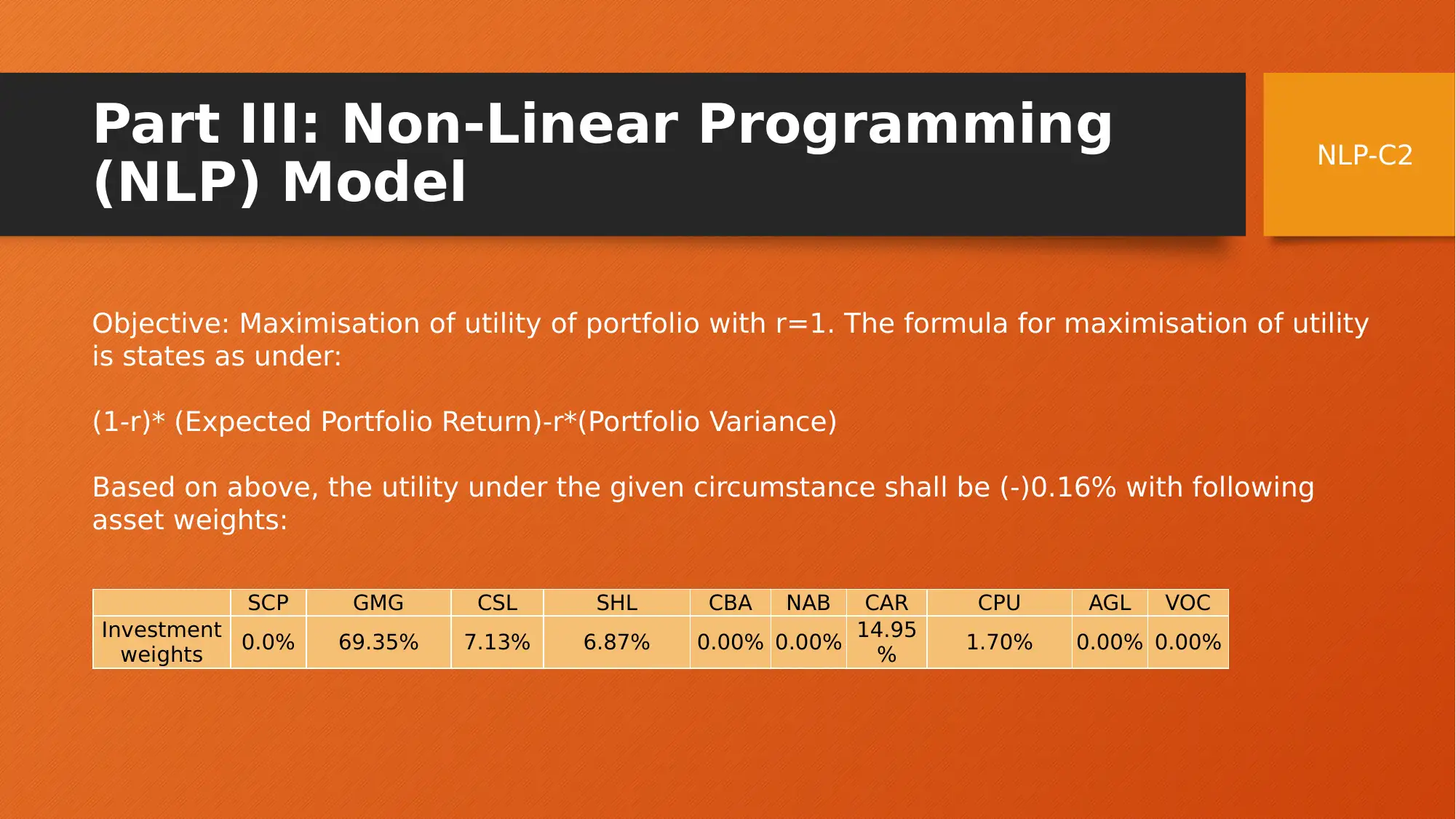

(NLP) Model

Objective: Maximisation of utility of portfolio with r=1. The formula for maximisation of utility

is states as under:

(1-r)* (Expected Portfolio Return)-r*(Portfolio Variance)

Based on above, the utility under the given circumstance shall be (-)0.16% with following

asset weights:

SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Investment

weights 0.0% 69.35% 7.13% 6.87% 0.00% 0.00% 14.95

% 1.70% 0.00% 0.00%

NLP-C2

Paraphrase This Document

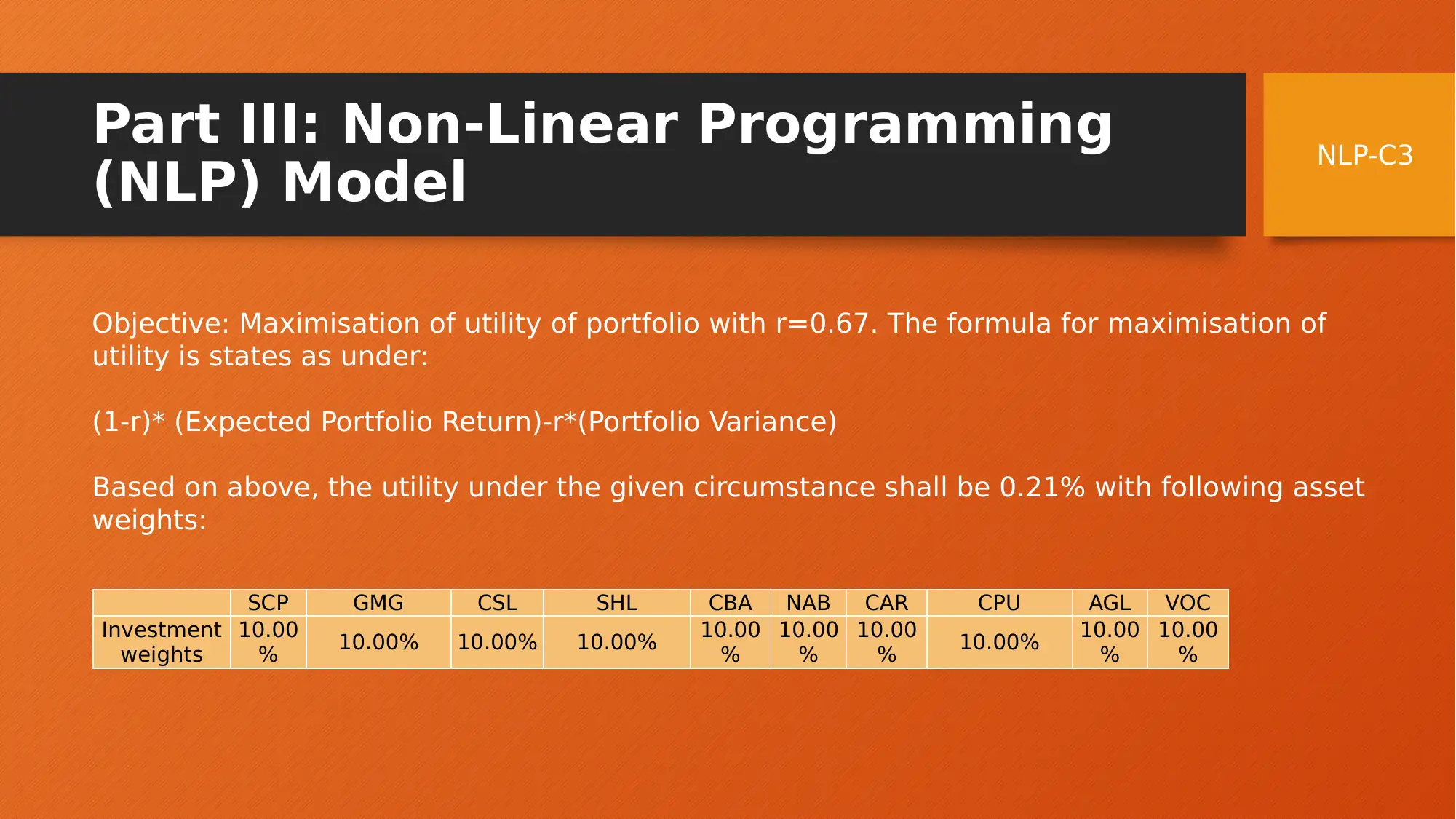

(NLP) Model

Objective: Maximisation of utility of portfolio with r=0.67. The formula for maximisation of

utility is states as under:

(1-r)* (Expected Portfolio Return)-r*(Portfolio Variance)

Based on above, the utility under the given circumstance shall be 0.21% with following asset

weights:

SCP GMG CSL SHL CBA NAB CAR CPU AGL VOC

Investment

weights

10.00

% 10.00% 10.00% 10.00% 10.00

%

10.00

%

10.00

% 10.00% 10.00

%

10.00

%

NLP-C3

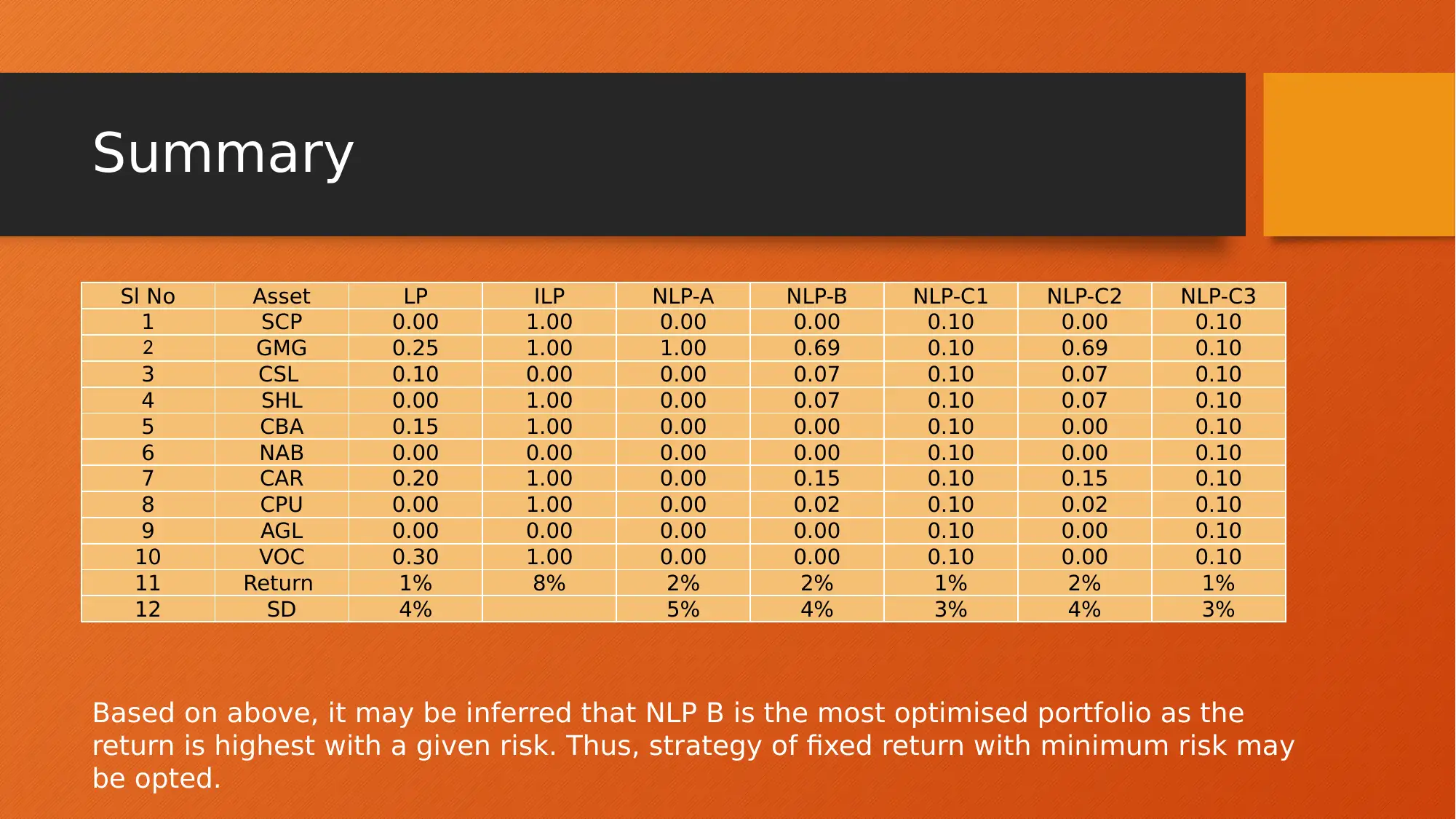

Sl No Asset LP ILP NLP-A NLP-B NLP-C1 NLP-C2 NLP-C3

1 SCP 0.00 1.00 0.00 0.00 0.10 0.00 0.10

2 GMG 0.25 1.00 1.00 0.69 0.10 0.69 0.10

3 CSL 0.10 0.00 0.00 0.07 0.10 0.07 0.10

4 SHL 0.00 1.00 0.00 0.07 0.10 0.07 0.10

5 CBA 0.15 1.00 0.00 0.00 0.10 0.00 0.10

6 NAB 0.00 0.00 0.00 0.00 0.10 0.00 0.10

7 CAR 0.20 1.00 0.00 0.15 0.10 0.15 0.10

8 CPU 0.00 1.00 0.00 0.02 0.10 0.02 0.10

9 AGL 0.00 0.00 0.00 0.00 0.10 0.00 0.10

10 VOC 0.30 1.00 0.00 0.00 0.10 0.00 0.10

11 Return 1% 8% 2% 2% 1% 2% 1%

12 SD 4% 5% 4% 3% 4% 3%

Based on above, it may be inferred that NLP B is the most optimised portfolio as the

return is highest with a given risk. Thus, strategy of fixed return with minimum risk may

be opted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.