Business Analytics Report: CF Ltd's Financial Performance Analysis

VerifiedAdded on 2022/11/24

|15

|4637

|147

Report

AI Summary

This business analytics report provides a detailed analysis of CF Ltd's financial performance. It begins with an introduction to business analytics and proceeds to examine the company's cost structure, including fixed and variable costs, and calculates profitability. The report includes a profit an...

BUSINESS ANALYTIC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

QUESTION 1.............................................................................................................................3

QUESTION 2.............................................................................................................................6

Calculation of coefficient of correlation for advertising and sales........................................6

Graphical representation of the data of sales and advertisement expenditure and

interpretation of the pattern....................................................................................................7

Critical analysis of the impact of expenditure on advertisement on the sales of the company

................................................................................................................................................8

Advising marketing manager on gaining competitive advantage by adopting alternative

marketing tactics....................................................................................................................8

QUESTION 3.............................................................................................................................9

a) Calculation of Break-even sales and margin of safety.......................................................9

b) Recommendation on adoption of Plan.............................................................................11

c) Factors that must be consider by Mansleep Plc. management in above case..................11

d) Benefits and Limitations of Break-even model...............................................................11

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION......................................................................................................................3

QUESTION 1.............................................................................................................................3

QUESTION 2.............................................................................................................................6

Calculation of coefficient of correlation for advertising and sales........................................6

Graphical representation of the data of sales and advertisement expenditure and

interpretation of the pattern....................................................................................................7

Critical analysis of the impact of expenditure on advertisement on the sales of the company

................................................................................................................................................8

Advising marketing manager on gaining competitive advantage by adopting alternative

marketing tactics....................................................................................................................8

QUESTION 3.............................................................................................................................9

a) Calculation of Break-even sales and margin of safety.......................................................9

b) Recommendation on adoption of Plan.............................................................................11

c) Factors that must be consider by Mansleep Plc. management in above case..................11

d) Benefits and Limitations of Break-even model...............................................................11

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION

Business analytics is defined as a process of analysing the actual business situation of

the venture. This is all about understanding the analytics of the different business operations

and revenue channels to understand the significance of the business performance. This report

will be detailed assessing the records and operational performance of the CF Ltd. Henceforth,

report will analysis about the costing of company. On the other had the aim of the report is to

analysis the profitability of the organisation. Performance of company will be understood

based on the next five financial years estimated sales. Correlation coefficient will be derived

under this project. Advice will be given over the advertisement expense and the sales of

company. Different areas associated with costing, operations of company will be understand

under this project.

QUESTION 1

(a) Mathematical information

Cost Amount (£)

Fixed cost 80000

Variable cost 130000 (200000 * .65)

Total cost 210000

The cost structure is segregated into fixed cost and variable cost. The fixed cost is an

expense that remains fixed irrespective of the level of operations and functions. This is a level

of costing that is all about keeping the cost level fixed in nature. This cost do never changes.

The variable cost on the other side is a cost structure that keeps on changes based on the level

of operations and production activity entertained. The basic difference between the fixed cost

and variable cost is one cost do change and get influenced with the level of production

activity entertained and the other cost do not face any impact with the level of activity

entertained by the business entity (Pietrzak, Wnuk-Pel and Christauskas, 2020). The fixed

cost derives value at 80000 and the variable cost identified as 130000. Both the type of cost

comprises with the value 210000. This can be stated that the total cost incurred by the

business unit is 210000 for the respective financial year.

(B) Profit and loss for business

Particular Amount (£)

Business analytics is defined as a process of analysing the actual business situation of

the venture. This is all about understanding the analytics of the different business operations

and revenue channels to understand the significance of the business performance. This report

will be detailed assessing the records and operational performance of the CF Ltd. Henceforth,

report will analysis about the costing of company. On the other had the aim of the report is to

analysis the profitability of the organisation. Performance of company will be understood

based on the next five financial years estimated sales. Correlation coefficient will be derived

under this project. Advice will be given over the advertisement expense and the sales of

company. Different areas associated with costing, operations of company will be understand

under this project.

QUESTION 1

(a) Mathematical information

Cost Amount (£)

Fixed cost 80000

Variable cost 130000 (200000 * .65)

Total cost 210000

The cost structure is segregated into fixed cost and variable cost. The fixed cost is an

expense that remains fixed irrespective of the level of operations and functions. This is a level

of costing that is all about keeping the cost level fixed in nature. This cost do never changes.

The variable cost on the other side is a cost structure that keeps on changes based on the level

of operations and production activity entertained. The basic difference between the fixed cost

and variable cost is one cost do change and get influenced with the level of production

activity entertained and the other cost do not face any impact with the level of activity

entertained by the business entity (Pietrzak, Wnuk-Pel and Christauskas, 2020). The fixed

cost derives value at 80000 and the variable cost identified as 130000. Both the type of cost

comprises with the value 210000. This can be stated that the total cost incurred by the

business unit is 210000 for the respective financial year.

(B) Profit and loss for business

Particular Amount (£)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

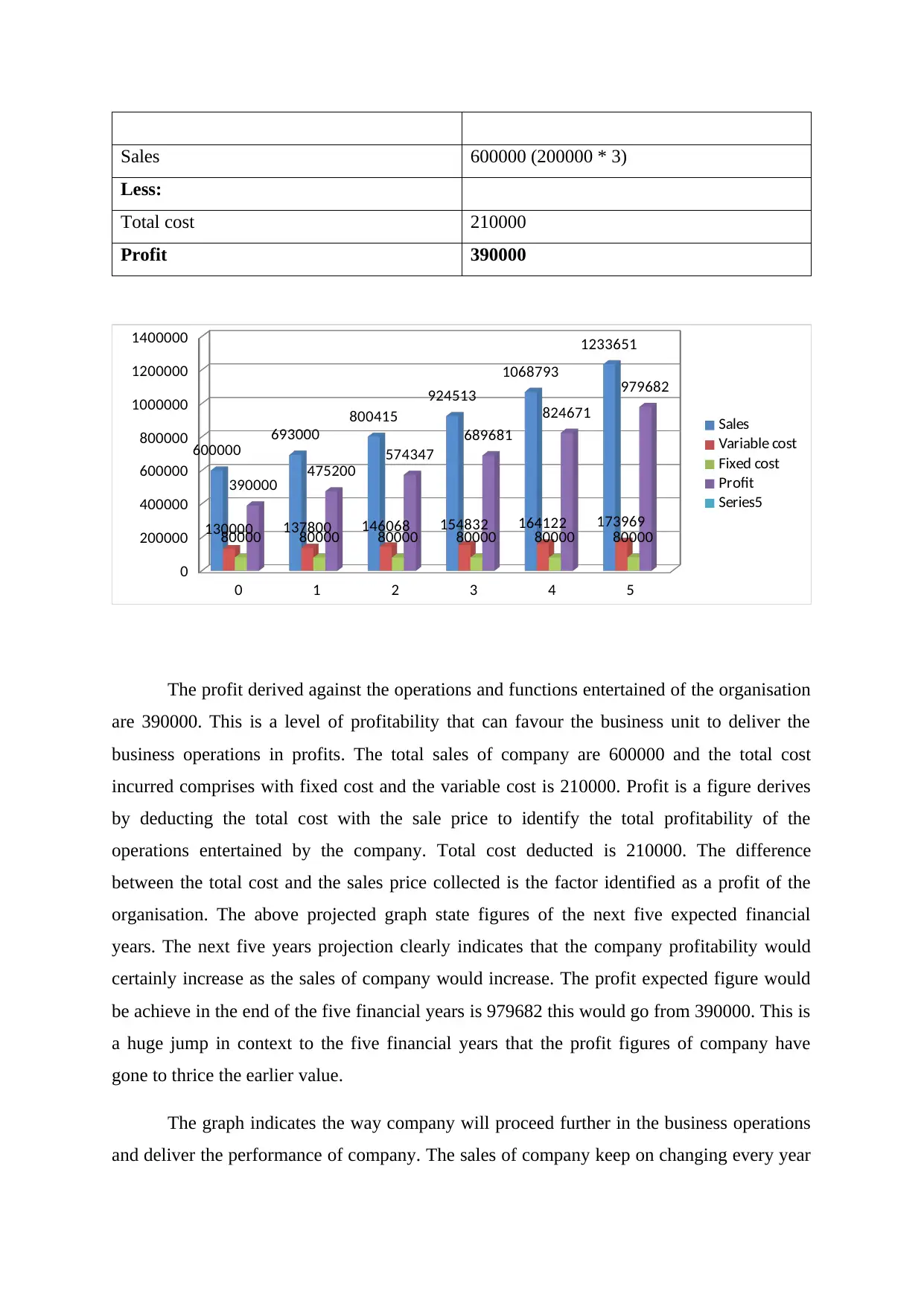

Sales 600000 (200000 * 3)

Less:

Total cost 210000

Profit 390000

0 1 2 3 4 5

0

200000

400000

600000

800000

1000000

1200000

1400000

600000

693000

800415

924513

1068793

1233651

130000 137800 146068 154832 164122 173969

80000 80000 80000 80000 80000 80000

390000 475200

574347

689681

824671

979682

Sales

Variable cost

Fixed cost

Profit

Series5

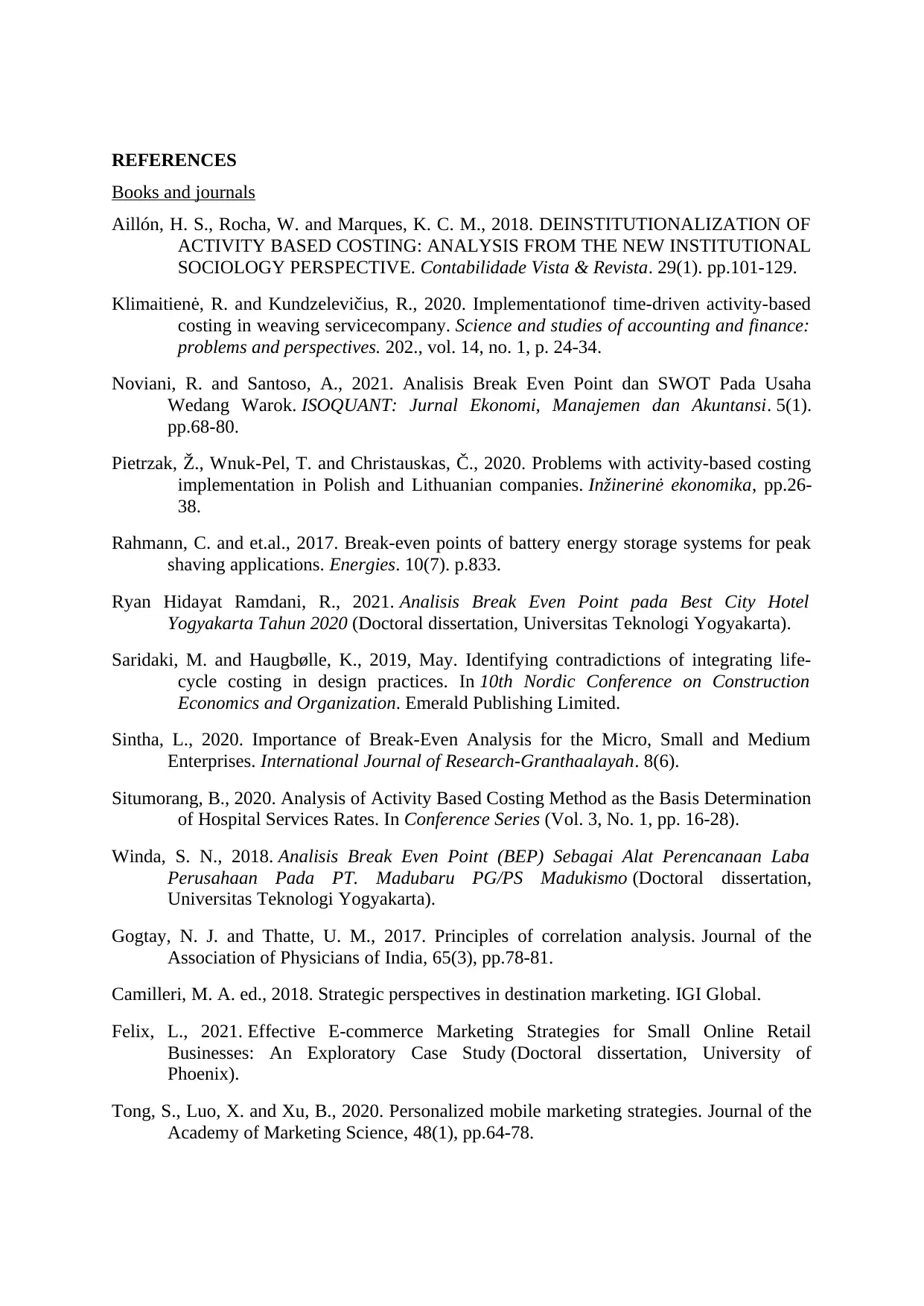

The profit derived against the operations and functions entertained of the organisation

are 390000. This is a level of profitability that can favour the business unit to deliver the

business operations in profits. The total sales of company are 600000 and the total cost

incurred comprises with fixed cost and the variable cost is 210000. Profit is a figure derives

by deducting the total cost with the sale price to identify the total profitability of the

operations entertained by the company. Total cost deducted is 210000. The difference

between the total cost and the sales price collected is the factor identified as a profit of the

organisation. The above projected graph state figures of the next five expected financial

years. The next five years projection clearly indicates that the company profitability would

certainly increase as the sales of company would increase. The profit expected figure would

be achieve in the end of the five financial years is 979682 this would go from 390000. This is

a huge jump in context to the five financial years that the profit figures of company have

gone to thrice the earlier value.

The graph indicates the way company will proceed further in the business operations

and deliver the performance of company. The sales of company keep on changing every year

Less:

Total cost 210000

Profit 390000

0 1 2 3 4 5

0

200000

400000

600000

800000

1000000

1200000

1400000

600000

693000

800415

924513

1068793

1233651

130000 137800 146068 154832 164122 173969

80000 80000 80000 80000 80000 80000

390000 475200

574347

689681

824671

979682

Sales

Variable cost

Fixed cost

Profit

Series5

The profit derived against the operations and functions entertained of the organisation

are 390000. This is a level of profitability that can favour the business unit to deliver the

business operations in profits. The total sales of company are 600000 and the total cost

incurred comprises with fixed cost and the variable cost is 210000. Profit is a figure derives

by deducting the total cost with the sale price to identify the total profitability of the

operations entertained by the company. Total cost deducted is 210000. The difference

between the total cost and the sales price collected is the factor identified as a profit of the

organisation. The above projected graph state figures of the next five expected financial

years. The next five years projection clearly indicates that the company profitability would

certainly increase as the sales of company would increase. The profit expected figure would

be achieve in the end of the five financial years is 979682 this would go from 390000. This is

a huge jump in context to the five financial years that the profit figures of company have

gone to thrice the earlier value.

The graph indicates the way company will proceed further in the business operations

and deliver the performance of company. The sales of company keep on changing every year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that too also influence the variable cost of company which is also increasing as the sales of

company is increasing. He further evaluation identified is the fixed cost that is remain the

same irrespective of the financial year passes and the level of operations or production

increases (Klimaitienė and Kundzelevičius, 2020). This is a basic nature of the fixed cost that

it remain unchanged at any point and position or the level of functions and operations. The

role of fixed cost and the variable cost is very significant in respect to the business venture.

With the process of time company sale is keep on increasing that could further influenced the

profitability of the business unit. The variable cost is not increasing in proportion to the sales

of company that significantly establishing the profit making opportunities for the business

organisation. This has been analysed that the business unit is capable enough to generate

profitability against delivering the business operations.

(c) Costing and revenue behaviour

The costing is a value that is a total outlay of the financial resources of the business

organisation. The costing behaviour is such that with the pace of time and output the total

costing is increases. This consumes variable cost and the fixed nature cost of the business

unit. With the process of time and production variable cost face by the CF Ltd would get an

increase. This would not further influence the fixed nature cost face by the business

organisation. It becomes important for the business venture to understand the significance of

the fixed cost and the variable cost entertained by the business organisation. The costing of

company is behaved very progressively (Situmorang, 2020). With the process of time the cost

incurred will also increase for the business unit. This is certainly indicated that the business

unit require facing the fixed and variable nature of cost that state about the level of costing

incurred by the business unit. The costing behaviour is all about the level of cost is certainly

influenced with the time factor and the level of production company deliver to incorporate the

business functions. The cost nature is very progressive that is influenced with various

elements of business environment that certainly create an impact over the costing and pricing

of the business unit.

The costing of the business unit is derived with the direct nature of cost and the

indirect nature of cost. The direct cost is a nature of cost that is directly involved under the

production and operations of the business venture. This is important for the organisation to

certainly guide the direct cost as it is directly associated with the operations and the

production processes of the business unit. This is a cost consumed over the direct material,

company is increasing. He further evaluation identified is the fixed cost that is remain the

same irrespective of the financial year passes and the level of operations or production

increases (Klimaitienė and Kundzelevičius, 2020). This is a basic nature of the fixed cost that

it remain unchanged at any point and position or the level of functions and operations. The

role of fixed cost and the variable cost is very significant in respect to the business venture.

With the process of time company sale is keep on increasing that could further influenced the

profitability of the business unit. The variable cost is not increasing in proportion to the sales

of company that significantly establishing the profit making opportunities for the business

organisation. This has been analysed that the business unit is capable enough to generate

profitability against delivering the business operations.

(c) Costing and revenue behaviour

The costing is a value that is a total outlay of the financial resources of the business

organisation. The costing behaviour is such that with the pace of time and output the total

costing is increases. This consumes variable cost and the fixed nature cost of the business

unit. With the process of time and production variable cost face by the CF Ltd would get an

increase. This would not further influence the fixed nature cost face by the business

organisation. It becomes important for the business venture to understand the significance of

the fixed cost and the variable cost entertained by the business organisation. The costing of

company is behaved very progressively (Situmorang, 2020). With the process of time the cost

incurred will also increase for the business unit. This is certainly indicated that the business

unit require facing the fixed and variable nature of cost that state about the level of costing

incurred by the business unit. The costing behaviour is all about the level of cost is certainly

influenced with the time factor and the level of production company deliver to incorporate the

business functions. The cost nature is very progressive that is influenced with various

elements of business environment that certainly create an impact over the costing and pricing

of the business unit.

The costing of the business unit is derived with the direct nature of cost and the

indirect nature of cost. The direct cost is a nature of cost that is directly involved under the

production and operations of the business venture. This is important for the organisation to

certainly guide the direct cost as it is directly associated with the operations and the

production processes of the business unit. This is a cost consumed over the direct material,

labour and many other cost included under the production process of the CF Ltd. This is all

about analysing the requirements of the business unit and based on that fact try to make the

cost cheaper than the earlier cost to make it more affordable in nature. On the other side the

costing structure also comprises with the indirect nature of cost (Aillón, Rocha and Marques,

2018). This is a cost that does not have any direct involvement in the production and

operations of the organisation. This is a cost that is all about the indirect nature of operations.

This is cost do not directly associate with producing the units and operations of the business

organisation. This cost is only involved in channelizing regular business operations. The

example of this cost is rent, electricity and all other cost. The nature of costing is very

progressive in nature and also the classification is very clear and identified. This is very

obvious that the business organisation know about the areas where costing is incurred as a

business venture.

On the other side the revenue generated by the business unit is also carry a nature of

progressive. The CF Ltd revenue is progressive in nature as it is increasing with the pace of

time. The more company proceed to deliver the business operations the more selling

opportunities company will get and the more the progression of business will be guided

towards the growth of company. This is important for the entity to guide the revenue in such

manner that company get to fulfil all its business objectives (Saridaki and Haugbølle, 2019).

The revenue of the company is keep on increasing every year that could also become the

possible reason why the business unit has upgraded its profit making opportunities in the

business. This is essential for the revenue situation as the business unit get to increases its

revenue every single financial year so that operations of company could been achieving all its

objectives.

QUESTION 2

Calculation of coefficient of correlation for advertising and sales

Year Advertisemen

t expenditure

(X)

Revenue

from

Sales (Y)

X2 Y2 XY

2016 2 100 4 10000 200

2017 5 90 25 8100 450

2018 4 70 16 4900 280

2019 6 60 36 3600 360

2020 3 80 9 6400 240

n = 5 ∑X = 20 ∑Y =

400

∑X2 =

90

∑Y2 =

33000

∑XY =

1530

about analysing the requirements of the business unit and based on that fact try to make the

cost cheaper than the earlier cost to make it more affordable in nature. On the other side the

costing structure also comprises with the indirect nature of cost (Aillón, Rocha and Marques,

2018). This is a cost that does not have any direct involvement in the production and

operations of the organisation. This is a cost that is all about the indirect nature of operations.

This is cost do not directly associate with producing the units and operations of the business

organisation. This cost is only involved in channelizing regular business operations. The

example of this cost is rent, electricity and all other cost. The nature of costing is very

progressive in nature and also the classification is very clear and identified. This is very

obvious that the business organisation know about the areas where costing is incurred as a

business venture.

On the other side the revenue generated by the business unit is also carry a nature of

progressive. The CF Ltd revenue is progressive in nature as it is increasing with the pace of

time. The more company proceed to deliver the business operations the more selling

opportunities company will get and the more the progression of business will be guided

towards the growth of company. This is important for the entity to guide the revenue in such

manner that company get to fulfil all its business objectives (Saridaki and Haugbølle, 2019).

The revenue of the company is keep on increasing every year that could also become the

possible reason why the business unit has upgraded its profit making opportunities in the

business. This is essential for the revenue situation as the business unit get to increases its

revenue every single financial year so that operations of company could been achieving all its

objectives.

QUESTION 2

Calculation of coefficient of correlation for advertising and sales

Year Advertisemen

t expenditure

(X)

Revenue

from

Sales (Y)

X2 Y2 XY

2016 2 100 4 10000 200

2017 5 90 25 8100 450

2018 4 70 16 4900 280

2019 6 60 36 3600 360

2020 3 80 9 6400 240

n = 5 ∑X = 20 ∑Y =

400

∑X2 =

90

∑Y2 =

33000

∑XY =

1530

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

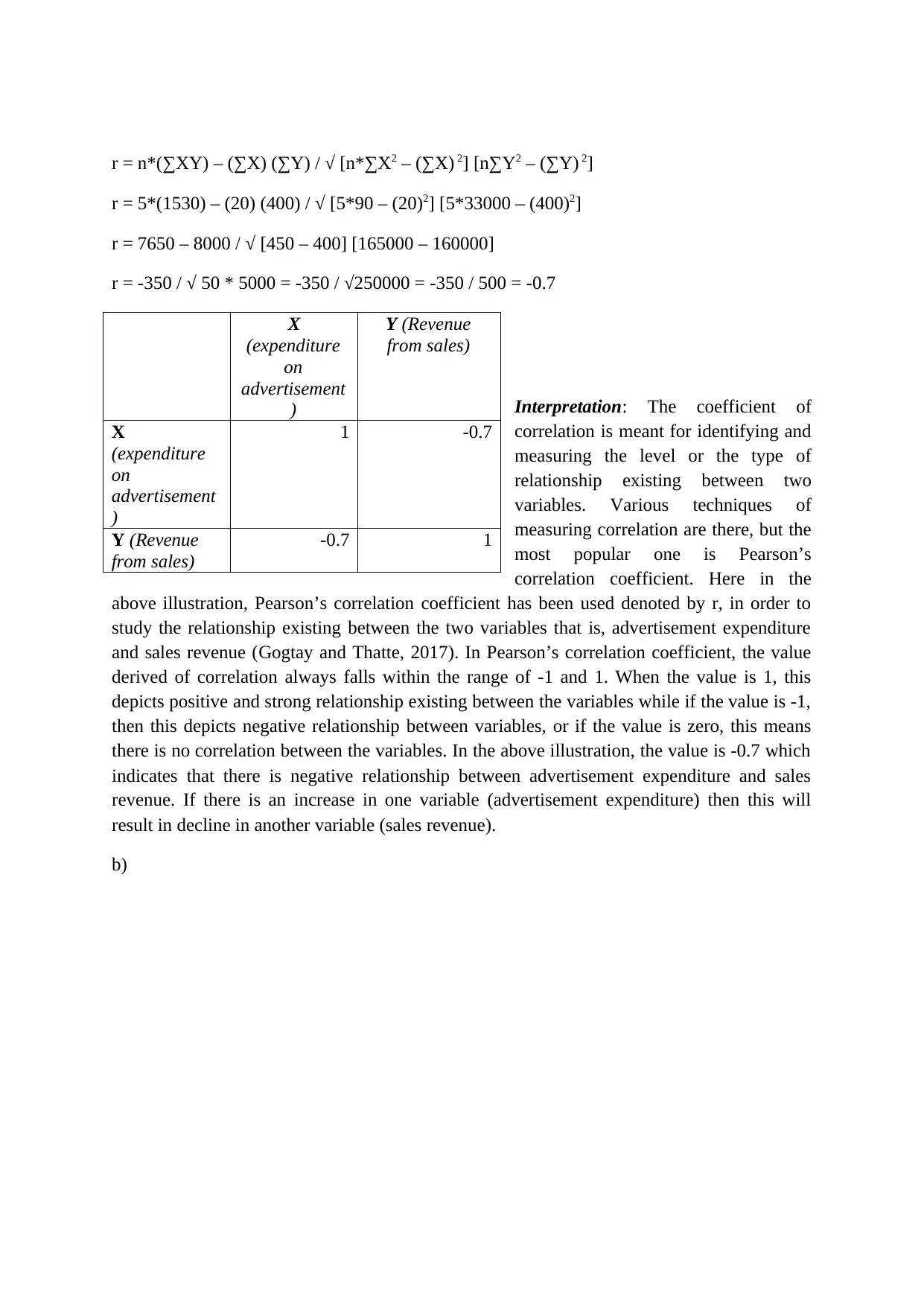

r = n*(∑XY) – (∑X) (∑Y) / √ [n*∑X2 – (∑X) 2] [n∑Y2 – (∑Y) 2]

r = 5*(1530) – (20) (400) / √ [5*90 – (20)2] [5*33000 – (400)2]

r = 7650 – 8000 / √ [450 – 400] [165000 – 160000]

r = -350 / √ 50 * 5000 = -350 / √250000 = -350 / 500 = -0.7

Interpretation: The coefficient of

correlation is meant for identifying and

measuring the level or the type of

relationship existing between two

variables. Various techniques of

measuring correlation are there, but the

most popular one is Pearson’s

correlation coefficient. Here in the

above illustration, Pearson’s correlation coefficient has been used denoted by r, in order to

study the relationship existing between the two variables that is, advertisement expenditure

and sales revenue (Gogtay and Thatte, 2017). In Pearson’s correlation coefficient, the value

derived of correlation always falls within the range of -1 and 1. When the value is 1, this

depicts positive and strong relationship existing between the variables while if the value is -1,

then this depicts negative relationship between variables, or if the value is zero, this means

there is no correlation between the variables. In the above illustration, the value is -0.7 which

indicates that there is negative relationship between advertisement expenditure and sales

revenue. If there is an increase in one variable (advertisement expenditure) then this will

result in decline in another variable (sales revenue).

b)

X

(expenditure

on

advertisement

)

Y (Revenue

from sales)

X

(expenditure

on

advertisement

)

1 -0.7

Y (Revenue

from sales)

-0.7 1

r = 5*(1530) – (20) (400) / √ [5*90 – (20)2] [5*33000 – (400)2]

r = 7650 – 8000 / √ [450 – 400] [165000 – 160000]

r = -350 / √ 50 * 5000 = -350 / √250000 = -350 / 500 = -0.7

Interpretation: The coefficient of

correlation is meant for identifying and

measuring the level or the type of

relationship existing between two

variables. Various techniques of

measuring correlation are there, but the

most popular one is Pearson’s

correlation coefficient. Here in the

above illustration, Pearson’s correlation coefficient has been used denoted by r, in order to

study the relationship existing between the two variables that is, advertisement expenditure

and sales revenue (Gogtay and Thatte, 2017). In Pearson’s correlation coefficient, the value

derived of correlation always falls within the range of -1 and 1. When the value is 1, this

depicts positive and strong relationship existing between the variables while if the value is -1,

then this depicts negative relationship between variables, or if the value is zero, this means

there is no correlation between the variables. In the above illustration, the value is -0.7 which

indicates that there is negative relationship between advertisement expenditure and sales

revenue. If there is an increase in one variable (advertisement expenditure) then this will

result in decline in another variable (sales revenue).

b)

X

(expenditure

on

advertisement

)

Y (Revenue

from sales)

X

(expenditure

on

advertisement

)

1 -0.7

Y (Revenue

from sales)

-0.7 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

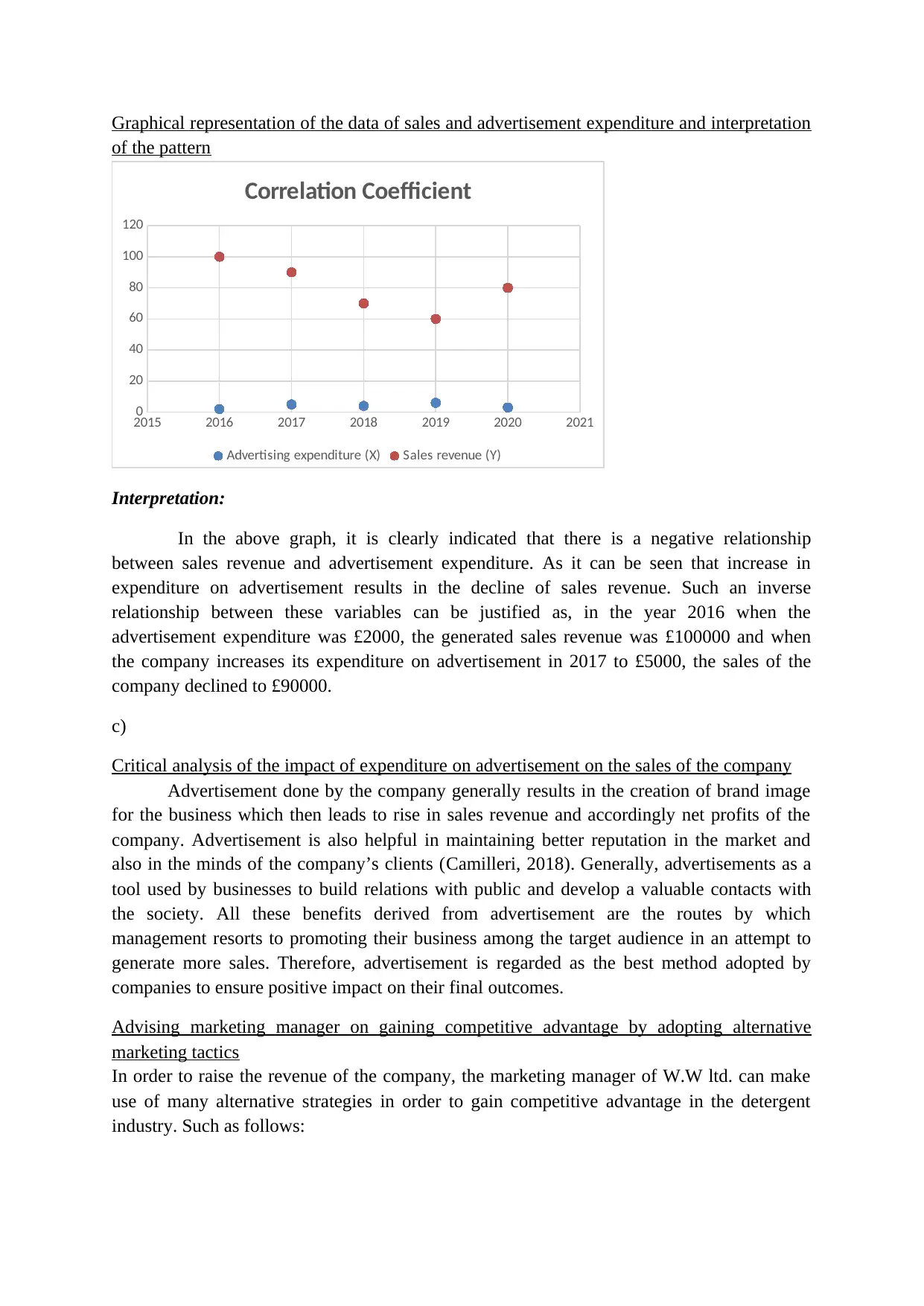

Graphical representation of the data of sales and advertisement expenditure and interpretation

of the pattern

2015 2016 2017 2018 2019 2020 2021

0

20

40

60

80

100

120

Correlation Coefficient

Advertising expenditure (X) Sales revenue (Y)

Interpretation:

In the above graph, it is clearly indicated that there is a negative relationship

between sales revenue and advertisement expenditure. As it can be seen that increase in

expenditure on advertisement results in the decline of sales revenue. Such an inverse

relationship between these variables can be justified as, in the year 2016 when the

advertisement expenditure was £2000, the generated sales revenue was £100000 and when

the company increases its expenditure on advertisement in 2017 to £5000, the sales of the

company declined to £90000.

c)

Critical analysis of the impact of expenditure on advertisement on the sales of the company

Advertisement done by the company generally results in the creation of brand image

for the business which then leads to rise in sales revenue and accordingly net profits of the

company. Advertisement is also helpful in maintaining better reputation in the market and

also in the minds of the company’s clients (Camilleri, 2018). Generally, advertisements as a

tool used by businesses to build relations with public and develop a valuable contacts with

the society. All these benefits derived from advertisement are the routes by which

management resorts to promoting their business among the target audience in an attempt to

generate more sales. Therefore, advertisement is regarded as the best method adopted by

companies to ensure positive impact on their final outcomes.

Advising marketing manager on gaining competitive advantage by adopting alternative

marketing tactics

In order to raise the revenue of the company, the marketing manager of W.W ltd. can make

use of many alternative strategies in order to gain competitive advantage in the detergent

industry. Such as follows:

of the pattern

2015 2016 2017 2018 2019 2020 2021

0

20

40

60

80

100

120

Correlation Coefficient

Advertising expenditure (X) Sales revenue (Y)

Interpretation:

In the above graph, it is clearly indicated that there is a negative relationship

between sales revenue and advertisement expenditure. As it can be seen that increase in

expenditure on advertisement results in the decline of sales revenue. Such an inverse

relationship between these variables can be justified as, in the year 2016 when the

advertisement expenditure was £2000, the generated sales revenue was £100000 and when

the company increases its expenditure on advertisement in 2017 to £5000, the sales of the

company declined to £90000.

c)

Critical analysis of the impact of expenditure on advertisement on the sales of the company

Advertisement done by the company generally results in the creation of brand image

for the business which then leads to rise in sales revenue and accordingly net profits of the

company. Advertisement is also helpful in maintaining better reputation in the market and

also in the minds of the company’s clients (Camilleri, 2018). Generally, advertisements as a

tool used by businesses to build relations with public and develop a valuable contacts with

the society. All these benefits derived from advertisement are the routes by which

management resorts to promoting their business among the target audience in an attempt to

generate more sales. Therefore, advertisement is regarded as the best method adopted by

companies to ensure positive impact on their final outcomes.

Advising marketing manager on gaining competitive advantage by adopting alternative

marketing tactics

In order to raise the revenue of the company, the marketing manager of W.W ltd. can make

use of many alternative strategies in order to gain competitive advantage in the detergent

industry. Such as follows:

Creation of user-friendly website: By creating a website of the company, many

useful information about the company, its products & services can be communicated to the

clients of the business such as customers, suppliers, etc. Also, it is helpful in online

transacting with clients which is considered as the best driver of customer satisfaction and

better service provision to them (Felix, 2021). It provides an ease to the customers in

navigating through the offerings of the company and making choices among the range of

products demonstrated online. Creating a company’s website involves a little bit higher costs

to the company, but on the other side it is very fruitful from the perspective of the long term

growth of the business.

Digital marketing strategy: This strategy of marketing company’s products and

services is a widely used modern technique by the companies in an attempt to target large

number of target audience with a minimum costs and efforts through the use of online or

digital platforms (Tong, Luo and Xu, 2020). With reference to detergent manufacturer, this

technique can be used to promote variants of products and services in an effective manner by

increasing their market presence through the use of channels such as social networking sites.

This would be helpful in enhancing the brand recognition in the market. By using this

strategy, W.W limited can share their pictures, videos, news and achievements of their

business and thus this will result in better image of their brand in the marketplace.

Accordingly, obtaining consideration from large audience in the form of sales generation

becomes easier. Also, such an online presence is helpful in communicating and hearing the

perspectives and views of the clients, tackling their queries and receiving their feedback from

time to time.

Competitor analysis: Analysing competitor’s strategy and attempts towards

promoting and marketing their products and services is also considered as a best marketing

tactics. Here, the company by evaluating and identifying the competition existing in the

market, what other players in the industry are doing and what are the expectations of

customers that has not yet been met by the competitors can be very much helpful in

identifying untapped opportunities (Quaye and Mensah, 2019). And by exploiting such

prevailing opportunities in the industry, W.W limited can enhance their market share. Also,

better knowledge about the existing conditions of the market can be obtained through such

analysis and therefore determination of unmet needs become easier and the company can take

advantage of the same before its competitors.

QUESTION 3

a) Calculation of Break-even sales and margin of safety

Income Statement under different scenario

Particulars Original Estimates

(£)

Production

manager suggestion

Marketing

manager

suggestion

useful information about the company, its products & services can be communicated to the

clients of the business such as customers, suppliers, etc. Also, it is helpful in online

transacting with clients which is considered as the best driver of customer satisfaction and

better service provision to them (Felix, 2021). It provides an ease to the customers in

navigating through the offerings of the company and making choices among the range of

products demonstrated online. Creating a company’s website involves a little bit higher costs

to the company, but on the other side it is very fruitful from the perspective of the long term

growth of the business.

Digital marketing strategy: This strategy of marketing company’s products and

services is a widely used modern technique by the companies in an attempt to target large

number of target audience with a minimum costs and efforts through the use of online or

digital platforms (Tong, Luo and Xu, 2020). With reference to detergent manufacturer, this

technique can be used to promote variants of products and services in an effective manner by

increasing their market presence through the use of channels such as social networking sites.

This would be helpful in enhancing the brand recognition in the market. By using this

strategy, W.W limited can share their pictures, videos, news and achievements of their

business and thus this will result in better image of their brand in the marketplace.

Accordingly, obtaining consideration from large audience in the form of sales generation

becomes easier. Also, such an online presence is helpful in communicating and hearing the

perspectives and views of the clients, tackling their queries and receiving their feedback from

time to time.

Competitor analysis: Analysing competitor’s strategy and attempts towards

promoting and marketing their products and services is also considered as a best marketing

tactics. Here, the company by evaluating and identifying the competition existing in the

market, what other players in the industry are doing and what are the expectations of

customers that has not yet been met by the competitors can be very much helpful in

identifying untapped opportunities (Quaye and Mensah, 2019). And by exploiting such

prevailing opportunities in the industry, W.W limited can enhance their market share. Also,

better knowledge about the existing conditions of the market can be obtained through such

analysis and therefore determination of unmet needs become easier and the company can take

advantage of the same before its competitors.

QUESTION 3

a) Calculation of Break-even sales and margin of safety

Income Statement under different scenario

Particulars Original Estimates

(£)

Production

manager suggestion

Marketing

manager

suggestion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(£) (£)

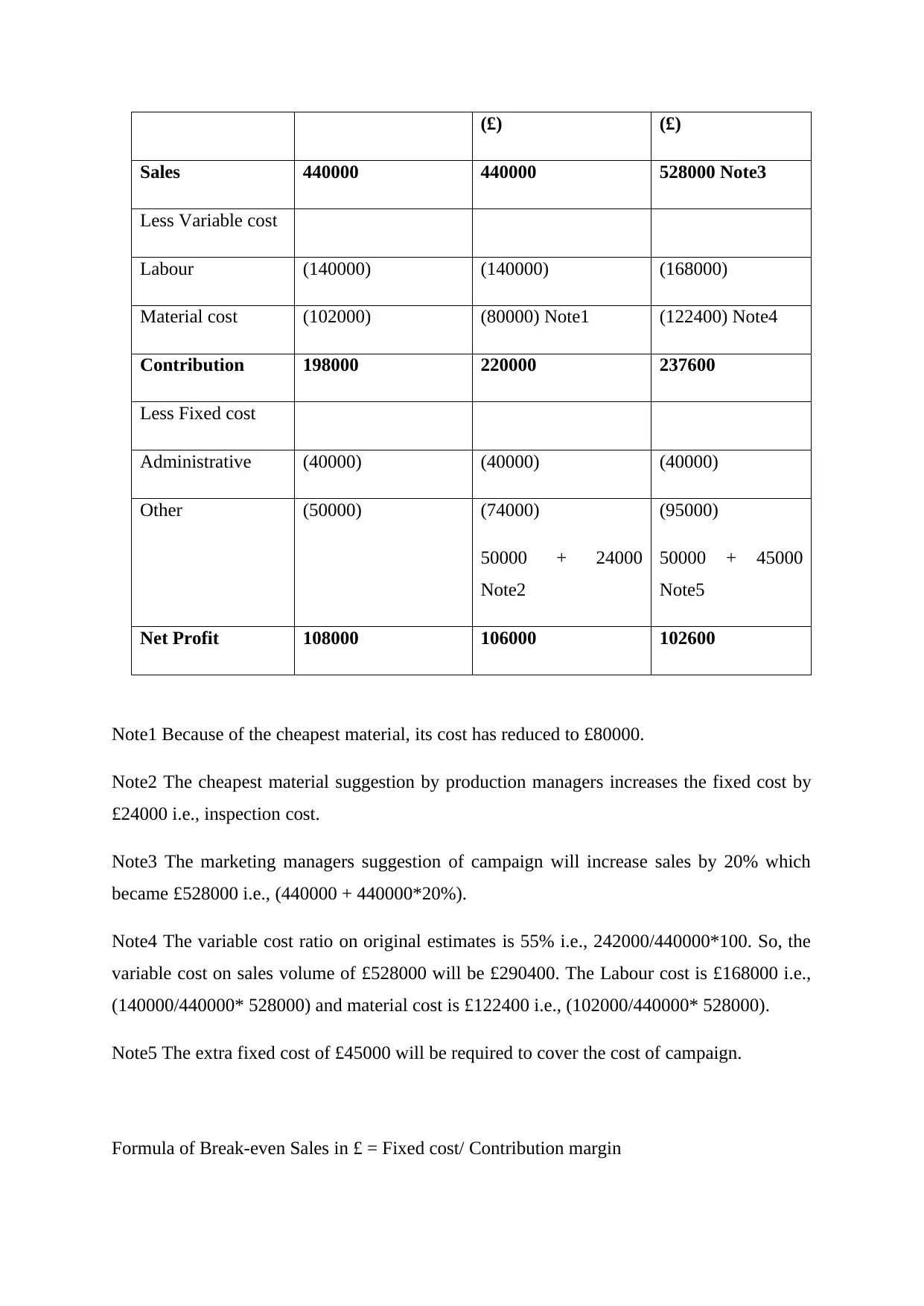

Sales 440000 440000 528000 Note3

Less Variable cost

Labour (140000) (140000) (168000)

Material cost (102000) (80000) Note1 (122400) Note4

Contribution 198000 220000 237600

Less Fixed cost

Administrative (40000) (40000) (40000)

Other (50000) (74000)

50000 + 24000

Note2

(95000)

50000 + 45000

Note5

Net Profit 108000 106000 102600

Note1 Because of the cheapest material, its cost has reduced to £80000.

Note2 The cheapest material suggestion by production managers increases the fixed cost by

£24000 i.e., inspection cost.

Note3 The marketing managers suggestion of campaign will increase sales by 20% which

became £528000 i.e., (440000 + 440000*20%).

Note4 The variable cost ratio on original estimates is 55% i.e., 242000/440000*100. So, the

variable cost on sales volume of £528000 will be £290400. The Labour cost is £168000 i.e.,

(140000/440000* 528000) and material cost is £122400 i.e., (102000/440000* 528000).

Note5 The extra fixed cost of £45000 will be required to cover the cost of campaign.

Formula of Break-even Sales in £ = Fixed cost/ Contribution margin

Sales 440000 440000 528000 Note3

Less Variable cost

Labour (140000) (140000) (168000)

Material cost (102000) (80000) Note1 (122400) Note4

Contribution 198000 220000 237600

Less Fixed cost

Administrative (40000) (40000) (40000)

Other (50000) (74000)

50000 + 24000

Note2

(95000)

50000 + 45000

Note5

Net Profit 108000 106000 102600

Note1 Because of the cheapest material, its cost has reduced to £80000.

Note2 The cheapest material suggestion by production managers increases the fixed cost by

£24000 i.e., inspection cost.

Note3 The marketing managers suggestion of campaign will increase sales by 20% which

became £528000 i.e., (440000 + 440000*20%).

Note4 The variable cost ratio on original estimates is 55% i.e., 242000/440000*100. So, the

variable cost on sales volume of £528000 will be £290400. The Labour cost is £168000 i.e.,

(140000/440000* 528000) and material cost is £122400 i.e., (102000/440000* 528000).

Note5 The extra fixed cost of £45000 will be required to cover the cost of campaign.

Formula of Break-even Sales in £ = Fixed cost/ Contribution margin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

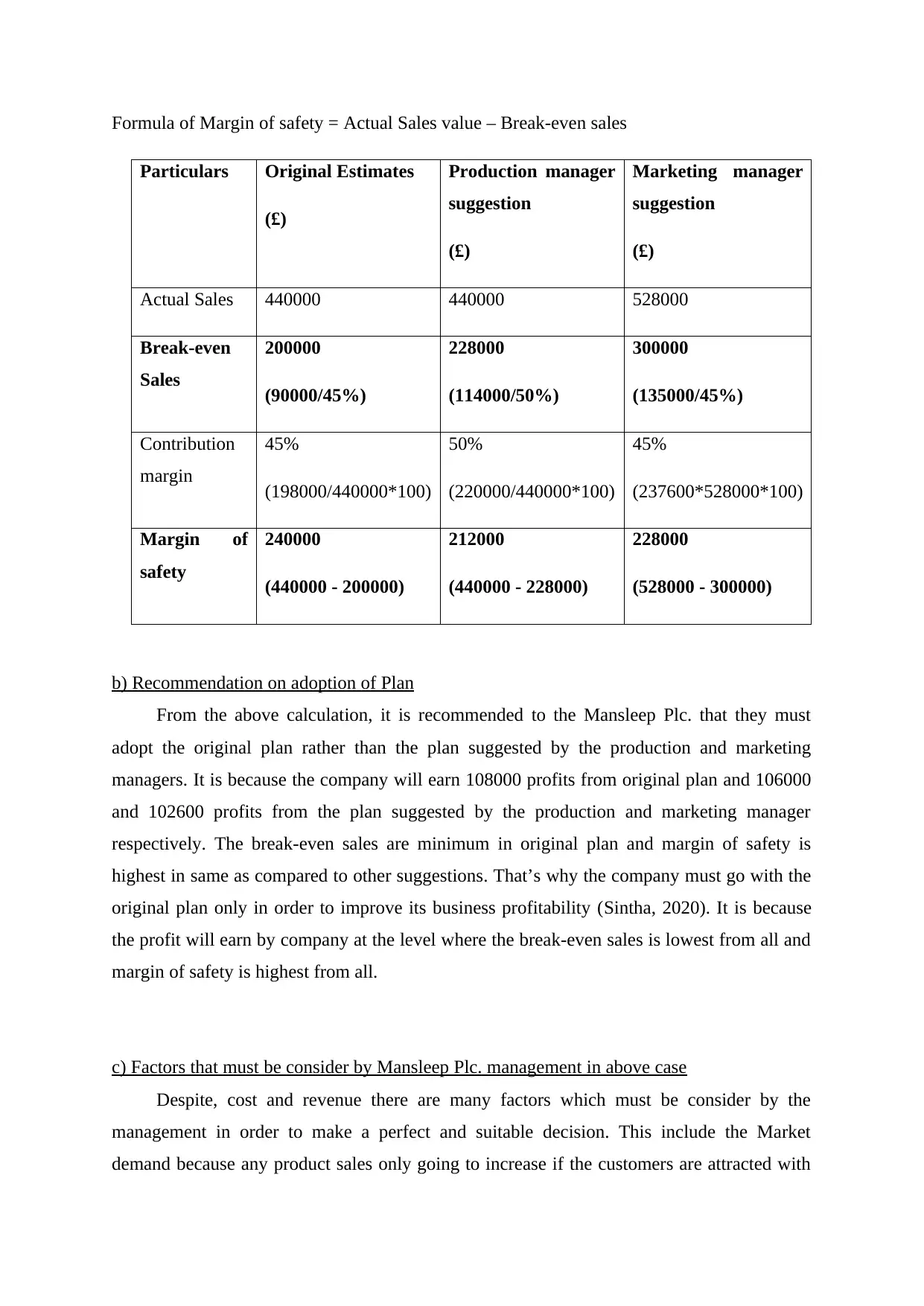

Formula of Margin of safety = Actual Sales value – Break-even sales

Particulars Original Estimates

(£)

Production manager

suggestion

(£)

Marketing manager

suggestion

(£)

Actual Sales 440000 440000 528000

Break-even

Sales

200000

(90000/45%)

228000

(114000/50%)

300000

(135000/45%)

Contribution

margin

45%

(198000/440000*100)

50%

(220000/440000*100)

45%

(237600*528000*100)

Margin of

safety

240000

(440000 - 200000)

212000

(440000 - 228000)

228000

(528000 - 300000)

b) Recommendation on adoption of Plan

From the above calculation, it is recommended to the Mansleep Plc. that they must

adopt the original plan rather than the plan suggested by the production and marketing

managers. It is because the company will earn 108000 profits from original plan and 106000

and 102600 profits from the plan suggested by the production and marketing manager

respectively. The break-even sales are minimum in original plan and margin of safety is

highest in same as compared to other suggestions. That’s why the company must go with the

original plan only in order to improve its business profitability (Sintha, 2020). It is because

the profit will earn by company at the level where the break-even sales is lowest from all and

margin of safety is highest from all.

c) Factors that must be consider by Mansleep Plc. management in above case

Despite, cost and revenue there are many factors which must be consider by the

management in order to make a perfect and suitable decision. This include the Market

demand because any product sales only going to increase if the customers are attracted with

Particulars Original Estimates

(£)

Production manager

suggestion

(£)

Marketing manager

suggestion

(£)

Actual Sales 440000 440000 528000

Break-even

Sales

200000

(90000/45%)

228000

(114000/50%)

300000

(135000/45%)

Contribution

margin

45%

(198000/440000*100)

50%

(220000/440000*100)

45%

(237600*528000*100)

Margin of

safety

240000

(440000 - 200000)

212000

(440000 - 228000)

228000

(528000 - 300000)

b) Recommendation on adoption of Plan

From the above calculation, it is recommended to the Mansleep Plc. that they must

adopt the original plan rather than the plan suggested by the production and marketing

managers. It is because the company will earn 108000 profits from original plan and 106000

and 102600 profits from the plan suggested by the production and marketing manager

respectively. The break-even sales are minimum in original plan and margin of safety is

highest in same as compared to other suggestions. That’s why the company must go with the

original plan only in order to improve its business profitability (Sintha, 2020). It is because

the profit will earn by company at the level where the break-even sales is lowest from all and

margin of safety is highest from all.

c) Factors that must be consider by Mansleep Plc. management in above case

Despite, cost and revenue there are many factors which must be consider by the

management in order to make a perfect and suitable decision. This include the Market

demand because any product sales only going to increase if the customers are attracted with

its no matter how much cost the company reduce. Another factor is pricing strategy where the

management need to analyse the customers reaction over the different prices and adopt the

best strategy such as value-based pricing (Winda, 2018). The fixed cost must be managed by

the management because if any sales increment causes double increment in fixed cost than

earning the profit will not be possible. So, this factor must be considered by the company’s

management while suggesting any plan because the ultimate goal of the company is profit

maximization.

d) Benefits and Limitations of Break-even model

Benefits

It basically helpful for measuring the profit and losses of the business on the different

level of production as well as sales.

It also helpful to identify and predict the selling price changes and its effect over the

business profitability.

This reflects the real profit earning of the company because it distributes the total cost

into fixed and variable by analysing the relationship between the same (Noviani and

Santoso, 2021).

Not only that, the break-even model and marginal costing tool helps the company in

understanding and predicting the effect of changes in the variable cost over the

business performance.

Limitations

The profits calculation under this model is not same in reality because of the

assumption that selling price remain constant at all level of the output.

Here, this model also assume that the production and sales remain same without the

concept of opening and closing stock along with the work-in-progress. And this is not

possible in reality.

This is quite time consuming for the company and the impact of which sometime

decision-making process get delay.

It can be applying only to a single product or a single product mix. When the

company deals with more than one product application of this model is not suitable

(Rahmann and et.al., 2017).

management need to analyse the customers reaction over the different prices and adopt the

best strategy such as value-based pricing (Winda, 2018). The fixed cost must be managed by

the management because if any sales increment causes double increment in fixed cost than

earning the profit will not be possible. So, this factor must be considered by the company’s

management while suggesting any plan because the ultimate goal of the company is profit

maximization.

d) Benefits and Limitations of Break-even model

Benefits

It basically helpful for measuring the profit and losses of the business on the different

level of production as well as sales.

It also helpful to identify and predict the selling price changes and its effect over the

business profitability.

This reflects the real profit earning of the company because it distributes the total cost

into fixed and variable by analysing the relationship between the same (Noviani and

Santoso, 2021).

Not only that, the break-even model and marginal costing tool helps the company in

understanding and predicting the effect of changes in the variable cost over the

business performance.

Limitations

The profits calculation under this model is not same in reality because of the

assumption that selling price remain constant at all level of the output.

Here, this model also assume that the production and sales remain same without the

concept of opening and closing stock along with the work-in-progress. And this is not

possible in reality.

This is quite time consuming for the company and the impact of which sometime

decision-making process get delay.

It can be applying only to a single product or a single product mix. When the

company deals with more than one product application of this model is not suitable

(Rahmann and et.al., 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application of Breakeven model in marginal costing and Mansleep Plc. business

strategy

Break-even point is a sales value where the total fixed cost is equal to its contribution

and the impact of which the company neither earn profit nor incur loses. While the margin of

safety is a level above the break-even sales in which the company earn profit from the sales

revenue. So, with the application of this model as a strategy within the business, the

Mansleep Plc. can understand and determine how many units the company need to produce

and sale in order to earn profit. The contribution concept helps the company in understanding

the relation between the variable cost and sales. And the impact of which the company put

more focus on its variable cost reduction rather than fixed cost. It is because fixed cost

remains constant over the period of time. The application of break-even model also helps the

Mansleep company in identifying that profit will not earn at all level and identify exact units

the company need to sale for profit earning as well as maximization (Ryan Hidayat Ramdani,

2021). Along with that this tool is also helpful for providing the motivation to the employees

especially the sales staffs because it helps them to analyse the profit at different sales point

and identifying the area which causes loss. The application of break-even sales is helpful for

the company which sales only single product in identifying the margin of safety and helps the

business to set the realistic, achievable targets for the employees.

CONCLUSION

Costing analysis is a process that is ability to analysis and ascertains the cost incurred

in delivering the certain operations. The cost of the company is segregated into the fixed cost

and the variable nature of cost. Fixed cost remains unchanged irrespective of the time and the

level of operations but on the other hand variable cost changes with the pace of time,

production and all other elements. The break even is a cost that is a point where company

derive all its spending over the production. This is a point where company gain no profit and

no loss kind of situation in business. The role of breakeven is very significant in the business

progression of company as it could completely influence the business performance of the

organisation.

strategy

Break-even point is a sales value where the total fixed cost is equal to its contribution

and the impact of which the company neither earn profit nor incur loses. While the margin of

safety is a level above the break-even sales in which the company earn profit from the sales

revenue. So, with the application of this model as a strategy within the business, the

Mansleep Plc. can understand and determine how many units the company need to produce

and sale in order to earn profit. The contribution concept helps the company in understanding

the relation between the variable cost and sales. And the impact of which the company put

more focus on its variable cost reduction rather than fixed cost. It is because fixed cost

remains constant over the period of time. The application of break-even model also helps the

Mansleep company in identifying that profit will not earn at all level and identify exact units

the company need to sale for profit earning as well as maximization (Ryan Hidayat Ramdani,

2021). Along with that this tool is also helpful for providing the motivation to the employees

especially the sales staffs because it helps them to analyse the profit at different sales point

and identifying the area which causes loss. The application of break-even sales is helpful for

the company which sales only single product in identifying the margin of safety and helps the

business to set the realistic, achievable targets for the employees.

CONCLUSION

Costing analysis is a process that is ability to analysis and ascertains the cost incurred

in delivering the certain operations. The cost of the company is segregated into the fixed cost

and the variable nature of cost. Fixed cost remains unchanged irrespective of the time and the

level of operations but on the other hand variable cost changes with the pace of time,

production and all other elements. The break even is a cost that is a point where company

derive all its spending over the production. This is a point where company gain no profit and

no loss kind of situation in business. The role of breakeven is very significant in the business

progression of company as it could completely influence the business performance of the

organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Aillón, H. S., Rocha, W. and Marques, K. C. M., 2018. DEINSTITUTIONALIZATION OF

ACTIVITY BASED COSTING: ANALYSIS FROM THE NEW INSTITUTIONAL

SOCIOLOGY PERSPECTIVE. Contabilidade Vista & Revista. 29(1). pp.101-129.

Klimaitienė, R. and Kundzelevičius, R., 2020. Implementationof time-driven activity-based

costing in weaving servicecompany. Science and studies of accounting and finance:

problems and perspectives. 202., vol. 14, no. 1, p. 24-34.

Noviani, R. and Santoso, A., 2021. Analisis Break Even Point dan SWOT Pada Usaha

Wedang Warok. ISOQUANT: Jurnal Ekonomi, Manajemen dan Akuntansi. 5(1).

pp.68-80.

Pietrzak, Ž., Wnuk-Pel, T. and Christauskas, Č., 2020. Problems with activity-based costing

implementation in Polish and Lithuanian companies. Inžinerinė ekonomika, pp.26-

38.

Rahmann, C. and et.al., 2017. Break-even points of battery energy storage systems for peak

shaving applications. Energies. 10(7). p.833.

Ryan Hidayat Ramdani, R., 2021. Analisis Break Even Point pada Best City Hotel

Yogyakarta Tahun 2020 (Doctoral dissertation, Universitas Teknologi Yogyakarta).

Saridaki, M. and Haugbølle, K., 2019, May. Identifying contradictions of integrating life-

cycle costing in design practices. In 10th Nordic Conference on Construction

Economics and Organization. Emerald Publishing Limited.

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and Medium

Enterprises. International Journal of Research-Granthaalayah. 8(6).

Situmorang, B., 2020. Analysis of Activity Based Costing Method as the Basis Determination

of Hospital Services Rates. In Conference Series (Vol. 3, No. 1, pp. 16-28).

Winda, S. N., 2018. Analisis Break Even Point (BEP) Sebagai Alat Perencanaan Laba

Perusahaan Pada PT. Madubaru PG/PS Madukismo (Doctoral dissertation,

Universitas Teknologi Yogyakarta).

Gogtay, N. J. and Thatte, U. M., 2017. Principles of correlation analysis. Journal of the

Association of Physicians of India, 65(3), pp.78-81.

Camilleri, M. A. ed., 2018. Strategic perspectives in destination marketing. IGI Global.

Felix, L., 2021. Effective E-commerce Marketing Strategies for Small Online Retail

Businesses: An Exploratory Case Study (Doctoral dissertation, University of

Phoenix).

Tong, S., Luo, X. and Xu, B., 2020. Personalized mobile marketing strategies. Journal of the

Academy of Marketing Science, 48(1), pp.64-78.

Books and journals

Aillón, H. S., Rocha, W. and Marques, K. C. M., 2018. DEINSTITUTIONALIZATION OF

ACTIVITY BASED COSTING: ANALYSIS FROM THE NEW INSTITUTIONAL

SOCIOLOGY PERSPECTIVE. Contabilidade Vista & Revista. 29(1). pp.101-129.

Klimaitienė, R. and Kundzelevičius, R., 2020. Implementationof time-driven activity-based

costing in weaving servicecompany. Science and studies of accounting and finance:

problems and perspectives. 202., vol. 14, no. 1, p. 24-34.

Noviani, R. and Santoso, A., 2021. Analisis Break Even Point dan SWOT Pada Usaha

Wedang Warok. ISOQUANT: Jurnal Ekonomi, Manajemen dan Akuntansi. 5(1).

pp.68-80.

Pietrzak, Ž., Wnuk-Pel, T. and Christauskas, Č., 2020. Problems with activity-based costing

implementation in Polish and Lithuanian companies. Inžinerinė ekonomika, pp.26-

38.

Rahmann, C. and et.al., 2017. Break-even points of battery energy storage systems for peak

shaving applications. Energies. 10(7). p.833.

Ryan Hidayat Ramdani, R., 2021. Analisis Break Even Point pada Best City Hotel

Yogyakarta Tahun 2020 (Doctoral dissertation, Universitas Teknologi Yogyakarta).

Saridaki, M. and Haugbølle, K., 2019, May. Identifying contradictions of integrating life-

cycle costing in design practices. In 10th Nordic Conference on Construction

Economics and Organization. Emerald Publishing Limited.

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and Medium

Enterprises. International Journal of Research-Granthaalayah. 8(6).

Situmorang, B., 2020. Analysis of Activity Based Costing Method as the Basis Determination

of Hospital Services Rates. In Conference Series (Vol. 3, No. 1, pp. 16-28).

Winda, S. N., 2018. Analisis Break Even Point (BEP) Sebagai Alat Perencanaan Laba

Perusahaan Pada PT. Madubaru PG/PS Madukismo (Doctoral dissertation,

Universitas Teknologi Yogyakarta).

Gogtay, N. J. and Thatte, U. M., 2017. Principles of correlation analysis. Journal of the

Association of Physicians of India, 65(3), pp.78-81.

Camilleri, M. A. ed., 2018. Strategic perspectives in destination marketing. IGI Global.

Felix, L., 2021. Effective E-commerce Marketing Strategies for Small Online Retail

Businesses: An Exploratory Case Study (Doctoral dissertation, University of

Phoenix).

Tong, S., Luo, X. and Xu, B., 2020. Personalized mobile marketing strategies. Journal of the

Academy of Marketing Science, 48(1), pp.64-78.

Quaye, D. and Mensah, I., 2019. Marketing innovation and sustainable competitive

advantage of manufacturing SMEs in Ghana. Management Decision.

advantage of manufacturing SMEs in Ghana. Management Decision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.